Nifty, Shifty, Grifty, Swift-y Fifty-50

By Michael Every of Rabobank

Ahead of the Fed meeting, our US strategist Philip Marey has just put out an FOMC preview titled ‘Casino’ that acts as reminder that his ahead-of-the-market call of three Fed 25bps cuts this year starting in September still holds – but there is now a substantial risk of a 50bp move this week. The market has been pricing the Fed as close to a 50-50 red-black roulette wheel spin. Yet his title is even better: because those who use analysis to predict the game’s outcome get their hands broken with a hammer.

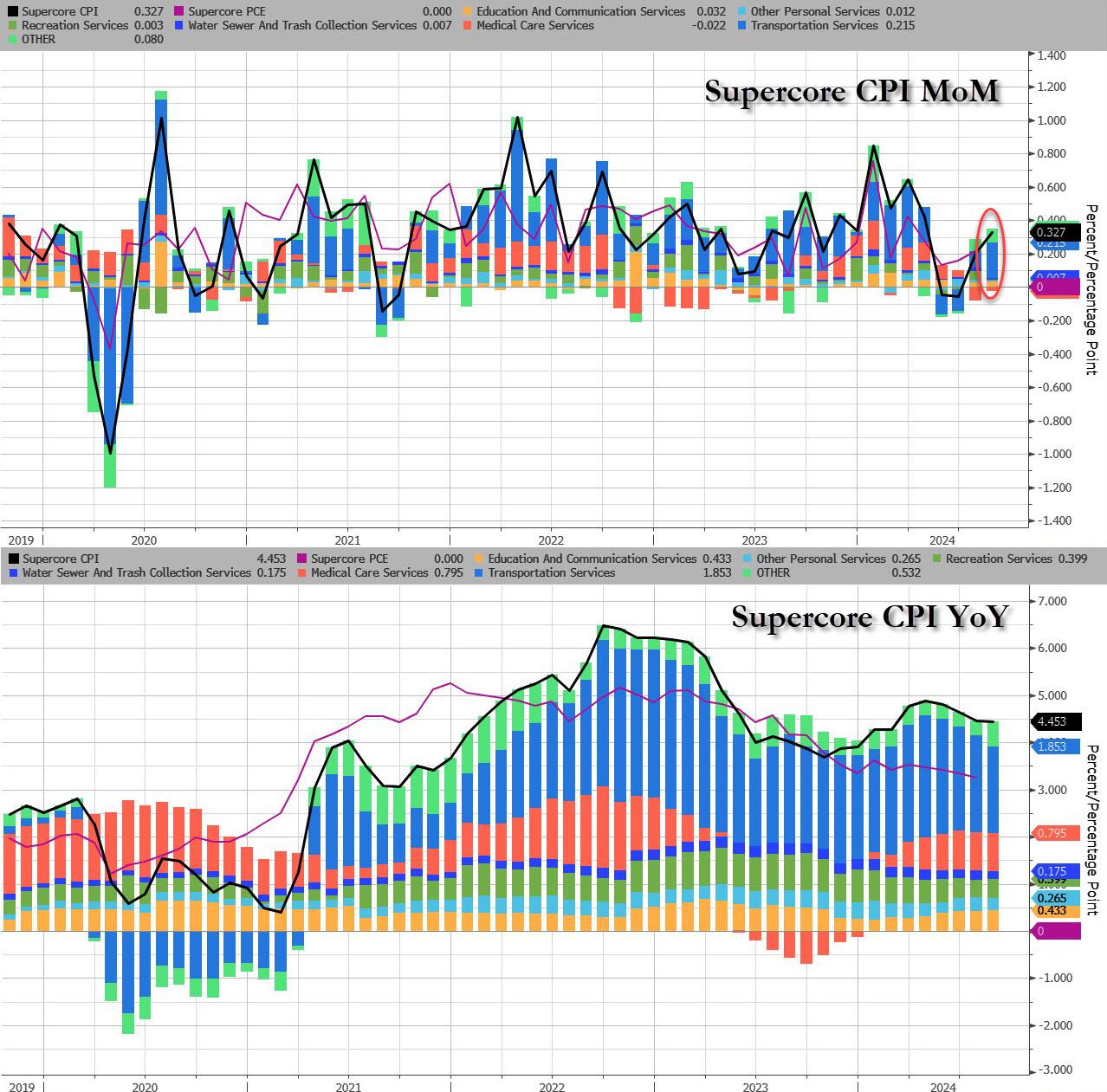

The Fed want inflation back at 2%. On a headline basis, it’s heading there. However, this is led by deflation in and from China, which the Fed has nothing to do with, and which is prompting tariffs globally. It’s also due to a collapse in global commodities pricing in a global downturn the Fed say isn’t coming. Core inflation is 3.2% y-o-y and not heading lower. On an ultra-core basis, it’s also over target, edging higher, held up by housing. There, rate cuts mean lower mortgage rates, so more housing demand, but not more supply. That means inflation, not deflation, regardless of what White House economic advisor and former Fed Deputy Chair Brainard just said.

The Fed want to see unemployment stay low – if it’s meaningful given recent demographic changes they apparently knew nothing about. Yes, the last payrolls revision shifted the dynamic there significantly: but again, did the Fed not know this was coming when some had been mentioning it for months in advance? Literally weeks ago, the Fed were unconcerned, now they worry: yet weekly initial jobless claims data are unchanged.

Nor are the Fed using their endless speaking opportunities to underline that financial conditions are not tight, but loose. Mortgage rates are moving lower before the Fed does. Stocks are at record highs. Credit and junk bond spreads are near lows. The two-year yield is so far below the Fed Funds rate that we almost don’t need to bother having a Fed Funds rate, which is a discussion that gets your hand broken by different people.

You count all those cards, and it suggests a near 50-50 call between 25 and 50bps as the first Fed cut. Even so, logic and consistency say the larger move, only seen at the start of past economic shocks, would suggest the Fed fears something they aren’t telling us. As Philip puts it, “if the economy has become fragile, a 50bps cut could even undermine confidence and make it even more fragile.” Indeed, I put it to you that to go 50bps one must contend either the Fed didn’t know what they were doing recently; or don’t know what they are doing now; or both.

Regardless, large men in suits and sunglasses are politely inviting us for a chat about the Fed in a room with no windows. Fed whisperers used as channels for unofficial communication when their constant prattling, dots, and plots still don’t get the market to ‘efficiently price’ what they want, have one message: 50bps. Nick Timiraos; Greg Ip; John Hilsenrath; former Fed members; oddly, even the Financial Times editorial board are all saying it. How have the verbose Fed gotten to the point where this full court press is required, or is this all just coincidental?

Worse, three Democratic senators, led by Elizabeth Warren, are openly calling for the Fed to go 75bps: these are the same people outraged at the idea that Trump should have a say in setting interest rates. Is that a framing device to make a 50bp move look measured, or is that just a conspiratorial thinking? It’s not like there isn’t a swirl of such thinking around right now, and for very good reasons, even if, again, it risks getting one’s hand broken even typing it.

Were we to get 50bp –which I repeat Philip sees as a tail risk, not a given– would the market see it as nifty (catching up to the curve), shifty (what am I missing?), grifty (who’s on the take?), or Swift-y (political)?

Yet, believe it or not, there are other high-stakes tables being played at elsewhere that matter:

- JPY is trading just above 140 after dipping below it during the Japanese holiday yesterday. The wild ride in the yen carry trade unwind likely isn’t over if the Fed as we hear “50!” and “No, 75!”

- The US has proposed closing the de minimis loophole allowing packages worth less than $800 to enter the US customs free, which is seen as targeting Chinese fast-fashion firms Temu and Shein. Thailand just made a similar move to protect its industries from postal Chinese imports.

- The second assassination attempt on Trump already seems to have a shorter media half-life than the first. Trump tweeted “0-2”, an improvement over “I HATE TAYLOR SWFIT!” The Babylon Bee tweeted: “Kamala safe and in stable condition after attempted interview.” Sadly, this all looks like the ‘DM = EM’ process in motion.

- Canada introduced 30-year mortgages for first-time and new-home buyers, and also allowed mortgage insurance on homes up to C$1.5m (up from C$1m), so buyers can bid on more expensive housing. Guess what this will mean? More expensive housing – demand goes up while supply remains unchanged; and more debt – especially alongside “RATE CUTS!” Can you tell there’s an election soon? And can you tell most politicians don’t have any new political-economy ideas yet?

- Germany reinstituted border controls as its coalition government tries to cap a surge in votes for the far right AfD and old-school far left BSW ahead of another state election this month; yet it also just signed an agreement with Kenya to allow 250,000 jobseekers to enter. That’s as VW may reportedly force through plant closures and 15,000 job cuts this year.

- EU commissioner Thierry Breton, who had threatened Elon Musk, resigned while alleging horse-trading over who gets what roles: what can one retort other than, “I am shocked, shocked that gambling is going on here!” Meanwhile a spat brews over the appointment of another commissioner alleged to have spied for former-communist Yugoslavia.

- Iran-backed Houthis fired what they claim was a hypersonic missile at Israel’s international airport, evading its defences. No harm was done, but the Houthis are getting better weapons, and a larger Israeli response seems inevitable. Israel’s war cabinet also set the goal of returning its displaced population to the north, into which Iran-backed Hezbollah fires almost daily from Lebanon. The US envoy to the region just stated attacking Hezbollah won’t allow displaced Israelis to return home, implying the key is a Hamas hostage deal – which means Hamas have an incentive not to make one to escalate the regional conflict. Meanwhile, rumours swirl PM Netanyahu is to fire defence minister Gallant for the second time (the first reversed after street protests, the interjection of the PM’s wife perhaps stymieing it this time). If it happens, there’s a higher probability of an attack on Lebanon including a ground operation. That would risk the regional conflagration simmering since October 7, 2023. But will it wait until after 5 November?

- The US has underlined its concerns Russia is helping Iran with nuclear technology in exchange for Tehran’s aid in fighting Ukraine. That’s as the new “reformist” Iranian president says his country “didn’t want to enrich uranium at near-weapons grade levels but had been forced to by the US withdrawal from its nuclear deal with world powers.” What can one retort other than, “I am shocked, shocked that nuclear weapons are going on here!”

- Russia announced it will expand its armed forces by 180,000 to a standing army of 1.5 million active servicemen (nearly double that including support staff). The EU feels like it has 180 people thinking how it can thrive in this realpolitik world, and 150 million rejecting their work.

“That’s the truth about Las Vegas. We’re the only winners. The players don’t stand a chance.” – Sam ‘Ace’ Rothstein, Casino

Tyler Durden

Tue, 09/17/2024 – 11:05

via ZeroHedge News https://ift.tt/PEeB7b1 Tyler Durden