China Reloads Monetary Bazooka With Record Cut To One-Year Policy Rate, But Everyone Waiting For Fiscal Firehose

China is not done stimulating.

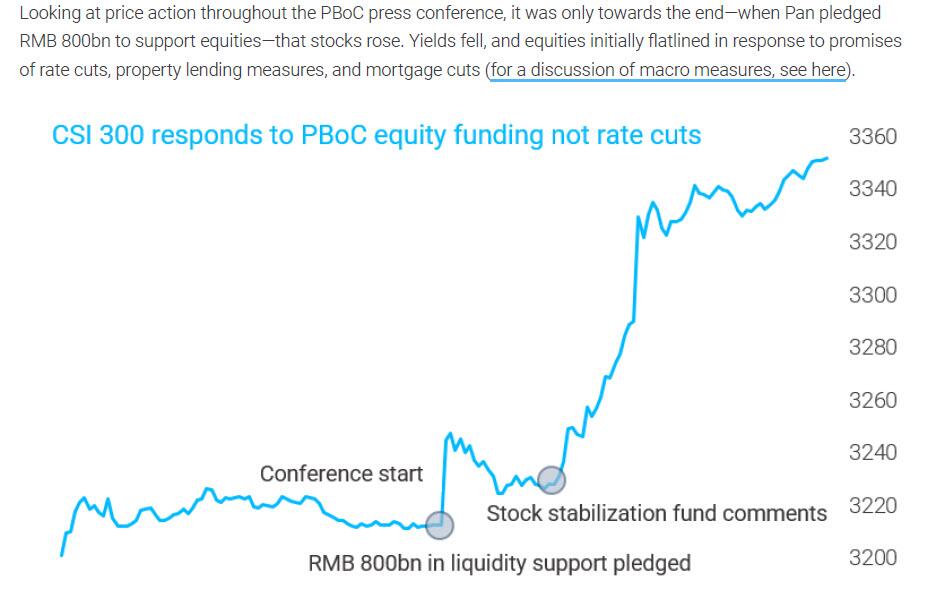

One day after the PBOC shocked markets with a monetary bazooka that included multiple rate cuts, house market supports and most notably, a remarkable RMB800 billion pledge to prop up the country’s flailing stock market (the Chinese Put has moved out of the “National Team” basement)…

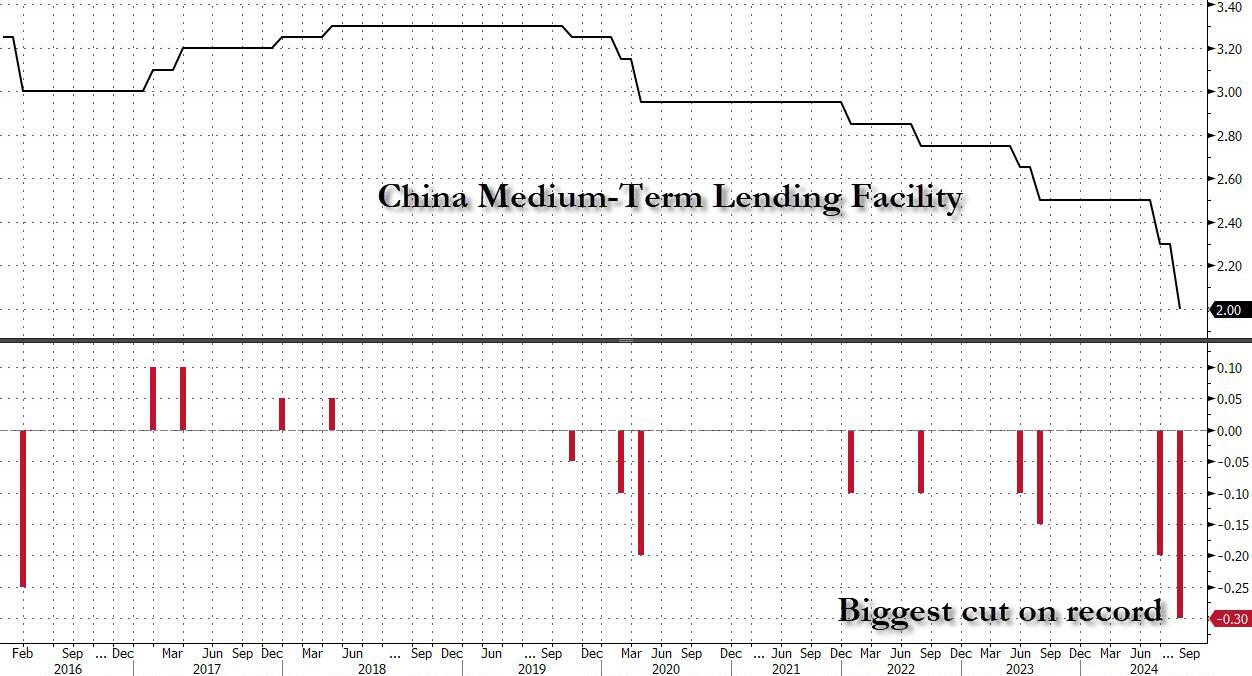

… China was at it again, and on Tuesday, lowered the interest rate charged on its one-year policy loans by the most on record, expanding on its sweeping program to revive confidence in the world’s second-largest economy (which already appears to be fading).

The PBOC cut the rate of the medium-term lending facility to 2% from 2.3%; the 30-basis-point cut was the biggest since the bank began using the monetary tool to guide market interest rates in 2016.

The expected move followed central bank Governor Pan Gongsheng’s announcement the previous day of a broad stimulus package that amounted to an adrenaline shot for an economy on the cusp of a deflationary spiral.

“The cut is part of the package,” said Bruce Pang, chief economist for Greater China at Jones Lang LaSalle, quoted by Bloomberg. “The market is keeping a close eye on the strength, frequency and synergy of measures to follow as China strives to achieve this year’s around 5% growth goal.”

The latest stimulus frenzy helped rally the yuan past the 7 per dollar milestone for the first time in 16 months. Chinese stocks extended their gains, with the onshore benchmark CSI 300 Index on track to wipe out all of its losses for 2024. The yield on China’s 10-year bonds fell 1 basis point to 2.05%, after reaching a record low of 2.00% the day before.

The cut to the MLF rate is a prelude to more significant measures such as a promised reduction in the rate on seven-day reverse repurchase notes, which the PBOC increasingly favors as the main policy lever. The rate on those instruments will be lowered by 20 basis points to 1.5% “soon,” Pan said Tuesday.

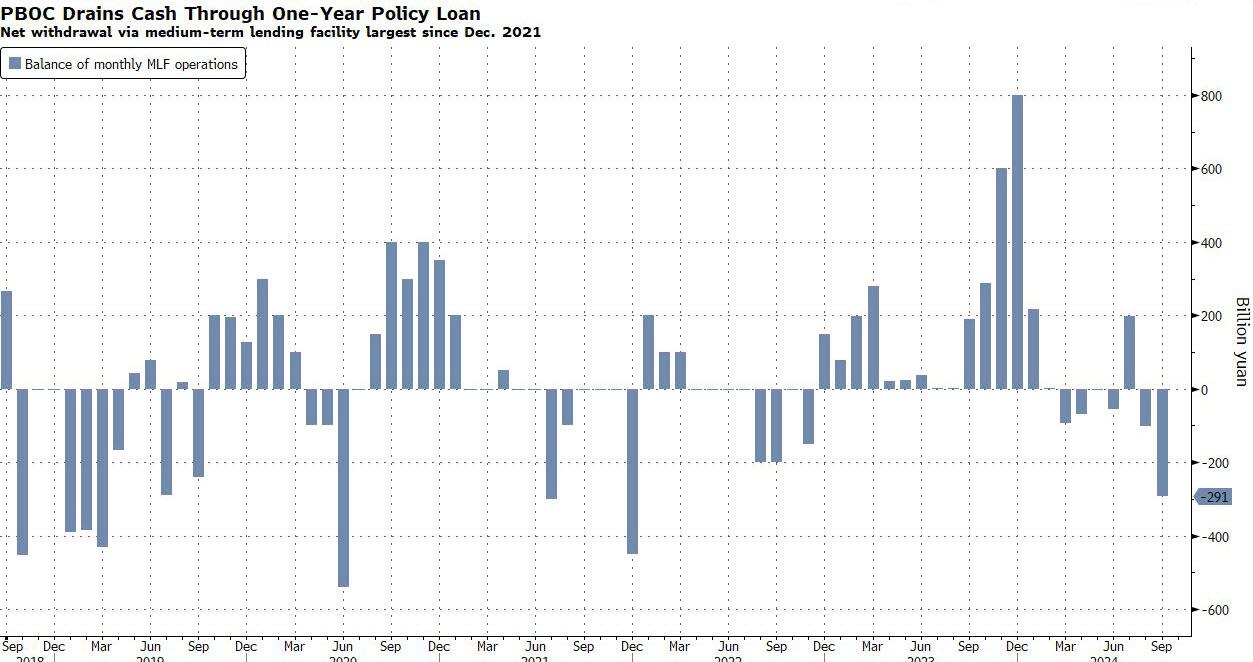

In reflection of the new framework, the PBOC drained a net 291 billion yuan ($41.4 billion) via the MLF, the biggest drainage since December 2021. The outstanding MLF loans are widely expected to be gradually replaced by other tools, including cash injections through reserve requirement ratio cuts, as the PBOC seeks to influence market borrowing costs more effectively.

“The MLF may be downgraded to become a tool to adjust the marginal borrowing costs of banks,” said Zhaopeng Xing, senior strategist at Australia & New Zealand Banking Group. “The MLF rate in the future could change following movements in market rates.”

One day earlier, the central bank chief revealed a plan to unleash 1 trillion yuan in long-term liquidity with a 50-basis-point reduction of the RRR, which determines the amount of cash lenders must keep in reserve. Along with other new funding tools, the measures more than compensated for the effect of the net withdrawal on market liquidity.

“Looking ahead, there is room for further replacement of MLF liquidity with RRR cut-induced liquidity given heavy MLF maturity in the coming months,” said OCBC strategist Frances Cheung. The rate cut on the one-year lending Wednesday “renders the facility more aligned with the funding costs” in the interbank market, she added.

So after this barrage of monetary easing by China, what does the market think? In short: “we’ve been here before.“

While China has repeatedly engaged in monetary stimulation in the past, what analysts say needs to happen for this rally to be sustainable and more than just a tactical bounce, is a boost of consumer demand, i.e., fiscal stimulus, i.e., a flood of new debt to give China’s middle class some extra take home money.

Overnight China the focus again enjoying another day in the sun albeit with headline price action softer than the move we saw yesterday. Elsewhere however Asian markets outside of China and futures are pointing lower.

As Goldman’s Lauren Rose writes, “after a wave of coordinated policy measures were announced in China yesterday the euphoria of price action did not quite match up to flows. Regionally the desk saw both LOs and HFs chase the move although noting that whilst market turnover remains strong today, the cadence of tickets has dropped off and now more passive in style. However in Europe and the US follow through was much more limited. Here in Europe there was an initial wave of both LO and HF demand for China proxies (Luxury and Miners), this dropped off into the afternoon session despite EU Miners basket closing up ~ 3 s.d. and Luxury and China Exposure baskets closing in more than 2 s.d. moves. Outside of single stocks the bulk of more constructive flow was in the options space with call buying evident. In the US flow was concentrated in ETFs where the desk saw buying in China levered products but whilst the cover bid was evident, LOs used the rally to trim.”

Ultimately this indicates a lack of conviction that this move higher can be sustained, according to the Goldman trader, who notes that “for this to be seen as an inflection point would need the reassurance likely of demand side stimulus and some stabilization in the data for September (after very weak August datapoints).”

Whilst the story in China is very specific, the lack of appetite to engage does feel emblematic of the sentiment across global equities right now. The macro focus has shifted from inflation to growth and yesterday’s US data was not helpful in this regards with a miss on Consumer Confidence and Richmond Fed factory index where composition was weaker (particularly in regards to employment and shipments). As the Goldman trader further notes, when looking at the micro, the 4% rally in Nvidia on pretty benign newsflow (report that CEO Jensen is no longer selling stock) is an example of the sensitivity to chasing moves in larger caps or at least missing out on performance there. However, “overall appetite to chase seems very low and positioning and sentiment on the whole does not match with markets around ATHs.” Rowe concludes that it is “hard to see this changing in the next month with another two sets of labor market reports, the next Fed meeting and the US election, alongside a weak period of seasonality in regards to earnings downgrades.”

Meanwhile, China will hope that its barrage of monetary stimulus will be enough. It won’t, and as we said yesterday, after an initial euphoric period of 1-2 months, expect the selling to resume…

The half-life of this intervention will be 2-3 months, then markets will realize China is not stimulating demand. Then we see new decade lows, then China goes all in with $2TN+ fiscal bazooka https://t.co/hmCFY1dV7I

— zerohedge (@zerohedge) September 24, 2024

… at which point Beijing – kicking and screaming – will have no choice but to finally unleash the stimulus bazooka, something which Bloomberg reports could come as soon as “the next few days” even though the administration is reticent to endorse any kind of stimulus that involves direct cash payments to the population (that, too, will change), at which point gold and crypto will scream to fresh all time highs.

Tyler Durden

Wed, 09/25/2024 – 13:05

via ZeroHedge News https://ift.tt/L95V1pR Tyler Durden