Italian Prime Minister Giorgia Meloni delivered a powerful speech after receiving the Atlantic Council’s Global Citizen Award in New York, focusing on the importance of Western values, democracy, and the fight against authoritarianism.

The Brothers of Italy (FdI) leader was awarded the prize on Monday during a gala dinner at the United Nations for her “groundbreaking role as Italy’s first female prime minister, her strong support of the European Union and the transatlantic alliance, and her 2024 chairmanship of the G7.”

In her acceptance speech, Meloni urged the West to reject the idea of decline and instead reaffirm its moral and democratic foundations.

Meloni warned that authoritarian regimes were gaining ground by exploiting the perceived weakening of Western democracies.

“We must resist the lure of authoritarianism because the true strength of democracies lies in their values and freedoms, not in power alone,” Meloni stated. She invoked patriotism as a guiding principle and argued that embracing national identity is essential for preserving democratic institutions and progress.

The Italian premier reiterated her commitment to Ukraine and urged the West to stand firm against Russian aggression, warning that the current conflict represented a pivotal moment for the West in its defense of self-determination and freedom.

“We must not waver in our support for Ukraine. This is about more than borders — it’s about the future of global order and democracy,” she said.

One prominent admirer Giorgia Meloni has attracted is the CEO of Tesla and owner of X, Elon Musk, who described her as “someone who is even more beautiful on the inside than she is on the outside.”

“She’s also someone who is authentic, honest, truthful — and that can’t always be said about politicians,” Musk added.

The tech billionaire has been particularly complimentary about Meloni’s apparent hard stance on illegal immigration (although Italian conservatives may contest her success on that issue) and her commitment to pro-family policies.

In response, Meloni praised Musk’s visionary leadership, stating: “Elon Musk has changed the way we think about technology, energy, and the future. It is leaders like him who push the boundaries of what is possible, and we are eager to see how Italy can be part of that future.”

Israeli Missiles Intercepted Over Syrian Port City Which Hosts Russian Navy

The Syrian Army has told Reuters that Israeli missiles have targeted the Syrian port city of Tartous shortly before midnight Tuesday evening (local time).

Syria’s air defenses reportedly intercepted the inbound missiles, with Al Mayadeen saying that at least two Israeli missiles were observed inbound. There are currently widespread reports of multiple explosions.

Tartous is Syria’s second largest coastal city. It lies just to the north of Lebanon, and Israeli attacks on it are very rare. Instead, most assaults have focused on Damascus and its environs over the past several years.

The staunchly pro-government stronghold didn’t even come under much Israeli fire throughout the totality of the Syrian proxy war.

Russian bases and assets are positioned in Tartous and nearby along the coast, a reality which has also ensured that Israeli strikes there remain relatively rare. The Russian Navy’s only deep water Mediterranean port is located in Tartous.

Israeli media has also picked up on the nighttime attack, and is writing that the Israeli Air Force was likely behind it.

Currently Israel is engaged in a new expanded anti-Hezbollah offensive in south Lebanon, which has resulted in over 550 Lebanese deaths and thousands of injuries.

There are fears that the fighting could spread through the region, if Shia paramilitary groups in Iraq and Syria get involved, and if Tehran directly enters the fighting in Lebanon. Damascus has always been a powerful state ally of Hezbollah.

So far, the Assad government has remained uncharacteristically quiet regarding what’s happening in Lebanon, even as some pro-Hezbollah Lebanese have questioned why Damascus hasn’t come to Hezbollah’s direct aid.

Belarusian media reported earlier this month that their security services busted a Japanese spy. He allegedly entered into a fictitious marriage that helped him legalize his stay in the country, after which he set up a business in Gomel to explain his travels, including to the border. He also taught Japanese. The spy allegedly had over 9,000 photos of roads, bridges, and military facilities and was actively in contact with his embassy. These reports raised a lot of eyebrows since few expected Japan to spy on Belarus.

As it turns out, his home base of Gomel is in Ukraine’s crosshairs as explained last month here, and it’s possible that the security services’ additional scrutiny on all activities there as part of their precautionary measures resulted in them finally catching him. His interrogation also revealed that he was involved in the failed summer 2020 Color Revolution and had been monitoring the socio-economic situation as well, including the availability and prices of goods as well as locals’ reaction to this.

Considering the importance of his activities, especially in the context of the specialoperation, there’s no way that he’d be allowed to continue operating if anyone had picked up on what he was doing earlier. It’s therefore almost certainly the case that he only came on their radar recently as was speculated above. This means that he was transmitting highly sensitive information during the past two years of the New Cold War’s top proxy war, thus raising the question of why Japan would want to do this in the first place.

What might have been going on is that Japan was passing everything along to its Western partners in the implied hopes of them then supporting it more in its own part of the world. His most recent activities might also have played a role in Ukraine’s recent drone provocations in Belarus. In fact, he might have been pressured by his handlers into taking more risks than usual because the West demanded more information for Ukraine, which could have contributed to him finally getting caught.

This explanation is the most logical since Japan couldn’t act on its own with what that spy hadn’t uncovered this entire time. It was also reported that he was spying on China’s Belt & Road Initiative investments too, of which its primary one in Belarus is the “Great Stone” industrial park, which could have disguised his more nefarious activities had he been caught earlier under different circumstances. It’s much better, after all, to be busted for conducting “business intelligence” than military intelligence.

In retrospect, there’s not much that the security services could have done better to have stopped him ahead of time.

He was legally in Belarus, had his own business, and was also teaching Japanese at a local university, thus making him a model immigrant. Nobody could have plausibly suspected that he was up to no good.

If there’s any silver lining to this case, it’s that the spy was finally caught and will no longer be sharing information with his handlers to pass along to the West and their Ukrainian proxies.

Escobar: Will A BRICS Bretton Woods Take Place In Kazan?

Authored by Pepe Escobar,

With less than a month before the crucial BRICS annual summit in Kazan under the Russian presidency, serious informed discussions are raging in Moscow and other Eurasian capitals on what should be at the table in the de-dollarization and alternative payment system front.

Earlier this month Andrey Mikhailishin, head of the task force on financial services of the BRICS Business Council, detailed the list of top projects under consideration. They include:

A platform for multilateral settlements and payments in BRICS digital currencies, connecting the financial markets of BRICS members: that’s BRICS Bridge, which bears similarities with the Bank of International Settlements-linked MBridge, already in effect. That will complement intrabank systems already in action, as in Russia’s SPFS and Iran’s CPAM settling financial transactions – and 60% of their trade – in their own currencies.

A blockchain-based payment system that entirely bypasses the US dollar: BRICS Pay. Arguably 159 participants may be ready to adopt this sanction-evading, similar-to-SWIFT mechanism right away.

A settlement depository (Clear).

An insurance system.

And crucially a BRICS rating agency, independent from the Western giants.

What’s at stake is the extremely complex design of a brand-new financial system – decentralized and using digital technology. BRICS Clear, for instance, will be using blockchain to record securities and exchange them.

As for The Unit, the value of the common unit of account is pegged by 40% to gold and by 60% to a basket of BRICS member’s national currencies. The BRICS Business Council considers The Unit a “convenient and universal” instrument, since a unit can be converted into any national currency.

That would definitely solve the nagging problem of exchange rate volatility when cash balances accumulate from settlements in national currencies; for example, a mountain of Indian rupees used to pay for Russian energy.

Who Do I Call to Talk to BRICS?

I asked a very direct question to two Russian analysts, one of them a finance tech executive with vast experience across Europe, and the other the head of an investment fund with global reach. Considering the sensitivity of their posts, they prefer to remain anonymous.

The question: Is BRICS ready to become an actor in Kazan next month, and what should be on the table in terms of the strategy to establish an alternative payment system?

The Answers. Analyst 1:

“Time has come for BRICS to become a real actor. The world demands it. The leaders of BRICS countries clearly understand it. They have the moral power and the political will to set up an organization to provide a number for BRICS to be called in – that’s the best question for the upcoming summit.”

The analyst is referring to what could be dubbed “the Kissinger moment”, when Dr. K famously quipped, in the Cold War era, “when I want to talk to Europe, who do I call?”

Now to Analyst 2:

“For a BRICS agreement amongst countries to mean something, countries need to agree on a framework of action and that means accepting some responsibilities in exchange for certain rights. And it sounds there’s no better way to achieve that than to arrive at mutually agreed obligations on settlement of financial transactions.”

One of the analysts added a very important, specific point: “By now the situation is pretty clear, to properly address the issue of cross-border payments. The best mechanism should be based on the New Development Bank (NDB), given that Russia has a mandate to propose the new president of that organization. Whoever the candidate will be, cross-border payments should be at the top of his agenda.”

The NDB is the BRICS bank, based in Shanghai. The analyst hopes this decision on the future of the NDB will be made before the BRICS summit: “Given the diplomatic and political considerations, the candidate should be made known, formally or informally to the member countries.”

New BRICS blockchain payment system to be game-changer amid ‘unstoppable’ dedollarization – expert

Moscow’s decision to create a new BRICS blockchain-based payment system is a “game changing” development for the multipolar world, Christopher Douglas Emms, head of the Brokerage… pic.twitter.com/4cEBFb3c7c

As it stands, the talk of the town in Moscow informed circles is that Alexey Mohzin, the IMF’s executive director for Russia, has a 60% chance to be appointed to the NDB. In parallel, Ksenia Yudaeva, a former G20 sherpa and former deputy of Russia Central Bank’s Elvira Nabiullina, may become the new representative with the IMF.

So what may be in the cards is a NDB/IMF reshuffle on the Russian front. The focus should be on the potential for future productive change – rather than missed opportunities; the NDB’s policies so far have not been exactly revolutionary – considering that the bank’s statutes are linked to the US dollar.

The new deal could place the NDB as leverage for a reform of the IMF, rather than an alternative to it.

The “Kissinger moment” does play a key role in this equation. It will highlight that until the moment turns into reality, the NDB should be the sole actor for effective changes in crucial matters like the stability of the financial infrastructure.

And from that perspective, as one of the analysts note, “The UNIT and all other similar projects may be presented as complementary risk management tools hedging against reckless monetary policies and Global Financial Crisis-2 risks.”

Time though is running out – fast. President Putin recently met with the Russian Union of Industrialists. They have sent a letter to the administration and the Russian Central Bank outlining what they consider the most promising ideas.

The Unit is one of them. Prime Minister Mishustin’s government is now on the final stages of deciding which projects to support: for the BRICS summit in Kazan, and one week before, for the annual summit of the BRICS Business Council in Moscow.

A BRICS Bretton Woods?

I posed the same BRICS question to the Russian analysts also to indispensable Prof. Michael Hudson – who actually provided a concise in-depth critique of what may be on the table, while offering a different solution.

For Prof. Hudson, “a new institution has to be created – a Central Bank empowered to issue credit to finance the trade and payments deficits of some countries, with an artificial bancor-type SDR [Special Drawing Rights].”

Prof. Hudson argues “this would be different (his italics) from a clearing house system for existing banks. It would be a BRICS’ IMF. Its bancors credit or balance sheet would only be for settlements among governments, not a generally traded currency. Indeed, making the bancor widely traded as a speculative vehicle (such as the UNIT is) would introduce major instability and have nothing to do with the needed bank transfer balance sheet.”

A reformed NDB, possibly next year under a new Russian presidency, should have all it takes to become a “BRICS’ IMF.”

Prof. Hudson adds that “to succeed, the Kazan conference should be a full-fledged BRICS Bretton Woods. Maybe it is too soon to actually introduce a fait accompli. Perhaps it would be a venue to throw open a set of alternatives — including what would happen by ‘doing nothing’ and going with the current IMF system. The fact that the IMF just cancelled its trip to analyze the Russian economy may be a catalyst.”

Prof. Hudson in fact refers directly to Executive Director for Russia, Alexey Mohzin, who confirmed that the IMF should have come to Russia for consultations, part of their annual review of the Russian economy, but cancelled it because of “technical unpreparedness”.

All that brings us once again to the “Kissinger moment”; it’s unclear whether Kazan will come up with a “BRICS number” anyone could call.

Leaving the dollar-based system for good: What are the digital ruble and BRICS Bridge?

By July 1, 2025, the largest Russian banks will have to provide their clients with the ability to conduct transactions in digital rubles, according to the Russian Central Bank. Pilot testing… pic.twitter.com/fXlp0He0X3

Prof. Hudson makes an essential last point on the Global South’s dollar debt: he stresses “how to handle BRICS members existing overhang of dollar debts” is a major problem.

What is clear is that “the BRICS bank [the NDB] should not finance deficits by member countries for such payments. In practice, there would have to be a moratorium on such payments – in view of the present weaponization of Western finance.”

Prof. Hudson recalls the chapter in his book Super Imperialism “on how the US moved against Britain in 1944 to get an agreement that it then presented as a pro-US fait accompli to Europe.” The book “reviews all the arguments that took place there.”

Prof. Hudson wishes he would be part of the new, ongoing process. Imagine if BRICS+ manages to pull it off: getting a Global Majority-approved agreement on a new, equitable, fair financial system then presented to the $35 trillion-indebted superpower as a fait accompli.

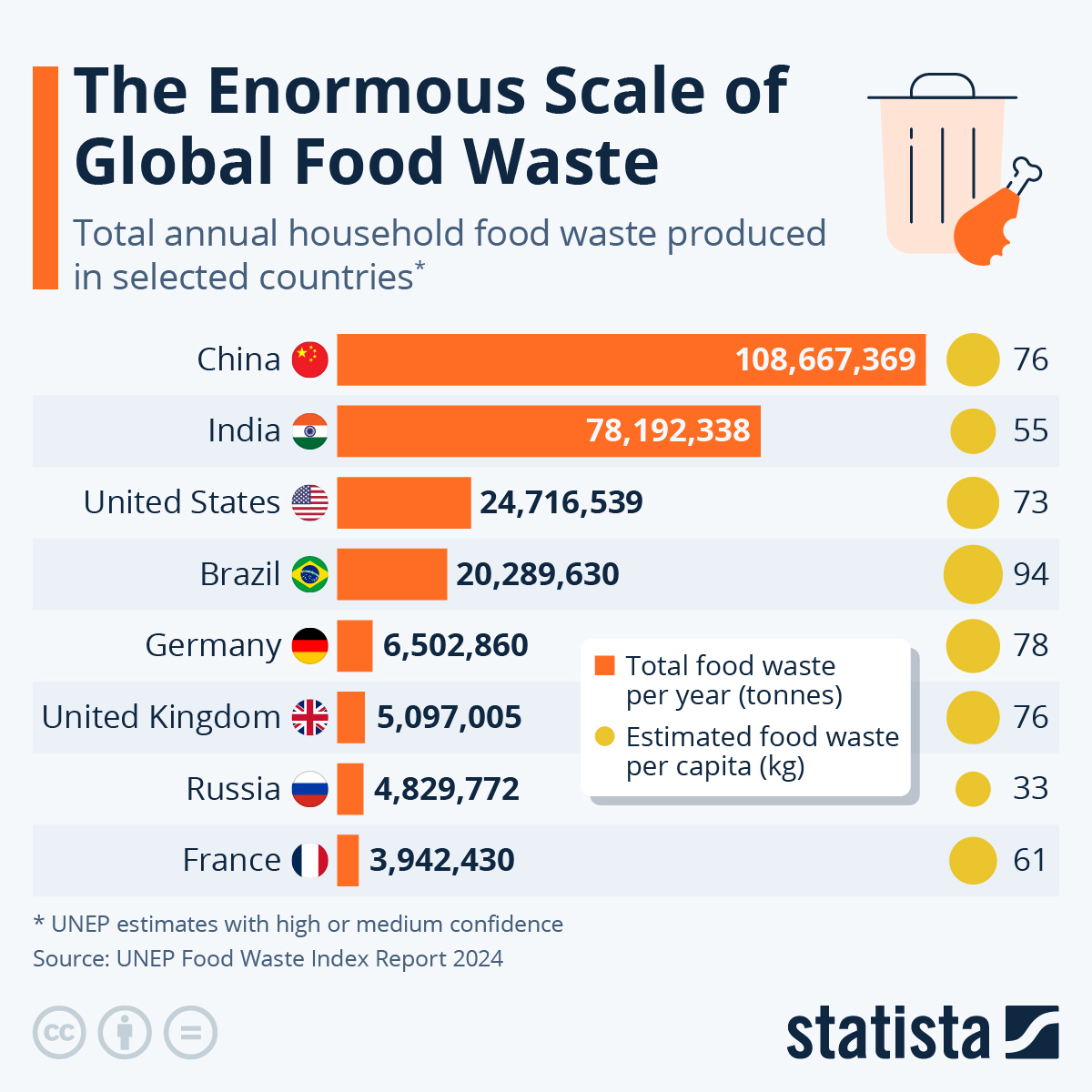

The UNEP estimates that in 2022, the world produced 1.05 billion tonnes of food waste across the retail, food service and household sectors.

The average amount of food waste per capita that year is estimated to be 132 kg, of which 79 kg was household waste. This equates to roughly 19 percent of food available to consumers being wasted across the retail, food services and household levels.

This is a problem seen across all levels of society, reflected in how the figure for household waste is broadly similar across country income groups at 81 kg per capita for high income, 88 kg per capita for upper middle, 86 kg for lower-mid income, while there was insufficient data for lower income countries.

When looking at the data on a country-by-country basis, the highest absolute figures for food waste were recorded in the two countries with populations of more than a billion people.

China wastes an estimated 108.7 million tonnes of food per year while India discards 78.1 million tonnes.

The United States creates 24.7 million tonnes of food waste annually, while in Europe, France and Germany produce between 3.9 and 6.5 million tonnes per year.

Things look rather different when it comes to waste produced per capita. For example, the average household in India discards 55 kg of food per year while for the United States the figure is 73 kg. By comparison, Russia’s total household waste comes to an estimated 4.8 million tonnes each year with waste per capita only coming to 33 kg.

It’s Friday, Sept. 20. Interestingly, Election “Day,” which is now a profound misnomer, begins today: In Virginia, Minnesota, and South Dakota, citizens 18 and older can begin voting in the 2024 presidential election.

Today is also the day of the week when I share a quote intended to be uplifting or educational. Earlier this week I wrote about Constitution Day, which fell on Tuesday, although the administration encourages us to think of this as “Constitution Week.”

I’m all for that, especially since the proclamation issued in President Biden’s name reprised the famous Benjamin Franklin “a Republic, if you can keep it” exchange. The White House didn’t garble the exchange as so many others have done. Nor did it provide the context that really makes the exchange so interesting – and so contemporary.

So how do we know about Ben Franklin’s profound “if you can keep it” rejoinder concerning the type of government forged at the Constitutional Convention in 1787?

The original source – the only source, actually – is a Scots-Irish immigrant from County Antrim named James McHenry, who arrived on these shores at 18. Young Mr. McHenry apprenticed as a physician under Benjamin Rush, a Founding Father from Philadelphia, and followed Rush into service as a military surgeon in George Washington’s army. Captured by the British during the war, McHenry was paroled, only to rejoin the Continental Army. He was with Washington at Monmouth and attached to Lafayette’s troops at Yorktown.

After the war, he was one of Maryland’s representatives to the Constitutional Convention and kept a regular diary. It is in that journal that McHenry records an exchange he apparently overheard – or heard from someone else – on Sept. 18, 1787, the last day of the convention:

“A lady asked Dr. Franklin Well Doctor what have we got a republic or a monarchy – A republic replied the Doctor if you can keep it.”

“Dr. Franklin” was an honorific for Ben Franklin, but who was the lady in question? Even though it’s not a mystery, succeeding generations of historians and politicians have obscured her identity – to their detriment and ours.

In his 2019 memoir, “A Republic, If You Can Keep It,” Neil Gorsuch flubs the facts of the story that forms the very title of his book. He writes that “a passerby asked what kind of government the delegates intended to propose” – thereby confusing the time sequence and hiding the identity of Franklin’s interlocutor.

A month after the book’s publication, House Speaker Nancy Pelosi took further liberties with the historical record.

Announcing the first impeachment inquiry of President Donald Trump, Pelosi said, “On the final day of the Constitutional Convention in 1787, when our Constitution was adopted, Americans gathered on the steps of Independence Hall to await the news of the government our founders had crafted. They asked Benjamin Franklin, ‘What do we have, a republic or a monarchy?’ Franklin replied, ‘A republic, if you can keep it.’ Our responsibility is to keep it.”

At least Pelosi had the time element correct. But the crowd on the steps of Independence Hall was a concoction.

Even those who don’t airbrush “the lady” Franklin spoke to that day give her short shrift. In his best-selling biography of Benjamin Franklin, Walter Isaacson properly identifies her, but hardly in complimentary fashion. He describes her an “anxious lady” who “accosted” Franklin. The author also mangles the famous quotation, having her ask, “What have you given us” rather than “What have we got …”

This is not a minor lapse, according to historian Zara Anishanslin, an expert in the Revolutionary War period, as it implies “her passive role in the political process.” Professor Anishanslin adds, “She is cast as a shrill, inappropriate woman, excluded from the politics of the nation’s founding.”

But this is not how Franklin’s contemporaries in Philadelphia would have viewed her. They would have known, or at least assumed, that Franklin’s inquirer was the erudite and well-connected Elizabeth Willing Powel. But James McHenry doesn’t require us to guess. His journal entry adds helpfully, “The Lady here alluded to was Mrs. Powel of Philada.”

It’s a sorry sign about the state of modern education that Eliza Powel is largely forgotten. She was just as much a Founding Father as James McHenry and the other signers of the Constitution (though Founding Mother is more precise).

Although no women were chosen as delegates to the Constitutional Convention, Mrs. Powel’s influence in these colonies was never in question. The wife of prosperous businessman Samuel Powel, she was known for convening salons that wrestled with the hardest questions of the day, including whether to break with Great Britain.

And not to diminish Samuel Powel, but the wealth and connections that made their home the epicenter in Pennsylvania politics and Philadelphia society originally came from her side of the family. Elizabeth’s father Charles Willing and her brother Thomas Willing were rich traders and merchants who served, as did Samuel Powel, as early mayors of Philadelphia. Eliza Powel wasn’t content just to enjoy the perks of power and wealth. In dinner parties at her home (the guests frequently included George and Martha Washington), she displayed a shrewd grasp of politics and a willingness and the intellectual dexterity to join the discussion that led to a new kind of government.

The political figure in modern America who seems to me most like Elizabeth Powel is Nancy Pelosi. Her father and brother were both mayors of Baltimore, and Pelosi’s father also served in the House of Representatives. Upon relocating to California, Nancy Pelosi befriended Phil and Sala Burton. One could say, a bit puckishly, that the Burtons were the George and Martha Washington of San Francisco in those years. (All of which is why Pelosi’s flight of rhetorical fancy regarding Ben Franklin and Eliza Powel seemed so discordant.)

In any event, in the 1780s the Powels were close friends of the Washingtons. Evidence in the form of letters found in the George Washington Papers at the Library of Congress shows that George Washington valued Eliza’s counsel greatly. That was a good thing for American history. In the third year of his presidency, George Washington confided in friends how much he longed to leave government and return to Mount Vernon. The friend whom Washington biographers credit with talking him out of it was none other than Elizabeth Powel.

James McHenry didn’t publish his account of the Franklin-Powel exchange until 1803, and even then he did so anonymously. He added other details, too, describing Powel as “a lady remarkable for her understanding and wit.” He also fleshed out the scene and had Franklin “entering the room” to talk to Powel.

Over time, friends began to ask Powel about the exchange. She didn’t remember it. Not because, as she wrote to a friend in 1814, it didn’t happen. But because she’d had so many momentous discussions over the years with the Founders and their contemporaries that 27 years later she couldn’t begin to recall them all.

Or, as she put it, she had been “associated with the most respectable, influential Members of the Convention that framed the Constitution, and that the all important Subject was frequently discussed at our House.”

“Tracing its twists and turns over the centuries, we see Powel, a politically active, influential patriot in her own time, shaped to mold expectations about the history of women and politics. The story shifts – from her own assertion that she couldn’t possibly remember all the many important political conversations that took place within her home, to one in which she is simply an ‘anxious’ lady ‘accosting’ Franklin, to the recent omission of women at all.

“As we consider how and why America continues to elide the history of founding women from its collective origin story, we should take note that in 2019 we actually give less credit to this politically savvy woman than men did during the founding era,” Anishanslin added before concluding: “Recognizing women’s leadership in the past, as well as the present, might make it easier to keep a republic.”

And that is our quote of the week.

Carl M. Cannon is the Washington bureau chief for RealClearPolitics and executive editor of RealClearMedia Group. Reach him on X @CarlCannon.

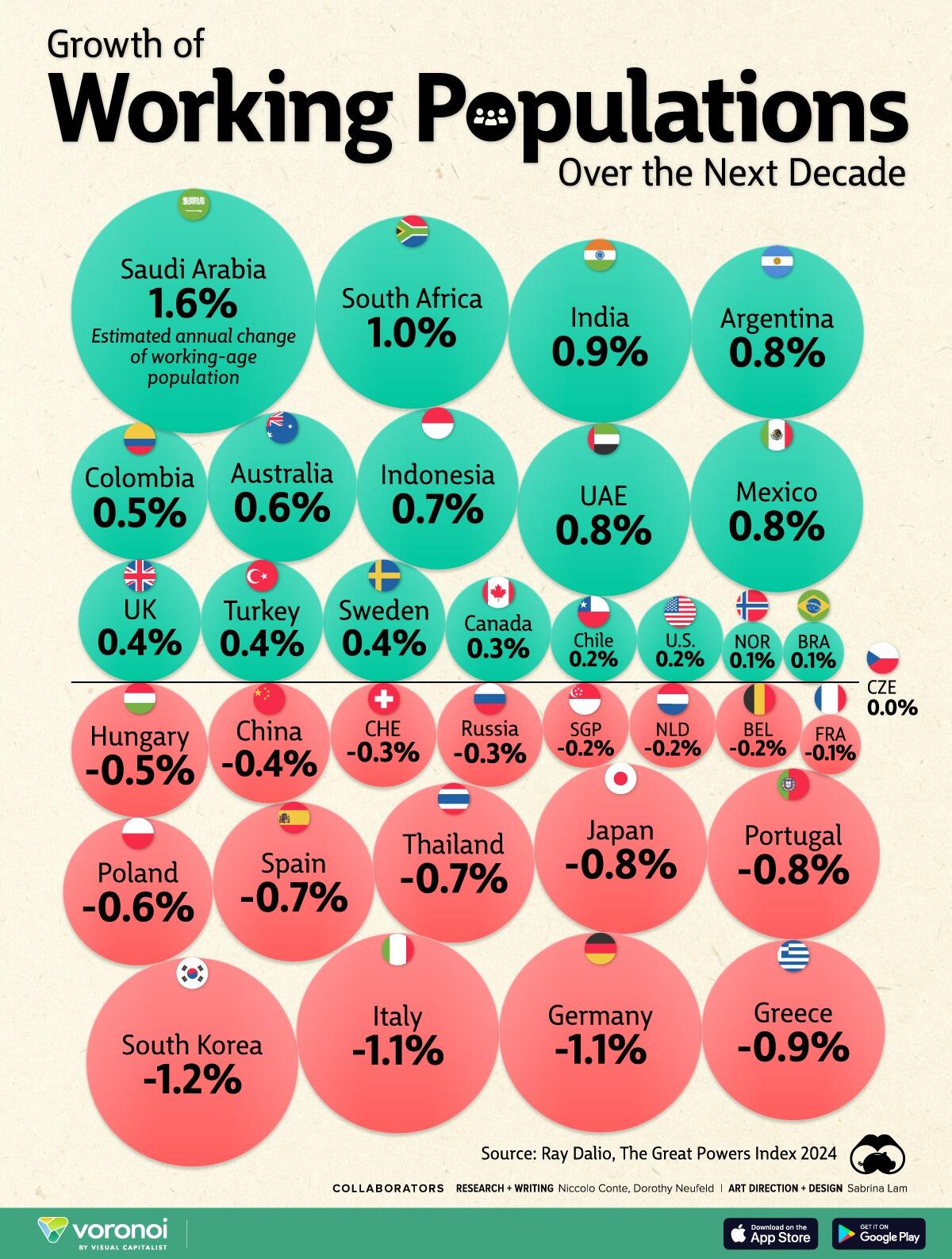

Visualizing The Expected Growth In Working Age Populations Around The World Over The Next 10 Years

Today, the working age population in almost half of U.S. metropolitan areas has declined due to demographic shifts, and this trend is set to continue.

As a result, the U.S. workforce is projected to grow at just 0.2% annually over the next decade, roughly a quarter of the rate of markets like India and Mexico. Given the low birth rates and aging populations across many advanced economies, the world’s workforce is set to change significantly, with implications for economic and productivity growth.

Here are the estimated annual changes in the working age population across 35 countries over the next decade:

Saudi Arabia is projected to see the fastest-growing workforce across major economies, driven by high fertility rates of 2.8 children per woman and a rising expatriate population.

India, ranking in third, is set to contribute 24.3% of the world’s workforce over the next decade. With a current median age of 28.4, its working age population is expected to surpass one billion by 2030. These factors provide a significant competitive edge, especially in the services and manufacturing sectors, while also driving increased consumption among younger generations in the world’s most populous country.

Largely due to falling birth rates, the U.S. ranks 15th overall in the 35 countries on the list. In fact, America saw the slowest decade of population growth between 2010 and 2020 since the Great Depression, growing by 7.4%. For perspective, the U.S. population grew at nearly double this rate during the 1990s.

At the other end of the spectrum, South Korea ranks in last, with its workforce projected to see an annualized growth rate of -1.2% over the next 10 years. South Korea has the lowest fertility rate worldwide along with restrictive immigration policies, which are straining working age population growth and productivity.

Overall, 49% of major economies are projected to see declining working age populations, particularly across European nations and countries in Asia including China, Japan, and Thailand.

To learn more about this topic from an asset class perspective, check out this graphic on 10-year asset class return forecasts.

Earlier this month, Real Clear Defense published my commentary, “West Point Needs a Reset,” detailing why I and many fellow graduates believe the United States Military Academy has lost its way and needs to get back to the basics of educating future Army officers to fight and win our nation’s wars. Almost immediately, the piece went viral, shared across many platforms, including STARRS (Stand Together Against Racism and Radicalism in the Services) and the MacArthur Society of West Point Graduates.

It also attracted the attention of West Point, which up to now has refused to discuss or even acknowledge serious graduate concerns over wokeness, politicization, divisive and battlefield-irrelevant course materials, merit-based admissions, and advancement, undermining of the cadet Honor Code, unanswered Freedom of Information Act filings and other such issues.

The day after publication, Real Clear Defense Editor and former Marine David P. Craig received the following email from West Point’s Director of Communications, Colonel Terence M. Kelley:

David,

I would like to discuss a recent op-ed you published, “West Point Needs a Rest,” by Tony Lentini.

To say the least, this piece is problematic. It makes false claims about statements by our superintendent, that we offer classes that we do not, and it is quite frank in its homophobia, equating the existence of a voluntary student LGBTQ alliance and social club with sexual deviance. Furthermore, it greatly distorts and misrepresents our curriculum and training programs in a deliberate manner to mislead the reader.

In short, this piece, even if opinion, undermines Real Clear Defense’s journalistic credibility. It is unworthy of your platform, and I respectfully request you consider removing it.

Please contact me at the number below to discuss.

Later that same day, Kelley sent Craig a follow-up email:

Bringing this to the top of your inbox. I would still like to discuss this op-ed. This isn’t about a difference of opinion—this is about fabricated quotes and false statements.

Mr. Craig independently verified the truth and accuracy of my piece, refused Kelley’s request to take down the article, and contacted me for comment on the colonel’s allegations. I offered to discuss everything with Craig, Kelley, MacArthur Society President Bill Prince, and anyone else who wanted to be on the call. Kelley has not responded to that offer. I also decided to do this follow-up piece of my own so that everyone can see how West Point responds to legitimate criticism with ad hominem attacks and false statements, some of which I will discuss here.

The Superintendent did refer to the Honor Code as “aspirational,” which is why I put it in quotes. The minutes of the Academy’s Board of Visitors from the Spring 2023 meeting contain the following on this subject: “LTG Gilland added that USMA was considering simplifying the mission statement, so people better understand what the Academy does and reviewing the Honor Code to make it more aspirational in nature.” Aspirational is most certainly not absolute.

I never said West Point offered “courses in DEI and CRT;” I said, “course materials.” Judicial Watch had to sue the Academy to obtain documents proving that such course materials have been offered. In fact, the Academy’s current course catalogue lists “SS392 Politics-Race, Gender and Sexuality” among its offerings. Included in the course description is: “Emphasis will be placed on the inherent inequalities found within the structures, rules, and processes of the American political system.” Other courses with woke teaching include EN352 Power and Difference, PL377 Social Inequality, HI461 Topics in Gender History, HI463 Race, Ethnicity, Nation, and DEI/CRT themes are woven into other courses and permeate West Point culture.

Referring to my outstanding and unanswered Freedom of Information Act request to learn the fate of those cadets who overdosed on fentanyl-laced cocaine on Spring Break two years ago, Kelley cited the Privacy Act of 1974 but failed to note that I had explicitly not asked for the cadets’ names, only their punishment. As a taxpayer and graduate, I most certainly am entitled to this information.

Kelley derogatorily describes my discussion of West Point sponsoring a Spectrum Club for LGBTQ+ cadets as “quite frank in its homophobia, equating the existence of a voluntary student LGBTQ alliance and social club with sexual deviance.” The context of my statement was that since admitting women, the Academy has struggled with sexual fraternization among cadets and would presumably not sanction a heterosexual club, nor should it. Elsewhere on the sexuality spectrum is bestiality, adultery, and pedophilia; would affinity clubs be permitted in these areas as well?

Kelley impugns my personal honor by repeatedly referring to my statements as “false,” “misleading,” with “fabricated quotes.” In fact, it is Colonel Kelley who is lying and quibbling.

I could go on and on about Kelley’s false allegations and other personal attacks but let me turn to a couple of final points.

First, toward the end of my military service, I sought civilian-relevant experience by serving in Col. Kelley’s MOS (Military Occupational Specialty) as a Public Affairs and Information Officer. Upon departing the Army, I then had a highly successful civilian career in public and international affairs, culminating as a vice president for two independent high-capitalization oil and gas companies. So, I know whereof I speak.

One thing I never did was demand that a news or opinion outlet take down a published piece. I would always manage queries from the media with honesty and integrity and would only ask for corrections of provably inaccurate statements. And I would never, ever engage in ad hominem attacks on a reporter. Colonel Kelley’s emails were completely unprofessional and unworthy of any member of West Point’s administration.

The crux of the problem is that West Point brooks no discussion of divergent viewpoints and issues of concern to graduates. It simply stonewalls or, as in Col. Kelley’s case, engages in ad hominem attacks on those who dare to criticize the institution. I hereby formally request the opening of a dialogue among graduates and the Superintendent about needed reforms at the Academy. But I won’t hold my breath.

* * *

Tony Lentini is a 1971 graduate of the United States Military Academy at West Point. He served five years in the Army, attaining the rank of captain. He is a founding board member of the MacArthur Society of West Point Graduates.

RFK Jr. Asks Supreme Court To Reinstate On NY Ballot For ‘Contingent Election’ Scenario

Robert F. Kennedy Jr. has asked the US Supreme Court to reinstate his name on New York’s presidential ballot after he was disqualified by a lower court.

Kennedy, an independent, suspended his campaign for president on Aug. 23. And while he’s tried to have his name removed from swing state ballots since then, he has left his name on the ballot in other states due to a longshot scenario known as a contingent election that would put the presidency in the hands of the US House of Representatives in the event of an electoral college deadlock.

“If you do vote for me, and neither of the candidates wins 270 electoral votes, which is quite possible—in fact, today our polling shows them tying at 269-269—I could conceivably still end up in the White House in a contingent election,” Kennedy previously said.

On Sept. 21, Kennedy filed an emergency application with the US Supreme Court, which appeared on the docket on Monday. New York state officials have until 4p.m. on Wednesday the 25th to respond, per orders by Justice Sonia Sotomayor.

As the Epoch Timesnotes further, the application states that Kennedy’s campaign gathered more than the required number of signatures from New York voters. The New York State Board of Elections certified more than 100,000 signatures as valid and ordered his name placed on the ballot.

On Aug. 12, Judge Christina Ryba of the New York Supreme Court found Kennedy had falsely claimed he had a New York residence despite living in California. The rented room in Katonah, New York, that he said was his residence wasn’t a “bona fide and legitimate residence, but merely a ‘sham’ address that he assumed for the purpose of maintaining his voter registration” and advancing his candidacy, Ryba wrote.

On Sept. 10, the New York Court of Appeals affirmed the ruling and the next day the elections board certified the general election ballot without Kennedy’s name on it.

On Sept. 18, the U.S. Court of Appeals for the Second Circuit denied the campaign’s motion to reverse the ruling in a one-sentence order.

Kennedy argues in the new application that U.S. Supreme Court precedent is on his side.

Ohio blocked independent presidential candidate John Anderson from that state’s ballot in 1980 after he gathered the required number of signatures from Ohio voters. State officials disqualified him for missing a filing deadline.

In Anderson v. Celebrezze, the U.S. Supreme Court “would have none of it, holding that Ohio’s interests in its filing deadline did not outweigh the First and Fourteenth Amendment rights at stake.”

The precedent “indisputably controls this case” and “is in all material respects indistinguishable,” the application states.

The U.S. Supreme Court “has long recognized the constitutional ‘right of voters to associate and to have candidates of their choice placed on the ballot.’”

“Absent immediate, emergency relief, over 100,000 New York voters who signed the invalidated Kennedy petition will be irrevocably deprived of that right,” the application states.

The Epoch Times reached out for comment to New York Solicitor General Barbara Underwood on Kennedy’s application and did not receive a reply by publication time.

Kennedy’s application followed the U.S. Supreme Court’s Sept. 20 rejection of the Green Party’s request to restore its candidates to the Nevada state ballot for the Nov. 5 election.

The ruling left intact a Nevada Supreme Court decision from Sept. 6 removing the party’s candidates—including presidential candidate Jill Stein—because they used the wrong form when gathering ballot-access signatures from the public.

The degradation of liberal education in America is anything but a niche public-policy concern.

Like all rights-protecting democracies – and especially as a 21st-century great power with globe-spanning interests – the United States requires a host of highly-trained individuals to keep its government functioning, military operating, economy churning, and civil society thriving. Essential men and women perform manual labor, offer basic services, and run small businesses. In addition, the nation needs physicists, chemists, and biologists; lawyers, doctors, and business executives; teachers, software engineers, and architects; journalists and civil servants; military officers, politicians, diplomats, judges, and religious leaders; and many more.

To acquire the professional skills necessary to fill key roles in America’s advanced industrial society, individuals must typically obtain a four-year college degree. Prestigious undergraduate programs, which incubate America’s highly credentialed elites, purport to offer the requisite professional training – or requisite introduction to professional training – within the framework of liberal education.

When true to its mission – transmitting knowledge, invigorating the moral imagination, cultivating independent thought, fostering toleration and civility – liberal education serves the public interest by making experts of all sorts more informed, thoughtful, and judicious. When it betrays its mission – indoctrinating, administering political litmus tests, encouraging a haughty self-regard among those who toe the party line, and mocking and punishing dissent – liberal education subverts the public interest. A doctrinaire liberal education sends into the world young men and women who confuse their reflexes, preferences, aversions, biases, and conceits with the last word and only acceptable outlook on citizenship, government, and justice.

Consequently, remedying liberal education’s rampant dysfunction – suppression of free speech, disregard for due process in cases involving allegations of sexual misconduct, and politicization and hollowing out of the curriculum – should unite left and right. Hectoring professors and sanctimonious administrators promulgating an illiberal campus orthodoxy – supplemented by a critical mass of students selected for their fervent illiberalism – involve a gross abuse of power. Over the long term, the higher indoctrination on campus diminishes elites’ ability to meet their obligations as good citizens, as private sector professionals, as government officials, and as fair-minded human beings.

City Journal editor Brian C. Anderson summarizes the grim situation: “[P]oorly educated students, frequently facing lousy prospects for remunerative work and owing too much money, are not a source of future national flourishing, to put it mildly.” That assessment comes from “A Crisis on Campus,” Anderson’s introduction to “Which Way the University?” Comprising ten short, crisp contributions, City Journal’s symposium on higher education performs a public service by examining the variety of problems that plague liberal education, offering proposals to repair existing colleges and universities, and articulating principles and objectives to guide the creation of new ones.

Conservatives, observes political scientist John Dilulio in “Third Time’s a Charm?,” have been criticizing higher education in America for at least 70 years. The young William F. Buckley Jr. led the charge in 1951 in “God and Man at Yale,” which excoriated the university from which he had just graduated for preaching collectivism and atheism in the classroom. “The latest wave of conservative critiques of elite universities might make a real difference,” Dilulio nevertheless maintains, because of “a broader public awareness of the university problem.” The anti-Israel, pro-Hamas, atrocity-defending demonstrators roiling America’s elite campuses following the jihadists’ Oct. 7, 2023, massacres in Israel concentrated the minds of many – parents, legislators, wealthy donors – who had averted their gaze from liberal education’s steady deterioration.

In “Free Speech Is Not Enough,” Hillsdale College history professor Wilfred M. McClay agrees that liberal education has been corrupted. He, too, condemns professors and administrators for the “imposition of an intellectual monoculture, driven by the imperious claims of identity politics, propounded by an activist faculty operating in ideologically committed disciplines, and resulting in a suppression of diverse points of view and a general deadening of intellectual life.” Yet, McClay cautions, it will not be enough to instill in higher education “a robust recommitment to one of America’s fundamental values: free speech.” Universities must do more than relearn how to serve as “a community of inquiry.” They must also regain the capacity to form “a community of shared memory, the chief instrument by which the achievements of the past are transmitted to the present as a body of knowledge upon which future knowledge can be built.”

The blight of ideologically driven scholarship and teaching extends well beyond the humanities, argues City Journal contributing editor John Tierney in DEI v. Science. The diversity, equity, and inclusion industry has turned the social sciences into “political monocultures.” The Society for Personality and Social Psychology (SPSP), for example, weaves a requirement for ideological conformity into its determination of worthy scholarship: “Since 2022, it has evaluated papers submitted for presentation at its annual convention by asking each researcher to explain how the work ‘advances the diversity, equity, inclusion, and anti-racism goals of SPSP.’” Meanwhile, “even the hard sciences have been politicized by demands to meet diversity quotas and to ‘decolonize’ physics and mathematics by introducing ‘indigenous perspectives.’” In biology, chemistry, and physics, writes Tierney, “younger professors, administrators, and journal editors are more likely to champion the diversity, equity, and inclusion (DEI) regime: they value ethnic and gender diversity over originality and productivity, and they are far more eager to silence and punish scientists daring to challenge progressive orthodoxy.”

In “Demystify the Ivies,” Manhattan Institute senior fellow Allison Schrager stresses the difficulty of reforming universities where “some academic departments are overrun with true believers, and university staff is dominated by administrators who will resist any change.” However, this “disgraceful spectacle” – made vivid by the “anti-Israel (and often anti-American) frenzies” that “seemed tolerated, if not supported, by university administrations and even encouraged by some faculty” – presents an opportunity. “A loss of trust and stature could be just what our elite universities need in order to fix themselves,” Schrager argues. “The recent campus tumults thus might be the best thing for these universities in the long run. If a degree from a great state school like Texas A&M is seen as no less valuable than one from an Ivy League university, then America’s top colleges might finally get out of the elite-minting business and return to their original mission of education and research.”

Furthermore, it is wrong to suppose that “college is a surefire ticket to a better life,” argues Foundation for Research on Equal Opportunity senior fellow Preston Cooper. Yes, “college can be a path to upward mobility,” Cooper writes in “Is College Still Worth It?,” but “plenty of four-year college pathways aren’t, and some even leave students worse off.” As economic realities sink in, undergraduate enrollments will continue to drop.

“Accreditation is a problem that gets comparatively little attention, even as it slowly erodes the foundations of higher education,” contends Cato Institute research fellow Andrew Gillen in “Accreditation is Broken; Can it be Fixed?” University accreditors are drawn from faculty elsewhere. According to Gillen, they largely accept universities’ definition of quality – which tends to focus on inputs and process rather than learning and reasoning – and determine how well universities live up to their formal standard. To make matter worse, accreditors’ knowledge that they and their institutions will be reviewed by colleagues from the universities that they review compromises their independence. In addition, accreditors increase costs, since colleges and universities are, on pain of losing federal funding, compelled to adopt their recommendations, which typically push a progressive agenda. Gillen envisages no easy way out, but he sees promise in promoting competition through the establishment of alternative accreditation organizations.

In “Make Schools Bear Some of the Risk of Student Loans,” Manhattan Institute legal policy fellow Tim Rosenberg argues that the federal government should rein in reckless spending on costly undergraduate education that leaves students ill-equipped for the workplace. Washington could do this by “making student-debt indemnification a feature of school accreditation.” Rosenberg also wants the federal government to “require that all universities guarantee the most recent ten years of student aid (loans and Pell Grants) received by the institutions.”

Other efforts are more ambitious. In the “The Difficult Work of Academic Reform,” Manhattan Institute senior fellow Christopher Rufo explains the transformation of New College of Florida in Sarasota. Appointing a new slate of trustees in Jan. 2023 – including Rufo – Gov. Ron DeSantis has sought to turn the “left-wing activist haven” into a center of liberal education. And Joe Lonsdale, managing partner at venture capital firm 8VC, highlights the admirable purpose of the University of Austin, which he co-founded in 2021. In “Building a New University on Firm Foundations,” Lonsdale directs attention to UATX’s constitution, which establishes “an institution of higher learning that champions the pursuit of truth, scientific inquiry, freedom of conscience, and civil discourse, and that is independent of government, party, religious denomination and business interest.”

The degradation of liberal education harms multifarious aspects of America’s well-being. It erodes elites’ understanding of their rights and responsibilities, impairs their performance of their professional tasks, and constricts their minds and hearts. Reform can’t wait and must proceed simultaneously on many fronts.

Peter Berkowitz is the Tad and Dianne Taube senior fellow at the Hoover Institution, Stanford University. From 2019 to 2021, he served as director of the Policy Planning Staff at the U.S. State Department. His writings are posted at PeterBerkowitz.com and he can be followed on Twitter @BerkowitzPeter.

{kind=link}

{kind=link}