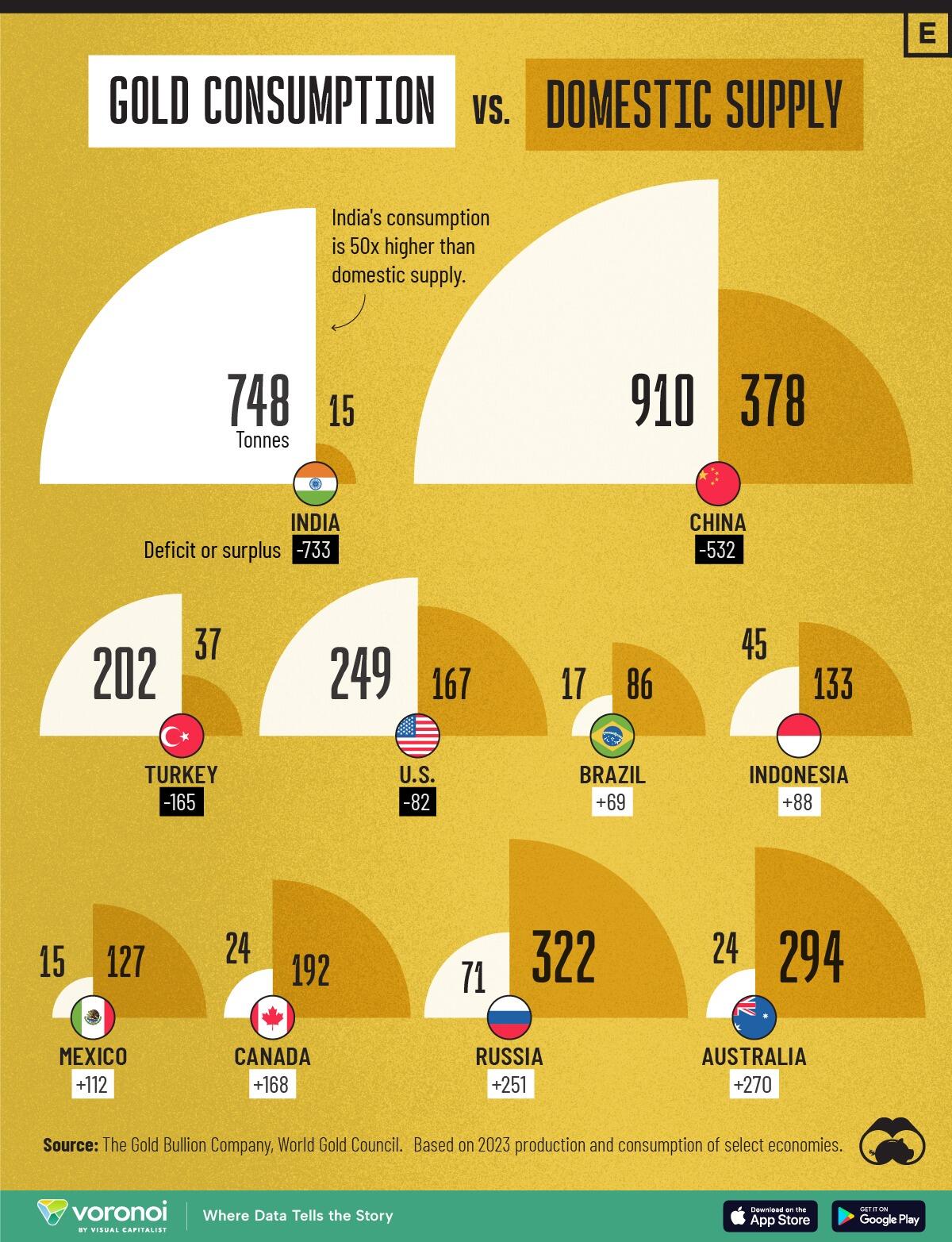

While India and China dominate the demand for gold, both countries face different scenarios when comparing supply gaps.

With its huge jewelry industry, India’s consumption is 50 times higher than its domestic supply. Meanwhile, China produces more than one-third of the gold it demands.

Gold holds a central role in India’s culture, considered a store of value, a symbol of wealth and status, and a fundamental part of many rituals. The metal is especially auspicious in Hindu and Jain cultures.

With a population of over a billion, India tops our ranking with substantial gold demand, primarily for jewelry and gold bars.

China ranks second, with demand driven primarily by gold’s role as a store of value, especially by the People’s Bank of China. Central banks seek gold as a hedge against inflation and currency devaluation. Since 2022, the People’s Bank of China has increased its gold reserves by 316 tonnes.

In third place for gold demand, the U.S. consumed 249 tonnes in 2023, against a domestic supply of 167 tonnes.

Turkey ranks fourth, with mine production in 2023 at 37 tonnes, which is five times lower than its demand of 202 tonnes.

To learn more about gold, check out this graphic that shows the value of gold bars in various sizes (as of Aug. 21, 2024).

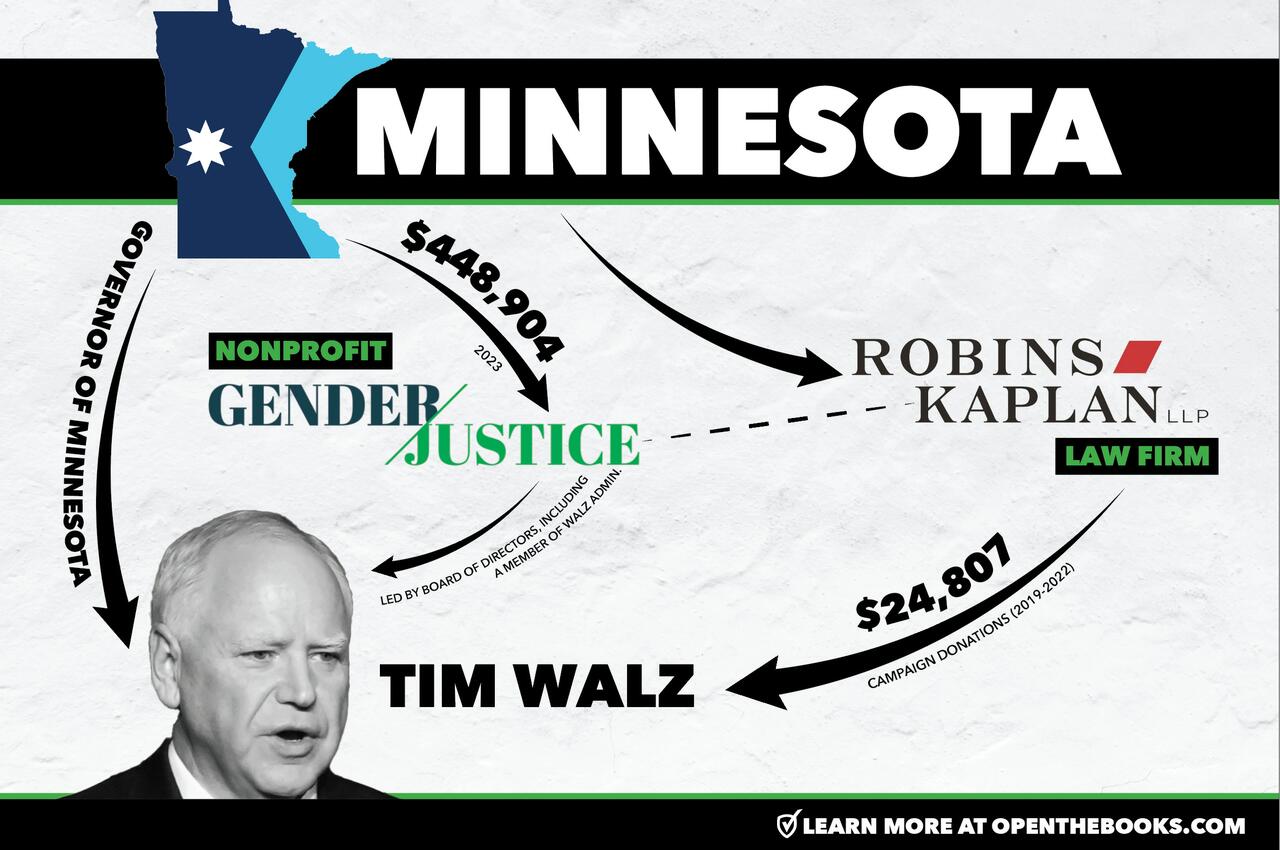

Earlier this month, we took a deep dive into Minnesota’s state checkbook. Unlike the state budget, a broad plan to allocate funds, the checkbook contains every line-by-line expenditure the state makes in a given year. By comparing the paid vendors with those who donated to Governor Tim Walz’s reelection campaign, we found interesting examples of overlap but not enough information to identify confirmed conflicts of interest.

One particular headline-making case, though, begged a closer look. It demonstrates how policy can change without the taxpayers having much say in the matter.

By suing the state, a constellation of interests was able to negotiate a deal behind closed doors on the controversial topic of treating and housing transgender inmates. While taxpayers foot the bill, as always, their representatives in St. Paul were sidestepped in the policymaking process.

The bill came to $495,000, but updated policies mean Minnesotans can expect more costs in perpetuity.

THE PLAINTIFF

Christina Lusk was an inmate at the Minnesota Correctional Facility-Moose Lake and identified as a transgender woman. Lusk had been working for several years to get access to what advocates call “gender-affirming” care. She wanted Gender Affirming Hormone Therapy (GAHT), assessment for and access to gender reassignment surgery, and a transfer to a women’s prison.

She was also seeking damages, bringing a suit under the Minnesota Human Rights Act, provisions of which have already been the subject of media controversy this year.

HELP FROM A CONNECTED NONPROFIT

Gender Justice is a nonprofit headquartered in St. Paul, Minn., focused on so-called “gender equity.” With policy education, advocacy and legal services arms, the organization lists among its mission “dismantling” legal structures that prevent equity. The group seeks to “create a world where everyone can thrive no matter their gender identity, expression, or sexual orientation. Central to this work is dismantling the legal, political and structural barriers to gender equity.”

The group is led by a Board of Directors that includes a member of the Walz administration. Gender Justice Board Treasurer EJ Dean, according to the website, also serves as Manager of Adult Mental Health Programs & Services at the MN Department of Human Services. In other words, Dean works as part of Governor Walz’s administration.

They have also served on the City of Minneapolis Transgender Equity Council. Per their own bio, Dean has “held multiple leadership roles at the intersections of mental health, human services and queer equity.” (Dean uses they/them pronouns according to the website).

Gender Justice collected $448,904 from the state in 2023 alone, much of it pursuant to Lusk’s suit. An additional $5,000 came from the Office of Higher Education for an unrelated matter.

SIDENOTE: Gender Justice is also favored by the Biden-Harris administration, having accepted an invitation to the 2024 Pride Month Celebration on the South Lawn of the White House.

Gender Justice extended their legal services to Lusk, part of work they call “impact litigation.”

BACKGROUND: Harvard Law School defines impact litigation as “planning, preparing, or filing and defending laws suits focused on changing laws or on the rights of specific groups of people. Impact litigation is brought or defended typically when the case affects more than one individual even if there is one individual involved. Many impact litigation organizations are also deeply involved in policy work.”

Lusk sued the Minnesota Department of Corrections, and Gender Justice partnered on the litigation with Robins Kaplan LLP. The firm is headquartered in Minneapolis but has offices across the country including in New York, Los Angeles, Silicon Valley, Boston and Bismarck.

Robins Kaplan employees donated $24,807 to the Walz gubernatorial re-election campaign (donations from 2019-2022), including a donation from chair emeritus Elliot S. Kaplan.

CLOSED-DOOR NEGOTIATIONS

After entering arbitration, the Department of Corrections settled with Lusk for a total of $495,000 in damages, split among the three parties.

Settlement By the Numbers

Christina Lusk: $245,903.72 in damages Gender Justice: $198,000 in legal fees and costs Robins Kaplan LLP: $51,096.28 in legal fees and costs

Beyond just financial damages, the Department of Corrections agreed to give Lusk what she was demanding. She received access to hormone therapy and would have a professional evaluate the need for gender reassignment surgery.

Under the arrangement, Lusk would be moved to women’s-only Shakopee prison. The deadline to do so would be a week after completing a chemical dependency program, but finishing wasn’t a requirement: Lusk could send a written request to move sooner.

THE FINE PRINT: You can read the full settlement agreement stemming from Christina Lusk v. Minnesota Department of Corrections, obtained by OpenTheBooks, here.

Equally concerning for taxpayers, the World Professional Association for Transgender Health (WPATH) Standards of Care are referred to as a North Star for Lusk’s regimen and state policy going forward. WPATH has received intense scrutiny after independent journalist Michael Shellenberger released leaked internal files detailing private discussions among doctors, and Environmental Progress’ Mia Long released a long-from follow-up report. The documents and meetings depict WPATH members acknowledging the difficulty of minors giving informed consent to surgical and hormonal interventions, and brainstorming fixes to complications. (Take a look at the Further Reading section for more).

Plus, if Lusk’s surgeries and the related treatments were not completed by her release date from prison (which happened last January), DOC would continue to reimburse her out-of-pocket expenses provided she gets health insurance.

POLICY AFTERMATH

Explicitly written into the legal settlement, the Minnesota DOC agreed to revise its policies as they apply to all transgender-identifying inmates.

First, they updated their policy called “Management and Placement of Incarcerated People Who Are Transgender, Gender Diverse, Intersex, or Nonbinary.” It now “expressly” states that DOC “provides medical care in accordance with WPATH” recommendations, and it explains the agency will give prompt responses to prisoner requests related to transgender care, using its “facility gender identity committees.”

Second, inmates who receive a legal name change at any time can request their prison records be updated to match it, “irrespective of the names under which they are committed to DOC custody.”

In a statement reported by NPR, Gender Justice Legal Director Jess Braverman said, “Thanks to Christina Lusk’s willingness to speak out, transgender people in custody will now have expanded access to the housing and health care they need, and the legal protections they deserve.”

Sister organization Gender Justice Action seeks to have a more direct impact shifting politics in Minnesota and surrounding states. According to its website:

“By mobilizing the majority of Minnesotans who support gender equity, we are building a grassroots movement to elect gender equity champions through targeted electoral strategies and pass policies to expand reproductive freedom and LGBTQ rights.”

They say they’re “advancing the boldest gender equity agenda in Minnesota history by pushing transformative legislation.”

CONCLUSION

It seems everybody did mighty well here — except for the taxpayers of Minnesota, who paid for the legal proceedings, underwrote the Gender Justice nonprofit and will ultimately fund controversial treatments for Lusk and many others.

The case study is reminiscent of a practice known at the federal level as “sue and settle,” which attracted scrutiny of the Environmental Protection Agency. The EPA would routinely settle claims from environmentalist nonprofits seeking stronger regulations. By making those deals in private, it cuts the taxpayer out of the conversation – including state governments and local business owners who have a stake in the outcome.

Likewise, in the Lusk case, taxpayers got off with only $495,000 – for now — but the policy change never had to survive a legislative debate. Those new practices and costs will continue unless lawmakers take new action.

“I Thank God”: Heroic Woman Saves Arkansas Trooper From Attack By Drunk Illegal Alien

The Biden-Harris administration’s disastrous open southern border policies have imported the third world into the first world, with dire consequences unfolding across the nation.

The latest example occurred in Arkansas, where Arkansas State Police released a trooper’s dash camera footage on Wednesday from an incident on July 27 that showed a drunk illegal alien speeding on the highway.

Benton County Prosecutor Joshua Robinson revealed that Trooper Alexandria Duncan’s use of deadly force was justified in Arkansas law after Angel Zapet-Alvarado, 26, of Guatemala, had a blood-alcohol level of twice the legal limit when he resisted arrest and assaulted the Trooper during a traffic stop on Interstate 49.

Arkansas State Police provided details about the violent encounter with the trooper and the migrant:

At approximately 7:43 p.m., Trooper Duncan attempted to stop Zapet-Alvarado on I-49 southbound after he passed her marked patrol unit traveling 114 miles an hour in heavy traffic near the 83-mile marker. Zapet-Alvarado initially showed no signs of stopping, even after Trooper Duncan activated her emergency lights and sirens. After stopping his vehicle on the right shoulder, Trooper Duncan instructed Zapet-Alvarado to exit the vehicle. Trooper Duncan observed Zapet-Alvarado with his hand on the gearshift and stopped him from driving away in the vehicle by taking his keys. He ignored commands to exit the vehicle and resisted Trooper Duncan’s efforts to remove him. She deployed her taser when he refused to comply. Zapet-Alvarado wrestled the Trooper’s taser from her hands and threw it into interstate traffic. During the incident, Zapet-Alvarado kicked Trooper Duncan’s head multiple times.

By the grace of God, a motorist, Kylie Sutton, 31, witnessed the altercation and assisted the trooper. Sutton was able to hand the trooper her service weapon, wounding Zapet-Alvarado in his right temple. The trooper then arrested the migrant.

“I thank God that He gave Alex the strength to survive that encounter, and that He put Kylie by her side when she needed support the most. I’m so proud of them both,” Col. Mike Hagar wrote in a statement.

X account Border Hawkfirst reported the incident. The account noted that Zapet-Alvarado is an illegal alien.

Arkansas: Heroic Motorist Rescues Female State Trooper Under Attack by Drunk Illegal Alien

An Arkansas woman is being hailed as a heroine after she stopped to aid an officer being attacked by an intoxicated illegal alien during a recent traffic stop that ended in a shooting,… pic.twitter.com/vDvTbuXVdh

“Zapet-Alvarado was hit with a slew of charges, along with an ICE detainer, and is currently being held at Benton County Sheriff’s Office Detention Center on $350,000 surety bond,” Border Hawk said.

Angel Zapet-Alvarado is being held on $350,000 surety bond at Benton County Sheriff’s Office Detention Center pic.twitter.com/3hxXM5nxRy

The big takeaway is that there will be many more incidents like this by illegal aliens because of the Biden-Harris’ disastrous open southern border policies that flooded the nation with millions of unvetted illegals.

Meanwhile, former San Diego Sector Border Patrol Chief Aaron Heitke dropped a bombshell this week in front of Congress, “I was told I could not release any information on this increase in SIAs [Special Interest Aliens (SIAs) — individuals with known or suspected ties to terrorism],” adding, “The administration was trying to convince the public there was no threat at the border.”

A federal judge has extended the restraining order blocking the Biden administration’s latest student loan forgiveness initiative, referred to in court filings as the “Third Mass Cancellation Rule.”

This extension follows allegations from a coalition of states claiming that the program is being implemented secretly without proper public notice or approval.

In the ongoing lawsuit led by Missouri against the Department of Education, U.S. District Judge Randal Hall ruled on Sept. 19 that there was “good cause” to prolong the temporary restraining order—which he initially issued earlier in the month—by an additional 14 days.

The extension follows a hearing where both sides presented arguments on competing motions—the plaintiffs seeking a preliminary injunction and the defendants pushing for the case’s dismissal.

Missouri Attorney General Andrew Bailey called the decision a “huge win” in a Sept. 18 social media post following the judge’s in-court decision, which was formalized in the order issued the following day.

In his written order, the judge explained that the extension allows the court time to thoroughly review the arguments presented in briefs and oral submissions before ruling on the broader motions.

The case stems from a lawsuit filed on Sept. 3 in the U.S. District Court for the Southern District of Georgia by seven states: Alabama, Arkansas, Florida, Georgia, Missouri, North Dakota, and Ohio.

The complaint names Education Secretary Miguel Cardona, the Department of Education, and President Joe Biden as defendants. The states allege that documents reveal Cardona is “unlawfully trying to mass cancel hundreds of billions of dollars” in student loans and has “quietly” instructed federal contractors to start the cancellation process as early as Sept. 7, potentially wiping out as much as $73 billion overnight, with further cancellations to follow.

The complaint further alleges that the real cost of the “Third Mass Cancellation Rule” program could reach $146.9 billion, adding to the $475 billion estimated cost of the Saving on a Valuable Education (SAVE) program that Cardona first proposed in August 2022.

“This is the third time the Secretary has unlawfully tried to mass cancel hundreds of billions of dollars in loans,“ the states’ complaint reads.

”Courts stopped him the first two times, when he tried to do so openly. So now he is trying to do so through cloak and dagger.”

The plaintiffs allege that Cardona’s third attempt at loan forgiveness is both the most aggressive and the least legally defensible.

Unlike prior attempts—such as with the SAVE plan, in which there was at least some transparency and litigation pauses—this latest move allegedly bypasses legal requirements, such as the 60-day notice rule, according to the complaint.

The Biden administration’s first attempt to cancel student loans was blocked when the U.S. Supreme Court ruled against using the Health and Economic Recovery Omnibus Emergency Solutions (HEROES) Act to authorize debt forgiveness.

The second attempt, related to the SAVE Plan, was halted by an Aug. 9 decision of the U.S. Court of Appeals for the Eighth Circuit, which the Supreme Court declined to overturn later in August.

The SAVE program aims to reduce monthly payments for millions of eligible borrowers based on their income levels and to accelerate student loan forgiveness. An estimated 8 million borrowers signed up for the program. Under SAVE, borrowers with lower incomes could qualify for significantly reduced or even zero monthly payments, while accrued interest on these loans would no longer be charged.

However, the Eighth Circuit found that Missouri and the other states challenging the program are likely to succeed in their claim that the SAVE plan violates the major questions doctrine. This legal principle requires courts to assume that government agencies cannot make significant policy decisions—especially those with far-reaching economic impacts—without clear authorization from Congress.

As a result, the Eighth Circuit issued a temporary, nationwide injunction that halts the federal government’s ability to forgive student loan principal or interest under the SAVE plan. The injunction also suspends the provisions that prevent interest from accruing on loans and those that allow borrowers to make reduced or zero payments based on their income.

The Supreme Court declined to reinstate the SAVE plan, leaving the case to proceed in the lower court, where the case remains pending. Most recently, on Sept. 10, the court granted the solicitor general of Missouri more time to file briefs in the case.

The Department of Education did not respond to The Epoch Times’ request for comment by publication time.

Woke Panic: Civil Rights Groups Demand That Corporations Stop Cutting DEI Programs

The invasion of woke ideology and Diversity, Equity and Inclusion (DEI) policies into every facet of American life seemed to happen out of the blue starting in 2015-2016, but in reality the agenda had been quietly and insidiously slithering into western institutions for decades prior.

Establishment controlled NGOs like the Ford Foundation, the Rockefeller Foundation and George Soros’ Open Society Foundation had been pumping billions of dollars into US universities since at least the 1960s, launching social justice programs and placing propagandists into teaching positions with the intent of “manufacturing consent” as Noam Chomsky once dubbed it.

The effort was to control the thinking of a top percentage of American professionals, turn them into rabid adherents of Cultural Marxism and globalism and then send them out into the world to create a progressive trickle-down effect in every major corporate and political institution. In other words, the establishment believed that if they could dominate the professional class with their suits and lab coats and specialized degrees the rest of the public would blindly follow along due to “expert bias.”.

As it turns out, they were wrong.

It took almost ten years to root out this tiny contingent of cult manipulators, but today the woke movement is well and thoroughly exposed. Woke organizations and DEI departments are now in fast decline and even the activists are beginning to admit they’re losing the battle for the minds of the masses. Let’s not forget, only a few years ago the political left denied the DEI agenda even existed and called anyone talking about it a “conspiracy theorist.”

Big Tech companies like Meta and Google made cuts to DEI staffers and resource officers in 2023. Dozens of major corporations are completely dropping their DEI initiatives in 2024. The Hollywood Reporter recently published an article lamenting the fall of DEI in Hollywood, spotlighting a list of DEI producers in an effort to assert that leftist activists still have power in Tinsel Town despite their failing ideology. Gay activist group GLAAD has complained that “LGBT representation” has started to decline in popular entertainment, with only 27% of films and television promoting gay and trans characters (given these people make up less than 3% of the global population, this level of representation is still far too high).

The reason for this precipitous collapse of DEI programs is three-fold:

First, after central banks hiked interest rates and ended QE programs the floodgates of ESG money closed and dried up. Venture capital disappeared and woke companies then had to rely on pure profits to stay afloat.

Second, the mass boycotting of woke companies proved beyond a doubt that there is no market for products that cater to DEI. For many years we have been told that woke is the majority, and anti-woke is a fringe minority. The truth is the exact opposite.

Third, lawsuits over DEI hiring programs are forcing companies to admit there is an element of ant-white and anti-straight prejudice involved in their employment practices. They are beginning to fear the backlash in civil courts, not to mention, hiring poorly qualified employees simply to check diversity boxes is a recipe for financial disaster.

There’s a good reason why the corporate media loses their minds every time there’s a successful boycott of a product like Bud Light or a progressive series like Star Wars: The Acolyte – Each time this happens the event stands as proof that the political left is a paper tiger, a tiny minority with no power or influence beyond their ties to corporations and governments. They are an astroturf movement created by psychopathic billionaires and politicians.

Consumers and the free market have spoken – They don’t like DEI and will not buy DEI products. But leftists insist the public is being “misled” by the right wing. The only way they can keep the farce going is to continue to maintain DEI programs across the board despite public refusal to participate. If corporate programs start to shut down then the entire facade is shattered. DEI finally dies.

This is probably the motivation behind a recent push by the NAACP, the National Organization for Woman and other “civil rights” activist organizations to pressure companies to keep DEI departments in place. At least 19 of these groups penned and published an open letter to corporate leaders of Fortune 1000 companies demanding that they stop cutting woke programs.

The groups claim that “companies that abandon their DEI programs are shirking their fiduciary responsibility to employees, consumers and shareholders.”

Their statement reads:

“Diversity, equity and inclusion programs, policies, and practices make business-sense and they’re broadly popular among the public, consumers, and employees…But a small, well-funded, and extreme group of right-wing activists is attempting to pressure companies into abandoning their DEI programs…”

Leftists always gaslight by accusing their political opponents of engaging in the same kind of sabotage they engage in all the time. In fact, these businesses only have a duty to their shareholders, and their shareholders are tired of losing money. The “corporate citizen” narrative is not going to fly anymore in 2024.

If there was a market for DEI then it wouldn’t matter if conservatives were boycotting these companies. If woke activists were anything other than an insignificant portion of the population then they would be buying up woke products like crazy and proving conservatives wrong. But, they don’t because they can’t.

In their letter, the civil rights organizations, which also included UnidosUS, the Urban League, Advocates for Trans Equality, the National Women’s Law Center and the American Association of People with Disabilities, said divesting from DEI would alienate a wide range of consumers. Again, the opposite is true. DEI propaganda and hiring practices have greatly degraded company performance, product quality and they have politicized consumer markets in a way that has angered Americans. Get woke, go broke.

It would be brand suicide to continue on this path, which is why so many companies are finally backing away. However, is it too late? Did corporations flirt with leftist ideology for too long and lose their customers forever? Only time will tell.

Two assassination attempts against former President Donald Trump have not clarified the Democratic position on whether that Republican represents an existential threat to democracy. The White House still calls him a threat. Vice President Kamala Harris, meanwhile, has mostly discarded that talking point.

Trump wants it to stop either way. At least, when directed towards him.

“It is time to stop the lies, stop the hoaxes, stop the smears, stop the lawfare or the fake lawsuits against me, and stop claiming your opponents will turn America into a dictatorship. Give me a break,” the Republican nominee said at a Wednesday rally in New York.

“Because the fact is that I’m not a threat to democracy,” he continued, before turning around and using the rhetoric he just condemned against his opponents. “They are.”

This was a sudden change, as Harris was in the habit of denouncing Trump as “a threat to our democracy.” She used that exact phrase numerous times while Biden was still on the ticket, most recently on July 13, which was coincidentally the day of the first assassination attempt.

It took Gov. Tim Walz a little longer. While he won national headlines for branding Republicans “weird,” the Minnesota Democrat also called Trump and his running mate, Ohio Sen. J.D. Vance, “fascists.”

“Are they a threat to democracy? Yes. Are they going to take our rights away? Yes. Are they going to put people’s lives in danger? Yes. Are they going to endanger the planet by not dealing with climate change? Yes,” Walz said at a press conference two weeks after the first attack on Trump.

All the same, the change has been complete. And since joining the ticket, Walz has followed the lead of Harris. During the ABC News debate, for instance, she pointed to the Jan. 6 riot, and she took Trump’s “bloodbath” comment out of context. The vice president did not, however, repeat claims that Biden first popularized by saying that democracy itself would end under a second Trump term.

The problem for Harris: The Democrats working the hardest to put her in the Oval Office still argue that Trump could end democracy itself.

Biden explained at the Democratic National Convention that he was leaving the ticket because “that threat is still very much alive.”

He loved the job, the outgoing president said on stage, before adding, “I love my country more, and we need to preserve our democracy.”

Sitting in the crowd, Harris beamed.

The remarks came little more than one month after the first attempt on Trump’s life.

The second assassination attempt, this one in Florida last week and thwarted by the Secret Service before the shooter could open fire, did not change White House rhetoric.

When pressed on whether it was appropriate to still describe Trump as a threat, an exasperated Karine Jean-Pierre said the administration was “not just saying that to say it.” Instead, the Biden spokeswoman replied, they were “using examples,” namely the Jan. 6 attack on the U.S. Capitol which she referenced more than a dozen times Tuesday.

Insinuating that Biden had fanned the flames with his rhetoric, an assertion held by Trump and nearly every elected Republican, she said was “dangerous.”

The press secretary repeatedly pointed out that “the president and the vice president have always forcefully condemned violence in all forms, including political violence.”

And the condemnation of violence has indeed been universal. The switch from the old “threat to democracy” framework, however, has not. While Harris has turned the page on calling Trump a threat, Democratic allies are following Biden’s lead, not hers.

During a Thursday interview on MSNBC’s “Morning Joe,” former Secretary of State Hillary Clinton returned easily and quickly to existential rhetoric.

“At the end of the day, this is a contest between freedom and oppression, between democracy and autocracy, between bringing people together and further dividing us,” said Clinton, who hit similar themes at the Democratic convention.

That exact message – one Harris has shied away from delivering – Clinton continued, “has to be communicated every single day between now and the election.”

Bank Deposits & Money-Market Funds See Sizable Outflows As Stocks Surge

For the first time in seven weeks, money market funds saw net outflows last week (-$20BN) – the largest weekly outflow since June…

Source: Bloomberg

The outflow was dominated by a major institutional drawdown (-$25BN) as Retail funds saw inflows yet again…

Source: Bloomberg

US Bank Deposits (seasonally-adjusted) also saw outflows in the week ending 09/11 (-$9.3BN), the first weekly outflow in five weeks…

Source: Bloomberg

On a non-seasonally-adjusted basis, US Bank Deposits also fell (-$15BN), backing off from April highs…

Source: Bloomberg

Excluding foreign deposits, domestic banks saw outflows (both SA -$34BN and NSA -$41BN) in the week ending 9/11 (before The Fed rate-cut), with Large Banks dominating the outflows (SA -$24BN and NSA -$32BN)…

Source: Bloomberg

On the other side of the ledger, loan volumes increased despite the deposit shrinkage with Small bank loans rising $4.1BN and Large bank loans rising $1.2BN…

Source: Bloomberg

Finally, US equity market capitalization surged back up towards all-time highs this week (after The Fed unleashed hell with a 50bps cut)…

Source: Bloomberg

…meanwhile, bank reserves at The Fed suggest stocks could be significantly lower.

Intel Shares Soar On Report Of Qualcomm Takeover Interest

Intel shares surged 6% in late afternoon trading (now halted) after a Wall Street Journal report revealed that Qualcomm had approached the struggling chipmaker earlier this week to discuss a potential acquisition.

Here’s more from WSJ’s reporting, citing people familiar with the talks:

A deal is far from certain, the people cautioned. Even if Intel is receptive, a deal of that size is all but certain to attract antitrust scrutiny, though it is also possible it could be seen as an opportunity to strengthen the country’s competitive edge in chips. To get the deal done, could intend to sell assets or parts of Intel to other buyers.

Five days ago, Intel CEO Patrick Gelsinger was citing bible verses. Now, investors are saying ‘hallelujah’ to end the week following the WSJ report.

“And when he had opened the fourth seal, I heard the voice of the fourth beast say, Come and see. And I looked, and behold a pale horse: and his name that sat on him was Death, and Hell followed with him.” Revelation 6:7 https://t.co/MxEE6P2YJq

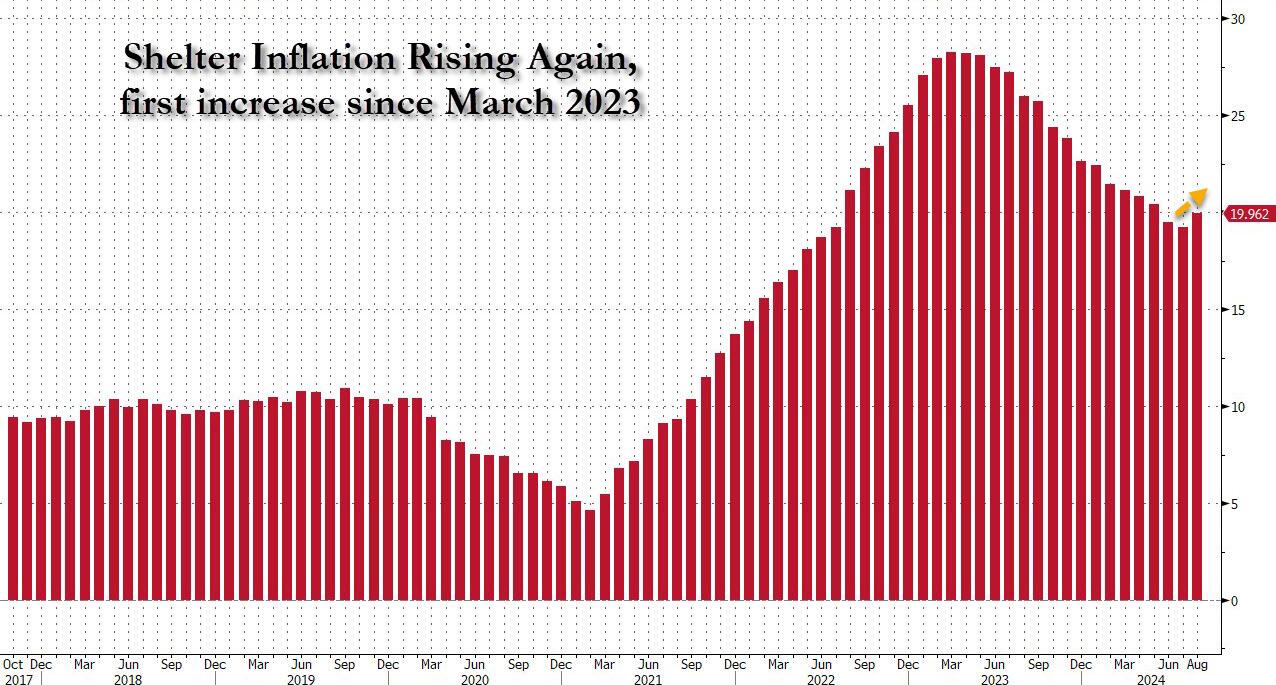

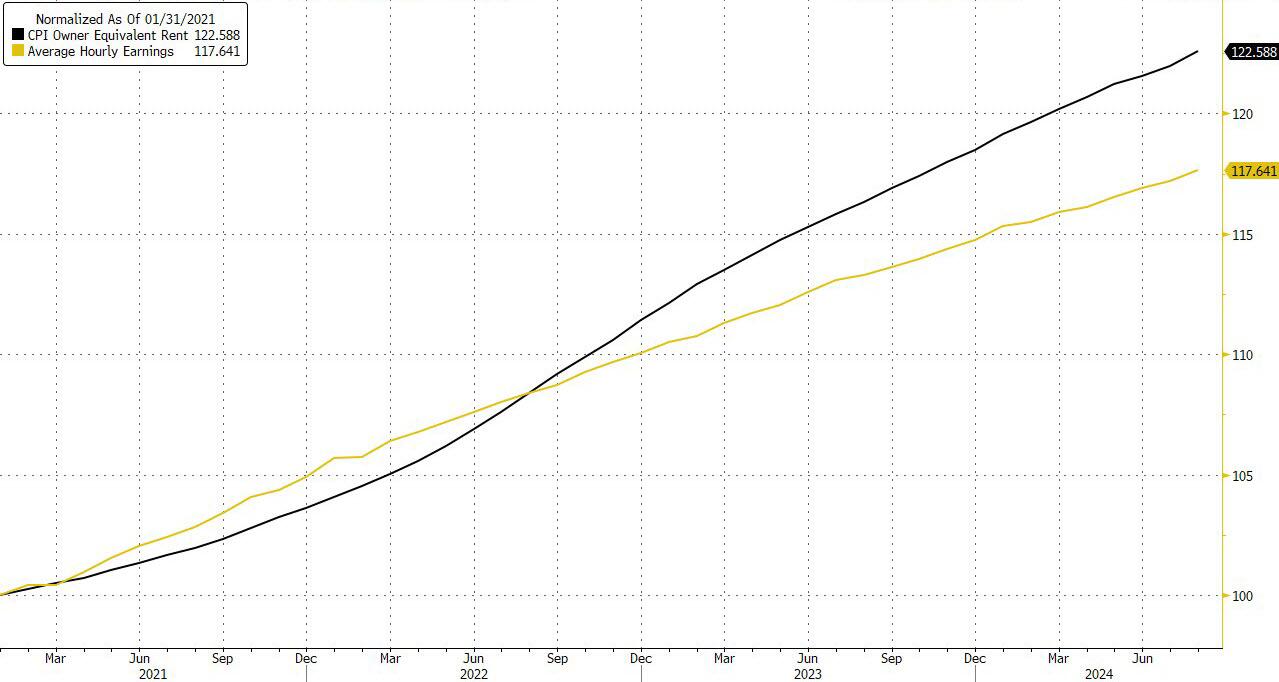

Swing State Renters Earn 17% Less Than Needed To Afford A Typical Apartment

With shelter costs once again rising year over year for the first time since last March…

… our prediction that by the time housing CPI – which is lagged by as much as 18 months – catches up with “today”, real rents will be rising by double digits, thanks to the Fed’s rate cut.

The next paradox for the Fed: since Shelter/OER inflation lags by 18 months, housing inflation will decline well into 2025 even as actual rents are again starting to tick up.

By the time lagged CPI catches up with “today”, real rents will be rising double digits. pic.twitter.com/sHOWxN2OVQ

And while the countdown to double digit rent inflation officially began on Wednesday when the Fed cut rates by a jumbo 50bps, the first rate cut since March 2020, we now get to sit back and watch the public’s delighted response – especially vis-a-vis the November election – to the Fed launching an easing cycle with record high home prices and rents,

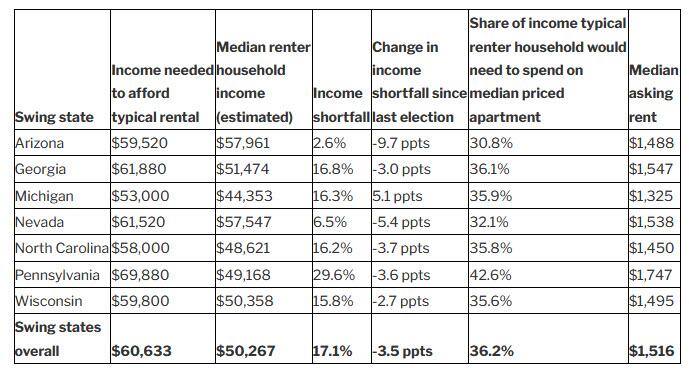

Case in point: according to real estate brokerage Redfin, the typical renter household in a swing state earns an estimated $50,267 per yea, $10,365 less than the $60,633 a renter must earn to afford rent for the median priced apartment in a swing state.

In other words, the typical swing state renter household earns 17.1% less than they need to afford the typical apartment. That’s a staggering shortfall, and one that will only grow now that Owner Equivalent Rent is once again starting to rise.

Redfin’s report focuses on swing states because voters in those states will decide the winner of the 2024 presidential election, and housing affordability – or lack thereof – is a crucial issue on voters’ minds. Redfin considers this year’s swing states to be Arizona, Nevada, Wisconsin, Michigan, Pennsylvania, Georgia and North Carolina. Indeed, as we said two months ago, this election will be decide not by not immigration, not crime, not equity, not abortion, not climate change, not guns, but just by one thing: inflation.

Only inflation matters: not immigration, not crime, not equity, not abortion, not climate change, not guns pic.twitter.com/eOQOyDE2zW

Rental affordability in swing states has deteriorated as income growth has failed to keep up with rising rents. The $50,267 estimated median renter household income in swing states is up doublt digits from the last election seasons but nowhere near enough to keep up with the national or growth in rent. Meanwhile, asking rents in swing states are flat from a year ago, but are up 23.8% from the last election cycle, and many renters struggle to afford their monthly housing costs.

The typical renter household in Arizona earns an estimated $57,961 per year—just 2.6% shy of the $59,520 they need to afford the median priced apartment. The second largest improvement was in Nevada, where the typical income shortfall is 6.5%. Next came Wisconsin, North Carolina, Georgia and Pennsylvania, perhaps the most important swing state of all: there, the income shortfall is a staggering 29.6%!

The typical renter household in Pennsylvania earns an estimated $49,168 per year. That’s 29.6% less than a renter must earn to afford the median priced Pennsylvania apartment—the biggest shortfall of any swing state by far. This is because Pennsylvania has a higher median asking rent ($1,747) than any other swing state. The typical renter household in Pennsylvania would now need to spend 42.6% of their income to rent the median priced apartment—a higher share than any other swing state, though down from both a year ago and the prior election.

“America’s swing state voters will decide the outcome of the next presidential election based on the candidates’ plans for tackling key issues including the housing affordability crisis,” said Redfin Chief Economist Daryl Fairweather. “While the economy has been improving on paper, that’s not what it feels like for a lot of U.S. families. Many renters—especially young people—still feel the rent is too damn high.”

The typical swing state renter is “rent burdened”—meaning they spend more than 30% of their income on housing—but less so than before. A swing state renter making the median income would now need to spend 36.2% of their income to rent the median priced apartment, down from 38.5% last year and 37.8% during the prior election cycle.

The Georgia Election Board has approved a new rule requiring election workers to hand count ballots in the November election and confirm that the numbers match machine counts before the vote can be certified.

The rule, which was first proposed in August, passed in a 3–2 vote on the morning of Sept. 20, making Georgia the only state in the union to adopt such a requirement as part of its standard vote-counting.

The new hand-count regulation was, at the time of reporting, the first of 11 that the board was set to vote on Friday. The others include a proposal that absentee ballots be visually distinct from other types of ballots, and another that requires poll workers to record the number of ballots cast from in-person scanners and reconcile those numbers to ensure accurate reporting of votes.

Advocates have framed the proposed rules as common-sense measures to bolster election security. Supporters of the hand-count rule, specifically, have argued it would help increase public trust in the voting process.

Critics, such as the Georgia Association of Voter Registration and Election Officials (GAVREO), say the proposed rules are, on the whole, impractical, poorly written, and inefficient in achieving their intended goals.

“We respectfully ask that these proposed rules, and any other petitions for rulemaking, be tabled until 2025,” the group wrote in a Sept. 17 letter to the election board.

GAVREO also expressed specific concern about the new hand-count rule, arguing in the letter that it could cause delays and introduce errors.

“We continue to oppose the rules for the reasons we have previously stated including: the rule’s potential to delay results; set fatigued employees up for failure; and undermine the very confidence the rule’s author claims to seek,” the group wrote.

Chris Carr, Georgia’s Attorney General, issued a letter on Sept. 18 stating that the proposed rules may be inconsistent with existing laws.

“A review of the proposed rules reveals several issues including that several of the proposed rules, if passed, very likely exceed the Board’s statutory authority and in some instances appear to conflict with the statutes governing the conduct of elections,” he wrote. “Where such is the case, and as outlined below, the Board risks passing rules that may easily be challenged and determined to be invalid.”

The letter from Carr’s office addressed the hand-count rule, stating that the statutes referenced in support of the rule do not allow for hand-counting ballots at the precinct level before they are delivered to the election superintendent for official tabulation.

“Accordingly, these proposed rules are not tethered to any statute—and are, therefore, likely the precise type of impermissible legislation that agencies cannot do,” the letter states.

Georgia Secretary of State Brad Raffensperger has also expressed concern that last-minute rule changes could introduce confusion on election night.

“Activists seeking to impose last-minute changes in election procedures outside of the legislative process undermine voter confidence and burden election workers,” he said in a statement in mid-August.

At a rally in August in Atlanta, former President Donald Trump praised the three Republican members of the Georgia Election Board, calling them “pit bulls fighting for honesty, transparency and victory.”

The Epoch Times has reached out to the Georgia Election Board with a request for comment on the criticism of the hand-count rule and the other proposals.