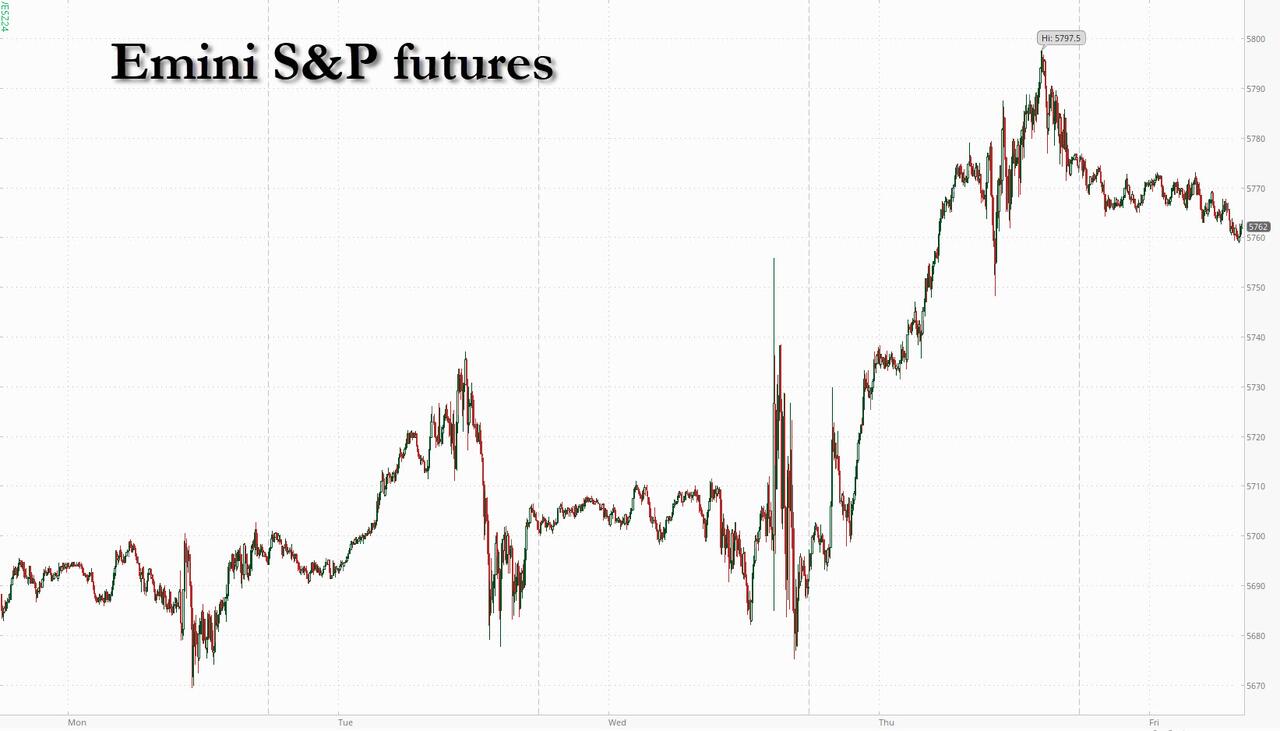

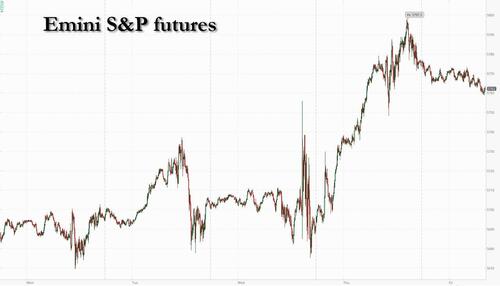

After yesterday’s delayed (and technically-driven) post-rate cut meltup, futures are set to close the week on a downbeat note as they slide across the board, following European stocks lower, but still just shy of the all time high they hit yesterday. As of 8:00am S&P futures are down 0.3% as disappointing earnings (FDX cratered -13% after missing and cutting guidance, dragging UPS -2.4% and logistics names lower) tempered the euphoria around the trajectory for interest rates; Nasdaq futures were down 0.4% with most MegaCap Tech names lower: TSLA (-3.6%) is the top mover, followed by META (-1.8%) and AAPL (-1.7%). The yen plunged more than 1% after the BOJ announced no hike to its policy rate, in line with expectation, and further signaled the gradualist approach to its rate hikes. USDJPY +0.8% to 143.8; NKY +1.5%. PBOC left loan prime rates unchanged. Throwing a potential wrench in what may have been a quiet end to the week is that today brings the ninth option expiry of 2024, and the last “quad witch” before the US election, where a record for September $4.5 trillion in notional will expire between now and 4pm ($2.6 trillion of this is SPX Sep regular / the remaining is split across etf and single stock at end of day) potentially triggering volatility, although market implied vol is low enough to rent delta in either direction. Yields are mostly higher, and USD is largely unchanged; 5-, 10-yr yields are 5bp, 10bp higher. Commodities are mixed with oil and metals higher, while ags are mostly lower. There is nothing on the macro calendar.

In premarket trading, FedEx plunged 14% after the parcel carrier lowed its annual outlook for adjusted earnings per share and revenue growth, while posting a worse-than-expected quarterly profit. Morgan Stanley downgraded the stock and warned Fedex could be facing structural risks. Nike shares rise 6.8% Friday after the company announced Elliott Hill will return to the company as CEO and president effective Oct. 14, replacing John Donahoe, who will retire. Analysts were positive about the announcement as Hill is an industry and company veteran. Here are some other notable premarket movers:

- Apellis Pharmaceuticals shares drop 7.5% after the drugmaker said a committee of the European Medicines Agency has upheld its negative opinion on the marketing authorization for the company’s eye drug, Syfovre.

- Assembly Biosciences shares rise 5.4% after Jefferies upgraded the stock to buy from hold ahead of data for the firm’s Herpes simplex virus (HSV) anti-viral drug.

- Snap shares edge lower, falling 1.2% as B Riley Securities initiated coverage on the social media company with a neutral recommendation. Analyst Naved Khan says the stock is trading at a premium to its peers with a “full” valuation.

The Fed’s bld half-point rate cut this week boosted confidence that it will be able to engineer a soft landing, but warnings such as the one from FedEx underscore lingering risks to the economy. Fed policymakers have projected a further half point of reductions this year.

“For all the optimism in markets right now, it’s clear that a few concerns still lie under the surface,” said Jim Reid, a strategist at Deutsche Bank AG. “In particular, futures are continuing to price in a more aggressive pace of cuts than was implied by the Fed’s dot plot on Wednesday, so investors think they might need to accelerate those rate cuts if downside risks materialize.”

For BofA’s resident bear, Michael Hartnett, the optimism in equity markets following the Fed’s move is stoking the risk of a bubble, making bonds and gold an attractive hedge against any recession or renewed inflation. In his latest Flow Show, he said stocks are now pricing in more Fed easing and about 18% earnings growth for the S&P 500 by end-2025. It doesn’t “get much better than that for risk, so investors are forced to chase” the rally, Hartnett wrote in a note. He also said stocks outside the US and commodities, especially gold, were a good way to play a possible soft economic landing, with the latter being an inflation hedge. And sure enough, gold just hit a fresh record above $2,600 an ounce as the Fed’s aggressive start to policy easing continued to ripple through markets.

Traders are also braced for the quarterly “quad witching,” when about $4.5 trillion in options and derivatives and futures are set to mature according to Goldman, making it the largest September expiry of all time. The options expiry coincides with the rebalancing of benchmark indexes. The event has a reputation for causing sudden price moves as contracts disappear and traders roll over their existing positions or start new ones (full preview here).

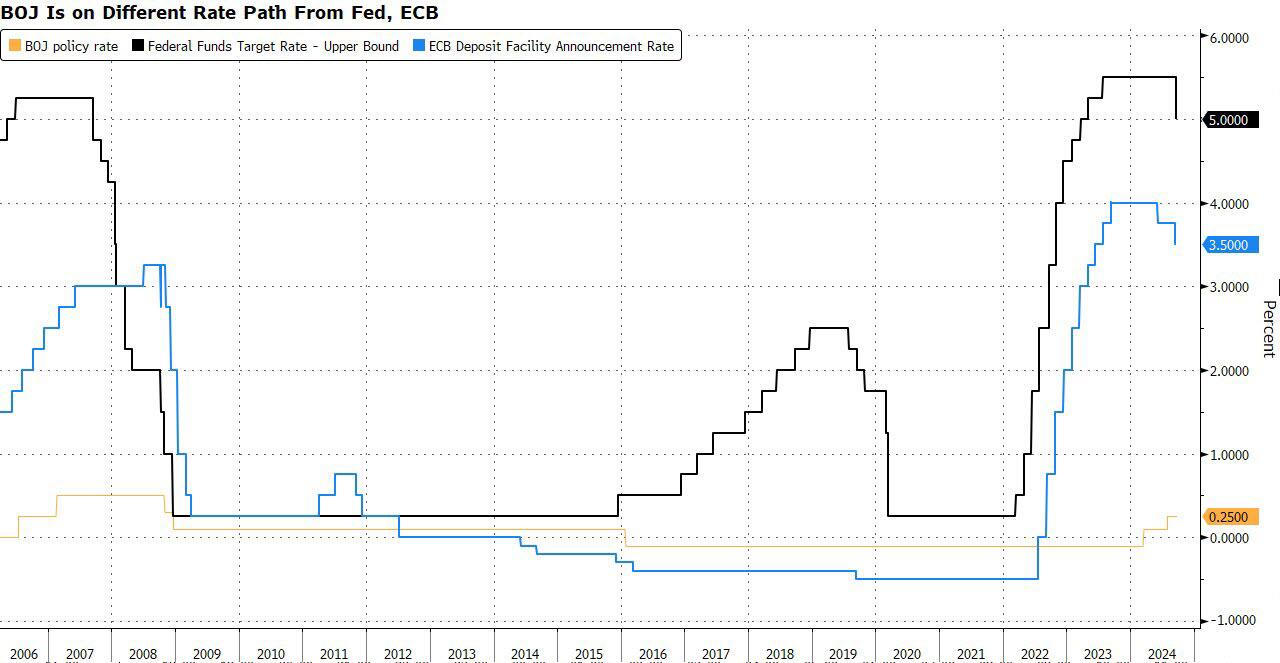

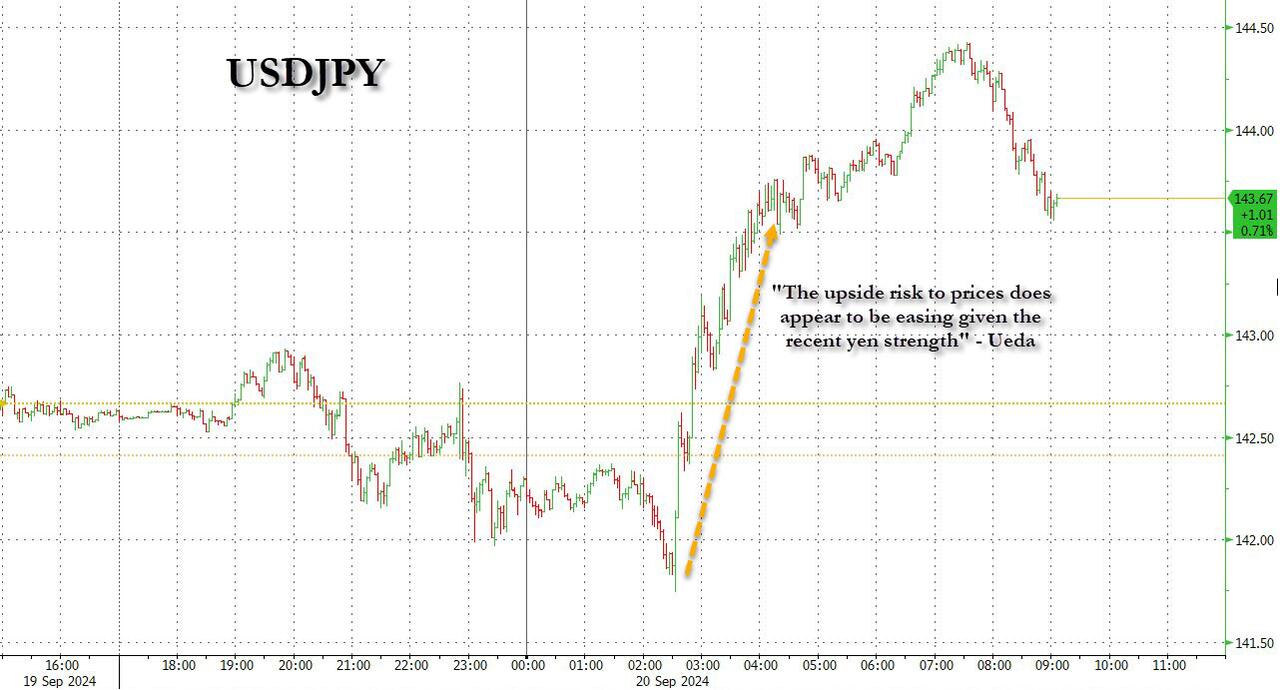

Elsewhere, the Bank of Japan was in focus as it kept policy unchanged, with the yen sliding 1.2% as Governor Kazuo Ueda proved less hawkish than some traders expected. Ueda signaled little urgency to hike rates, and said that upside risks to inflation are easing.

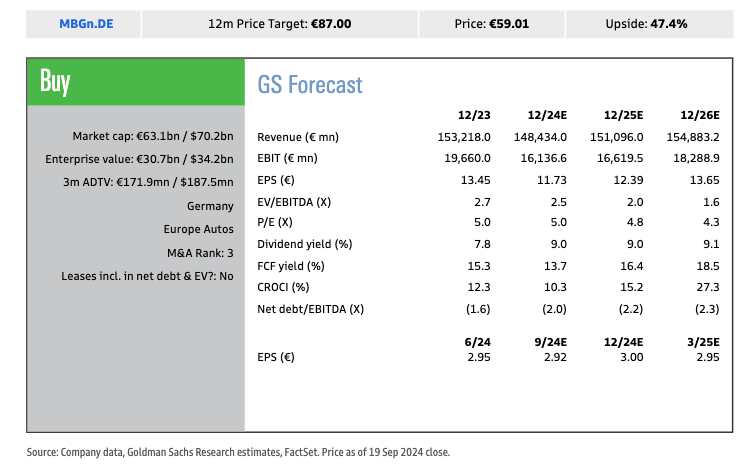

European stocks slumped, with the Estoxx 50 falling almost 1% as Mercedes-Benz Group tumbled as much as 8.4% after cutting its financial forecast because of sluggish China sales; besides autos, info tech and consumer discretionary sectors underperformed while utilities and telecommunications stocks are the biggest outperformers. Here are the biggest European movers:

- Mercedes shares fall as much as 8.4% to nearly a two-year low after the German carmaker cut its 2024 financial forecast in a profit warning that RBC called both surprising and ambiguous

- Atoss Software gains as much as 2.3% after Deutsche Bank initiated coverage of the German software firm with a buy recommendation, calling it a “leader” in the German-speaking workforce management market

- Card Factory advances as much as 8.3% and Moonpig +6.8% as UBS recommends buying shares of the UK-listed greetings-card retailers

- Volution Group shares rise as much as 12% to hit a record high after the maker of indoor air quality products agreed to buy the Fantech Group of companies for up to a total of AUD280 million

- ASML shares fall as much as 2.7% after Morgan Stanley downgraded the chip-equipment maker to equal-weight from overweight, seeing earnings growth at risk of uncertain demand from memory chipmakers, Intel and China

- Hexpol falls as much as 7.8%, the most sinceJanuary 2023, after Kepler Cheuvreux reiterated its hold rating ahead of the Swedish polymer and rubber firm’s 3Q report on Oct. 25

- JDE Peet’s shares fall as much as 8.3% after a shareholder sold about 3.5 million shares in the Dutch coffee maker at a discounted price of €19 per share, according to terms seen by Bloomberg

- Burberry falls as much as 5.1%, extending yearly losses to 58% and among the worst performers on the Stoxx 600, after Jefferies cut its recommendation on the firm to underperform in a bearish review on the sector, advising investor caution

- Dr. Martens shares slide as much as 18%, hitting a fresh record low, after an unnamed investor sells around 70 million shares via Goldman Sachs at a 9.8% discount versus Thursday’s close

Earlier in the session, Asian stocks set its best week in a month as the Federal Reserve’s larger-than-expected rate reduction and hopes of China’s stimulus rekindled appetite for riskier assets. The MSCI Asia Pacific Index rose 0.7% to a two-month high on Friday, taking this week’s advance to 2%. Most benchmarks gained with the Hang Seng China Enterprises Index up for a sixth session. Japanese shares held onto gains as the Bank of Japan kept its monetary policy steady, signaling it’s in no rush to raise interest rates. Financial markets across the region have been upbeat, with a gauge of the region’s currencies reaching a 16-month high this week. The Malaysian ringgit and the Indonesian rupiah have strengthened against the dollar this week.

In FX, the Bloomberg Dollar Spot Index traded in a narrow range against most of its other Group-of-10 peers and swung from losses to gains as the yen first gained then tumbled. And speaking of the yen, it plunged more than 1% after Governor Kazuo Ueda indicated the Bank of Japan isn’t in a hurry to increase interest rates again. The pound outperformed its peers after UK retail sales grew at a faster pace than expected

In rates, treasuries were cheaper across the curve and yields rose in a mild bear-flattening move that partially unwinds the steepening trend advanced by Wednesday’s half-point Fed rate cut. Front-end yields are cheaper by more than 2bp, narrowing 2s10s and 5s30s curve spreads; 10-year around 3.73% is less than 2bp cheaper on the day with bunds and gilts outperforming by 1bp and 2bp. Treasury coupon auctions ahead next week include 2-, 5- and 7-year note sales Tuesday, Wednesday and Thursday

In commodities, oil was on track for the biggest weekly advance since February. Gold hit a fresh record above $2,600 an ounce as the Fed’s aggressive start to policy easing continued to ripple through markets.

US economic data calendar is blank; Fed speaker slate includes Philadelphia Fed President Harker at 2pm as well as ECB President Lagarde.

Market Snapshot

- S&P 500 futures down 0.2% to 5,703.75

- STOXX Europe 600 down 0.7% to 518.09

- MXAP up 0.7% to 186.70

- MXAPJ up 0.7% to 583.56

- Nikkei up 1.5% to 37,723.91

- Topix up 1.0% to 2,642.35

- Hang Seng Index up 1.4% to 18,258.57

- Shanghai Composite little changed at 2,736.81

- Sensex up 0.9% to 83,965.54

- Australia S&P/ASX 200 up 0.2% to 8,209.47

- Kospi up 0.5% to 2,593.37

- German 10Y yield little changed at 2.18%

- Euro little changed at $1.1165

- Brent Futures down 0.5% to $74.49/bbl

- Gold spot up 0.9% to $2,610.23

- US Dollar Index little changed at 100.70

Top Overnight news

- Japan’s BOJ left rates unchanged, as was widely expected, but said the economy was progressing in a manner consistent with its expectations (the view on consumption was tweaked higher), reinforcing expectations that another hike could occur this year. Nikkei

- China disappoints markets by leaving its Loan Prime Rates unchanged (some felt the country’s weakening growth outlook, coupled with the Fed’s outsized move, would spur a reduction in the LPR). WSJ

- China is working on a proposal to remove home purchase restrictions as the gov’t scrambles to support an economy that continues to cool. BBG

- The European Central Bank’s rate cutting cycle could accelerate over coming months, governing council member Fabio Panetta said on Thursday. RTRS

- After months of saying a cease-fire and a hostage-release deal was close at hand, senior U.S. officials are now privately acknowledging they don’t expect Israel and Hamas to reach an agreement before the end of President Biden’s term. WSJ

- Port of New York/New Jersey executives have begun preparations for a potential complete work stoppage by the International Longshoreman’s Association which is the largest union in North America: CNBC

- Warren Buffett’s disposals of BofA shares have covered his investment cost of $14.6 billion, leaving him with a stake worth more than $34 billion that’s pure profit. Berkshire Hathaway sold about $900 million of the stock in the latest tranche. BBG

- OpenAI’s latest fundraising is nearing completion, with prospective investors set to find out Friday whether they’ll be part of the deal, according to people familiar with the matter. The $6.5 billion funding round for the artificial intelligence startup is oversubscribed, meaning investors were hoping to put in more money than the company was ready to take on. BBG

- Nike (+7% pre mkt) announced that Elliott Hill will become President and CEO, effective October 14, 2024. WSJ

- FedEx (-14% pre mkt) reported a miss on EPS, margins, and sales due to weak volumes and a mix shift to lower-priced products, and the full-year guidance was trimmed. RTRS

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly gained following the rally stateside where the S&P 500 and the Dow surged to fresh record highs as the dust settled after the Fed over-delivered in its first rate cut in four years and US data topped forecasts. ASX 200 followed suit to its US counterparts as tech led the advances and the index printed a new all-time high. Nikkei 225 outperformed again and approached closer to the 38,000 level, while the BoJ policy announcement provided no major fireworks in which the central bank kept its short-term rates unchanged at 0.25%, as unanimously forecast. Hang Seng and Shanghai Comp were mixed with the former joining in on the optimism in the region owing to the recent central bank activity and with EV makers finding some encouragement from recent China-EU EV tariff talks. Conversely, the mainland lagged despite the recent pledge by the NDRC to roll out a batch of incremental measures and reports that China is mulling removing major homebuying curbs, while the PBoC also announced China’s latest Loan Prime Rates which were unsurprisingly maintained at their current levels.

Top Asian news

- China weighs removing major homebuying curbs to boost demand and may end distinctions between first and second home purchases, while it may also ease restrictions on non-local homebuyers in Beijing and Shanghai, according to Bloomberg. People familiar with the matter also said authorities are mulling measures to shore up the sluggish stock market but didn’t provide specifics.

- China and EU both aim to resolve differences via consultations over the EU investigation into Chinese EVs, while China’s Commerce Minister and EU’s Trade Commissioner are to continue pushing forward negotiations on price commitments and the sides are to spare no effort to reach a mutually acceptable solution through dialogue, according to Xinhua. This followed a previous report that no deal was reached in EU-China talks on EV tariffs and EU’s Dombrovskis said both sides agreed to intensify efforts to find an effective, enforceable and WTO-compatible solution.

- USTR office said it will accept public comments from Monday on plans for steep tariff increases on Chinese polysilicon, silicon wafers and tungsten products, according to Reuters.

- Republican Senator Rubio is introducing a bill to prevent Chinese companies from benefiting from favourable US trade rules by operating in other countries.

- China’s NDRC will cut retail gasoline and diesel prices by CNH 365/ton and CNH 350/ton respectively, starting September 21, via Bloomberg

European bourses, Stoxx 600 (-0.6%) are entirely in the red, but to varying degrees; price action today has been fairly lacklustre, with indices generally slowly drifting lower as the morning progressed. European sectors hold a strong negative bias; Utilities takes the top spot alongside Telecoms. Autos is by far the clear underperformer, dragged down by Mercedes-Benz (-7.1%) after it cut guidance citing China weakness. Consumer Products and Tech also lag, with the latter hampered by ASML (-2%) after it was downgraded at Morgan Stanley.

Top European news

- ECB’s Rehn says they have progressed well towards the inflation target, easing pace is data-dependent.

- ECB’s de Guindos says they have left the door totally open and in December they will have more information than in October.

- BoE’s Mann says she agrees with investors who think inflation could stay above target for an extended period of time. It is better, under inflation uncertainty, to remain restrictive for longer, until right tail risks to the inflation process dissipate, and then to cut more aggressively. Has a guarded view on initiating a cutting cycle despite agreeing with the majority for a hold at the meeting just concluded. Policy needs to remain restrictive to purge inflationary behaviours. Risk of inflation expectations de-anchoring have subsdided. Did consider voting to cut rates in August but wanted to avoid a “boogie-dance” with policy rates.

BOJ Decision

- BoJ kept its short-term policy rate unchanged at 0.25%, as expected with the decision made by unanimous vote, while it said Japan’s economy is recovering moderately albeit with some weaknesses and inflation expectations are heightening moderately. BoJ also stated that inflation is likely to be at a level generally consistent with the BoJ’s price target in the second half of its 3-year projection period through fiscal 2026 and it sees medium and long-term inflation expectations increasing. Furthermore, it sees exchange rate trends as having a greater influence on prices and said Japan’s economy is likely to achieve growth above potential but also stated that they must be vigilant to the impact of financial and FX market moves on Japan’s economy and prices.

Ueda press conference

- Outlook for overseas economies, incl. the US and markets, remains unstable. When asked about remarks from Uchida, says markets remain unstable. Remarks which sparked USD/JPY upside.

- Upside price risks have decreased given recent FX moves; risks of an inflation overshoot have somewhat diminished.

- No change to the thinking that they will continue to lift rates if the economy develops as expected; will take the next policy step when there is enough evidence.

- Aware that more efforts are needed to change market expectations as policy rates have shifted in earnest to positive territory from zero or negative over long period.

- Need to watch to see if the US economy attains a soft landing, making a judgement on the US is difficult.

FX

- DXY is steady vs. peers (ex-JPY) in what has been an eventful week for the USD after the Fed delivered an outsized 50bps rate cut and sent DXY to a fresh YTD trough at 100.21.

- EUR is flat vs. the USD but in close proximity to recent highs. EUR/USD is sitting just below the WTD peak set on Wednesday at 1.1189 with focus on a test of 1.12.

- GBP is the marginal outperformer across the majors on account of better-than-expected UK retail sales and yesterday’s “hawkish hold” by the BoE which led markets to no longer fully price a 25bps reduction at the November meeting. Cable is off best levels, however, printed another multi-year high earlier in the session at 1.3340.

- JPY is the laggard across the majors, initially unreactive to the BoJ policy announcement, which kept rates unchanged. However, follow-up remarks from BoJ Governor Ueda gave the impression that the Bank was not in a rush to hike rates further as policymakers assess the impact of prior tightening. Accordingly, USD/JPY rose from a 141.75 base to a 143.75 peak but is yet to eclipse yesterday’s 143.94 peak.

- AUD/USD’s recent run of gains since Monday has paused for breath with the USD a touch firmer vs. AUD. NZD/USD is seeing uneventful trade with the pair contained within yesterday’s 0.6181-0.6268 band.

- PBoC set USD/CNY mid-point at 7.0644 vs exp. 7.0637 (prev. 7.0983).

- Chinese major state-owned banks are seen buying dollars in the onshore currency market to prevent the yuan from strengthening too fast, according to sources cited by Reuters.

Fixed Income

- USTs are slightly firmer with specifics light thus far for the US but with action coming from the BoJ; while the decision itself was largely uneventful the presser saw a particularly dovish Ueda. Thus far, USTs have probed but failed to breach 115-00 or, by extension, test yesterday’s 115-02+ top. Fed’s Bowman (who dissented at the most recent meeting) is set speak about her decision later.

- JGBs climbed by almost 30 ticks during Ueda’s speech and potentially driving the broader modest move higher in USTs/EGBs/Gilts across the morning.

- Gilts gapped lower by nine ticks as the benchmark reaction to UK data points from earlier in the morning with strong Retail Sales (buoyed by good weather) sparking a hawkish reaction in GBP at the time a modest but fleeting move in market pricing. The move ultimately proved fleeting, broadly a factor of the JGB upside.

- Bunds are towards the top end of a sub-30 tick range with European specifics relatively light aside from a handful of ECB speakers, though commentary was in-fitting with the data-dependent tone and as such did not merit any reaction. At a 134.53 peak, someway shy of Wednesday’s 134.86 best.

Commodities

- Crude complex is slightly softer largely a factor of today’s subdued market sentiment. Brent’Nov sits near the lower end of a USD 74.40-74.87/bbl parameter.

- Precious metals are firmer but to varying degrees with spot silver the outperformer, spot gold printing fresh record highs, and spot palladium relatively flat. XAU rose from a USD 2,584.87/oz APAC low to a high of USD 2,612.60/oz in early European hours.

- Overall a mixed session for base metals amid the cautious tone elsewhere, but industrials are seemingly still supported by the Fed’s 50bps rate cut alongside reports that China weighs removing major homebuying curbs to boost demand, according to Bloomberg.

- Operator of Kazakhstan’s Karachaganak field says it cut oil output on Sept 9-5 due to maintenance; says it will run another round of maintenance on Sept 23-28.

Geopolitics: Middle East

- Israel conducted dozens of strikes in south Lebanon in a major intensification of bombing, according to Reuters citing security sources, while Israeli military later said that their fighter jets struck hundreds of rocket launcher barrels in southern Lebanon that were ready to be used immediately to fire toward Israeli territory, according to Reuters.

- “Senior adviser to (Israeli PM) Netanyahu presented the Biden administration with a new proposal for a ceasefire and the liberation of hostages”, via Al Jazeera citing CNN

- Hamas source told Al-Arabiya that they are keen to reach an agreement in Gaza.

- The US doesn’t expect an Israel-Hamas deal before the end of US President Biden’s term, according to WSJ

- “Russia warns of ‘dire consequences’ if Israel launches large-scale military operation in Lebanon”, according to Al Arabiya.

Geopolitics: Other

- Russia says it is concerned by increasingly “provocative” NATO activity on the border with Belarus. Russia notes that it has tactical nuclear weapons in Belarus, says Kyiv and the West risk “disastrous consequences” if they pursue provocative scenarios.

- Russian Foreign Minister Lavrov said they see how NATO is increasing its manoeuvres near the North Pole and that Russia is ready to defend its interests militarily, according to Asharq News.

- China Defence Ministry spokesperson said US arms sales to Taiwan seriously violated the One-China principle and provisions of China-US joint communiques.

US Event Calendar

DB’s Jim Reid concludes the overnight wrap

Markets put in a buoyant performance over the last 24 hours, as growing optimism about a soft landing and the Fed’s 50bp rate cut pushed risk assets up to new highs. In particular, the S&P 500 (+1.70%) surged to a fresh record, marking its 39th all-time high of 2024 so far, and taking it above its previous peak from mid-July. That was echoed across the board, with credit spreads tightening and oil prices rising, alongside a mounting belief that this economic cycle could still have some way to run.

This belief in the US soft landing got fresh support yesterday from the weekly initial jobless claims. Bear in mind that these are one of the timeliest indicators we have on the US labour market, and they showed claims were down to 219k (vs. 230k expected) in the week ending September 14. That’s the lowest number since May, and there are growing signs that isn’t just a blip, because the 4-week moving average was also down to 227.5k, which is the lowest since early June. The decline may have been boosted by residual seasonality, with strong September declines visible the previous two years. But the release comes on top of other strong data earlier in the week, including the retail sales and industrial production releases for August. Indeed, the Atlanta Fed’s GDPNow forecast is currently at an annualised +2.9% for Q3, almost in line with the +3.0% number in Q2, which doesn’t look like a recession at all.

Obviously it’s early days in this cycle of rate cuts, but so far at least, we appear to be in the benign scenario where the Fed are cutting rates outside of a recession. Historically, that has been a very good combination for equities, as Jim pointed out in his chart of the day earlier this week (link here). Moreover, with the Fed’s decision to cut on Wednesday, that’s adding to the global synchronicity of this monetary policy easing, as many of the developed world central banks are now cutting rates again.

That said, for all the optimism in markets right now, it’s clear that a few concerns still lie under the surface. In particular, futures are continuing to price in a more aggressive pace of cuts than was implied by the Fed’s dot plot on Wednesday, so investors think they might need to accelerate those rate cuts if downside risks materialise. For instance, the median dot signalled a further 50bps of cuts by year-end, with just one member opting for more than that at 75bps. But futures are pricing in 73bps of cuts by the December meeting, so by implication they think it’s more-likely-than-not that the Fed will cut faster than the dot plot.

The other interesting feature of recent sessions has been the recovery in near-term inflation swaps. As recently as September 6, the 2yr inflation swap fell to just 1.98%, which was the lowest it had been since 2020, before the inflation spike began. But over recent sessions, that has recovered back to 2.23%, which is the highest since July 19, before the market turmoil really kicked off in earnest at the start of August. Now clearly that’s pretty low by the standards of recent years. But with fears of a downturn falling back, it’s a sign that markets have become a little bit more cognisant of inflation risk over recent sessions, and gold prices (a classic inflation hedge) closed at another all-time nominal high yesterday of $2,587/oz.

Whilst many central banks have begun to ease policy again, one exception to this pattern of course is the Bank of Japan (BOJ), and their rate hike in July was a contributing factor to the market turmoil in early August. However, in their latest decision overnight, they’ve left their policy rate unchanged, in line with expectations. Their statement warned of “high uncertainties surrounding Japan’s economic activity and prices” and said that “it is necessary to pay due attention to developments in financial and foreign exchange markets”. Separately, data also showed that Japanese inflation picked up as expected, with headline inflation up to a 10-month high of +3.0% in August, having been at +2.8% in July. Against this backdrop, the Japanese Yen has strengthened +0.32% this morning, and is currently trading at 142.18 per US Dollar.

Otherwise in Asia, the region’s equity markets have built on the global rally overnight, with sizeable advances for the Nikkei (+1.90%), the Hang Seng (+1.45%) and the KOSPI (+0.94%). The exception to this have been equities in mainland China, where the CSI 300 (-0.27%) and the Shanghai Comp (-0.23%) are both lower this morning. That comes as the People’s Bank of China left their key lending rates unchanged, with the 1yr loan prime rate staying at 3.35%, and the 5yr loan prime rate at 3.85%.

Those moves in Asia follow a very strong performance in the US and Europe yesterday, with equities surging on both sides of the Atlantic. In the US, this saw the S&P 500 (+1.70%) hit a new record after its best session since early August, with tech stocks leading the way. That meant the NASDAQ was up +2.51%, and the Magnificent 7 saw an even larger gain of +3.44%. Small-cap stocks were another beneficiary, and the Russell 2000 (+2.10%) posted a 7th consecutive advance for the first time since March 2021. Meanwhile in Europe, it was a similar story of tech stocks leading the way, supporting gains for the STOXX 600 (+1.38%), whilst the DAX (+1.55%) hit a new record as well. However, futures are pointing to a pullback again this morning, with those on the S&P 500 (-0.12%) and the DAX (-0.33%) both lower.

Otherwise yesterday, the Bank of England announced their latest policy decision, where they kept their policy rate unchanged at 5%, in line with expectations. That follows their first rate cut of this cycle at the previous meeting, but Governor Bailey warned in a statement that “we need to be careful not to cut too fast or by too much”, even as he said they “should be able to reduce rates gradually over time”. At the meeting, they also voted to reduce their stock of gilts by £100bn over the next 12 months, maintaining the same pace as the previous year.

Against this backdrop, sterling strengthened to its highest level against the US Dollar since March 2022, at $1.3284 by the close yesterday. Similarly against the Euro, it was up to €1.1901. Gilts also underperformed their counterparts elsewhere, with the 10yr yield up +4.5bps, in contrast to yields on 10yr bunds (+0.7bps) and OATs (+1.5bps), which saw smaller rises.

When it came to US Treasuries, there was a fresh bout of curve steepening yesterday, which left the 2s10s at 13bps, the steepest it’s been since June 2022. That steepening has been seen across the yield curve, with the 5s30s up +3.2bps yesterday to 57bps, the steepest since January 2022. That came as the 10yr yield was up +0.9bps to 3.71%, whilst the 2yr yield fell back -3.6bps to 3.58%.

Looking at yesterday’s other data, US existing home sales fell to an annualised rate of 3.86m in August (vs. 3.90m expected), their lowest in 10 months. Separately, the Conference Board’s leading index fell -0.2% (vs. -0.3% expected).

To the day ahead now, and data releases include UK retail sales and German PPI for August. Otherwise, central bank speakers include ECB President Lagarde and the Fed’s Harker.