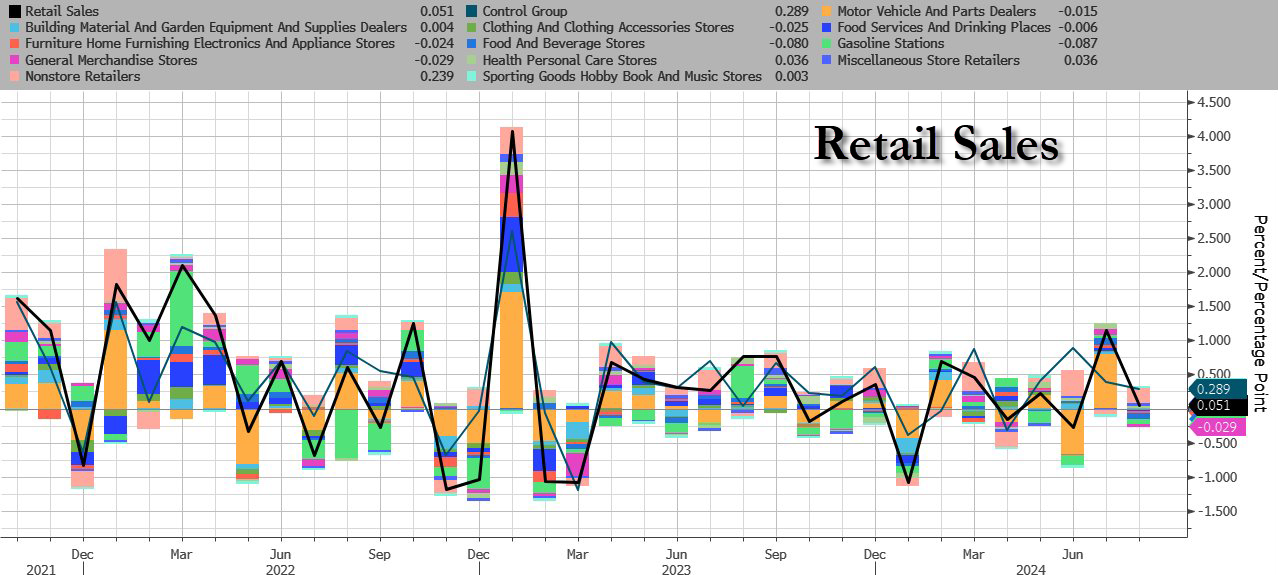

US equity futures gain, and trade just shy of all time highs, led by Tech (especially Mag7 and Semis) as global markets trade higher ahead of the FOMC tomorrow as traders continue to increase probability of 50bps cut (~70% chance now) prompted by another Nick Timiraos WSJ article saying the decision between at 25 vs 50bps rate cut is complicated but withholding a larger cut could raise awkward questions. As of 8:00am ET, S&P futures are up 0.4%, rising for a 7th consecutive day, while Nasdaq 100 futs gain 0.5%, with INTC (+6.9%) the standout and MSFT +1.9% on a new $60 billion buyback. European stocks are also broadly higher as Asian markets are mixed and Japan stocks tumbled 2% after reopening from holiday and getting dragged lower by the surging yen. Bond yields are lower across the curve as the 10Y TSY yields drop to 3.60%, a new 2024 low ahead of tomorrow’s Fed rate decision where odds are now 70% of a 50bps rate cut. The USD remains under pressure, dropping for a fifth consecutive session, falling 0.1% to the lowest since January. Commodities are mixed: crude down, natgas up, precious down, base up, and Ags higher. For the US session, focus is on retail sales this morning, with the market looking to firm up expectations for tomorrow’s FOMC meeting (currently ~-40bps priced). The latest BofA card spending data suggests retail sales will miss estimates (est are for headline retail sales at -0.2%, control group +0.3%) reflecting mixed card spending and a moderation from the 7.7% annualized pace of retail control growth over the prior two months, but a potential boost from back-to-school shopping. Also this morning we have IP, NAHB housing market data and pre-recorded remarks from FOMC non-voter Logan (note, her remarks will not address monetary policy or the economy, reflecting the FOMC’s blackout period).

In premarket trading, Microsoft gains +2% after after it raised its quarterly dividend 10% and announced a new $60 billion stock repurchase program. Intel is up +6.5% after it announced it will make custom AI chips for Amazon AWS. Here are some other notable premarket movers:

- AppLovin climbs 2.4% following an upgrade of the software maker to buy at UBS on improving revenue growth visibility.

- HP Enterprise rises 3.5% as BofA upgrades to buy from neutral, citing numerous upcoming catalysts for the computer hardware and storage company.

- Shopify advances 2.1% following an upgrade to buy at Redburn Atlantic, which sees the company as a prime beneficiary of expected accelerated growth in US social e-commerce.

- SolarEdge Technologies shares fall 7.1% as Jefferies cuts to underperform from hold, citing significant headwinds in Europe.

- Torrid Holdings shares gain 3.5% after William Blair raised the apparel retailer to outperform from market perform, seeing potential for the stock to “effectively” double over the next six to 12 months.

- Viasat shares fall 3.7% as JPMorgan cut the recommendation on the communication company to neutral from overweight, after United Airlines chose to partner with Elon Musk’s Starlink instead of the broadband satellite provider to power its inflight Wi-Fi.

On the eve of the Fed’s first rate cut in more than four years, investor attention will home in on US retail figures due later (our preview is here). The numbers will feed into a debate raging across markets over whether the Fed will ease by 25 basis points, or by double that amount.

“August’s US retail sales report is, arguably, the most important of today’s releases, given that a soft print would likely see participants go ‘all-in’ on the idea of a jumbo 50 basis point Fed cut tomorrow,” wrote Michael Brown, a strategist at Pepperstone Group Ltd., in a note. “Though it’s tough to imagine an equally aggressive paring of dovish bets were the data to beat expectations.”

Former NY Fed President Bill Dudley was among those expecting a 50 basis-point move. “Monetary policy is tight, when it should be neutral or even easy,” he wrote in a Bloomberg column. “And a bigger move now makes it easier for the Fed to align its projections with market expectations, rather than delivering an unpleasant surprise not warranted by the economic outlook.”

But for Jacques Henry, head of cross-asset research at Silex in Geneva, such a large reduction is “a double-edged sword,” as it could suggest the Fed is worried the US economy is slowing faster than expected. The quarter-point cut he expects brings the risk of some short-term disappointment for equity markets. “There could be some drawback on sectors such as real estate and tech,” Henry said.

Meanwhile, optimism around Fed rate cuts has boosted investor sentiment for the first time since June, according to a global survey by Bank of America, Fund managers see a 79% chance of a soft landing as rate cuts support the economy. Still, investors are “nervous bulls,” with risk appetite tumbling to an 11-month low, said BofA strategist Michael Hartnett. The poll also showed a big rotation into bond-sensitive sectors such as utilities from those that typically benefit from a robust economy.

European stocks climb to their highest in two-weeks with all 20 sectors in the green. The Stoxx 600 was up 0.7%, led by retail and banking stocks while healthcare and telecommunications stocks lagged. Gains were also boosted by the latest German ZEW Investor Confidence print which was weaker than expected (expectations 3.6 vs cons 17; current situation -84.5 vs -80 cons, lowest since May 2020/expectations lowest since Oct ‘23) boosting hopes for even more rate cuts by the ECB. Here are the biggest European movers Tuesday:

- Hermes advances as much as 1.4% after the luxury fashion house was upgraded to outperform from neutral at BNP Paribas Exane, which said the company will be stronger than peers for longer

- Flutter shares rise as much as 1.3% in London trading after the group agreed to acquire Playtech’s Italian gambling operation Snaitech for a total enterprise value of €2.3 billion in cash

- Kingfisher gains as much as 8.4%, the most in about four years, after the UK home-improvement retailer lifted the bottom-end of its guidance ranges for annual earnings and cash flow

- Barry Callebaut shares rise as much as 7.8% after getting a double upgrade to overweight at Barclays, while Lindt & Spruengli shares also gain after being raised by one notch at the broker

- SUSS MicroTec rises as much as 13% as Jefferies starts coverage with a buy rating, describing the process equipment provider as a “hidden gem” within the European semiconductor sector

- Pure Biologics surge as much as 30% after the Polish biotechnology company signed a term sheet on a possible partnership with an undisclosed US company to develop two drug projects

- Auction Technology Group shares rise as much as 5.1% after the online marketplace platform operator was upgraded by analysts at JPMorgan, who said the shares are now “overly discounting” the risk to earnings in 2025

- Dometic falls as much as 14%, the most since March 2020, after the Swedish recreational vehicle and camping equipment maker issued a profit warning, saying that macroeconomic challenges were weighing on sales

- THG shares drop as much as 5.2% after the online retailer reported weaker-than-expected first-half results and said it expected earnings for the year at the lower end of consensus estimates

- Essentra shares sink 25%, their steepest drop since 2016, after the component maker cut its guidance for full-year adjusted operating profit by about 17% at the midpoint

- JTC drops as much as 7.4% on Tuesday after releasing its first-half results, with the financial firm retreating from yesterday’s record high close

Earlier in the session, Asian stocks were mixed as gains in Hong Kong were negated by losses in Japanese stocks as a stronger yen weighed on exporters. The MSCI Asia Pacific Index rose less than 0.1%, recovering from early declines, as Tencent and Alibaba climbed in Hong Kong. The nation’s benchmark index rose nearly the most in three weeks. Meanwhile, Japan’s Topix plunged nearly 2% as the market reopened following a holiday on Monday as stocks caught down to the recent plunge in the USDJPY. Markets in mainland China, Taiwan and South Korea were closed for holidays, while Australian shares climbed for a fourth day, and Indian stocks rose. Benchmarks also traded higher in Southeast Asia, led by the Philippines, Singapore and Malaysia.

All eyes are on policy decisions and commentary this week by the Federal Reserve and Bank of Japan. The yen strengthened through the psychological level of 140 per dollar Monday amid expectations the gap between US and Japanese interest rates will narrow further. “We continue to think the earnings picture of Japan’s exporters and multinationals will likely get murkier, as much of the forex gains that have greatly flattered corporate earnings in the past two years disappear,” Asymmetric Advisors said in a note.

In FX, the Bloomberg Dollar Spot Index drops for a fifth consecutive session, falling 0.1% to the lowest since January ahead of Wednesday’s Federal Reserve policy decision. “The US retail sales numbers out later today will likely be significant,” Michael Wan, a senior currency analyst at MUFG Bank in Singapore, wrote in a research note. They “may perhaps help to settle the ongoing debate about whether the Fed may do a 25 or 50 basis point cut later this week.” The yen erased an earlier loss against the dollar as a slide in Japanese shares boosted demand for the currency as a haven.

In rates, treasuries inch higher, with US 10-year yields falling 1 bp to 3.61%. Treasuries are narrowly mixed in early US trading with the curve flatter as front-end yields rise about 1bp on the day with 7Y-30Y sectors little changed. 2s10s, 5s30s spreads extend Monday’s flattening move and remain near session lows. Bunds outperform Treasuries in the wake of weaker-than-expected September ZEW survey data. Focal points of US include August retail sales data and 20-year bond auction. Treasury coupon auctions resume with $13b 20-year bond reopening at 1pm New York time; WI 20-year yield near 3.995% is ~17bp richer than last month’s, which drew good demand.

In commodities, oil prices are little changed, with WTI trading near $70.10 a barrel. Spot gold falls $7 to around $2,576/oz. Bitcoin rises 2%.

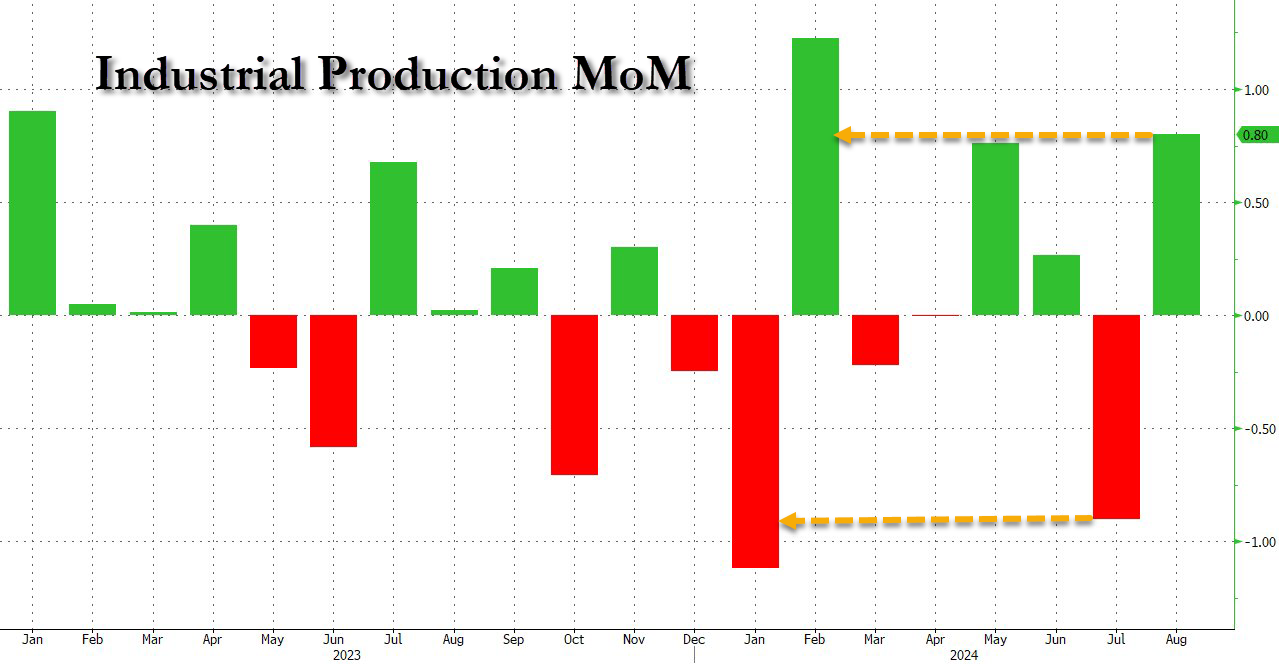

Looking to the day ahead now, and data releases include US retail sales, industrial production and capacity utilisation for August, Canada’s CPI for August, and the German ZEW survey for September. From central banks, the FOMC will begin their two-day meeting today.

Market Snapshot

- S&P 500 futures up 0.2% to 5,650.50

- STOXX Europe 600 up 0.5% to 517.71

- MXAP little changed at 183.82

- MXAPJ up 0.6% to 574.41

- Nikkei down 1.0% to 36,203.22

- Topix down 0.6% to 2,555.76

- Hang Seng Index up 1.4% to 17,660.02

- Shanghai Composite down 0.5% to 2,704.09

- Sensex up 0.2% to 83,115.80

- Australia S&P/ASX 200 up 0.2% to 8,140.90

- Kospi up 0.1% to 2,575.41

- German 10Y yield little changed at 2.11%

- Euro little changed at $1.1135

- Brent Futures down 0.1% to $72.67/bbl

- Gold spot down 0.0% to $2,582.31

- US Dollar Index down 0.14% to 100.63

Top Overnight News

- Fed watcher Nick Timiraos wrote “Fed Prepares to Lower Rates, With Size of First Cut in Doubt: The central bank usually prefers to move in increments of a quarter point. This time, it’s complicated” which noted the decision whether to cut by 25bps or 50bps will come down to how Powell leads his colleagues through a finely balanced set of considerations, while he added that data over the past months showed inflation resumed a steady decline to the 2% goal but the labor market has cooled: WSJ

- US officials are traveling to China with a warning to Beijing about the flood of exports being sent by Chinese companies around the world as the country’s domestic growth cools. WSJ

- Washington and Tokyo are nearing a deal that would impose fresh restrictions on the ability of non-US chip firms to export products to China. FT

- Shigeru Ishiba has taken the lead in the latest Nikkei opinion poll asking who the best person is to lead the LDP (and therefore become the country’s next PM). Nikkei

- There’s little chance that the European Central Bank will lower interest rates again next month, according to Governing Council member Gediminas Simkus. BBG

- UniCredit is set to ask the ECB within days for regulatory permission to build a stake of as much as 30% in Commerzbank, a person familiar said. BBG

- Justin Trudeau suffered a big political setback as his Liberal Party lost a special election in Montreal. It’s the second major defeat at the ballot box for the Canadian PM after his party lost a seat in the Toronto area in June, raising the pressure on him to step aside before the next election. BBG

- Blinken is headed back to the Middle East, but a Gaza ceasefire breakthrough isn’t imminent. WSJ

- Israel updated its war goals, adding the safe return of its citizens to their homes near the border with Lebanon. RTRS

- A panel of federal judges sounded skeptical about TikTok’s legal arguments as the company combats a recent bill that would force the platform to be sold or face a US ban. NYT

- BofA September Global Fund Manager Survey: Sentiment improves for first time since June on “Fed cuts = soft landing” optimism; cash level dips to 4.2%; Big rotation to bond sensitives from cyclicals, overweight utilities since 2008; Tactically survey says the bigger the Fed cut, the better for cyclicals.

- Microsoft announced a quarterly dividend increase of 10% to USD 0.83/shr and a new USD 60bln share repurchase program.

- Intel said it and AWS are expanding their strategic collaboration by co-investing in custom chip designs, including an AI fabric chip and a custom Xeon 6 chip; the partnership supports US semiconductor manufacturing and AWS’s data centre expansion in Ohio. Separately, it said it plans to establish Intel Foundry as an independent subsidiary to provide clearer separation for external customers and suppliers. Will be pausing manufacturing buildout projects in Poland and Germany.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive but with gains capped as participants continued to second-guess the magnitude of the looming Fed rate cut, while markets in Mainland China, Taiwan and South Korea remained closed for holidays. ASX 200 marginally edged higher and printed a fresh intraday record high with early advances led by real estate and tech. Nikkei 225 suffered on return from the long weekend and fell beneath 36,000 amid headwinds from the recent currency strength. Hang Seng shrugged off early cautiousness and gradually climbed higher ahead of the Mid-Autum Festival in Hong Kong, while Midea Group’s H shares surged over 8% on its Hong Kong debut following Hong Kong’s largest IPO in three years.

Top Asian News

- US and Japan are nearing a deal to curb chip technology exports to China, according to FT.

- Japanese Finance Minister Suzuki said FX fluctuations have both merits and demerits on Japan’s economy, while they will respond appropriately after analysing the impact of FX moves. Furthermore, he reiterated that rapid FX moves are undesirable and it is important for currencies to move in a stable manner reflecting fundamentals.

- German KfW executive says looking to grow investments in India to USD 1bln from current USD 400mln over the next few years.

European bourses, Stoxx 600 (+0.5%) opened on a firmer footing, and have traded at session highs throughout the European morning, not deviating much from the levels seen at the cash open. European sectors hold a strong positive bias; Retail is the clear outperformer, propped up by post-earnings strength in Kingfisher (+7.2%). Healthcare is found at the foot of the pile, alongside Telecoms. US Equity Futures (ES +0.2%, NQ +0.5%, RTY +0.3%) are modestly firmer across the board, with very slight outperformance in the tech-heavy NQ, attempting to pare back some of the losses seen in the prior session.

Top European News

- ECB’s Simkus says the economy is developing in line with forecasts; the likelihood of an October rate cut is very small; will not have many new data points in October.

- EU Commission President von der Leyen proposes France’s Sejourne as Commissioner for Industrial Strategy and Ribera for Competition Commissioner; proposes Sefcovic as the Trade Commissioner and Dombrovskis as the Economy Commissioner. Serafin as the Budget Commissioner. Kubilius as Defence Commissioner

FX

- USD is a touch softer vs. peers as the dovish Fed repricing continues. Markets now assign a near 70% chance of a 50bps cut by the Fed this week vs. circa. 15% in the wake of last week’s CPI data. Today’s US Retail Sales at 13:30 BST / 08:30 EDT is due.

- EUR is steady vs. the USD after another batch of soft data from Germany saw the pair pullback from its session high at 1.1146. If upside in the pair resumes, the 6th September high resides at 1.1155.

- GBP is flat vs. the USD with UK-specifics light in the run up to UK CPI tomorrow and the BoE policy announcement on Thursday with the former unlikely to have much impact on the latter. The 1.3218 high for today’s matches that of Monday’s.

- JPY is steady vs. the USD after the pair failed to hold below 140 yesterday (printed a trough at 139.57). Focus this week will no doubt be on the FOMC on Wednesday ahead of the BoJ on Friday.

- Antipodeans are both broadly steady vs. the USD. AUD/USD has just about eclipsed yesterday’s best of 0.6753 and is at its highest level since 6th September; 0.6767 was the high that day.

- CAD is steady vs. the USD in the run up to today’s CPI metrics. Today’s release comes in the context of comments over the weekend from BoC Governor Macklem that the Bank could begin cutting rates in 50bps increments.

- Canada’s ruling party has lost a key Quebec seat in the Montreal special election, framed as a blow to PM Trudeau, via CBC.

Fixed Income

- USTs are essentially flat; overnight focus was on the latest WSJ Timiraos piece which highlighted that when the Fed has doubts around the size of its first cut it generally favours 25bps; however, “this time, it’s complicated”. This could potentially be the reason USTs caught a slight bid to a 115-21 high, where it currently resides.

- Bunds are firmer; a modest bounce was seen across fixed income as European players rejoined the session. Specific developments were slim but the move was potentially a function of participants reacting to an overnight Timiraos piece. A move which took Bunds to a 135.39 peak, stopping 10 ticks shy of last week’s 135.49 best.

- Gilts are firmer, in tandem with the broader strength seen across peers; Gilts hit a new contract peak at 101.52, but unable to matierally hold above 101.50 ahead of the 2054 Gilt auction. The tap was strong but not as stellar as the last outing, but Gilts themselves were unreactive to the auction.

- UK sell GBP 2.75bln 4.375% 2054 Gilt: b/c 2.89x (prev. 3.35x), average yield 4.329% (prev. 4.636%), tail 0.2bps (prev. 0.2bps)

Commodities

- Crude futures began the European morning on a firmer footing, but has since slipped off best levels and currently trades towards the bottom end of today’s ranges; Brent’Nov currently within a 72.35-73.21/bbl range.

- Mixed trade overall in the precious metals complex, with spot silver flat and gold dips lower but spot palladium outperforms with gains of some 1% at the time of writing. XAU sits in a narrow USD 2,574.63-2,587.02/oz range.

- Mixed trade across base metals futures with traders not committing to a particular direction ahead of the upcoming risk events. APAC trade was also tentative amidst the lack of Chinese participants amid the Mid-Autumn festival break.

- PBF’s 166k BPD Torrance California refinery reports flaring due to malfunction

Geopolitics: Middle East

- US Secretary of State Blinken will travel to Egypt today for US-Egypt strategic dialogue.

- “Houthi leader: ready to send hundreds of thousands of trained fighters to Hezbollah”, via Sky News Arabia.

Geopolitics: Other

- North Korea’s Foreign Minister travelled to Russia, according to KCNA.

- Two Chinese Coast Guard ships arrived in Russia’s Port of Vladivostok for joint drills, according to RIA.

US Event Calendar

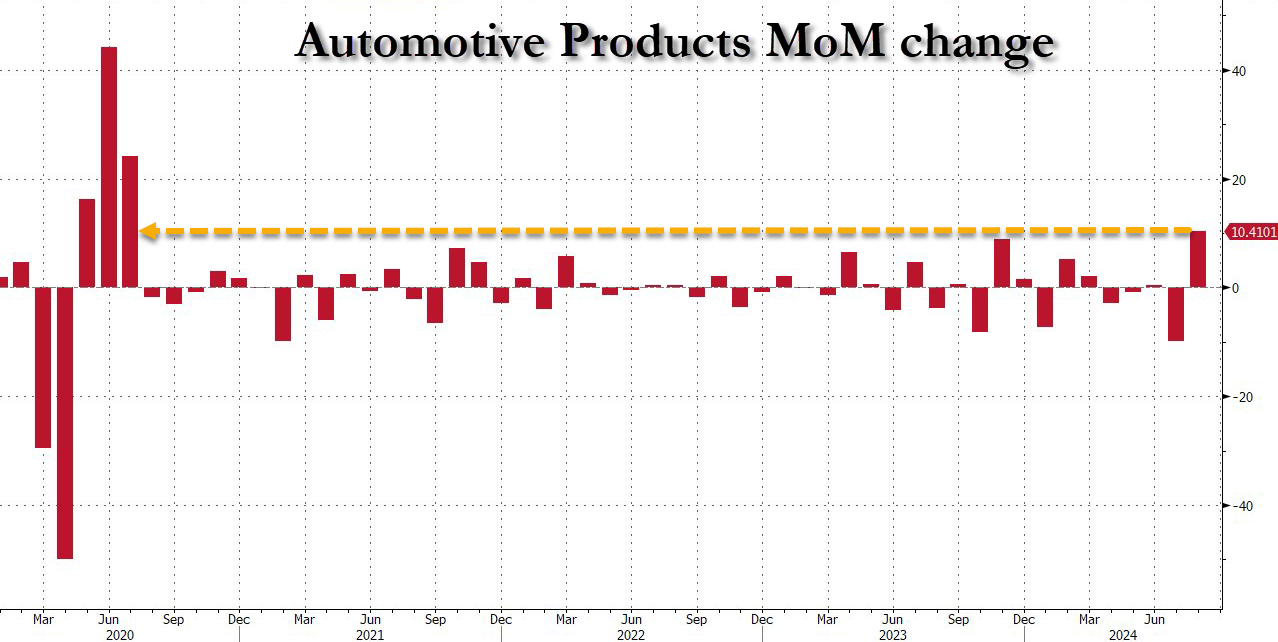

- 08:30: Aug. Retail Sales Advance MoM, est. -0.2%, prior 1.0%

- Aug. Retail Sales Ex Auto MoM, est. 0.2%, prior 0.4%

- Aug. Retail Sales Ex Auto and Gas, est. 0.3%, prior 0.4%

- Aug. Retail Sales Control Group, est. 0.3%, prior 0.3%

- 08:30: Sept. New York Fed Services Business, prior 1.8

- 09:15: Aug. Industrial Production MoM, est. 0.2%, prior -0.6%

- Aug. Manufacturing (SIC) Production, est. 0.2%, prior -0.3%

- Aug. Capacity Utilization, est. 77.9%, prior 77.8%

- 10:00: July Business Inventories, est. 0.3%, prior 0.3%

- 10:00: Sept. NAHB Housing Market Index, est. 41, prior 39

DB’s Jim Reid concludes the overnight wrap

If you’ve been following DB’s macro research over the last few days, you’ll be aware of the view that if there was no informed Fed sources massaging the market back down to 25bps by the close of play last night, then the consensus here is that this would imply the Fed is leaning towards 50bps tomorrow night. For most of yesterday the market was pricing in around 40bps of cuts which as Matt Raskin pointed out in a great chart we highlighted yesterday, left this meetings’ pricing the furthest from both a 25 and 50bps move two days out from the meeting since for over 15 years. So a very rare level of uncertainty. As we type this morning, the pricing has ticked up further to 43.5bps, or in other words a 74% chance of a 50bp move. Overnight, we’ve had another WSJ article from Nick Timiraos, although it didn’t steer things in either direction and the headline indicates the ongoing uncertainty, saying “Fed Prepares to Lower Rates, With Size of First Cut in Doubt”.

In recent times, the closest parallel to this uncertainty is the decision in March 2023, amidst the regional bank turmoil. Before SVB’s collapse on March 10 last year, it was widely expected that the Fed would proceed with a rate hike on March 22. But as the turmoil grew worse, there were serious doubts about whether the Fed would still go ahead, and there were similar debates happening about whether a dovish decision might signal that things were worse than markets thought. Ultimately, the Fed did proceed with the hike, but on the Monday before the decision, futures were still only pricing it as a 73% chance, and right before the announcement it had only drifted up to 80%. So there was a little bit of doubt as to what they’d do, although not to the extent that we’re seeing today.

Of course, there are quite a few residual nerves today about going for 50bps. Indeed, on all the recent occasions when the Fed have accelerated up to 50bp cuts, bad things have then happened. That was the case when they opened in 2001 and 2007 with 50bp cuts, whilst the first Covid cut in March 2020 was also an initial 50bp move (followed up by a 100bp cut less than two weeks later). But although the precedents aren’t good, it’s worth bearing in mind that correlation isn’t causation, and it’s hardly like the GFC only happened because the Fed opened with 50bps. So it’ll be fascinating what history has to say about this time.

With growing anticipation for a 50bp cut, that helped pushed US Treasury yields down to fresh lows. For instance, the 2yr yield (-3.1bps) closed at a fresh two-year low yesterday of 3.55%, and the 10yr yield (-3.4bps) closed at a 15-month low of 3.62%. It was a similar story for real yields, and the 10yr real yield (-4.2bps) fell back to 1.53%, which hasn’t been seen since July 2023. Already that’s been filtering through into lower mortgage rates, and last week’s data from the MBA showed that the average 30yr mortgage rate in the US was down to 6.29% in early September, the lowest in over 18 months. However there wasn’t much negative impact from rates going up aggressively as most homeowners have a 30yr fixed (low) rate. So it’s unlikely that lower mortgage rates will have a big impact on housing unless it goes a lot lower and prompts refinancing and more voluntary home moves.

We will get a final batch of data today before tomorrow’s big decision, as US retail sales and industrial production numbers for August are out later. So it’ll be interesting to see how they affect estimates for Q3 growth. Currently, the Atlanta Fed’s GDPNow tracker stands at an annualised rate of +2.5% for this quarter, and we’ll get another update today after that data is out, so one to keep an eye on. We didn’t get much data yesterday, although there was the Empire State manufacturing survey for September, which posted its strongest reading since April 2022, at 11.5 (vs. -4.0 expected).

For equities, the main theme yesterday was the rotation trade, as the Magnificent 7 (-0.70%) fell back again even as the small-cap Russell 2000 (+0.31%) advanced. That continued the theme from Friday, and it means that over the last two sessions, the Russell 2000 is now up +2.81%, whereas the Mag 7 is down -0.39%. That weakness among the Mag 7 was led by Apple (-2.78%) as the first weekend of new iPhone pre-order sales appeared to have come in at the weaker side of expectations. But the broader mood was positive, with the S&P 500 (+0.13%) advancing for a sixth session in a row, closing just -0.60% beneath its all-time high from mid-July. Indeed, three quarters of the index constituents were higher on the day, led by financials (+1.22%) and energy (+1.20%) stocks, which helped the equal-weighted S&P 500 (+0.66%) to reach a new all-time high.

Over in Europe, that rotation theme was also evident. The STOXX 600 (-0.16%) posted a modest decline, mostly as the STOXX Technology Index (-1.25%) saw a decent pullback. Sovereign bonds also echoed the US rally, with yields on 10yr bunds (-2.6bps), OATs (-0.7bps) and BTPs (-3.3bps) all moving lower. Moreover, for BTPs that left them at 3.48%, their lowest closing level so far this year.

Overnight in Asia it’s been a fairly quiet morning, with markets in mainland China and South Korea closed for public holidays. But in Japan, equities have slumped amidst the continued appreciation of the Japanese Yen, with the Nikkei (-1.81%) and the TOPIX (-1.76%) both seeing sharp declines. Indeed, the prospect of a 50bp Fed rate cut saw the Japanese Yen strengthen past 140 per dollar at one point yesterday, which is its strongest since July 2023, although this morning it’s weakened again to 140.71 though. Nevertheless, there has bene some more positivity elsewhere, and in Hong Kong, the Hang Seng is up +1.44% this morning. Looking forward, US equity futures are pointing a bit lower, with those on the S&P 500 down -0.11% as we await the Fed’s decision tomorrow.

To the day ahead now, and data releases include US retail sales, industrial production and capacity utilisation for August, Canada’s CPI for August, and the German ZEW survey for September. From central banks, the FOMC will begin their two-day meeting today.