“Congratulations On Becoming The Richest Man In The World,” Said JP Morgan To Andrew Carnegie In 1901

By Eric Peters, CIO of One River Asset Management

Move On:

“Congratulations on becoming the richest man in the world,” said JP Morgan to Andrew Carnegie in 1901, merging various industrial firms into US Steel. The new firm was capitalized at $1.4bln and became the world’s most valuable company (the US federal budget in 1901 was $517mm for comparison). Carnegie was born in Scotland in 1835. His mom was an impoverished weaver, disrupted by mechanized weaving. She moved Andrew to Pennsylvania. At 13 he went to work in a cotton mill, earning $1.20 for a 12hr day. Morgan paid him $492mm.

Carnegie spent the last 20yrs of his life giving away 90% of his fortune. Beginning in 1880, he built 2,500 libraries in the US, Canada, Britain – feeding hungry young minds. The 1st was in his hometown of Dunfermline, Scotland. By his death in 1919, half the US public libraries had been built by Carnegie. Colonel James Anderson let apprentices and working boys borrow books from his personal library when Carnegie was a kid. “To him I owe a taste for literature which I would not exchange for all the millions that were ever amassed by man.”

US Steel was so dominant that it inspired anti-trust laws. In 1943 it employed 340k workers, supporting the war effort. In 1953 it produced 35.8 million tons of steel, while Europe and Japan struggled to rebuild their productive capacity. But it was slow to innovate and relied on old technology. It now produces 14.5 million tons and is the world’s 27th largest producer. In 1991 it was kicked out of the Dow Jones Industrial Average. Japan’s Nippon Steel is trying to buy US Steel for $14.9bln. Our politicians seem to care. But America moves on.

Whatever it Takes:

Draghi in his argument for a new EU industrial strategy calls for 800bln euros of new annual investment spending. At 4.7% of GDP, it’s double the scale of the Marshall Plan relative to the size of the economy. Imagine that bureaucratic trough. And setting aside the fact that the Germans, who would have to shoulder yet more Italian debt, will never agree to anything remotely close to this, it is worth asking why Europe would turn to a former central banker to draft plans for an economic renaissance? Perhaps they misunderstand their problems.

In the 12yrs since Draghi’s “whatever it takes” speech [here], Europe’s benchmark Euro Stoxx 50 index has rallied +108% ex dividends (+67% in real terms). The S&P 500 is +196% higher (+126% on a real basis). When it comes to producing real prosperity, manipulating money is never the answer. In 2012, EU GDP was $14.6trln and has grown to $18.4trln (2023). US GDP over that period has grown from $16.3trln to $27.4trln. The divergence is utterly staggering. And now, of the globe’s top 25 largest companies, just one is European [here].

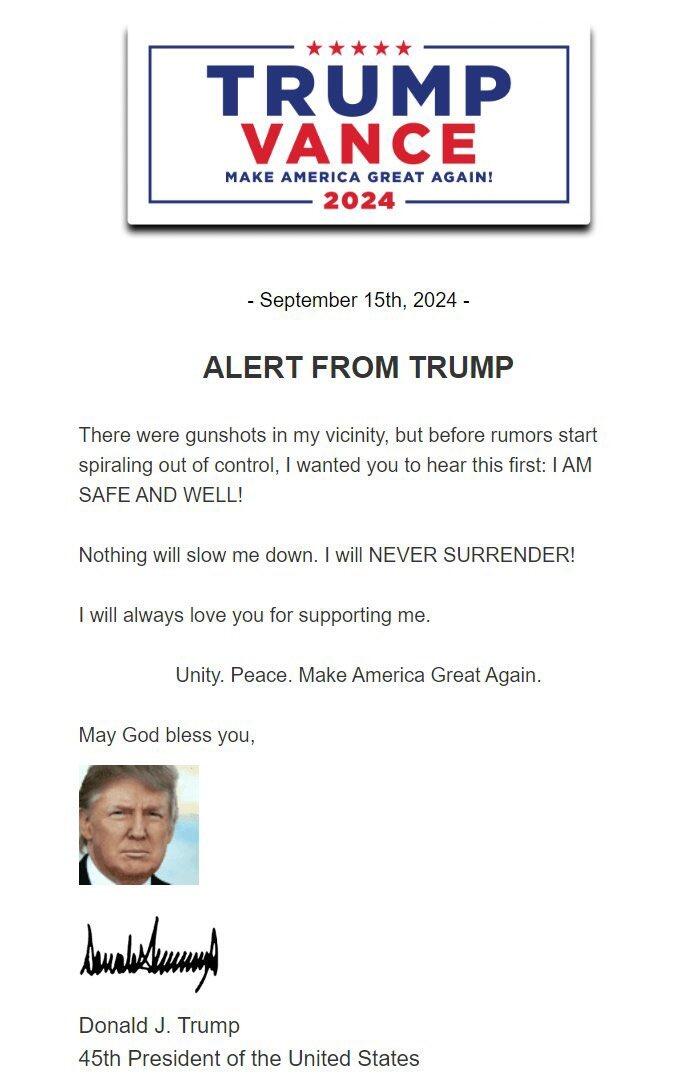

“Nothing Will Slow Me Down” – Trump Reacts After Being Reportedly Targeted By Shooter With AK47 While Golfing, Secret Service Returned Fire

Update (1615ET): The former president has issued a statement confirming he is “safe and well” and declaring “nothing will slow me down”…

AP reports that the alleged shooter fled in an SUV and was later apprehended in a nearby county by local law enforcement, the officials said. The officials were not authorized to discuss the matter publicly and spoke on condition of anonymity about an ongoing investigation.

An AK-style firearm was recovered at the scene near Trump’s golf course, one of the officials and a third law enforcement official said.

The golf course was partially shut down for Trump as he played, and agents were a few holes ahead of him when they noticed the person with the firearm, the officials said.

The person appeared to push the muzzle of the rifle through the fence line and that’s when agents fired, the officials said

CNN reported that police have recovered a backpack and a GoPro camera.

They think the attempted Trump shooter wanted to film it.

The following clip shows a heavy police presence on the roads leading to the golf club…

BREAKING: Donald Trump *was* the intended target of the shots fired at Trump International Golf Club according to CNN.

Agents opened fire on a man who was at the Trump International Golf Course after they saw what appeared to be a gun according to the NYP.

The Trump campaign on Sunday said that former President Donald Trump is safe after reports of gunshots in his vicinity outside the Trump International Golf Course.

“President Trump is safe following gunshots in his vicinity,“ a brief statement released by Trump spokesman Steven Cheung said.

”No further details at this time.”

The U.S. Secret Service wrote on social media platform X that it is working with the Palm Beach County Sheriff’s Office to investigate the incident, adding that it occurred before 2 p.m. ET.

“The former president is safe,” the federal agency said.

The sheriff’s office will provide more details about the incident “soon,” the agency added.

CNN is reporting the shots were intended for the former president…

BREAKING: CNN has said: “Officials believe the shots fired at Trump International Golf Club were intended for former President Donald Trump.” pic.twitter.com/FhHpOSGy1p

CNN goes on to report that a person has been detained in connection to the incident at Trump International Golf Club on Sunday, according to a law enforcement source.

Secret Service fired at the suspect, according to multiple sources.

Officials believe an armed individual intended to target former President Donald Trump at his golf club, according to sources briefed on the matter.

However, The New York Post said two people exchanged fire at Trump golf club in Florida, targeting each other (a narrative that has since been deleted).

The White House was quick to express their “relief” that Trump was not hit:

“The President and Vice President have been briefed about the security incident at the Trump International Golf Course, where former President Trump was golfing. They are relieved to know that he is safe. They will be kept regularly updated by their team.”

As the above suggests, no one is really sure WTF happened for now.

However, one thing we know for sure, the same rhetoric that likely prompted the first assassination attempt has not stopped…

Legacy media has spent the week hyperventilating over conservatives “inciting threats” for expressing their opinions on the migrant issues in Ohio.

Meanwhile they didn’t stop calling Trump a “n*zi” and a “threat to Democracy” for one second since J13.

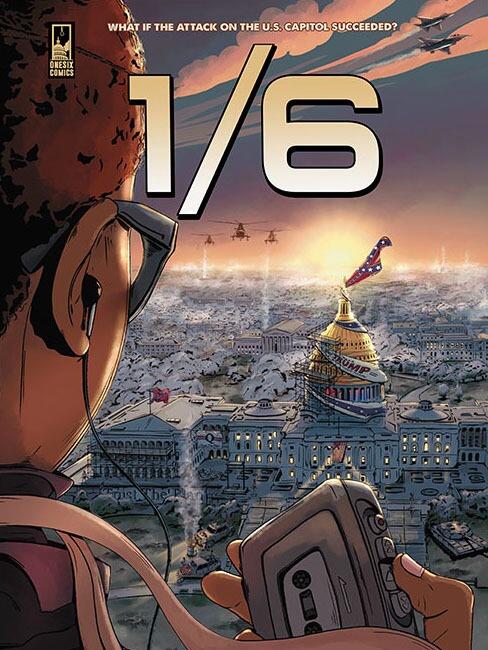

The Harvard Law professor who co-authored a “what if?”-style graphic novel about the January 6 “insurrection” succeeding is sending free copies to every public high school in Pennsylvania.

Alan Jenkins, formerly president of the Harvard “social justice communication lab” Opportunity Agenda, and his co-author Gan Golan are giving out gratis copies of “1/6: A Graphic Novel” in order “to convey the risks facing American democracy,” The Philadelphia Inquirer reports.

“The forces that led to that insurrection … the white supremacy, disinformation […] are all very still much with us,” Jenkins said.

He added that he hopes students will see January 6 as “not unlike the 9/11 terrorist attacks.”

Jenkinssaid he chose Pennsylvania because it’s faced a lot of book “bans.” He noted it’s possible “1/6” might get banned “but [he’s] ready for that.”

“We think the truth always is stronger than censorship,” he added.

But one may wonder how a completely fictitious tale of alternative history counts as “truth.” Here’s a sample from “1/6’s” first issue, according to the Inquirer:

[…] a society controlled by armed militias who take over a TV network — declaring it to be “an enemy of freedom.” At a “patriots parade,” a speaker blasts the “thugs and criminals from Black Lives Matter” while adherents repeat white nationalist slogans, with the phrases “Blood and Soil” and “I will not be replaced” in word bubbles. Dissidents work covertly, avoiding the militias enforcing curfew while transporting Electoral College ballots — “the last evidence of our democracy.”

And were there Confederate flags flying around DC on Jan. 6? Jenkins’ book features it on top of the Capitol and Lincoln Memorial.

In the story’s second issue, “readers are taken through events leading up to and including Jan. 6 — starting with the 2017 [Charlottesville] ‘Unite the Right’ rally.” Jenkins’ “truth” includes the common — and devoid-of-context — Trump quote about “fine people on both sides” (Trump specifically condemned the neo-Nazis and white nationalists at the rally).

There’s also the missing-context phone calls to Georgia election officials in which Trump said “find 11,780 votes.”

Ironically, Jenkins (pictured below) said he expects “pushback” regarding the comic as many Pennsylvania parents have accused schools of “indoctrinating” students.

The state’s high schools also will receive a supplementary “action guide” for “1/6” which “lays out facts” about the insurrection, election “deniers,” increases in hate crimes, and legislators “banning” books — “a hallmark of authoritarianism.”

Philadelphia-area schools did not respond to Inquirer queries about whether they would stock the book in their libraries or “how they would use it.” One district did note that “1/6” would first have to be reviewed by “a committee of librarians and administrators.”

Jenkins and Golan previously sent 150 copies to members of Congress who allegedly denied the 2020 election results.

According to his faculty page, Jenkins teaches courses on race and the law, communication, and Supreme Court jurisprudence. Along with his law degree, Jenkins has an MA in media studies and a BA in psychology and social relations.

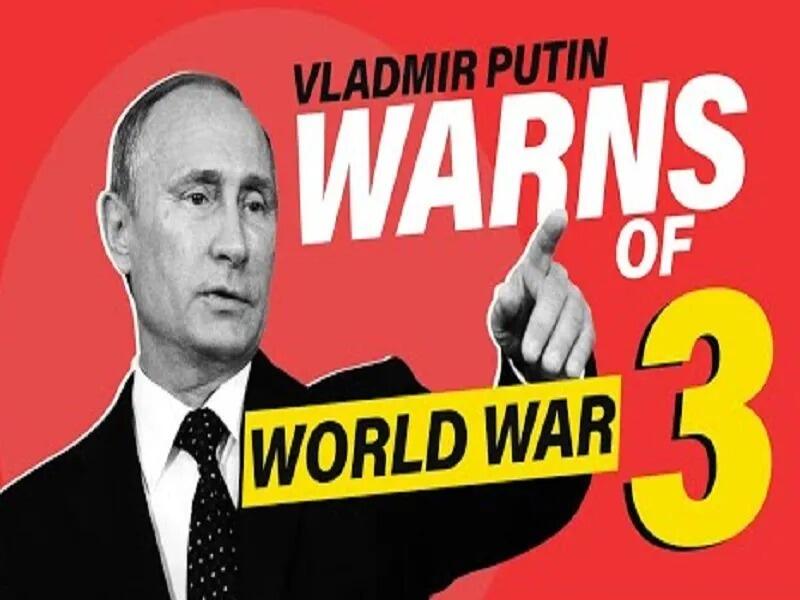

Putin warned last week that letting Ukraine use Western long-range weapons to strike deep inside of Russia “will mean that NATO countries, the United States, and European countries are parties to the war in Ukraine. This will mean their direct involvement in the conflict, and it will clearly change the very essence, the very nature of the conflict dramatically. This will mean that NATO countries – the United States and European countries – are at war with Russia.”

He preceded his words by reminding everyone that “the Ukrainian army is not capable of using cutting-edge high-precision long-range systems supplied by the West. They cannot do that. These weapons are impossible to employ without intelligence data from satellites which Ukraine does not have. This can only be done using the European Union’s satellites, or US satellites – in general, NATO satellites…(and) only NATO military personnel can assign flight missions to these missile systems.”

Foreign Minister Lavrov briefed foreign ambassadors about this on the same day, repeating the same points as his boss but also adding that “Our experts are confident that without such (Western) specialist involvement, it would be impossible (for Ukraine) to use these complex systems. These tasks can only be performed by professionals who have worked with these systems for a long time and know how to operate them. It would be impossible to train someone to use them in just a few weeks.”

Even though Kremlin spokesman Peskov assessed that “we have no doubt that this statement has reached its recipients”, Biden still signaled that he and Starmer might very well approve this proposal regardless.

Russian Deputy Foreign Minister Ryabkov was then quoted by TASS as saying that “We know that the corresponding decisions were made some time ago, and signals of this kind have been transmitted to Kiev.” In other words, everything that’s played out thus far is political choreography.

Although the risk of World War III breaking out by miscalculation continues to grow as a result of these irresponsible Western escalations, it’s unlikely that Putin will radically respond by authorizing his forces to hit targets inside of NATO, let alone launch a nuclear first strike. If he was indeed planning to do so, then there wouldn’t be the need for this political choreography, he’d just do it, plus this latest escalation won’t result in reshaping the military-strategic dynamics of this proxy war in NATO and Ukraine’s favor.

Accordingly, there’s no reason for Putin to react as radically as some are worried that he will, with the most that he might do is finally authorize a US-inspired “shock-and-awe” bombing campaign or at least maybe hit a few bridges across the Dnieper. Even that might not happen though and he could instead just announce another round of partialmobilization of experienced reservists like he did two years ago. Another possibility could be curtailing or cutting off critical mineral and energy exports to the West.

With these much more realistic options in mind, Putin’s political choreography can be seen as an attempt to pressure Kiev into complying with his ceasefire precondition from this summer by withdrawing from all the territory that Moscow claims as its own. If that fails and he doesn’t ramp up bombing, then the secondary motive might be to prepare his people for another round of mobilization. By describing NATO as being in a state of war with Russia, he might also be hinting that he’ll curtail resource exports to it.

As for the West’s political choreography, it appears to be yet another example of “boiling the frog” by gradually crossing every one of Russia’s so-called “red lines”. This helps manage Western public opinion given the unprecedented nature of this proxy war and give Russia the time to prepare for the next escalation so that it’s not caught totally off guard and thus considers “overreacting” like some hawks have wanted. Observers should remember that the West is only just now doing this 2.5 years down the line.

Seeing as how their specialists would be handling pretty much everything connected to these long-range missiles, the fact that this hasn’t happened earlier speaks to their decisionmakers’ desire to control the escalation ladder with Russia, at least in terms of how they see it. Going through with it at this point is pure vindictiveness to inflict as much damage on Russia, including to its civilians, for foiling their strategic defeat of it. Once again, it won’t be game-changer, it just gives Kiev the chance to kill more Russians.

Reflecting on everything, this experience should teach observers that political choreography is only for the sake of perception management since backchannels exist for rival parties to discreetly convey real threats to one another, some of which might then be reaffirmed in public for soft power purposes. Rarely is everything as clear-cut as it seems, with it almost always being the case that much more is going on behind the scenes than meets the eye.

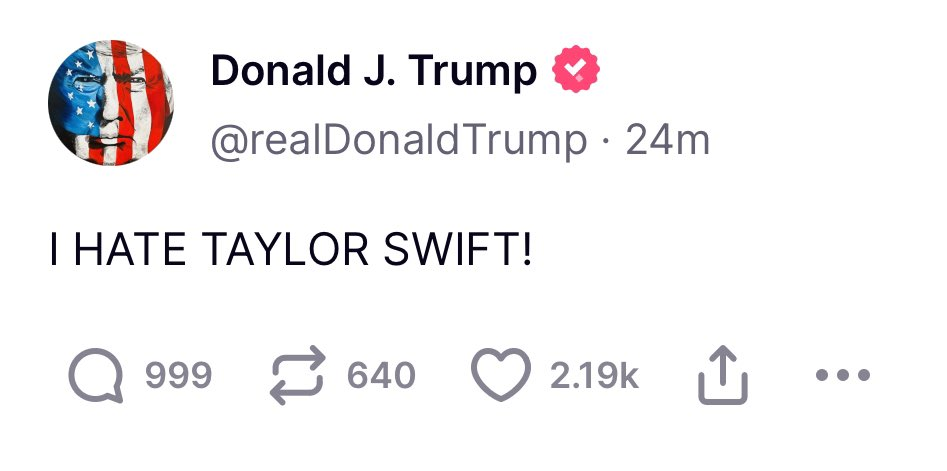

Sour Note: Taylor Swift Harris Endorsement Backfires As More Voters Turn To Trump

Taylor Swift’s post-debate endorsement of Vice President Kamala Harris and her running mate, Minnesota Governor Tim Walz, appears to have completely backfired. A new post-debate poll from YouGov released Saturday found that while 8% of voters said Swift’s endorsement made them “somewhat” or “much more likely” to support the Democratic ticket, a significant 20% said they are “somewhat” or “much less likely” to vote for former President Donald Trump’s opponent after Swift spoke out.

The majority of respondents, however – 66% – said Swift’s high-profile endorsement made no difference in how they will vote in the upcoming November election, according to the NY Post.

The Grammy-winning artist made waves on Instagram to her 283 million followers shortly after Tuesday night’s presidential debate, stating, “I’ve done my research, and I’ve made my choice.” She encouraged her followers to do the same, emphasizing that “the choice is yours to make.” Swift praised Harris as “a steady-handed, gifted leader” who could lead with “calm and not chaos.”

Despite Swift’s powerful platform, the endorsement seems to have mixed, and even negative, impacts on voter sentiment. While 32% of those polled believe her endorsement could have a positive effect on Harris’ campaign, 27% said they don’t think it will make a difference either way. A notable 41% – nearly 460 respondents – expressed the view that the “Shake It Off” singer shouldn’t speak publicly about politics at all, reflecting the persistent debate over whether celebrities should wade into political waters. Meanwhile, 38% felt she should make public endorsements, indicating that there remains a split on the role celebrities should play in shaping political discourse.

Most of the poll’s participants – 66% – reported not being fans of Swift, while 28% identified as fans and 6% as big fans. Unsurprisingly, the majority of her “big fans” were women and registered Democrats.

Trump, meanwhile, didn’t hold back after Swift’s endorsement of Harris, writing on Truth Social:

Swift’s endorsement may have stirred more than just political conversations; it also sparked a wave of civic action. Reports indicate that her call to action led to a flood of traffic on the voter registration website, vote.gov, well into Wednesday afternoon. A spokesperson for the site noted that 337,826 visitors came to vote.gov after clicking a custom link Swift shared on Instagram, showing that while her endorsement may not have swayed many votes, it certainly mobilized civic engagement.

That said, the YouGov poll reveals a potential disconnect between public celebrity endorsements and actual voting behavior. While 46% of respondents thought Harris won the debate, compared to 19% for Trump, only 6% said the debate caused them to reconsider their vote. A substantial 76% of respondents said it did not impact their decision, reflecting a possible gap between high-profile endorsements and tangible voting shifts.

NYC Subway Murders Soar 60% As Nationwide Data Backs Trump On Crime Spike Under Biden-Harris

Murders across New York City’s subway system have surged by a shocking 60% so far this year, even as overall crime on the rails has dipped, leaving straphangers increasingly terrified for their safety.

According to NYPD data, eight people have been slaughtered on subway cars or in stations as of September 8, up from just five during the same period last year. The surge in killings is closing in on the 25-year high set in 2022, which saw ten murders in the transit system—a grim milestone unseen since 1997. For over two decades, from 1997 to 2020, the city never recorded more than five subway murders in a single year, the NY Post reports.

“It’s not a safe environment to be waiting for the train,” said Jakeba Dockery, 42, whose husband, Richard Henderson, was fatally gunned down in January on a 3 train in Brooklyn while trying to break up a fight between riders over loud music. “It just feels evil,” she told The Post.

The latest casualty in the wave of violence was Freddie Weston, a 47-year-old grocer shot dead near the MetroCard booth at the Rockaway Avenue station in Brooklyn on September 5, just after 11 p.m. Weston, who was heading to work in College Point, might still be alive if there had been cameras near the station’s ticketing area, his sister Tina claimed. “They took the opportunity because there wasn’t [any] camera,” she said, her voice cracking.

Despite these horrific incidents, the NYPD points to a slew of high-profile safety initiatives that have helped tamp down an early-year surge in underground crime. Heavily trafficked stations were flooded with 750 National Guardsmen, and an additional 1,000 NYPD officers were deployed to monitor the subway system.

And, indeed, there has been some success: Total subway crime has decreased nearly 6% this year compared with the same period in 2023, with robberies down about 18% and felony assaults dropping nearly 5%, according to an NYPD spokesperson.

“This overall crime reduction is due in large part to thorough investigations by detectives into every major crime within the subway, and the proactive work of officers deployed in the transit system,” the spokesperson said. “This year alone, those very officers removed 43 guns (compared to 28 last year) and 1,536 knives (compared to 1,004 last year) from the subway system, the highest weapons seizure rates in the last decade.”

But even with more weapons off the rails, violent crime remains well above pre-pandemic levels, and many riders are still sweating over whether their next ride will be on the “Murder Express.”

“You don’t know if you’re going to make it home,” retiree Vickie Reeves, 68, bemoaned while making a rare subway trip at the Times Square station. “There’s a lot of mental illness, and it’s painful to your heart that you don’t know who you come in contact with, if they’re going to push you in front of the train.”

Joseph Giacalone, an adjunct professor at John Jay College of Criminal Justice, believes the persistence in murders is partly due to a “worn out” police force and a brain-drain of veteran transit officers, as many cops resign or retire. “You can’t have just anyone patrol the subway — it’s a different animal,” he said.

For Dockery, the widow of the Brooklyn shooting victim, the solution is simple: avoid the subway altogether. She now drives her car around the city – ferrying her daughter to and from high school basketball games and running errands. “I don’t do the MTA,” she said. “Between the anger [of violent straphangers], the mentally ill, I can’t.”

Crime Rates Remain High Across America Under Biden Administration

While New York’s subway system contends with a wave of murders, new national data reveals a troubling trend: crime rates across the United States have remained elevated under President Biden, directly contradicting propaganda spat out by the media and the White House.

According to data from the National Crime Victimization Survey released by the Justice Department on Thursday, 22.5 of every 1,000 residents reported being the victim of a violent crime in 2023, and 102.2 per 1,000 reported experiencing a property crime. Both figures are statistically unchanged from 2022 but are significantly higher than in 2020, the last year under President Trump, the Washington Times reports.

John R. Lott Jr., president of theCrime Prevention Research Center, noted that the data paints a stark picture of rising crime under the Biden administration, contrasting with the drop seen under Trump. “Violent crime increased by 37% under the Biden administration, compared to a drop of 17% under the Trump administration,” Lott said.

The discrepancy in narratives has been a point of contention in political arenas. Mr. Trump’s campaign quickly seized on the new data, stating, “crime rates remain WAY UP under Kamala Harris — throwing a dagger straight through the heart of claims to the contrary by Democrats and their Fake News allies.“

FACT: Violent crime is up 37% between 2020 and last year.

Rape is up 42%.

Robbery is up 63%.

Assault is up 34%.

Violent crime (excluding simple assault) is up 55%.

Domestic violence is up 32%.

Stranger violence is up 61%.

Violent crime (with an injury) is up 10%.

Violent crime (with a weapon) is up 56%.

Motor vehicle theft is up 42%.

FACT: The total number of violent crimes reported last year is higher than any year under President Trump.

FACT: Kamala has overseen the two highest years for total Americans victimized by violent crime since 2012.

FACT: Kamala has presided over three of the four most murderous years in the last quarter century.

FACT: In most cities, murder rates remain higher than pre-pandemic levels.

Meanwhile, the Biden administration and Vice President Kamala Harris’ campaign have cited FBI data to argue that crime rates are falling. However, Lott argues that FBI data is misleading. In 2020, 97% of police departments reported their data to the FBI, but by 2022, 31% were not reporting at all, and another 24% were providing incomplete data.

“Crime is through the roof,” said Trump during last week’s presidential debate. When debate moderator David Muir attempted a fact-check using FBI data suggesting a decrease in violent crime, Trump fired back, questioning the reliability of the data—a sentiment echoed by Lott.

“The victimization data showed significant improvements in several major crimes during the Trump administration. Aggravated assaults fell by 24% under Mr. Trump but rose 55% under Mr. Biden, according to the data for 2023,” Lott continued. “Robbery, which fell 6% under Mr. Trump, is up 63% under Mr. Biden. Rape, which was flat under Mr. Trump, is up 42% under Mr. Biden.”

While the FBI’s homicide data did show a 6.1% drop in homicides from 2021 to 2022, the discrepancy between victimization data and FBI-reported data raises questions about the real state of crime in America. The FBI’s better coverage of homicides, which are almost always reported, is an exception in what Lott calls an increasingly unreliable dataset.

Some experts caution that neither survey alone provides a full picture of crime trends, noting that regional variations can skew national data. But as crime remains a hot-button issue, both in New York’s subways and across the country, the battle over the truth is far from over.

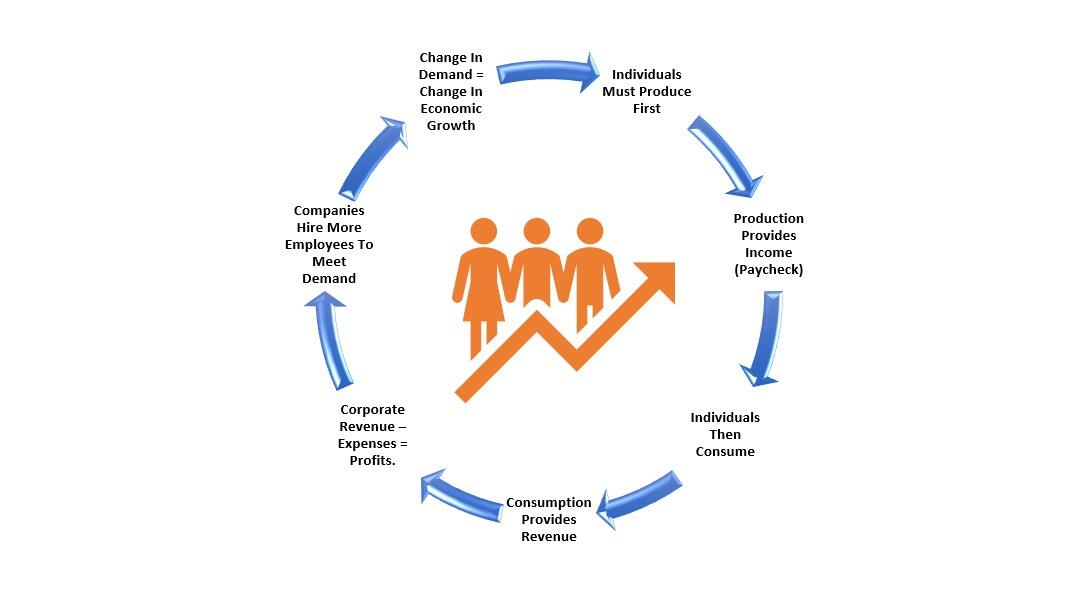

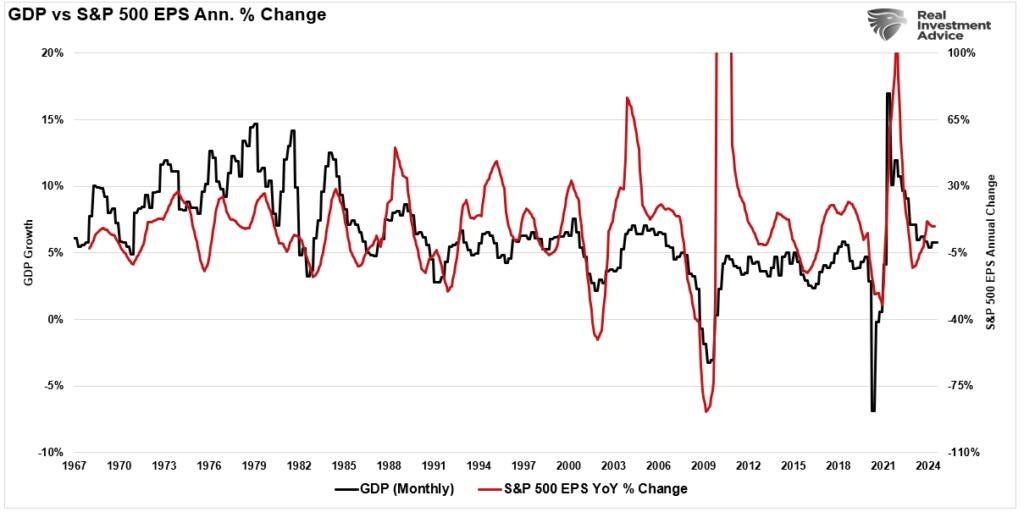

The August jobs report highlighted a critical reality: the labor market is cooling off. While the headline figures seemed decent, the underlying data reveals clear warning signs that worker demand is slowing. Investors should pay attention because the link between employment and its impact on the economy and the market is undeniable. While often overlooked, as we will discuss, there is an undeniable link between economic activity and corporate earnings. Employment is the driver of a consumption-based economy. Consumers must produce first before consuming, so employment is critical to corporate earnings and market valuations. We will discuss these in order.

Slowing Labor Market: The First Red Flag

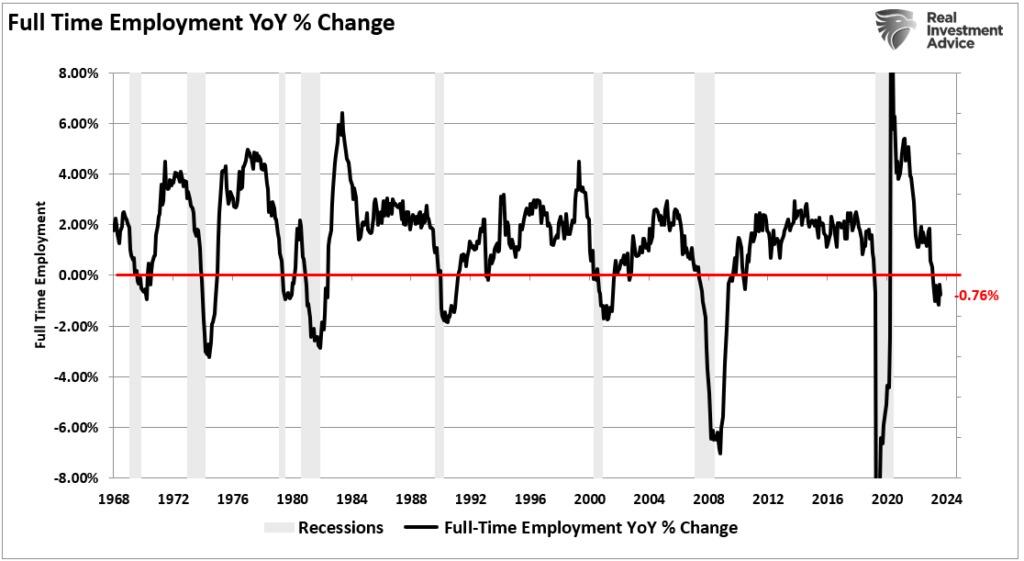

The August jobs report indicated that job creation has slowed dramatically, particularly in crucial manufacturing, retail, and services sectors. For months, we’ve relied on the narrative that a strong labor market could buoy the economy through rough patches. But that narrative quickly falls apart as hiring freezes and job cuts become more common. The data trend is always more critical than the actual employment number. The message is simple: employment is weakening.

However, as discussed in the “Sahm Rule,” full-time employment is a far better measure of the economy than total employment. As noted, the U.S. is a consumption-based economy. Critically, consumers can not consume without producing something first. As such, full-time employment is required for a household to consume at an economically sustainable rate. These jobs provide higher wages, benefits, and health insurance to support a family, whereas part-time jobs do not. It is unsurprising that, historically, when full-time employment declines, a recession typically follows.

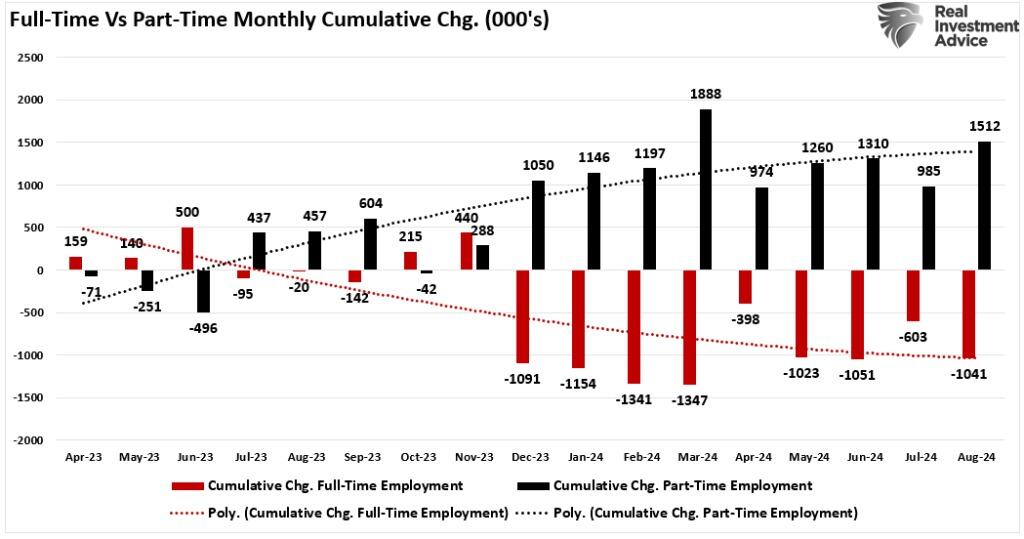

If full-time employment drives economic growth, it is logical that more robust trends in full-time employment are required. However, since 2023, the economy lost more than 1 million full-time jobs versus gaining 1.5 million part-time jobs. That does not scream economic strength.

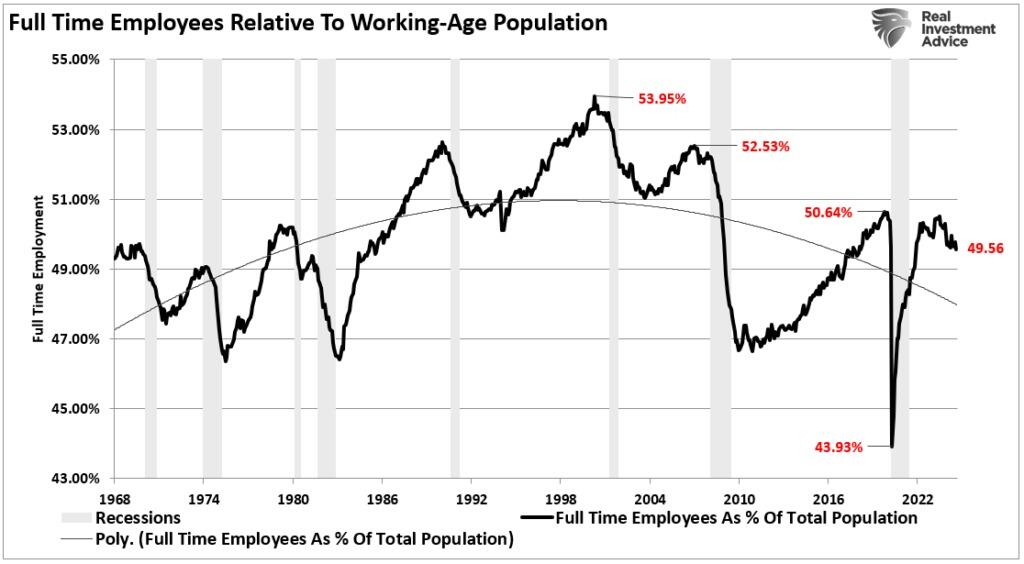

Furthermore, a comparison of full-time employment to the working-age population shows why the U.S. can not sustain annual economic growth rates above 2%.

Since the turn of the century, as the U.S. has increasingly integrated technology and outsourcing to reduce the need for domestic labor, full-time employment has continued to wane. If fewer Americans work full-time, as a percentage of the labor force, the ability to consume at higher rates diminishes as disposable income decreases.

Since corporate earnings depend on economic activity, companies continue to adopt technology and other productivity-enhancing tools to reduce the need for labor. If slower economic demand begins to weigh on corporate profit margins, earnings forecasts will be revised downward in the coming months.

Corporate Earnings Are in Jeopardy

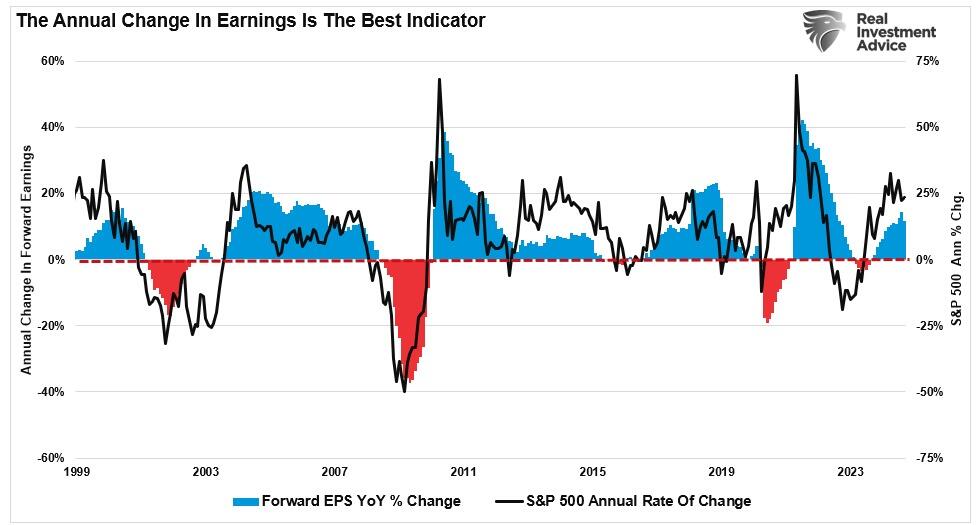

Understanding how a weakeninglabor market translates into weaker earnings is essential. When companies are uncertain about future demand, they stop hiring and look to cut costs. These cost-cutting measures appear in numerous ways, such as layoffs, automation, outsourcing, or increasing temporary hires. Such measures can buy companies some time but don’t solve declining revenues. When fewer people have jobs or wage growth stalls, consumer spending slows down, and that hits the top line for many companies, particularly in consumer-driven sectors. Unsurprisingly, there is a relatively high correlation between the annual change in GDP and corporate earnings.

As such, given that market participants bid up stock prices in anticipation of higher earnings and vice versa, the correlation between the annual change in earnings and market prices is also high.

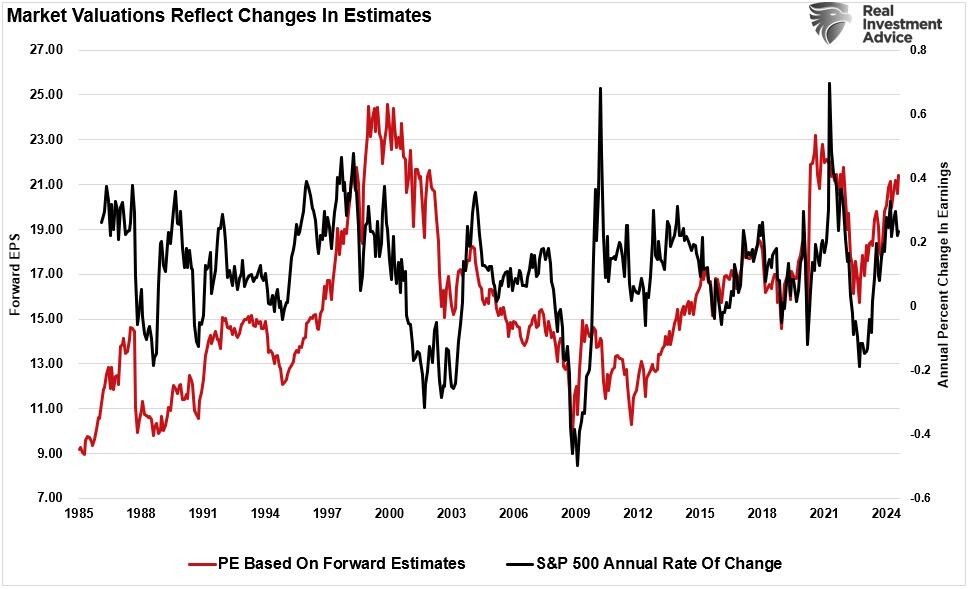

In past economic cycles, we’ve seen how quickly earnings can disappoint when the labor market weakens. Analysts have been overly optimistic about earnings growth, and now the reality of slower consumer demand will force them to adjust their projections. As earnings expectations come down, investors will need to rethink current valuations. This is a straightforward equation—lower earnings lead to lower stock prices as markets reprice current valuations.

Investors should prepare for a slowing labor market’s impact on stock prices. The market is a forward-looking mechanism, and it’s already starting to price in the effects of weaker job growth. Sectors most exposed to consumer spending, such as retail and travel, are likely to see the sharpest declines in stock prices as investors adjust to the reality of softer earnings.

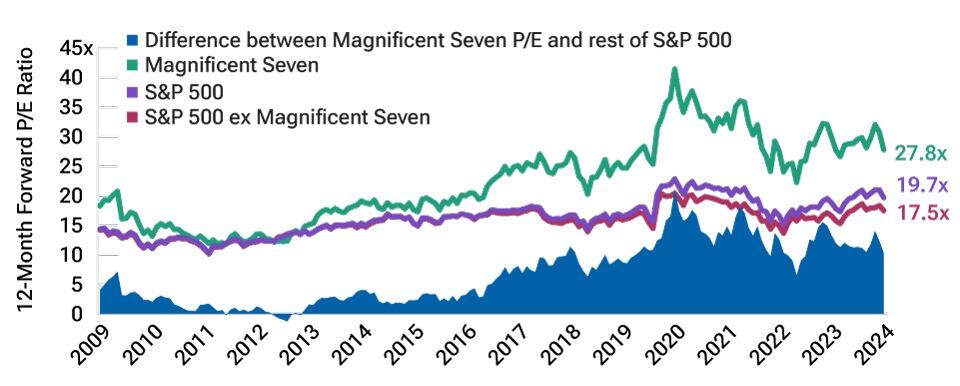

Technology companies, which have driven much of the stock market’s performance this year, will also be vulnerable. These companies rely on high growth expectations to justify their lofty valuations. If the labor market weakens, consumer demand for tech products and services will also fall, leading to earnings misses and stock price declines.

Investor Implications

The broader financial markets are potentially at risk of a “bumpier ride” as the effects of the weakening labor market ripple through the economy. As we’ve seen in previous cycles, investors will begin to move away from riskier assets like stocks and into safer investments such as Treasury bonds. Such a shift could exacerbate market volatility if earnings get revised lower to reflect slower economic activity.

There’s also the question of how the Federal Reserve will respond. A slowing labor market often leads to lower inflation, which might allow the Fed to cut interest rates more aggressively and reverse the current reduction in its balance sheet. However, if inflation remains well above the Fed’s 2% target, despite weaker job growth, the Fed could find its hands tied. A potential market risk is when the Fed gets forced to keep rates elevated while the economy slows. Such would prolong the economic downturn and increase stock price pressure.

Recent employment reports show a clear trend: the labor market is losing momentum. That spells trouble for the economy and the stock market. The slowdown in job creation, coupled with weaker corporate earnings, is setting the stage for increased market volatility.

As noted, with markets still near all-time highs, it is an excellent time to reassess portfolio risk exposures. Rebalancing positions in overvalued growth stocks and shifting toward more defensive assets could be prudent. As we have often said, capital preservation should be the priority in times of uncertainty. The labor marketindicates that uncertain times are ahead, and investors should prepare accordingly.

Welcome Back To Planet Earth: SpaceX Polaris Dawn Crew Returns After Historic Spacewalk Mission

The five-day Polaris Dawn mission, operated by Elon Musk’s SpaceX, ended early Sunday as the Crew Dragon capsule safely splashed down off the coast of Florida. The mission, hailed as a massive success, featured the world’s first commercial spacewalk with astronauts traveling further into space than any humans for more than half a century and marked a breakthrough in testing inter-satellite laser communication through SpaceX’s Starlink network.

The Crew Dragon capsule carrying four astronauts, including billionaire entrepreneur Jared Isaacman, SpaceX engineer Sarah Gillis, and two others, splashed down off the coast of Dry Tortugas, Florida, around 0337 ET.

The mission’s top focus was testing SpaceX’s most advanced spacesuits at an apogee – or farthest point from Earth – than any human has traveled since NASA’s Apollo Program ended in 1972. Astronauts Isaacman and Gillis exited the spacecraft for ten minutes each to test the new suits.

The inter-satellite laser communication between the Dragon Spacecraft and SpaceX’s Starlink satellite constellation was also successfully tested during the mission.

Looking ahead, Musk revealed one week ago that the Starship mega rocket will begin flying Mars missions in two years when the next Earth-Mars transfer window opens. The mission will be uncrewed to test the rocket’s ability to land intact on the Red Planet.

Democrats are fuming over SpaceX’s space successes, while Boeing’s Starship and Jeff Bezos’ Blue Origin are light-years behind Musk.

So far, the Biden administration has not congratulated Musk on Polaris Dawn’s push to advance humanity toward becoming a multi-planetary species because of politics.

Last week, Metals Focus attended the China Silver and Photovoltaic Industry Chain Seminar in Wuxi. During this event, our research consultant, Elvis Chou, presented on the outlook for the silver market, including the photovoltaic (PV) sector.

As has been widely reported, the PV market has undergone substantial changes over the past decade, with the industry’s expansion significantly boosting demand for silver.

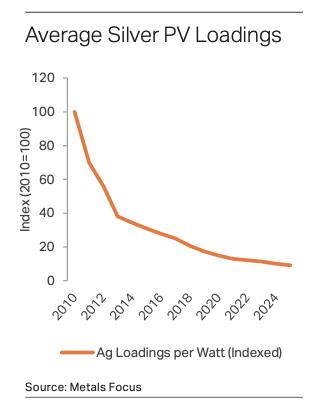

As a reminder, in World Silver Survey 2024 Metals Focus reported a 64% y/y surge in silver PV offtake to a record total of 6,017t (193Moz). However, with technological progress and market fluctuations, it is important to examine if this trend will continue, or if new dynamics will emerge, laying out a different path for this sector.

Following the dramatic surge in installed capacity over the last two years, which reached 444GW last year against 182GW in 2021, the PV sector has achieved a substantial base level of demand.

However, taking into account several developments, including global cuts in solar energy bid prices, increased financing costs, fewer government subsidy projects, and diminishing investment returns, it is widely anticipated that the industry’s expansion will start to moderate.

That said, the H1 performance indicates that, except for Europe, solar installations in other major markets, including China, India, the US, the Middle East and Africa, all increased, reflecting a positive trend in solar adoption across these locations.

However, what also emerged were indications of a somewhat slower pace of installations as the first half progressed. This prompted an immediate reaction from the supply chain, which initially scaled back production and has continued to manage output in Q3.

As a result, this quarter is experiencing a slower-than-expected peak season, which in turn has introduced some uncertainty in trying to project demand for the latter half of the year. The somewhat cautious outlook for PV demand in the coming months has also intensified competition within the supply chain, which is already dealing with surplus capacity, resulting in weaker module prices.

For instance, in China in Q3.23 the bidding price (how much the government pays for power from a new project) was RMB 1.6-1.7 per watt, but this has plummeted to RMB 0.7 per watt this September. This means that most panel and module manufacturers are now losing money. To help address this these companies are increasingly focusing on enhancing product efficiency and reducing costs.

As part of this strategy, N-type solar cells (which covers TopCon and HJT), known for their superior efficiency, have emerged as the market’s dominant technology this year (as widely expected). The initial market perception was that, with the increasing popularity of N-type cells, the growth in silver consumption would exceed that of installations, due to their higher silver loadings compared to P-type cells, like PERC.

Contrary to these expectations, our field research revealed that Chinese producers have made more progress in thrifting and substitution than previously anticipated. Since the beginning of this year, each quarter the industry has reduced the amount of silver paste that is applied to a panel by roughly 4-5% compared with the previous quarter.

This has been achieved through a series of improvements, notably: upgrading production processes to increase efficiencies and shrink line width by introducing Laser Enhance Contact Optimisation (LECO); optimising the structural design by transitioning from Super Multi-BusBar (SMBB) to Zero-BusBar (0BB) conductive lines, and introducing some silver coated copper powder.

As a result, we expect silver usage per watt to drop by 10-15% y/y in 2024. And so, with this cost-cutting roadmap in place, leading panel and module producers have effectively reduced the proportion of silver as a share of the total module cost to less than 10%. This in turn has helped to cushion the effects of elevated and volatile silver prices.

Additionally, to protect themselves against further gains in the silver price, these companies are looking to implement further cost reductions well into 2025.

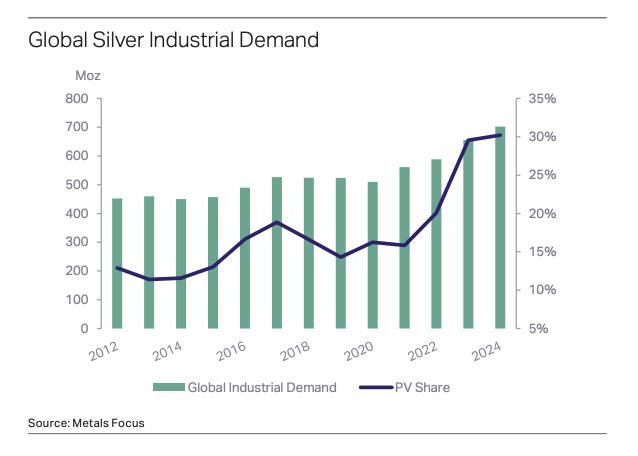

As the single largest application for silver in the industrial sector, accounting for more than 30% of global silver industrial offtake, PV has had a profound impact on global silver supply chains.

Despite the above headwinds, we still expect the sector to consume around 6,600t (212Moz) of silver this year, a new high. Considering the huge potential for expansion in the green energy space, we believe that solar energy will remain pivotal in the industrial silver market in the coming years.

However, the worldwide deployment of solar systems is encountering several obstacles that could hinder its growth, including the capacity of the underlying power grid, the impact of land utilization, and challenges associated with panel recycling.

Therefore, as newly added capacity broadly stabilizes, albeit at record highs, further cuts to silver loadings may exceed the growth rate of installations, potentially leading to a slightly softer trend in total silver consumption. Even so, this should not detract from the fact that silver PV demand will remain historically high and so retain its position as the largest single end-use of global silver industrial demand.

Metals Focus is a London-based independent precious metals consultancy specializing in gold, silver, platinum, palladium, and rhodium markets. They offer research, consultancy, and bespoke services, producing reports like Precious Metals Weekly and World Silver Survey. Their global team spans key markets, including the UK, Singapore, Mumbai, and Shanghai, providing industry insights for professionals, investors, and governments.

Navient, once the largest student loan servicer in the United States, has been permanently barred from federal student loan servicing and ordered to pay a $120 million settlement following years of alleged regulatory and legal violations.

The Consumer Financial Protection Bureau (CFPB) announced the proposed order against the servicer formerly known as Sallie Mae on Sept. 12. In 2017, the company at one point serviced loans of more than 12 million borrowers, half of which were accounts under its contract with the Department of Education, accounting for more than $300 billion in federal and private student loans.

The CFPB estimates that hundreds of thousands of consumers may be eligible for redress in the settlement, but the agency has not yet determined a precise number of consumers, or the amount each individual will receive.

The CFPB will identify consumers who are eligible for redress under the order in the coming months. There is no need for consumers to contact the CFPB or take any other action to get a check, and eligible consumers will receive a check from the CFPB or its contractor in the mail, the agency said.

“For years, Navient’s top executives profited handsomely by exploiting students and taxpayers,” CFPB director Rohit Chopra said in a statement. “By banning the notorious student loan giant from federal student loan servicing and ensuring the wind-down of these operations, the CFPB will finally put an end to the years of abuse.”

The settlement stems from CFPB’s 2017 lawsuit against Navient. The lawsuit accused the company of steering student loan borrowers into costly repayment options, depriving them of more affordable income-driven repayment plans, and engaging in other unlawful practices.

The order, which is pending court approval, would impose a permanent ban on Navient’s involvement in servicing federal direct loans and prohibit the company from acquiring most loans under the Federal Family Education Loan Program (FFELP).

Under the terms of the settlement, Navient will pay a $20 million penalty and provide $100 million in redress to borrowers harmed by its practices.

This includes compensation for borrowers who were allegedly steered into forbearance—a practice that allowed Navient to avoid the more complex process of enrolling borrowers in income-driven repayment plans but led to increased interest charges for many.

According to the CFPB, these actions resulted in numerous borrowers paying significantly more than they should have.

The settlement represents what CFPB said is a broader effort by state and federal agencies to hold loan servicers accountable for their role in steering borrowers into forbearance and other harmful repayment strategies.

U.S. Under Secretary of Education James Kvaal praised the CFPB’s action, stating, “I applaud the CFPB for obtaining concrete relief for borrowers and deterring similar failures in the future.”

In recent years, Navient has been at the center of several legal battles, including a 2014 case in which it was ordered to pay nearly $100 million for overcharging servicemembers, and a 2022 settlement with 39 state attorneys general for $1.85 billion over its alleged predatory lending practices.

In response to the CFPB’s latest enforcement action, Navient issued a statement saying that while the company disagrees with the allegations, the resolution is consistent with its plans to move forward.

“This agreement puts these decade-old issues behind us,” Navient said. “Navient is no longer a servicer or purchaser of federal student loans.”

The company ceased servicing federal direct loans in 2021, transferring its remaining loans to a third-party servicer, it said in the statement.

Earlier this year, Navient also outsourced the servicing of its legacy FFELP student loans. The CFPB’s order ensures that Navient can no longer directly service federal student loans or expand its FFELP portfolio.

In addition to the financial settlement, the order mandates that Navient take several steps to protect borrowers’ rights, including ensuring that they can enroll in affordable repayment plans.

The CFPB will distribute checks to affected borrowers, cautioning them to remain vigilant against scammers who may attempt to exploit the redress process.

The CFPB also will identify injured consumers who will receive redress for Navient’s forbearance steering practices and Navient’s furnishing of inaccurate information for consumers who had their loans discharged due to a total and permanent disability. For the forbearance steering claims, these determinations may take into account the length of time the borrower was enrolled in forbearance, among other criteria, the agency said.