November Weekend Surprises

By Benjamin Picton, senior macro strategist at Rabobank

Election day looms and market pricing has tightened substantially for Kamala Harris. Prediction markets which had recorded leads of more than 30pts for Donald Trump this time last week now have that lead down to single digits. In the case of PredictIt, Kamala Harris is now narrowly favoured to win, although on Polymarket Trump’s lead has returned.

On top of the dramatic tightening in prediction markets, we have also seen some curious polling results in the final days of the campaign. A NYT/Sienna poll found Vice President Harris leading in North Carolina and Georgia, while Donald Trump closed the gap in Pennsylvania and remained well ahead in Arizona. AtlasIntel found that Donald Trump leads in every swing state, including Georgia and North Carolina, and Rasmussen found that Trump has a 3-point lead in their national polling! Meanwhile, Ann Selzer published a poll showing Kamala Harris leading 47-44 in Iowa, which raised plenty of eyebrows given the state’s reputation as a Republican stronghold and Selzer’s strong reputation for the accuracy of her predictions.

Political genius Ann Selzer appears confused over what the “R” and “D” letters refer to in polling cross tabs pic.twitter.com/R7iADsusbT

— Tom Elliott (@tomselliott) November 3, 2024

Given the variability and contradictory nature of these recent results, it might be best to adopt the Nate Silver perspective of “we just don’t know who is going to win”. Silver has recently suggested that pollsters have been “herding” by publishing a lot of polls showing a statistical tie. Silver says that the probability of that many polls turning up that result (even if it is accurate) is infinitesimally small, so there’s some funny business going on. Silver himself has the election as a virtual coinflip, though he does award a slight edge to Trump, while RealClearPolitics also has Trump ahead in a very tight race.

Two days out, President Trump’s chances to win from…

Nate Silver: 52.6%

FiveThirtyEight: 53%

DecisionDeskHQ: 54%

The Economist: 51%VOTE, VOTE, VOTE! pic.twitter.com/SJsSE0iZzd

— Jake Schneider (@jacobkschneider) November 4, 2024

Nevertheless, if the published polls that serve as inputs to these models really are herding, we might be headed for a more decisive result that the polling figures have been suggesting. Could the rapid tightening in betting markets be a head-fake?

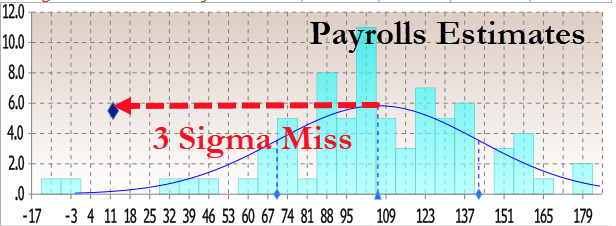

While attention has been understandably focused on the US election, October non-farm payrolls printed at just 12,000 on Friday evening. This was a big miss compared to the median estimate of 100,000 on the Bloomberg survey, which was already a low figure to account for the effects of Hurricanes Helene and Milton.

Two surveyed analysts actually predicted a worse number, but the end result was still almost 3 standard deviations from the median, suggesting that it came as a bit of a shock to the economics profession at large. That probably shouldn’t have been the case given that the September JOLTS report released earlier in the week showed the total number of job openings was more than 100,000 below even the most pessimistic forecast in the Bloomberg survey. Perhaps its time for analysts to revise their Beveridge Curve models?

Private payrolls declined by 28,000 and manufacturing payrolls were down by 46,000, suggesting that the market economy is in retreat and the sacred cow of good manufacturing jobs is looking a little shaky, despite bipartisan efforts to amp up protectionism over the last 7.5 years. The two-month revision to net employment was -112,000 (continuing the run of job gains being given away in subsequent downward revisions) and participation dropped by a tenth of a percentage point to keep the unemployment rate constant at 4.1%. All things considered, this looks to be the worst jobs report of the Biden Presidency arriving just days out from the beginning of his lame-duck period.

Back in May of this year Jerome Powell said that he didn’t “see the stag’ or the ‘flation” in the US economy, but it looks like the stag might be getting a little easier to spot. Our own US analyst Philip Marey has been suggesting that the Fed would be cutting rates this year not because the inflation fight had been won (core PCE printed at 2.7% YoY last week), but because the Fed would be getting worried about the shape of the jobs market and the outlook for future growth. Powell and Co starting the easing cycle with a 50bps bang in September and saying that they did not want to see further deterioration in the labour market seems to suggest that Philip was on the money

OIS futures are now pricing in an extra 4bps of cuts to the Fed Funds rate in 2024 compared to this time last week. A 25bps cut from the FOMC later this week is 98.5% priced into the futures, but a follow up cut in December is slightly less assured. Powell himself issued forward guidance to suggest that 25bps cuts at each meeting was the base case, but a few Fed speakers since then have intimated that the Fed might skip cutting at one of the two remaining meetings in 2024.

While the short end of the curve parsed the vagaries of employment data and Fed talking points to fine-tune rate cut expectations, long end yields continued to march higher last week. The US 10-year finished the week more than 14bps higher, but comments from Iranian Supreme Leader Khomeini over the weekend might temper some of the selloff.

Khomeini said that Iran would deliver a “crushing response” to recent Israeli strikes on Iranian military targets. The Wall Street Journal reports that Iranian attacks would not occur before the US elections, but would take place before the next President can be inaugurated and would not be limited to missiles and drones, as the two previous strikes were. This leaves Joe Biden in the hotseat to coordinate a response with an expired electoral mandate, and Israel in the position where a strike on Iranian oil or nuclear assets may again need to be countenanced given that Iran doesn’t seem to be getting the message.

Oil prices are up a little more than $1/bbl since the close on Friday. This is likely due to a combination of factors, including the Khomeini speech and news from OPEC+ that the 180,000 bb/day production cuts due to expire in December will be extended for at least one more month. RaboResearch’s energy analysts see the global crude oil market in a state of oversupply over the remainder of 2024 and into 2025. Our expectation is therefore for risk rallies to remain capped by the laws of arithmetic in the absence of supply interruptions. Having said that, it would be a brave trader who shorts this market as it would only take a few Israeli missiles headed toward Kharg Island to change the calculus completely.

Tyler Durden

Mon, 11/04/2024 – 10:25

via ZeroHedge News https://ift.tt/ji4dr19 Tyler Durden