Futures Flat As Geopolitical Tensions Offset Latest China Stimulus Vows

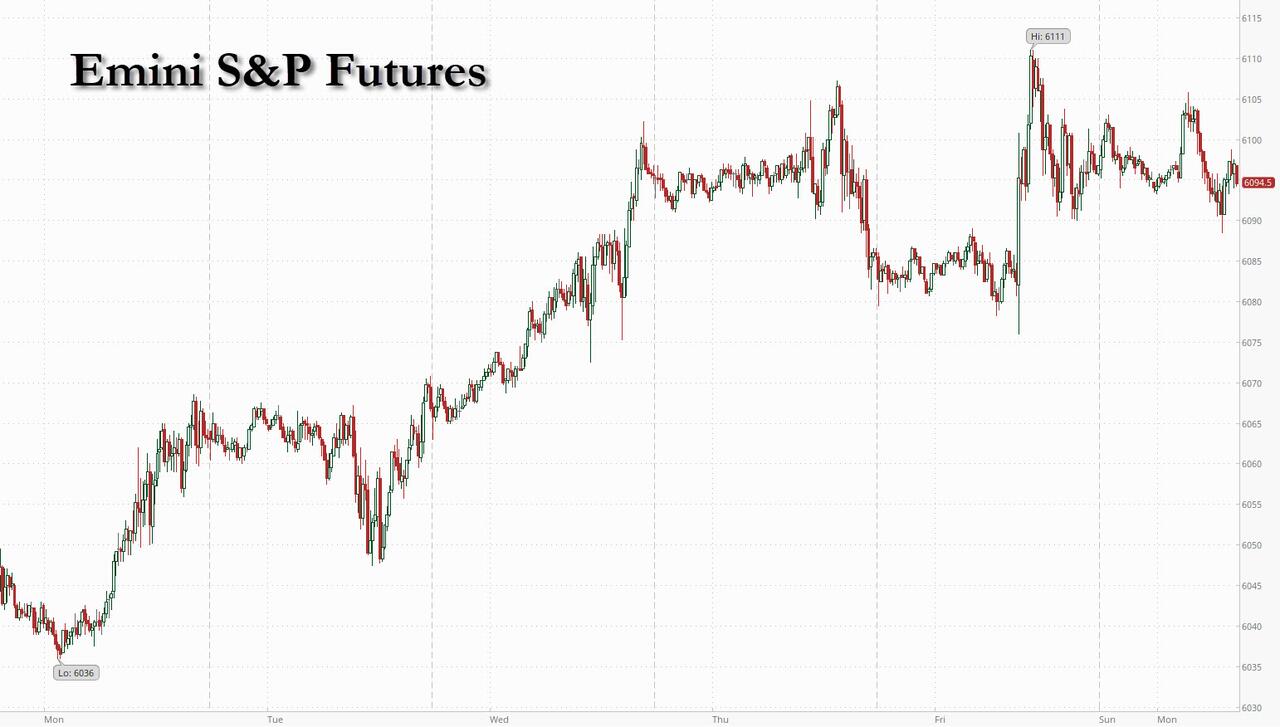

S&P futures are flat after hitting a fresh record highs on Friday and ceding brief gains sparked by China’s monetary-policy shift, as investors focused on an upsurge in geopolitical risk and the outlook for interest-rate cuts in the US and other major economies. As of 8:00am, S&P futures dipped 0.1% and Nasdaq 100 futs were down 0.2% after rising earlier following China’s announcement that authorities will embrace a “moderately loose” strategy next year. More steps on the fiscal side could be unveiled at Wednesday’s Central Economic Work Conference. While Beijing’s pledge boosted Asian markets and supported US-listed Chinese shares in premarket trading, gains elsewhere were short-lived with South Korean stocks plunging as the political crisis deepened. Pre-mkt, Mag7 is mixed while bond yields are flat to up 2bps. the Bloomberg dollar index is flat even as the yen tumbles as hopes that the BOJ will hike in December once again crumble. Commodities are stronger, led by energy and base metals, as moves are being driven by the positive stimulus news from China. As the Fed enters its blackout window, the key macro data points are CPI/PPI, though it would take a tail-risk type of print to move the Fed away from cutting next.

US premarket gainers included Apollo Global (APO) and Workday (WDAY) as the stocks are set to replace Qorvo and Amentum in the S&P 500 Index. Apollo +6%, Workday +9%. Super Micro Computer gained 8% after the embattled server maker said Nasdaq had granted the firm more time to become compliant with listing rules. To the downside, Nvidia slipped premarket on news of a probe in China over suspicions the the AI chipmaker broke anti-monopoly laws. Here are the other notable premarket movers:

- Alibaba (BABA) rises 6% along with other Chinese stocks listed in the US after the country’s top leaders provided a sign of further stimulus ahead. Baidu (BIDU) +5%, PDD (PDD) +8%

- Arcellx (ACLX) rises 6% after the drug developer gave data from a mid-stage trial of its experimental therapy for a form of blood cancer, which Baird says appears to support “best-in-class” efficacy for the drug.

- BioAge Labs (BIOA) sinks 69% following news late Friday that the clinical-stage biopharmaceutical company is halting a Phase-2 trial evaluating its azelaprag drug for the treatment of obesity.

- Interpublic (IPG) jumps 13% after the Wall Street Journal reported that Omnicom is in advanced talks to buy the advertising and marketing company.

- Macy’s (M) rises 2% after the Wall Street Journal reported that activist investor Barington Capital has built a position in the department-store operator and plans to push for changes, including the establishment of a separate real estate unit.

- Nvidia (NVDA) slips 1% as China has opened a probe into the company over suspicions that the US chipmaker has broken anti-monopoly laws.

- Reddit (RDDT) rises 5% after a Morgan Stanley analyst admits he missed the boat on the company’s huge post-initial public offering gains. Yet he feels there’s still time to jump aboard.

In a desperate attempt to once again jawbone the markets higher, China’s top leaders doubled down on what they did in September, and signaled bolder economic support next year using their most direct language on stimulus in years, as Beijing braces for a trade war when Donald Trump takes office. President Xi Jinping’s decision-making Politburo vowed to embrace a “moderately loose” monetary policy in 2025, signaling more rate cuts ahead and shifting from a “prudent” strategy that’s held for 14 years, although following the huge disappointment that was the September fiscal stimulus “bazooka”, traders quickly took profit on the meager gains demanding deeds not words.

“The somewhat looser monetary policy stance by the Politburo is welcome news, though it won’t materially change the situation for the Chinese economy,” said Joachim Klement, head of strategy, economics and ESG at Panmure Liberum. “What is needed is substantially more fiscal stimulus that is supported by a looser monetary policy.”

Elsewhere, crude oil as well as gold prices rose after the toppling of Bashar al-Assad’s regime in Syria unsettled an already restive Middle East. South Korea also risks prolonged political impasse, with opposition lawmakers pushing for another impeachment vote on President Yoon Suk Yeol. That saw Korean markets extending declines, sparking fresh selling in crypto, while the won fell about 1% against the dollar.

Amid the geopolitical turmoil, investors will turn their attention to this week’s central bank meetings. The ECB meeting for the first time since the collapse of governments in Paris and Berlin, is expected to cut interest rates, as are the Bank of Canada and the Swiss National Bank. Australia’s central bank will likely keep rates on hold. US inflation data will be another key event, potentially determining whether the Federal Reserve eases policy again at its Dec. 18 meeting. While the November jobs report indicated on Friday that the labor market is cooling enough to allow a rate cut, the inflation print could heighten uncertainty, should it show price pressures accelerating last month by more than the 0.3% forecast in a survey.

“Inflation remains too high regardless, which has been limiting the central bank’s ability to loosen monetary policy,” Daniela Sabin Hathorn, a senior market analyst at Capital.com. told clients in a note. “The current odds show an 87% chance of a 25-bps cut next week, but this could quickly change if the CPI data does not come in as expected.”

European stocks and US equity futures also initially rallied on the China news but have now retreated from the day’s highs though sectors exposed to China, including miners and consumer products, advanced. Among individual stock movers, Turkish construction-related stocks such as Oyak Cimento Fabrikalari AS and Cimsa Cimento Sanayi VE surged as investors bet the companies will play a role in Syria’s reconstruction. Here are the biggest movers Monday:

- Europe’s basic resources sector leads gains in the Stoxx 600 benchmark rising as much as 2.9% as copper and iron rise as China’s top leadership announced they would embrace a “moderately loose” monetary policy next year, the first shift in stance since 2011

- BASF gains as much as 3.7%, the most in a month, following an upgrade to buy from hold at Warburg which says “not all is doom and gloom” for the German chemicals firm

- Banco BPM rises as much as 3.9% in Milan trading after Credit Agricole raised its stake in Italy’s third-largest bank, a move aimed at defending its interests in the country

- CompuGroup shares jump as much as 31%, to €21.64, after CVC made a voluntary public takeover offer for the German software company at €22 per share

- Pharming gains as much as 10%, the most since October 2023 after Jefferies initiated buy citing that the current valuation as failing to reflect potential from two rare disease drugs

- HelloFresh shares drop as much as 8.2%, a move that Jefferies analyst Giles Thorne describes as “unjust” after a report that the US Labor Department is investigating allegations concerning the use of child labor at a cooking and packaging facility in Illinois

- DocMorris shares fall nearly 5% after Zuercher Kantonalbank cut its recommendation on the Swiss pharmaceutical products retailer to market perform from outperform, citing a liquidity shortage

- European defense shares fall after Ukrainian President Volodymyr Zelenskiy described talks with US President-elect Donald Trump and French President Emmanuel Macron as “good and productive” in a social media post

Earlier in the session, Asian equities advanced as stocks in Hong Kong staged a late rally after Beijing pledged to support growth. Shares in South Korea continued to drop amid a deepening political crisis. The MSCI Asia Pacific Index rose as much as 0.4%, after trading in a narrow range earlier in the day. TSMC and Alibaba were among the biggest boosts to the regional gauge. Chinese stocks listed in Hong Kong rebounded in the final hour of trading after the nation’s top leaders vowed to ease monetary policy and expand fiscal spending. The Hang Seng China Enterprises Index reversed a small drop to end the day 3.1% higher, it’s biggest gain since Oct. 18. The Politburo said it will embrace a “moderately loose” strategy for monetary policy in 2025, marking its first major shift in stance since 2011, and also pledged to “stabilize property and stock markets.” “The wording in this politburo meeting statement is unprecedented,” said Zhaopeng Xing, senior China strategist at ANZ Bank China Co Ltd. “We think the commentary points to strong fiscal expansion, big rate cut and asset buying. The policy tone shows strong confidence.”

Meanwhile, Korea’s benchmark Kospi dropped more than 2% amid the risk of a prolonged stalemate after Saturday’s impeachment motion against President Yoon Suk Yeol failed. The ongoing drama has complicated the government’s efforts to reform corporate governance and eradicate the perennial undervaluation of the nation’s equities.

In FX, the Bloomberg dollar spot index is down. JPY and CHF are the weakest performers in G-10 FX, AUD and NZD outperform. The offshore yuan and commodities climbed after China’s top leaders announced they plan to loosen monetary policy and expand fiscal spending next year.

In rates, Treasuries are narrowly mixed with the yield curve steeper, unwinding a portion of Friday’s rally sparked by November jobs data. Long-end yields are ~2bp cheaper on the day, with 2s10s, 5s30s spreads steeper by 1bp-2bp near session wides. 10-year is around 4.165%, lagging bunds and gilts in the sector by 1.5bp and 3bp.

In commodities, oil gained as the market weighed the fallout from the toppling of the Syrian government, which dealt a blow to longtime backers Russia and Iran. WTI trades within Friday’s range, adding 1.4% to near $68.12. Spot gold rises roughly $24 to trade near $2,657/oz. Spot silver gains 1.5% near $31.

Bitcoin dropped below the 100k mark, to a current session trough of USD 98,274, following a rout in Korean shares as Korean momentum traders liquidated positions to fund stock margin calls. Since Donald Trump became president-elect, nearly USD 10bln has flowed into US ETFs that invest directly in Bitcoin (BTC), Bloomberg reports. This surge in investment is driven by optimism that Trump’s crypto-friendly policies will fuel market growth. The funds now total approximately USD 113bln, BBG added.

Looking at today’s calendar, US economic data calendar includes October wholesale inventories (10am) and November New York Fed 1-year inflation expectations (11am). Fed officials are in self-imposed quiet period ahead of their Dec. 18 Fed policy announcement. This week’s risk events include CPI and PPI reports and coupon auctions beginning Tuesday.

Market Snapshot

S&P 500 futures little changed at 6,098.00

Brent Futures up 1.0% to $71.85/bbl

Gold spot up 0.8% to $2,653.38

US Dollar Index down 0.13% to 105.91

Top Overnight News

- Trump announces Michael Needham will serve as Counsellor of the Department of State, and Christopher Landau to serve as Deputy Secretary of State, via Truth Social.

- Trump aides reportedly contacted Google (GOOG), Meta (META), and Snap (SNAP) over online drug sales, according to The Information.

- Donald Trump told NBC that he has no plans to replace Jerome Powell as Fed chair. He also said he had an exchange with Xi Jinping in recent days, without elaborating. BBG

- China will adopt an “appropriately loose” monetary policy next year, the first easing of its stance in some 14 years, alongside a more proactive fiscal policy to spur

- economic growth. RTRS

- Chinese state media said the country has room to increase its borrowing and fiscal deficit in 2025 as investors closely watch to see whether Beijing would use its fiscal firepower to increase stimulus in its key economic meeting next week. BBG

- China’s CPI for Nov fell short of expectations at +0.2% Y/Y (down from +0.3% in Oct and below the consensus of +0.4%) while the PPI deflation eased modestly to -2.5% (vs. -2.9% in Oct and a bit better than the -2.8% consensus). BBG

- South Korea banned President Yoon Suk Yeol from leaving the country as the political crisis deepened. The won fell and the Kospi closed lower, shedding more than 5% since the botched martial law declaration. BBG

- Israel moves to occupy a buffer zone in Syria and launches air strikes against chemical weapons depots as the government looks to reduce the risk of fallout from the Assad downfall. WSJ

- US strikes Islamic State targets in Syria and is monitoring Assad weapons stockpiles to prevent them from falling into the wrong hands. Axios

- Interpublic shares jumped premarket after the WSJ reported Omnicom is in advanced talks to buy the advertising and marketing firm. BBG

- APO (Apollo) and WDAY (Workday) will join the S&P 500 prior to the open of trading on Mon 12/23. BBG

A more detailed look at global markets courtesy of Newsquawk

Top Asian News

European bourses began the session entirely in the green, with sentiment in the region lifted following the readout from the Chinese Politburo meeting. On that, it noted that China’s fiscal policy is to be more proactive next year and that monetary policy is to be moderately loose. Since, some indices have given back initial gains and slipped into negative territory to display a mixed picture in Europe. European sectors began the European session with a strong positive bias, given the risk-on sentiment vs a current mixed picture. Unsurprisingly, the China-exposed sectors top the pile following the Chinese Politburo meeting; Consumer Products topped the pile, followed closely by Basic Resources. Real Estate is found at the foot of the pile. US equity futures are mixed vs with the initial readout from the Chinese Politburo meeting sparking some modest upside in the price action; upside which has since faded.

Top European News

- Fitch affirmed Hungary at “BBB”, revised outlook to “Stable” from “Negative”

FX

- USD is showing a mixed performance vs. peers (weaker vs. cyclicals, stronger vs. havens). US President-elect Trump over the weekend said he has no plans to remove Powell and said he cannot guarantee Americans will not pay more as a result of tariffs. DXY briefly breached Friday’s high at 106.15 before fading upside and slipping back onto a 105 handle.

- EUR is incrementally firmer against the USD and off worst levels. Focus for the Eurozone this week is on events in Frankfurt with the ECB set to pull the trigger on a 25bps cut. After struggling to hold above 1.06 post-NFP, EUR/USD remains stuck on a 1.05 handle, just above the 1.0550 mark.

- JPY, along with CHF is lagging across the majors as news out of China has triggered a pick-up in sentiment and subsequently weighed on havens. For Japan specifically, focus overnight was on an upward revision to Q3 GDP. USD/JPY is back on a 150 handle with the pair now showing a great deal of direction over the past few sessions.

- GBP is slightly firmer in what has been a catalyst-thin session for the Pound thus far. As such, it is possible that the USD leg of the equation will do the heavy lifting for the pair. Cable has gained a firmer footing on a 1.27 handle.

- Antipodeans are both at the top of the G10 leaderboard following positive commentary out of China in which the Politburo noted that fiscal policy is to be more proactive next year, whilst monetary policy is to be moderately loose. AUD/USD has reclaimed the 0.64 mark but is below Friday’s 0.6455 high. RBA is expected to deliver an unchanged decision on Tuesday.

- PBoC set USD/CNY mid-point at 7.1870 vs exp. 7.2627 (prev. 7.1848)

Fixed Income

- Mar’25 UST contract is a touch lower after pulling back from highs after positive commentary from the Chinese Politburo which noted that fiscal policy is to be more proactive next year, whilst monetary policy is to be moderately loose; first shift in monetary policy since 2011. The main focus this week will be on US CPI on Wednesday. Mar’25 UST is currently tucked within Friday’s 110.28+ to 111.20+ range.

- European paper is a touch higher but off best levels following updates out of China. For the Eurozone this week, focus will largely be on the ECB’s rate decision which is expected to see the GC deliver a 25bps rate cut with policymakers refraining from publicly backing a 50bps move ahead of the meeting. Bunds are currently holding above the 136 mark and within Friday’s 135.94-136.52 range, with the corresponding 10yr yield back above 2.1%.

- Gilts are marginally higher after moving sideways for the past few sessions. As has been the case for the past several sessions, fresh UK drivers have been lacking. BoE’s Ramsden is due later today. As it stands, the Mar’25 Gilt contract has met resistance at 96.00 with the corresponding 10yr yield holding above 4.25%.

- Amundi tactically downgrades core European Fixed Income to Neutral.

Commodities

- WTI and Brent began the European session on a slightly firmer footing, with the complex lifted amid geopolitical uncertainty in the Middle Eastern region after Syrian fighters toppled the Assad regime. Just ahead of the European cash open, the Chinese Politburo meeting sparked considerable upside in the oil complex, with Brent’Jan 25 rising to a session peak of USD 72.15/bbl.

- In a similar vein to the above, spot gold began the European session on a firmer footing with sentiment lifted amid the geopolitical uncertainty in the Middle Eastern region. Alongside this, Reuters reported that the PBoC resumed gold purchases in November after a six-month hiatus. Upside was also seen following the Politburo release. XAU currently sits at the upper end of a USD 2,627.62-2,651.22/oz range, and just shy of its 50 DMA at 2,667.96/oz.

- Base metals were mixed overnight, with copper initially benefiting from the better-than-feared Chinese PPI figures; thereafter the red-metal moved lower in tandem with a pick-up in the Dollar. After that, metals jumped to session highs following the Chinese Politburo meeting.

- Saudi Arabia set January Arab Light crude OSP to Asia at +USD 0.90 vs Oman/Dubai average (prev. +USD 1.70); NW Europe at -USD 1.25 vs ICE Brent (prev. -0.15); United States at +USD 3.80 vs ASCI (prev. +USD 3.80), according to Reuters.

- Polish pipeline operator Pern said it has restored proper operation of first branch of Western Druzhba pipeline after incident on December 1st, according to Reuters.

- PBoC resumed gold purchases in November after a six-month hiatus, according to Reuters.

Geopolitics: Middle East

- Israel says it struck suspected chemical weapons sites and long-range rockets in Syria in order to prevent them from falling into the hands of hostile actors, according to Guy Elster.

- Syrian rebel fighters captured the capital Damascus and toppled Bashar al-Assad’s regime.

- Syria’s ousted President Bashar al Assad has arrived in Moscow, according Russian state media. Kremlin sources suggested a deal has been done to ensure the safety of Russian military bases in Syria, according to Reuters.

- Israeli ground forces advanced beyond the demilitarized zone on the Israel-Syria border over the weekend, “marking their first overt entry into Syrian territory since the 1973 October War”, according to Israeli officials cited by NYT

- IDF called Syria ‘fourth front’, according to Sky News Arabia.

- Israeli military was instructed to seize the buffer zone and control points in order to ensure the protection of all Israeli communities in the Golan Heights, according to Israeli Defense Minister Katz.

- Israeli official said that in the coming days, Israel might capture more areas inside Syria, and further deepen the attacks against strategic targets in Syria, to prevent weapons from falling into the hands of the rebels, according to Kann’s Stein.

- Israel’s Channel 13 said “The Israeli army is considering continuing the incursion into Syrian territory to expand the buffer zone in the Golan., according to Sky News Arabia.

- Israel’s Channel 13 said “Israeli intelligence is monitoring what is happening in Iran for fear that the collapse of the axis loyal to it will push it to develop nuclear weapons”, according to Sky News Arabia.

- “US administration officials fear that Assad’s fall will increase pressure on Iran’s Supreme Leader Ali Khamenei to give the green light to produce a nuclear bomb.”, according to Kann News.

- Israeli PM Netanyahu said the fall of Assad was a direct result of blows dealt to Hezbollah and Iran by Israel, and added that Israel will not allow any hostile force to establish itself on its borders, according to Reuters.

- Hezbollah pulled all forces out of Syria on Saturday, according to Lebanese security sources cited by Reuters.

- US encouraged Iraq to not get drawn into Syrian unrest, according to a Senior US official cited by Reuters, and US has been in discussions with Turkish officials and US focus is “a new Syria”. Senior US official does not see role for US troops on the ground addressing chemical weapons in Syria.

- US Central Command said its forces conducted dozens of airstrikes on Islamic State camps in central Syria on Sunday, and struck over 75 Islamic State targets in central Syria, according to Reuters.

- US President Biden said the US will support Syria’s neighbours through period of transition, and will speak with leaders in region in coming days and send administration officials, according to Reuters.

- US-backed Syrian Kurdish forces said they are still fighting Turkish-backed forces in Syria’s Manbij, according to Reuters.

- Iran said it will monitor developments in Syria and the region closely, and will adopt appropriate approaches and positions, according to a Foreign Ministry statement, adding that the long-standing and friendly relations between the Iranian and Syrian nations are expected to continue.

- “Iranian Foreign Minister: Conflicts are expected to spread not only to Iraq but to the entire region”, according to Sky News Arabia.

- President-elect Trump’s Middle East envoy met Israel and Qatar PMs to broker a ceasefire, according to the FT.

Geopolitics: Other

- US president-elect Trump said there should be an immediate ceasefire and negotiations in Ukraine this is time for Russia’s Putin to act, and China can help, via Truth Social.

- US president-elect Trump, French President Macron and Ukrainian President Zelenskyy had “very good conversation” over the weekend, according to a source close to Macron cited by Reuters.

- Taiwan’s Defence Ministry said on Sunday China has almost doubled the number of warships around Taiwan in the past 24 hours, ahead of what is suspected to be a new round of war games, according to Reuters.

- Taiwan Defence Ministry said it instructed troops to closely monitor situation, maintain high alert on Chinese PLA drills; have raised alert level on Taiwan’s outlying islands; activated combat readiness drills to carry out at strategic locations, according to Reuters.

- Chinese military and coast guard boats have entered waters around Taiwan and the Western Pacific to carry out missions, according to Reuters.

- Taiwan Coast Guard said seven Chinese Coast Guard ships began conducting “grey-zone harassment’ against Taiwan from early Monday, according to Reuters.

- China currently has almost 90 navy and coast ships in the waters near Taiwan, Southern Japanese islands, East and South China Seas, according to Reuters.

US Event Calendar

- 10:00: Oct. Wholesale Trade Sales MoM, prior 0.3%

- 10:00: Oct. Wholesale Inventories MoM, est. 0.2%, prior 0.2%

- 11:00: Nov. NY Fed 1-Yr Inflation Expectations, prior 2.87%

Central Bank speakers

- Dec. 7-Dec. 19: Fed’s External Communications Blackout

DB’s Jim Reid concludes the overnight wrap

This morning we published a new chart book, “Curveballs for 2025” which looks at potential realistic positive and negative curveballs that could change the direction of travel for the global economy and markets in 2025. So far this has been a decade of surprises and we have to consider what 2025’s out of consensus surprise will be. In 2020 the pandemic meant the year-ahead outlooks were redundant by the end of Q1, in 2021 a surge in inflation surprised virtually everyone, in 2022 markets were caught off guard by the most aggressive rate-hiking cycle since the 1980s, in 2023, the consensus wrongly expected a US recession and in 2024, no-one expected an S&P 500 return that could hit 30% YTD in the days ahead. So as we look forward to 2025, it’s safe to say that the most surprising thing would actually be a lack of surprises.

Tech and AI could surprise in both directions in 2025 and maybe the answer will come today when I see if I’ve won the school Xmas Fayre “guess how many sweets are in this big glass jar” competition from Saturday. I took a photo of the jar and uploaded it to ChatGPT and asked it to tell me. ChatGPT gave me a range and I plumped for the middle of it. For me this will decide whether AI is hype or the biggest innovation since the wheel!

A further surprise for 2025 would be a hike from the Fed and events like Wednesday’s US CPI will be a key determinant even if the near-term implication will be whether the Fed cut next week or not. After Friday’s mixed payrolls report that went up from around 70% to 85% at the close. So that’s the main event of the week. The ECB meeting the following day will also be a key event with markets pricing in a small chance of a 50bps cut but with 25bps nailed on. Elsewhere the key events of note will be the RBA decision (hold expected), China trade data and Danish and Norwegian CPI tomorrow, the BoC decision on Wednesday (possible consecutive 50bps cut), the Brazilian rate decision (75bps hike to 12% expected), alongside a 10yr UST auction, US PPI, the SNB decision and a 30yr UST auction on Thursday, and the BoJ Tankan quarterly survey on Friday ahead of an “in the balance” BoJ meeting on December 19th where the market is expecting a 36% probability of a hike. See the full week ahead at the end as usual but now we’ll preview the US CPI and the ECB decision in more detail.

For US CPI on Wednesday, our US economists expect headline CPI growth to pick up to +0.30% (+0.24% in October), in line with the median forecast on Bloomberg, and see core printing at +0.27% (+0.28%) also in line with consensus. The headline YoY rate will therefore likely move up two-tenths to 2.8%, with core staying at 3.3%. The PPI report will follow on Thursday and our economics team forecast the headline to grow by +0.3% MoM (+0.2%). As ever the components that feed into core PCE will be the main thing to watch.

For the ECB, DB expect a 25bp cut to 3.00% in December. This will be the fourth cut since the start of the easing cycle, making it 100bp of cuts so far in this cycle. See Mark Wall’s preview here. The team expect the December ECB press conference to emphasize uncertainty and the Governing Council to reach a compromise on communications that creates more policy optionality. There is considerable uncertainty going forward, not least around the timing, extent and impact of US tariffs, and as such the Governing Council is likely to want to keep its policy options wide open in 2025.

It’s been a weekend full of interesting news with Syrian President Assad’s reign collapsing as rebel forces ousted him. With Russia and Iran historically backing the Assad government but being distracted by other conflicts on their own doorstep, the rebel forces have taken their opportunity. While many countries will be happy to see the current regime fall, the big question mark is what happens next. The rebels have been led by HTS, who spun out of al-Qaeda in 2016, so there will remain question marks about the succession. The situation probably isn’t market moving at the moment (Crude up 0.4% overnight) but has longer-term implications for a lot of the current geopolitical hotspots dominating the world at the moment.

Meanwhile Mr Trump spoke to NBC’s “Meet the Press” yesterday and said he had no plans to replace Powell as Fed Chair and said “tariffs are going to make our country rich. Tariffs are going to help us pay off $35 trillion in debt”. The trade comments didn’t have a lot of extra substance beyond that so hard to get too much from it at the moment.

Asian equity markets are soft this morning amid continued political upheaval in South Korea and a seemingly slow demand recovery in China. As I check my screens, the KOSPI (-2.54%) is rapidly losing steam and leading losses in the region after gaining ground initially as opposition lawmakers indicated that they would push for another impeachment vote on President Yoon after the first one failed. Elsewhere, the Hang Seng (-0.57%), and the Shanghai Composite (-0.36%) are also losing ground. S&P 500 (-0.07%) and NASDAQ 100 (-0.05%) futures are trading just below flat.

Coming back to China, consumer prices cooled to +0.2% y/y in November (v/s +0.4% expected), its lowest in 5 months and down from a +0.3% increase in October. At the same time, factory gate inflation shrank -2.5% y/y in November but higher than the Bloomberg forecast of a -2.8% decline and against a -2.9% contraction in the previous month. The reading marked over two years of consistent declines in PPI though. Elsewhere, Japan’s GDP grew at an annualised pace of +1.2% in Q3 (v/s +1.0% expected), thus keeping alive market expectations for an interest rate hike next week from the BOJ.

Looking back at last week now, risk assets put in another strong performance, with the S&P 500 up +0.96% (+0.25% Friday) to yet another new record. Indeed, it was a third consecutive weekly advance for the index, and it means that it’s now up +27.68% on a YTD basis, not far off the +29.6% gain in 2013 that marks the strongest annual performance of the 21st century so far. That strength was echoed across global equities, with the STOXX 600 also up for a third consecutive week with a +2.00% gain (+0.18% Friday), whilst Japan’s Nikkei was up +2.31% (-0.77% Friday).

The week ended with a mixed US jobs report for November on Friday, where the headline gain for nonfarm payrolls was broadly as expected at +227k (vs. 220k consensus). Moreover, there were positive revisions to the previous couple of months, so October was revised up from +12k to +36k. That said, there were also some more negative features in the report, with the unemployment rate ticking up to 4.246% (vs. 4.1% expected), so it was just shy of being rounded up to 4.3% again. Indeed, it’s worth noting that the recent July peak in the unemployment rate (that helped trigger the summer market turmoil) was 4.253%, so only 0.07bps above what we saw on Friday.

From a market perspective, investors welcomed the report as it still kept the door open to a December rate cut. For instance, futures dialled up the probability of a cut to 85% by the close on Friday, having been around 70% just before the jobs report came out. And in turn, that proved supportive for US Treasuries, and the 2yr Treasury yield fell -4.7bps last week (-4.0bps Friday) to 4.104%. Meanwhile, the 10yr yield fell by a smaller -1.6bps (-2.3bps Friday).

Over in Europe, there were significant developments in France given the political turmoil that led to a vote of no confidence in the government. However, whilst the Franco-German 10yr spread initially hit its widest since 2012 last Monday, it then continued to fall over the rest of the week. So overall, it tightened -3.8bps last week (-1.0bps Friday) to 77bps. Moreover, other countries in Europe saw a larger tightening, with the Italian 10yr spread over bunds down -12.6bps last week to 108.5bps, whilst the Spanish spread tightened -5.3bps to 65bps. In part, that was because yields on 10yr bunds themselves rose +2.0bps (+0.3bps Friday) to 2.11%.

Tyler Durden

Mon, 12/09/2024 – 08:26

via ZeroHedge News https://ift.tt/3TH8aN6 Tyler Durden