Futures Rise As Tariff Uncertainty Grows Ahead Of “Liberation Day”

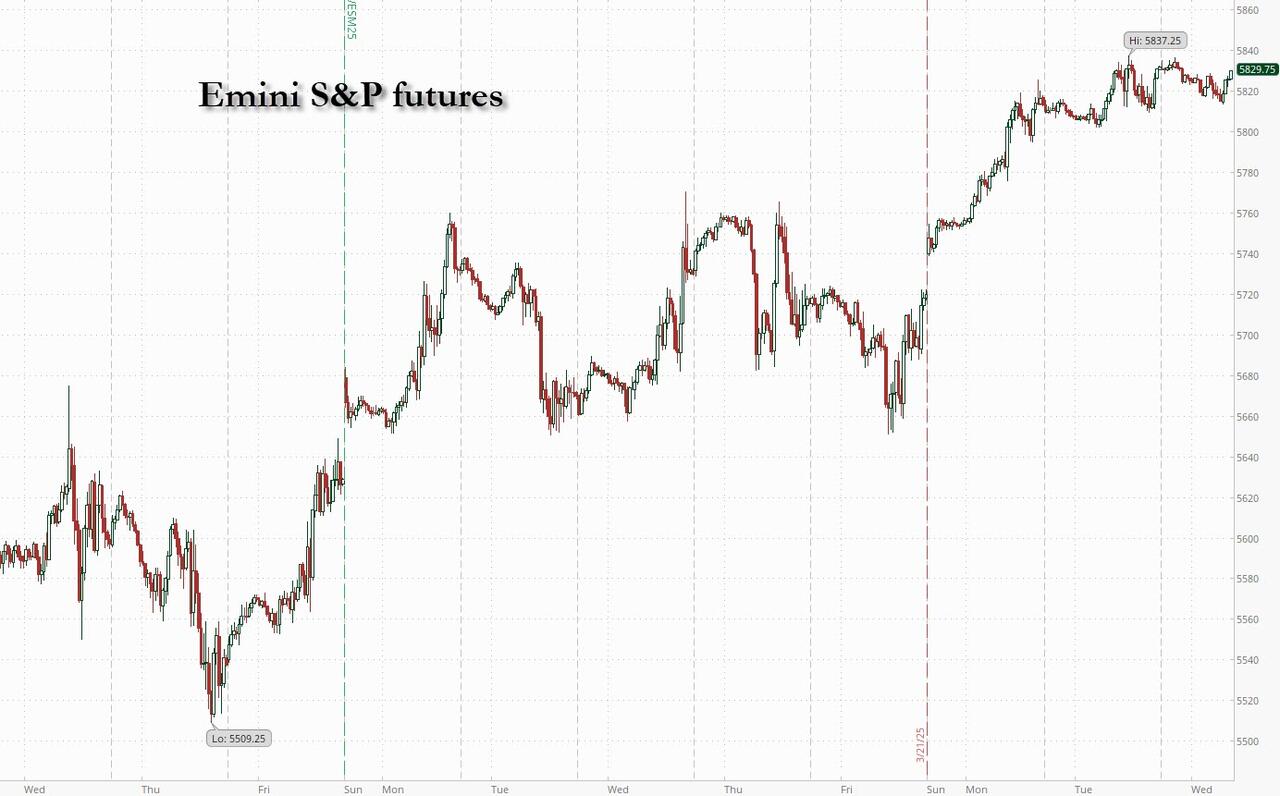

US equity futures are flat, reversing earlier losses while global markets were mixed (Europe down, Asia up) as investors awaited more clarity on US tariff plans and the economic outlook before Donald Trump’s April 2 “Liberation Day” deadline to impose a fresh reciprocal tariffs. As of 8:00am ET, S&P futures were up 0.1% following modest gains on the indexes on Tuesday, while Nasdaq futures were flat as Tesla and Nvidia shares edged lower, pressuring the Mag 7. Europe’s Stoxx 600 index dropped 0.5%. Bond yields are 1-3bp higher and USD is higher. Commodities are mostly higher led by oil and base metals. Copper futures in New York surged to a record high (up 1% now after easing off records) as traders priced in the possibility of hefty import tariffs that may come within several weeks. Headlines were mostly quiet since market close yesterday. Today’s economic calendar includes Feb durable goods orders at 8:30am; Fed speaker slate includes Kashkari (10am) and Musalem (1:10pm).

In premarket trading, video game retailer GameStop jumped 14% after the struggling video-game retailer that became a favorite of retail traders during the meme stock frenzy said its board approved a plan to add Bitcoin as a treasury reserve asset. Tesla and Nvidia lead losses among the Magnificent Seven stock (Alphabet -0.4%, Amazon +0.2%, Apple +0.1%, Microsoft -0.1%, Meta +0.1%, Nvidia -1.4% and Tesla -1.2%). Dollar Tree (DLTR) rises 2% as the company will sell its Family Dollar chain for about $1 billion to Brigade Capital Management and Macellum Capital Management a decade after buying the business. Here are some other notable movers:

- Global-e Online (GLBE) rises 3% after Morgan Stanley upgraded the software firm to overweight, citing achievable growth targets.

- Humacyte (HUMA) slides 26% after the biotech firm offers 25 million shares at $2 apiece, a discount of around 30% to its previous close.

- Goldman Sachs (GS) rose 1% Tuesday for an 8th day, on its longest winning streak since November 2022.

- Playtika (PLTK) rises 7% following a double upgrade of the mobile-games company at BofA, removing the only negative analyst view on the stock.

- Summit Therapeutics (SMMT) rises 4% after Citi upgraded the biotech to buy on stronger conviction on the firm’s HARMONI-2 clinical trial.

The tariffs issue remains front and center for investors, who took comfort earlier this month from the Trump adminstration’s signal that the coming wave of levies may be less expansive and more targeted than originally feared. However, the president has since sown confusion by saying he didn’t want too many tariff exceptions, but he would “probably be more lenient than reciprocal.” All that has left investors struggling to work out how to position ahead of the April 2 deadline that Trump has dubbed “Liberation Day.”

“Uncertainty on the tariff front remains ridiculously high, leaving it incredibly tough for businesses or consumers to plan more than about a day into the future, and still making it nigh-on impossible for market participants to price risk,” said Michael Brown, a strategist at Pepperstone Group Ltd.

European stocks retreated on lingering jitters about US tariffs. UK mid-caps rise on an unexpected cooldown in inflation before a key budget statement from the government later in the day. The Stoxx 600 fell 0.6% to 549.21 with 366 members down, 223 up and 11 unchanged. In Britain, the FTSE 250 gauge of mid-sized stocks advanced about 0.5%, as data showing an unexpected inflation slowdown strengthened the case for the Bank of England to cut interest rates. Here are some of the biggest movers on Wednesday:

- Ocado shares rise as much as 16% as the firm gets a positive analyst rating from JPMorgan for the first time in over seven years, with the broker upgrading to overweight from neutral to reflect a “turning tide” in the digital grocery sector.

- Danieli shares gain as much as 11% after better-than-expected net cash results and FY targets confirmation for this year, analysts say, as the Italian metal-production company released 1H24/25 results on Tuesday after market close.

- ProSieben shares rise as much as 5.7% after Reuters reported that MFE had called a board meeting for Wednesday to review a possible bid for the company.

- TotalEnergies shares rise as much as 1.1% after being upgraded by analysts at Citi, who say the oil giant will increase cashflow at a much faster pace than key European peers over the coming years.

- Avon rises as much as 9.2%, the most in over four months, after the maker of helmets and respirators raised its revenue growth and margin guidance for this year, as the firm announced new orders and contracts from European nations and a ramp-up of volumes for deliveries in the US.

- Mips shares gain as much as 5.4%, the most since February, after the Swedish helmet technology firm was upgraded to buy from hold at SEB, citing an attractive risk/reward after a 30% share price drop since August.

- Evoke shares sink as much as 19%, the most since July 2023. Though the William-Hill owner reported in-line results for fiscal year 2024, a soft start to 1Q25 is likely to raise concerns on whether the gambling operator can meet its guidance for 2025, JPMorgan notes.

- Vistry shares drop as much as 11%, the biggest drop since December, after analysts warned of weak current trading and low visibility on the homebuilder’s 2025 financial results.

- CD Projekt shares fall as much as 13%, the steepest drop since March 2021, after the video-games maker said its Witcher 4 game won’t be released before 2027, overshadowing strong 4Q earnings and news of a cooperation pact with US peer Scopely.

- Wetherspoon slides as much as 4.7% after Deutsche Bank assigns the only sell rating on the pub operator, downgrading from neutral based on the impact of changes related to the UK Government’s budget.

Earlier in the session, Asian equities rose, heading for their first advance in four days, helped by gains in Chinese technology heavyweights and a rally in Indonesia’s market. The MSCI Asia Pacific Index climbed as much as 0.5%. Nintendo Co. was among the biggest contributors after Goldman Sachs reinstated coverage of the Japanese games maker with a buy rating. Samsung Electronics, Alibaba and Tencent were among other major stocks buoying the regional benchmark. The Jakarta Composite Index jumped 4%, the most in the region, after several state-owned banks increased their dividend payouts. Stocks in Australia closed higher after the government unveiled tax cuts and other sweeteners in a pre-election budget. Chinese equities listed in Hong Kong also gained. Morgan Stanley strategists raised their targets for the nation’s equities for the second time in a little more than a month, citing upside for valuations amid an improving outlook for earnings. A gauge of Chinese tech shares in Hong Kong rebounded after falling to the brink of a technical correction in the previous session.

In FX, the dollar is little changed, supported on the view that the US would limit exceptions to the next tranche of tariffs expected next week. The Bloomberg Dollar Spot Index rose 0.1% before paring gains during the European session; it is on track to gain for the five of the last six days.

- USD/JPY gained as much as 0.5% to 150.62 as Bank of Japan Governor Kazuo Ueda indicated he aims to keep his options open ahead of the bank’s next policy meeting, adding to the view that Japan’s yield discount to the US will remain wide

- GBP/USD fell 0.5% to the day’s low 1.2886 after data showed an unexpected slowdown in UK CPI; traders await the country’s fiscal statement later in the day

In rates, treasuries edged lower as investors await speeches by Federal Reserve officials later in the day for more steer into the US interest rate outlook. Treasury yields are 1bp-3bp cheaper across a slightly steeper curve, with 5s30s spread around 1bp wider on the day; 10-year, 3bp higher near 4.35%, trails bunds and gilts in the sector by 2bp and 5bp.

Gilts outperform, led by front-end tenors as swaps price in additional easing by Bank of England after UK February CPI data rose less than estimated. UK 2-year yields are more than 5bp lower on the day after the inflation data, steepening the gilts curve. Treasury auction cycle continues with $70 billion 5-year note sale at 1pm New York time, following good demand for 2-year notes on Tuesday. It concludes with $44 billion 7-year note auction Thursday

In commodities, copper futures in New York surged to a record high as traders priced in the possibility of hefty import tariffs that may come within several weeks. WTI oil edged higher after an industry report signaled a large decline in US crude stockpiles, while the market weighed the prospect of a Russia-Ukraine ceasefire in the Black Sea. Gold extended gains, rising 0.6% to $3,027.

Looking to the day ahead now, data releases include the preliminary durable goods orders for February. Meanwhile from central banks, we’ll hear from the Fed’s Kashkari and Musalem, along with the ECB’s Villeroy and Cipollone.

Market Snapshot

- S&P 500 futures little changed at 5,822.50

- STOXX Europe 600 down 0.2% to 551.61

- MXAP up 0.4% to 189.10

- MXAPJ up 0.4% to 590.15

- Nikkei up 0.7% to 38,027.29

- Topix up 0.5% to 2,812.89

- Hang Seng Index up 0.6% to 23,483.32

- Shanghai Composite little changed at 3,368.70

- Sensex down 0.7% to 77,508.02

- Australia S&P/ASX 200 up 0.7% to 7,998.97

- Kospi up 1.1% to 2,643.94

- German 10Y yield little changed at 2.78%

- Euro little changed at $1.0792

- Brent Futures up 0.4% to $73.29/bbl

- Gold spot up 0.3% to $3,027.85

- US Dollar Index little changed at 104.27

Top Overnight News

- GOP leaders said they’re getting close to agreeing on a plan to pass an extension of Trump’s 2017 tax cuts and an increase to the debt ceiling. The CBO will today release its estimate for when the debt ceiling will be reached. BBG

- Trump’s copper tariffs could arrive within the next several weeks, earlier than initially anticipated. BBG

- Fed’s Goolsbee (2025 voter) said it may take longer than anticipated for the next cut to come because of economic uncertainty and ‘wait and see’ is the correct approach when facing uncertainty. Goolsbee also commented that market angst over inflation would be a red flag and believes borrowing costs will be a fair bit lower in 12–18 months, while he noted that if investor expectations begin to converge with those of American households, the Fed would need to act: FT

- China economic optimism rises, and the Street has raised their growth forecasts on back of stimulus, although tariffs loom as a risk. WSJ

- China wields significant policy room to stimulate its economy this year while some reform was needed to boost consumption, Huang Yiping, an advisor to China’s central bank and a professor at Peking University, said on Wednesday. China has unveiled fresh fiscal measures, including a rise in its annual budget deficit, to help hit an economic growth target of around 5% this year, which analysts have described as ambitious. The central bank has pledged to cut interest rates and pump more money into the economy at an appropriate time. RTRS

- The Bank of Japan may consider monetary tightening if a surge in food prices causes broader and stronger inflation, the central bank governor said Wednesday, adding fuel to expectations for a near-term rate hike. WSJ

- UK CPI cools by more than expected in Feb on headline (+2.8% vs. the Street +3% and vs. +3% in Jan) and core (+3.5% vs. the Street +3.6% and vs. +3.7% in Jan) while services held steady at +5% (vs. the Street +4.9% and vs. +5% in Jan). WSJ

- Australia’s CPI in Feb ticks down to +2.4% (vs. the Street +2.5%), helped by a fall in electricity prices, while the continued easing in home building costs and rents supported fueling expectations for further RBA rate cuts. RTRS

- Signs that investors in the US bond market are baking in higher inflation would be a “major red flag” that could upend policymakers’ plans to cut interest rates, Goolsbee warned. He added that the Fed is no longer on the “golden path,” and that the rate cuts will take longer than expected. “If you start seeing market-based long-run inflation expectations start behaving the way these surveys have done in the last two months, I would view that as a major red flag area of concern,” said Goolsbee. FT

- Canada and India are taking steps to cool diplomatic tensions, including considering sending back envoys after tit-for-tat expulsions last year, people familiar said. The two nations are looking to strengthen trade ties to counter US tariff threats. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with a mostly positive bias after the somewhat mixed performance stateside where the focus centred on tariffs, data and geopolitics including reports that Ukraine and Russia agreed with the US on a maritime ceasefire. ASX 200 was led higher by gains in the mining, resources and financial sectors in the aftermath of the recent budget announcement, while participants also digested softer-than-expected monthly inflation from Australia. Nikkei 225 reclaimed the 38,000 level with upside supported by a weaker currency and after slightly softer Services PPI data. Hang Seng and Shanghai Comp eked slight gains but with upside capped amid ongoing tariff uncertainty with a Chinese delegation to meet with the US Commerce Secretary and the USTR today to negotiate over tariffs in which they will also discuss fentanyl and trade barriers among other issues, while a PBoC adviser warned at the Boao Forum that changes in the global environment will be challenging for China and China must boost domestic demand, especially consumption.

Top Asian News

- PBoC adviser said at the Boao Forum that changes in the global environment will be challenging for China and China must boost domestic demand, especially consumption, while it added that there is still very big macro policy space for supporting China’s economy and reform measures alongside recent policy steps are needed to support consumption.

- BoJ Governor Ueda said cost-push factors are likely to gradually dissipate but also noted that underlying inflation is likely to gradually converge towards the 2% target even when the temporary boost from food inflation disappears. Ueda said the BoJ will make a judgment call by looking at various indicators to determine whether underlying inflation has hit the target and underlying inflation is close to but has yet to move into the narrow band defined as sufficient achievement of the 2% price target. Furthermore, Ueda said the BoJ remains vigilant to the possibility that underlying inflation may accelerate faster than projected and expects to keep raising interest rates if the economy and prices move in line with forecasts in the quarterly outlook report but later commented that if price risks overshoot expectations, they will take stronger steps to adjust the degree of monetary support.

- BoJ’s Koeda says the Bank’s mandate is to contribute to a healthy economy, various indicators show Japan’s underlying inflation moving towards a sustainable achievement of BoJ’s 2%.

Despite a steady and firmer open European bourses now find themselves mostly in the red, Stoxx 600 -0.6%. Selling pressure picked up after the cash open with no obvious catalyst for the price action at the time. Sectors began mixed but now have a negative bias with Health Care, Chemicals and Autos bottom of the pile; the latter seemingly hit on remarks from Trump about Europeans “freeloading”, reports of copper tariffs and pressure in Porsche SE on an Volkswagen impairment.

Top European News

- ECB’s Villeroy says in the short-term, US President Trump’s “lose-lose” strategy is harming the US as the Fed’s downgrade of its forecast show. A 25pp increase in US tariffs in Q2 would have a limited impact on European inflation, but could reduce EZ GDP by 0.3pp in a year

FX

- DXY is currently flat but with modestly diverging fortunes against peers, greenback softer vs. cyclicals and firmer vs. havens despite the pullback in European stocks seen since the cash open. Comfortably above 104.00 but at the lower-end of a 104.18-38 band.

- EUR attempting to get back above the 1.08 mark and while it has tested the figure it is yet to convincingly breach it. Upside which comes despite the rhetoric from Trump and with incremental drivers light since the Ifo.

- Cable the G10 laggard after cooler-than-expected inflation data this morning and ahead of the Spring Statement which commences from 12:30GMT. Cable back above 1.29 but only modestly so after slipping as low as 1.2887 early doors.

- USD/JPY rebounded overnight from the prior day’s trough and reclaimed the 150.00 handle with tailwinds amid the constructive APAC risk tone and following the softer Services PPI data from Japan; got to a 150.63 peak but has since pulled back towards the mentioned figure.

- AUD was hit on soft domestic inflation data overnight which saw a 0.6279 low in AUD/USD print but it has since recovered back above the mark and to a high some 30 pips above.

- PBoC set USD/CNY mid-point at 7.1754 vs exp. 7.2559 (Prev. 7.1788).

- Riksbank Minutes (March): Thedeen says “…we have some scope to see through upturns in inflation if we judge that they are temporary”.

Fixed Income

- Gilts gapped higher by 33 ticks at the open after an almost entirely cooler-than-expected inflation series. A series which has sparked a modest dovish move in BoE pricing, though the overall narrative hasn’t shifted.

- Got to as high as 91.58 though this proved short lived as we approach the Spring Statement from 12:30GMT where Reeves is expected to try and raise/save GBP 17bln, to plug the fiscal hole she finds herself in and then to provide headroom of just under the GBP 9.9bln she had in October; full preview available.

- Bunds modestly firmer after picking up early doors on the above. Thereafter, hit a 128.36 session high which is a tick above Tuesday’s best. Specifics light into supply which was strong but sparked no reaction in the benchmark. Leaving it marginally in the green around 128.20.

- USTs in the red but only modestly so with action relatively steady in the European morning as we await updates to numerous catalysts in addition to Fed speak, data and supply with 70bln of 5yr Notes due and following the 2yr tap on Tuesday which was strong when compared to recent averages though not quite as well received as the outing in February.

Commodities

- Crude continues to inch higher and is at highs of USD 69.54/bbl and USD 73.57/bbl respectively for WTI and Brent but remains within Tuesday’s parameters. Upside driven by the private inventory report, absence of sanctions removal on oil tankers and Yemeni forces targeting the USS Truman.

- Dutch TTF in the red with Ukraine-Russia geopols in focus and the most recent language from the Kremlin being that talks are continuing with the US and they are satisfied with the dialogue. There have been reports of drone strikes on/from both sides, with the Kremlin continuing to state that they will only comply with the Black Sea truce once specific sanctions are lifted.

- Gold indecisive and flat on the session, around the mid-point of a USD 3013-3032/oz band. Copper was bid overnight after futures hit a record high in Tuesday’s session which followed through into 3M LME and lifted it above the USD 10k mark on latest tariff reports; since, the metal has pulled back and is in the red as we await further updates.

- Goldman Sachs maintains its 3-, 6- and 12-month copper price forecasts at USD 9,600, USD 10,000 and USD 10,700, respectively.

- US Private Energy Inventories (bbls): Crude -4.6mln (exp -2.6mln), Distillate -1.3mln (exp. -2.2mln), Gasoline -3.3mln (exp. -2.2mln), Cushing -0.6mln.

- TotalEnergies (TTE FP) CEO says he would not be surprised if two of the Nord Stream gas pipelines came back.

- Reliance has paused purchases of Venezuelan crude following US President Trump’s 25% tariff, according to Bloomberg.

Geopolitics: Middle East

- Two Israeli raids were reported on the northeastern areas of Gaza City, according to Al Jazeera.

- Houthi military spokesman said they targeted Israeli military sites in the Jaffa area with a number of drones and targeted US aircraft carrier Harry Truman.

Geopolitics: Ukraine

- Russia’s Foreign Minister Lavrov said the Black Sea deal is aimed at Russia making legitimate profit in fair competition and ensuring food safety in Africa and elsewhere. Lavrov also commented that Russia and the US are discussing other things than Ukraine in their talks, according to TASS.

- Russian drone attacks caused major destruction in the central Ukrainian city of Kryvyi Rih, according to the local military administration. It was also reported that emergency power cuts were implemented in Ukraine’s Mykolaiv port following reported drone attacks, according to the mayor.

- Russia’s Kremlin says the order on moratorium on energy strikes is still in force and Russia are compliant; are continuing contacts with the US, satisfied with the dialogue. Black sea initiative will be activated after a number of conditions are met.

US Event Calendar

- 07:00: March MBA Mortgage Applications , prior -6.2%

- 08:30: Feb. Durable Goods Orders, est. -1.0%, prior 3.2%

- Feb. Durables-Less Transportation, est. 0.2%, prior 0%

- Feb. Cap Goods Ship Nondef Ex Air, est. 0.2%, prior -0.3%

- Feb. Cap Goods Orders Nondef Ex Air, est. 0.2%, prior 0.8%

Central Banks

- 10:00: Fed’s Kashkari Hosts Fed Listens, conversation

- 13:10: Fed’s Musalem Speaks on Economy, Monetary Policy

DB’s Jim Reid concludes the overnight wrap

Markets put in a decent performance yesterday, with the S&P 500 (+0.16%) posting a third consecutive advance for the first time since early February. The moves came despite several obstacles, including an unexpectedly large drop in the US Conference Board’s consumer confidence indicator. But ultimately investors shrugged that off, as there were still no signs that this recent survey weakness was being reflected in the hard data. Moreover, the rally got further support thanks to hopes that next week’s reciprocal tariffs wouldn’t be as bad as previously feared. So that helped to lift sentiment around the US outlook, with signs of market stress continuing to ease after the S&P 500’s correction. Indeed, the VIX index of volatility fell to its lowest level in over a month yesterday, at 17.15pts.

That story had looked quite different around the US open, when the Conference Board’s indicator was released. It showed an unexpectedly large drop in consumer confidence to 92.9 in March (vs. 94.0 expected), leaving it at its lowest level since January 2021, back when the economy was still emerging from the pandemic. Moreover, the expectations measure fell to a 12-year low of just 65.2. So that took it beneath its 2022-lows, when the Fed were still hiking rates aggressively and CPI inflation was running above 8%. But despite the negative headlines, investors were reassured by the fact that the labour market measures were still holding up. For instance, the differential between those saying jobs were plentiful versus hard to get actually moved up slightly in March, to a net +17.9%. On top of that, investors also recognised that we still hadn’t seen this deterioration echoed in the hard data yet. So they’re still waiting for more evidence before they’re willing to price a more significant economic downturn.

That more positive tone led to a fresh pickup for US equities, with the Magnificent 7 (+1.23%) leading the way once again. That group are now up +6.21% over the last three sessions, making it their best 3-day performance since the news of Trump’s election victory in early November. However, the broader equity performance was more subdued, and even though the S&P 500 advanced (+0.16%), the equal-weighted version of the index was down -0.27% and the small cap Russell 2000 (-0.66%) lost ground after its Monday surge.

Equities also got support from a fresh drop in Treasury yields, with the 10yr yield coming off a one-month high of 4.37% intraday, before closing down -2.3bps at 4.31%. Near term market expectations for the Fed were little changed, but a modest decline in 2026 pricing helped 2yr yields post a similar -2.0bps decline to 4.02%. Otherwise, we didn’t hear from many Fed speakers, but Governor Kugler sounded a patient note, saying that “FOMC policy is well positioned”, and that they could keep policy on hold “at the current rate for some time”. Meanwhile, Chicago Fed President Goolsbee said in an FT interview that the Fed wasn’t on the “golden path” of 2023-24, and that “there’s a lot of dust in the air”.

Nevertheless, he still said he thought borrowing costs would be “a fair bit lower” in 12-18 months time. Overnight, 10yr Treasury yields have reversed course again, moving up +2.1bps to 4.33%.

Over in Europe, there was an even stronger risk-on tone yesterday, with the STOXX 600 (+0.67%) recovering after three consecutive declines. That got a boost from the Ifo’s latest business climate indicator in Germany, which moved up to an 8-month high of 86.7 in March, in line with expectations. However, sovereign bonds sold off, in contrast to their US counterparts, after some hawkish comments from several ECB officials. They cast doubt on the prospect of another rate cut at the April meeting, with Croatia’s Vujcic saying that he saw the next meeting “as a completely open question.” Separately, Slovakia’s Kazimir said that he was “open to discussing either further interest-rate cuts or holding steady”, while France’s Villeroy noted that “the easing cycle is neither finished nor automatic”. So all that contributed to a rise in yields, with those on 10yr bunds (+2.7bps), OATs (+2.3bps) and BTPs (+2.1bps) all moving higher.

Elsewhere, there was a clear market reaction after the US said yesterday that Russia and Ukraine had agreed to a ceasefire in the Black Sea, as well as on the previously signalled 30-day halt to strikes against energy infrastructure. President Zelenskiy said Ukraine would implement this partial ceasefire immediately. Oil prices fell back in response, as the news eased fears about supply disruptions, with Brent trading crude falling by about 1% following the headlines to trade -0.7% lower intra-day. However, it rose back to close +0.03% on the day at $73.02/bbl, perhaps reflecting some inconsistency in the signals from the different sides. Notably, the Kremlin said the maritime ceasefire was conditional on the lifting of sanctions against Russian banks and companies involved in agricultural trade, a detail that was absent from the US statement. Still, there was a positive reaction among Ukraine’s dollar bonds, with the 10yr yield down -22.5bps on the day. And given the Black Sea’s importance for grain shipments, wheat (-0.82%) and corn (-1.29%) futures also fell back.

Overnight in Asia, markets have continued their strong performance, with decent gains for the Nikkei (+1.13%) and the KOSPI (+1.14%). Meanwhile in Australia, the S&P/ASX 200 (+0.71%) is also higher, which comes after the February CPI print was a bit softer than expected, falling to +2.4% (vs. +2.5% expected). However, there’s been a weaker performance in mainland China, where the CSI 300 (-0.19%) has lost ground this morning, and the Shanghai Comp (+0.06%) has only seen a modest increase. Looking forward, European equity futures are broadly positive, with those on the DAX up +0.22%, but US futures are very slightly lower, with those on the S&P 500 down -0.01%.

In terms of today, one of the main highlights will be the UK Government’s Spring Statement. That includes a new set of forecasts from the Office for Budget Responsibility, who are the UK’s independent fiscal watchdog, and they judge if the government are on track to meet their fiscal rules. However, because the economy has been weaker than the OBR set out last autumn, and gilt yields have also moved higher, our UK economist thinks that will remove the fiscal headroom set out at the time of the budget. In his preview for today’s event (link here), he expects fiscal consolidation near £14.5bn, comprising of welfare savings, departmental efficiency savings, and NHS reforms. And from a market perspective, he says the focus is likely to be on the size and composition of the 2025/26 gilt remit, how much fiscal headroom the government now has, and the credibility of any medium-term fiscal consolidation.

To the day ahead now, and here in the UK, Chancellor Rachel Reeves will deliver the spring statement, and there’s the CPI report for February as well. In the US, data releases include the preliminary durable goods orders for February. Meanwhile from central banks, we’ll hear from the Fed’s Kashkari and Musalem, along with the ECB’s Villeroy and Cipollone.

Tyler Durden

Wed, 03/26/2025 – 08:24

via ZeroHedge News https://ift.tt/zTDbE14 Tyler Durden