Authored by Lance Roberts via RealInvestmentAdvice.com,

“The great economist John Maynard Keynes once said: ‘Practical men, who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist.’” – John Coumarianos

The whole idea of “efficient markets” and “random walk” theories play out well on paper, they just never have in actual practice. The reality is investors make repeated emotional mistakes which are ultimately driven by the very volatility they are supposed to withstand.

These emotional mistakes, as I have discussed repeatedly in the past, are the biggest reason for underperformance by investors. These behavioral biases can be broadly defined as Loss Aversion, Narrow Framing, Anchoring, Mental Accounting, Lack of Diversification, Herding, Regret, Media Response, and Optimism.

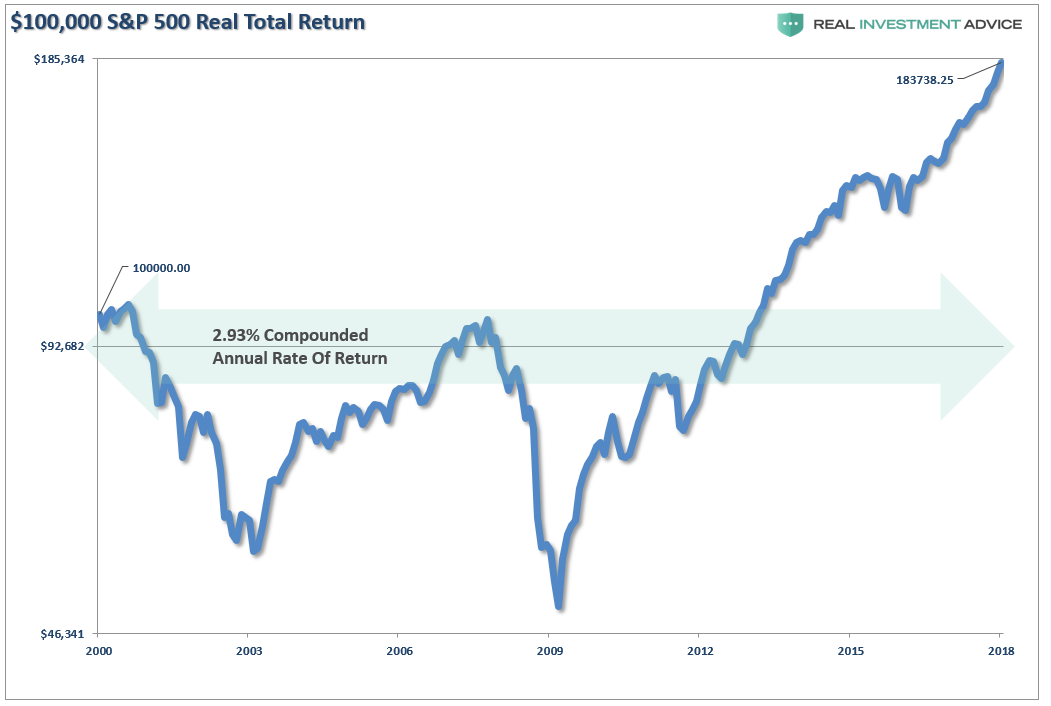

When prices rise on a consistent basis, investors begin viewing stocks as a “no lose proposition“ which simply deliver high-rates of return over the long-term. The reality has actually been quite different. The chart below shows the real, total return, (inflation and dividends included) versus it’s annualized rate of return using a geometric average.

It took nearly 14-years just to break even and 18-years to generate just a 2.93% compounded annual rate of return since 2000. (If you back out dividends, it was virtually zero.) This is a far cry from the 6-8% annualized return assumptions promised to “buy and hold” investors.

But such a low rate of return should not have been surprising.

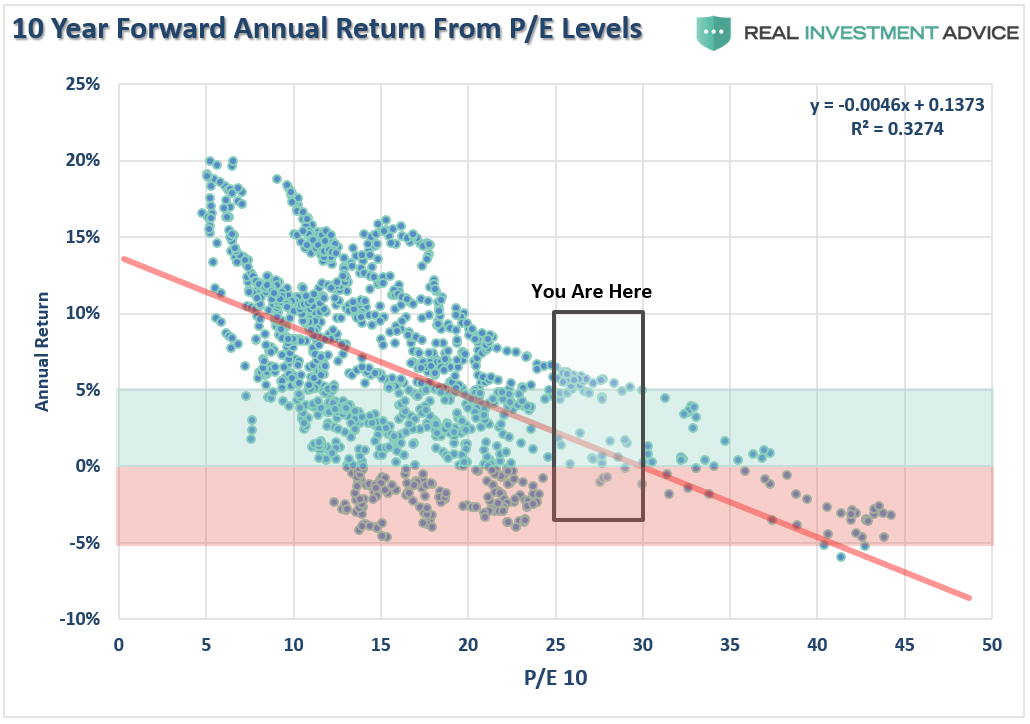

What drives stock prices (long-term) is the value of what you pay today for a future share of the company’s earnings in the future. Simply put – “it’s valuations, stupid.”

Instead of magical lottery tickets that automatically and necessarily reward those who wait, stocks are ownership units of businesses. That’s banal, I know, but everyone seems to forget it. And it means equity returns depend on how much you pay for their future profits, not on how much price volatility you can endure.

Stocks are not so efficiently priced that they are always poised to deliver satisfying returns even over a decade or more, as we’ve just witnessed for 18 years. A glance at future 10-year real returns based on the starting Shiller PE (price relative to past 10 years’ average, inflation-adjusted earnings) in the chart above tells the story. Buying high locks in low returns and vice versa.

Generally, if you pay a lot for profits, you’ll lock in lousy returns for a long time.

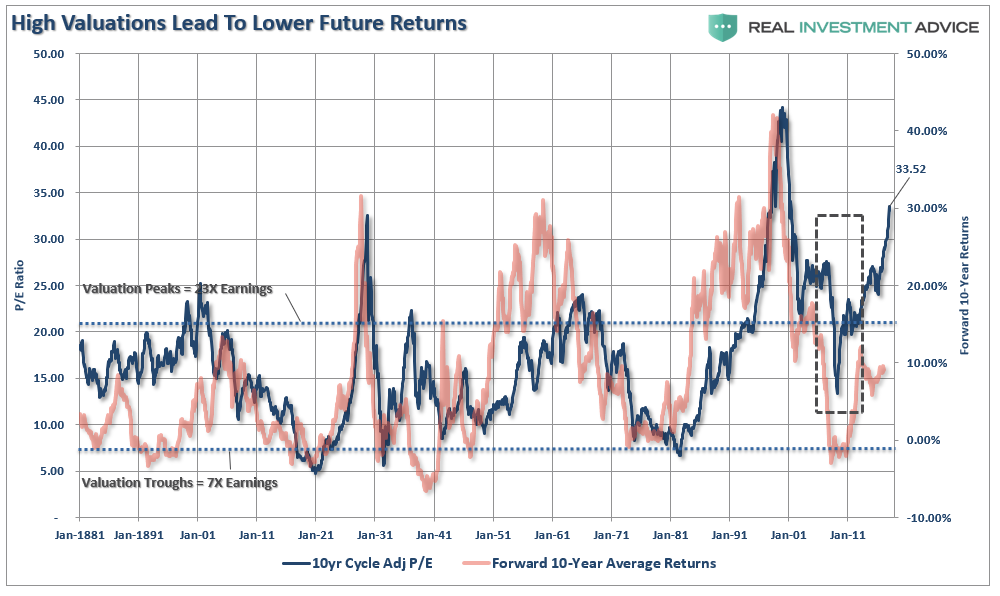

While volatility is the short-term price dynamics of “fear” and “greed” at play, in the long-term it is simply valuation. Despite the recent correction, valuations are once again pushing more extreme levels which suggest lower future forward returns.

“With valuations at levels that have historically been coincident with the end, rather than the beginning, of bull markets, the expectation of future returns should be adjusted lower. This expectation is supported in the chart below which compares valuations to forward 10-year market returns.”

“The function of math is pretty simple – the more you pay, the less you get.”

As a long-term investor, we experience short-term price volatility as “opportunity,” and high prices as “risk.” With economic growth to remain weak, and valuation expansion elevated, the risk of high prices has risen sharply.

Nothing But “Net”

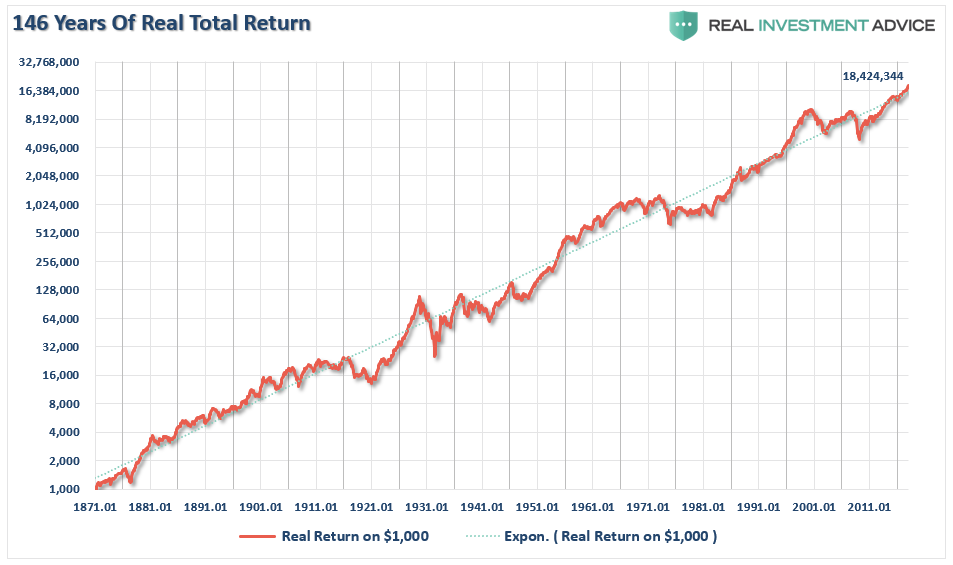

This brings me to one of the biggest myths perpetrated by Wall Street on investors. Individuals are often shown some variation of the following chart to support the claim that over the “long-term” the stock market has generated a 10% annualized total return.

The statement is not entirely false. Since 1900, stock market appreciation plus dividends have provided investors with an AVERAGE return of 10% per year. Historically, 4%, or 40% of the total return, came from dividends alone. The other 60% came from capital appreciation that averaged 6% and equated to the long-term growth rate of the economy.

However, there are several fallacies with the notion the markets will compound over the long-term at 10% annually.

1) The market does not return 10% every year. There are many years where market returns have been sharply higher and significantly lower.

2) The analysis does not include the real world effects of inflation, taxes, fees and other expenses that subtract from total returns over the long-term.

3) You don’t have 146 years to invest and save.

The chart below shows what happens to a $1000 investment from 1871 to present including the effects of inflation, taxes, and fees. (Assumptions: I have used a 15% tax rate on years the portfolio advanced in value, CPI as the benchmark for inflation and a 1% annual expense ratio. In reality, all of these assumptions are quite likely on the low side.)

As you can see, there is a dramatic difference in outcomes over the long-term.

From 1871 to present the total nominal return was 9.15% versus just 6.93% on a “real” basis. While the percentages may not seem like much, over such a long period the ending value of the original $1000 investment was lower by millions of dollars.

Importantly, the return that investors receive from the financial markets is more dependent on “WHEN” you begin investing with respect to “valuations” and your personal “life-span”.

Curb Your Expectations

Following on with the point above, with valuations currently at one of the highest levels on record, forward returns are very likely going to be substantially lower for an extended period. Yet, listen to the media, and the majority of the bullish analysts, and they are still suggesting that markets should compound at 8% annually going forward as stated by BofA:

“Based on current valuations, a regression analysis suggests compounded annual returns of 8% over the next 10 years with a 90% confidence interval of 4-12%. While this is below the average returns of 10% over the last 50 years, asset allocation is a zero-sum game. Against a backdrop of slow growth and shrinking liquidity, 8% is compelling in our view. With a 2% dividend yield, we think the S&P 500 will reach 3500 over the next 10 years, implying annual price returns of 6% per year.”

However, there are two main problems with that statement:

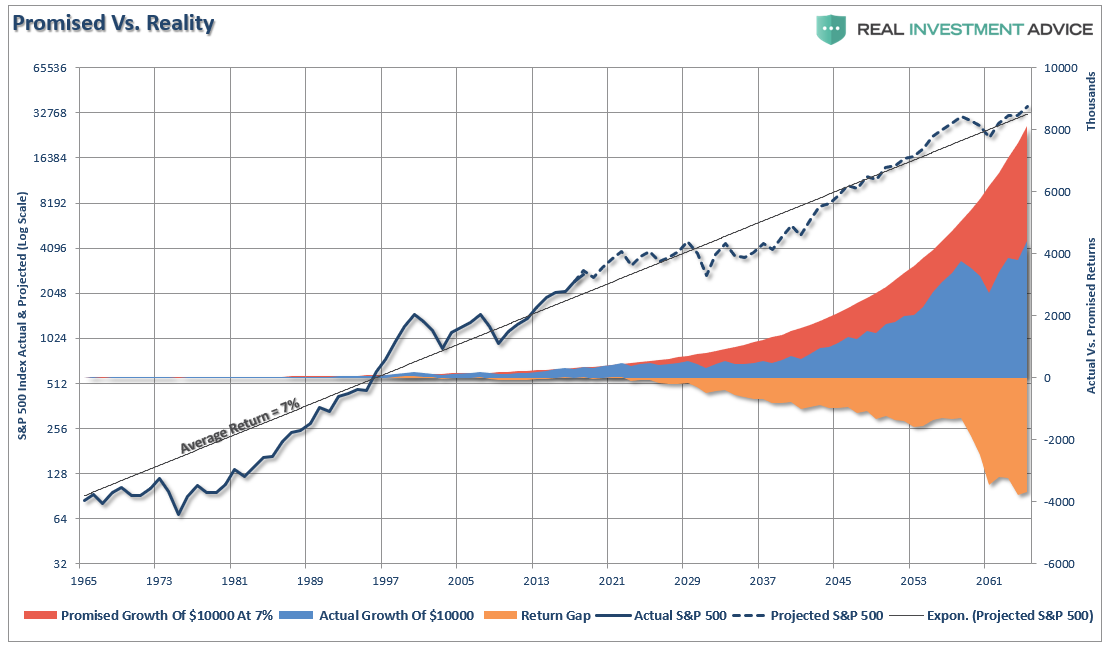

1) The Markets Have NEVER Returned 8-10% EVERY SINGLE Year.

Annualized rates of return and real rates of return are VASTLY different things. The destruction of capital during market downturns destroys years of previous capital appreciation. Furthermore, while the markets have indeed AVERAGED an 8% return over the last 117 years, you will NOT LIVE LONG ENOUGH to receive the same.

The chart below shows the real return of capital over time versus what was promised.

The shortfall in REAL returns is a very REAL PROBLEM for people planning their retirement.

2) Net, Net, Net Returns Are Even Worse

Okay, for a moment let’s just assume the Wall Street “world of fantasy” actually does exist and you can somehow achieve a stagnant rate of return over the next 10-years.

As discussed above, the “other” problem with the analysis is that it excludes the effects of fees, taxes, and inflation. Here is another way to look at it. Let’s start with the fantastical idea of 8% annualized rates of return.

8% – Inflation (historically 3%) – Taxes (roughly 1.5%) – Fees (avg. 1%) = 3.5%

Wait? What?

Hold on…it gets worse. Let’s look forward rather than backward.

Let’s assume that you started planning your retirement at the turn of the century (this gives us 15 years plus 15 years forward for a total of 30 years)

Based on current valuation levels future expected returns from stocks will be roughly 2% (which is what it has been for the last 17 years as well – which means the math works.)

Let’s also assume that inflation remains constant at 1.5% and include taxes and fees.

2% – Inflation (1.5%) – Taxes (1.5%) – Fees (1%) = -2.0%

A negative rate of real NET, NET return over the next 15 years is a very real problem. If I just held cash, I would, in theory, be better off.

However, this is why capital preservation and portfolio management is so critically important going forward.

There is no doubt that another major market reversion is coming. The only question is the timing of such an event which will wipe out the majority of the gains accrued during the first half of the current full market cycle. Assuming that you agree with that statement, here is the question:

“If you were offered cash for your portfolio today, would you sell it?”

This is the “dilemma” that all investors face today – including me.

Just something to think about.

via Zero Hedge http://ift.tt/2optJEV Tyler Durden