Authored by Michael Lebowitz via RealInvestmentAdvice.com,

The following article was originally a PowerPoint presentation that highlights several aspects of recent price movements across assets classes and within equity industry sectors. Many investors are unfamiliar with these relationships and their importance. While the current correction may prove only to be a speed bump on the way to higher prices, close inspection of asset class and security interactions often hold important clues about the future. The information contained in these pages argues for caution.

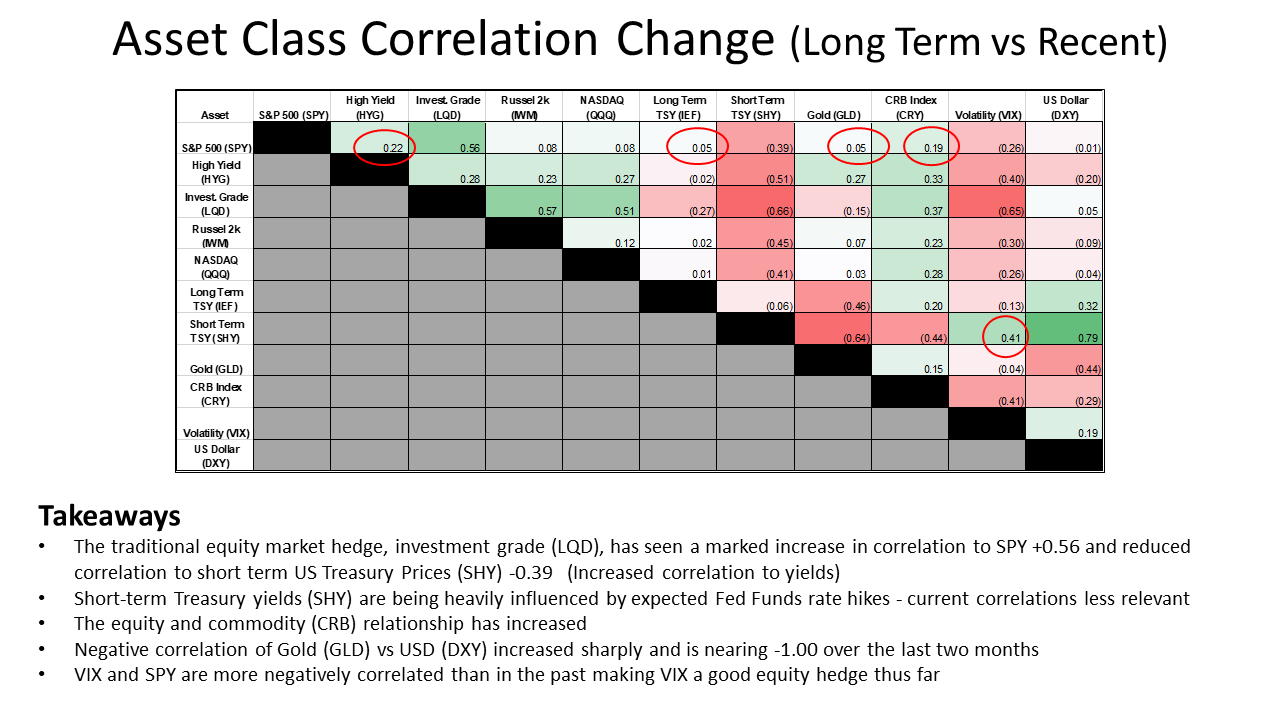

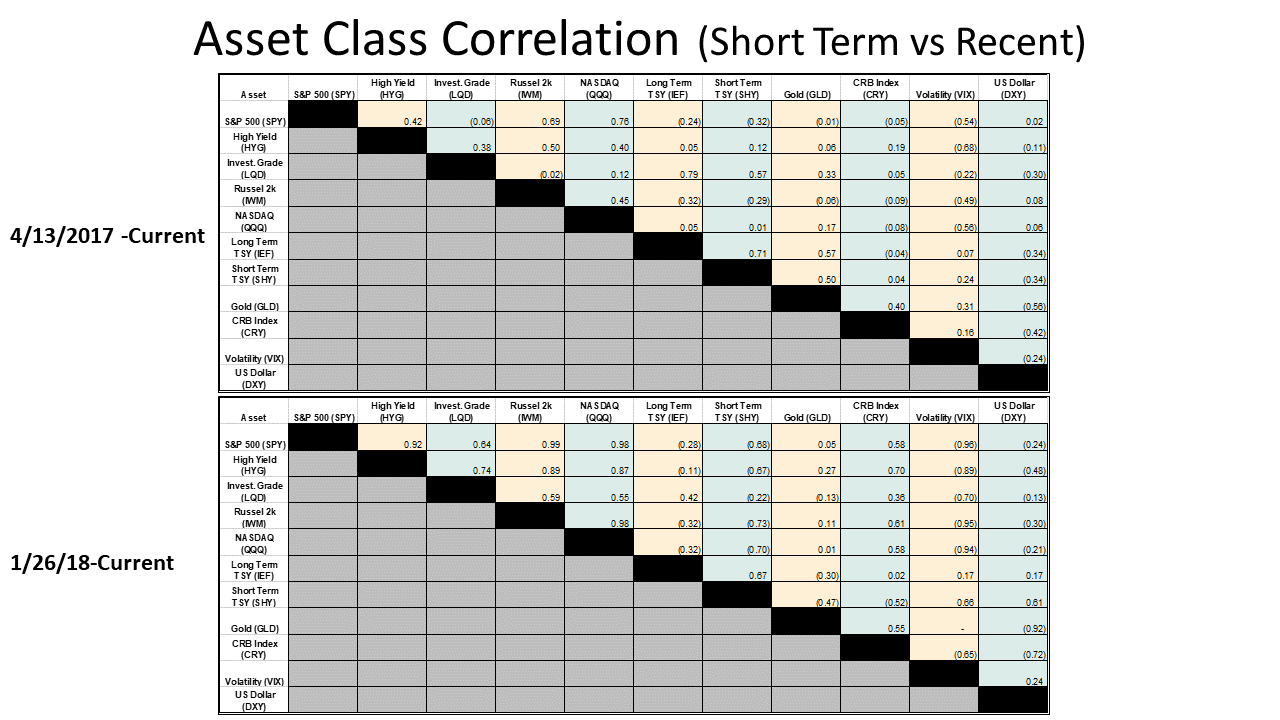

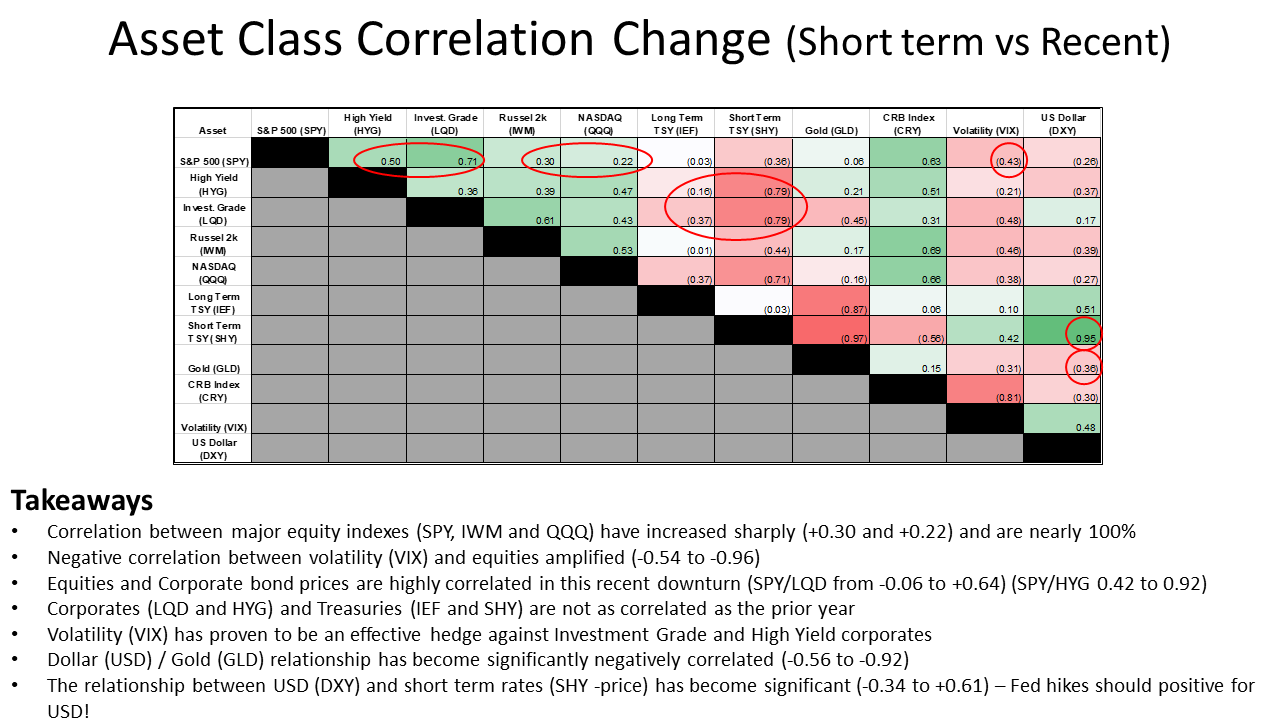

Click on any table below for a full size image making them easier to read.

Nowhere to Hide

The messages from shifting cross asset and S&P 500 sector correlations

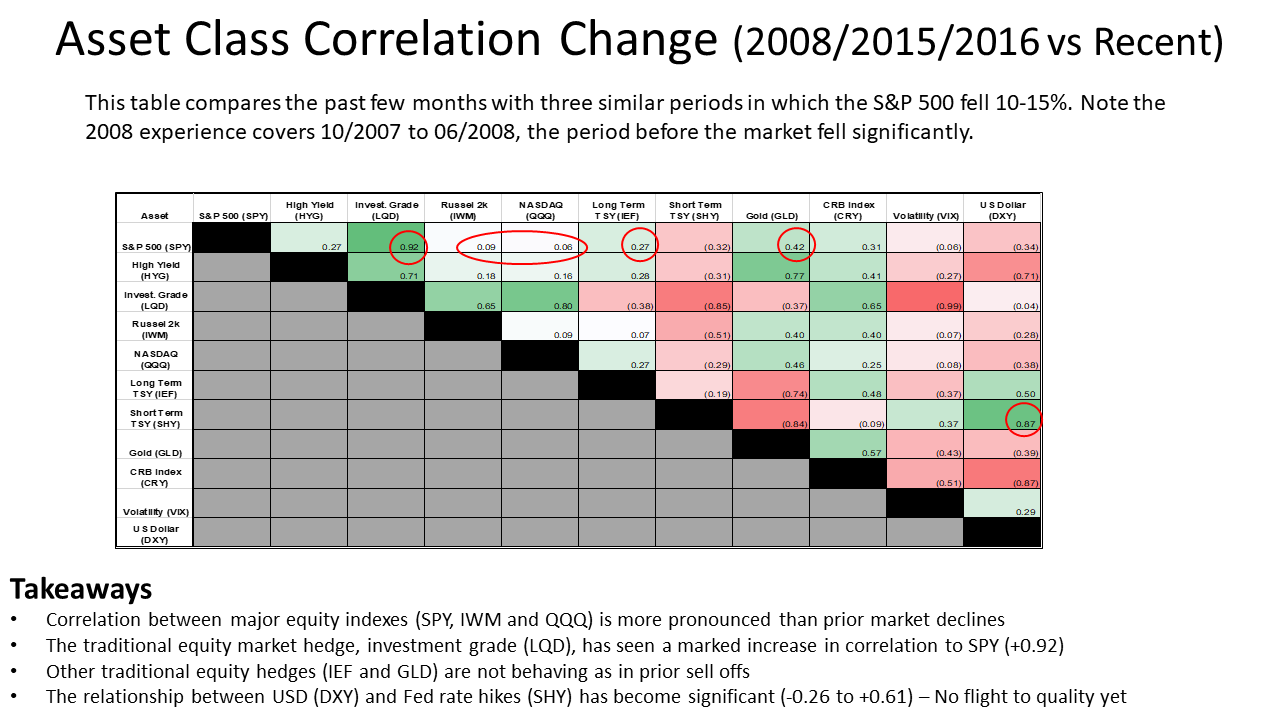

Why Correlations Matter

Correlation is a statistical measure that quantifies the relationship between two financial assets or securities. A correlation of +1.0 is perfect, meaning the two securities or assets move one-for-one with each other. A correlation of -1.0 means they move exactly opposite of each other. As correlations move away from +/- 1.0 the relationship weakens. A correlation of zero quantitatively implies no relationship in the movement between the two instruments.

Correlations between and within asset classes plays an integral role in portfolio management. From a big picture perspective, changing correlations can be a signal that broader market trends are changing. Investors may reduce risk during such periods. Also of importance, changing correlations may increase or decrease the value of “hedges” within a portfolio. For instance, investors tend to assume they are taking a more defensive posture moving technology to utility stocks, or from stocks to bonds when they sense a downturn coming. While such trades have been effective in the past, correlations allow us to observe changes and develop opinions about the future.

The following charts and notes provide recent and historical context on how correlations have changed since the equity market turned lower in late January. Whether these changes turn out to be a dependable warning of trend change, or a multi-month anomaly, is unknown. What is known is that the market is not behaving as it has for the last few years and investors should pay close attention to correlations for more market insight.

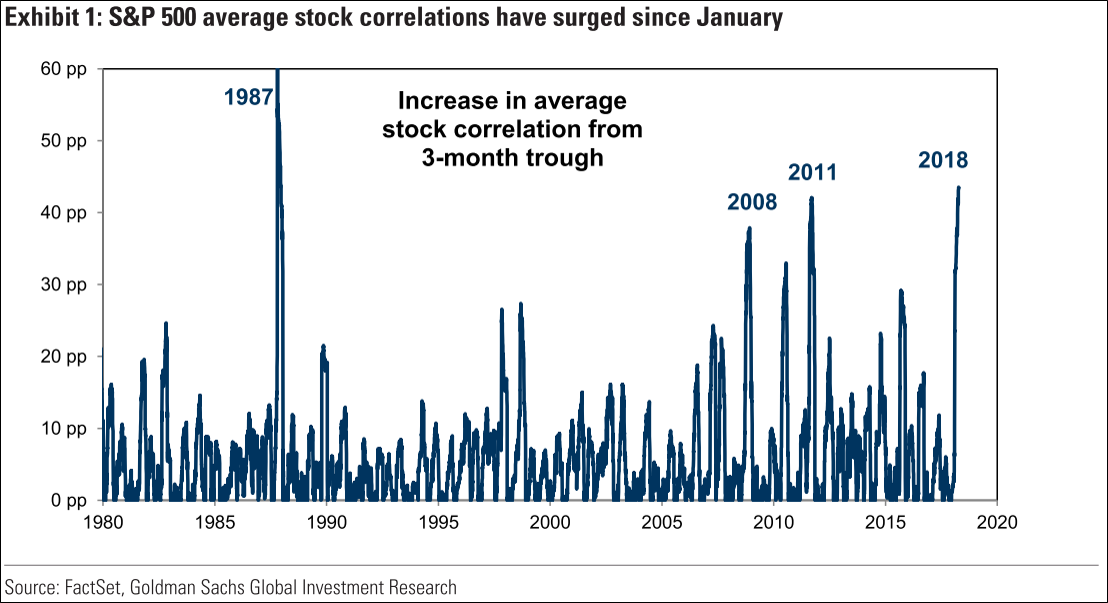

Under Appreciated Price Action

This graph, courtesy of Goldman Sachs, shows how correlations between S&P 500 stocks have increased at a rate greater than anytime in the last 40 years except 1987.

Cross Asset Correlations

S&P 500/UST Correlation

Given the popularity of formal and informal risk parity strategies, this graph showing the well below average correlation of the S&P 500 versus 10 year UST yields should be of vital concern if this equity sell-off continues and the correlation remains low.

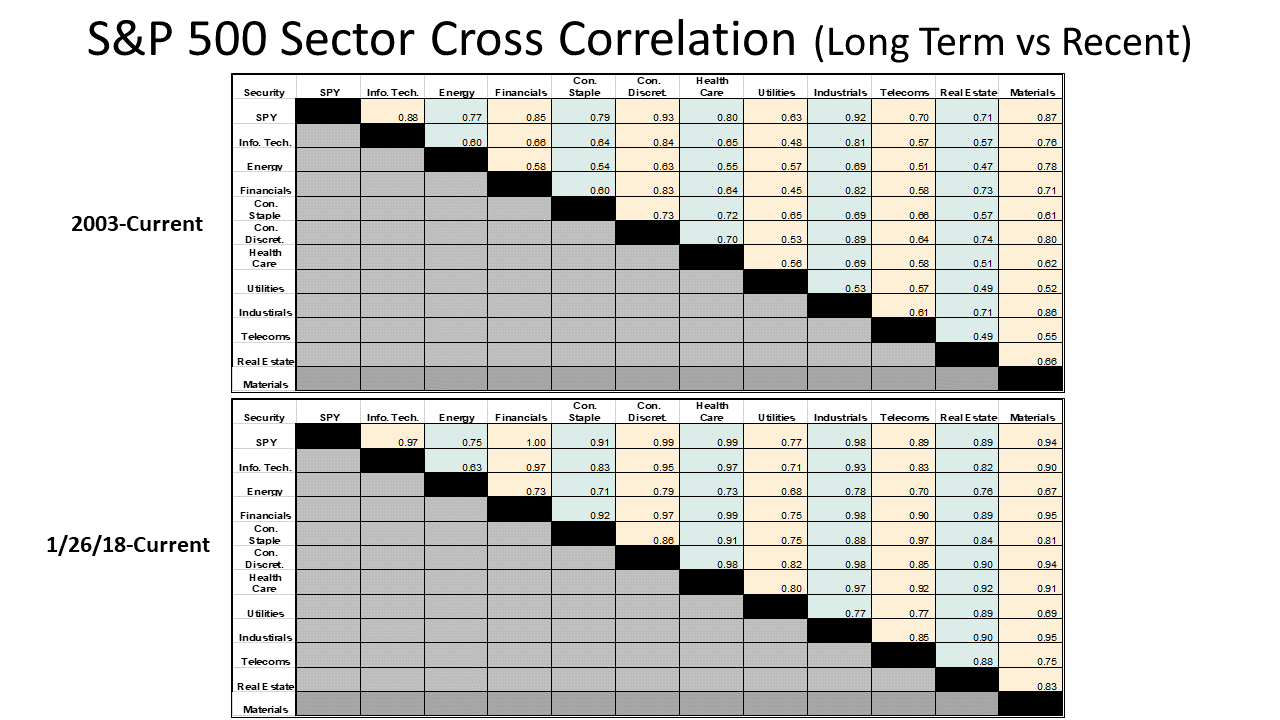

S&P 500 Sector Correlations

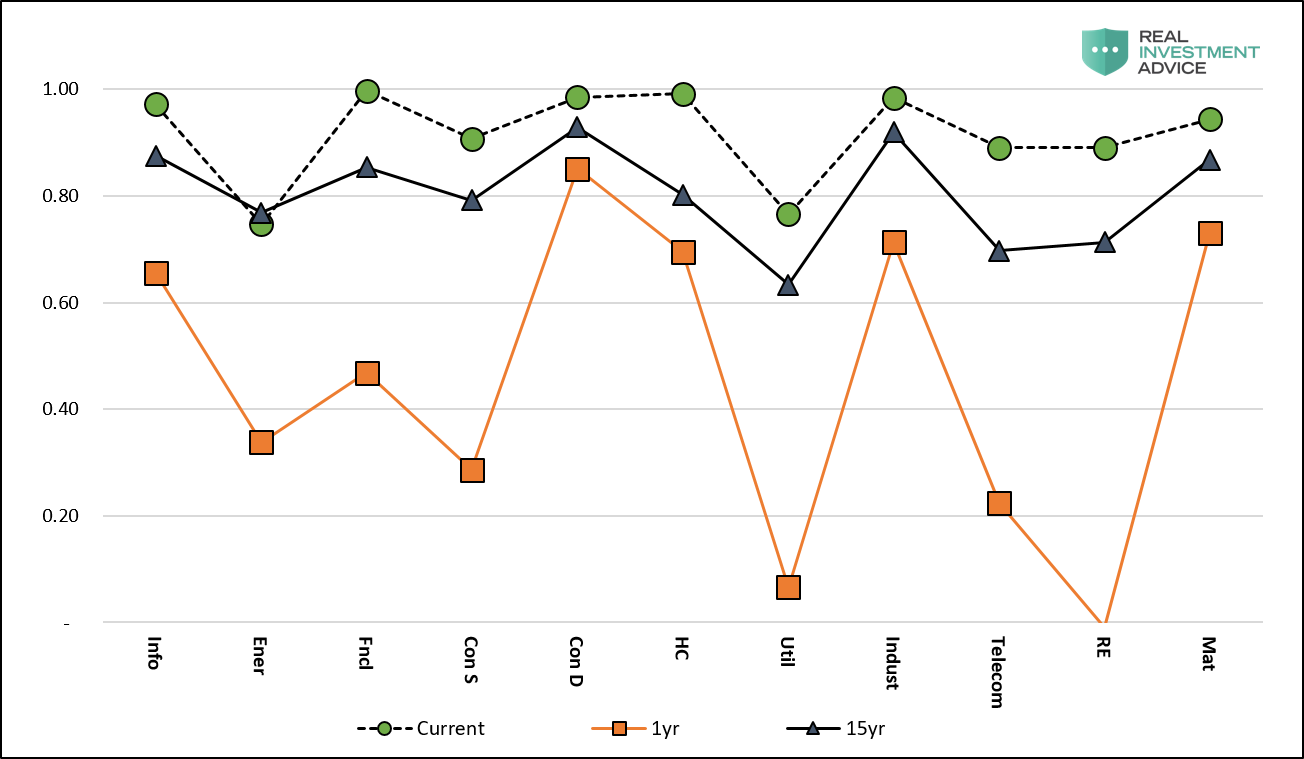

To further highlight the uniqueness of current sector correlations versus the S&P 500, this graph compares the current period (green dots) versus the prior year (orange squares) and the prior 15 years (gray triangles).

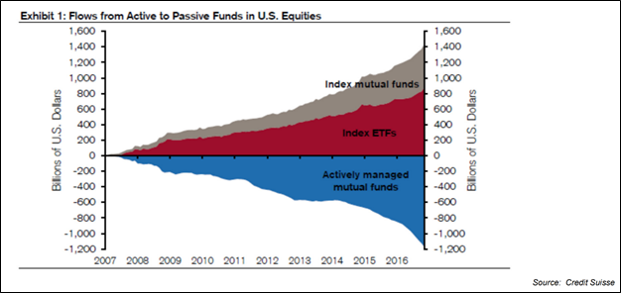

Something is different this time

This graph serves as a reminder that passive investing has grown significantly over the past 10 years. In our opinion this popularity will play a role in making it more likely that correlations between asset classes and sectors will behave differently in the next downturn than they have in the past. As such alternative hedging strategies should be considered now.

Conclusions

-

Passive funds and strategies have increased the likelihood that future correlations between asset classes and the S&P 500 and its constituents are higher

-

Equity and fixed income correlations have increased recently, rendering fixed income hedges for equities not as dependable

-

Gold and commodities as measured by the CRB index have also not been as good an equity hedge as in the past

-

Long equity volatility (VIX) has thus far proven a good ballast for stock and fixed income hedging

-

Traditional safety, low beta, equity sectors have been well correlated to other sectors and the equity market as a whole

-

Higher beta equity indexes (Russel 2k and the NASDAQ) have moved nearly perfectly in line with the S&P 500

-

It is too early to tell if the market is topping or just taking a breather, but the signals discussed in this article and others we did not highlight, should be taken seriously

via RSS https://ift.tt/2HuOvew Tyler Durden