Authored by Andrew Critchlow via S&P Global Platts blog,

Oil tankers ablaze in the Gulf of Oman and the US pointing the finger at Iran should be enough to send the price of the world’s most vital commodity skyrocketing.

Instead, oil prices have barely budged. Traders are not buying into the theory that Tehran wants a war, but they are worried about demand.

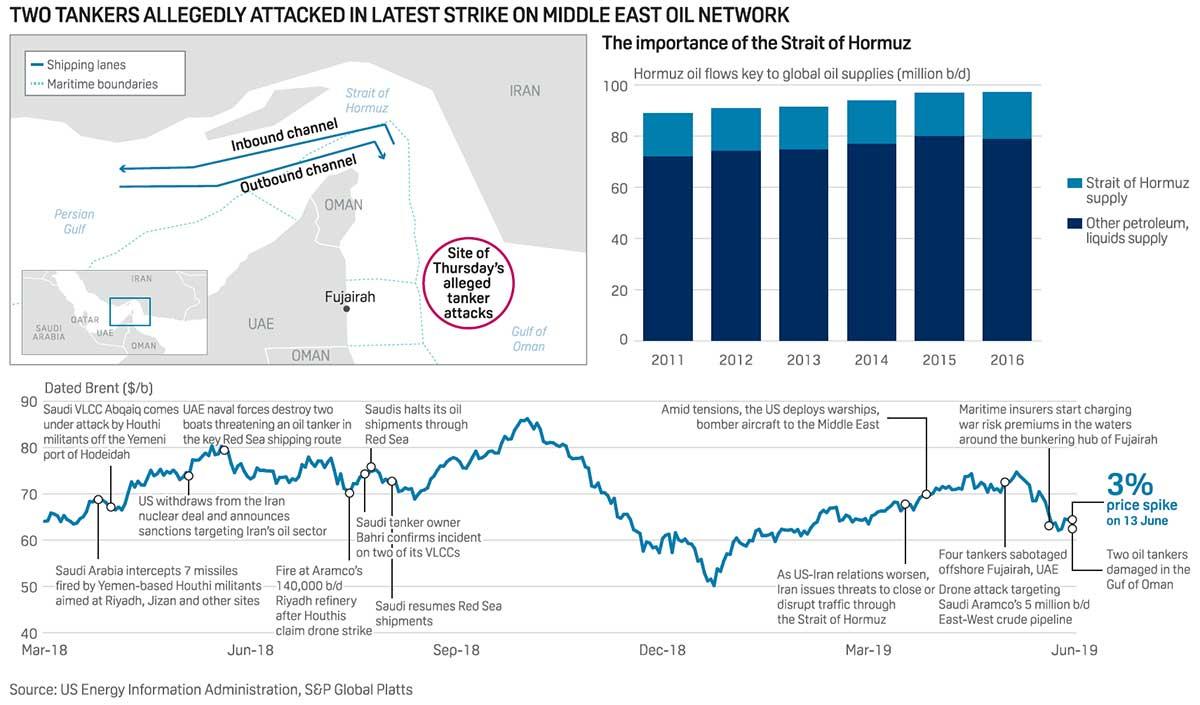

Dated Brent assessed by S&P Global Platts – the world’s most important oil benchmark – spiked by over 4% following the attacks on June 13 and traded briefly just above $62/b. On the face of it, this modest rise doesn’t reflect the risk to almost a fifth of the world’s oil shipped through the Strait of Hormuz, a narrow 21-mile-wide channel separating Iran from the Arabian Peninsula.

“I see the limited reaction in the crude oil market as an indication of traders saying ‘hang on a minute’,” said Ole Hansen, head of commodity strategy at Saxo Bank.

“If Iran did this it would be an open invitation to the US to step up its involvement and that should have sent the price much higher.”

Supporting Hansen’s point, crude had futures tumbled earlier in the week, with Brent falling below $60/b for the first time since late January, after data showed a larger-than-expected increase in US crude oil inventories.

Demand-side worries

The combination of rising stockpiles, tepid demand growth and fears of a slowing global economy has been enough to wipe $13 off the value of a barrel of Brent crude since May, despite the recent attacks on oil shipping and infrastructure in the Middle East.

Last week’s attacks were described by US Secretary of State Mike Pompeo as “an unacceptable campaign of escalating tension by Iran”.

Click for full-size infographic

The Islamic Republic has already been blamed for orchestrating clandestine attacks last month on tankers moored off the coast of Fujairah in the UAE. Tehran denies responsibility despite Iranian officials threatening to close down Hormuz, in response to US sanctions preventing the regime from exporting oil.

“The situation on the ground presents an intensely significant risk to oil markets that could unfold this summer,” warned RBC Capital Markets global head of commodities, Helima Croft in a research note following the attacks.

“While many market participants see the recent security incidents as business as usual for the region, we see an abundance of escalation risks in large part because the US sanctions are subjecting Iran to almost unprecedented economic pain.”

Instead of fretting about what could happen, traders have continued to focus their minds on the fundamentals of supply and demand. US crude inventories climbed 2.21 million barrels at the beginning of June to 485.47 million barrels. America’s stockpiles of crude – excluding its strategic reserves – have added almost 50 million barrels to their tanks since the end of the first quarter.

Meanwhile, crude production has increased by 1.4 million b/d from a year ago, solidifying America’s positions as the world’s biggest producer ahead of Russia and Saudi Arabia, according to official data.

Forecasters are also toning down their oil market predictions. The International Energy Agency on June 14 reduced its estimate for daily demand growth this year by 100,000 barrels to 1.2 million b/d, signaling more bearish sentiment for crude. OPEC itself has also warned of the impact a trade war between China and the US could have on oil markets. The cartel has revised down its own demand growth projections for the second half of the year.

“The pressure from lower demand growth, confirmed by all three major forecasters this week and the counter seasonal rise in US crude stocks continues to weigh,” warned Saxo’s Hansen.

OPEC has few options

Given the facts, OPEC has little choice but to extend its 1.2 million b/d of production cuts and do everything necessary to hold its alliance together with Russia if it wants to boost prices.

There is also an argument for even deeper cuts, but this would risk losing more market share to the US. However, the group is struggling to even agree a final date for its next policy setting meeting after Russia requested a timing change.

Of course, Iran’s leaders oppose any rescheduling of OPEC meetings in the current environment. The Islamic Republic’s vital oil industry is already feeling the full impact of sanctions and has received little support from its partners in the Vienna-based group, which is dominated by Saudi Arabia. Output last month plunged by almost 230,000 b/d to just under 2.2 million b/d after waivers allowing eight countries to buy Iranian crude expired.

Traders may believe Tehran’s denials that it is trying to provoke a war with the US by sticking limpet mines on tankers, but they cannot ignore it is playing with fire by mixing politics with oil.

“The risk of miscalculation in the Middle East is clearly rising,” warns Paul Sheldon, chief geopolitical adviser at S&P Global Platts Analytics.

via ZeroHedge News http://bit.ly/2WM4tYp Tyler Durden