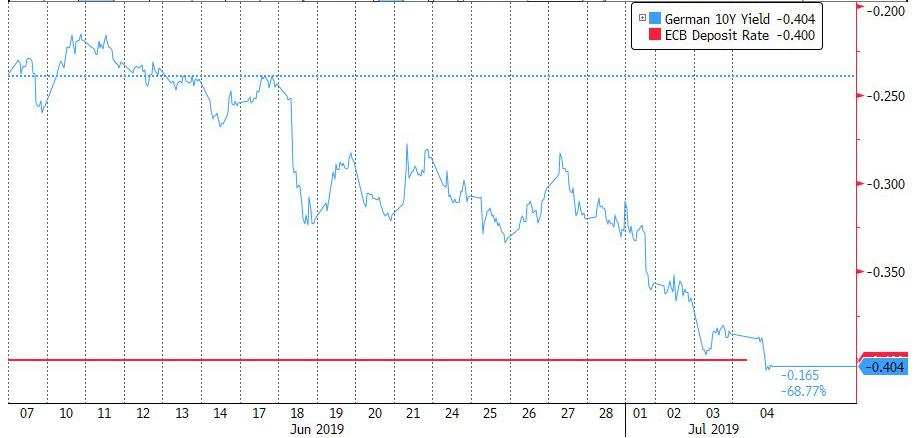

For the first time ever, the yield on the German 10Y Bund, considered as Europe’s go to safe asset, dropped below the ECB’s -0.40% deposit rate, as consensus forms that the ECB will cut rates by at least 10bps in September, if not sooner especially with Christine Lagarde – widely perceived as just as dovish as Mario Draghi if not more – set to head the ECB.

“The markets are really saying we expect more from the ECB,” Marilyn Watson, head of global fundamental fixed-income strategy at BlackRock told Bloomberg TV. “We expect yields to go lower still.”

The inversion is notable because while the ECB can buy bonds that yield less than the deposit rate, priority is given to those that still offer a premium…. although in Germany, only 15% of the entire bond universe still has a positive yield as 20-year yields also turned negative this week and the 30Y set to follow soon.

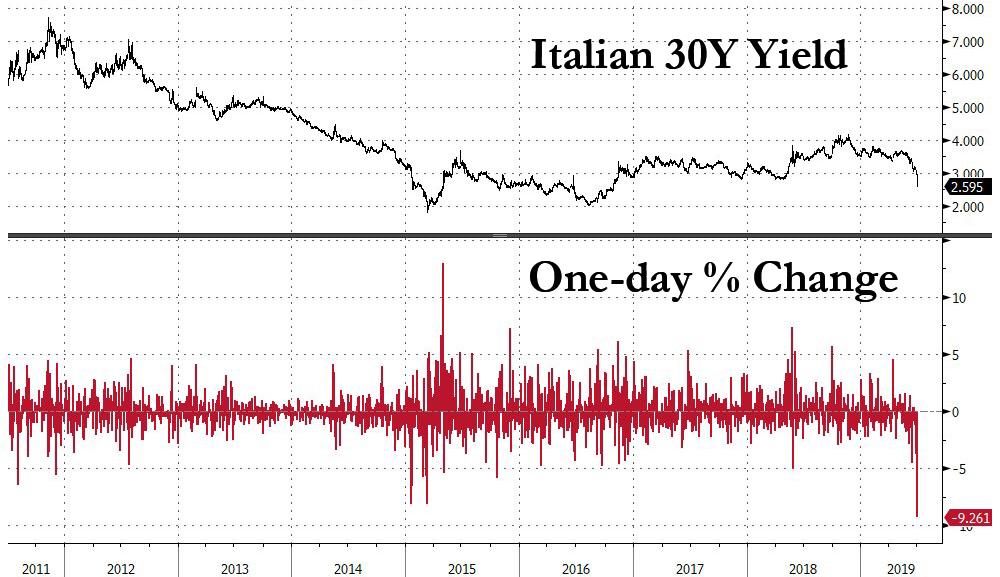

This latest curve inversion, which signals that a European recession is looming, has spurred investors to buy riskier assets such as 30 Year Italian bonds, which yesterday saw their biggest one day gain since Draghi’s 2012 “whatever it takes” speech.

10-year German bund yields fell 8bps this week to a record-low minus 0.41%. Italian bonds have outpaced the bund rally to narrow the spread between the two to below 200 basis points Wednesday, the lowest since May 2018.

Germany joins the global curve inversion party, where the U.S., Japan, Canada and the U.K. all now have benchmark bond yields below the central bank’s key interest rate.

Meanwhile, confirming that Albert Edwards’ deflationary “ice age” is upon us, 10Y bonds from Belgium, France and the Netherlands have already joined the sub-zero club, which now amounts to a record $13.4 trillion in negative-yielding debt.

Predictably, as Bloomberg notes, European governments are cashing in, with both Spain and France auctioning debt at record-low borrowing costs on Thursday. France sold a total of 10 billion euros of 10- and 15-year bonds at record-low yields, while Spain sold 3.5 billion euros of debt across the curve.

And while the “Ice Age” is only set to get colder as the world slows down, ADM Investor Services strategist Marc Ostwald warned that the huge stock of bonds yielding below zero might pose risks if the global economy shows signs of a rebound in the second half of the year: “There’s too much cash looking for a safe haven home,” Ostwald said. “Bonds are in for a rough ride.”

Finally, courtesy of Bloomberg’s Tanvir Sindhu, here are some remarkable stats as global bond yields hit all time lows:

- Year-to-date EGBs returns led by Greece (23%), Spain (10%), Portugal (9.8%) and Belgium (8.8%)

- Around 25% of global debt now has a negative yield, amounting to a record high of $13.4 trillion

- The entire core and semi-core European government bond spectrum out to 10-year is trading in negative yielding territory

- Around 85% of the German government curve trades below 0%

- Around 55% of Spanish government debt has a negative yield (with selective carry the place to be this year, see more here and here)

- Italian front-end goes negative as BTPs turbo-charged sending 10Y lower by ~50bps in the five days through Wednesday, the largest such move since June 2018

- Around 75% of Japanese government debt trades below 0%, highlighting the importance of yield-thirsty flow from Japan into the global bond markets (see examples of analysis here and here on this theme)

- Around 80% of the active covered bonds of Germany and France, 83% of Spain and 57% of Denmark have negative yields

- EUR 5y5y inflation swap has given back nearly all of the post-Sintra spike; the ECB needs to restore some inflation credibility, which should be the trigger for 10Y Bund yield to move back toward 0%, helped by positioning being built at yield lows

via ZeroHedge News https://ift.tt/2RSB4ef Tyler Durden