Submitted by Joseph Carson, Former Director of Global Economic Research, Alliance Bernstein

The Phillips curve has been dormant for over two decades, as the dynamic between tight labor markets and inflation has virtually disappeared. Yet, the demise of the Phillips curve should not be used as a reason for policymakers to think it is safer to run with a more stimulative monetary policy.

The transmission of modern day monetary policy works mainly through the asset markets and shifts the balance of risks towards asset cycles and financial stability. Decision to ease monetary policy today against a backdrop of record asset values would be tantamount to easing policy at the peak of previous high inflation cycles.

In testimony before Congress, the Fed Chair Jerome Powell acknowledged that the linkage between unemployment and inflation has been broken for at least 20 years ago. A number of fundamental and technical factors have come into to play in the past two decades to alter this relationship.

For example, in 1998 the Bureau of Labor Statistics (BLS) determined that it could no longer find an adequate sample of owner-occupied housing to safely ensure an accurate measurement of owners rent so BLS decided to rely exclusively on the survey data from the rental market to measure both owner’s rent and apartment rents, even though the two markets are fundamentally different.

Measurement changes for technical reasons tend to be of minor importance but in this case the risk of altering the behavior of reported inflation as well as its relationship to other series was high for two reasons; first, the owner’s rent is the single largest component, accounting for over 30% of the core consumer price index; and, second, it was being replaced with a rent series that tends to move countercyclical, or the opposite direction of house price inflation.

Here’s a quick glance at how the owners rent series tracked housing prices under the original and new measurement practices.

During the 15-year period (1983 to 1998) when BLS used the original owner’s sample, the owners rent index rose cumulatively 74%, nearly matching the 72% increase in house price inflation as measured by the S&P Core Logic Case-Shiller series. Yet, during the housing boom period of 2002-06 when house price inflation jumped 50%+, the new owners rent index showed a cumulative increase of only 15%.

The near disappearance of housing inflation from reported inflation is mainly technical, but it did contribute (a lot) to the breakdown in the Phillips curve. Meanwhile, the loss of the house price signal should not be interpreted that real asset inflation is any less important to the economy’s performance or to monetary policy. Yet, from an operational standpoint for monetary policy the change moved housing inflation from the inflation-targeting bucket to the financial stability mandate.

Why is this important? Monetary policy feeds asset cycles through the same channels (interest rates and expectations) as it does general inflation. Yet, policymakers treat asset cycles differently believing that supervision and regulation—as a substitute for tighter money— is a better approach to promote financial stability.

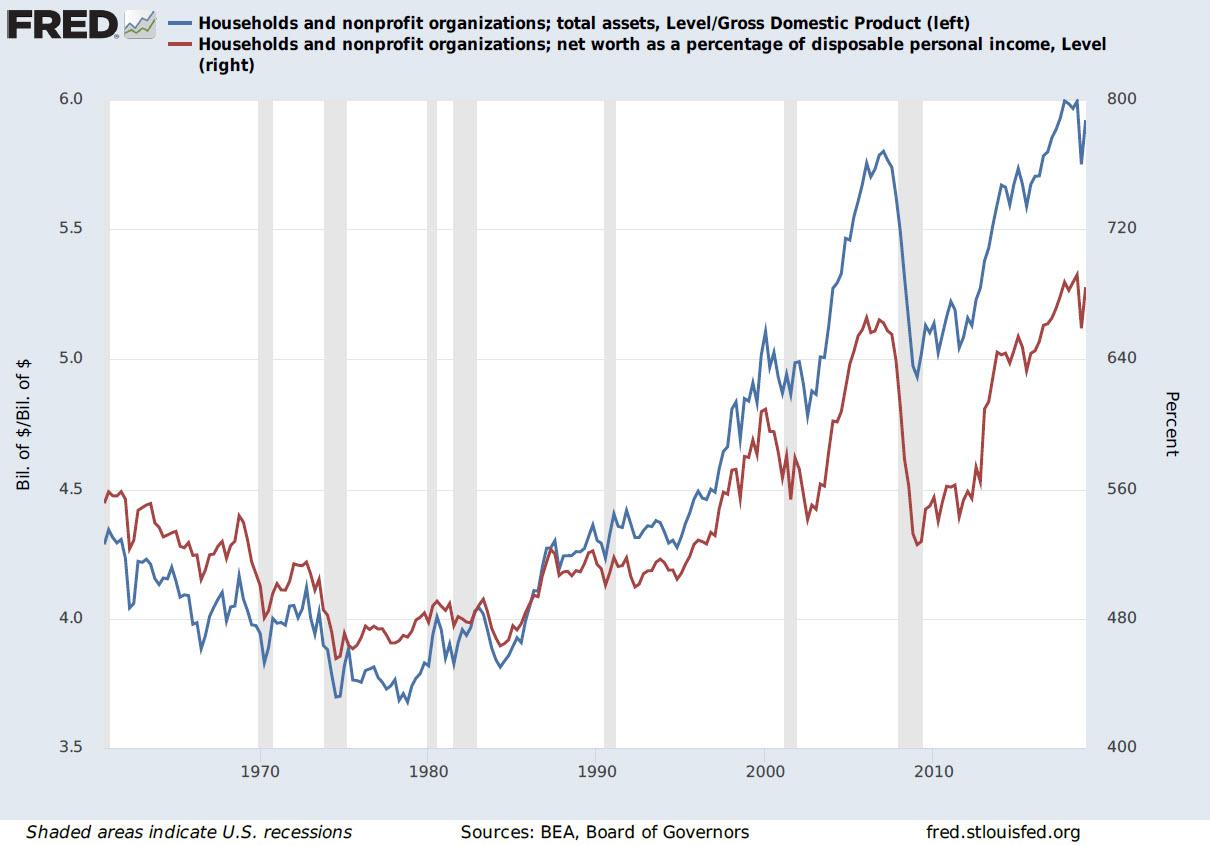

It always difficult to prove causation but its hard to deny the recurring pattern of boom/bust asset cycles ever since this two-prong policy has been used in the past two decades. Moreover, the tipping point for the last two recessions came from destabilizing excesses in the asset markets and not from imbalances tied to general inflation. Today’s readings on asset values – relative to nominal income and GDP – exceed those of the dot.com and the housing bubble.

Each generation of policymakers has had to deal with fundamentals changes in the economy, and with the changing transmission and channels of monetary policy. During the high inflation cycles of the 1970s, policymakers misread inflation dynamics leading policymakers to believe that by accommodating the inflation cycle it would extend the economic cycle. That did not end well. Are policymakers nowadays falling into the same trap, misreading the dynamics of asset cycles believing that by promising more easy money it will help extend the economic cycle, while overlooking the risks to financial stability?

The Phillips curve might be dead, but its “ghost” lives on in the “Asset” curve (or the new dynamic between monetary policy and asset cycles). Policymakers should proceed with caution.

via ZeroHedge News https://ift.tt/30McJdq Tyler Durden