Grant’s Almost Daily, submitted by Grant’s Interest Rate Observer

Keep digging

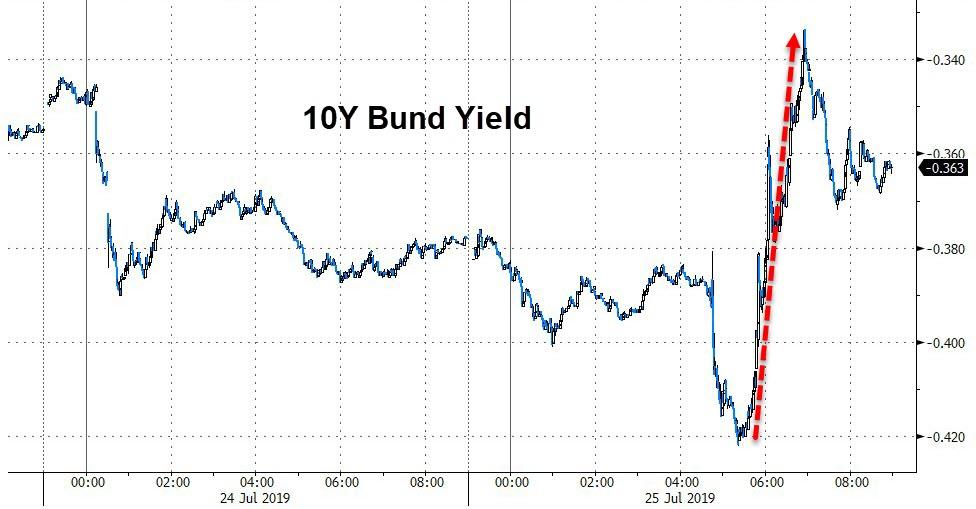

Yesterday, the European Central Bank held a stand-pat meeting, keeping the benchmark deposit rate at negative 40 basis points.

However, ECB president Mario Draghi indicated that rate cuts and a resumption of asset purchases are on tap for September. In the accompanying presser, the outgoing ECB chief captured the mood of central bank-levitated markets, stating that: “it’s difficult to be too gloomy today,” while the outlook “is getting worse and worse.” The German 10-year yield traded as low as negative 42 basis points, briefly crossing below the 40 basis point deposit rate.

While sovereign debt holders continue to rack up mark-to-market gains, not everyone is enamored with the prospect of still-more negative interest rates.

“We already have a devastating interest rate situation today, the end of which is unforeseeable,” Peter Schneider, who represents banks in the south-eastern German state of Baden-Württemburg, told Bloomberg yesterday.

“If the ECB aggravates this course, that would hit not only the entire financial sector hard, but especially savers.”

Meanwhile, policymakers down under attempt to quantify the practical limits of negative policy rates. In a paper written to New Zealand finance minister Grant Robertson in January and recently released to the public, staffers in the Treasury Department concluded:

“The Reserve Bank expect rates could only fall at most 35 basis points below zero before risking the hoarding of physical cash.”

Today, the global stock of negative-yielding debt rose to $13.74 trillion, a new record.

Yellow light

As we close out month 121 of the longest economic expansion on record, let’s take a look at the state of U.S. corporate credit. Year to date, investment-grade bonds have generated a whopping 12.3% total return, while high-yield has returned 10.6%. Leveraged loans have lagged far behind, with the LSTA Index gaining just 3.3% so far this year.

That standout performance from investment-grade comes as fears of an economic slowdown percolate, while the Fed’s dovish turn has raised the relative value proposition for fixed rate IG and high-yield bonds over floating-rate loans. U.S. leveraged loan funds saw a $446 million outflow for the week ended July 17 according to Lipper, extending the streak of withdrawals to 35 straight weeks.

As loan demand cools, yields for the most creditworthy portion of collateralized loan obligations (which purchase and securitize leveraged loans; see the Sept. 7, 2018 edition of Grant’s for more) continue to climb. According to S&P’s LCD unit, spreads of triple-A CLO tranches reached a post-crisis low of 93 basis points above Libor in March, from 130 basis points in February 2017. Since then, they have reversed higher, with the index rising to 109 basis points in May, while some recent issues have come in well above that. Oaktree Capital Management L.P.’s CLO 3 triple-A tranche priced at 128 basis points above Libor on July 17, and Pikes Peak CLO 4 saw its triple-A slice set at 137 basis points over Libor on July 12.

While high yield has enjoyed a gangbusters 2019, investors have retained some reticence, as a Bloomberg story from July 18 notes that buyers are prioritizing “large, liquid issues as the economy slows. That defensive posture has led to oversubscribed offerings from higher-rated and well-known borrowers.” Sure enough, the triple-C-rated cohort of the high-yield index has lagged the group, logging a year-to-date gain of 7.6%. Despite that quasi-defensive posture on the part of investors, high-yield remains “extremely overvalued,” according to an analysis yesterday from Marty Fridson, chief investment officer of Lehmann Livian Fridson Advisors LLC.

In an investor letter circulated today, Greenlight Capital founder and president David Einhorn concurs, revealing that his fund has taken a short position against U.S. corporate credit:

Over the past few years, corporate debt has expanded dramatically, while covenant packages and other bondholder protections have weakened considerably.

Rating agencies have been complacent and allowed debt to Ebitda and debt to equity ratios to deteriorate without a corresponding reduction in credit ratings. Meanwhile, we are a decade into an economic recovery and there are signs the economy may be slowing.

via ZeroHedge News https://ift.tt/32SVsRL Tyler Durden