“This Is Remarkable”: For The First Time Ever, Companies Missing EPS Are Surging (By The Most On Record)

Following a decade during which markets learned that economic data is irrelevant in a time when central banks are injecting trillions in liquidity and corporations are issuing trillions in debt to repurchase trillions in stocks pushing the S&P to all time highs, one can now say the same about corporate earnings, initially in Europe and soon in the US, where Q3 corporate earnings are set to post their first decline in three years.

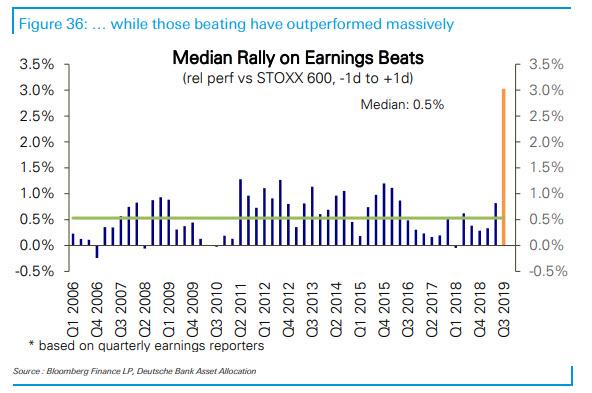

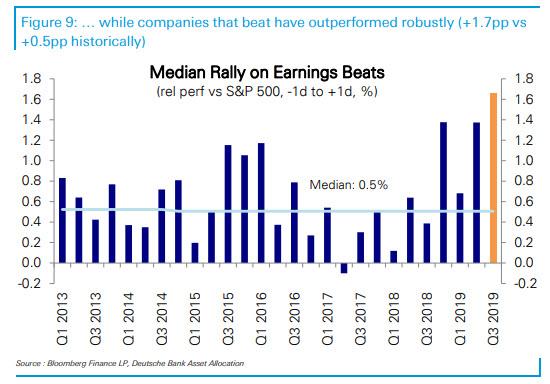

As the following remarkable chart from Deutsche Bank shows, we have reached a point where not only are earnings misses by European companies not punished, but they are being rewarded by the most on record, resulting in a median rally of 0.5% after a company reports an EPS miss!

As for those rare Stoxx 600 companies that beat depressed EPS expectations, well the reward is unlike any seen before, with the median post-earnings rally for the victorious stock rising to an all time high 3.0%.

And while Europe is clearly impacted by the recent return of QE, where the ECB is now purchasing €20BN in bond each month even as rates were recently cut to a record low -0.50%, what can one observe about the US?

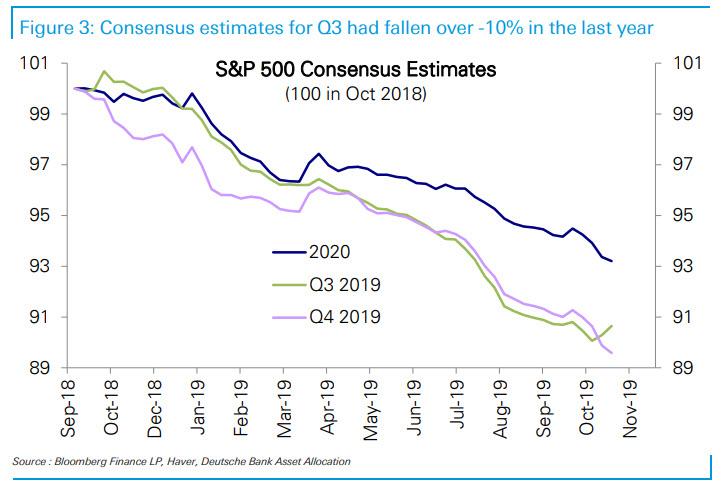

As Deutsche Bank strategist Binky Chadha writes, following persistent downgrades of S&P500 earnings, which are down 10% over the past 12 months…

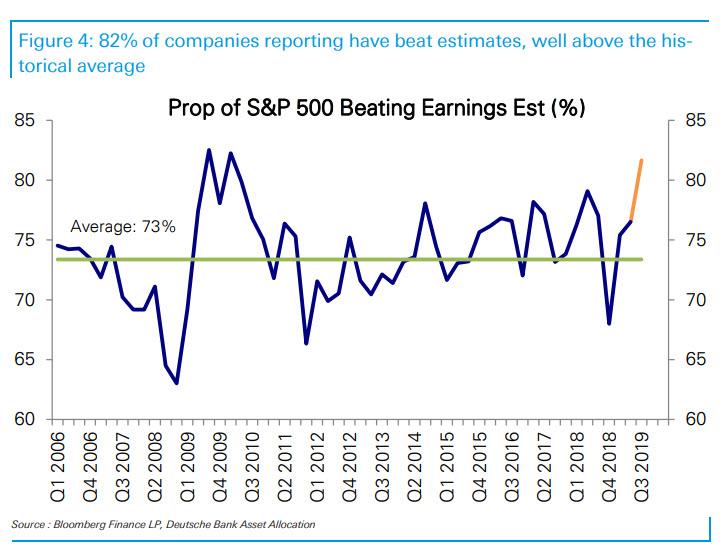

… Q3 earnings are beating at a slightly above average historical rate.

Some more details:

A third of the way into earnings season (169 companies, 37% of S&P 500 market cap), 82% of companies reporting have beat, with the breadth better than the average 73%. Companies have beat by 4.4% in aggregate, slightly better than typical (3.4% historical average). Sales have beat by 1.2% (0.3% historical average), with 65% above consensus (56% historical average). Elsewhere the earnings season is not as far advanced, but the early read is similar.

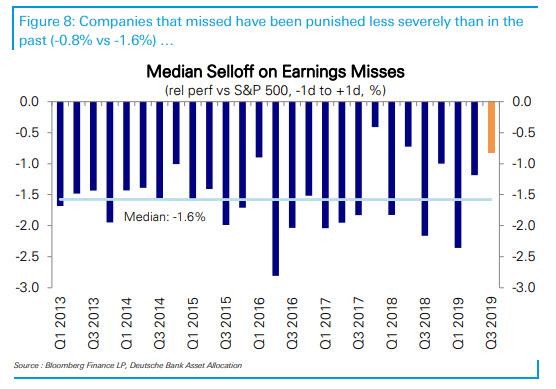

Yet where the US differs from Europe, for now, is that there is still a modest, if clear, negative reactions to misses unlike the Stoxx, where missing companies are now rewarded.

That said, just like in Europe, the violently bullish reaction to beats suggests the slowdown was well priced in, according to Chadha.

Some other observations from Deutsche Bank: while we have yet to pass the midpoint of earnings seasons, headline earnings are roughly flat (as a reminder, consensus is for annual EPS to decline despite record buybacks)…

… but the median company continues to fare much better (6-7%).

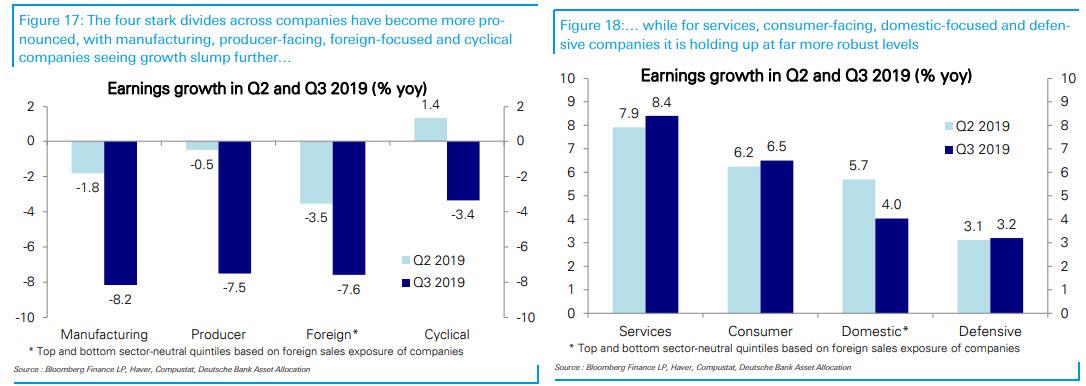

As one would expect, there are big divides between manufacturing (-8.2%) and services (+8.4%); producer- (-7.5%) vs consumer-facing (+6.5%); foreign- (-7.6%) vs domestic-sales (+4.0%); and cyclical (-3.4%) vs defensive (+3.2%) companies. Forward estimates continue to fall, but remain high relative to expectations for macro growth.

Finally, should earnings be bottoming, a rebound won’t be due to an improvement in the economy. As DB notes, global growth forecasts point to earnings growth in the low- to mid single digits for next year, well below the double digit rates projected by the bottom up consensus.

That said, the bulk of the earnings rebound is expected to be from the groups seeing the biggest declines currently, leaving them the most vulnerable to downgrades. Finally, the answer whether that means that soon we will see those groups rebound after missing expectations will have to wait until next quarter.

Tyler Durden

Mon, 10/28/2019 – 12:15

via ZeroHedge News https://ift.tt/2PnlyIh Tyler Durden