Fed’s Third “Year-End” Repo Oversubscribed Again Amid Liquiduity Scramble As Dec 16 Tax Day Looms

One week after the Fed’s second 42-day term repo which allowed dealers to lock in funding into the new year and which was again oversubscribed, confirming a growing scramble for year-end funding, traders were looking ahead to the result from today’s third “year-end” repo, this time with a 28-day term maturing on January 6. And, as we noted last week, year-end liquidity fears remain front and center as the $25 billion – which the Fed expanded from $15 billion late last week – proved to again be roughly 40% below the required size to satisfy all liquidity demands.

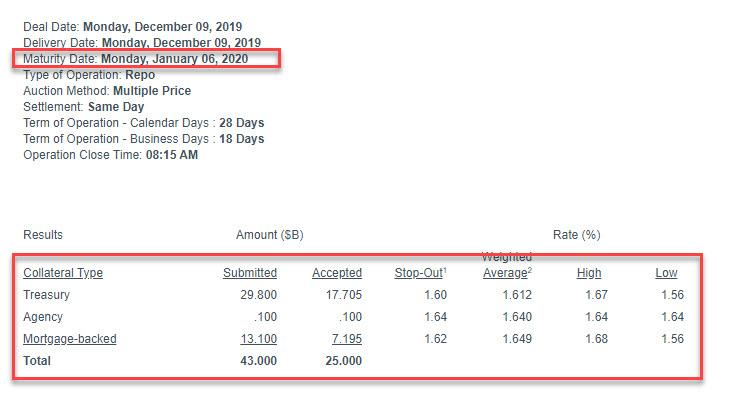

Dealers submitted $43 BN in bids for the 28-day op ($29.80 BN in Treasurys, $0.1BN in Agency, $13.1BN in MBS paper), resulting in an oversubscription of the $25BN in available repo, and confirming that the Fed may have to add additional “year-end” repos to satisfy all dealer liquidity demand as we enter 2020.

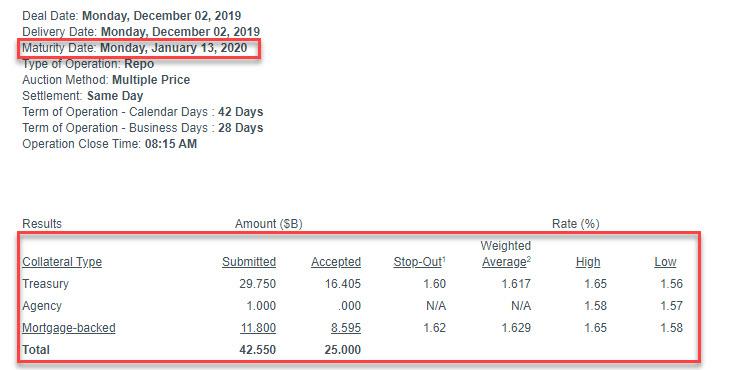

This was modestly above the $42.550 billion submitted last week in the second 42-day repo operation conducted on December 2:

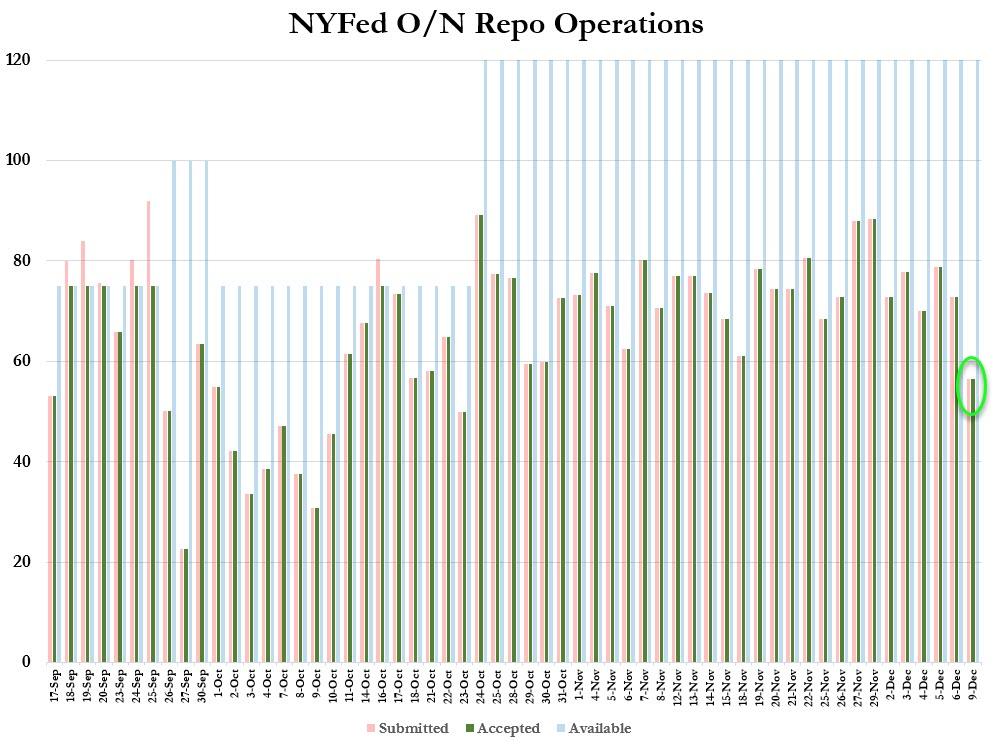

At the same time, the Fed also announced that in the latest overnight repo, it had accepted $56.4 billion in securities, a modest drop from the recent range and the lowest roll amount since the Fed expanded the available size of overnight repos to $100 billion. A big reason for this is likely that $25 billion was shifted over from overnight to 28-day term repos.

The biggest concern: the repo rate over year end remains stubbornly stuck well above 3%, more than double the Fed Fund rate, and clear evidence that the US interbank plumbing remains broken.

It remains a pressing question for funding markets why, even with QE4 in place and now daily overnight and short-term repo operations in place, banks continue to rush to lock in year-end liquidity, where some fear a similar explosion in overnight repo rates as was observed on Dec 31, 2018 when General Collateral soared amid a widespread liquidity shortage. Indeed, even with the Fed’s commitment to continue providing liquidity to the financial system around year-end, the market is still showing concerns, indicating that for all its telegraphed firepower, the Fed has failed to calm markets and ease counterparty risks which as the BIS observed yesterday, now involve hedge funds.

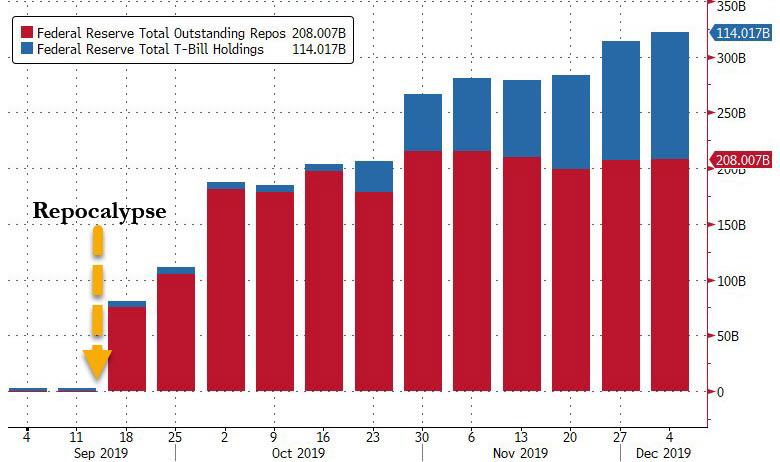

As a reminder, since the Sept 16 repo blow up, the Fed has injected $208 billion via “temporary” rolling overnight and term repos, and $114 billion via permanent T-Bill purchases.

What is even more troubling is that in just 6 days, the next major potential crack in the repo market is due: on Dec. 16 there is a tax payment day looming; that’s when cash is drained from the banking system, similar to the Sept 16 tax payment which many alleged sparked the original repo crisis, and as Bloomberg’s Marcus Ashworth notes, “with the repo rate over the year end more than double the Fed rate of 1.5%-1.75%, this is not proving to be a temporary problem.“

Tyler Durden

Mon, 12/09/2019 – 08:53

via ZeroHedge News https://ift.tt/2qwtEEi Tyler Durden