With VIX Hitting 50, The Fed Must Now Step In Or A Catastrophic Crash Is Inevitable

With stocks tumbling, the VIX has, predictably, soared, briefly tipping above 50 intraday on Friday and last trading above 46, surpassing the levels hit during the Volmageddon in Feb 2018 and the highest level since the US credit rating downgrade in August 2011.

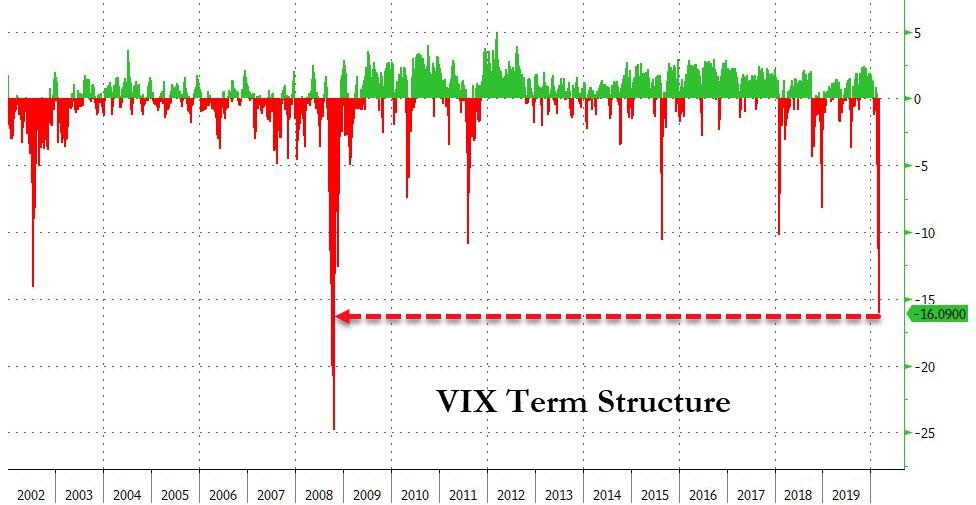

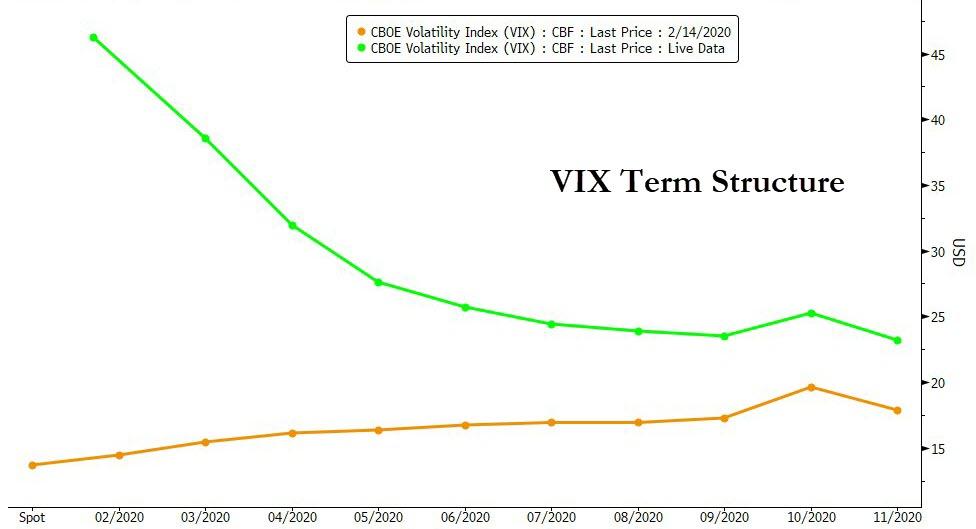

Just as dramatic is the accelerating VIX term structure inversion, which has pushed the curve to the steepest backwardation since the financial crisis…

… as spot has exploded higher even as the move in futures has been far more normal.

But while we have extensively discussed the ongoing equity crash where realized vol has soared, and has been a direct factor in the surge in implied volatility, there is another, potentially far more dire impact that the soaring VIX will have on the cross-asset universe, one that could potentially unleash a historic crash driven by the one pillar that has so far supported the US economy and stock market: credit.

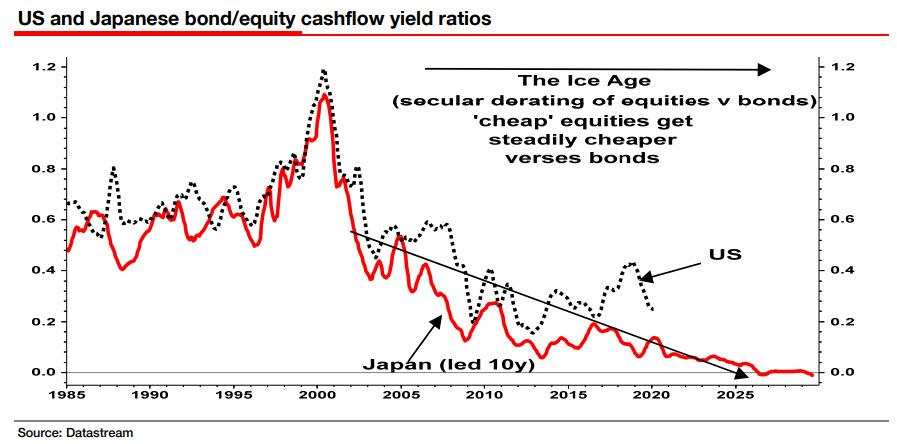

What sparked our concern was the latest note from SocGen’s Albert Edwards, who laments the ongoing collapse in yields, which he had fully predicted in the past as part of his Ice-Age thesis (at least until MMT steps in and blows yields up into the stratosphere as the monetary endgame begins) and is familiar to anyone who has followed Edwards’ writings over the years. We won’t spend much time on this part of his note, suffice to point out that the unprecedented plunge in yields may be just the beginning now that the Japanification of the US has begun in earnest, and that we are nearing that tipping point for yields beyond which further downside becomes a negative for risk assets as it no longer stimulates equity buying in contravention to the Fed Model, or as Edwards puts it, “If Japan remains the template, much more downside lies ahead for the US .”

One final point on where Edwards see stocks headed to if he indeed right, and further yield declines turn negative for risk:

The lesson from the recent landmark move in the 30y US T-Bond yield below the equity dividend yield is simple. If we are right and US 30y yield falls below zero, US PEs will contract from their lofty 19x forward earnings peak seen recently, especially in a likely recession. Try 8x instead at the bottom of the next recession and see where that takes us!

Shifting attention from stocks to credit, this is where things more interesting.

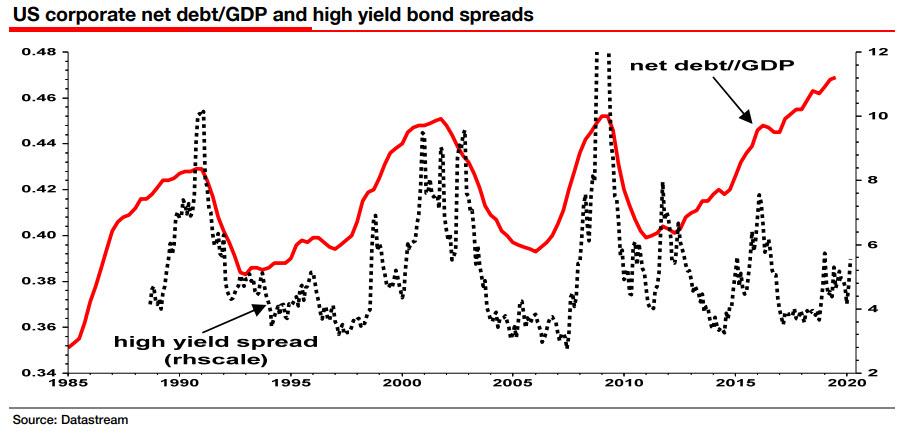

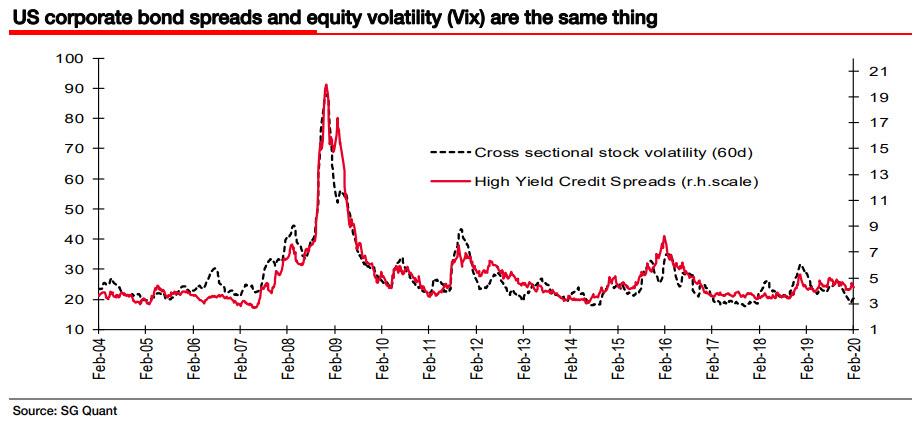

Addressing the massive credit bubble that was built up over the past decade on the back of record cheap debt, and where trillions in BBB-rated issuance was used to repurchase stock pushing stocks to mindblowing levels even as most investors pulled money from the market for the past several years, Edwards reminds us that “almost every major supranational economic organisation, including the OECD, IMF and BIS, has warned that the huge build-up of US corporate debt is the Achilles Heel of the US economy – the new credit bubble to replace the mortgage-backed securities bubble of the 2000s. This Zero Hedge article for example, highlights a recent IMF report that some 20% of US companies are vulnerable to default or bankruptcy in the next recession – link. The surprise to many, such as myself, has been the complacency of the corporate bond market in the face of the sky high corporate debt ratios (see chart below).”

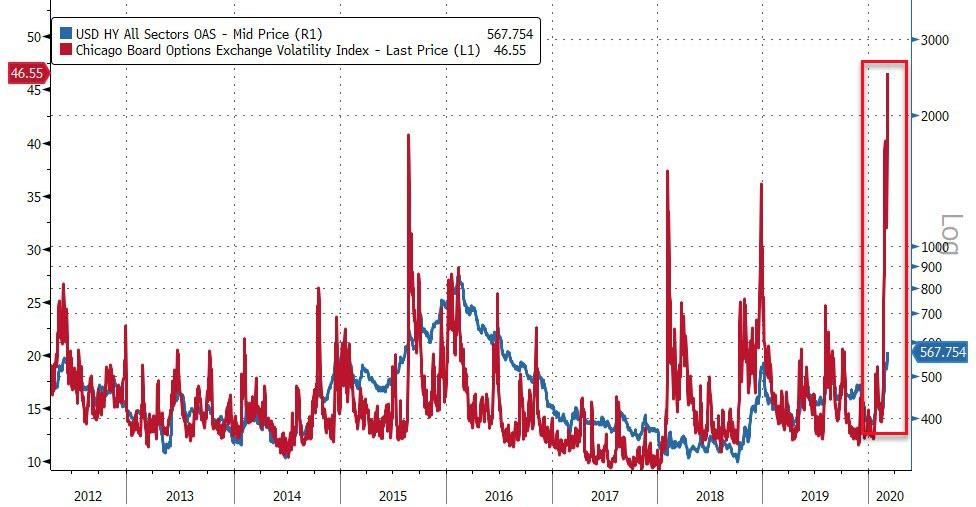

Edwards then highlights a theory proposed by his SocGen colleague, Andrew Lapthorne, explaining the complacency in the corporate bond market despite companies loading their balance sheets up to the eyeballs with debt, one which brings us to the punchline of why the surge in VIX may soon result in a shockwave that topples the record US credit bubble. “He notes the equivalence of corporate bond spreads and measures of equity volatility (see chart below). This is not just a spurious correlation in the sense that recessions could cause both series to surge independently. Andrew believes there is a direct causal relationship from low levels of equity vol directly to tight corporate bond spreads.“

In other words, SocGen’s theory is that the ultra low VIX of the past few years was the necessary and sufficient condition permitting record low yields:

Andrew says that credit models such as Merton’s ‘distance to default’ and Moody’s KMV models suck in equity volatility and spit out the appropriate credit spreads (see this BoE analysis – link). It is low equity vol encouraged by continual Fed interventions and the market’s belief in the continued Fed Put that has sustained low corporate bond spreads, depressed defaults and allowed companies to borrow excessively.

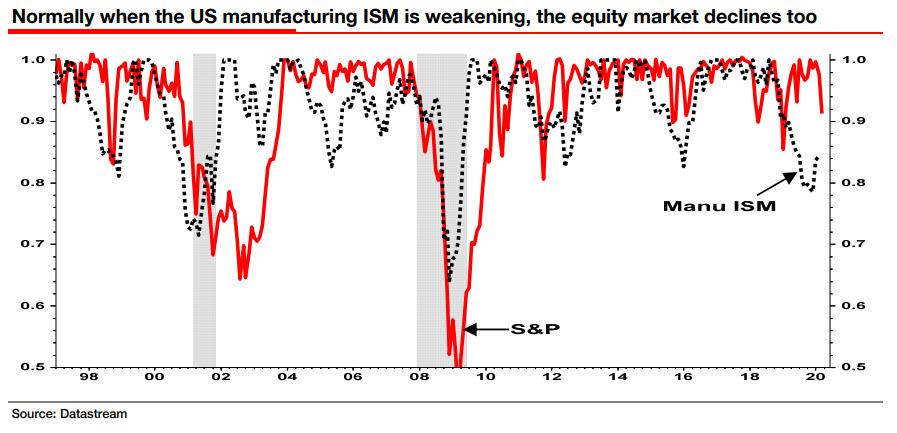

Of course, until just two weeks ago, the equity market had remained at or close to all-time highs despite accelerating weakness in the economy, as Edwards shows in the chart below.

And echoing an argument we have made repeatedly in the past, to the extent that the Fed’s recent monetary largesse (or “Not-QE” as most people know it) has kept an over-valued equity market at or close to record highs, Edwards claims that it is the Fed that directly and explicitly suppressed equity market volatility.

To the uninitiated, measures of equity market volatility tend to be low while a market is rising, but spike up sharply when the market declines. As the saying goes “the market rises on foot, but descends in the elevator”.

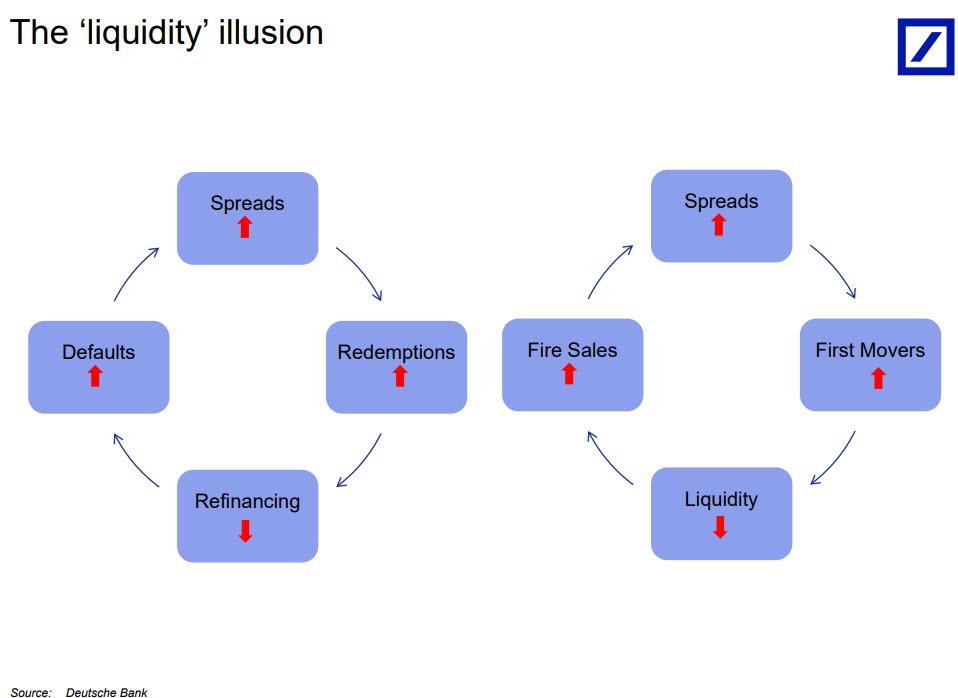

The relationship between high stock prices and low yields (for whatever reason) has been a reflexive one adding further complexity to the causal link: in any case, to the extent that a buoyant equity market has suppressed corporate bond spreads, despite balance sheets groaning with debt, companies have been able to access funds they would never have been allowed to do in more normal times, the SocGen strategist points out, or as he puts it “Low vol and low interest rates misallocate resources.” That is why, as the next chart shows, there is a direct causal relationship between rising equity vol and defaults. The markets can break a company even if it is in a position to maintain its coupon payments.

The chart above is among the reasons why we, along with many commentators, highlight that the investment grade universe of corporate bonds is now majority populated by the lowest BBB grade bonds. It is also why Edwards shows in his work that the Russell 2000 group of smaller companies has the highest levels of leverage of all the US quoted sectors: “that is why we highlight the huge retail flows of funds into corporate bond vehicles. That is why we highlight the imbalance between the tradability of corporate bond investment vehicles and their underlying assets.”

In short: by suppressing VIX, the Fed’s visible hand has created a credit bubble. And now the VIX has exploded to levels seen just once in the past decade.

What happens next? Here, Edwards’ imagination about the coming devstation is – as usual – without parallel:

Just wait until the first corporate bond fund is forced to “gate” their fund as redemptions soar. You will then hear a loud sucking sound coming out of the whole corporate bond mutual fund and ETF complex. This is a surely a flow of funds disaster waiting to happen.

He is right: the growing liquidity mismatch among investment funds, and the creeping “gates” among funds holding on to illiquid paper, is precisely the reason why last July we wrote that there is a “New, Ticking Time Bomb In The Market.“

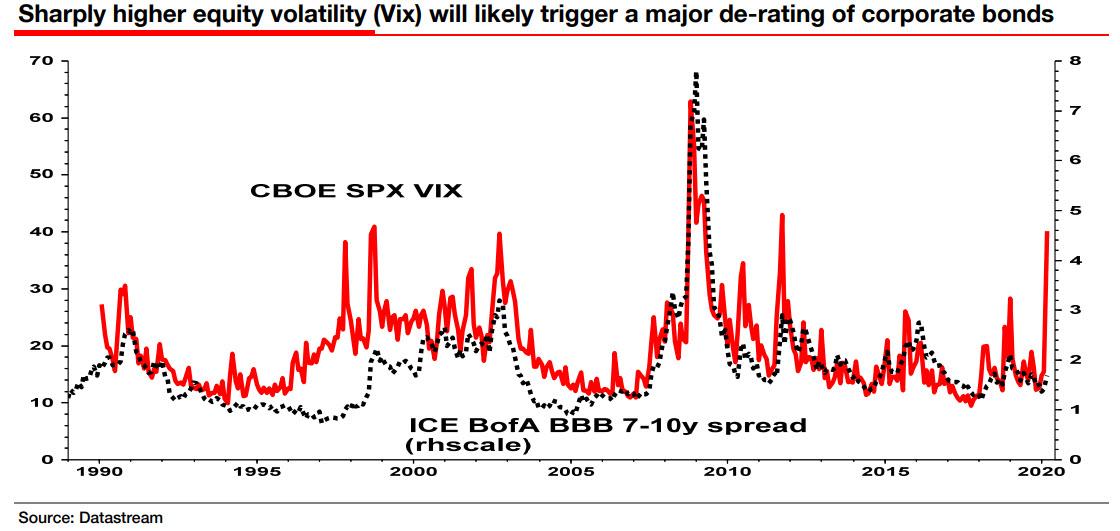

Back to Edwards who continues his apocalyptic tour de force, warning that “this time around things are much, much worse than 2008, particularly as the whole economy effectively cantilevers off multiple financial market bubbles. For when the equity market begins its long descent in the elevator and Vix begins to spike upwards, as it has begun to do in recent days (see chart below), we would expect corporate bond spreads to eventually explode higher.”

Said otherwise, “companies that are already likely struggling with the profit-crushing effects of the coronavirus will see a cascade of defaults and bankruptcies and the economy will be plunged into deep deflationary recession. The coronavirus will be blamed, but it is the tottering pyramid of financial cards built on sand, constructed by the Fed, that is to blame. It’s the Fed’s fault.“

We couldn’t agree more.

* * *

And just in case anyone skipped right to the conclusion, here it is in one sentence and one chart: unless the Fed manages to hammer the VIX as it always has in the past decade, and puts the “coronapanic” genie back in its bottle, the credit bubble – the biggest ever – is about to burst and wipe out the US – and global – economy in the process.

Tyler Durden

Fri, 03/06/2020 – 15:02

via ZeroHedge News https://ift.tt/2wwV6oj Tyler Durden