The Fraud That Is ESG Strikes Again: Six Of Top 10 ESG Funds Underperform The S&P500

While the global coronavirus pandemic has had its share of tragic consequences, including tens of thousands dead, a near halt in the global economy, millions of businesses on the verge of collapse, and the biggest intervention of central banks in capital markets in history, there have been two distinctly positive consequences: the collapse in oil prices and the decimation across the buyside has meant that Greta Thunberg and her carefully scripted climate cult have been all but forgotten, and that the ESG insanity shoved down everyone’s throat by virtue signaling banks desperate to find a new revenue source is about to go extinct.

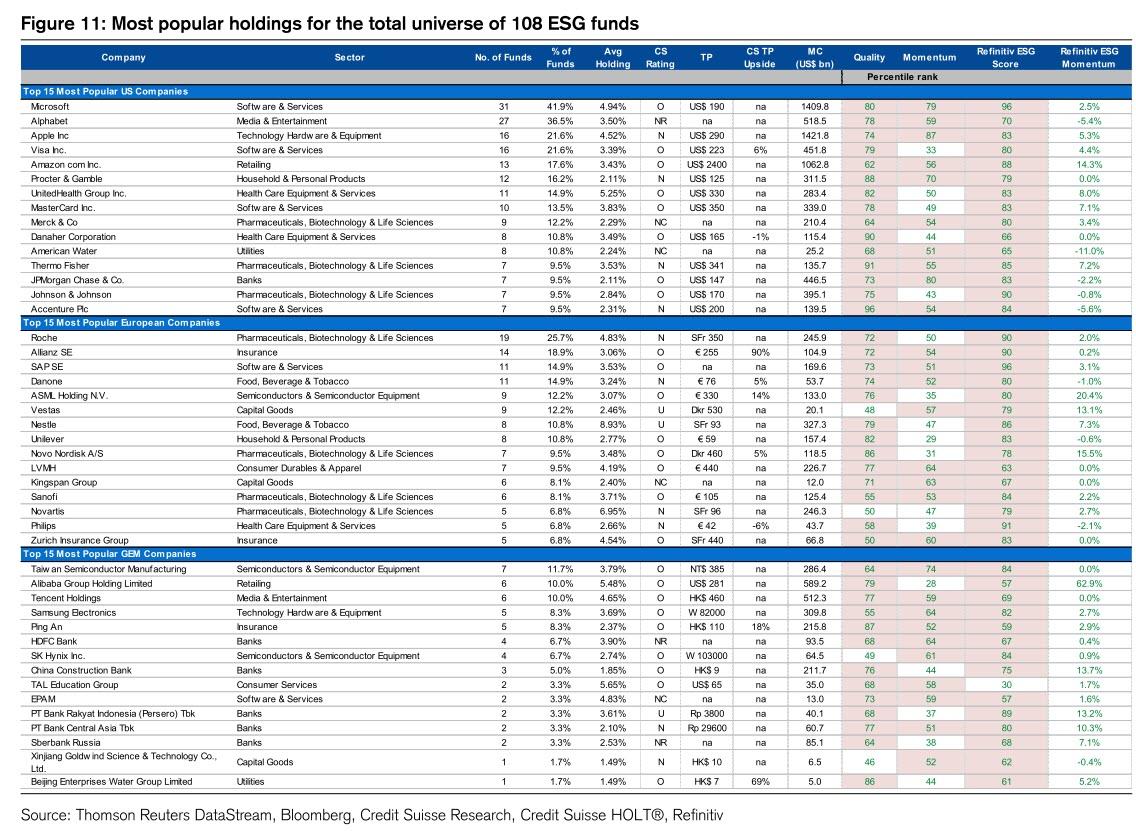

As a reminder, two months ago we reported that when virtue-signaling tour de force that is ESG, or Environmental, Social, and Governance, is anything but, as a quick look at the most popular holdings across the various ESG funds revealed.

This is what we said in February:

Instead of finding companies that, well, care for the environment, for society or are for a progressive governance movement, it turns out that the most popular holdings of all those virtue signaling ESG funds are companies such as…. Microsoft, Alphabet, Apple and Amazon, which one would be hard pressed to explain how their actions do anything that is of benefit for the environment, or whatever the S and G stand for. It gets better: among the other most popular ESG companies are consulting company Accenture (?), Procter & Gamble (??), and… drumroll, JPMorgan (!!?!!!?!).

In short: even as everyone was rushing to jump on the ESG bandwagon in hopes of boosting “virtuous” investing money, virtually none of the so-called ESG funds were actually investing in.. drumroll… ESG. In fact, it turns out that most ESG funds were in fact nothing more than a portfolio of some of the highest momentum and biggest buyback names, and since the wave of passive investing was being allocated disproportionately to ESG, it helped boost those stocks even if they had nothing to do with ESG at all!

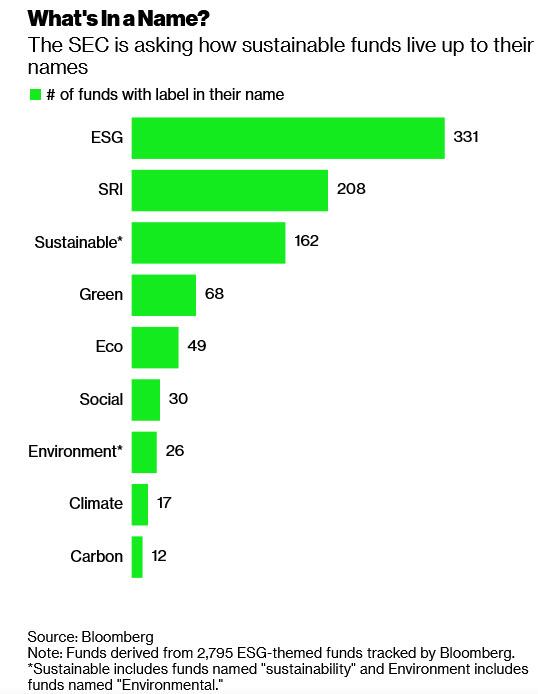

Just a few days later, in the first sign that Wall Street’s latest bout of epic hypocrisy was about to be exposed, Bloomberg reported that “the Securities and Exchange Commission wanted to know whether money managers are engaging in false advertising by saying funds are devoted to doing good when the reality is much murkier.”

… the SEC asked whether ESG products should have to follow existing rules that require a fund’s name to broadly match what it invests in. For instance, a fund that includes “stocks” in its name generally has to have at least 80% of its portfolio in equities.

Additionally, on ESG, the SEC asked for comment on issues including whether:

- The rule for naming funds should apply to ESG or sustainable products?

- Investors are relying on these terms to understand funds’ strategies?

- There should be specific requirements that funds must adhere to in order to call their investments ESG or sustainable?

Fast forward to today when the SEC may also want to look into performance criteria as well.

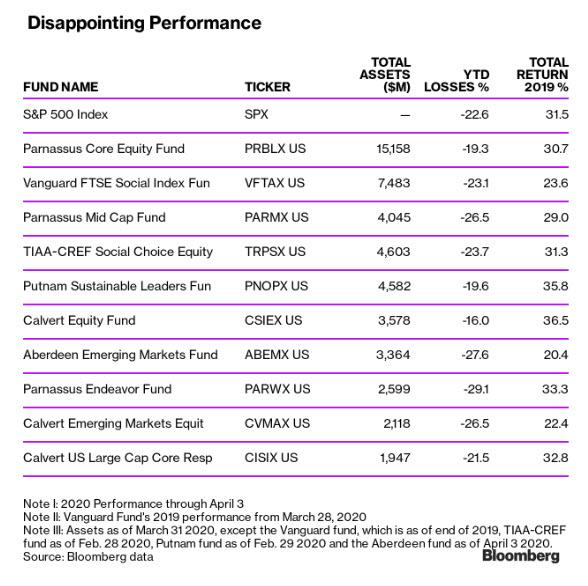

The reason: Six of the 10 biggest “ESG-focused” U.S. mutual funds – with such “ESG” holdings as Microsoft, Alphabet, Apple, Accenture, Procter & Gamble, and – of course – JPMorgan, posted bigger losses than the Standard & Poor’s 500 Index this year as the Covid-19 outbreak roiled global markets.

The worst performer was the $2.6 billion Parnassus Endeavor Fund, which has lost 29.1% through Friday, compared with the S&P 500’s 22.6% decline. The fund with the least losses was the $3.6 billion Calvert Equity Fund, which was down 16% .

As Bloomberg notes, that ESG stalwart Macroclimate pardon Microsoft were among the top picks for the Calvert Equity in the past year, according to fund manager Joe Hudepohl.

“Their movement toward the cloud, which is a good growth area, helped as well as being a leader in privacy issues, and they are strong on diversity at the top level too,” he said, adding the usual disclaimer for any investor that has suffered a huge loss, namely that “the fund is a long-term investor and doesn’t focus too much on short-term market gyrations.“

And when the fund does start to focus on short-term market gyrations, which usually takes place just as the margin calls start coming in, the fund also tends to demand a bailout. Because, clearly, its Millennial managers were so “good” in investing and collecting their management fee, that their only recourse when their precious “ESG” stocks plunge, is to see a bailout from the Fed.

In short, one can only hope that if nothing else, the coronavirus crisis at least wipes out the virtue signaling quasi-fraud that is ESG, even if it means that sellside desks will be forced to write about fundamental analysis instead of spinning long presentations full of nothing more than poignant bullshit.

Tyler Durden

Mon, 04/06/2020 – 15:45

via ZeroHedge News https://ift.tt/2RgUZ7T Tyler Durden