“World’s Most Bearish Hedge Fund” Makes Revolutionary Transformation To His Investing Approach

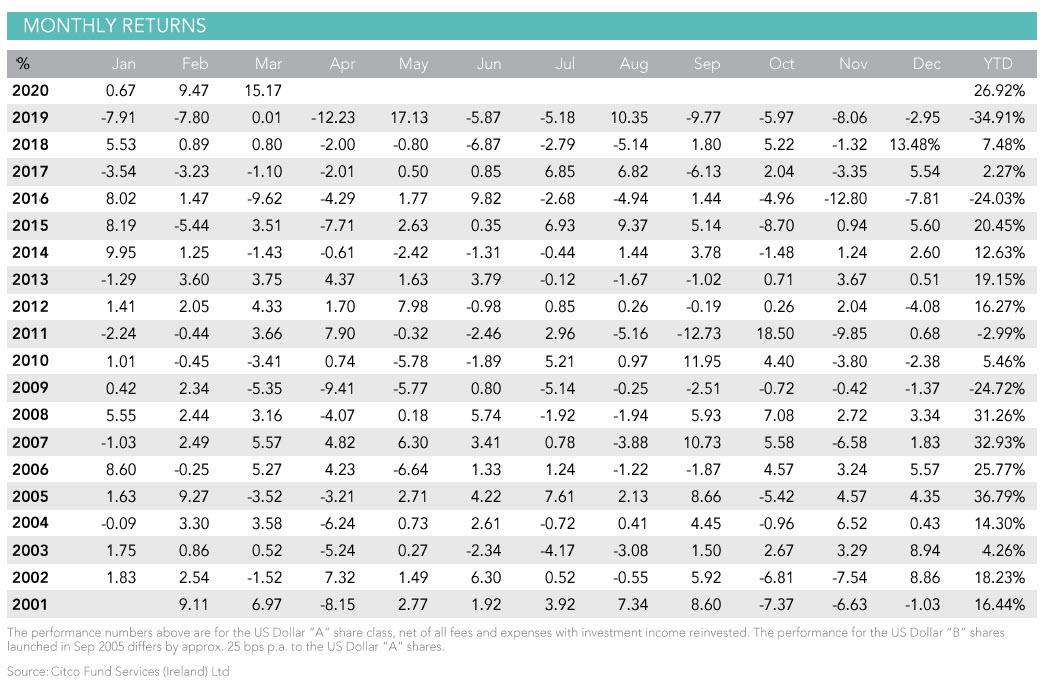

Every trader has heard the age-old saying “don’t fight the Fed”. Everyone, perhaps with one exception: Horseman Global’s CIO, and recently owner, Russell Clark, who has been upping his bearish bets in the face of a relentless liquidity onslaught by the Fed, ECB and PBOC. And in 2019, in his ambition to take on the central banks, Clark overdid it, because not only did the fund end 2019 down 34.91%, its worst annual performance in history, but the fund lost 75% of its assets under management which shrank from $581MM at the start of the year to just $150MM.

Things however turned around in 2020, and especially in March, when the fund generated an impressive 15.2% return, following a just as solid 9.5%, resulting in a remarkable 26.9% which makes Horseman one of the best performing “non fat tail” funds; and if the fund can sustain its performance until the end of the year, it would make 2020 its best year since the 31.3% return in 2008.

The question, however, remains is it too little, too late? After all, despite the impressive start to the year, Horseman’s AUM is now just $145MM, an all time low, with $327MM in assets for the entire firm. And while we commend CIO Russell Clark’s persistence, there comes a time when the management fee no longer covers even basic infrastructure.

And yet, it seems that the last thing on Clark’s mind is throwing in the towel, perhaps because the veteran hedge fund manager knows that all it takes to stage a miraculous recovery is just a few months of solid double digit returns, and the money will come flooding back (institutional memory is very short).

Not surprisingly, Clark thinks he may have just found the recipe to achieve that and much more, because as he writes in his latest letter, “after 20 years working in the markets, I finally feel like I have seen one full investment cycle. Back in 2000, it was all healthcare and tech stocks, and the US was the lead market. Then ten years later it was all China and commodities, and gold and other commodities was the lead market. And now another 10 years later, it’s all healthcare and tech stocks, and once again the US is the lead market.”

What is the simple observation to be made here?

The same one that Michael Wilson did two weeks ago when the Morgan Stanley strategist turned bullish: runaway inflation is coming as a result of the helicopter money that has arrived everywhere, not just in banana republics. As Wilson said at the start of the month, “this time, we have a potentially much more inflationary combination of an unprecedented targeted fiscal stimulus and possible deregulation of the banks to get the cash into the hands of lower income individuals and small businesses that are inclined to spend it. Such a dramatic shift in US fiscal and monetary policy relative to other regions should lead to a materially weaker dollar, which is ultimately the easiest path to reflation not only for the US, but also the world.”

Picking up on this, Clark writes that if using the pattern of the past, now is the time to “go long emerging markets and commodities again.” But as Wilson notes, “it is hard for me to shake the feeling that we are coming to an end of a much bigger deflationary trend, that started in the early 1980s.“

But has central bank helicopter money really doomed the era of falling prices to death? Here is what the Horseman CIO writes in his later letter to clients:

Paul Volcker is often credited with ending inflation. And in some ways he did. But central bank independence was one of several institutional changes made in the 1980s to keep inflation under control. These changes included weakening union power, cutting tariffs, liberalizing huge swathes of the economy, and wherever possible allowing the market to determine winners and losers. These institutional changes have largely remained in place, both in the West and Japan, and despite the best efforts of the worst central bankers seen in generations, we have continued to have deflation. And when we look at the bond markets, yields are on the floor and investors have adopted long bond strategies like risk parity, balanced portfolio strategies and private equity. Deflation is priced into markets and is expected to continue.

Clark’s argument is, to paraphrase Milton Friedman, “inflation is always and everywhere a political phenomenon”. It’s also the thesis we have held ever since 2009: “The world has too much debt, but there is no political appetite for the bankruptcies that could rid us of this debt, and there is also no political appetite for the inflationary policies to inflate the debt away.” But in a radical departure from the past decade, Clark claims that Covid-19 has changed that political calculation.

After all, “no sane politician would stand in the way of raising the salaries of essential workers, and the unions know this. The central banks, happily financing 15% of GDP fiscal deficits, have proved that they are willing to finance anything the government wants. The institutional defences put in place to combat inflation have been fully dismantled.”

He then adds that the big, recurring argument made against inflation is that Covid-19 has destroyed demand. But as he notes, “what drives inflation is lack of supply. And I see supply chain disruption everywhere. I also see falling investment in the supply chain everywhere.”

Which brings us to the punchline: having seen the (inflationary) light, Clarke has made a revolutionary transformation to his portfolio, using the opportunity offered by the Covid-19 crisis “to exit deflationary positions. We have sold all our government bonds, and I am now trying to short assets that have benefited from very low interest rates, wages and commodity prices, namely commercial property, restaurants and utilities (and potentially private equity).”

There is another key tangent to expecting reflation, or rather stagflation, instead of deflation in the future:

The weird thing about inflation, is that it is very bearish for US assets. As soon as inflation begins to appear, markets begin to worry about the Federal Reserve “taking away the punchbowl”.

That was lesson #1 of 2018; the second, and even bigger, lesson of 2018, which reappeared in 2020, is that the US equity and bond market is now totally reliant on the Federal Reserve.

And, as he summarizes, “if inflation appears, then US markets are in big trouble. For me, the 1970s and stagflation beckons. Short bonds and long commodities look right, with a bias to shorting US equities. I see inflationary assets outperforming deflationary assets.“

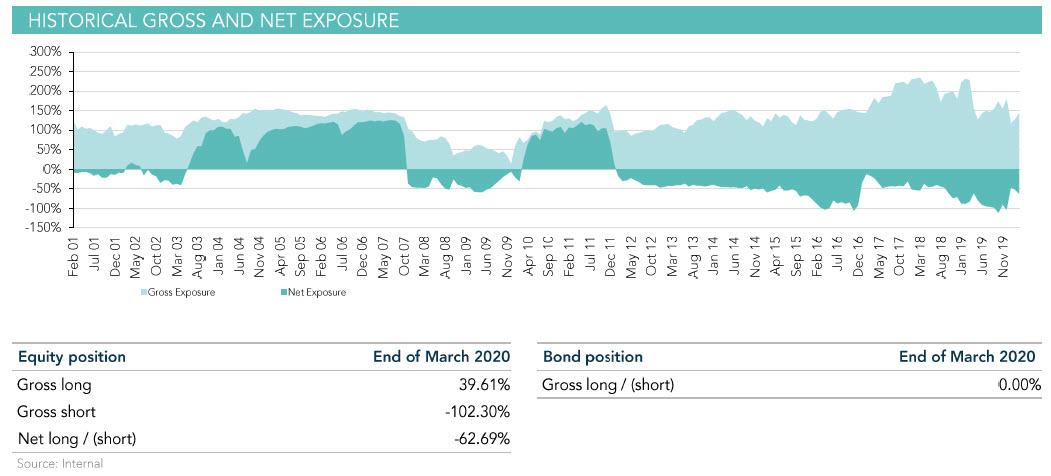

Finally, before we present Clark’s conclusion, we will remind readers why more than 5 years we first dubbed his Horseman Global as the world’s most bearish hedge fund: simply because that’s what he was, if only one looks at his net exposure which for much of the past five years was between -50 and -100%.

In retrospect, it appears Clark did not particularly enjoy that moniker, as his conclusion makes clear:

Intellectually we have been in the deflation camp for 10 years. We are now much more in the inflation camp. I will let others decide if that still qualifies me for “most bearish fund manager”. Personally, I prefer to be known as someone who is “the most logical and rational fund manager” – but that does not make a good headline!

Russell, if you are right, and if stagflation/hyperinflation is indeed coming, and gold heads to $2,000, $5,000, $10,000 or more, we will call you anything you want.

Tyler Durden

Thu, 04/16/2020 – 19:45

via ZeroHedge News https://ift.tt/2VgzpCw Tyler Durden