Everyone On Wall Street Is Bearish, And This Is What Keeps Them Up At Night

Tyler Durden

Tue, 05/19/2020 – 11:45

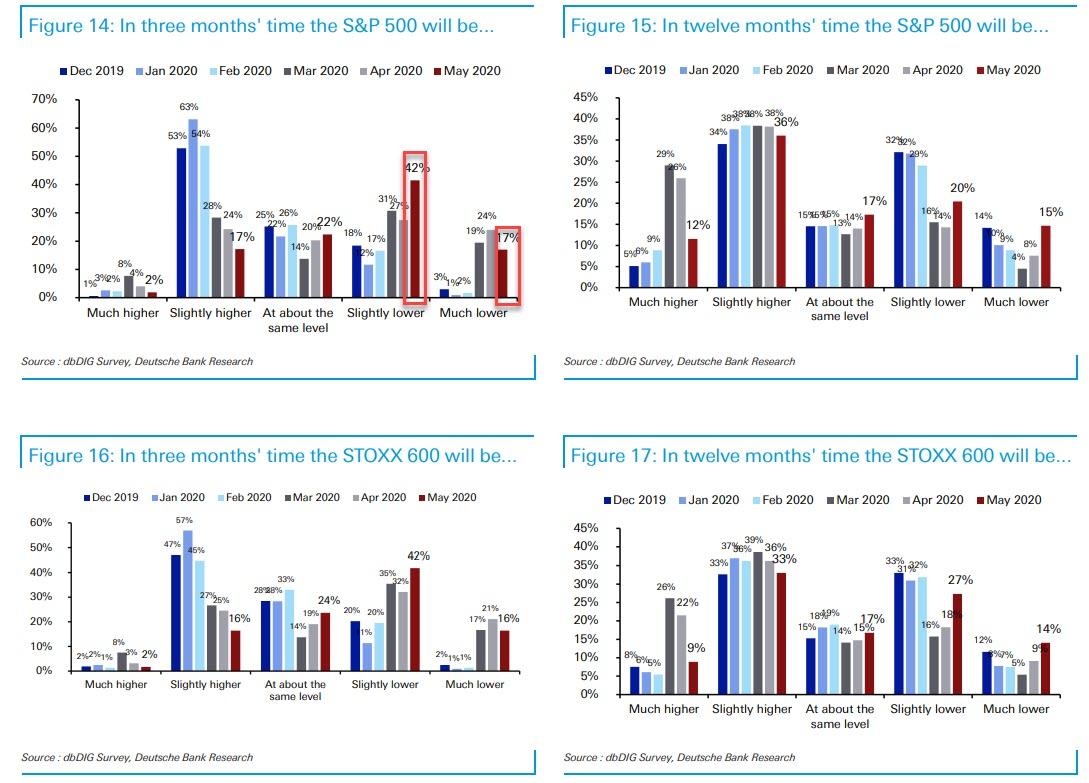

One day after we showed that according to the latest Deutsche Bank monthly survey of Wall Street professionals the majority, or 59% of respondents, see the S&P either “lower” or “much lower” in three months than where it is now…

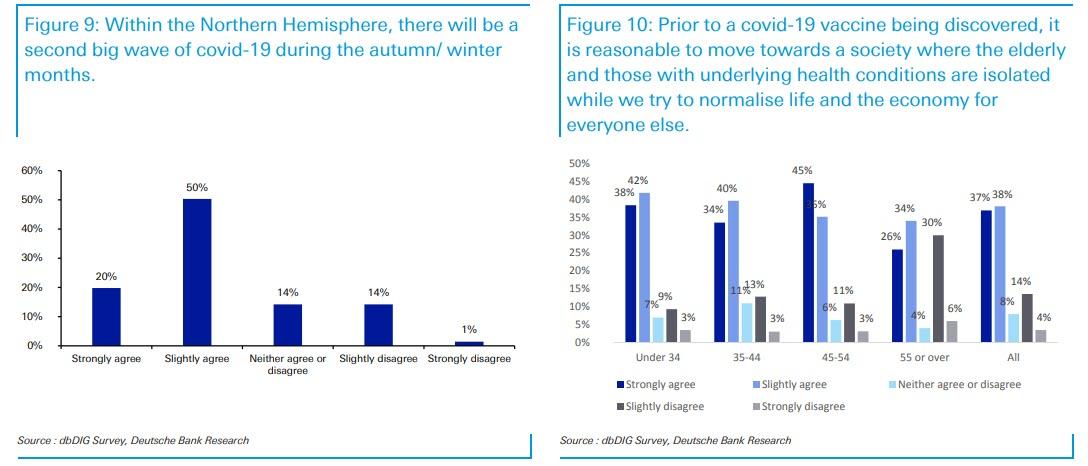

… with 53% confident that there will be a second wave of the virus in the fall/winter…

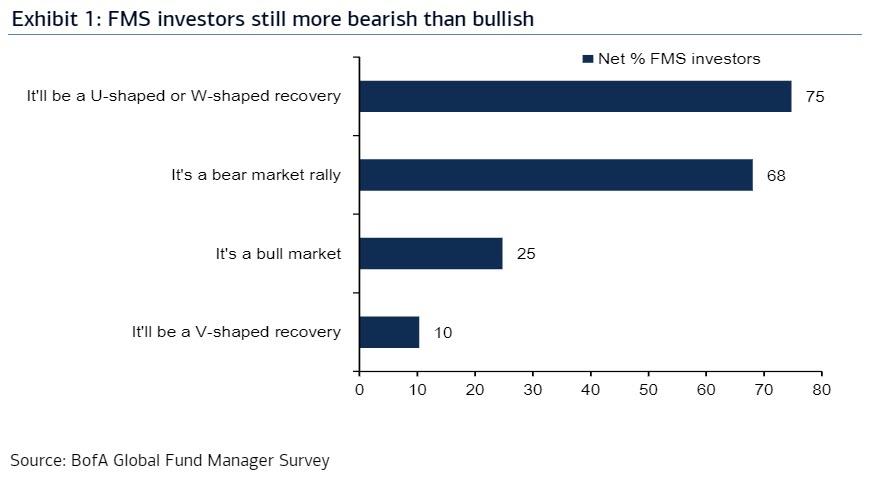

… this morning BofA also published its latest Fund Manager Survey, which polled 223 participants with $651BN in AUM, and which confirmed the conclusions from the DB poll, namely that the vast majority of financial professionals remain extremely bearish – and which likely means that stocks will keep rising as Powell will do everything in the Fed’s power to avoid another crash.

Indeed, as BofA’s Michael Hartnett summarizes the zeitgeist, just 10% expect a V-shaped recovery, 25% a new bull market; in contrast 75% expect a U or W-shaped recovery, 68% a bear market rally.

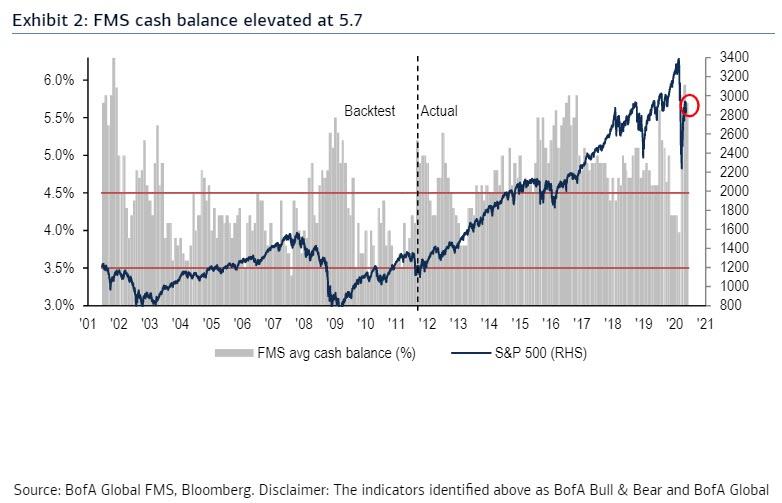

Yet despite the seeping pessimism, investors invested in risk assets, with cash levels dropping to 5.7%, down from 5.9%, though well above 10-year average of 4.7% (as a reminder, the BofA Bull & Bear Indictor remains pinned at 0, i.e. investors still extreme bearish, although with the S&P at 3,000 it appears that survey respondents have a habit of openly making up stuff in their responses, a lament we have had about the BofA FMS for years).

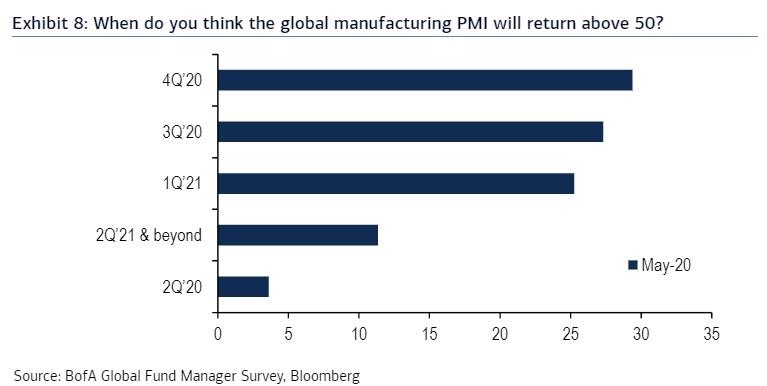

Looking at the global economy, poll respondents’ global growth expectations jumped by 40ppt to net 38% (65% stronger, 28% weaker) of FMS investors expecting global growth to strengthen over the next 12 months, but investors do not expect global manufacturing PMI to rise back above 50 before November (latest = 40).

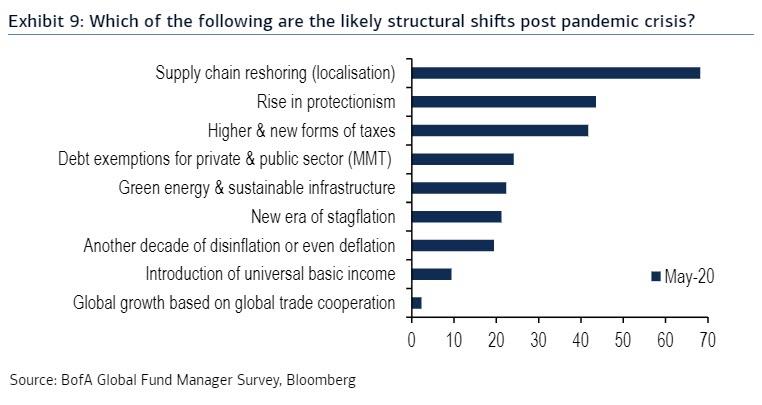

Precipitating the very slow, U-shaped recovery, two-thirds of the survey respondents said that the biggest structural shift will be supply-chain reshoring, followed by protectionism at 44%, and higher taxation at 42%.

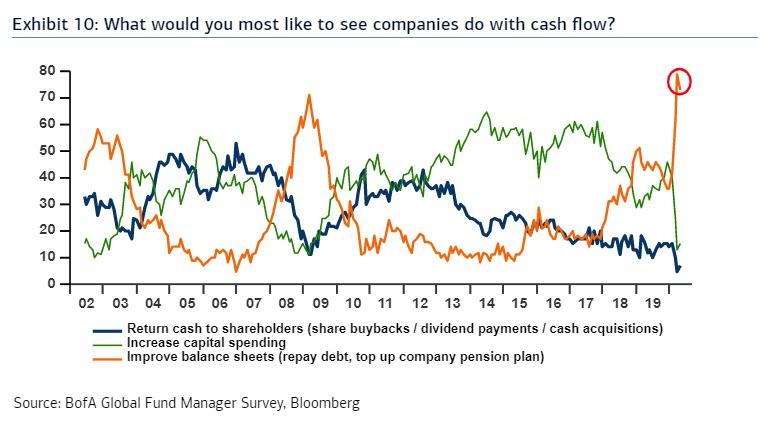

As usual, most respondents found that most companies are obese debt monsters, with 73% saying that companies should use cash flow to reduce debt, 15% said increase capex, only 7% said buyback stocks, increase dividends. None of this will ever happen, and instead companies will lever up even more as a result of the Fed’s actions promoting an even greater debt bubble.

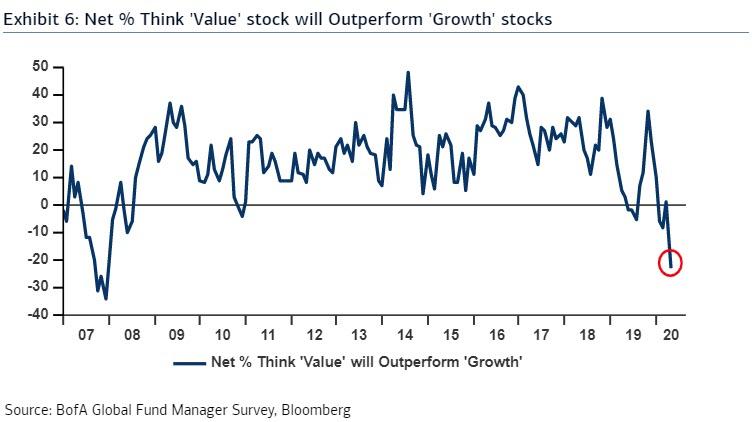

Looking at markets, the vast majority of respondents, believe value will underperform growth, with Hartnett noting that last time this many FMS investors, a net 23% of FMS investors, expected value to underperform growth was Dec’07. Which means that value will almost certainly outperform growth, which however would mean a tech/FAAMG crash is imminent.

While most respondents are bearish, they are far more bearish on Europe, and as a result the spread between those long the US (24% overweight) vs short Europe (17% underweight) is now the highest since 2012.

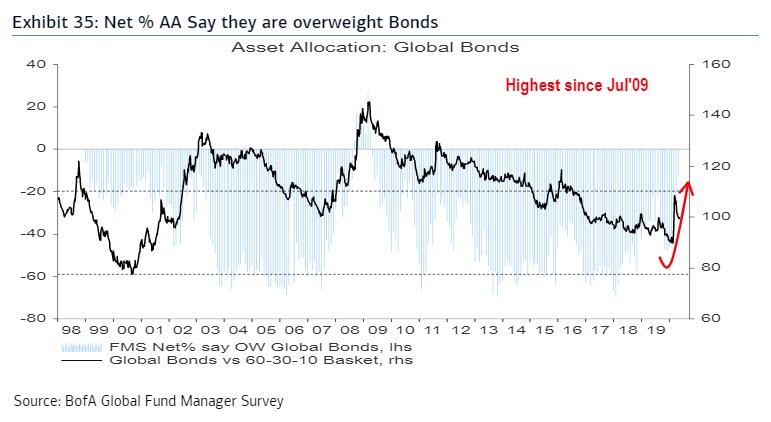

That said, as noted above the vast majority is tactically bearish, with bond allocations rising to the highest since Jul’09, jumping 15% MoM to net 13% underweight (which would mean that survey respondents have either been losing money for the past decade as bond yields plunged, or they are simply so dumb they have no idea what is going on in the bond market)…

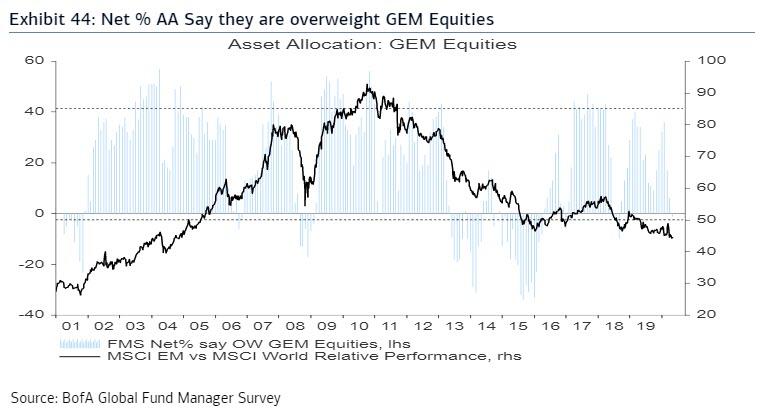

…. investors short EM for 1st time since Sept’18…

… along with a record long in healthcare.

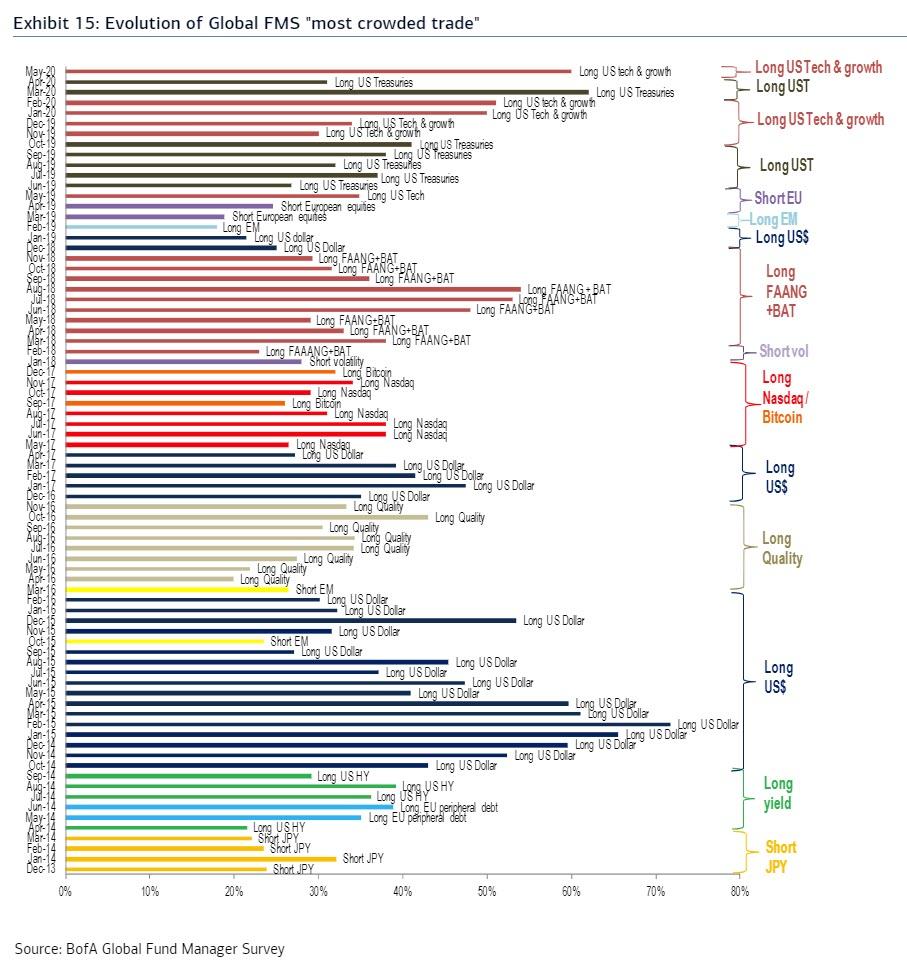

Yet despite this self-reported bearishness, when asked what Wall Street views is that most crowded trade, their answer – long US tech & growth stocks (60%). In other words, everyone is confident that everyone else is long the most overvalued sector in asset bubble history, even as most investors expects stocks to slide. That’s one paradox; an even bigger one is that during the biggest health crisis in modern history and the biggest economic depression in decades, everyone is rushing into tech stocks.

As a result of this widespread pessimism, the biggest pain trade for Wall Street in for both stocks and credit remains up, consistent Hartnett’s near-term reco of SPX>3020, RTY>1500, HY spreads<650bps.

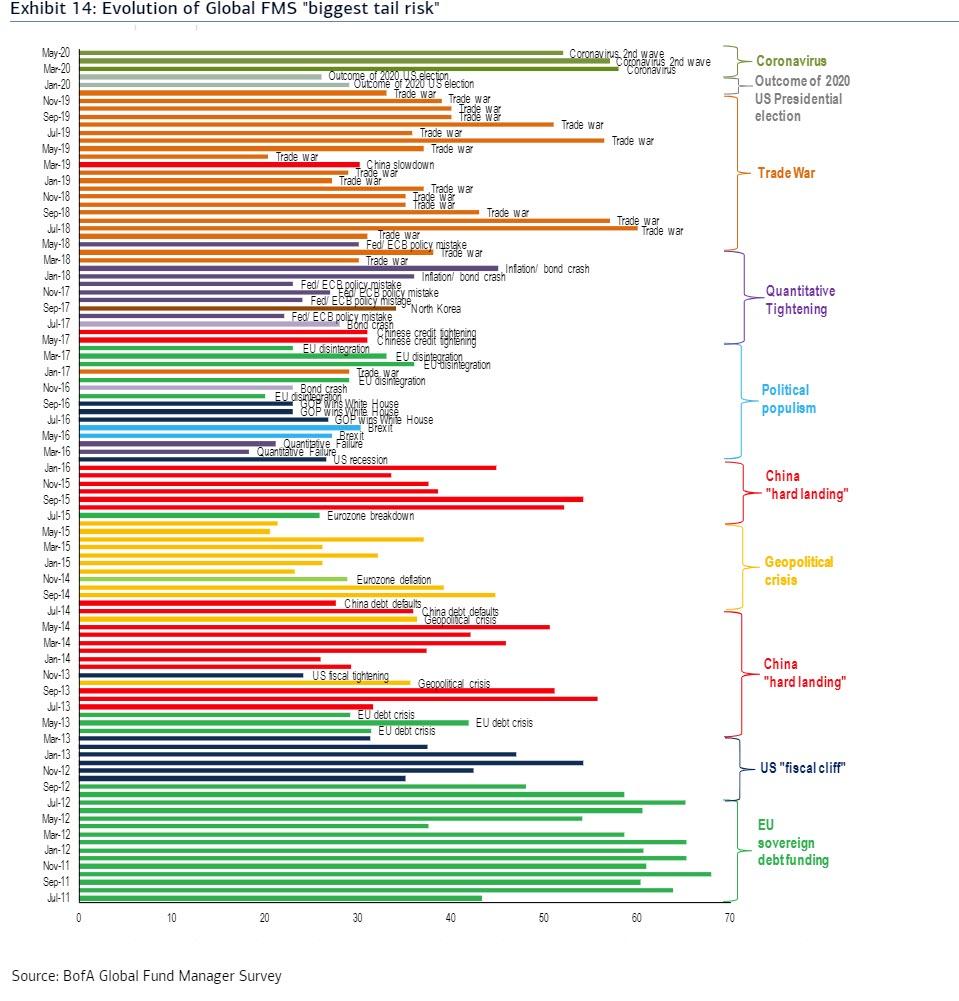

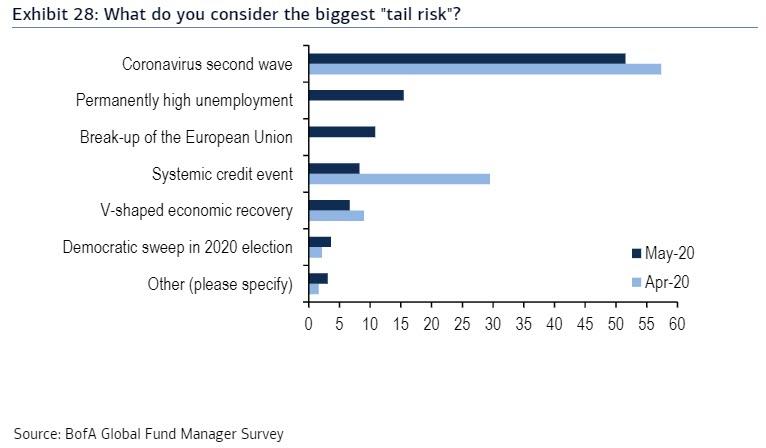

Finally, looking at what keeps Wall Street up at night, there were no surprise here as the biggest risk from April carried over, and 52% of respondents see a “second wave” as the biggest risk…

… followed by permanently high unemployment, and a systemic credit event storming in the biggest fears.

via ZeroHedge News https://ift.tt/2X8QzSs Tyler Durden