S&P Set To Open At New Record High; Tesla, Apple Trade Post-Split

Tyler Durden

Mon, 08/31/2020 – 08:13

The melt-up continues: S&P futures rose on Monday for the eighth session in a row alongside European markets, despite fading some of their earlier gains after setting fresh all time highs on Friday amid investor confidence that central bank support will prop up risk for years, setting up the S&P 500 for its best August in over three decades.

The three main US indexes are set for their fifth straight monthly rise following this year’s March lows, with the S&P 500 looking at its biggest percentage rise in August since 1984, even as economic data pointed to an uneven recovery from the steep downturn. Among early movers, Aimmune Therapeutics more than doubled premarket after Swiss food group Nestle offered to pay $2 billion for full ownership of the peanut allergy treatment maker to expand its fast-growing health science business.

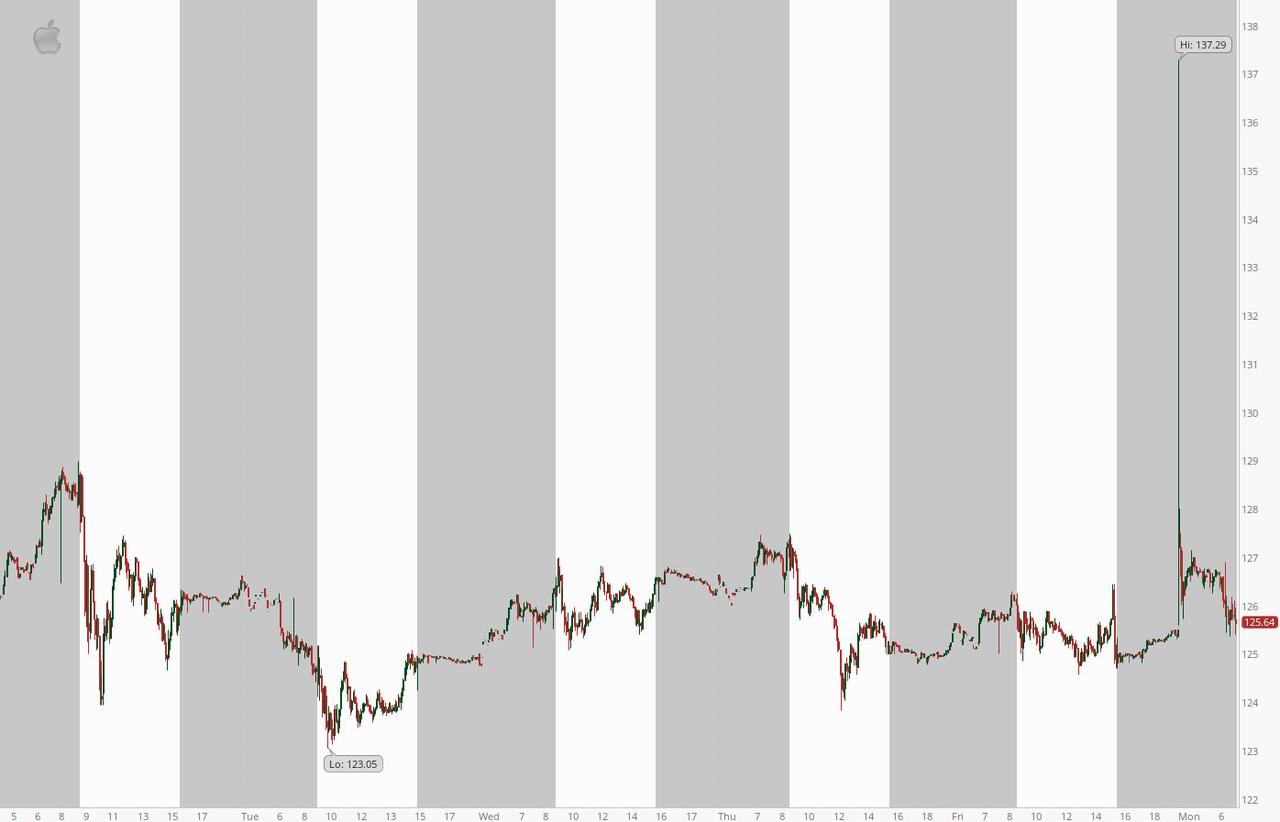

Apple gained 1.5% to $126.64…

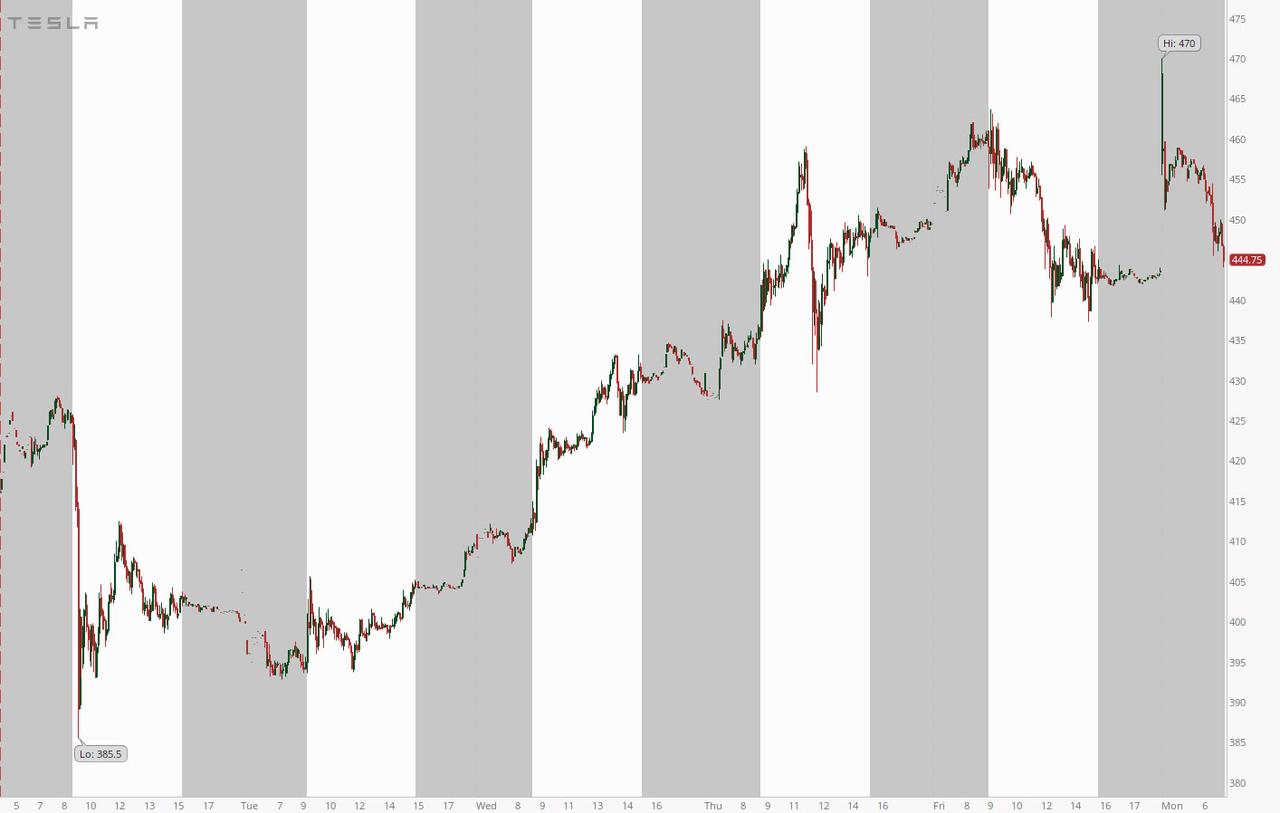

while Tesla initially spiked to a new all time high, rising to $470 before reversing in a $22 billion swing, as both stocks became “less costly” after their pre-announced stock splits took effect.

Shares of the Cupertino company, which have rallied nearly 30% since it announced its surprise 4-for-1 stock split and blockbuster quarterly results on July 30, were priced at $126.56, up 1.4% when compared to Friday’s split-adjusted close, in pre-market trade. It will be Apple’s latest stock split since a 7-for-1 move in 2014 and its fifth since going public in 1980. Apple shares closed at $499.23 before the split on Friday, up 70% this year, a rally which helped the iPhone maker overtake Saudi Aramco as the world’s most valuable publicly listed company and become the first publicly listed U.S. company to breach $2 trillion in market capitalization.

Tesla followed suit earlier this month by announcing a 5-for-1 split to portion its richly valued stock into smaller chunks, which also takes effect on Monday. Tesla’s stock has surged more than five-fold this year, while shares of General Motors and Ford Motor declined on fallout from the COVID-19 pandemic. Shares of Tesla, up 61% since it announced what is its first stock split in mid-August, closed at $2,213.4 on Friday. They were priced up 2.33% at $453 when counted at their post-split value in pre-market on Monday.

The unprecedented surges driven entirely by stock split news have stunned market watchers because while in theory no new value was created, the fact that “more” retail daytraders can now purchase the stocks was seen as a catalyst to push them higher, even though online brokerages Robinhood, Charles Schwab Corp and Fidelity, along with several smaller shops, have begun offering slices of individual shares.

In Europe, the Stoxx Europe 600 Index rose 0.5% as of 10:30 a.m. in London, with automakers and energy shares advancing the most among sectors. Mining shares also outperformed along with utilities including Suez SA, which jumped after an approach by rival Veolia Environnement SA. The Stoxx Europe 600 Oil & Gas Index gained as much as 1.5% to lead gains among sectors as the price of Brent crude price climbed to the highest since early March with traders focusing on demand recovery. European energy gauge extends gain in Aug. to 5.7%, after retreating 5.4% in July. London markets are closed for a public holiday

Earlier in the session, Asian stocks fell, led by communications and IT, after rising in the last session. Japanese stocks outperformed peers in Asia, the Topix Index gaining 0.8%, bolstered by Berkshire Hathaway’s purchase of stakes in five major trading companies in one of billionaire Warren Buffett’s biggest investments in the nation. Aside for Japan, most markets in the region were down, with Jakarta Composite dropping 2% and India’s S&P BSE Sensex Index falling 1.6%. Trading volume for MSCI Asia Pacific Index members was 22% above the monthly average for this time of the day. The Topix gained 0.8%, with Artra and Segue rising the most. The Shanghai Composite Index retreated 0.2%, with Zoy Home Furnishing and Tibet Tourism posting the biggest slides.

Chinese economic activity continued to rebound in August as the world’s second- largest economy emerges from the virus slump. The August Manufacturing PMI from the National Bureau of Statistics (NBS) signaled a continued recovery in overall activity. The NBS manufacturing PMI stayed solid at 51.0 in August (despite being 0.1pp lower than July). The NBS non-manufacturing PMI rose in August as the services PMI climbed to the highest level since early 2018. The construction PMI was modestly lower but remained strong in absolute terms.

- China official NBS manufacturing PMI: 51.0 in August (GS forecast: 51.1, Bloomberg consensus: 51.2), vs. 51.1 in July.

- Official non-manufacturing PMI: 55.2 in August, vs. 54.2 in July.

The Chinese PMI data gave investors some renewed comfort in the global economy’s reemergence from virus shutdowns. The eurozone on Tuesday publishes manufacturing and inflation data, followed by U.S. jobs numbers on Thursday and Friday. Inflation readingsfrom Spain, Italy and several German states are well below where the region’s central bank wants them to be.Still, with coronavirus infections in the U.S. ticking up again, India becoming the world’s epicenter for new cases, and the worldwide total surpassing 25 million, the pandemic is far from beaten.

“While momentum has slowed in light of rising cases, in the U.S. in July and in Europe in August, the economic recovery continues to unfold,” Esty Dwek, head of global market strategy at Natixis Investment Managers Solutions, said in a note. “Central banks have already stated they would remain ultra-accommodative for a long time. Risk assets are likely to remain supported, even if the ride will probably be bumpy.”

In FX, the Bloomberg dollar index edged up with U.S. equity futures while Treasuries steadied amid month-end positioning. The pound weakened versus the euro after a news report said U.K. Treasury officials are pushing for significant tax increases. The country’s stock and bond markets are closed for a public holiday. The yen gave back some of Friday’s gain, the biggest in five months, as Japan searched for a new prime minister following Abe’s surprising resignation.

In rates, treasury futures were lower on anemic volume with U.K. on holiday, leaving yields cheaper by less than 2bp across the curve. Month-end flows may provide support, while no U.S. coupon auctions this week puts data in focus, especially ISM manufacturing Tuesday and August jobs report Friday. 10-year yields around 0.74%, cheaper by 1.6bp vs Friday’s close with 2s10s and 5s30s steeper by ~1bp; 5s30s at 124bp is within 5bp of its June 5 YTD high; stock futures remain higher, off best levels of the day. Long end may begin to find support from the approach of month-end index rebalancing that’s been inflated by growth in issuance, at 3pm ET.

In commodities, West Texas crude oil advanced above $43 a barrel, while Brent jumped 3% to $46.33, the highest price since the March crash. Silver rose, outperforming gold.

U.S. presidential campaigns are set to take center-stage in the coming weeks with market volatility expected to spike ahead of polling in November. At 1030am ET we get the Dallas Fed Mfg Activity (est. 0, prior -3), while Catalent and Zoom Video are reporting earnings.

Market Snapshot

- S&P 500 futures up 0.4% to 3,516.75

- MXAP down 0.7% to 172.93

- MXAPJ down 1.2% to 571.92

- Nikkei up 1.1% to 23,139.76

- Topix up 0.8% to 1,618.18

- Hang Seng Index down 1% to 25,177.05

- Shanghai Composite down 0.2% to 3,395.68

- Sensex down 1.8% to 38,757.94

- Australia S&P/ASX 200 down 0.2% to 6,060.46

- Kospi down 1.2% to 2,326.17

- STOXX Europe 600 up 0.6% to 371.09

- German 10Y yield rose 1.5 bps to -0.394%

- Euro down 0.1% to $1.1886

- Italian 10Y yield rose 2.4 bps to 0.918%

- Spanish 10Y yield rose 1.4 bps to 0.393%

- Brent futures up 1.4% to $46.44/bbl

- Gold spot down 0.3% to $1,958.42

- U.S. Dollar Index little changed at 92.37

Top Overnight News

- There isn’t any urgency for the Federal Reserve to offer more clarity on how long it will hold interest rates near zero at the moment because investors already understand the central bank won’t be tightening for a while, Minneapolis Fed President Neel Kashkari said

- Figures from Italy’s statistics office, Istat, showed that the nation’s economy shrank 12.8% in the second quarter; household spending fell 11.3% in the second quarter, and exports dropped 26.4%

- India is fast becoming the world’s new virus epicenter, setting a record for the biggest single-day rise in cases as experts predict that it’ll soon pass Brazil — and ultimately the U.S. — as the worst outbreak globally

- Chinese economic activity continued to rebound in August, with a gauge of the services industry at the strongest level since early 2018 while the expansion in manufacturing activity slowed slightly

A quick look around global markets courtesy of NewsSquawk:

Asian equity markets were mostly higher amid tailwinds from last Friday’s gains on Wall St where the S&P 500 extended on record highs and is on course for its best August performance in more than 3 decades, helped by the recent big-tech surge and dovish undertones from last week’s Jackson Hole Symposium. ASX 200 (-0.2%) and Nikkei 225 (+1.1%) were both positive but with gains in Australia’s benchmark capped by mixed fortunes among the mining names and varied data releases, while sentiment in Tokyo was buoyed after stronger than expected Industrial Production which showed the largest M/M increase on record and on hopes of political continuity after reports that staunch Abe loyalist and current Chief Cabinet Secretary Suga is to run in the LDP elections to succeed PM Abe. Furthermore, the biggest gainers in Japan have been the largest general trading companies after Berkshire Hathaway acquired at least a 5% stake in the industry leaders including Itochu Corp. (8001 JT), Marubeni Corp. (8002 JT), Mitsui & Co. (8031 JT), Mitsubishi Corp. (8058 JT) and Sumitomo Corp. (8053 JT). Hang Seng (-1.0%) and Shanghai Comp. (-0.2%) also conformed to the upbeat tone despite mixed PMI data in which headline Manufacturing PMI missed expectations although remained in expansionary territory, while Non-Manufacturing PMI was the highest since January 2018 and Composite PMI also improved. There was a slew of earnings from China including the Big 4 banks which all showed weaker profits and China’s largest oil company Sinopec posted its first loss since 2003, although the weaker results failed to dent the risk appetite with the relevant companies all sitting on respectable gains, while concerns regarding the sale of TikTok after China tightened tech export rules were also brushed aside. Finally, 10yr JGBs were initially lacklustre and briefly slipped below 151.50 with demand for bonds subdued by the heightened risk appetite in Japan, although downside was later reversed amid the BoJ presence in the market for JPY 870bln of JGBs predominantly focused on 1yr-5yr maturities.

Top Asian News

- China’s Economic Recovery Continues on Strong Services

- Reliance Buys Future Assets for $3.4 Billion; Bonds Jump

- Israel’s El Al Pilot Says UAE Flight to Pass Over Saudi Arabia

- Credit Suisse Plans to Double China Headcount in Five Years

European stocks kick the week off on a firm footing (Euro Stoxx 50 +0.3%) but have drifted off of opening highs heading into month end, as the region coattails on the lead from Wall Street on Friday; while, initially at least, brushing off the overall downbeat APAC performance. Note, UK markets remain closed on account of Summer Bank Holiday. Sectors trade modestly higher across the board with a mild cyclical/value bias; utilities are the marked outperformer on the back of Suez (+18.8%) after Veolia (+3.4%) is offering to purchase ~30% of the group from Engie (+6.3%) for EUR 15.50/shr, amid speculation, since confirmed, that such a move would be a precursor to launching a takeover bid. Other notable movers include Sanofi (+0.3%), whose CEO noted that recent data has increased confidence in the success of the group’s two COVID-19 vaccine candidates. Nestle (+0.7%) is higher after stating it is to purchase Aimmune for USD 34.50/shr totaling USD 2.6bln, with the deal expected to close in Q4. On the other end of the spectrum, Natixis (-2.0%) is pressured as its H20 asset management arm is to temporarily suspend some of its funds, albeit this is not set to have a financial impact on Natixis.

Top European News

- Wirecard Inquiry Zooms In on Why Germany Missed Fraud of Century

- Philips Cuts Outlook After U.S. Slashes Ventilator Contract

- Regulator Tells H2O to Freeze Funds on Valuation Uncertainty

- Italy Plunged Into Recession by Investment, Consumer Slump

In FX, it remains to be seen whether the Dollar succumbs to remaining month end selling and the usual 4 pm scramble to complete portfolio rebalancing requirements, but for now the Buck is clawing back lost ground and declines against the Yen in particular after Japanese PM Abe confirmed his departure last Friday. In fact, the Greenback on a firmer footing vs most G10 counterparts and the DXY has bounced from a 92.142 low to 92.480 at best awaiting comments from Fed’s Clarida and Bostic alongside the Dallas Fed manufacturing business index for any further opinion on the new flexible average inflation targeting regime.

- JPY – Not quite zero from hero, but the Yen has retreated further from post-Abe peaks amidst reports that staunch supporter and current Cabinet Secretary Suga is in the running to become new LDP leader. Usd/Jpy is now nudging through 105.90 and also taking on board remarks from another challenger to takeover as PM, as Ishiba contends that there is no need to radically change Abenomics or monetary easing, adding that a weaker Yen is not preferable in his view.

- GBP – The next weak major link, and perhaps the Pound is taking note of Brexit news and media speculation suggesting that the UK is prepared to walk away from negotiations with the EU if Brussels does not back down on its demand for alignment with state aid rules. Cable is struggling to keep hold of 1.3300, albeit with volumes lighter than normal due to the August Bank Holiday.

- AUD/NZD/EUR – Also unwinding recent gains/outperformance vs the US Dollar as the Aussie fades ahead of 0.7400 in wake of mixed data (Q2 business inventories fell 3 times more than forecast, but company profits rebounded from -7.5% to +15%) and pre-RBA, while the Kiwi has stalled around 0.6750 following deteriorations in ANZ business sentiment and the activity outlook. Elsewhere, the Euro is straddling the 1.1900 handle amidst benign German state, Spanish and Italian national CPI data, but also wary of hefty option expiry interest at the strike in 1.5 bn.

- CAD/CHF – The Loonie is bucking the broad trend and holding 1.3100+ status against the backdrop of firm crude prices and awaiting Canadian data in the form of building permits and ppi, while the Franc is meandering between 0.9050-25 after an acceleration in Swiss retail sales and not really hindered by latest increases in bank sight deposits.

- SCANDI/EM – The aforementioned buoyancy in oil and no change in daily FX purchases by the Norges Bank for September appear to be underpinning the Nok, while the Try has derived some support from Turkish GDP defying expectations for a steeper contraction and the Cnh via another firmer PBoC Cny midpoint fix rather than somewhat mixed official Chinese PMIs.

In commodities, WTI Oct and Brent Nov futures continue grinding higher in early European trade as the benchmarks remain supported by overall sentiment. An uptick in prices coincided with source reports that UAE’s ADNOC are reportedly to cut October crude oil term supplies to Asia customers by 30% across all grades. In terms of Gulf of Mexico developments, BSEE estimates of shut in for Gulf of Mexico production at 69.76% vs. Prev. 82.13% following Hurricane Laura. Meanwhile, Goldman Sachs which anticipates Brent prices to reach USD 65/bbl by Q3 next year. WTI Oct has tested USD 43.50/bbl to the upside (vs. low USD 42.90/bbl), whilst Brent Nov is yet to convincingly breach USD 46.50/bbl after printing an overnight base at USD 45.80/bbl. Elsewhere, spot gold falls victim to the firming Dollar and trickles lower from overnight highs of USD 1976/oz closer towards USD 1950/oz. Spot silver conversely remains supported around the USD 27.75/oz area. In terms of base metals, Shanghai copper posted its fifth consecutive month of gains – with robust construction and infrastructure activities keeping the red metal buoyed.

US Event Calendar

- 9am: Fed Vice Chair Clarida Speaks on Monetary Policy Framework

- 10:30am: Dallas Fed Manf. Activity, est. 0, prior -3

- 10:30am: Fed’s Bostic Gives remarks to Florida Philanthropic Network

via ZeroHedge News https://ift.tt/31GicFX Tyler Durden