“A Crypto Bank Like No Other”: Morgan Stanley Initiates Silvergate With “Overweight”, Setting Stage For Big Squeeze

It is hardly a secret that in addition to energy and uranium equities, we have been favorably predisposed toward the small crypto-linked bank, Silvergate…

Silvergate announced that Fidelity Digital Assets will serve as a custody provider for its SEN Leverage product.

— zerohedge (@zerohedge) March 29, 2021

… widely unknown until May, when the company attracted the attention of Wall Street when it announced a partnership with Facebook to roll out the social network’s stablecoin, Diem (formerly known as Libra).

The bullish thesis is simple: as we explained previously, should regulators crackdown on Tether or any of the other popular stablecoins (which judging by Gary Gensler’s latest comments is just a matter of time), the most likely winner will be an institutionalized alternative, and with Diem’s Facebook backing – which will be issued by Silvergate – it doesn’t get any more institutional…or more of a contingency plan to a tether crackdown.

But while SI stock had fluctuated in a tight range after breaking out early in the year then sliding to the ~$100 range, it had attracted little bank coverage. Until now.

This morning Morgan Stanley analyst Ken Zerbe published an initiating coverage with an overweight rating and $158 price target on Silvergate which “is one of the most distinctive banks we cover” adding that the company gives bank investors “a nearly pure-play way to participate in the rapid growth of the nascent cryptocurrency industry.”

Silvergate is one of the most distinctive banks we cover. We initiate coverage at OW with a $158 PT (52% upside). We see a 3:1 bull:bear skew, but recognize that SI has the widest risk-reward of any bank we cover as its growth is tied directly to the health and growth of the cryptocurrency industry.

Some more details from the note:

We recommend an Overweight position in Silvergate. Silvergate is unlike any other bank we cover,and that could be a very good thing. At the heart of its business model is a real-time payments platform — the Silvergate Exchange Network (SEN) — that facilitates the transfer of US dollars between its digital currency customers. Thus, Silvergate gives bank investors a nearly pure-play way to participate in the rapid growth of the nascent cryptocurrency industry. It is the fastest growing bank we cover, with earning asset balances expected to increase 48% over the next 12 months (and already up 434% LTM), with minimal credit risk as loans held for investment are just 6% of earning assets. It has the highest percentage of noninterest-bearing deposits at 99.3% (vs. the peer median of 35%) of any bank in our coverage, the lowest cost of funds at just 1 basis point (vs. peer median of 19 bps),and is the most asset-sensitive bank by far, with a 100-bp increase in rates driving a 52% increase in net interest income (vs.a 5.5% increase for the median midcap bank). We expect 37% annual EPS growth through 2025, and see the potential for further earnings growth (which is not included in our model) from new lending or fee-based products yet to be introduced.

The SEN is the core of its distinctive business model. The company does not charge to use the Silvergate Exchange Network, but it does benefit because customers hold their deposits with Silvergate in order to use the SEN to transfer money around the digital currency ecosystem. Growth in core deposits, which are up 581% Y/Y to $11.4 bil, is a key part of our investment thesis. We expect deposit growth will remain robust,albeit growing at a much slower pace than the over the last year, rising 47% over the next 12 months, driven by the growing number of participants in the cryptocurrency market using the SEN and increased acceptance of cryptocurrency as an asset class and a form of payment. Moreover, Silvergate pays no interest on its digital currency deposits,although its customers benefit from improved capital efficiency and positive network effects.

SEN Leverage and stablecoins could provide earnings upside. Silvergate makes bitcoin-backed loans to its digital currency customers through its SEN Leverage program. Since this program started in early 2020, ithas never incurred a loss or a forced liquidation given its constant monitoring and low LTV requirements. We expect SEN Leverage to drive most of the company’s loan growth going forward, although even at $900 mil in loans expected by the end of 2022, SEN Leverage loans would still account for just 4.5% of earning assets. Unlike most other banks, loan growth is not a meaningful driver of earnings growth (but deposit growth is), implying far less credit risk at Silvergate than most other banks. Potential upside to our EPS estimates could come from the company switching to an originate and sell model for its SEN Leverage loans,as well as moving to a variable fee for the use of the SEN when stablecoins are minted or burned. As stablecoin adoption improves for merchant payments and cross-border transactions, including remittances,a variable fee structure could provide meaningful upside to our EPS estimates. Neither originate and sell nor a variable fee is included in our earnings model currently.

Sizable upside… We believe Silvergate should be valued based on its earnings growth (similar to other faster-growing financials), rather than being compared against more traditional and slower-growing banks, particularly given its minimal credit risk as its held for investment loan portfolio is just 6% of earning assets. Using a peer group of 34 faster-growing financials, Exhibit 11 and applying a 50% discount to account for the volatility and uncertainty around its earnings growth, its potential credit risk (however minimal), the volatility of the crypto markets, and other potential risk factors (including regulation of the cryptocurrency markets), we arrive at a price target of $158. And that includes our expectation that SI issues another 6.3 mil shares through 2025 to fund its rapid balance sheet growth (it has already issued 7.4 mil shares since the start of the year). However, given the wide range of outcomes, both in terms of its growth potential and meaningful risk factors, SI has the widest risk-reward skew of our coverage, with a $300 bull case (189% upside) and a $40 bear case (61% downside)

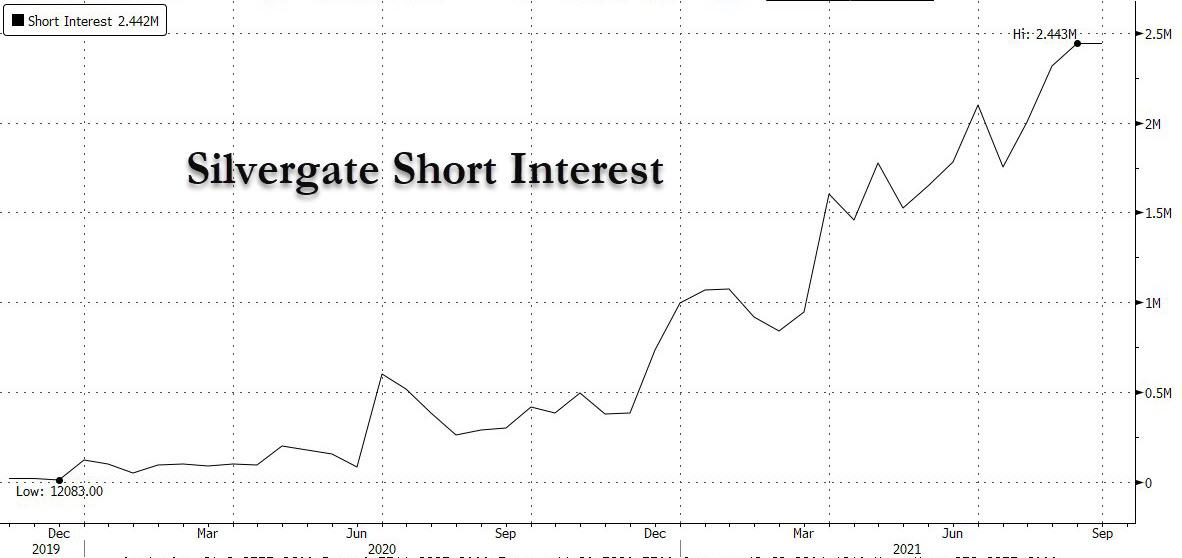

There is much more in the full Morgan Stanley report (available to pro subs in the usual place), but we would add another reason why we think this stock could grow substantially from here: with a very modest market cap (below $3 billion), the stock which is quite illiquid has seen its short interest surge to record highs.

This means that in keeping with other heavily shorted stocks, it wouldn’t take much of a move to start a squeeze especially if it is compounded with Silvergate becoming a meme stock du jour (or longer) for the reddit daytrading crowd, an outcome we expect is inevitable as more big banks follow Morgan Stanley in initiating bullishly in the name.

Tyler Durden

Mon, 09/27/2021 – 12:59

via ZeroHedge News https://ift.tt/3CRtRBK Tyler Durden