What Happened To The $650 Billion In SDRs Issued In 2021?

Submitted by Jan Nieuwenhuijs of Gainesville Coins

A bazooka issuance of 456 billion new SDRs (~$650 billion) by the IMF in August 2021, “to boost global liquidity,” has accomplished very little of what was intended. Numerous nations are teetering on the brink of collapse and global growth is declining. Paltry SDR trading volume over the past year confirms the flaws of this asset.

As we shall see, the SDR is mainly used to grease the IMF’s wheels of bureaucracy.

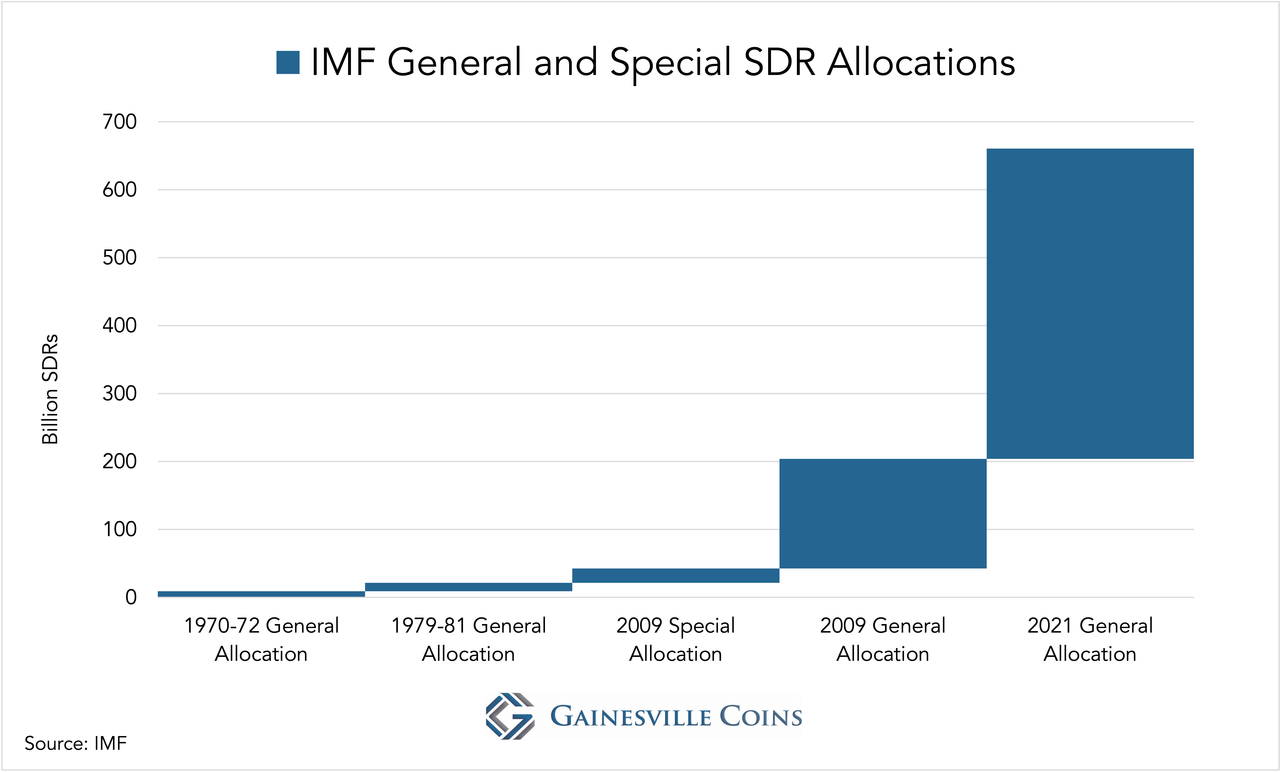

Before August 2021 total Special Drawing Right (SDR) allocations to International Monetary Fund (IMF) members stood at 204 billion. (1 SDR is currently worth about $1.3 U.S. dollars). Through the addition of 456 billion SDRs, total allocations increased by 124%. Yet the new issuance has done next to nothing of what IMF’s Managing Director Kristalina Georgieva promised in 2021:

This is a historic decision—the largest SDR allocation in the history of the IMF and a shot in the arm for the global economy at a time of unprecedented crisis. The SDR allocation will benefit all members, address the long-term global need for reserves, build confidence, and foster the resilience and stability of the global economy. It will particularly help our most vulnerable countries struggling to cope with the impact of the COVID-19 crisis.

When it sounds too good to be true, it usually is. First off, creating more SDRs doesn’t increase global liquidity (the quantity of international reserves). Nor does it benefit all members, build confidence, stabilize the global economy, or foster resilience.

The SDR disappoints because it’s not a currency, it isn’t backed by anything, there is no free market to exchange them, and trade is illiquid (difficult to convert large quantities into cash). Regardless, the IMF spreads falsehoods about the SDR to keep up appearances.

Let’s dispel the myths surrounding the SDR.

What Is an SDR?

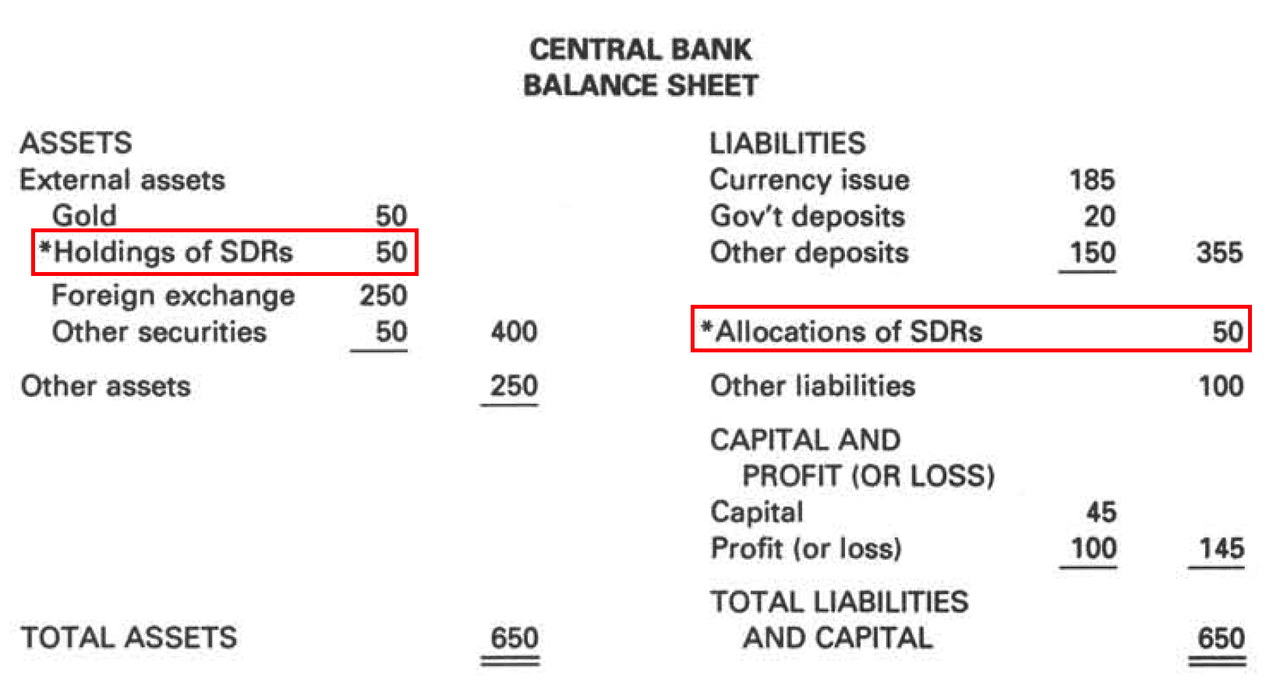

Officially the SDR “is a potential claim on the freely usable currencies of IMF members.” The IMF can allocate new SDRs to all of its member states. The IMF can’t allocate SDRs to itself. At issuance a member gains a double book entry on its balance sheet based on its IMF quota. SDR holdings on the asset side are equal to the amount of SDR allocations on the liability side. Because holdings and allocations net out, a new issuance of SDRs doesn’t make any member richer nor poorer.

Only central banks or monetary authorities, and several international financial institutions such as the IMF and BIS, can hold SDR positions. SDRs cannot be spent on goods and services. Commonly, the only way for a member to make use of its SDR position is to exchange SDR holdings for freely usable currencies (dollars, euros, yen, etc.) with another member.

There is no free market for SDRs to relieve excess supply or demand. Members can exchange SDR holdings through the IMF’s SDR Department, or they can be exchanged directly between parties, though this is more rare. States will notify the SDR Department if they want to buy or sell SDR holdings, in what quantity, and in exchange for which currency. Next, they await if their orders are filled.

Only SDR holdings can be exchanged. A member’s SDR allocations are static unless the IMF decides to issue new SDRs. The SDR exchange rate is set by the exchange rates of a basket of currencies designated by the IMF: the U.S. dollar, euro, Chinese renminbi, Japanese yen, and British pound.

Suppose member A and member B both hold an equal amount of SDR holdings relative to their SDR allocations. Member A wants to sell 100 million SDR holdings for Japanese yen, and member B, coincidentally, wants to buy 100 million SDR holdings with Japanese yen. Both notify the SDR Department, and the exchange is cleared. After A received yen and B received SDR holdings, A will have more SDR allocations relative to its holdings, and, conversely, B will have more SDR holdings relative to its allocations.

Member A will now pay the SDR interest rate to the SDR Department and B will receive the SDR interest rate. Simplified, every member that is a net seller of SDR holdings will pay interest until it has bought back those holdings and vice versa (net buyers receive interest until they sell back). The SDR Department manages all interest flows. Effectively, selling SDRs is borrowing currency and buying SDRs is lending currency.

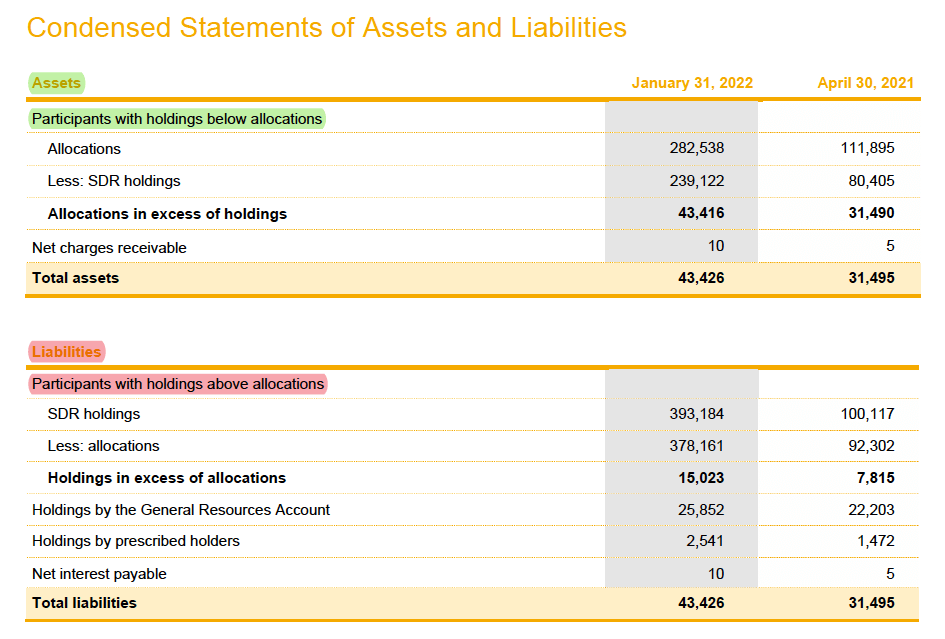

The IMF states SDRs are not their liabilities. This is although a country having a net SDR holding (more holdings than allocations), and thus eligible for receiving interest, is a liability of the IMF. See the SDR Department’s balance sheet from a Quarterly Report below. A country having a net allocation is an asset for the IMF.

The SDR interest rate is based on short term interest rates of the currencies that comprise the basket of currencies used to calculate the SDR’s exchange rate. SDR interest is paid every three months in SDRs, and the floor rate is 0.05%.

An SDR holding (“SDR” hereafter) provides the owner a potential opportunity to borrow freely usable currencies. An SDR is central bank collateral for a potential swap* without a specified maturity. I write, “potential opportunity to borrow,” and, “potential swap,” because there is little liquidity in SDRs and anything but a guarantee there is a seller of usable currency willing to buy SDRs. Hence, the SDR officially “is a potential claim on the freely usable currencies of IMF members.”

*In this case a swap means a “forward swap,” which has a spot and a forward leg. In the spot transaction a member sells SDRs for foreign exchange (FX)—and its counterparty does the opposite—and in the forward transaction this trade is undone buying SDRs with FX. A forward swap is the same as a collateralized loan. Hence, “swaps” often refer to lending/borrowing.

For more details, such as how the SDR exchange rate is calculated, please read my previous article.

The SDR’s Shortcomings

1. Trading in SDRs is illiquid because there is no free market. Only 190 countries and a few institutions can own and exchange SDRs; no private entities can expand the user base and improve liquidity. Nor does the IMF ever want to create a free market. When several Highly Indebted Poor Countries (HIPCs) want to sell (supply) SDRs for currency through the SDR Department, but demand is much lower, the IMF selects the HIPCs to prioritize. On this basis, the IMF will prefer to maintain a managed market. As with communism, managed markets come with a wide variety of problems.

When confronted with the SDR’s poor liquidity, IMF economists will point to the “designation mechanism.” This option should allow the IMF to decree which country must buy SDRs. All members have signed the IMF’s charter—the Articles of Agreement—that stipulates all rights and obligations. But when push comes to shove the Articles of Agreement can’t overrule sovereign nations.

In 1971 the U.S. unilaterally suspended gold convertibility, ended Bretton Woods, and introduced an era of free floating exchange rates. In 1973, “not a single IMF member was any longer in conformity with the Articles of Agreement,” according to Benn Steil, author of The Battle of Bretton Woods. Just as the Articles of Agreement couldn’t force countries to sustain fixed exchange rates in 1970s, today they can’t force countries to buy SDRs in quantities dictated by the IMF.

2. The last SDR issuance was, according to the IMF website, “to boost global liquidity.” It seems the IMF (the Fund) wants us to think that an SDR issuance increases the total amount of convertible currencies. SDRs can’t be spend on goods and services, though, and thus an increase in SDRs “does not increase the total liquidity of the global monetary system.” Why the Fund states new SDRs increase net international reserves is due to the subtle art of accounting.

There is a discussion on creating and trading SDRs and its effect on the money supply in a paper from 2011 that reads, by the IMF’s own admission: “Overall, the creation and use of SDRs is likely to have a neutral effect on the global money supply.” So why all the talk about issuing SDRs to boost global liquidity and meet the global need for reserves? (By the way, why not revalue gold if there is a global need for reserves?)

3. Newly allocated SDRs are distributed among members based on their IMF quota. In general, due to how quotas are calculated, wealthy developed countries that have large economies are being allocated the most SDRs, and poor undeveloped countries that have small economies get the least. About two-thirds of the SDR allocation implemented in August 2021 went to developed economies.

4. All the literature about SDRs is focused on the benefits of selling SDRs, how many developing countries can or have sold SDRs, and so on. It is as if this instrument is designed to be sold. What about buying and owning SDRs?

Buying SDRs is risky. Suppose China buys 10 billion SDRs with U.S. dollars. Over time, these holdings grow due to compounding interest. If China can ever sell those SDRs to get back currency when needed is uncertain. The Fund may prioritize other countries, provided there are buyers. The more SDRs the bigger the risk.

5. The SDR only pays out a short-term interest rate. For central banks that have a long-term investment strategy, the SDR isn’t suitable, as it doesn’t offer a long-term interest rate, which is normally higher than the short-term rate.

6. According to the Fund, SDRs are not a claim on the IMF. In court this statement might hold true; in practice the counterparty of a net SDR holding—the one responsible for paying the SDR interest rate—is the IMF. Furthermore, members rely on the IMF for being able to exchange SDRs. Long story short, SDR owners are greatly exposed to the Fund and thus all its members. What happens when members default? Counterparty risk increases.

7. More than once the IMF has changed the essence of the SDR in the past and can do so again in the future. What an SDR is today can be something different tomorrow.

Who Are the Largest Buyers and Sellers of SDRs?

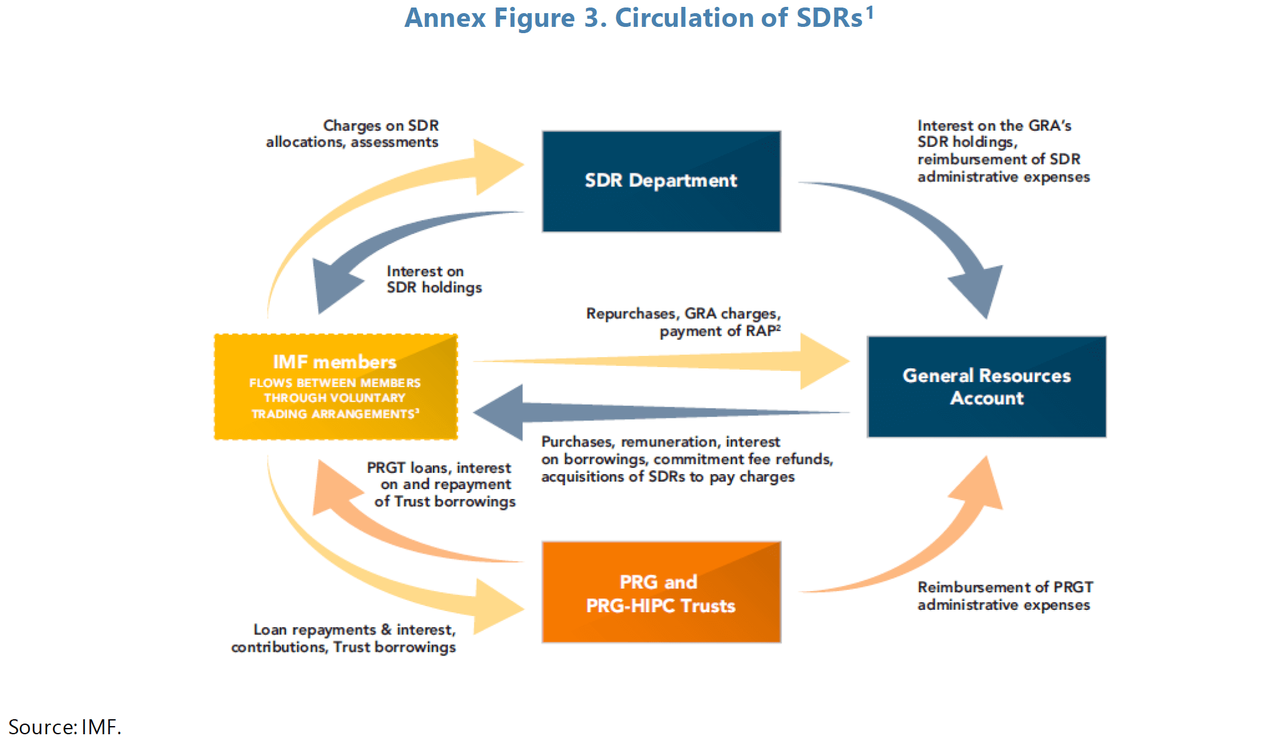

Although detailed SDR trading data is not available, it can be said the bulk of SDR trading comes from transactions between the Fund itself and member states. The biggest buyer of SDRs is the Fund and the largest sellers are developing countries. Consequently, the largest wallet is the IMF’s General Resources Account (GRA). In July 2022 the GRA held 23 billion SDRs, while the second-largest owner, the U.S., held 4.6 billion SDRs. From the IMF:

Broadly, most SDR transactions relate to Fund-related operations versus uses of SDRs unrelated to GRA … operations (see … Annex Figure 3).

Regarding residual trading activity, SDRs are mostly sold by poor countries to rich countries.

A chart of all SDR holdings shows how big of a buyer the IMF exactly is.

The Fund’s operations in a nutshell: members have to pay a subscription to the IMF (based on their quota) mainly in their national currencies and reserve currencies. In line with its mandate the IMF then lends out these funds to nations with balance of payments problems. If the borrowers want to repay those loans they can do so in SDRs, to a certain extent, and hence the Fund’s GRA tends to amass.

Strangely, as the SDR has existed since 1969, no basic SDR trading data is published on a recurrent basis. An imperfect option is to collect position data from all participants in the SDR universe and track changes month by month. Or, for more figures, wait until special reports are published.

Based on the first option I estimate 36 billion SDRs have changed hands over the twelve month period since the end of July 2021. By comparison, trading volume in the global repo market is $3.5 trillion U.S. dollars (2.7 trillion SDRs) per day! A meager 36 billion exchanged in a year after 456 billion SDRs were issued reflects the disadvantages of this asset.

Although it’s possible actual trading volume was somewhat higher or lower, I would like to stress it’s much lower if we subtract trades related to IMF transactions.

Here is an example of how monthly changes in SDR holdings (my measurement of trading volume) are often affected: in August 2021, Argentina was allocated 3 billion SDRs. Up until February 2022 Argentina managed to sell nearly all its SDRs (+3 billion in trading volume). From August 2021 till February 2022 the Fund was the biggest buyer of SDRs, having mopped up 30% of all (and thus Argentina’s) sales. In March 2022, the IMF approved a loan to Argentina worth $44 billion U.S. dollars. Argentina received part of this loan in 5 billion SDRs from the IMF’s GRA (+5 billion in trading volume). Since March Argentina has mostly been selling, and so the cycle of shuffling SDRs between Argentina and the GRA can repeat.

Argentina has been responsible for nearly 10 billion of my total estimate of 36 billion in SDR trading volume, though 75% of it was sent back and forth with the Fund.

In 2009, trading after the 183 billion SDR issuance was also lackluster. During the twelve months that followed the allocation in 2009, only 3.4 billion SDRs changed hands in non-IMF-related transactions. The sellers were mostly developing nations, of which more than 80% sold at least 75% of their new SDRs. After an initial “spike,” volumes came down, save a few larger trades in 2015. Just 5 trades accounting for 35 million SDRs were executed in 2020. See the table below.

Before the 2009 issuance the Fund projected annual volume in non-IMF-related transactions to be 20 billion SDRs, which turned out to be 83% lower at 3.4 billion. Disappointing indeed.

In its first ever Annual Update on SDR Trading Operations, released in October 2021, not much is written about SDR trading volume after August 23, 2021. Without making a distinction between IMF-related and non-IMF-related transactions, it’s stated total volume was 6.9 billion SDRs in August and September 2021. My estimate of trading volume—based on month to month changes in positions of all participants—is roughly equal for this period. All sellers were developing countries, on average selling 82% of their new allocations.

Conclusion

According to the IMF, SDRs can be used by members to borrow FX unconditionally as opposed to the Fund’s regular lending operations that come with strings attached. I’m having a hard time acknowledging the unconditional aspect, because “most SDR transactions relate to Fund-related operations” and every member is largely depended on the Fund’s managed market to trade SDRs. The SDR is misrepresented by the Fund.

In my view, the SDR is an instrument used to reinforce the IMF’s right to exist. Certain theories of bureaucracy state that officials, too, “are motivated by their own self-interest [income and power] at least part of the time.” Like every other bureaucratic entity in existence the Fund wants to grow. Its inherent mission has produced a narrative about how the SDR is to “benefit all members, address the long-term global need for reserves, build confidence, and foster the resilience and stability of the global economy.” A great pitch, of which little is true.

Here’s my theory of why new SDRs are issued periodically. Because the Fund is the biggest buyer and owner of SDRs, it’s also the largest recipient of SDR interest. As mentioned above, many developing nations sell 80% of their SDRs instantly when new ones are issued. In the course of time paying SDR interest becomes a problem for these countries as they run out of SDRs. For the Fund there is an incentive to issue new SDRs to bail out these countries and thus itself. When all countries get new SDRs, the ones in debt (having sold SDRs) can continue paying interest to the Fund. Yes, several countries had almost no SDRs left before August 2021.

In the Proposal For a General Allocation of Special Drawing Rights, published in July 2021, the IMF writes: “Potential additional SDR inflows to the GRA resulting from increased use by members of SDRs for transactions with the Fund would be closely monitored and are expected to be manageable.” Ironically, the IMF knows that buying too much SDRs is risky.

The SDR’s “value as a reserve asset derives from the commitments of members to exchange SDRs for freely usable currencies…” SDRs have no value outside the SDR system, and if members aren’t committed to the system anymore, for example because other members default or oppose the political views of partner members, the SDR value drops to zero.

The SDR will never be more than a fringe reserve asset, and thus can’t replace the dollar as the world reserve currency, like some economists want to believe.

Tyler Durden

Mon, 08/29/2022 – 05:00

via ZeroHedge News https://ift.tt/RcAnBzH Tyler Durden