One Bank Surveys The Epic Carnage: “The Faster We Crash, The Sooner Fed Can Pivot”

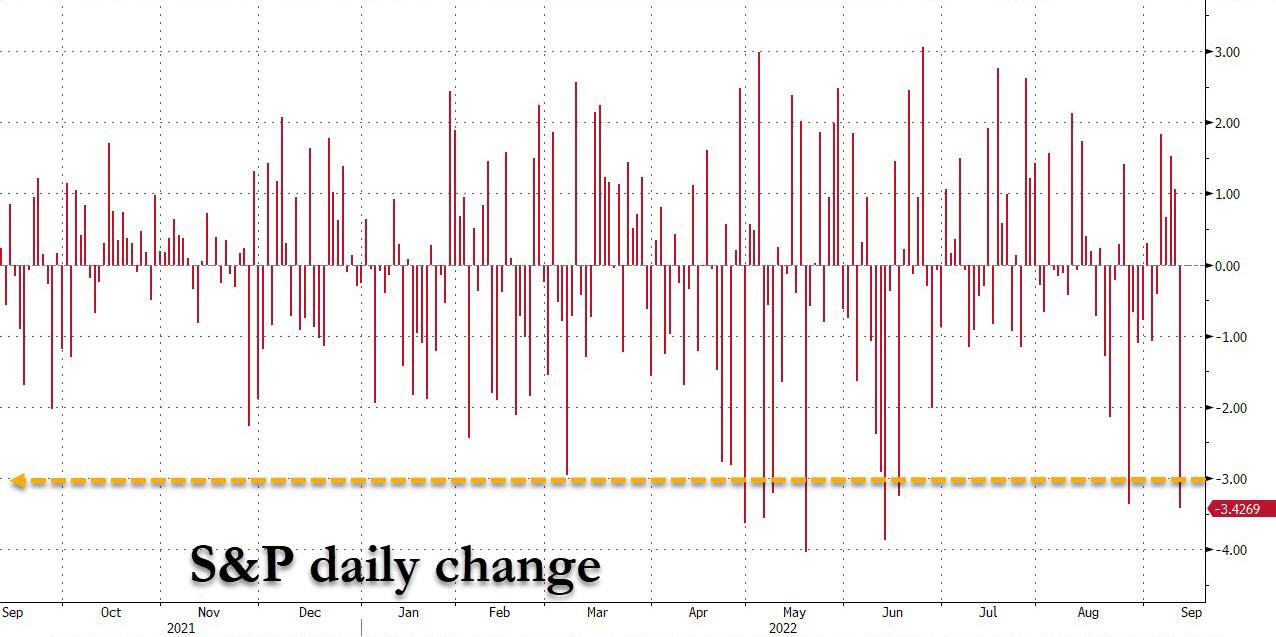

Anyone hoping that the post-CPI bloodbath, which will send the S&P to its 8th 3+% drop of 2022 (offset by just 1% jump this year)…

… will lead to at least a little peace and stability in the markets, will be woefully mistaken, because as Goldman reminded us last night, Friday is not only when the buyback blackout period begins…

“We estimate the next blackout window will begin at the end of this week ~9/16 when ~50% of the S&P 500 are in their closed window. As a reminder, we typically expect flows to decrease by ~30-35% during blackout.” – GS

— zerohedge (@zerohedge) September 13, 2022

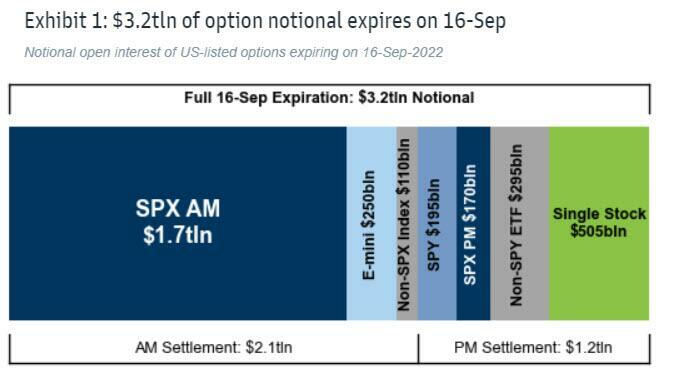

… but is also when we get another massive $3.2 trillion opex…

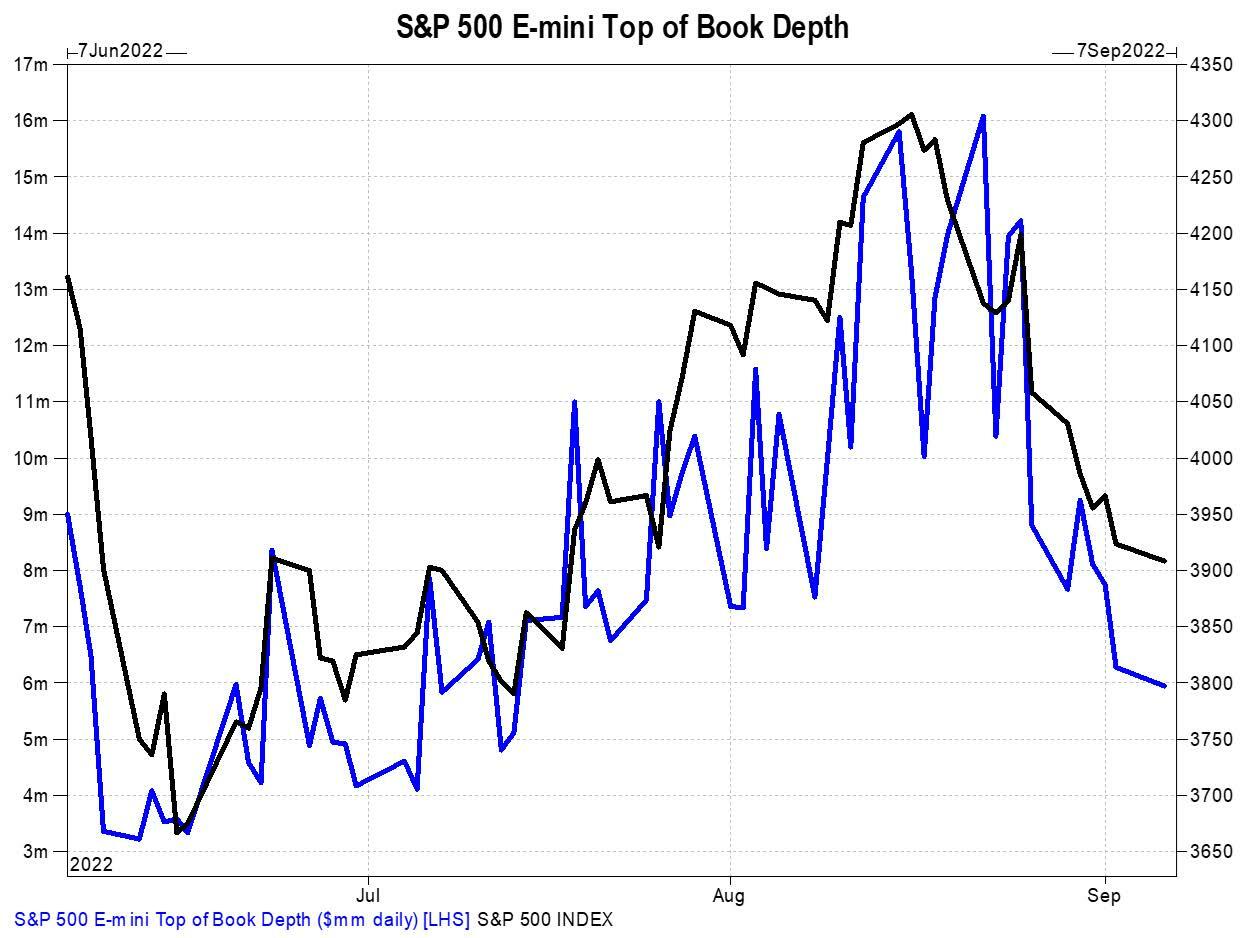

… at a time when there is zero liquidity….

… effectively guaranteeing a surge in volatility (if not an outright market crash).

And as we survey the carnage, here is Nomura’s Charlie McElligott summarizing the biggest shocks today in i) macro, ii) vol/options and iii) systematic and and rebal EOD flows .

MACRO:

- So first things first: Today’s CPI print (and ensuing gap higher in Fed “Terminal rate” ~ +35bps to 4.35%) is killing any hopes of a “Soft Landing,” and instead increasing odds of “Hard Landing,” as the Fed is now perceived as HAVING TO “slam the breaks” with even-tighter financial conditions into hot inflation and labor markets (lends more credibility to their “worst fears” of “wage / price spiral”)

- Accordingly, the EDM3EDZ3 curve (Jun23-Dec23) has INVERTED further to -40.5bps, seeing an incremental 8.5bps of implied FED CUTS added today in that 2H23 window—bc the worse the “Hard Landing,” to larger the commensurate EASING required thereafter to jumpstart things

- Perversely, the only real “bid” to US Equities Index Vol today is being displayed in Upside / Call Skew (or “crash-UP”), moving higher today on the selloff…which I am gonna take a leap of faith on, and tie into the above Rates idea that “the sooner / larger magnitude that we crash it, the sooner Fed can pivot” narrative….and as I said, all while Equities selloff, but while downside hedges bleed-out and underperform, because by being so low net exposure / so high cash holdings / so under-exposed, you’re already running de-facto “Short”

- On the flipside, we are seeing ATM Vol and Downside (shorter-dated) move lower, which might be counter-intuitive to some, but it’s actually continuing the theme all year: clients have so little exposure on that they are not actively seeking out fresh downside or “crash” hedges, and are instead really just monetizing remaining legacy downside hedges into downside.

VOL / OPTIONS:

- Today’s gap-down now shows us in tricky territory ahead of Qtrly Options Expiration on Friday, where we now see Dealers back in “Short Gamma vs Spot” location across the board in US Eq Index Options—which means their Options position hedging flows could likely act as an “accelerant” and “press” moves—sell into selloffs, buy into rallies

- SPX / SPY “Short Gamma vs Spot” below 4056, with Spot 4000 approx -$5B per 1%, “Max Short Gamma” @ 3825 approx -$12B per 1%

- QQQ “Short Gamma vs Spot” below 304.45

- IWM “Short Gamma vs Spot” below 194.95

- Current supports are 4000 (50% retrace, old support and with $3.2B of $Gamma into Friday’s expiration)…and from there, 3920 (61.8% retrace of June low to August high move)

- To that point on clients and Index / ETF level hedging, however, I would say that Options are expensive enough still where I think many have instead moved away from the options space, and instead, are going the cheap route of “dynamic hedging” with futures….which should be noted could act as a source of synthetic “Negative / Short Gamma” in the market to contend with, as it could further exacerbate moves and “overshoots” in both directions

SYSTEMATIC AND REBALANCING END OF DAY FLOWS:

- Taking a snapshot of the current “-3.0%” day and projecting…

- Resumption of fresh CTA “sell flows” (after the recent impulse “buy to cover”!) are actually showing realtively smallish notional today in US Equities, approximately “just” -$5.8B across S&P, Nasdaq and Russell positions, as frankly, the recent back and forth volatility is reducing the position sizing from a risk-management perspective….while next “sell” levels (to get back to “-100% Short”) are meaningfully below market and are far OTM lower, while in-light of today’s gap down, “buy to cover” levels of any magnitude are now also v far OTM higher

- Vol Control strategies are actually a meaningful story today and in coming-days, however..because they have added-back +$33B of US Equities exposure over the past 3m …and now on a -3.0% day would imply approx -$8B to sell off this now recently larger notional exposure…as this has been the first truly “crashy” day in a long while (only eight days YTD of 3% drop or more)

- Leveraged ETFs definitely do matter on a “-3%” day, where we currently approximate ~ -$11B for sale across US Equities products, majority of that being Nasdaq / Tech sector heavy as it is so Rates sensitive

Tyler Durden

Tue, 09/13/2022 – 15:22

via ZeroHedge News https://ift.tt/IPyFTXk Tyler Durden