Goldman Trader: I Said “This Reminds Me Of 2008” More Times This Week Than I Can Remember

Over the weekend, we discussed that the probability of another sharp leg lower on Monday after Friday’s panicked reversal of Thursday’s furious gains is extremely low (in fact it’s likely that we will get yet another squeeze), if only due to technicals and positioning as hedge funds doubled-down on short aggressively into Friday’s dump while overall hedge fund net leverage fell to the lowest level since Mar ’20.

And if that isn’t enough, Sundial Capital’s Jason Goepfert pointed out something far more startling: “Last week, retail traders bought $19.9 billion worth of puts to open. They bought only $6.5 billion in calls to open. This is the first time in history that puts were 3x calls.“

I don’t think people really appreciate what’s happening in the options market right now.

Last week, retail traders bought $19.9 billion worth of puts to open. They bought only $6.5 billion in calls to open.

This is the first time in history that puts were 3x calls. pic.twitter.com/GR2apNfFtb

— Jason Goepfert (@jasongoepfert) October 16, 2022

Translation: the massive Delta hedge unwind that sent futures explosively higher on Thursday after the dismal CPI print is back even bigger than before, and just waiting for the signal to unwind the dealer delta hedge that will send futures soaring higher.

Still, as we discussed yesterday, while technicals point to a rollercoaster reversal on Monday as we get another overshorted, oversold rally on Monday and we may get a powerful bear market rally in November that pushes stocks to 4,000 or higher by year end, “the bear market won’t end until the Fed pivots. The timing of that still remains to be determined, however after the midterm elections when the political blinders drop, we expect that the full – and dire – picture of the US labor market will finally emerge and shock everyone, especially the Fed.”

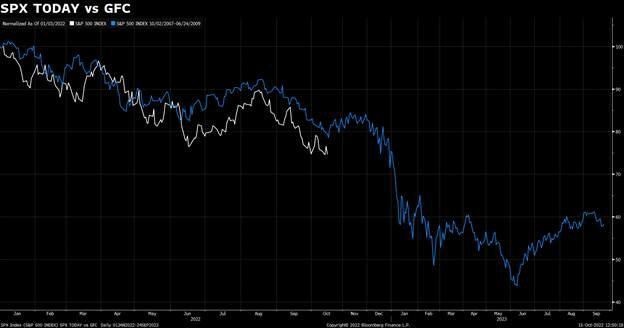

Until then, however, the bear market will be alive and raging, and it is this part of the market cycle that Goldman flow trader, Matt Fleury, who has been one of the most vocal bears on the bank’s trading desk, focuses on not only the bear market that is yet to come but also on the Mother of all bear markets, the Global Financial Crisis.

As he writes in his latest note, titled “Adult Swim” (available to pro subs in the usual place), “I said “this reminds me of 2008” more times this week than I can remember. The velocity of moves is increasing. The pace of tremors quickening.”

Below we excerpt from Fleury’s must-read note, published with quite a bit of urgency late on Saturday night ahead of what is shaping up to be another hair-raising week, at a time when as Bank of America warned that “Liquidity Breaks And Credit Freezes” as its Credit Dysfunction Indicator Breaches The Critical Zone. In short, all hell may be about to break loose.

The year when you started in this business shapes you. I started in 2006 at Bear Stearns with a Bachelor & Masters in how good the economy of Ireland was during the Celtic Tiger. Quite a baptism.

If you started in this business after 2009, all you know is a ‘buy the dip’ market, all you know is a Fed that has your back. You have got glimpses of crashing bear markets. But never rolling bear markets.

A crashing bear market is like swimming in shallow water; eventually you put your feet down and its ok, and there is a lifeguard on duty (the Fed) who is there to save you.

A rolling bear market is deep water swimming, with no lifeguard.

That’s what we are in. A rolling bear market.

The pain trade is lower. It’s always lower.

I get in this debate all the time, and it’s usually with people who started after 2009. It’s a pain trade to watch your friends lose their entire net worth because they never sold a Bear Stearns share. It’s a pain trade to watch your parents lose what money they had saved their whole lives which were in Irish bank shares when they went under.

It is not a pain trade when a hedge fund returns +0.5% on a given day and the market is 2%. They get paid on that +0.5%.

The pain trade is lower, and I do not believe we have seen the worst yet. Sample conversation on the trading floor:

“Matt, but everyone is bearish.”

“Yes, but those same people have their entire net worth ex their homes in equities.”

“Oh.”

Liquidity is tightening

“Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks, and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves market.” – Stan Druckenmiller

The Fed’s continued aggressive pace of hikes is causing unexpected knock on effects. I was certainly not aware of how levered the UK LDI pensions were. This had an eerie feel to me of the Bear Stearns hedge funds that went down in 2007 and all I could think of “what else is out there we don’t know about?”

The inflation reading in the US was undoubtedly bearish for risk assets.

There was an oversold/technical bounce which was swiftly sold. Ironically this is exactly what I was looking for last month which turned out to be a very strong candidate for worst call of the year.

It is noticeable however how these bounces are getting shorter and shorter. This makes me very uneasy.

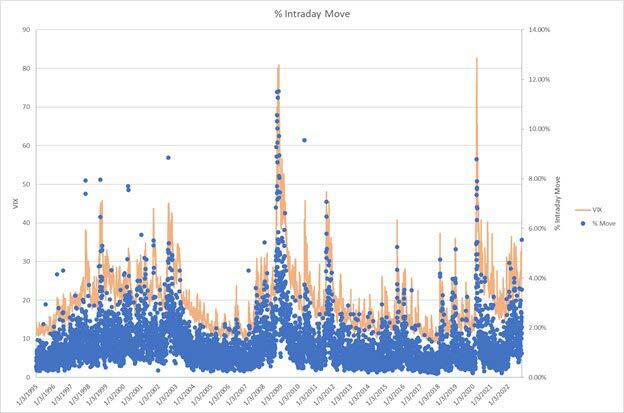

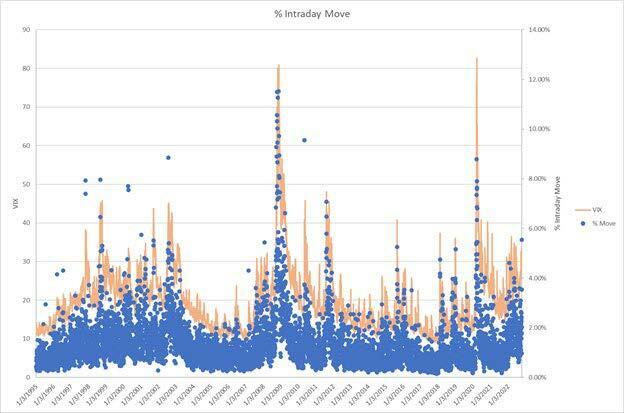

The mark of a bear market is large intraday trading ranges. H/t Matt Kaplan for the chart, which I think is a good illustration of when you get wide intraday trading ranges, it tends to be in the depths of bear markets. Based on history, there is certainly more scope for these to increase in frequency.

Here are a few headlines which caught my eye this week in my inbox for GIR’s excellent econ team. A worrying theme:

- Poland: Large Inflation Increase in September Confirmed, As Underlying Inflation Reaccelerates

- USA: Core CPI Inflation Jumps to 6.6% on Service-Sector Strength

- Romania: Inflation Rises by 0.6pp to +15.9%yoy, Surprising Expectations to the Upside

- India: CPI inflation increased in September driven by higher food prices

- USA: Producer Prices Above Expectations In September

- Hungary: Sharp Rise in Inflation on Household Energy Price Hike, And Underlying Inflation Rises Further

- Asia in Focus: ASEAN-5 Inflation Outlook: Higher For Longer

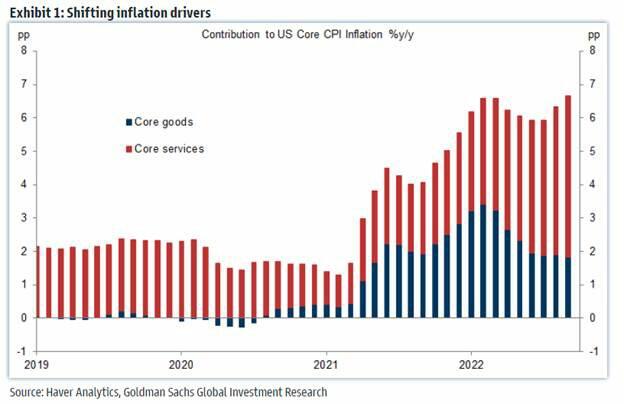

Within the US there is an increased focus on sticky inflation. The transition from goods consumption to services consumption kicks off labor demand and wages drive shelter inflation which is sticky.

Here is the 12mo Atlanta Sticky-Price CPI:

GIR breaks this move from goods to services down nicely:

The Fed’s hands are tied here and the terminal rate which the market is pricing continues to move higher.

If you are waiting for the Fed to pivot and save you, I point you towards the 2024 dots.

I am of the opinion that the Fed has already made one error by not moving quick enough to hike rates, is now compounding that error, and is also making it up as they go along. They will stay the course into 2023 at least.

The market is leading the Fed, and it is moving ever higher.

This hawkish impulse has been a consistent headwind for equities and I don’t see that stalling in the near term.

Putting the UK in the rearview mirror

For quite some time S&P futures have moved hand in hand with Britcoin (GBP), but that seems to be breaking as the events within the UK take almost circus like turns.

I do believe the live cam of “who will last longer?” of Liz Truss versus a head of lettuce (LINK) will mark the “peak UK fears” for stock operators.

Rolling bears

These are what rolling bears look like. This is the environment we are in.

I have seen a lot of talk about the 200wk moving average acting as support. Well yes, it does aside from in rolling bear markets. 200wk MA with Fed support:

But when it breaks in rolling bears, it is ugly:

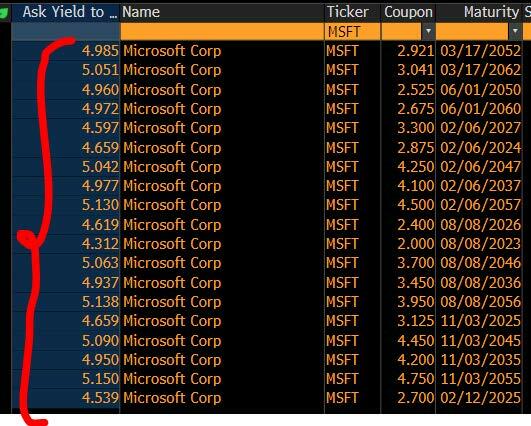

Corporate Finance 101

These are the MSFT bonds on Bloomberg. Let’s call it a 5% average. You can debate the attractiveness of owning a 23x MSFT P/E vs its bond at 5%.

But a more important question right now, if the market deems MSFT paper should yield 5%, where will it price lower quality company debt when they need to come to market?? 10%? 12%?

This is the GIR estimate for net corporate demand in 2023.

Question for the upcoming conference calls:

“Hey great quarter guys. Mr. CFO, in this backdrop, with your cash yielding ~4%, are you really buying back stock? And where do you think you would be able to issue debt in the current environment?”

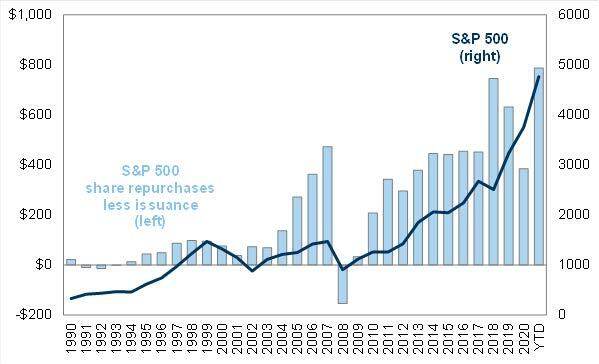

In difficult times, corporate issuance ramps up. I will be watching to see how companies choose to fund themselves in 2023 – via debt or via equity issuance.

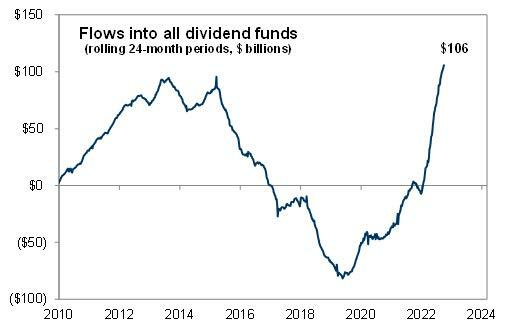

Additionally, there has been a lot of money that flowed into dividend funds – surely that can now buy some high quality IG paper?

Similarly, is there a home to be found for fallen heroes? This is the market value of AAPL + AMZN + GOOGL + MSFT. That looks like a break.

What am I watching this week?

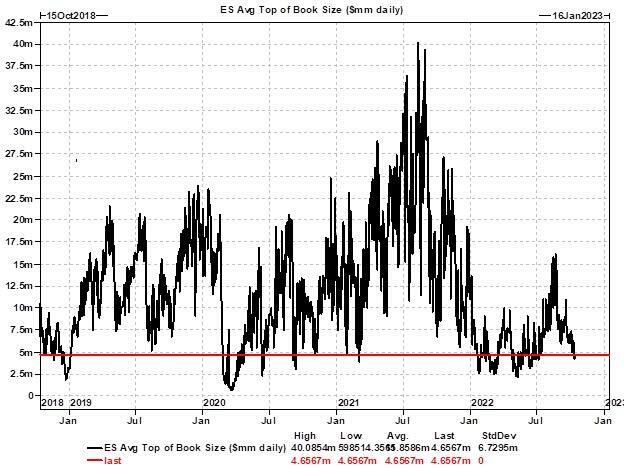

Liquidity remains poor. Top of book depth:

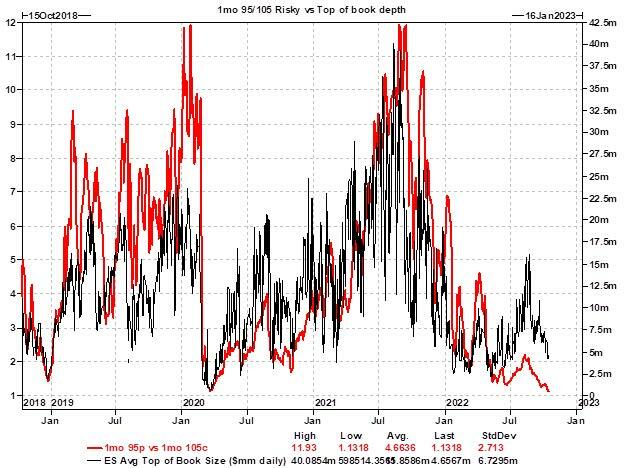

I call this chart the “potential for destruction” – it is top of book depth normalized by 1mo implied vol. It’s as bad now as it was in March 2020.

Overlaying top of book depth in futures vs 1mo 95/105 risk reversals, it will tell you that it is now worse:

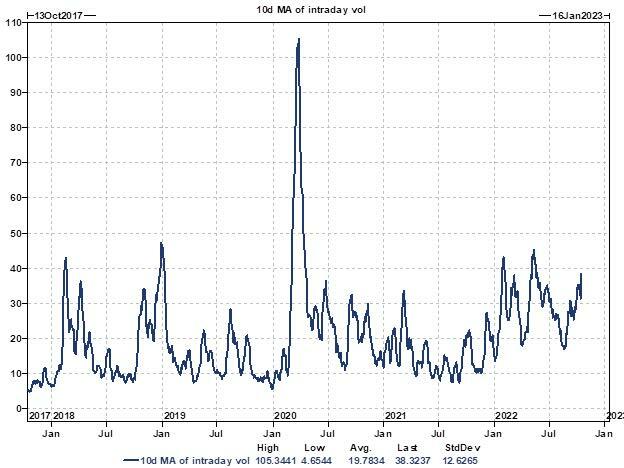

Intraday vol is picking up:

Puts are not helping as much as they could. This is the 100d SPX % change vs SPX 25dp change in vol points. If hedges aren’t working, degrossing is more likely.

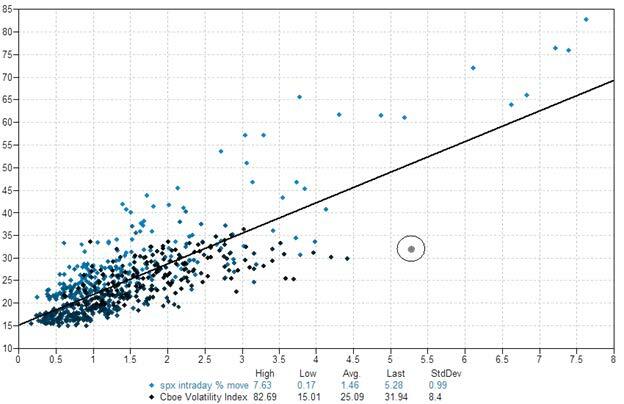

This was the chart from Thursday of intraday SPX move vs Vix level (h/t Cullen Morgan):

This could change soon. I sent around some thoughts to those on my direct mailing list. Options volume is exploding. The tail is wagging the dog.

More daily notional calls traded in SPX on Thursday than ever before.

The 5dma of $put notional is ever climbing. It now dwarfs 2008/9 when dealers hands were less tied due to banking regulation and risks they could absorb.

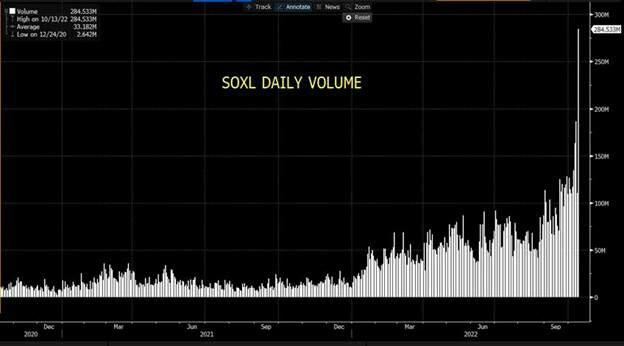

Levered ETF volumes are picking up, and SOXL (Semis 3x levered ETF) is the centre of attention. $10bn+ daily rebalances at the close in this ETF are common place now.

These are not healthy undercurrents. And the Fed’s hands are tied due to the inflation set up.

The Fed pivot will come, but when it comes the Fed pivot will be bearish. It is my view they will be forced to pivot because inflation is coming down due to a cardiac arrest in economic activity.

It is somewhat ironic that a Fed pivot is both part of the bull and bear case.

I do not believe we have seen the full pain of a Fed tightening this quickly yet.

Where are the bankruptcies? Where are the private mark downs? Who owns too much illiquid assets that haven’t had a real mark in years? Where are the over levered homebuilders going under?

The UK LDI pensions look like the first domino to me. The old regime of a central bank supported market is gone. And many business models that were spawned in that era will be tested.

This also comes at a time when the west has no allies in Opec for the first time since inception as the US drains the SPR (potential for oil price to stay elevated further causing headaches for the Fed?), and geopolitical tensions with China potentially impacting future global growth (see escalation on semiconductors late this week).

Good luck out there; it is adult swim, and there is no liFEguarD.

{kind=link}

The full note available to pro subs.

Tyler Durden

Sun, 10/16/2022 – 23:00

via ZeroHedge News https://ift.tt/60FAelP Tyler Durden