Futures Flat With S&P On Cusp Of Bull Market, Oil Jumps After OPEC Production Cut

Futures are flat with oil jumping after OPEC+ cut output by an extra 1mm bpd in a unilateral move by Saudi Arabia taking its production to the lowest level for several years.At 7:30am ET, S&P futures were flat, while Nasdaq futures were down 0.2% with some artificial-intelligence exposed stocks like Nvidia Corp. and C3.ai Inc. trading down. In contrast, Apple Inc. surpassed its previous closing record in premarket ahead of what’s expected to be its most significant product launch event in nearly a decade. Oil rose 2%, with oil giants such as Chevron and Exxon up in premarket trading. The Bloomberg dollar index is up as are 10Y yields now that the market’s attention turns to the $1+ trillion deluge in new debt issuance. Gold dropped, as did bitcoin after the crypto currency got its usual Asian session rugpull.

Oil-related stocks rose in US premarket trading after Saudi Arabia announced it would scale back oil output by a further 1 million barrels a day in July, taking the OPEC+ member’s production to the lowest level for several years after a slide in crude prices. Saudi Energy Minister Prince Abdulaziz bin Salman said he “will do whatever is necessary to bring stability to this market”; with oil prices being weighed down by relentless shorting by hedge funds amid a softer economic outlook. The rest of the 23-nation OPEC+ group offered no additional action to buttress the current market, but did pledge to maintain their existing cuts until the end of 2024. Chevron, Exxon Mobil and Occidental Petroleum all rise more than 1%, as do Phillips 66 and Schlumberger.

Also in premarket trading, Apple rose 0.6% putting the shares on track to reach a new record high. The company is expected to launch a mixed-reality headset at the Worldwide Developers Conference on Monday, marking its most significant product launch in nearly a decade. Here are some other notable premarket movers:

- Bellerophon Therapeutics shares slid 74% Monday after the company said its phase 3 rebuild study of INOpulse to treat fibrotic interstitial lung disease failed to meet its primary endpoint.

- Day One Biopharmaceuticals shares rise as much as 35% after the biotech company provided updated data for its drug for the treatment of pediatric low-grade brain tumors that was “highly impressive,” according to a Wedbush analyst.

- Epam Systems falls as much as 11% after the IT services company cut its adjusted earnings per share forecast for the second quarter.

- ImmunoGen shares gain as much as 19% in premarket trading on Monday, after the biotech company provided full results from its late-stage trial for its treatment of ovarian cancer.

- Oil-related stocks rise after Saudi Arabia announced it would scale back oil output by a further 1 million barrels a day in July, taking the OPEC+ member’s production to the lowest level for several years after a slide in crude prices.

- Palo Alto Networks Inc. (PANW) shares gain 4.9% on Monday, following a Friday announcement that the stock is set to replace Dish Network Corp. in the S&P 500.

- Southwestern Energy Co. (SWN) rises 2% as it looks like a “logical target” for either Coterra Energy Inc. or Chesapeake Energy Corp., according to Citi.

With the debt ceiling now behind us, markets will now prepare for a deluge of issuance; BBG reports that bearish positioning in the S&P is highest since 2007 while bullish bets on NDX are near last year’s highs. Meanwhile, the steamrolling of the bears continues with S&P 500 is just 0.2% short of a 20% gain from its October low in the previous trading session; the Nasdaq 100 is already firmly in a bull market, as traders anticipate a pause in the Federal Reserve’s rate hiking cycle. Expectations that any slowdown in the US would be mild and optimism about developments in AI have also fueled the gains.

James Athey, investment director at Abrdn, said the advance toward a bull market focused on the small number of important but highly backward-looking economic readings that suggest the economy is doing well. “The broader data set shows much less strength and much more volatility and vulnerability,” he said. “But until jobs crack, I’m sure equities will choose to ignore.”

Strategists are split about the path forward for stocks from here. A Morgan Stanley team led by Michael Wilson said the likelihood of Fed rate cuts in 2023 and durable growth playing out simultaneously is low and they expect a tactical correction in equities before a durable recovery and a real bull market.

UBS Global Wealth Management strategists also said the risk-reward balance for stocks, especially in the US, remains unfavorable. On the flip side, Evercore ISI strategists raised their S&P 500 target as inflation easing likely signals a Fed pause.

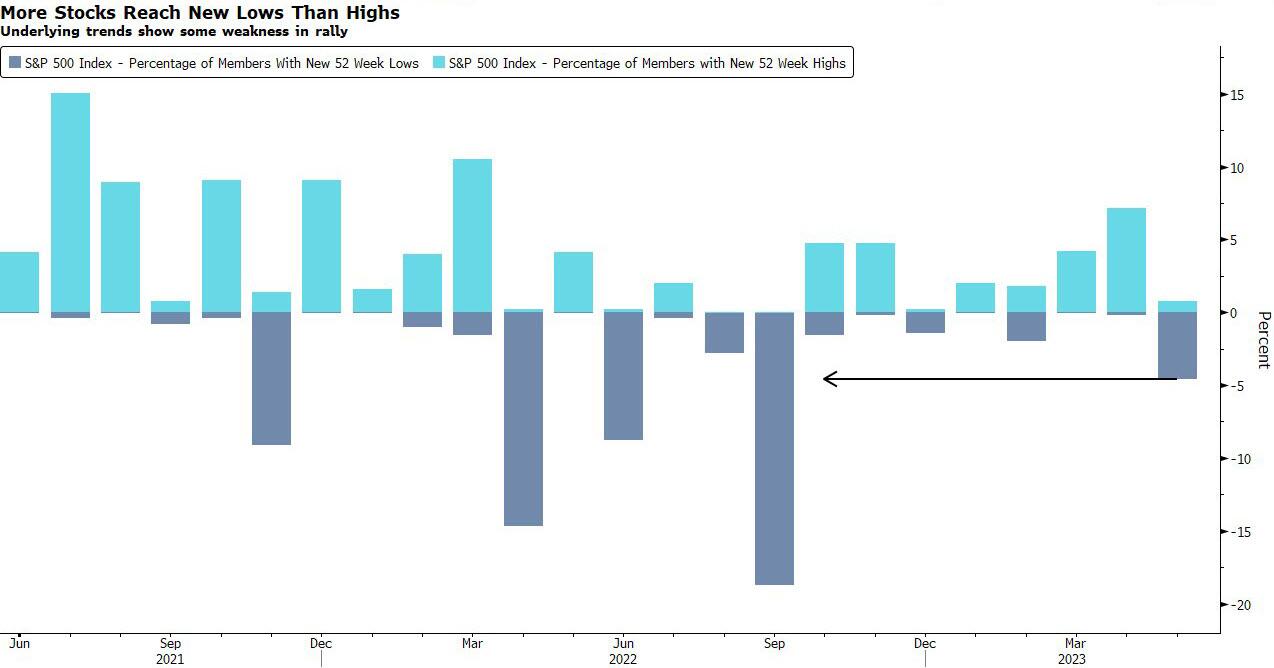

Meanwhile, frustration among bears has rarely been greater with more stocks making new 52-week lows in the S&P 500 than 52-week highs in May. “Breadth is awful,” Athey said, referring to the limited number of stocks contributing to the rally. “There’s very narrow leadership. It doesn’t look too healthy to me.”

In Europe, the Stoxx 50 is little changed while FTSE 100 outperforms peers, adding 0.6%, FTSE MIB lags, dropping 0.3%. Consumer products, tech and travel are the worst-performing sectors. The region continues to lose momentum from being the proxy for China’s reopening boom; do investors buy the dip with China looking to add stimulus? PMIs continue to slow and are at 3-month lows. Value is leading, Momentum is lagging; Defensives over Cyclicals. UKX +0.5%, SX5E -0.0%, SXXP +0.1%, DAX +0.0%. Here are some of the most notable European moves:

- Energy stocks were among the strongest gainers in Europe Monday as crude advanced following Saudi Arabia’s pledge to make an extra 1 million barrel-a-day supply cut in July, taking its production to the lowest level for several years. Shell rises as much as 1.6%.

- Shares of European telecom operators rise across the board, rebounding from a selloff on Friday when Bloomberg News reported that Amazon is planning to provide low-cost mobile phone service to Prime members in the US. Deutsche Telekom and Vodafone gain respectively as much as 3.5% and 3.4%.

- UBS shares gain 1.3% on Monday after the banking giant announced it expects to complete its acquisition of Credit Suisse as early as June 12. ZKB sees this as a positive development, initiating what it sees as a “protracted integration process.” Credit Suisse rises as much as 2.3%.

- Asos shares jump as much as 14%, the most since Jan. 12, after the Sunday Times reported that the online fast fashion retailer received a takeover approach from Turkish online retailer Trendyol in December.

- Indivior shares surge as much as 13%, to highest in 15 weeks, after the drugmaker announces it has reached an agreement to resolve antitrust claims brought by the Attorneys General of 41 states and the District of Columbia.

- Red flags that pricey luxury shares have hit a peak are piling up as conviction on the China reopening trade takes a hit. LVMH shares fall as much as 1.2%

- Viaplay shares fall as much as 59% to a record low after the Nordic media firm slashed its 2023 guidance, scrapped 2025 targets and said CEO Anders Jensen stepped down with immediate effect.

- Bollore shares fall as much as 3.7%, after Kepler Cheuvreux cut its recommendation on the French conglomerate to hold from buy, noting the stock’s recent outperformance and the simplified offer.

Earlier in the session, Asian stocks were mostly positive amid momentum from Friday’s post-NFP gains on Wall Street and as participants digested stronger Chinese Caixin Services and Composite PMI data.

- Hang Seng and Shanghai Comp. were kept afloat following the encouraging Caixin PMIs but with gains capped amid US-China frictions and after China’s Cabinet noted that the foundation for the economic recovery is not solid, while property names were also pressured despite reports that China is mulling a support package for the property sector and bolster the economy.

- Australia’s ASX 200 was led higher by gains across nearly all sectors with early tailwinds in energy names following Saudi Arabia’s additional 1mln bpd output cut, while the RBA is seen to keep rates unchanged at tomorrow’s meeting.

- The Nikkei 225 climbed above 32,000 for the first time since 1990 with exporters propelled by a weaker currency.

- Key stock gauges in India ended with gains mirroring a board-based rally across Asian markets on Monday as investors assess prospects of a pause in rate hikes by the Federal Reserve and easing concerns over a US recession. The S&P BSE Sensex rose 0.4% to 62,787.47 in Mumbai just shy of its all-time closing high levels, while the NSE Nifty 50 Index advanced 0.3% to 18,593.85. Strong automobile sales data triggered buying in auto stocks in India with the Nifty Auto index climbing 1.3%, its best day since May 8.

In FX, the Bloomberg Dollar Spot Index gained as much as 0.3%, taking gains into a second day, after last week’s jobs data added to the market’s view that the Fed will raise rates by 25 basis points next month. CAD and EUR are the strongest performers in G-10 FX, with the Canadian currency receiving some support as oil prices advance; SEK and GBP underperforms. BRL (1.1%), COP (1.1%) lead gains in EMFX, TRY (-1.1%) lags.

In rates, Treasuries were cheaper across the curve, following bigger losses in core European rates with S&P 500 futures steady near Friday’s highs. The two-year Treasury yield rises 4 basis points to 4.54%, rising toward a 2-1/2-month high of 4.64% touched just over a week ago. Yields higher by 4bp-6bp on the day with 2s5s30s fly wider by 2bp as belly underperforms; 10-year yields around 3.74% with bunds and gilts cheaper by 2bp and 1.5bp in the sector. Traders are pricing in a near 90% possibility that the Fed will hike rates to 5.5% in July; they see just the prospects of a June rise at around 30%. Elsewhere, gilts bear-flatten, Bunds bear-steepen. Peripheral spreads are mixed to Germany; Italy widens, Spain widens and Portugal tightens.

In commodities, Crude oil futures remain higher by about 2% after a 4.6% advance sparked by Saudi Arabia’s output-cut pledge at weekend’s OPEC+ meeting. Spot gold falls roughly $6 to trade near $1,942/oz.

US session includes factory orders data and ISM services gauge and Durable Goods/Cap Goods, while Fed speakers are in quiet period ahead of June 13-14 FOMC meeting.

Market Snapshot

- S&P 500 futures little changed at 4,289.00

- MXAP up 0.6% to 163.41

- MXAPJ up 0.2% to 514.82

- Nikkei up 2.2% to 32,217.43

- Topix up 1.7% to 2,219.79

- Hang Seng Index up 0.8% to 19,108.50

- Shanghai Composite little changed at 3,232.44

- Sensex up 0.5% to 62,885.07

- Australia S&P/ASX 200 up 1.0% to 7,216.27

- Kospi up 0.5% to 2,615.41

- STOXX Europe 600 up 0.1% to 462.66

- German 10Y yield little changed at 2.36%

- Euro down 0.2% to $1.0689

- Brent Futures up 2.5% to $78.06/bbl

- Gold spot down 0.3% to $1,941.52

- U.S. Dollar Index up 0.24% to 104.26

Top Overnight News

- 1) Inflation is pushing Japan into a new era that could lift equities by spurring more households to move savings out of low-yielding bank deposits, the head of the country’s stock exchange operator has said. Hiromi Yamaji, president of the JPX group that controls the Tokyo and Osaka exchanges, said he expected many Japanese to stop sitting on so much cash — the country’s households have amassed ¥1 quadrillion ($7tn) in bank savings — and look to stock markets for better returns in response to rising living costs. FT

- 2) China’s defense minister attacked the US policy in the Pacific, accusing the Pentagon of stoking confrontation (and a Chinese navy ship sailed within 140 meters of a US Navy guided missile destroyer). Worth noting China will soon account for less than 50% of US imports from low-cost countries in Asia as Western firms shift supply chains out of the mainland. London Telegraph / FT

- 3) China’s Caixin services PMI for May was strong, coming in at 57.1 (up from 56.4 in April and ahead of the Street’s 55.2 forecast). Also, Indonesia’s CPI for May undershot the Street, coming in at +2.66% (down from 2.83% in April and below the Street’s 2.81% forecast). RTRS

- 4) Ukrainian President Volodymyr Zelensky said he was now ready to launch a long-awaited counteroffensive but tempered a forecast of success with a warning: It could take some time and come at a heavy cost. “We strongly believe that we will succeed,” Zelensky said in an interview in this southern port city as his country’s military girded for what could be one of the war’s most consequential phases as it aims to retake territory occupied by Russia. WSJ

- 5) Banks in the US could see their capital requirements jump as much as 20% under new rules being formulated at the Fed (the rules would apply to institutions with assets >$100B, and fee-based activities, such as wealth mgmt. or interchange revenue, will be punished under the new framework). Also, Banks in the US are preparing to sell commercial property loans at a discount even when borrowers are current on their payments as firms rush to reduce their exposure to this segment of the market. WSJ / FT

- 6) With a debt ceiling deal freshly signed into law Saturday by President Joe Biden, the US Treasury is about to unleash a tsunami of new bonds to quickly refill its coffers. This will be yet another drain on dwindling liquidity as bank deposits are raided to pay for it — and Wall Street is warning that markets aren’t ready. BBG

- 7) Yesterday’s OPEC+ meeting was moderately bullish, on net, with three main developments. First, Saudi Arabia pledged to deliver an additional 1mb/d unilateral “extendible” output cut in July (bullish). Second, the voluntary cuts from the 9 OPEC+ countries are scheduled to extend until December 2024, from December 2023 previously (somewhat bullish). Third, output baselines will be redistributed in 2024 from countries struggling to reach their targets to those with ample spare capacity (somewhat bearish output effect, but bullish cohesion). GIR

- 8) Hedge funds accelerated selling in US Energy amid price declines last week. Last week’s notional net selling in US Energy was the largest in 10 weeks and ranks in the 97th percentile vs. the past five years. Info Tech was the most notionally net bought global sector on the Prime book for the 4th straight week. Last week’s net buying in Info Tech was the largest in 5+ months and ranks in the 92nd percentile vs. the past five years. GS PB

- 9) AMZN wireless story met with skepticism as firms deny involvement (Amazon, T-Mobile, and Verizon all said nothing is in the works) and analysts suggest economics/logistics don’t make sense. Barron’s

- 10) More bank insiders are buying shares in their own companies, a vote of confidence in the industry after a crisis sparked by the collapse of four regional lenders earlier this year. The number of buyers has already jumped to 778 in the second quarter through May 26 from 524 in the first three months of the year, according to research firm VerityData, which said the surge is being driven by small and midsize banks. More purchasers stepped up even as share prices sank to multiyear lows in early May. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive amid momentum from Friday’s post-NFP gains on Wall Street and as participants digested stronger Chinese Caixin Services and Composite PMI data. ASX 200 was led higher by gains across nearly all sectors with early tailwinds in energy names following Saudi Arabia’s additional 1mln bpd output cut, while the RBA is seen to keep rates unchanged at tomorrow’s meeting. Nikkei 225 climbed above 32,000 for the first time since 1990 with exporters propelled by a weaker currency. Hang Seng and Shanghai Comp. were kept afloat following the encouraging Caixin PMIs but with gains capped amid US-China frictions and after China’s Cabinet noted that the foundation for the economic recovery is not solid, while property names were also pressured despite reports that China is mulling a support package for the property sector and bolster the economy.

Top Asian News

- on Friday, while the meeting was said to be candid, constructive and part of ongoing efforts to maintain open lines of communication, according to the Treasury.

- China is soon to account for less than half of US low-cost imports from Asia in 2023 for the first time in over a decade, according to an annual reshoring index from Kearney cited by the FT.

- Wuhan Commerce Bureau said initial talks have started with Disney (DIS) for the US firm to start a project in the city, according to Reuters.

European equities trade flat with not much in the way of weekend newsflow to guide prices following Friday’s solid session for the region, whilst the FTSE 100 narrowly outperforms. Equity sectors are a mixed bag with Telecoms top of the leaderboard, followed closely by Energy and Real Estate, while Tech, Travel & Leisure, and Consumer Products & Services reside at the bottom. US equity futures are flat following Friday’s session of gains (ES -0.1%, NQ -0.2%, RTY +0.1%)

Top European News

- BoE is looking to broaden reform of the deposit guarantee scheme after the collapse of SVB’s UK arm highlighted the weakness of the current regime, according to FT.

- ECB’s Vujcic said Eurozone inflation risks are tilted to the upside; wage pressures are “still very lively”, according to Bloomberg.

- Fitch affirmed the Bank of England at AA-; Outlook Negative.

- S&P said France’s “AA/A-1+” ratings affirmed; outlook remains negative; says tighter financial conditions and still-high core inflation will restrain France’s economic activity in 2023 and 2024

FX

- DXY maintains a bullish momentum above 104.00 in the wake of Friday’s strong US payrolls gain which resulted in a hawkish tilt in Fed pricing.

- USD/JPY rebounds sharply towards 140.50 from just shy of 140.00 overnight amidst higher Treasury yields and wider spreads to JGBs after slowdowns in Japan’s services and composite PMIs.

- Euro extends declines against its US counterparts and against the backdrop of mostly sub-prelim or expected Eurozone services and composite PMIs.

- Aussie straddles 0.6600 on the eve of the RBA that could be a very close call.

- Yuan weakens irrespective of a firmer than forecast Chinese Caixin services PMI that boosted the composite number along with the manufacturing PMI, as China-US/Canadian/NATO tensions overshadowed the encouraging surveys.

- PBoC set USD/CNY mid-point at 7.0904 vs exp. 7.0918 (prev. 7.0939)

Fixed Income

- Bunds are off worst levels having pared some losses from 134.81 amidst more mixed Eurozone macro releases including soft PMIs, PPI, Sentix readings vs a healthier-than-expected German trade balance.

- Gilts have slipped to a new intraday base, albeit marginal at 96.25 in recent trade and probably in recognition of minor upward revisions to the final services and composite PMIs

- US Treasuries remain underwater, but the curve is a bit more stable after post-NFP flattening in advance of the final PMIs, services ISM and a speech from Fed’s Mester.

Commodities

- WTI and Brent contracts gapped higher upon the return of futures trading following the weekend OPEC+ deliberations (see below).

- Spot gold is subdued under USD 1,950/oz as the Dollar index remains firmer on the session – with the yellow metal finding support at its 100 DMA (1,939/oz) earlier.

- Base are mostly subdued but to varying degrees amid the aforementioned APAC growth concerns, although the complex has trimmed losses. Iron ore continued rising overnight.

OPEC+ Meeting

- Saudi Arabia announced it is to cut an additional 1mln bpd of oil output for July in which its output will drop to 9mln bpd and all other OPEC+ producers agreed to extend earlier cuts through to the end of 2024. OPEC+ agreed to a new output target of 40.4mln bpd from 2024 with the output target for 2024 lowered by 1.4mln bpd and said Russia, Angola and Nigeria are to see significant production cuts in 2024, while the next OPEC+ meeting is to take place on November 26th, according to Reuters.

- Saudi’s Energy Minister said they are not targeting prices and that the extra voluntary cut is a precautionary measure, while they will keep the markets in suspense on whether the additional voluntary cut for July will be extended and will review the extra voluntary cuts every month.

- Saudi’s Energy Minister said Russia is delivering on its oil output commitments, while the UAE’s Energy Minister said there are some discrepancies in Russian production numbers and they don’t want politics involved in how they look at Russian production numbers, according to Reuters.

- Russian Deputy PM Novak said OPEC+ agrees total oil output cuts of 3.66mln bpd and that the oil market is more or less balanced, while he added they are seeing oil demand rising and they have the possibility of tweaking decisions. Furthermore, he said they will take decisions so that the oil market is stable and that Russia is fulfilling its obligations in full, according to Reuters.

- White House officials said they will continue to work with all fuel producers to ensure energy markets support US economic growth, according to Reuters.

Tyler Durden

Mon, 06/05/2023 – 08:19

via ZeroHedge News https://ift.tt/kqcmsT5 Tyler Durden