Key Events This Jobs Week: JOLTS, ADP And Payrolls

After a week that tracked global PMIs and sliding inflation, and ushered in the Fed’s quiet period with a “fireside chat” bang, this week all roads point to payrolls on Friday with the usual build up via JOLTS (tomorrow) and ADP (Wednesday). Elsewhere in the US, DB’s Jim Reid notes that the Services ISM is out tomorrow (we will also watch the employment sub component ahead of payrolls), and the initial read on inflation expectations in the University of Michigan confidence sentiment release (Friday) will be of note after 5-10yr expectations ticked up to a decade high of 3.2% last month. As a reminder, the Fed are now on a blackout period ahead of next week’s FOMC so some of the big catalyst for moves of late, i.e. Fed speakers, won’t be there.

Around the globe, other highlights include a few important releases in Germany including the trade balance (today), factory orders (Wednesday) and industrial production (Thursday). Industrial production indicators are also due in France and Italy. Retail sales data is out for the Eurozone on Wednesday. In China, the Caixin services PMI (tomorrow) and trade balance figures (Thursday) are the highlights. Tokyo CPI is out just before midnight tonight

From central banks, Lagarde and Guindos speak today with the RBA (tomorrow) and Bank of Canada (Wednesday) expected to hold rates by the consensus although our economist is an outlier and predicts a hike in Australia . For the full week ahead the day-by-day calendar is at the end as usual.

Digging a bit deeper into the US employment picture, DB’s US economists expect headline and private payrolls to come in at +130k with consensus at +180k and +160k respectively. The returning post-strike autoworkers will boost the data by around +30k. Unemployment is expected to hold steady at 3.9% according to consensus, although DB economists see the risks tilted to a 3.8% print. One thing economists look carefully at is the diffusion index that shows the breadth of job gains. It’s currently at 52%, its lowest rate since the pandemic. They show that 70% of the private job gains in the last year come from only two sectors, namely leisure and hospitality and private education and healthcare. Outside of that job creation in the last 12 months is a very lowly 0.7% and just 0.2% over the last 6.

Staying with US labour markets, the JOLTS data tomorrow is also important even if it’s October data. While the hiring and quits rates were at or below their 2019 averages in September, the layoffs and discharges rate remained near historical lows. So that gap is keeping labor markets tight for now. DB’s base case is that the demand for labor eases in the next few months.

Finally, thanks to way too many public companies, Q3 earnings season is still going on – with just a month left until Q4 earnings season begins – thanks to the following stragglers.

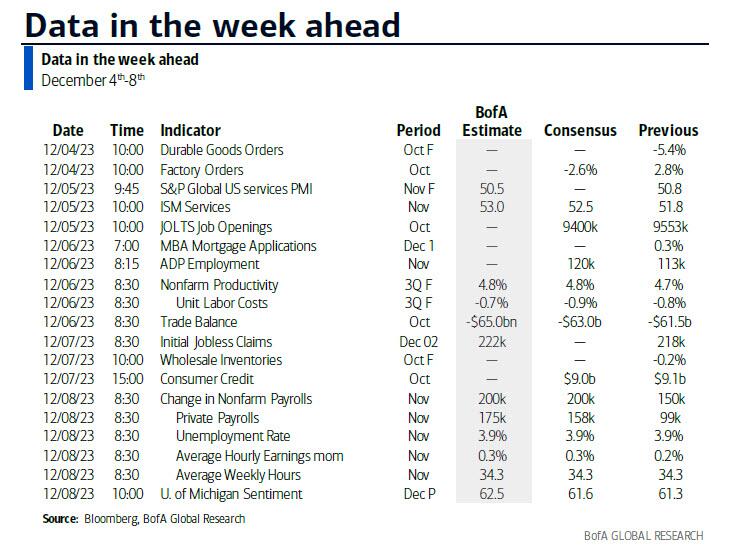

Courtesy of DB, here is a day-by-day calendar of events

Monday December 4

- Data: US October factory orders, Japan November Tokyo CPI, Germany October trade balance

- Central banks: ECB’s Lagarde and Guindos speak

Tuesday December 5

- Data: US October JOLTS report, November ISM services, China November Caixin services PMI, UK November official reserves changes, new car registrations, Italy November services PMI, France October industrial production, Eurozone October PPI, Canada November services PMI

- Central banks: ECB consumer expectations survey, RBA decision

Wednesday December 6

- Data: US November ADP report, October trade balance, UK November construction PMI, Germany October factory orders, November construction PMI, Eurozone October retail sales, Canada Q3 labor productivity, October international merchandise trade

- Central banks: BoC decision, BoE financial stability report

Thursday December 7

- Data: US Q3 household change in net worth, October wholesale trade sales, consumer credit, initial jobless claims, China November trade balance, foreign reserves, Japan October trade balance, current account balance, leading index, labor cash earnings, household spending, coincident index, November bank lending, Italy October retail sales, industrial production, Germany October industrial production, France October trade balance, current account balance, Canada October building permits Central banks: ECB’s Holzmann and Elderson speak

- Earnings: Broadcom, Lululemon, Dollar General

- Other: EU-China summit, through December 8

Friday December 8

- Data: US November jobs report, December University of Michigan survey, Japan November Economy Watchers survey, Canada Q3 capacity utilization rate

- Central banks: BoE / Ipsos inflation attitudes survey

* * *

Finally, turning to just the US, Goldman writes that the key economic data release this week is the payrolls report on Friday. There are no speaking engagements from Fed officials this week, reflecting the FOMC blackout period.

Monday, December 4

- 10:00 AM Factory orders, October (GS -2.7%, consensus -3.0%, last +2.8%); Durable goods orders, October final (consensus -5.4%, last -5.4%); Durable goods orders ex-transportation, October final (last flat); Core capital goods orders, October final (last -0.1%); Core capital goods shipments, October final (last flat): We estimate that factory orders declined by 2.7% in October following a 2.8% increase in September. Durable goods orders decreased by 5.4% in the October advance report, and core capital goods orders decreased by 0.1%.

Tuesday, December 5

- 09:45 AM S&P Global US services PMI, November final (consensus 50.8, last 50.8)

- 10:00 AM JOLTS job openings, October (GS 9,300k, consensus 9,300k, last 9,553k)

- 10:00 AM ISM services index, November (GS 52.1, consensus 52.3, last 51.8): We estimate that the ISM services index rebounded 0.3pt to 52.1 in November. Our GSAI and our nonmanufacturing tracker increased in November (+1.8pt to 52.3) but we expect a drag from residual seasonality.

Wednesday, December 6

- 08:15 AM ADP employment change, November (GS +150k, consensus +120k, last +113k): We estimate a 150k rise in ADP payroll employment in November, reflecting generally stronger Big Data employment indicators.

- 08:30 AM Nonfarm productivity, Q3 final (GS +4.9%, consensus +4.9%, last 4.7%); Unit labor costs, Q3 final (GS -0.8%, consensus -0.9%, last -0.8%): We expect a 0.2pp upward revision to nonfarm productivity growth to +4.9% (qoq ar) in the final Q3 reading. We expect no revision on net to unit labor costs—compensation per hour divided by output per hour—previously reported at -0.8%.

- 08:30 AM Trade balance, October (GS -$65.4bn, consensus -$64.2bn, last -$61.5bn)

Thursday, December 7

- 08:30 AM Initial jobless claims, week ended December 2 (GS 220k, consensus 222k, last 218k); Continuing jobless claims, week ended November 25 (GS 1,930k, consensus 1,910k, last 1,927k): We estimate that initial jobless claims were roughly unchanged at 220k. We estimate that continuing claims edged up to 1,930k, reflecting continued upward pressure from seasonal distortions. We would note that this week’s period for continuing claims coincides with Thanksgiving, which could contribute to additional volatility.

- 08:30 AM Wholesale inventories, October final (consensus -0.2%, last -0.2%)

Friday, December 8

- 08:30 AM Nonfarm payroll employment, November (GS +238k, consensus +180k, last +150k); Private payroll employment, November (GS +198k, consensus +160k, last +99k); Average hourly earnings (mom), November (GS +0.25%, consensus +0.3%, last +0.2%); Average hourly earnings (yoy), November (GS +3.92%, consensus +4.0%, last +4.1%); Unemployment rate, November (GS 3.8%, consensus 3.9%, last 3.9%); Labor force participation rate, November (GS 62.7%, consensus 62.7%, last 62.7%): We estimate nonfarm payrolls rose by 238k in November (mom sa), reflecting a 200k underlying gain plus a 38k boost from the return of striking workers. Big Data employment indicators were generally strong in the month, and while initial jobless claims rebounded, they remain at levels consistent with a low pace of layoff activity. We estimate that the unemployment rate declined one tenth to 3.8%, reflecting a rebound in household employment following its sharp drop in October. We assume labor force participation was unchanged at 62.7%. We estimate a 0.25% increase in average hourly earnings (mom sa) that lowers the year-on-year rate by two tenths to 3.9%, reflecting waning wage pressures and neutral calendar effects.

- 10:00 AM University of Michigan consumer sentiment, December preliminary (GS 62.0, consensus 62.0, last 61.3); University of Michigan 5-10-year inflation expectations, December preliminary (GS 3.0%, consensus 3.0%, last 3.2%): We estimate the University of Michigan consumer sentiment index increased to 62.0 in December. We estimate the report’s measure of long-term inflation expectations declined two tenths to 3.0%, reflecting the further decline in gasoline prices and a sequential reduction in public focus on the Israel-Hamas conflict.

Source: DB, Goldman, BofA

Tyler Durden

Mon, 12/04/2023 – 09:37

via ZeroHedge News https://ift.tt/T1lq9db Tyler Durden