Apollo: 10 Reasons Why The Fed Won’t Cut Rates In 2024

Two weeks ago, with inflation reversing higher, oil surging, home price gains just unstoppable, oh and of course stonks trading at all time high thanks to a new tech bubble which has pushed bitcoin back to record highs, we asked if the Fed’s next move won’t be a rate hike (even if that means that more banks will blow up, forcing the Fed to both hike and QE at the same time, in keeping with the Reverse Twist idea just floated by Waller this morning).

Fast forward to today when Apollo’s chief economist and resident permabear Torsten Slok (who won’t rest until you have sold all your assets to private equity giant Apollo which will be very happy to buy everything yo uhave to sell), published ten reasons why the Fed won’t cut at all in 2024 (and thus, why a hike is much more likely).

We excerpt from his note below:

The market came into 2023 expecting a recession. The market went into 2024 expecting six Fed cuts.

The reality is that the US economy is simply not slowing down, and the Fed pivot has provided a strong tailwind to growth since December.

As a result, the Fed will not cut rates this year, and rates are going to stay higher for longer.

How do we come to this conclusion?

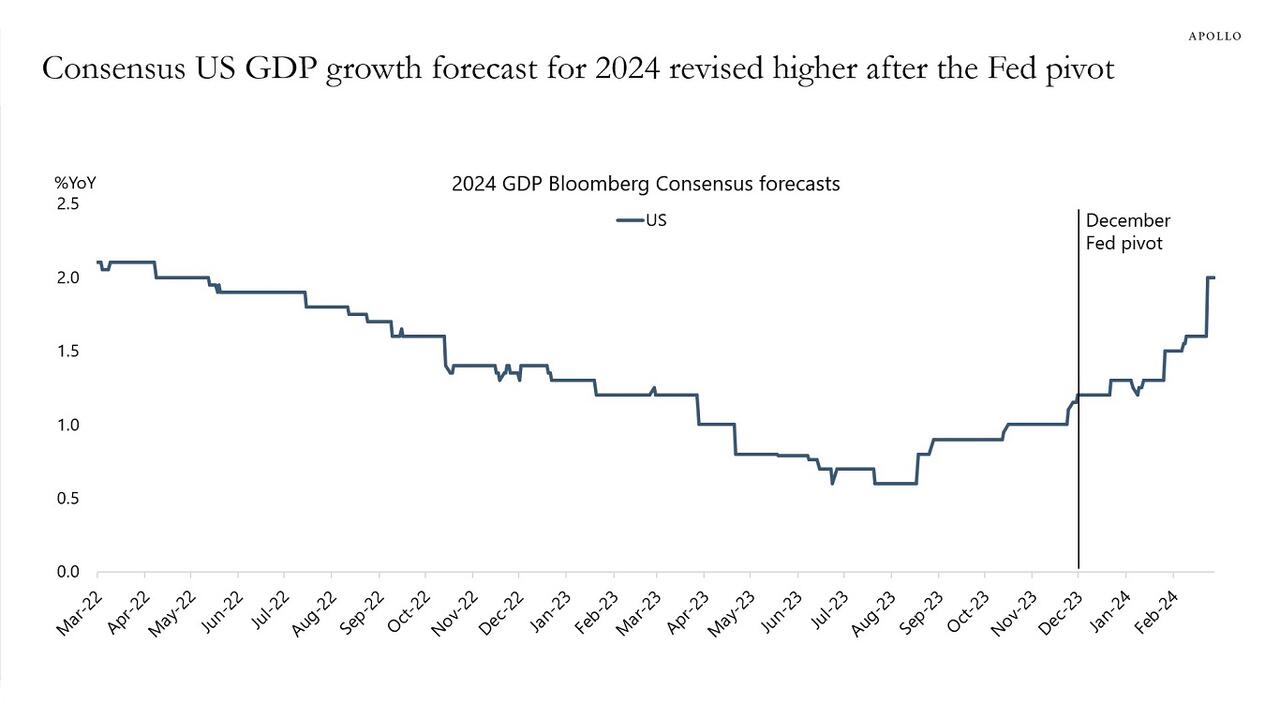

1) The economy is not slowing down, it is reaccelerating. Growth expectations for 2024 saw a big jump following the Fed pivot in December and the associated easing in financial conditions. Growth expectations for the US continue to be revised higher.

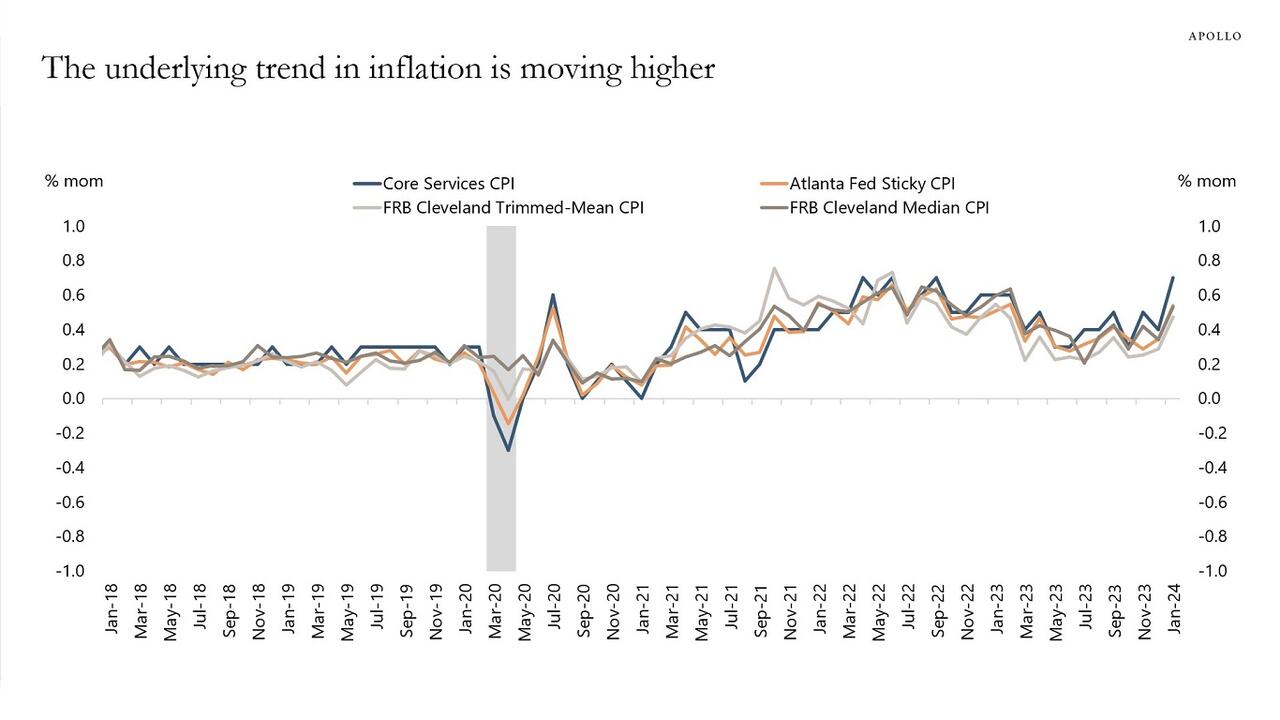

2) Underlying measures of trend inflation are moving higher.

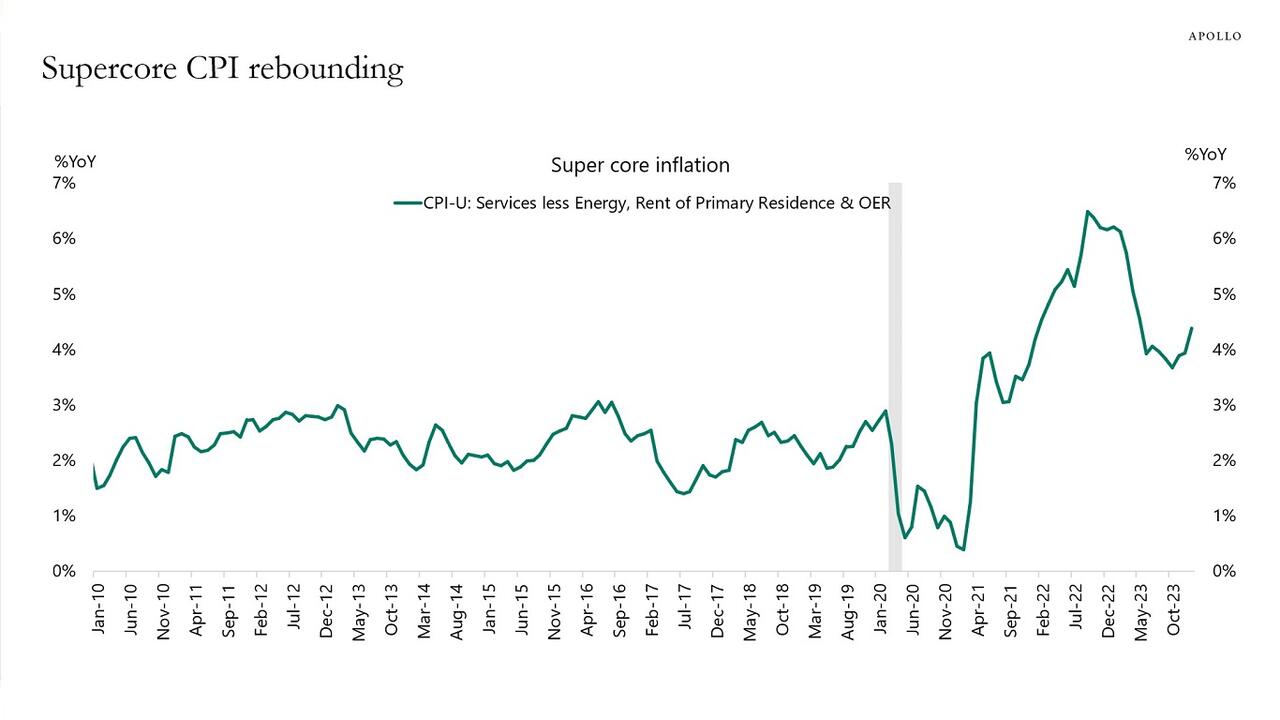

3) Supercore inflation, a measure of inflation preferred by Fed Chair Powell, is trending higher.

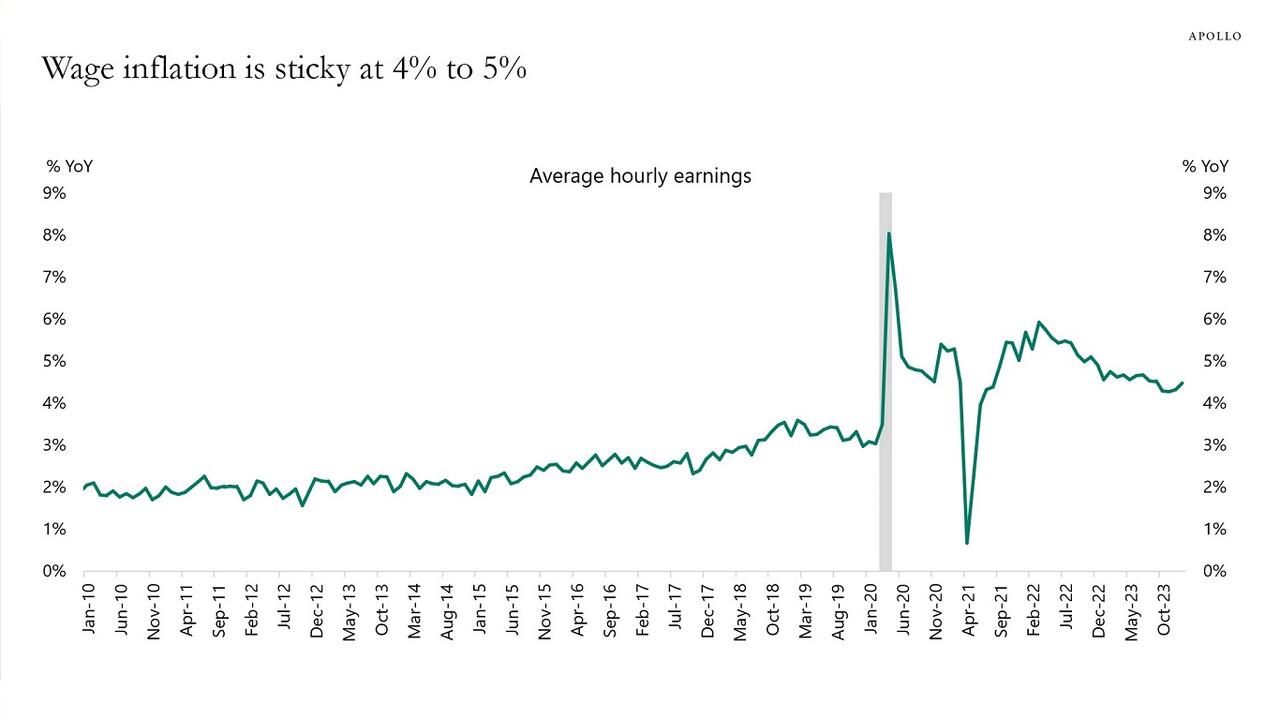

4) Following the Fed pivot in December, the labor market remains tight, jobless claims are very low, and wage inflation is sticky between 4% and 5%.

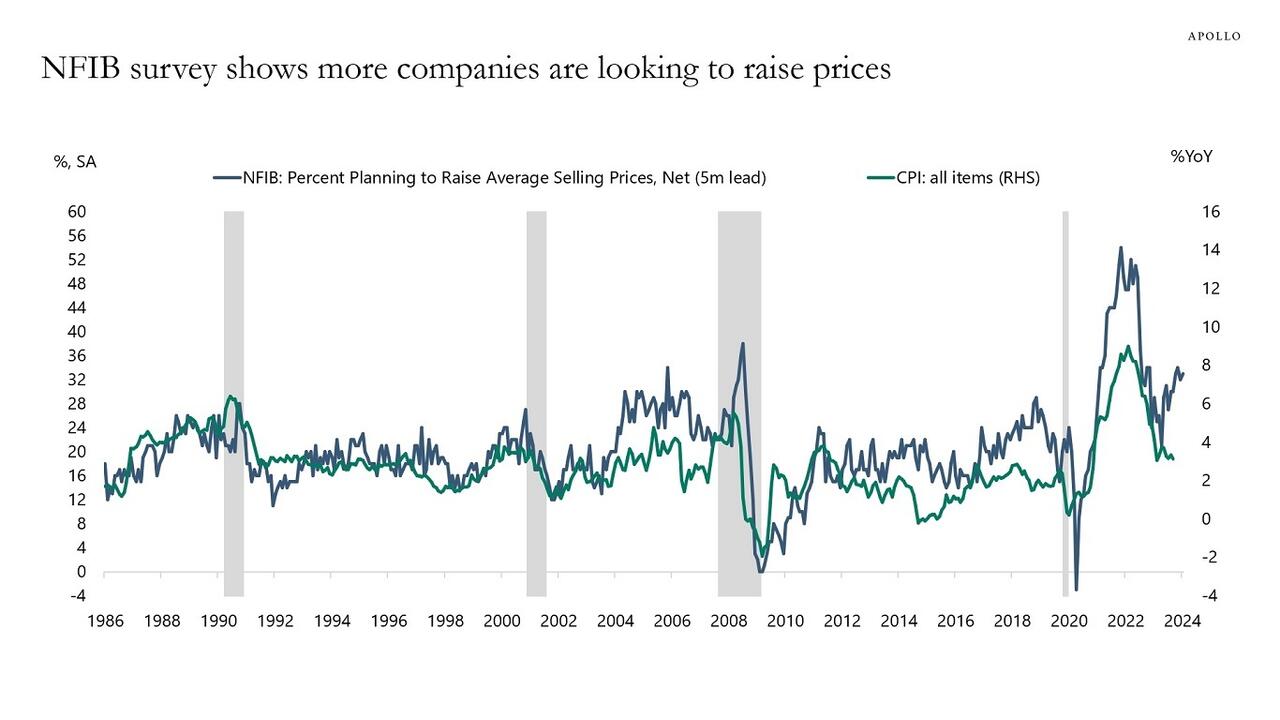

5) Surveys of small businesses show that more small businesses are planning to raise selling prices.

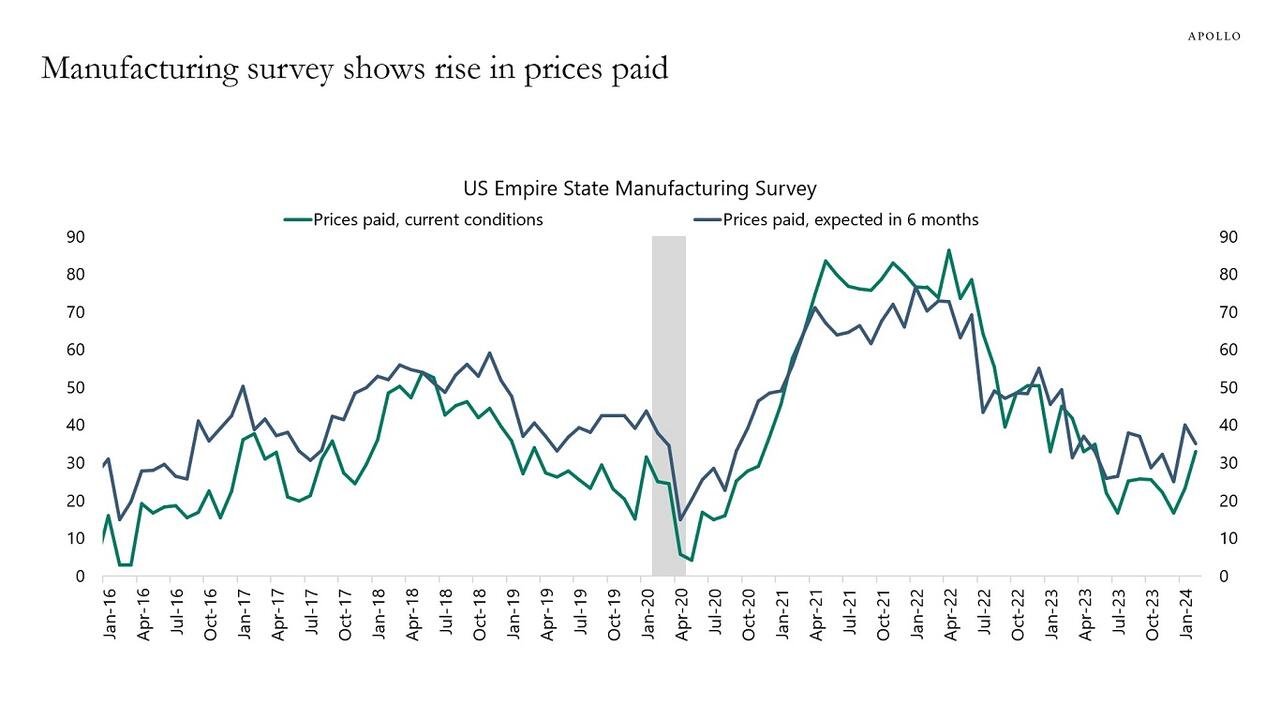

6) Manufacturing surveys show a higher trend in prices paid, another leading indicator of inflation.

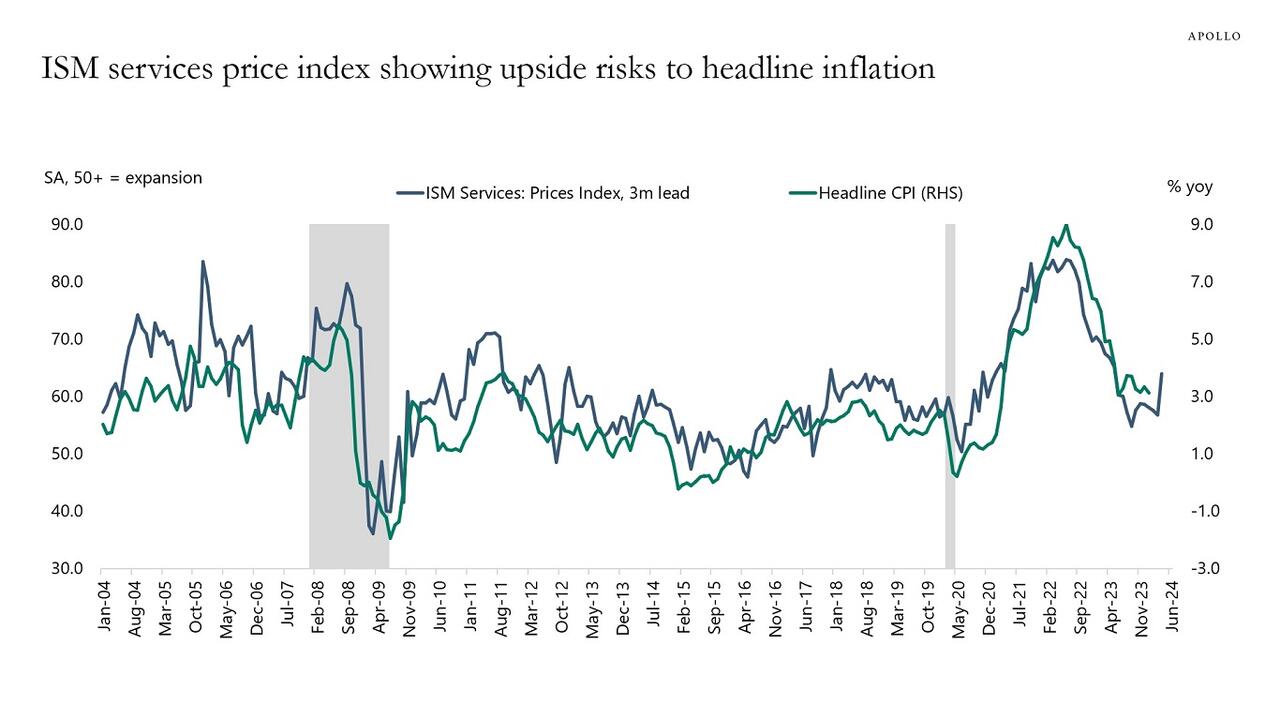

7) ISM services prices paid is also trending higher.

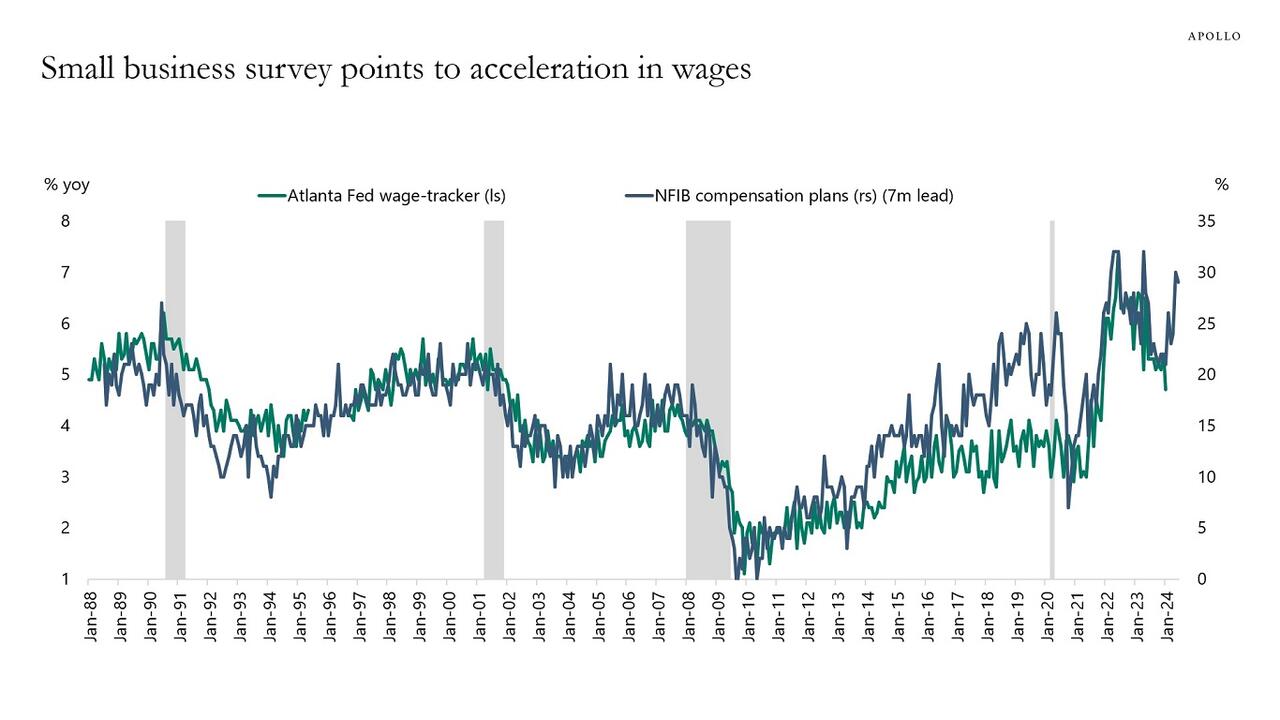

8) Surveys of small businesses show that more small businesses are planning to raise worker compensation.

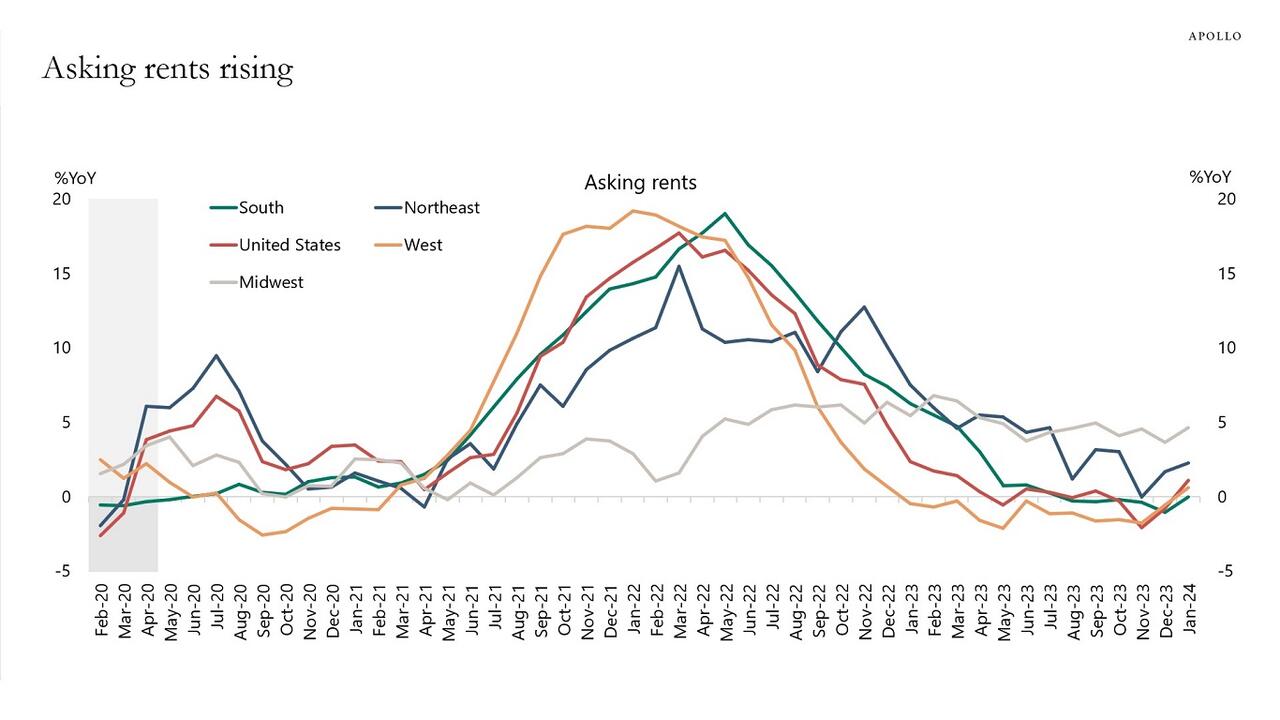

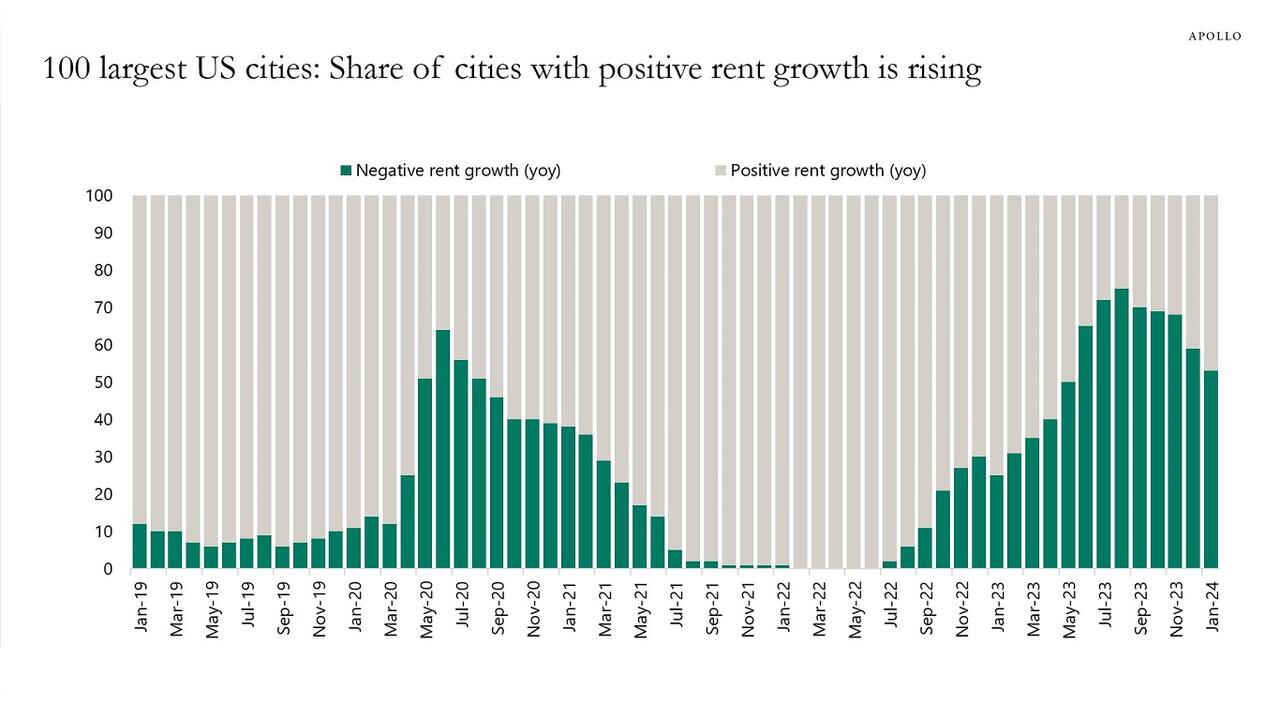

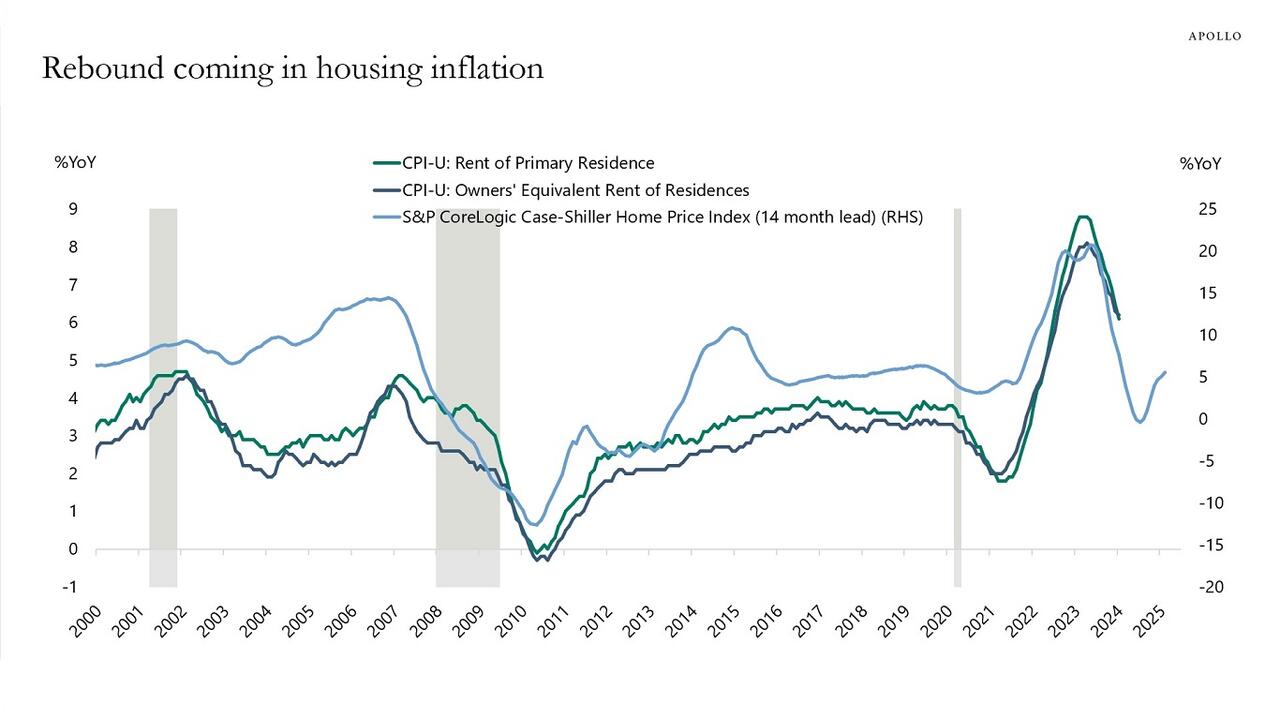

9) Asking rents are rising, and more cities are seeing rising rents, and home prices are rising, see the ninth, tenth, and eleventh charts.

10) Financial conditions continue to ease following the Fed pivot in December with record-high IG issuance, high HY issuance, IPO activity rising, M&A activity rising, and tight credit spreads and the stock market reaching new all-time highs. With financial conditions easing significantly, it is not surprising that we saw strong nonfarm payrolls and inflation in January, and we should expect the strength to continue.

As Slok concludes, “the bottom line is that the Fed will spend most of 2024 fighting inflation. As a result, yield levels in fixed income will stay high.”

Tyler Durden

Fri, 03/01/2024 – 13:45

via ZeroHedge News https://ift.tt/6nOU42p Tyler Durden