Yields Tumble, Set For Bigger Plunge If CPI Comes In Cool

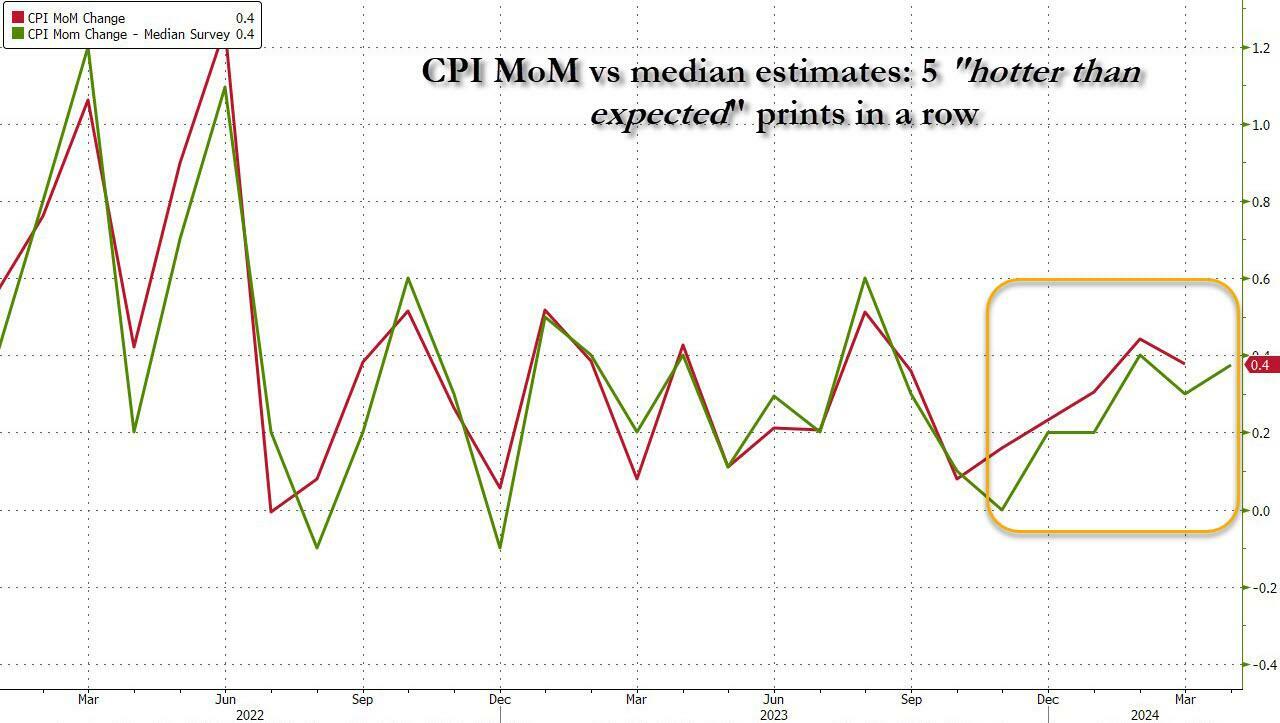

Perhaps taking a cue from our CPI commentary last week in which we explained why today’s inflation print will likely come in on the dovish side after beating estimates for 5 months in a row…

… moments ago 10Y yields plumbed fresh multi-week lows, sliding to just above 4.40% (from a high of 4.65% two weeks ago), ironically the lowest lowest since the last CPI release five weeks ago….

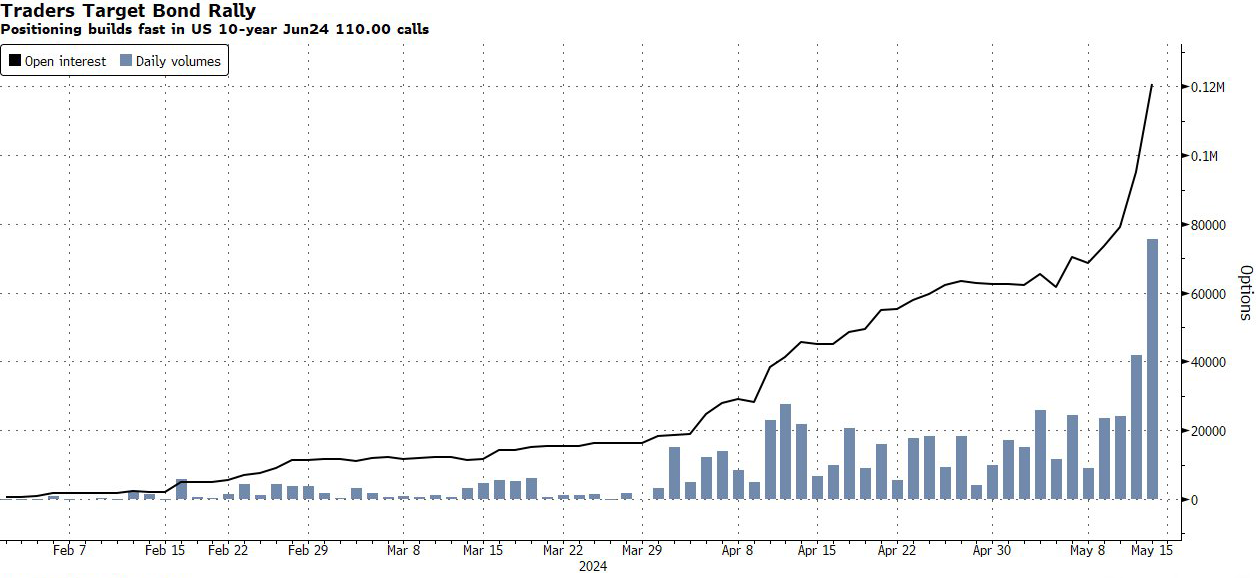

… as traders of Treasury options are positioning for a sharp bond rally in the aftermath of crucial inflation data on Wednesday, according to Bloomberg’s Ed Bolingbroke (European bonds posted even stronger gains, with benchmark German and UK rates both falling as much as seven basis points).

According to the Bloomberg strategist, heavy option buying over the past week has centered on options that would stand to benefit from US 10-year yields dropping to roughly 4.3%, the lowest in more than a month. One high-risk trade stood out: it stood to make $15 million windfall by risking just $150,000 should the 10-year benchmark fall even further to 4.25% by May 24.

Open interest, or the amount of new positioning, surged recently in options tied to the so-called 110.00 call strike, which pairs with a roughly 4.3% 10-year yield level, according to CME data. Buying was concentrated in the June tenor expiring May 24, capturing this week’s big economic news including the reports on producer and consumer prices.

“There’s been a lot of positioning both ways, but most recently there’s been a lot more leaning toward the possibility of easing, and conceivably the chance of aggressive easing,” said Alex Manzara, a derivatives broker at R.J. O’Brien & Associates. “The market is clearly concerned about something going bad that could lead to rapid easing.”

But it’s not just the expectation that something will break: “There seems to be an expectation that the data will cool from last month and the market does seem to be somewhat set up that way,” said Samuel Zief, head of global FX strategy at JPMorgan Chase Bank.

Indeed, a majority now agrees with our recent take: a survey conducted by 22V Research showed 49% of investors expect the market reaction to the CPI report to be “risk-on” — while only 27% said “risk-off.”

Meanwhile, asset managers continued to add to long bets in futures, adding to bullish positions for a fourth week in a row, data from the CFTC shows.

Agreeing with the general setup, Bloomberg commentator Ven Ram writes that “the recent bullish mood in Treasuries is likely to extend if today’s inflation and retail-sales data for April prove to be soft” and he points out that on Tuesday, 10-year bonds made the most of higher-than-forecast PPI numbers. With Chair Jerome Powell describing the data as “mixed,” the markets ran ahead with the idea that components from the data that feed into the Fed’s own PCE gauge weren’t all pointing northward.

To Ram, that mindset suggests that barring a shock, above-forecast inflation readings today, Treasuries will more likely extend their nascent rally, however tenuous that may be. A reading that matches the median expectation for 0.4% on month will spur the markets to move in the direction of pricing 50 basis points of interest rate cuts for the year (current pricing is about 44 basis points). Based on correlations that we have seen this year, that would suggest a 10-year yield at 4.3592%.

A double whammy of soft inflation and weak retail sales would kindle the markets’ imagination afresh, spurring traders to fully price in a first cut in September and more than 50 basis points of policy reduction by the end of the year. That would send the two-year yield toward 4.6809% in the coming days and the 10-year toward 4.30%.

His conclusion is that “whether or not the rally has endurance is a different matter, but the market’s mood seems to be decidedly one of a bullish tactical bias heading into the all-important data sets today.”

Finally, it’s not just bonds that will rip higher (in price, not yield) if CPI comes in soft: “An in-line-with-consensus US core CPI read is discounted and in the price, but that may be enough to promote relief buyers and see the index push higher,” said Perpperstone’s head of research Chris Weston.

“A core CPI read below 0.25% month-on-month and I certainly wouldn’t want to be short.”

Tyler Durden

Wed, 05/15/2024 – 08:00

via ZeroHedge News https://ift.tt/un3rxJp Tyler Durden