Key Events This Blockbuster Week: Fed, BOJ, BOE, Jobs, Jolts, QRA, And Earnings Galore

As we hit the last few days of July, we are facing a blockbuster week ahead for markets, arguably the single-most important week of the summer which sees a convergence of central bank, macroeconomic, earnings and geopolitical events all hitting at once. As DB’s Jim Reid notes, “it’s probably easier to start with what I think are the potential market moving day by day highlights before we expand deeper into the main events: Today we see the latest Treasury borrowing estimates as part of the quarterly refunding announcement (QRA). Tomorrow sees Microsoft report, US JOLTS, German/French/Italian Q2 GDP and German July CPI. Wednesday sees Meta report, both the BoJ and the Fed deciding on rates, China PMIs, French and Eurozone July CPI, and Australian Q2 CPI. Thursday sees Apple and Amazon report, various global PMIs and the US ISM, and the BoE decision. Friday sees US payrolls.”

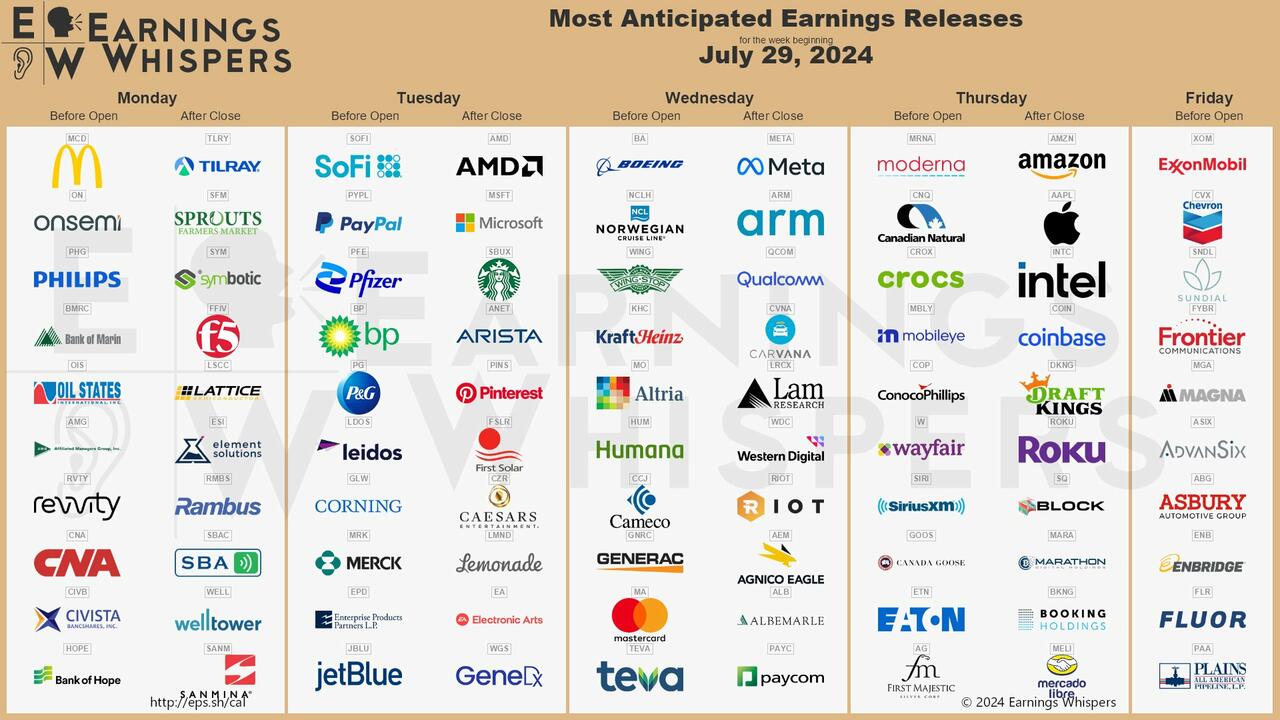

It’s hard to guess which of the above will have the largest impact on markets but it’s probably going to be the four Mag-7 tech companies that report this week. They cover around 19.7% of the S&P 500 on their own so will have a huge influence on sentiment. The Mag-7 is down -12% from its peak 2 and a half weeks ago with the Russell 2000 outperforming by around 25pp over this period which shows the extreme rotation that has been occurring over this period. So their results will be a huge driver with some nerves after Tesla and Alphabet disappointed last week.

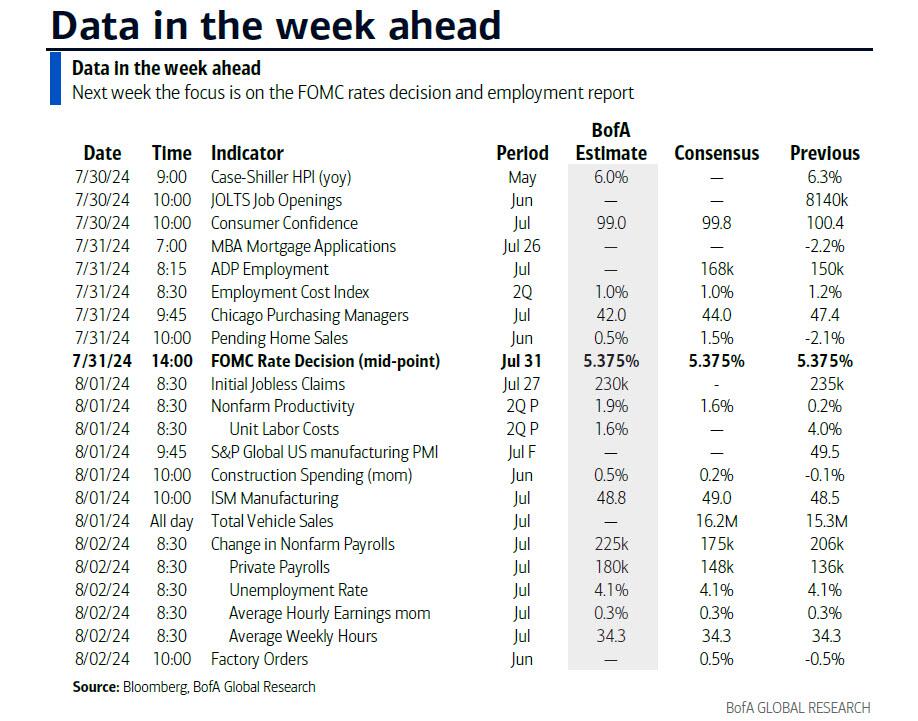

With the Fed likely to start an easing cycle soon – as the WSJ’s Nikileaks definitvely previewed over the weekend – the FOMC (Wednesday) has the potential to be a big event but the likelihood is that they will simply signal a rate cut which is a reasonable baseline for September without pre-committing. So it may not be hugely market moving. Jackson Hole (August 22-24) may see a more definitive signal from Powell. Note that no economist on the street expects a cut this week with the market pricing in a very small (4%) probability.

Earlier that day the BoJ seem more likely than not to hike rates and to reduce bond buying. Momentum towards the hike has been building over the last couple of weeks with the Yen now at 153.28 from a low of 161.69 on July 3. In another close decision our UK economists thinks the BoE will vote 5-4 to cut rates on Thursday.

With all the above it’s easy to forget Friday’s payrolls, but with some signs that the US labor market is weakening it is a very important release. DB’s economists find this tricky to forecast given storms in Texas earlier this month. They think headline (+175k vs. +206k last month) and private (+150k vs. +136k last month) payrolls will contain a roughly 15k drag from the storms. This shouldn’t impact an unchanged unemployment rate of 4.1% though. We’re not far from breaching the Sahm rule as on a 3m average basis we’re 0.43pp above the lows. However the bulls would point to a rise in the labor force rather than lay-offs being the main driver. Ex Fed President Dudley did point out last week that this also happened around the 1970s recessions though.

For European CPI, DB’s economists expect July flash data to come in at 2.59% YoY (2.52% in June) for the Eurozone, with core HICP to remain at 2.87%. Across countries, they forecast HICP in Germany at 2.5% (2.5%), France at 3.0% (2.5%), Italy at 1.1% (0.9%) and Spain at 3.4% (3.6%). More of their analysis and forecasts can be found in the latest inflation chartbook here .

As a curiosity, this week marks a year since the huge bearish surprise for bond markets from the Treasury QRA. Today’s borrowing estimates and Wednesday’s refunding statement should be much calmer affairs.

Finally, a whopping 34% of the S&P reports earnings this week, including names such as MCD, MSFT, AMD, PYPL, SBUX, PFE, BA, META, QCOM, MRNA, AMZN, INTC, COIN, XOM, CVX.

Courtesy of DB, here is a day-by-day calendar of events

Monday July 29

- Data: US July Dallas Fed manufacturing activity, UK June net consumer credit, June M4, Sweden June GDP

- Earnings: McDonald’s, Welltower, Heineken

- Auctions: US Treasury quarterly borrowing estimates

Tuesday July 30

- Data: US June JOLTS report, July Conference Board consumer confidence index, Dallas Fed services activity, May FHFA house price index, Japan June jobless rate, job-to-applicant ratio, Germany Q2 GDP, July CPI, France Q2 GDP, June consumer spending, Italy Q2 GDP , Eurozone July services confidence, industrial confidence, economic confidence, Q2 GDP

- Earnings: Microsoft, Procter & Gamble, Merck & Co, AMD, L’Oreal, Pfizer, S&P Global, Stryker, Airbus, Rio Tinto, Arista Networks, American Tower, BP, Mondelez, Starbucks, Diageo, PayPal, Electronic Arts, Pinterest, First Solar, Live Nation Entertainment, Leonardo, Davide Campari-Milano, Covestro

Wednesday July 31

- Data: US July ADP report, MNI Chicago PMI, June pending home sales, Q2 employment cost index, China July PMIs, UK July Lloyds Business Barometer, Japan June retail sales, industrial production, housing starts, July consumer confidence index, Germany July unemployment claims rate, June import price index, France July CPI, June PPI, Italy July PPI, June PPI, May industrial sales, Eurozone July CPI, Canada May GDP, Australia Q2 CPI

- Central banks: Fed’s decision, BoJ’s decision

- Earnings: Meta, Mastercard, Samsung Electronics, T-Mobile US, Qualcomm, ARM, Schneider Electric, Lam Research, Boeing, KKR, Safran, GSK, Marriott, Humana, Hess, adidas, Kraft Heinz, eBay, Carvana, Teva, Albemarle, Norwegian Cruise Line, Etsy, Telecom Italia

- Auctions: US Treasury refunding statement

Thursday August 1

- Data: US Q2 nonfarm productivity, unit labor costs, July ISM index, total vehicle sales, June construction spending, initial jobless claims, China July Caixin manufacturing PMI, Italy July manufacturing PMI, June unemployment rate, July new car registrations, budget balance, Eurozone June unemployment rate, Canada July manufacturing PMI

- Central banks: BoE’s decision, Pill speaks, decision maker panel survey, ECB’s economic bulletin

- Earnings: Apple, Amazon, Toyota Motor, Shell, Intel, ConocoPhillips, Booking, Vertex, AB InBev, Eaton, Regeneron, Cigna, Ferrari, Merck KGaA, EOG, Apollo, BMW, Volkswagen, Deutsche Post, BAE, Rolls-Royce, Moderna, DoorDash, Haleon, Hershey, Block, Blue Owl, Vonovia

Friday August 2

- Data: US July jobs report, June factory orders, Japan July monetary base, France June industrial production, budget balance, Italy June industrial production, retail sales, Switzerland July CPI

- Central banks: BoE’s Pill speaks

- Earnings: Exxon Mobil, Chevron, Linde, Ares, Engie

* * *

Finally, looking at just the US econ calendar, Goldman writes that the key economic data releases this week are the JOLTS job openings report on Tuesday, the ISM manufacturing index on Thursday, and the employment report on Friday. The July FOMC meeting is on Wednesday. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM.

Monday, July 29

- There are no major economic data releases scheduled.

Tuesday, July 30

- 09:00 AM FHFA house price index, May (consensus +0.3%, last +0.2%)

- 09:00 AM S&P Case-Shiller 20-city home price index, May (GS +0.3%, consensus +0.3%, last +0.2%)

- 10:00 AM JOLTS job openings, June (GS 7,900k, consensus 8,055k, last 8,140k): We estimate that JOLTS job openings fell by 0.2mn to 7.9mn in June, reflecting further pullback in online job postings and possible reversion in the government and manufacturing sectors after experiencing outsized increases in measured job openings in the prior month.

- 10:00 AM Conference Board consumer confidence, July (GS 100.3, consensus 99.5, last 100.4)

Wednesday, July 31

- 08:15 AM ADP employment change, July (GS +140k, consensus +149k, last +150k); We estimate ADP payroll employment growth slowed to 140k in July, partly reflecting a drag from Hurricane Beryl.

- 08:30 AM Employment cost index, Q2 (GS +1.0%, consensus +1.0%, last +1.2%); We estimate the employment cost index rose by 1.0% in Q2 (qoq sa), which would lower the year-on-year rate by one tenth to 4.1% (nsa yoy). Our forecast reflects deceleration in average hourly earnings of production and nonsupervisory workers. We also expect a slower pace of ECI growth among unionized workers—following 1.7% increases on average in Q4 and Q1 (SA by GS, not annualized)—and a moderation in ECI benefit growth after resetting higher in Q1 (0.9% vs. 1.1% in Q1).

- 09:45 AM Chicago PMI, July (GS 45.5, consensus 44.5, last 47.4)

- 10:00 AM Pending home sales, June (GS +2.6%, consensus +1.3%, last -2.1%)

- 02:00 PM FOMC statement, July 30-31 meeting: As discussed in our FOMC preview, we continue to expect the first rate cut in September as encouraging inflation news and a further rise in the unemployment rate have moved the FOMC closer to cutting. After September, we expect quarterly rate cuts for a total of two cuts in 2024 and four cuts in 2025.

Thursday, August 1

- 08:30 AM Nonfarm productivity, Q2 preliminary (GS +1.7%, consensus +1.7%, last +0.2%); Unit labor cost, Q2 preliminary (GS +1.8%, consensus +1.9%, last +4.0%)

- 08:30 AM Initial jobless claims, week ended July 27 (GS 230k, consensus 236k, last 235k); Continuing jobless claims, week ended July 20 (consensus 1,855k, last 1,851k)

- 09:45 AM S&P Global US manufacturing PMI, July final (last 49.5)

- 10:00 AM Construction spending, June (GS +0.1%, consensus +0.2%, last -0.1%)

- 10:00 AM ISM manufacturing index, July (GS 48.5, consensus 48.8, last 48.5): We estimate the ISM manufacturing index was unchanged in July (at 48.5), reflecting weaker regional manufacturing surveys so far on net this month (GS manufacturing survey tracker -1.0pt to 48.2) but a potential boost from residual seasonality.

Friday, August 2

- 08:30 AM Nonfarm payroll employment, July (GS +165k, consensus +178k, last +206k); Private payroll employment, July (GS +125k, consensus +148k, last +136k); Average hourly earnings (mom), July (GS +0.3%, consensus +0.3%, last +0.3%); Average hourly earnings (yoy), July (GS +3.7%, consensus +3.7%, last +3.9%); Unemployment rate, July (GS 4.1%, consensus 4.1%, last 4.1%); Labor force participation rate, July (GS 62.6%, consensus 62.6%, last 62.6%): We estimate nonfarm payrolls rose by 165k in July (mom sa). While job growth tends to accelerate in the summer when the labor market is tight (as an influx of the labor supply allows vacant positions to be filled), we assume a 15k drag from Hurricane Beryl and a moderating (albeit still above-trend) contribution from the recent surge in immigration. Additionally, Big Data measures indicate a pace of job creation below the recent payrolls trend. We estimate that the unemployment rate was unchanged at 4.1%, reflecting higher household employment and flat labor force participation at 62.6%. We estimate average hourly earnings rose 0.3% (mom sa), which would lower the year-on-year rate by 0.2pp to 3.7%.

Source: DB, Goldman

Tyler Durden

Mon, 07/29/2024 – 09:27

via ZeroHedge News https://ift.tt/u4UWwvy Tyler Durden