Futures Gain As Expectations For A 50bps Rate Cut Spike

US futures pointed to modest gains after a rally that lifted the Nasdaq 100 more than 5% this week thanks to Nvidia, and the S&P 500 by 3.5%. As of 8:00am ET, S&P futures rose 0.2% led by small-caps which rose 1% as hopes of a jumbo 50bps rate cut jumped overnight; Nasdaq futures were 0.1% higher, with GOOG, META, and NVDA the top performers in megacap land despite a plunge by Adobe on poor guidance. Treasuries yields fell with the 10Y trading at 3.65% and the policy-sensitive 2Y yield down 5bps, while the dollar continues to slide, dropping for a third day, and retreating 0.3% after an article by the WSJ’s Nick Timiraos and comments by Nevertrumper Bill Dudley restored speculation that a 50bps rate cut is possible next week. The yen soared to a fresh 2024 high. Commodities are higher. Today, the data focus will be on Michigan Sentiment and inflation expectation. The consensus is at 68.5 vs. 67.9 prior.

In premarket trading, Adobe plunged -8% after the guidance disappointment despite a strong FQ3 upside. Oracle jumped another +6% after its positive ultra long-term revenue guidance. Boeing shares fall as much as 4.4% after the planemaker’s factory workers walked off the job for the first time in 16 years. Here are some other notable movers:

- Halliburton (HAL) shares are down 0.6% in premarket trading after RBC Capital Markets downgraded the energy company to sector perform from outperform.

- Instil Bio (TIL) shares jump 9.2% in premarket trading after Baird increased its price target on the stock to a Street-high of $180 — an increase of 463% from the broker’s last figure.

- Moderna shares (MRNA) fall as much as 4.9% in premarket trading on Friday, set to extend losses for a second session, as at least two brokerages, including JPMorgan and Jefferies, downgrade their ratings on the stock. The downgrades come after the biotech company said it aims to reduce its research and development budget by about 20% over the next three years. The company also lowered its annual revenue guidance for 2025.

- RH (RH) shares soar 20% in premarket trading after the furniture retailer reported second-quarter revenue and profit that topped Wall Street expectations. The company touted an improvement in customer demand in recent months, though it cut its sales forecast for the year, saying revenue will lag demand as it adjusts its assortment.

- Vistra Corp. (VST) shares rise 2.9% in premarket trading after Jefferies called the stock its top pick as it launched coverage of the power sector with a constructive view.

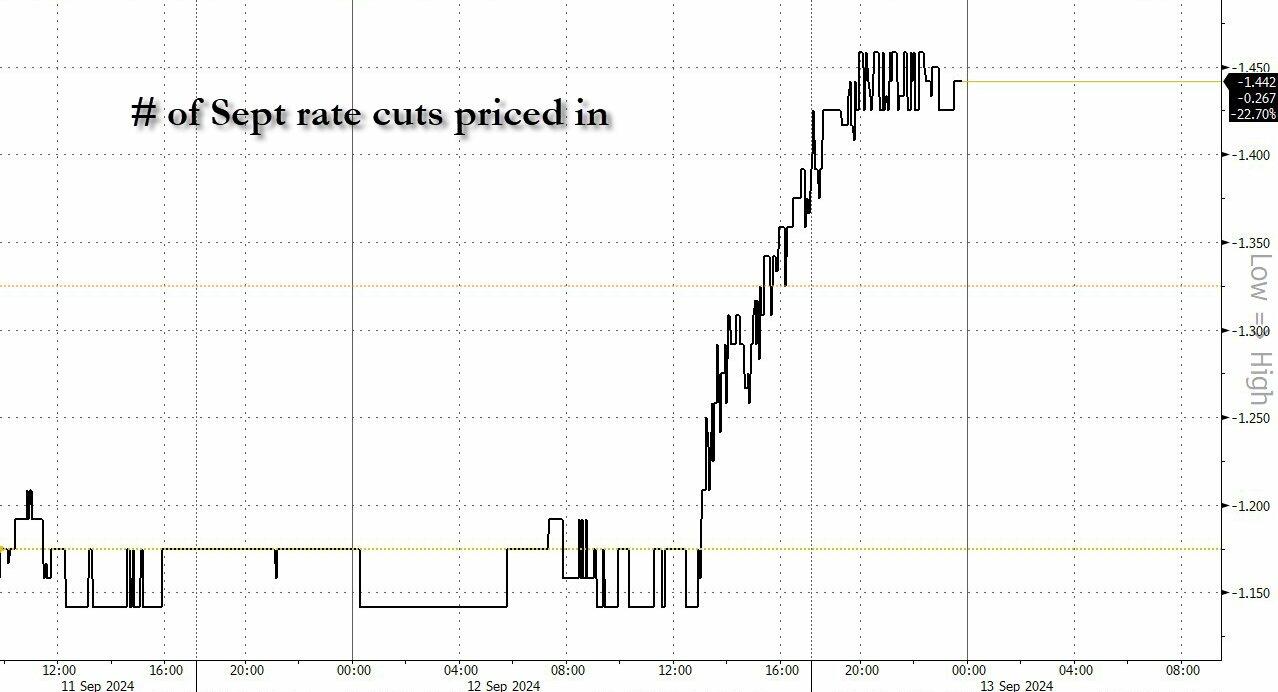

Investors remain divided on the magnitude of the Fed’s anticipated pivot to policy easing starting at next week’s meeting. The debate has continued after data Thursday showed that the US producer price index picked up slightly in August after the previous month’s numbers were revised lower. Meanwhile, an uptick in applications for unemployment benefits renewed concerns about a weakening labor market. Traders are now betting on 33 basis points of cuts from the Fed on Sept. 18 (45% odds of a 50bps rate cut), versus 31 basis points on Thursday and 26 basis points on Wednesday.

“If I were in the room, I would actually be pushing for a 50 basis-point rather than a 25 basis-point cut,” Evercore Chairman Emeritus Ralph Schlosstein said in an interview with Bloomberg TV. “The balance of risks has shifted from a risk that inflation doesn’t come down as we hope, to a risk that unemployment grows up faster than we would hope.”

His view echoed that of former New York Fed President William Dudley, a Bloomberg Opinion columnist and adviser, and chair of the Bretton Woods Committee. “I think there’s a strong case for 50,” he said Friday in Singapore. “I know what I’d be pushing for.”

Thursday’s wholesale inflation data followed the more closely watched consumer price index, which showed underlying inflation accelerated in August. Yet policymakers have made it clear that they’re currently highly focused on softness in the labor market, which is more likely to drive policy discussions in the months ahead.

In Europe, the Stoxx 600 rose 0.4%. IBEX outperforms peers, adding 0.4%, FTSE 100 is flat and underperforms. Autos, construction and real estate are the best-performing sectors in Europe. Danish stocks hit a record for the first since November 2021, paced by gains im DSV A/S after the logistics firm agreed to buy a Deutsche Bahn AG unit for €14.3 billion ($15.9 billion). Here are the most notable European movers:

- Roche shares gain as much as 2.7% after Bank of America upgrades to buy, saying the EPS downgrade cycle is over for the Swiss drugmaker.

- DSV shares gain as much as 4.3% after the Danish logistics firm announced it has signed an agreement to buy 100% of Deutsche Bahn’s DB Schenker unit for €14.3 billion.

- Fresenius shares gain as much as 4% to the highest intraday level since May 2022 after being upgraded to overweight from neutral at JPMorgan.

- Konecranes shares climb as much as 8.7%, the most in seven weeks, after the Finnish industrial crane manufacturer raised its FY sales outlook, citing “strong delivery execution.”

- Bollore shares rise as much as 7.1% after the holding company of the French tycoon Vincent Bollore announced plans to squeeze out minority shareholders in three holding companies.

- Precious-metals producers advance for a second day in Europe and South Africa as gold rises to a fresh record.

- Travis Perkins shares rise as much as 3%, the most since July, after RBC boosted its price target to a Street-high 1,150p from 950p.

- Worldline shares slump as much as 14% to a record low after cutting full-year guidance for a second time in two months, citing “slow trading conditions” and performance issues.

- AstraZeneca shares drop as much as 2.8%, falling for a fourth straight session, after Deutsche Bank downgrades to sell from hold and sets a Street-low price target.

- Salmar shares fall as much as 2.4% as Berenberg cuts its price target for the Norwegian salmon farmer, expecting falling global prices despite relatively tight demand.

- Kesko shares drop as much as 2.6% after the Finnish home goods and improvements retailer reports its sales figures for August, which DNB Markets views as “mixed.”

- Chemometec shares drop as much as 4.4% after Nordea gives the Danish lab-equipment firm its only sell rating, as it downgrades from hold.

In FX, the Bloomberg Dollar Spot Index falls 0.3%. AUD and CAD are the weakest performers in G-10 FX; JPY and SEK outperform.

In rates, front-end Treasuries outperform global bonds across the curve as traders revive the chance that the Federal Reserve might start its easing cycle with a 50bps interest-rate cut. Two-year yields drop more than 6bps to 3.57%. Treasuries and bunds curves bull steepen, while gilts lag peers with the Bank of England largely expected to keep rates on hold next week.

In commodities, WTI trades within Thursday’s range, adding 0.9% to near $69.61 amid a rebound from record bearish levels. Spot gold rises roughly $12 to trade near $2,570/oz as it climbs to a record high.

To the day ahead now, and data releases include Euro Area industrial production for July, and in the US there’s the University of Michigan’s preliminary consumer sentiment index for September. From central banks, we’ll hear from ECB President Lagarde and the ECB’s Rehn.

Market Snapshot

- S&P 500 futures up 0.2% at 5,614.50

- STOXX Europe 600 up 0.4% to 513.88

- MXAP up 0.5% to 183.11

- MXAPJ up 0.5% to 569.20

- Nikkei down 0.7% to 36,581.76

- Topix down 0.8% to 2,571.14

- Hang Seng Index up 0.7% to 17,369.09

- Shanghai Composite down 0.5% to 2,704.09

- Sensex little changed at 82,946.86

- Australia S&P/ASX 200 up 0.3% to 8,099.95

- Kospi up 0.1% to 2,575.41

- German 10Y yield down 2 bps at 2.13%

- Euro up 0.2% to $1.1091

- Brent Futures up 0.3% to $72.21/bbl

- Gold spot up 0.3% to $2,566.68

- US Dollar Index down 0.36% to 101.01

Top Overnight News

- Boeing’s largest labor union voted overwhelmingly to go on strike as of Friday, dealing a fresh blow to the company that’s already struggling mightily. WSJ

- China suspended the operations of PricewaterhouseCoopers LLP for six months and imposed a record penalty over lapses in its auditing of China Evergrande Group. The accounting firm was fined 441 million yuan ($62 million) for its auditing work on Evergrande’s inflated financial reports from 2018 to 2020. BBG

- Xi subtly downshifts China’s focus on achieving its economic growth targets as headwinds mount. SCMP

- Putin warns he would consider Moscow to be directly at war with NATO if Ukraine is given permission to conduct strikes deep into Russian territory. RTRS

- Worldline shares tumble in European trading on Fri after the company cut its revenue/earnings guidance for 2024 and replaced its CEO (“over the summer, Worldline experienced slow trading conditions coupled with specific performance issues in our Pacific business and on some global online verticals, including travel”). RTRS

- European banks are buying back AT1 bonds at a record pace, with $4.5 billion repurchased this year, as regulatory clarity and strong investor demand embolden lenders. BBG

- Biden close to signing off on allowing Ukraine to launch long-range weapons into Russia (just so long as they aren’t weapons provided by the US). NYT

- William Dudley (former head of the NY Fed) says there’s a “strong case” for a 50bp rate cut at the 9/18 FOMC meeting. BBG

- Former Trump administration officials are working on a plan to privatize Fannie and Freddie and will look to execute it should Trump win in Nov. WSJ

- Turkey seeks US approval to buy GE aerospace (GE) engines for military jets: BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were ultimately mixed and initially took their cues from the gains in the US, but with upside capped by a lack of fresh drivers ahead of a long weekend. ASX 200 was led by outperformance in mining stocks with gold miners boosted after the precious metal hit a fresh record high. Nikkei 225 underperformed owing to currency strength and as participants headed towards the extended weekend in Japan. Hang Seng and Shanghai Comp were mixed as the former spearheaded the advances in the region with the help of developers, energy stocks and financials, while the mainland was lacklustre ahead of the latest Chinese activity data on Saturday and the four-day weekend closure.

Top Asian News

- China’s top legislative body approves draft proposal to raise retirement age, via Xinhua; China will raise retirement age of men to 63 (prev. 60) and female to 55-58 (prev. 50-55)

Top European News

- German Economy Ministry said economic recovery is only likely to occur towards the end of the year; German export economy not expected to see significant impetus in coming months.

- The Bank of England/Ipsos Inflation Attitudes Survey: Median expectations of the rate of inflation over the coming year were 2.7%, down from 2.8% in May 2024. Asked about expected inflation in the twelve months after that, respondents gave a median answer of 2.6%, unchanged from 2.6% in May 2024. Asked about expectations of inflation in the longer term, say in five years’ time, respondents gave a median answer of 3.2%, up from 3.1% in May 2024.

FX

- DXY is trading around the 101.00 mark following a dovish repricing of Fed bets, attributed to an article by Fed-watcher Timiraos, where he noted that it could be a close call between 25 or 50bps, whilst former FOMC Member Dudley said he would push for a 50bps if he was stll on the committee.

- EUR/USD is on the rise after picking itself up from a 1.1005 base yesterday to a current peak at 1.1094, which has subsequently brought a test of 1.11 into view; upside stemming from a scaling back of dovish ECB bets at the October meeting.

- GBP is a touch firmer vs. the USD as the dovish repricing for next week’s Fed meeting stands in contrast to a widely-expected hold by the BoE next week. Accordingly, Cable has picked itself up from a 1.3001 low earlier in the week to a current peak of 1.3150.

- JPY is the best performer across the majors as USD/JPY extends its move lower for a fourth consecutive session in what appears to be a Fed vs. BoJ play.

- AUD/USD is currently pausing for breath after gaining on Wednesday and Thursday; some notable Opex activity for the pair is in play today.

- PBoC set USD/CNY mid-point at 7.1030 vs exp. 7.1048 (prev. 7.1214).

- Peru Central Bank cut its reference rate by 25bps to 5.25%, as expected, but stated that the rate cut does not necessarily mean future rate cuts will follow. The pair has now moved as low as 140.64; its lowest level since December 28th 2023.

Fixed Income

- USTs are scaling back yesterday’s losses with upside primarily attributed to an article by Fed-watcher Timiraos, where he noted that it could be a close call between 25 or 50bps. Comments from former FOMC member Dudley that he would be pushing for 50bps if he were on the committee is also a factor. The 10yr yield has slipped as low as 3.623% but is holding above Wednesday’s 3.605% trough.

- Bunds are higher alongside gains in global counterparts and a reversal of Thursday’s price action which saw the curve bear-flatten as odds of an October rate cut were scaled back. German 10yr yield is currently towards the middle of yesterday’s 2.098-169% range.

- Upside in Gilts is more a by-product of price action elsewhere in the fixed income space, given the light UK-docket. The UK 10yr yield is currently towards the middle of yesterday’s 3.744-798% range.

Commodities

- WTI and Brent continue the gains seen in the prior session, with upside facilitated by the broader risk-on sentiment coupled with the shut-ins amid Hurricane Francine (now a post-tropical cyclone). Brent Nov resides in a USD 72.17-52/bbl.

- Precious metals are mostly firmer, with modest gains seen in spot gold and silver whilst spot palladium is subdued, following the prior day’s outperformance. The complex will be mindful of a meeting between US and UK governments, where it will decide on allowing Ukraine to use long-range missiles to hit targets in Russian territory. Spot gold trades in a USD 2,566-2,571.12/oz range.

- Mixed trade across base metals and reflective of the tentative tone across the market.

- US Coast Guard said the New Orleans Port condition is normal following waterway assessments, with vessel movement and cargo operations authorised within the COTP New Orleans Zone.

- Macquarie said global oil market faces heavy surplus in 2025. Oil may drop into low USD 50s/bbl, outside base case.

ECB speak

- ECB’s Nagel said expect to reach inflation goal at the end of next year and core inflation is also going in the right direction, according to German radio.

- ECB’s Simkus discussed monetary policy in interview on Radio LRT, while he stated that additional reductions will rely on information and speed of rate cuts will depend on data.

- ECB’s Rehn said the ECB’s rate cuts support growth but Europe should get on the road to better productivity. Current uncertainties further emphasise the dependence on fresh data and analysis about the economy. Council will continue to base monpol on the inflation outlook, the dynamics of core inflation net of energy and food prices and strength of monpol transmission.

- ECB’s Vasle said inflation is to be largely steered by core and services; not committing to a pre-determined path.

- ECB’s Villeroy said that recent activity data has been somewhat disappointing. Should gradually reduce the degree of monetary restriction as appropriate.

- ECB’s Rehn said EZ GDP growth is projected to gradually pick up; disinflation in the EZ is on the right track; downside risks to growth increased over the summer; have full freedom of action and flexibility at all meetings.

Geopolitics: Ukraine

- Lebanese media reported that rockets were fired from southern Lebanon towards Safad in northern Israel, according to Sky News Arabia.

- Sirens sounded in the Israeli settlement of Alemon in the West Bank warning of an infiltration of militants, according to Al Jazeera.

Geopolitics: Other

- Russian President Putin warned the UK and the US that they will be “at war” with Russia if they allow Ukraine to use long-range missiles to strike targets inside Russia, according to The Times.

- US Ambassador to Ukraine strongly condemned Russia’s attack on a vessel carrying grain from Ukraine.

- Russian Deputy Defence Minister said the China-Russia relationship is a model of nation-to-nation collaboration and is a peace guarantee, while their two defence ministries have continuously expanded cooperation and interactions such as drills and exchanges, including more than 100 projects this year. The official added that the US is trying to suppress any technological development centre that is not obedient to it which is double containment and suppression of China and Russia. Furthermore, the Russian Deputy Defence Minister said Russia has unique experience of fighting against various Western weapons and is ready to share it with partners, according to RIA.

- China’s Defence Ministry said major countries must the take lead in safeguarding global security and should never interfere in other countries’ internal affairs. China’s Defence Ministry also stated it is important to uphold fairness, justice, international rule of law, and enhance the authority of the UN, while it added that peace talks and political settlement are the only solutions for the Ukraine crisis and Israeli-Palestinian conflict.

- North Korean leader Kim oversaw a test-fire for the new 600MM multiple rocket launcher, while he inspected a training base for special operations armed forces and guided combatants drills, as well as inspected the nuclear weapons institute and production base of weapons-grade nuclear materials, according to KCNA. It was later reported that South Korea condemned North Korea’s unveiling of a uranium enrichment facility and said it will never accept North Korea’s possession of nuclear weapons, according to the Unification Ministry.

US Event Calendar

- 08:30: Aug. Import Price Index MoM, est. -0.2%, prior 0.1%

- Aug. Import Price Index ex Petroleu, est. 0.2%, prior 0.2%

- Aug. Import Price Index YoY, est. 0.9%, prior 1.6%

- Aug. Export Price Index MoM, est. -0.2%, prior 0.7%

- Aug. Export Price Index YoY, est. 1.4%, prior 1.4%

- 10:00: Sept. U. of Mich. Sentiment, est. 68.5, prior 67.9

- Sept. U. of Mich. Current Conditions, est. 61.6, prior 61.3

- Sept. U. of Mich. Expectations, est. 72.2, prior 72.1

- Sept. U. of Mich. 1 Yr Inflation, est. 2.8%, prior 2.8%

- Sept. U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

Earlier this week, Jim and I published our latest chartbook, which is called “At the crossroads”. It looks at 5 themes where markets are currently debating the direction of travel. The outcomes will have profound impacts over the quarters and years ahead.

One theme markets are still debating this morning is whether the Fed are going to cut by 25bps or 50bps at their meeting next week. Up until yesterday afternoon, it had looked as though 25bps was increasingly likely, with futures only placing a 15% chance on a 50bp move. But then a couple of articles were published in the Wall Street Journal and the FT suggesting that a 50bp move was still in play, which has led markets to once again re-evaluate their expectations, and futures are now pricing in a 47.5% chance of a 50bp move this morning. So very much in the balance.

The initial driver of this was a story by Nick Timiraos in the Wall Street Journal, which appeared to favour arguments for a 50bp cut next week. In particular, it said that even though it was “all but settled” that the Fed would cut rates this week, “how much is shaping up to be a close call.” So that was something of a surprise to investors, who had been increasingly pricing in 25bps, not least after the core CPI print was a bit stronger than expected on Wednesday. In many respects, this echoes what took place before the June 2022 meeting, when markets had been expecting a 50bp hike going into the Fed’s blackout period, but an article by Timiraos shortly before the decision said they were likely to consider a larger 75bp hike, which led markets to adjust their expectations just before the decision, before they did indeed hike by 75bps. Expectations for a 50bp cut then got further traction yesterday from an FT report, which suggested the Fed “faces a close call” whether to cut by a larger 50bps.

We’ll have to see if market pricing stays at these levels, as there are still several days to go before the decision. But it’s worth noting that if expectations for a 50bp cut remain at 47.5%, that would be the most uncertain market pricing for a Fed decision in this cycle so far. After all, even as policy expectations have shifted about a lot, since the pandemic we’ve always seen the Fed deliver the rates decision that markets were pricing in just beforehand as the most likely. So when markets have moved higher or lower after the Fed’s decisions, the reactions have generally been in response to factors like the dot plot, or comments in the press conference, rather than the rates decision itself, which has been widely expected. So if pricing stays where it is currently, it would be the first meeting in years where there’s serious uncertainty about the rates decision.

In terms of the market reaction, we can already see how investors are pricing in the potential for 50bps again. For instance, the 2yr Treasury yield is down by -5.4bps overnight to 3.58%, and if it stays there it would be its lowest closing level in just over two years. Similarly, the 10yr yield is down -3.0bps overnight to 3.64%. The effects have also been evident globally, and the Japanese Yen has strengthened to 140.81 per US Dollar this morning, on track for its strongest level since July 2023. In the meantime, US equities got a fresh boost from the prospect of a 50bp cut, with the S&P 500 (+0.75%) posting a fourth consecutive advance, which left the index just over 1% beneath its all-time high from a couple of months ago. And futures for the index are up another +0.06% this morning. However, Japanese equities have come under pressure overnight given the yen’s appreciation, with the TOPIX (-0.91%) and the Nikkei (-0.81%) both losing ground. Although in China, the CSI 300 (+0.04%) stabilised after closing at a 5-year low the previous day, and South Korea’s KOSPI (-0.11%) has only posted a modest decline.

Before the Fed news came through, the day was going largely according to script, with the US data coming in broadly in line with expectations, whilst the ECB delivered an expected 25bp rate cut. That rate cut took the ECB’s deposit rate down to 3.50%, marking their second cut of this cycle after an initial move in June, and markets continue to anticipate further cuts over the months ahead. We also had their latest forecasts, which showed growth projections a tenth lower each year relative to June, rising from +0.8% this year to +1.3% in 2025 and +1.5% in 2026. Otherwise, the forecasts for headline inflation were unchanged, coming in at +2.2% in 2025 and +1.9% in 2026. But they did upgrade the core CPI forecasts for next year, up by a tenth to +2.3%, before coming down to +2.0% in 2026, as before.

Against that backdrop, European sovereign bond yields moved higher yesterday, with those on 10yr bunds (+3.8bps) and OATs (+2.4bps) both picking up. The sell-off was stronger at the front end, with 2yr German yields (+7.3bps) seeing their biggest rise in four weeks amid some dialling back of rate cut expectations over the next several months. While there were few surprises from the ECB meeting, President Lagarde’s tone showed less scepticism on growth and inflation than had emerged in markets, which had moved to price the ECB deposit rate falling to below 2% by next summer. In the press conference, Lagarde kept the ECB’s options open, saying that they would “remain data-dependent”, and that a “declining path is not pre-determined”. And later in the session, a Bloomberg article citing “people familiar with the matter” said that although an October cut was unlikely, downside risks to growth meant they’d rather keep the option open. Our European economists at DB continue to expect the next cut of 25bps in December. While they see risks as skewed towards faster easing, it is not obvious to them that policy rates need to go below neutral. See their full reaction note here.

Elsewhere yesterday, there was some focus on the latest US data, but there really wasn’t much that changed our understanding of the economy. For instance, the weekly initial jobless claims were broadly in line with expectations at 230k over the week ending September 7 (vs. 226k expected), and the continuing claims covering the previous week were exactly in line with expectations at 1.850m. Otherwise we did get the PPI inflation release, which was a bit stronger than expected at +0.2% for August (vs. +0.1% expected). But the previous month was revised down a tenth at the same time, so again our overall understanding wasn’t too different to before.

For equities, there was a fairly benign backdrop yesterday, and the news about the potential for a 50bp cut helped the S&P 500 advance +0.75%. The index has now risen every day this week, up +3.46% as it stands, so it’s clawed back most of its losses from last week, when it had its worst weekly performance since SVB’s collapse in March 2023. And it’s only just over 1% beneath its all-time high from July again. Tech stocks led the rally, with the Magnificent 7 (+1.40%) also up for a 4th consecutive day, leaving its own gains at +7.06% since the start of the week. But the gains were broad based, and all eleven S&P 500 major sector groups were higher on the day, whilst the small-cap Russell 2000 rose +1.22%. And over in Europe, the STOXX 600 was up +0.80%, alongside other indices including the DAX (+1.03%) and the CAC 40 (+0.52%).

To the day ahead now, and data releases include Euro Area industrial production for July, and in the US there’s the University of Michigan’s preliminary consumer sentiment index for September. From central banks, we’ll hear from ECB President Lagarde and the ECB’s Rehn.

Tyler Durden

Fri, 09/13/2024 – 08:15

via ZeroHedge News https://ift.tt/JVeQHGm Tyler Durden