BMO: The Strike Price Of The “Powell Put” Is Only Known To The Fed… So Markets May Retest It Soon Tyler Durden

Sat, 09/05/2020 – 16:20

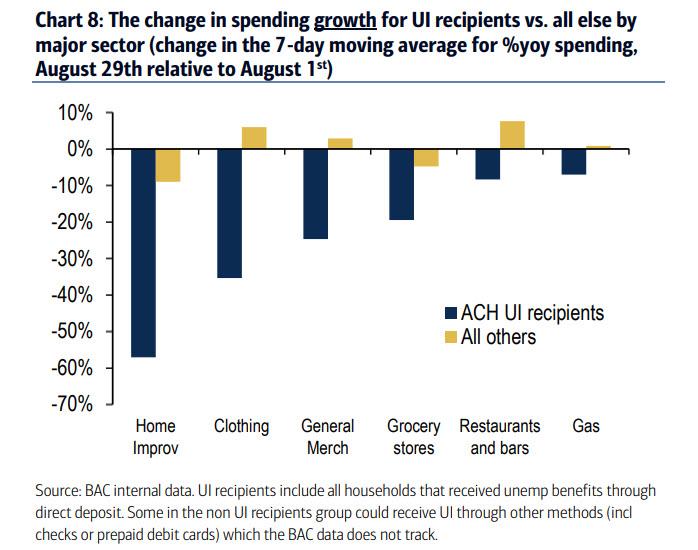

After the most tumultuous week in markets since the June mini crash, the week ahead will offer very little in terms of economic data to augment investors understanding of the state of the economy or the domestic consumer, although the fiscal cliff continues to bit. According to the latest BofA data, total card spending as measured by aggregated BAC credit and debit card data declined 0.7% yoy for the week ending Aug 29th, confirming any recent upward momentum has now fizzled out.

Worse, spending by recipients of Unemployment Insurance – which has either stopped or substantially tapered off since August 1 – has cratered, especially in home improvement, clothing and general merchandise categories.

It is in this context of declining spending that an updated read on core-inflation will test the response of US rates to the first CPI print since the Fed unveiled its new Average Inflation Targeting framework.

As BMO’s Ian Lyngen and Jon Hill writes, an emphasis on consumer pricing pressure “risks fiddling while equities burn, as it were” because the dramatic retracement of domestic stocks from the fresh record highs – in large part due to the collapse of the gamma meltup trade following the identification of SoftBank as the responsible party – wasn’t exactly what the market needed to ease ongoing apprehension regarding the still-record high valuations.

More importantly, according to the BMO rates strategists, it also could mark the beginning of a troubling period for the Fed, because “in the wake of the NFP data, there was very little on the horizon that might have caused the Fed to bring forward any dovish policy action to the September 16 FOMC – with the exception of a sharp tightening in financial conditions led by a spike in equity vol.” Translated: the Fed may freak out about the market’s 4% drop which the following chart puts into perspective.

To be sure, the market hasn’t exercised the Powell put in a few months, so “no time like the present”, and as BMO further adds “conventional wisdom holds that it’s not the magnitude of any stock market correction that prompts monetary policymakers into action but rather the pace.” In any case, just two significant back-to-back selloffs from the highs won’t be sufficient (even if circuit breakers come into play) unless of course Powell wants to repeat Bernanke’s panic when he cut rates by 75bps in Jan 2008 in response not to a systemic crisis but a bad trade by Jerome Kerviel.

And speaking of the Powell Put, BMO writes that the performance of risk assets continues to be relevant even after a period of big-tech led weakness called into the question the sustainability of the S&P 500’s unrelenting march higher. “Indeed, eight consecutive sessions of all-time highs raises concerns about asset bubbles and financial stability” Lyngen writes however noting that “Powell has made it abundantly clear that until the labor market heals and signs of inflation percolate, the FOMC will be extremely reluctant to be anything other than accommodative.” This also confirms that the relationship between equities and financial conditions – i.e., the primary reason why the Fed openly is propping up stocks – should also not be discounted. Yet not even in the Fed’s centrally-planned universe does last week’s -4% drop warrant a policy response. On the other hand, “where exactly the strike price for the Powell put lies is only known to those in the Eccles Building, but we have no doubt another round of volatility akin to March and April would quickly bring the Fed back into play,” BMO concludes, as it hints that the market may soon retest just how low the Fed will allow stocks to drop now that the meltup is over, before Powell intervenes again.

In any case, it is safe to say that the performance domestic equities during a period of radio silence from Fed-speakers ahead of the FOMC meeting is uniquely positioned to be more influential on the direction of monetary policy than would typically be the case, and so watch for any dovish hints from the Fed after Labor Day. Of course, “if stocks are down 35%-40% from the highs this time next week, it is difficult not to assume investors will look to Powell for reassuring dovishness” Lyngen writes, although it is unlikely that the market will lose a third of its value in the coming days.

* * *

Finally, in terms of what the Fed unveils at the Sept FOMC when expectations are high for even more easing, a recent BMO survey indicates that the market is divided on whether the next move is outcome specific forward guidance or an extension of the weighted-average-maturity of the existing QE program. There is also the option of increasing the balance sheet at a faster rate using the existing breakdown of purchasing in Treasuries, MBS, and corporates. That said, It’s much too soon to speculate if the upcoming meeting is anything more than a placeholder, although there is little question the sharp upward trajectory of the VIX will be first in the post-holiday ‘what to watch’ queue (unless of course the blow up of Masa Son’s gamma gambit doesn’t send implied vol plunging).

via ZeroHedge News https://ift.tt/355IPX3 Tyler Durden

Outlets claiming to have “confirmed” Jeffrey Goldberg’s story about Trump’s troops comments are again abusing that vital term…

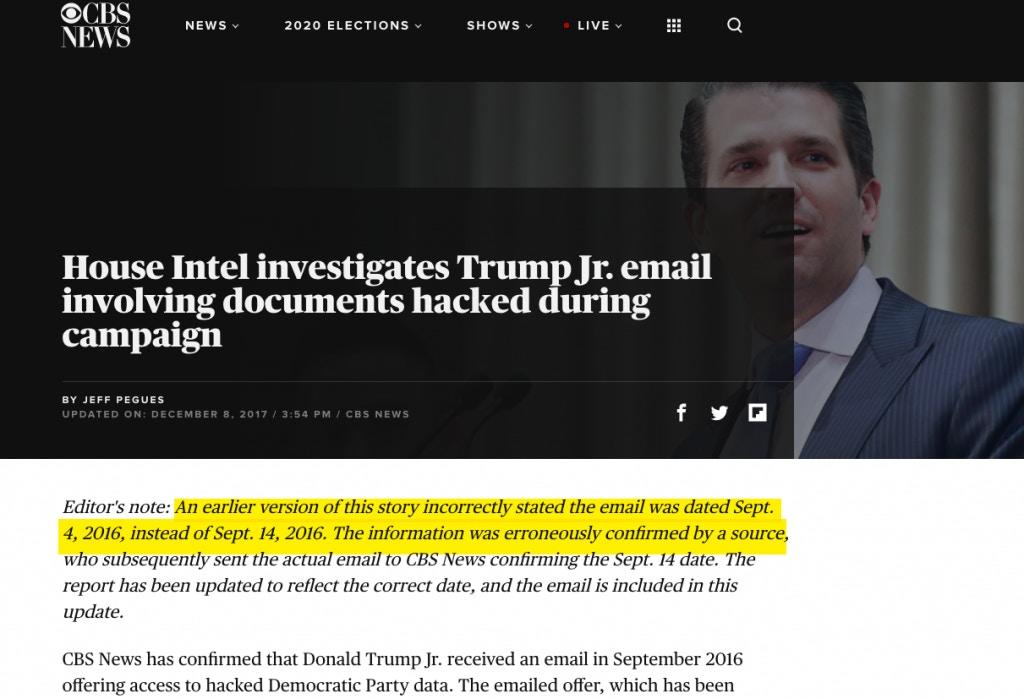

ONE OF THE MOST HUMILIATING journalism debacles of the Trump era played out on December 8, 2017, first on CNN and then on MSNBC. The spectacle kicked off on that Friday morning at 11:00 a.m. when CNN, deploying its most melodramatic music and graphics designed to convey that a real bombshell was about to be dropped, announced that anonymous sources had provided the network with a smoking gun proving the Trump/Russia conspiracy once and for all: during the 2016 campaign, Donald Trump, Jr. had received a September 4 email with a secret encryption key that gave him advancedaccess to WikiLeaks’ servers containing the DNC emails which the group would subsequently release to the public ten days later. Cable news and online media spontaneously combusted, as is their wont, in shock, hysteria and awe over this proof that WikiLeaks and Trump were in cahoots.

CNN has ensured that no videos of the festivities are available on YouTube for anyone to watch. That’s because the claim was completely false in its most crucial respect. CNN misreported the date of the smoking gun email Trump, Jr. received: rather than being sent to him on September 4 – ten days prior to WikiLeaks’ public release, thus enabling secret access – the email was merely sent by a random member of the public after the public release by WikiLeaks (September 14), encouraging Trump, Jr. to look at those now-public emails.

Though the original false report cannot be viewed any longer (except in small snippets from other networks, principally Fox, discussing CNN’s debacle), one can view the cringe-inducing video of CNN’s Senior Congressional Correspondent Manu Raju explaining, after the Washington Post debunked the story, that “we are actually correcting” the reporting, doing his best to downplay what a massive blunder this was (though the whole thing is fantastic, my favorite line is when Raju says, with no small amount of understatement: “this appears to change the understanding of this story,” followed by: “perhaps the initial understanding of what this email was, perhaps is not as significant based on what we know now”: perhaps):

Washington (CNN) Correction: This story has been corrected to say the date of the email was September 14, 2016, not September 4, 2016. The story also changed the headline and removed a tweet from Donald Trump Jr., who posted a message about WikiLeaks on September 4, 2016.

So mistakes happen in journalism, even huge and embarrassing ones. Other than some petty schadenfreude, why is this worth remembering? The reason is that that sorry episode reflects a now-common but highly corrosive tactic of journalistic deceit.

Very shortly after CNN unveiled its false story, MSNBC’s intelligence community spokesman Ken Dilanian went on air and breathlessly announced that he had obtained independentconfirmation that the CNN story was true. In a video segment I cannot recommend highly enough, Dilanian was introduced by an incredibly excited Hallie Jackson — who urged Dilanian to “tell us what we’ve just now learned,” adding: “I know you and some of our colleagues have confirmed some of this information: what’s up?” Dilanian then proceeded to explain what he had learned:

That’s right, Hallie. Two sources with direct knowledge of this are telling us that Congressional investigators have obtained an email from a man named “Mike Erickson” — obviously they don’t know if that’s his real name — offering Donald Trump and his son Donald Trump, Jr. access to WikiLeaks documents… It goes to the heart of the collusion question….. One of the big questions is: did [Trump Jr.] call the FBI?

MSNBC, December 8, 2017

How could that happen? How could MSNBC purport to confirm a false story from CNN? Shortly after, CBS News also purported to have “confirmed” the same false story: that Trump, Jr. received advanced access to the WikiLeaks documents. It’s one thing for a news outlet to make a mistake in reporting by, for instance, mis-reporting the date of an email and thus getting the story completely wrong. But how is it possible that multiple other outlets could “confirm” the same false report?

It’s possible because news outlets have completely distorted the term “confirmation” beyond all recognition. Indeed, they now use it to mean the exact opposite of what it actually means, thereby draping themselves in journalistic glory they have not earned and, worse, deceiving the public into believing that an unproven assertion has, in fact, been proven. With this disinformation method, they are doing the exact opposite of what journalism, at its core, is supposed to do: separate fact from speculation.

CNN ultimately blamed its anonymous sources for this error, but refused to out them by insisting that it was a somehow a good faith mistake rather than deliberate disinformation (how did multiple “good faith” sources all “accidentally misread” an email date in the same way? CNN, in the spirit of news outlets refusing to provide the accountability and transparency for themselves that they demand from others, refuses to this very day to address that question).

But what is clear is that the “confirmation” which both MSNBC and CBS claimed it had obtained for the story was anything but: all that happened was that the same sources which anonymously whispered these unverified, false claims to CNN then went and repeated the same unverified, false claims to other outlets, which then claimed that they “independently confirmed” the story even though they had done nothing of the sort.

IT SEEMS THE SAME MISLEADING TACTIC is now driving the supremely dumb but all-consuming news cycle centered on whether President Trump, as first reported by the Atlantic’s editor-in-chief Jeffrey Goldberg, made disparaging comments about The Troops.

Goldberg claims that “four people with firsthand knowledge of the discussion that day” — whom the magazine refuses to name because they fear “angry tweets” — told him that Trump made these comments. Trump, as well as former aides who were present that day (including Sarah Huckabee Sanders and John Bolton), deny that the report is accurate.

So we have anonymous sources making claims on one side, and Trump and former aides (including Bolton, now a harsh Trump critic) insisting that the story is inaccurate. Beyond deciding whether or not to believe Goldberg’s story based on what best advances one’s political interests, how can one resolve the factual dispute? If other media outlets could confirm the original claims from Goldberg, that would obviously be a significant advancement of the story.

Other media outlets — including Associated Press and Fox News — now claim that they did exactly that: “confirmed” the Atlantic story. But if one looks at what they actually did, at what this “confirmation” consists of, it is the opposite of what that word would mean, or should mean, in any minimally responsible sense.

AP, for instance, merely claims that “a senior Defense Department official with firsthand knowledge of events and a senior U.S. Marine Corps officer who was told about Trump’s comments confirmed some of the remarks to The Associated Press,” while Fox merely said “a former senior Trump administration official who was in France traveling with the president in November 2018 did confirm other details surrounding that trip.”

In other words, all that likely happened is that the same sources who claimed to Jeffrey Goldberg, with no evidence, that Trump said this went to other outlets and repeated the same claims — the same tactic that enabled MSNBC and CBS to claim they had “confirmed” the fundamentally false CNN story about Trump Jr. receiving advanced access to the WikiLeaks archive. Or perhaps it was different sources aligned with those original sources and sharing their agenda who repeated these claims. Given that none of the sources making these claims have the courage to identify themselves, due to their fear of mean tweets, it is impossible to know.

But whatever happened, neither AP nor Fox obtained anything resembling “confirmation.” They just heard the same assertions that Goldberg heard, likely from the same circles if not the same people, and are now abusing the term “confirmation” to mean “unproven assertions” or “unverifiable claims” (indeed, Fox now says that “two sources who were on the trip in question with Trump refuted the main thesis of The Atlantic’s reporting”).

It should go without saying that none of this means that Trump did not utter these remarks or ones similar to them. He has made public statements in the past that are at least in the same universe as the ones reported by the Atlantic, and it is quite believable that he would have said something like this (though the absolute last person who should be trusted with anything, particularly interpreting claims from anonymous sources, is Jeffrey Goldberg, who has risen to one of the most important perches in journalism despite (or, more accurately because of) one of the most disgraceful and damaging records of spreading disinformation in service of the Pentagon and intelligence community’s agenda).

But journalism is not supposed to be grounded in whether something is “believable” or “seems like it could be true.” Its core purpose, the only thing that really makes it matter or have worth, is reporting what is true, or at least what evidence reveals. And that function is completely subverted when news outlets claim that they “confirmed” a previous report when they did nothing more than just talked to the same people who anonymously whispered the same things to them as were whispered to the original outlet.

Quite aside from this specific story about whether Trump loves The Troops, conflating the crucial journalistic concept of “confirmation” with “hearing the same idle gossip” or “unproven assertions” is a huge disservice. It is an instrument of propaganda, not reporting. And its use has repeatedly deceived rather than informed the public. Anyone who doubts that should review how it is that MSNBC and CBS both claimed to have “confirmed” a CNN report which turned out to be ludicrously and laughably false. Clearly, the term “confirmation” has lost its meaning in journalism.

via ZeroHedge News https://ift.tt/2Gp8NdF Tyler Durden

NBA Gives Award To Montrezl Harrell, Who Called Opponent A “B*tch Ass White Boy” Days Ago Tyler Durden

Sat, 09/05/2020 – 15:25

The NBA has undoubtedly been in the spotlight of the social justice battle currently taking place across the country.

Most recently, the NBA made news when it cancelled a slate of playoff games due to players boycotting and protesting in response to the shooting of Jacob Blake in Kenosha, WI.

And in addition to painting “Black Lives Matter” across all NBA courts…

…and the National Basketball Coaches Association, in conjunction with the Obama Foundation and the Equal Justice Initiative, forming Coaches for Racial Justice…

…and approving social justice messages on the back of NBA jerseys for the remainder of the season…

…the NBA has also provided players with warm up clothing and bench clothing that sports social justice messaging.

And so regardless of what you think of these actions, it’s pretty clear that the NBA is on the forefront of racial equality and condems racism of all kinds.

That is, of course, unless it comes from the LA Clippers’ Monrezl Harrell. Harrell made headlines a couple weeks ago when after hitting a shot against Luka Doncic of the Dallas Mavericks, he was seen backpedaling down the court and referring to Doncic as a “b*tch ass white boy”.

Given the giant uproar about racial equality in the NBA of late, one would think this would have major repercussions within the organization. But Harrell was not warned or reprimanded by the NBA for his statements.

In fact, just the opposite: on Friday, the NBA honored Harrell with their “Sixth Man of the Year” award for the 2019-2020 NBA season.

Harrell beat out Dennis Schröder and teammate Lou Williams for the award after averaging 18.6 points, 7.1 rebounds and 1.7 assists per game over the season. He has also been active in helping the LA Clippers advance through the playoffs, where they hope to bring in their first title in franchise history.

In fairness, Doncic later said he had no problems with the comment and trash talk is generally part of any professional sport.

But bringing race into the equation had many thinking: what would have happened if a white person had referred to a person of color in such a way while on the court.

Would it be written off as simply trash talk?

Would they be receiving awards from the NBA?

via ZeroHedge News https://ift.tt/3jPlA7B Tyler Durden

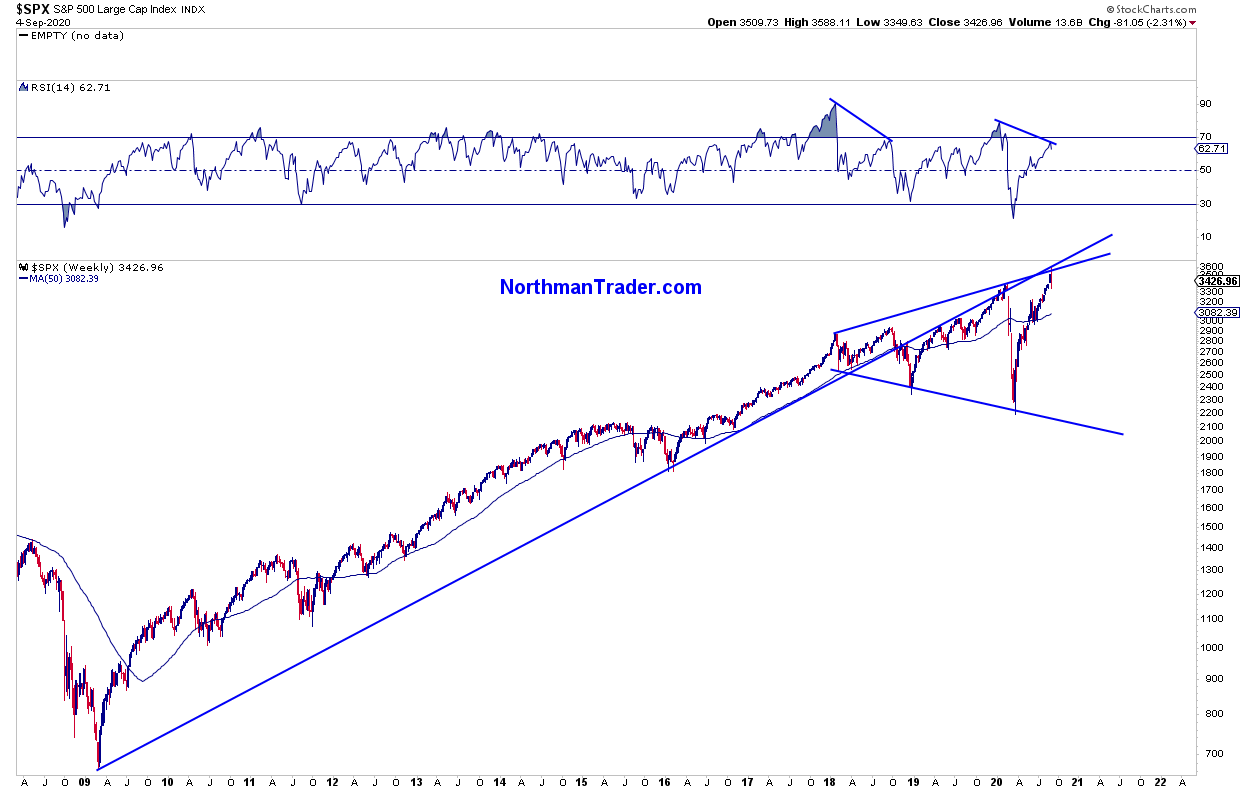

A confluence of factors led to this week’s sell-off in markets. In the lead up to this week’s market top we saw all the classic signs: Weakening participation, highly overbought readings, vast technical extensions, historic valuations accompanied by extreme complacency and bear capitulations.

And make no mistake: This sell off was intense. $NDX dropped 10% within 2 days off of all time highs, one of the fastest and steepest drops from all time highs in history if not the most in history. High flying tech stocks such as $AAPL and $TSLA dropped 20% and 26% in 2 days as well.

A mere flesh wound in what was an unstoppable rally or signs of the end or the beginning of the end?

I’m discussing these issues and more of the macro context in a new edition of Straight Talk. As announced this week I’ve moved Straight Talk to a podcast format and in the next few days/weeks I’ll make sure it gets listed in your favorite podcast directories such as Apple Poscats, Spotify and Google Podcasts and perhaps others as well so you can follow new episodes from there as well.

For now here’s the newest edition of Straight Talk:

As I discuss some charts in the episode I post some here for reference.

Namely:

The $VIX. In August I published $VIX 46 when $VIX was trading at 22 calling for a breakout to come with a target for 46. While the target has not been reached as of this writing we did get a major breakout and the $VIX hit 38 on Friday an over 70% move from the original post:

Also in August I mentioned the $DJIA having potential of its February gap and this gap was filled this week and it produced a rejection from here:

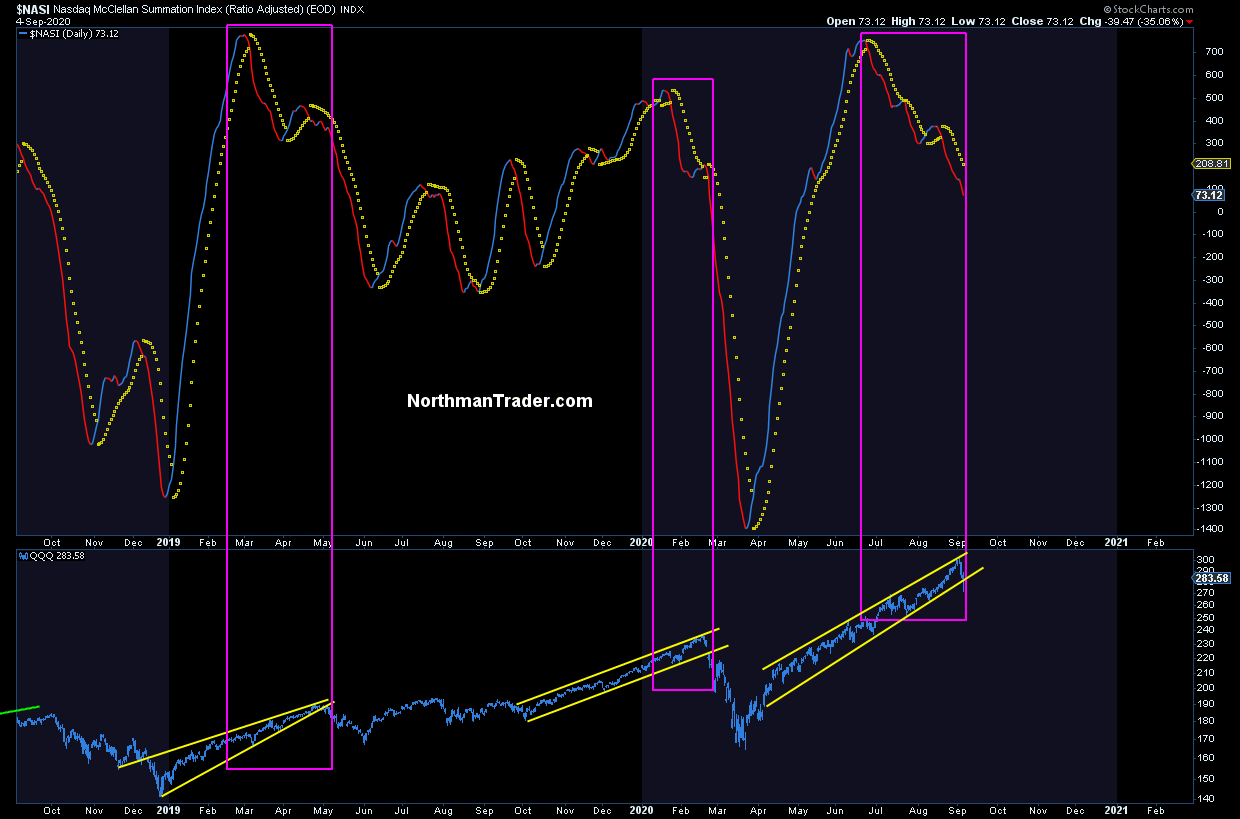

Also in August I kept talking about the weakening signals underneath and a warning sign on tech specifically the $NASI pointing to a coming correction in tech:

And I kept talking about the lack of confirmation in the value line geometric index $XVG with its message:

I repeat: New highs in select indices have been highly deceiving. They were driven by a few mega cap stocks.

The $XVG index suggests a border market still in a bear market.

Based on that measure $SPX would be trading at 2,600 were it not for mega cap expansions in 6/7 stocks. pic.twitter.com/UFSi7HchgD

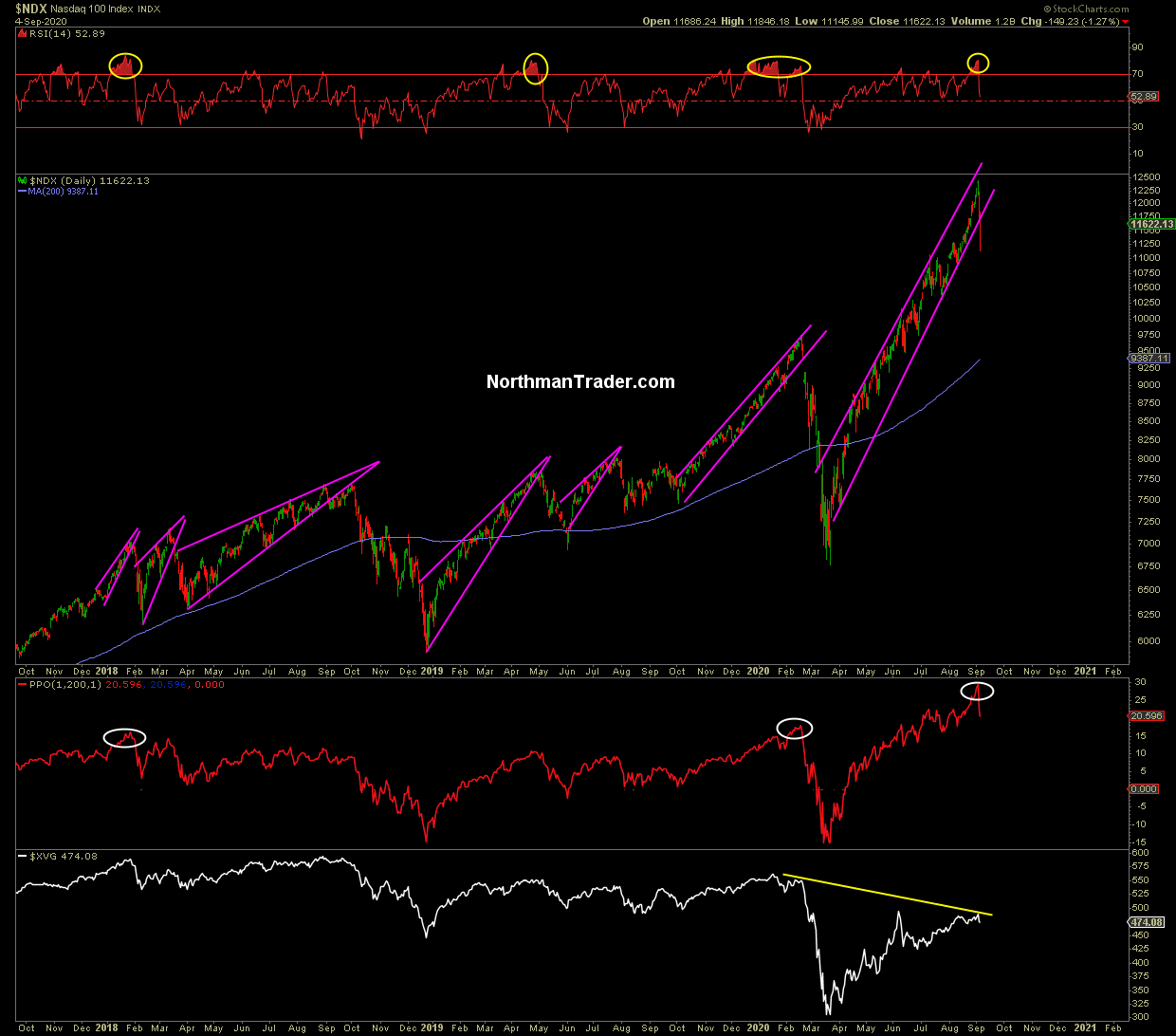

While indices kept driving to new highs in ever more extended patterns, similar to rallies we’ve seen before with this being the most extended since the year 2000. $SPX traded the highest above its 200MA and $NDX reached prices 33% above its 200MA:

All this as put/call ratios hit historic lows:

I repeat: New highs in select indices have been highly deceiving. They were driven by a few mega cap stocks.

The $XVG index suggests a border market still in a bear market.

Based on that measure $SPX would be trading at 2,600 were it not for mega cap expansions in 6/7 stocks. pic.twitter.com/UFSi7HchgD

And finally as outlined in Bear Capitulation and Panic Buying $SPX was reaching historic resistance as evidence by 2 key trend lines, both were hit this week and $SPX rejected from there:

In the context of history is this a coincidence that this all happened to come together at the beginning of September?

After all, following the market top in March of 2000 the subsequent counter rally peaked on September 1 and the top in 1929 ended on September 3rd, as did now this rally. This rally topping on September 2nd and in pre-market on September 3rd could all be a coincidence of course, but only time will tell.

The similarity in structure though between the historic run leading to the top in 1929 and the last 13 years is striking:

Pretty wild actually. Not sure if it means anything, but the structural similarity, despite all the differences in time and global technology is pretty impressive. pic.twitter.com/GHs15JDT81

I’ll be publishing a detailed analysis of the technicals and implications tomorrow Sunday September 5th in the latest edition of Market Videos (if not signed up yet you can do so via the link)

For now I hope you enjoy the discussion in Straight Talk: Bear Raid.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2RbGjqd Tyler Durden

Police Arrest 27 After Another Violent Protest In Portland Tyler Durden

Sat, 09/05/2020 – 14:35

Portland police made multiple arrests overnight on Friday during what one independent journalist described as a “violent Antifa riot”. Nearly 100 days have passed since the unrest started, and it looks like the seemingly professional class of demonstrators keeping the unrest alive aren’t slowing down at all.

The night after the suspect in a fatal shooting – a suspect who once described himself on camera as “100% Antifa” – was himself gunned down after pulling a gun on the cops who came to arrest him, violent rioters in Portland once again came out to attack federal property.

According to Reuters, police arrested 27 people, mostly on charges of interfering with law enforcement or disorderly conduct. Many were arrested for throwing projectiles at officers.

“Officers began to make targeted arrests and in some cases moved the crowd back and kept them out of the street,” according to a press released issued on Saturday.

Here’s a more in-depth description of the protest from the AP, which said a few hundred demonstrators participated. The demonstrators ultimately tried to target the Portland Police Association building.

A few hundred demonstrators had met at Kenton Park before making their way to the Portland Police Association building, where officers warned protesters to stay off the streets and private property. Those who refused could be subject to citation, arrest, the use of tear gas, crowd-control agents or impact munitions, police said.

Around midnight, police ran down the street, pushing protesters out of the area, knocking people down and arresting those who they say were not following orders — as some people were being detained, they were pinned to the ground and blood could be seen marking the pavement. Law enforcement officers used smoke devices and shot impact munitions and stun grenades while trying to get the crowd to disperse, The Oregonian reported.

The Portland Police Bureau issued a statement Saturday morning, saying some officers reported that rocks, a full beverage can and water bottles had been thrown at them, prompting police to declare the gathering an unlawful assembly.

Police said at one woman who was detained was bleeding from an abrasion on her head, and she was treated by medics at the scene before being transported by an ambulance. The Portland Police Bureau said she jumped out of the ambulance and ran away before it left the scene, however.

Most of those arrested were arrested on suspicion of interfering with a peace officer or disorderly conduct, police said.

Portland wasn’t alone: violence, vandalism and looting swept across Rochester and NYC last night, too.

But protesters claimed they had a right to keep coming out following the new revelations of the killing of Daniel Prude revealed on Wednesday, while President Trump signed a memo threatening to cut federal funding to “lawless” cities, including Portland, unless they bring the street violence under control.

And Ngo, the faithful chronicler of the unrest sweeping across the US since the killing of George Floyd, shared video of the latest round of protests from last night, including one scene where protesters nearly hit their “comrades” with thrown projectiles as they were being taken into custody.

Portland Police arrest antifa rioters overnight. One of them is crying. Their comrades continue throwing projectiles at police, nearly hitting those being arrested on the ground. #PortlandRiotspic.twitter.com/s2e5k5h7eX

One woman who was arrested at the “violent” protest reportedly escaped from an ambulance.

Based on known details released by @PortlandPolice, this appears to be the woman arrested at the violent antifa protest who escaped from the ambulance overnight. pic.twitter.com/FfCHRbGxix

And for all the ‘blue checks’ who insist on soliciting donations to “bail funds”, here’s where that money is going to.;

Breaking: Kevin Phomma was arrested by Portland Police after he allegedly attacked cops w/bear mace at an #antifa riot. His $33,000 bail was quickly paid.

We imagine they’ll be back again on Saturday, as the cycle of unrest continues and Democratic mayors move to “defy” President Trump over his threat to cut federal funding.

Finally, as we’ve said before, it’s important to remember that the violence we are seeing is in mostly white cities by mostly white people. Minneapolis is 19% black. Seattle is 7% black and Portland is 6% black. Kenosha is 10% black and close to 80% white. Even LA, which has a larger population of blacks, hasn’t seen riots erupt like Portland, even after the city suffered yet another police shooting of a black man.

via ZeroHedge News https://ift.tt/326O9Yt Tyler Durden

If you think that price inflation runs at about 1.6% you have fallen for the BLS’s CPI myth. Two independent analysts using different methods — the Chapwood Index and Shadowstats.com – prove that prices are rising at a far faster rate, more like 10% annually and have been doing so since 2010.

This article discusses the consequences of price inflation suppression, particularly in the light of Jerome Powell’s Jackson Hole speech when he downgraded the importance of price inflation in the Fed’s policy objectives in favour of targeting employment.

It concludes that the reconciliation between the BLS CPI figure and the true rate of price inflation is inevitable and will be catastrophic for the Fed’s policy of suppressing interest rates, its maximisation of the “wealth effect” of inflated financial asset prices, and for the dollar itself.

Monetary inflation takes off

Last week saw a virtual Jackson Hole conference, where Jerome Powell downgraded inflation targeting in favour of the other Fed mandate, employment. And Andrew Bailey, Governor of the Bank of England, claimed “We are not out of firepower by any means…. to be honest it looks from today’s vantage point that we were too cautious about our remaining firepower pre-Covid”.

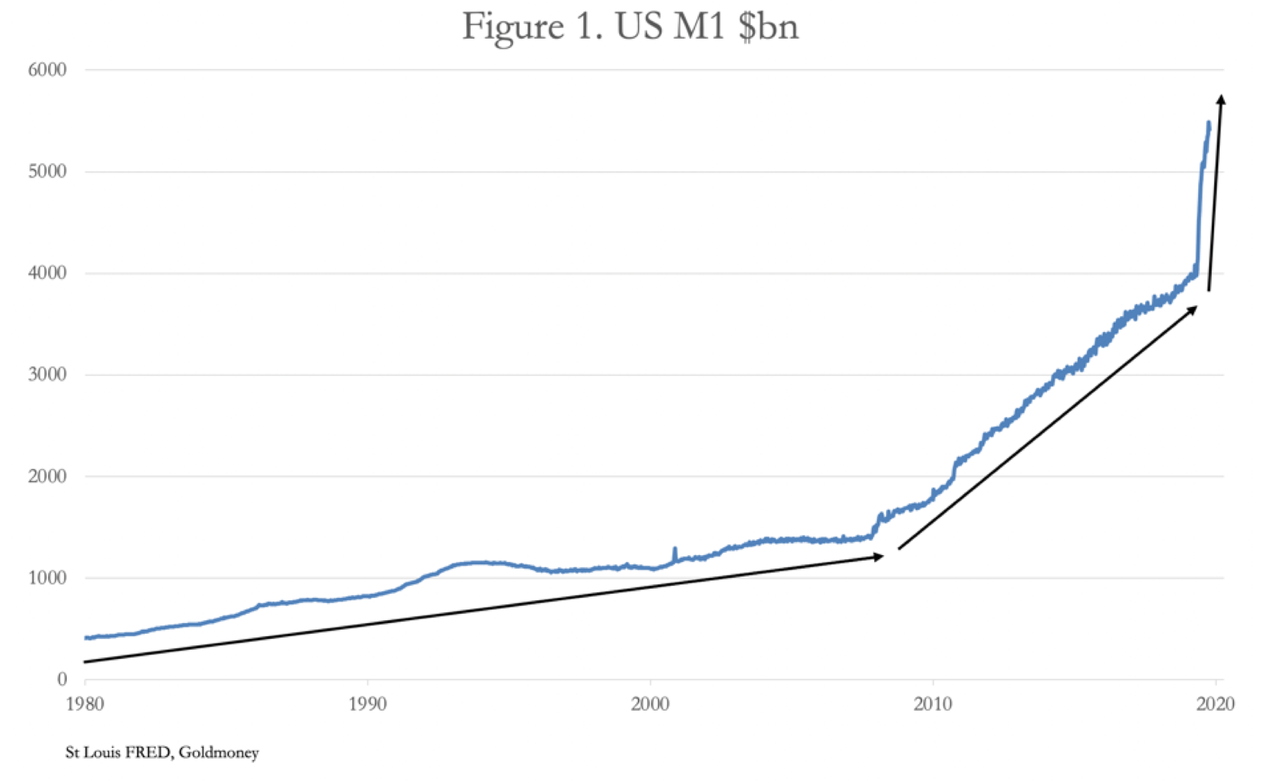

Both men were tearing up earlier scripts. Since they will likely tear up these as well there is little point in examining them further. For the fact is that all the major central banks are trapped in problems of their own making, and some time ago they lost control of their destinies. Figure 1 below encapsulates the problem.

M1 is the US narrow money indicator. Over 28 years from 1980, it grew at a simple average annual rate of 8.8% per annum. From 2008 to last February, following the Lehman crisis it grew at an average annual rate of 16.6%, From 24 February in six months it has grown by 34%, which is an average annual rate of 68%. What Powell effectively admitted at Jackson Hole was that M1 annualised growth of 68% was not enough to ensure the US economy would recover. He would have had to downplay the effect on prices to create leeway for further increases in the rate of monetary growth.

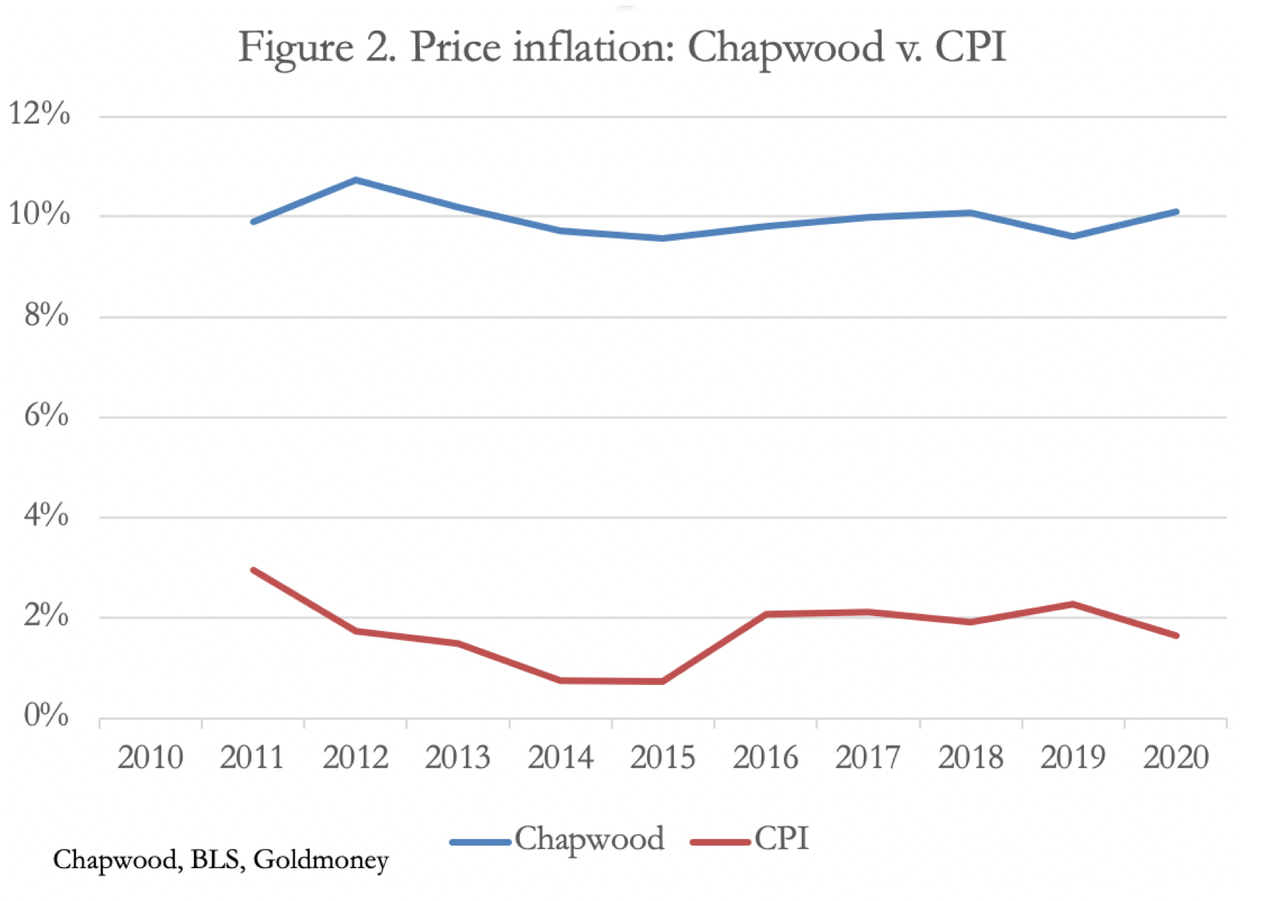

The Fed is evidently trapped by its inflationary policies. And the US Bureau of Labour Statistics, which calculates US consumer price indices, will have to work even harder to suppress the evidence of price inflation. Over the last ten years they have recorded an average annual rate of price inflation of 1.69% measured for US cities (CPI-U), and for the first half of 2020 they say it was 0.83%, or 1.66% annualised. To maintain this fiction has been a remarkable feat of statistical management, when compared with the unadulterated fifty city figures collected by the Chapwood Index.[i] Figure 2 shows the gap between the BLS’s CPI and Chapwood’s unadulterated estimates.

It is not our purpose to imply that the Chapwood Index of prices is an accurate representation of price inflation. We can talk about the general level of prices in a theoretical sense, but in practice it cannot be measured because each consumer has a different price experience. It is only when one subscribes to the macroeconomics version of economics and talk of unworldly aggregates that a figure is calculated. But if you remove the changes in the BLS’s calculation methods since 1980, you end up with a similar rate of price inflation to that of the Chapwood index, which is confirmed by John Williams at Shadowstats.com.

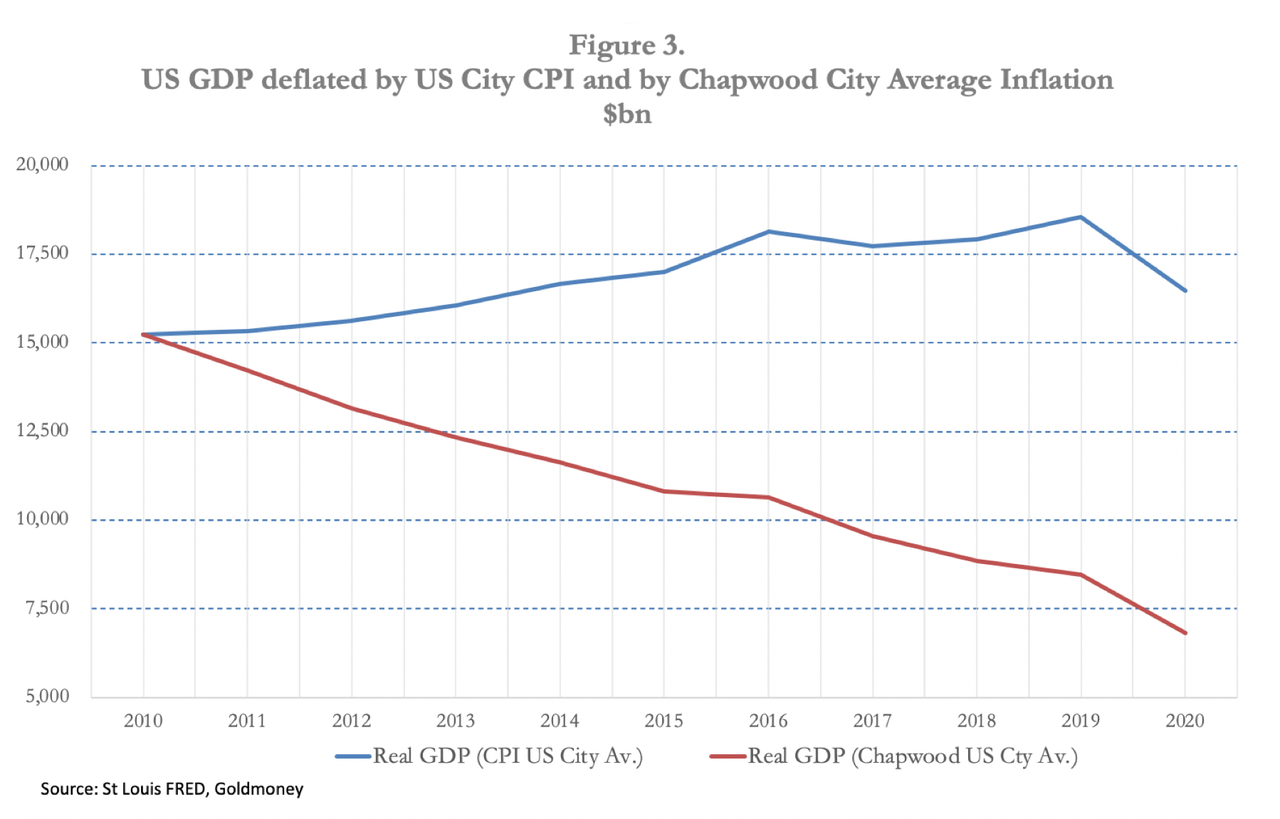

Now let us reconsider Jay Powell’s and Andrew Bailey’s Jackson Hole speeches in this light. Instead of an average rate of annual price inflation over the last ten years of 1.69%, Chapwood tells us that that average is 10.1%, varying between 13.4% in Sacramento and 7.1% in Albuquerque. It is against this background that Powell proposes to downgrade the Fed’s inflation mandate. Given M1 monetary inflation averaged 16% between the Lehman crisis and last February (see Figure 1) the price effect recorded by Chapwood is not surprising. But it gets worse for Powell. If we accept Chapwood’s numbers as being realistic and use them to deflate nominal GDP, we can see that the US economy has been in a slump for the last ten years: adjusted GDP has contracted by 65% since 2010. This is illustrated in Figure 3.

The only offset is the Fed’s much vaunted wealth effect that comes from speculating in financial assets. But that relief is only available to American investors and those employed in financial and related services, disadvantaging the poor and unemployed who inhabit Main Street, the non-financial economy. It is in this context, perhaps, that we should view the current civil unrest and racial strife in America.

Waking up to reality

Nobody in the investment and media mainstreams, let alone at the Fed, appears to understand the extent of statistical distortions and the consequences. We can count them all, including economics professors and senior figures in the investment game, among the 999,999 out of the proverbial million who don’t understand money and the consequences of its debasement.

The other side of the slump in real GDP illustrated in Figure 3 is the transfer of wealth from producers and consumers in the non-financial economy. If, as implied by a Chapwood GDP deflator, GDP has declined by 65% in real terms since the Lehman crisis, then we can say that gives us an approximation of the net wealth transfer through monetary inflation from producers and consumers to the state, the Fed, the commercial banks and their favoured customers.

If macroeconomists think that inflation stimulates demand, apart from initial artificial and final catastrophic effects perhaps, they are wrong: it kills it. The element of monetary debasement that ends up in government hands, taken from the productive non-financial sector along with all taxes, is wasted because a government produces little more than interference with an otherwise working economy. The true purpose of monetary inflation is not to improve our lives but to finance government deficits.

The element of bank credit inflation which ends up with the banking system’s favoured customers, comprised mainly of the large lumbering zombie corporations of yesteryear, disadvantages the more dynamic entrepreneurial businesses among the small and medium size sectors to the extent they are denied similar credit terms. The element of monetary inflation that ends up fuelling speculation in the financial economy is robbed from the liquidity balances and earnings of producers and consumers without their knowledge or consent. Monetary inflation is virtually impossible for the robbed to detect, not being revealed by accounting methods.

Despite M1 money supply accelerating, deflation remains a common fear, prompted doubtless by commercial banks being reluctant to extend credit at a time of increasing loan risk. But the Fed is already concerned that the commercial banks will not pass on its monetary policies, which is why it is bypassing them by buying corporate bonds and commercial mortgage backed securities through BlackRock. Other similar schemes are sure to follow. But it always amounts to supporting yesterday’s businesses, which the markets would otherwise likely judge to be today’s failures.

Clearly, any tendency for bank credit to contract will be countered by the Fed through further and appropriately aggressive expansion of narrow money, for which Powell was clearing the decks at Jackson Hole. It could lead to an even faster rate of M1 growth than the annualised 68% since February. Those who worry about the deflation of bank credit are therefore premature in their analysis and obviously believe in monetary inflation as an economic cure-all. But in real terms the US economy is already contracting because monetary inflation is leading to far faster price rises than is generally realised. Monetary inflation as a policy was only going to make things worse.

It is also a myth that monetary inflation is helpful to businesses. While an artificial and temporary cheapening of domestic manufacturing costs is lauded by neo-Keynesians, businesses need monetary stability in order to calculate the value of future payments: a healthy economy depends on business calculation which relies on the certainty of price stability. It is not good enough to say that suppressing interest rates benefit businesses: it is only true for over-indebted zombie businesses which with state aid can survive a little longer. But that is an artificial boost in their fortunes at the expense of a hidden inflation tax on everyone else. Not only does inflation coupled with the suppression of interest rates promote and sustain these commercial failures, but by doing so it also restricts the redistribution of all forms of capital into more productive use.

If the effects of monetary inflation become apparent to actors in the non-financial economy, they begin a process of reducing their monetary liquidity, knowing that money will buy less in the future than at the present. Until now, economic actors appear to place greater credence in the BLS’s inflation figures than from their own experience; but that cannot last. When the effect on prices of an annualised expansion of narrow M1 money of 68% becomes apparent it is likely to undermine widespread complacency. And when people realise that the general level of prices is rising despite the slump in economic activity, they will begin to dump all forms of dollar liquidity they possess in return for goods, driving price inflation even higher than increased money quantities would suggest. The transition from the false stability of prices as measured by government statistics into a final crack-up boom when money is dumped as worthless need not take long: all it needs is a trigger.

Shutting our eyes to this reality is nonsensical. The BLS’s CPI figures will prove to be defined by a vulgarity suggested by its own acronym. And when markets rumble it, the Fed will be unable to contain US Treasury yields at anything like current low levels. If we take the Chapwood price inflation figures for this year, then the current yield on the 10-year US Treasury bond is minus 9.45%, which must be close to a record in the annals of US monetary history.

Let us assume, for a moment, that financial markets adjust to price inflation rates closer to the Chapwood figures, which have already accelerated from an annual average of 9.6% for 2019 to 10.1% in the first half of 2020. US Treasury yields would initially rise at the short end of the curve to reflect that figure, perhaps with a margin over it. With the government’s budget deficit sure to exceed $3 trillion in the current fiscal year (to October) and perhaps double that next, the 2019 interest bill of $383bn on existing debt and the higher rate for US Treasury bond roll-overs plus the interest on new debt, total annual funding costs are likely to rapidly approach a trillion dollars . It is a debt trap sprung firmly shut and investors will take that into account.

An out of control budget deficit will continue to be funded through quantitative easing — there’s no other way. But a rise in bond yields will also have a catastrophic effect on equities, on their valuations as financial assets, on the cost of new and rolled-over corporate debt, and on valuations for loan collateral. The much-vaunted wealth effect, which has concealed the collapse in real GDP since the Lehman crisis, will quickly evaporate. Because the Fed has gone all in on using monetary inflation to sustain a financial bubble, it has also tied the dollar’s future to it, so its bursting is bound to have a profoundly negative effect on the dollar’s purchasing power.

The inflation problem is about to get worse

We have now established that the Fed is committed to accelerating the increase in the money quantity. We have also established that its monetary policies combined with statistical price manipulation has had the opposite effect of that intended, so much so that since the Lehman crisis the US economy has contracted in real terms by more than half, which any competent sociologist will tell you leads to civil unrest — plainly evidenced today.

We have reached a high point in macroeconomic madness.

It’s about to get worse.

Despite the post-Lehman acceleration of money supply, last September the repo market blew up on the day when Deutsche Bank sold its prime brokerage to BNP, the French global systemically important bank — a G-SIB. It may or may not have been the trigger for ongoing problems in the repo market, but clearly, there were liquidity issues in the US’s financial and banking system at that time.

It came on top of last year’s contraction in international trade, due in large measure to trade tensions between America and China with knock-on effects for China’s trading partners, such as Germany. Non-banks, principally insurance companies, pension funds and hedge funds acting directly or through agencies had accumulated large positions in fx swaps, ripping out interest differentials between euros and yen on one side, and a rising dollar on the other. The G-SIBs, particularly JPMorgan, had no excess reserves available to finance further non-bank speculation in this market. The turn of the cycle of bank credit expansion was upon us due to these liquidity issues, instead of the normal end of cycle problem of over-geared bank balance sheets facing escalating lending risk. However, thanks to covid-19 lending risk is now rising rapidly.

The S&P500 index crashed by fully one-third between mid-February and 23 March, as institutional investors suddenly realised the deflationary consequences of liquidity shortages in the banking system. It took the Fed’s cut in its funds rate from 1% to 0% on 16 March and its statement on 23 March, when it promised new QE and infinite monetary support for businesses and households, to relieve the liquidity problem.

At the same time came the covid-19 lockdowns. China had imposed lockdowns in Hubei Province in January, but from early March the rest of the world started to go into lockdown, with the UK going into lockdown on 23 March. In the US a number of states announced lockdowns from 17 March, with New York locking down on 22 March. The Fed’s actions, cutting its funds rate on 16 March and announcing infinite QE on 23 March were both timely and a financial watershed.

In all the mayhem of lockdowns it is easy to forget that the collapse of overnight liquidity was already a six-month old evolving crisis, marking a cyclical turning point in the expansion of bank credit. Unlike Lehman, which reflected a cycle of excessive property speculation, this one has its roots in a downturn in global and now domestic trade, as well as a global currency imbalance in favour of the dollar. According to US Treasury TIC figures, at end-June 2019, which are the most recent available estimates, foreigners owned $20,534 bn of US securities. To this must be added bills and cash, which on the most recent TIC report (June 2020) totalled a further $6,227 bn. Therefore, putting to one side the different dates of record and higher equity valuations today, foreign ownership of dollars is roughly $27 trillion, which equates to 125% of US GDP in 2019.

Foreign ownership amounts to such a large figure relative to GDP due to the dollar’s reserve status, foreign participation in funding US budget deficits and anticipation of an expansion of future trade. But as we have seen, global trade began to contract in 2019, which if continued, reduces the need to hold dollars. And we can be certain that if foreign holders take the view that the US economy is in a slump, beyond their requirements for marginal liquidity there is no reason for them to hold dollars at all because they can always buy them when actually needed.

Consequently, the US is vulnerable to foreign liquidation of securities, comprised of US Treasuries and other bonds, together with portfolio investments amounting to 20% of total US long-term securities extant.[v] So far, on a net basis foreigners appear to have stopped or slowed their net buying of US securities and cash dollars. Some positions will have been unwound by US hedge funds and other entities operating in the fx swap market rather than foreigners, driving the dollar’s trade weighted lower by about ten per cent so far from its 23 March high. But foreigners appear to have not yet began to sell dollars in meaningful quantities. When they do, they will be selling US Treasury and corporate bonds and liquidating equity portfolios as well. And if they do so at a time when there are insufficient domestic buyers to absorb their selling, these markets will crash along the dollar, which will be sold as well.

In the short-term, the course of financial asset prices and of the dollar’s exchange value will in large measure be determined by non-Americans. [As a side note, the last time a currency and financial assets became so intertwined was in the Mississippi bubble. The Irish-French banker, Richard Cantillon, made his second fortune in the latter part of 1719 by shorting the livre currency before the peak in the shares in late-February 1720. A similar pattern could be emerging today in the relationship between fiat money and financial assets, with the dollar weakening before US financial assets][vi]

Pricking the bubble

We know that the two versions of price inflation, that of the BLS and Chapwood (which accords with Shadowstats) are far apart. The finance sector is pricing financial assets on the basis of the BLS’s CPI and therefore accepts the Fed’s monetary policy of keeping short-term interest rates close to the zero bound. But rising prices for metallic money, gold and silver, indicate that the policies of suppressing apparent price inflation and interest rates are running into trouble.

We know, therefore, that the financial asset bubble itself is on a last hurrah, and its imploding deflation, driven initially perhaps by a resolving of the tension between the BLS’s CPI and the true rate of price inflation, is only a matter of time. We can identify a few key reasons likely to trigger the bursting of the financial asset bubble:

A growing realisation that the covid-19 shutdowns are additional to the credit cycle and liquidity problems that surfaced in September 2019 and that a post-covid-19 recovery will be followed by a deeper and more intractable slump.

Liquidity problems in the banking system and for its non-financial customers, together with the escalation of bad debts are leading towards bank failures. Fortunately, US banks are generally less leveraged than those elsewhere. But Eurozone, Japanese, Chinese and some UK G-SIB banks pose exceptional systemic risks, making their continued survival as independent commercial banks unlikely beyond the near term.

Foreign selling of US financial assets and the repatriation of their funds.

The first two bullet points will simply guarantee a further escalation in the rate of monetary inflation as the partnership of central banks and state treasury departments desperately attempt to contain a deteriorating situation. But foreign repatriation of funds will hit the dollar hardest, making it lose purchasing power against other currencies as financial asset values collapse. The euro, yen and Chinese yuan will appear perversely strong for a brief period, with their central banks desperate to contain the rises in their own currencies in the belief they are deflationary.

The sheer scale of dollar inflation will also mean that global commodity and raw material prices will rise, signalling that the dollar’s purchasing power is falling.

Empirical evidence in these situations indicates that an inflating currency is hit first in the foreign exchanges, before the domestic population discovers what is happening to their money. There is then followed by a growing panic among domestic users to dump money. In the best documented monetary collapses, such as Germany’s of 1923, cash was increasingly demanded in order to be spent as soon as possible, and evidence from Venezuela suggests this is still true today. However, more sophisticated financial systems have eliminated cash for most transactions, replacing it with credit and debit cards as well as other forms of electronic money. Internet banking and shopping further speeds up the process of turning money into goods.

This has the effect of speeding up the spending process significantly, leading to a more rapid loss of purchasing power compared with a currency whose users first make a trip to their bank to encash their deposits before heading for the shops. Additionally, a generation of cryptocurrency-savvy millennials have been forewarned of the consequences of fiat money inflation and stand prepared to ditch currencies earlier than their equivalents would have been in the past.

Taking these factors into account, the collapse in purchasing power of a currency which has been deployed to save financial assets and failed, once the general public finally understands the consequences, will likely be surprisingly rapid. In 1923 Germany, the final collapse took roughly six months. In 2020 America it could take as little as a few weeks.

Other currencies that refer to the dollar for their relative values are sure to suffer the same fate, not helped by the fact that their central banks have been pursuing similar monetary policies and will likely cooperate with each other to the bitter end.

via ZeroHedge News https://ift.tt/3buqjc0 Tyler Durden

Consumer Reports Slams Tesla’s $8,000 Full Self Driving Vaporware In Scathing New Review Tyler Durden

Sat, 09/05/2020 – 13:45

Tesla’s full self driving (FSD) concept has been at the intersection of a textbook case study in selling vaporware mixed with a poignant statement about the gullibility of Tesla consumers all wrapped up in a commentary about how regulators, both in the world of public securities and highway safety, have become irrelevant.

In short, it’s a product that doesn’t exist.

Tesla has been collecting $8,000 for something called “Full-Self Driving” based on the promise that the car will be able to drive itself, 24/7/365, at some point in the future. But for now, those putting down deposits for the future promises have been left with a series of unimpressive features like Autopilot, which have become an industry standard (i.e. lane assist, parking assist) with other major auto manufacturers.

In some cases, people who were paying for FSD weren’t even getting the hardware they were being promised. And nobody has seemed to notice and/or care.

Until now.

Consumer Reports released a scathing article on Friday, noting what many of us have been screaming from rooftops for years: “The $8,000 [full self driving] option doesn’t make the car self-driving”. CR says “consumers should be wary” about shelling out the money for a product that doesn’t exist:

The features might be cutting edge, even cool, but we think buyers should be wary of shelling out $8,000 for what electric car company Tesla calls its Full Self-Driving Capability option.

Tesla claims every new vehicle it builds includes all the hardware necessary to be fully autonomous, and the company says that through future over-the-air software updates, its cars should eventually be capable of driving themselves.

But for now, Full Self-Driving Capability, which includes features that can assist the driver with parking, changing lanes on the highway, and even coming to a complete halt at traffic lights and stop signs, remains a misnomer.

“Owners should not rely on Tesla’s driver assistance features to necessarily add safety or to make driving easier, based on Consumer Reports’ extensive testing and experience,” the article warns.

Jake Fisher, senior director of auto testing at Consumer Reports, said: “Despite the name, the Full Self-Driving Capability suite requires significant driver attention to ensure that these developing-technology features don’t introduce new safety risks to the driver, or other vehicles out on the road.”

He continued: “Not only that, in our evaluations we determined that several of the features don’t provide much in the way of real benefits to customers, despite the extremely high purchase price.”

“Most features within Tesla’s Full Self-Driving Capability suite worked inconsistently,” the report continues. Consumer Reports says of Autopark:

“Sometimes it would recognize a parking space as suitable, and we’d park in it. But when we drove by the same space again later, it was as if the parking spot didn’t exist. It also often didn’t park straight between the parking lines.”

The article also torched Tesla’s “Smart Summon”:

Smart Summon, which allows the car to drive remotely to a location within a private parking lot, would sometimes drive on the wrong side of parking lot driving lanes, and it didn’t always stop at stop signs in the lot.

The article also called Tesla’s “Navigate on Autopilot” inconsistent, stating the system would ignore exist ramps and drive in the carpool lane. Consumer Reports also said control around traffic lights and stop signs was dangerous: “At times, it also drove through stop signs, slammed on the brakes for yield signs even when the merge was clear, and stopped at every exit while going around a traffic circle,” the review read.

William Wallace, manager of safety policy for Consumer Reports, concluded: “Tesla has repeatedly rolled out crude beta features, some of which can put people’s safety at risk and shouldn’t be used anywhere but on a private test track or proving ground.”

We have to ask again: how long is the NHTSA going to allow this? We have documented a litany of accidents involving Tesla’s supposed “Full Self Driving”, the latest of which can be found here. How many more people have to die before regulators take notice?

Consumer Reports says Tesla did not respond when approached for comments and questions.

You can read the full article here and watch Consumer Reports’ full video review of FSD here:

via ZeroHedge News https://ift.tt/3588myJ Tyler Durden

India Passes 4 Million Cases, 300 Arrested At Melbourne Anti-Lockdown Protest: Live Updates Tyler Durden

Sat, 09/05/2020 – 13:20

Summary:

India passes 4 million cases

Aussie police arrest 300 people at Melbourne anti-lockdown protest

Mexico cases climb

Brazil still No. 2 highest case count with 4.09 million

Iraqi health care system on the brink as country suffers record spike in cases

Italy tries to stop soccer fans from returning to stadiums

* * *

As we noted just the other day, India is on the cusp of passing Brazil to become the country with the second-largest number of confirmed cases of COVID-19. It took yet another step closer late this week as it crossed the 4 million-case threshold.

Now the world’s new virus epicenter, having recorded more cases than any other country during the month of August, as India’s outbreak appeared to accelerate due to an ambitious government-sponsored mass-testing, India added 86,432 infections in 24 hours, pushing the total tally to 4.02 million, according to data released by India’s health ministry Saturday. Over 69,500 people have died from the novel pathogen, making it the third-largest by number of Covid-19 deaths.

Brazil, on the other hand, has confirmed 4,091,801 infections while the United States has 6,200,186 confirmed cases, according to the data from Johns Hopkins University.

India’s health ministry on Saturday also reported 1,089 deaths for a total of 69,561.

The world’s second-most populous country imposed the world’s biggest lockdown as early as March, but began relaxing it in phases from June after millions of Indians were thrust into poverty, sparking a wave of social unrest that rattled the country’s population centers, before spreading throughout India’s vast countryside.

The virus has followed a similar pattern. The increased testing comes as India moves to loosen even more restrictions to try and revive its faltering economy. It’s widely expected that India will eventually surpass both Brazil and the US.

Some other important developments in the global COVID-19 pandemic occurred overnight:

Police in the Australian city of Melbourne arrested about 300 people protesting against the city’s ongoing coronavirus lockdown, which has endured despite showing minimal effectiveness in quashing the region’s still-relatively-tame outbreak. Victoria State, which includes Melbourne as its capital, Australia’s coronavirus hotspot said its death toll rose by 59 – though not all cases actually died over the past day – and there were 81 new cases. 50 of these deaths were people in aged-care facilities who died in July and August, the state health department said.

Mexico saw confirmed cases climbed to 623,090, while deaths reached 66,851.

Iraq has recorded its highest single-day rise in COVID-19 cases since the start of the pandemic, prompting authorities to warn hospitals might “lose control” as new serious cases overwhelm the region’s meager health-care resources, which are heavily centralized in hospitals.

According to the Iraqi health ministry, 5,036 new infections were confirmed within 24 hours on Friday, bringing the total number of cases across the country to 252,075. Of these, 7,359 have died.

The health ministry attributed the spike to recent “large gatherings” – many related to an important holiday in Shia Islam – that violated social distancing recommendations.

Italy’s government is lobbying against the return of football fans to stadiums as the number of newly reported cases begins to climb. Former prime minister Silvio Berlusconi is in a stable condition two days after being admitted to a nearby hospital with serious COVID-19 symptoms.

“This instils cautious but reasonable optimism,” said spokesman Alberto Zangrillo in a brief statement. Italy’s longest-serving postwar leader is 83.

Around the world, some 26.5 million people have been diagnosed with the virus, while another 872,000 have died. More than 17.6 million people have recovered.

New Jersey yesterday announced that its rate of transmission had popped back above “1”, meaning that the outbreak is spreading once again. Though this has happened several times since the last outbreak slowed.

via ZeroHedge News https://ift.tt/3gZNwUx Tyler Durden

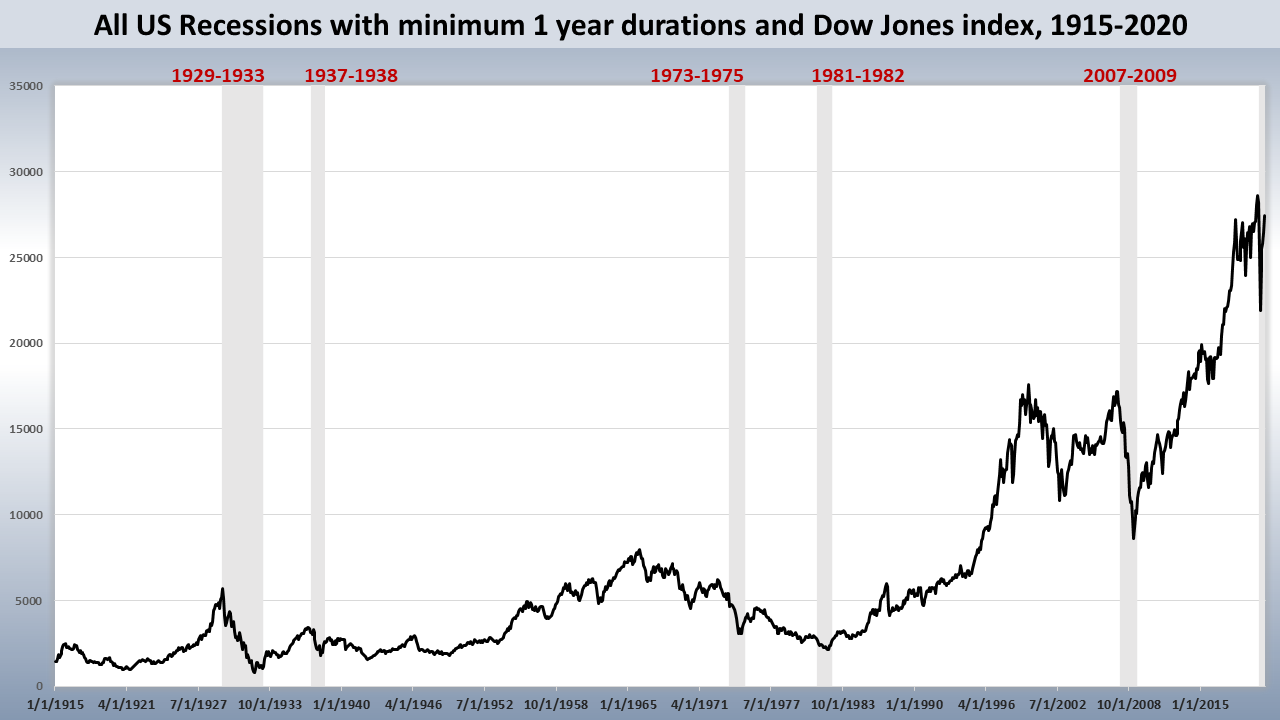

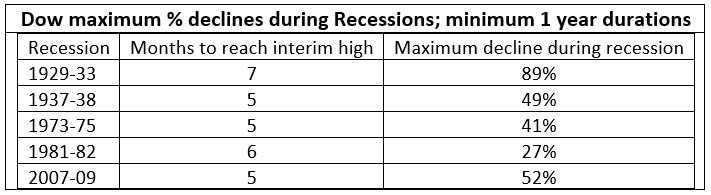

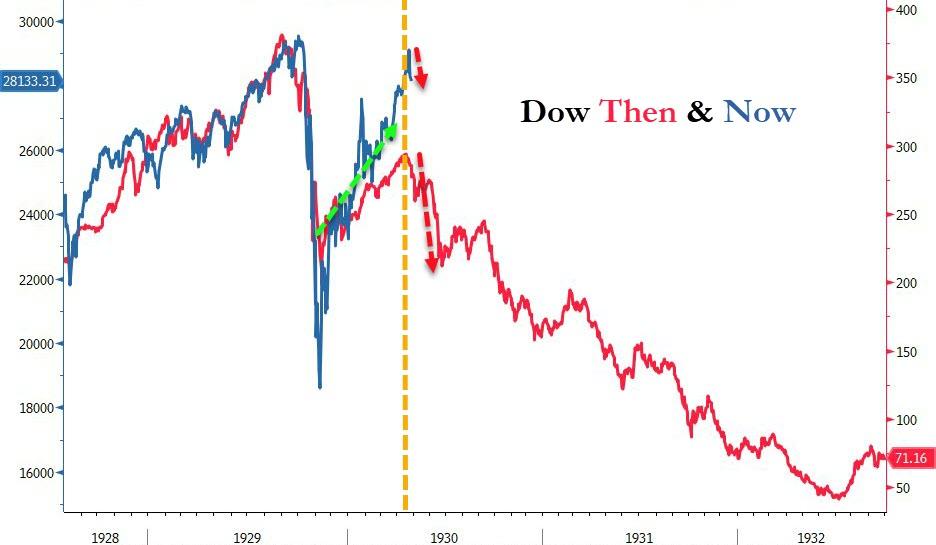

Based on new empirical research findings, the Dow Jones 30 (Dow) composite index is likely to soon peak. It will then begin a steady decline to new lows in 2020 or 2021.

According to the SCPA (Statistical Crash Probability Analyses) algorithm, the probability is 90% for the Dow to reach new lows before the current US recession ends. The algorithm’s forecast assumes that the 2020 recession will last until at least March of 2021.

The Forecast

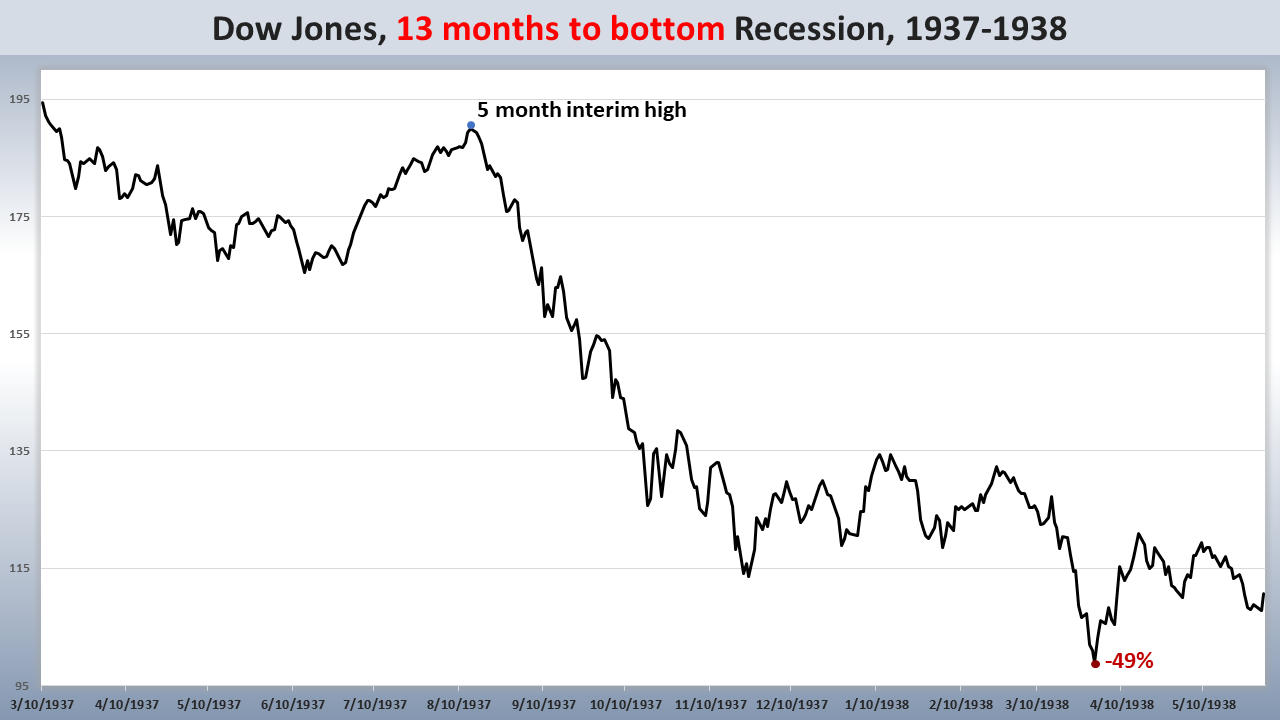

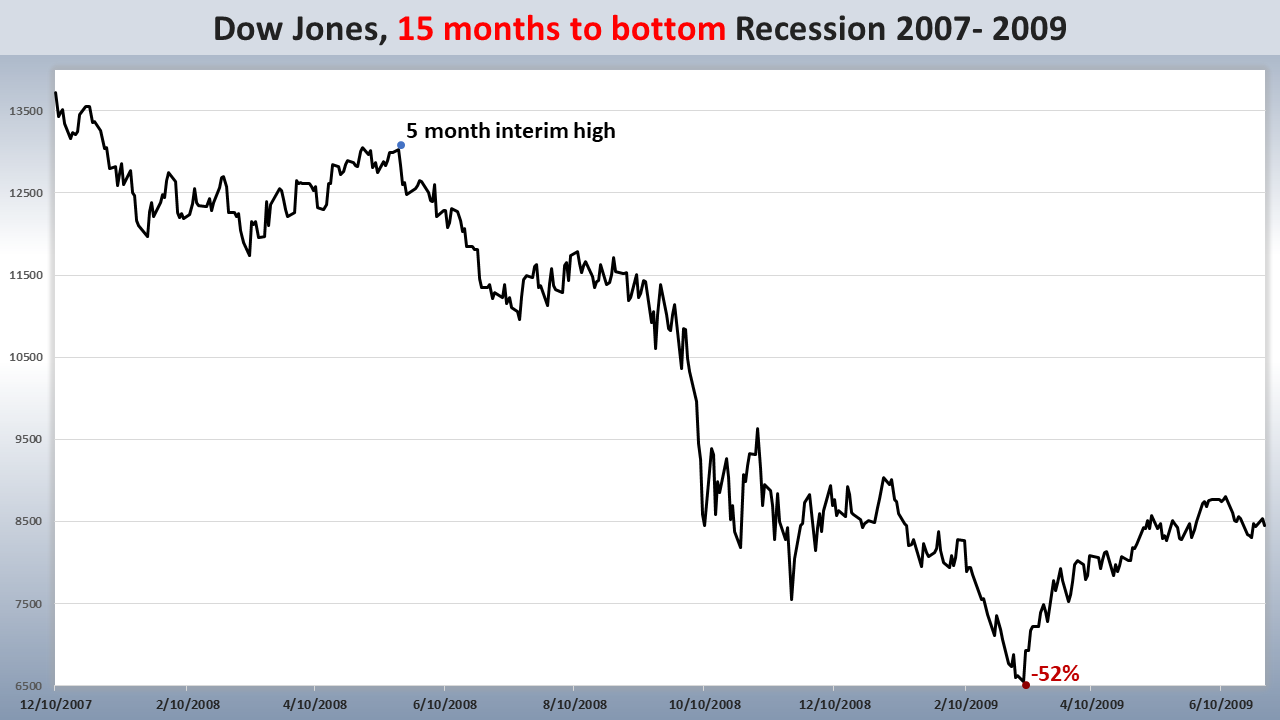

The forecast, based on SCPA research of the Dow’s performance during the five US recessions from 1929 to 2007. Each recession lasted a minimum of one year. The chart below depicts the five recessions.

The research findings revealed that the Dow:

initially declined after each of the five recessions began

rallied to interim highs within five to seven months after the recessions had begun

fell to new recession lows after reaching the temporary highs

The Charts

The five charts below break out the performance of the Dow for each of the recessions.

The chart below for the Dow Jones depicts that the index closed at its post-crash high on September 2, 2020.

The Probability

Based on SCPA, the probability is 100% for the Dow to have already reached its post-crash high, or by September 2020. Such will be the seventh month since the recession began. Coincidentally, the SCPA has forecasted the post-crash high to occur for a dozen other countries by September 18, 2020, as well.

Conclusion

The Dow’s big question for the recession of 2020 is will it last a minimum of one year? If the answer is yes, the SCPA’s probability is 90% for the Dow to pierce its March 23, 2020 low before the 2020 recession ends. The calculation of the 90% probability came from computing the average of the following:

As of the March 23 low, the Dow had declined by 36.5%. For four of the prior five (80%) recessions, the minimum decline ranged from 41% to 89% before the economic downturn concluded.

The Dow for all five (100%) of the prior recessions reached its recession low after the seventh month of the recession.

From the findings published on August 27, 2020, in “Probability of V-Shape Recovery Low, Depression High,” the probability is 99% for the current recession to last at least one year. The findings were comprised of Deloitte’s forecasts for the US economy from 2020 through 2025. The empirical data for the US economy dates back to 1929.

With the probability almost 100% for the Dow Jones composite index to reach a new low in 2020 or 2021, and before the recession ends, investors need to be defensive.

via ZeroHedge News https://ift.tt/358QIej Tyler Durden

Social unrest surged Saturday across Melbourne and Sydney, as hundreds of protesters took to the streets, defying arcane coronavirus lockdowns that have been in effect for nearly five weeks following a spike in virus cases and deaths.

Anti-lockdown groups gathered at the Shrine of Remembrance, a war memorial in Melbourne, Victoria, Australia, with some demonstrators wearing no masks, holding signs, and were heard chanting “freedom” and “human rights matter,” reported Reuters.

“It is not safe, it is not smart, it is not lawful. In fact, it is absolutely selfish for people to be out there protesting,” Victorian Premier Daniel Andrews told reporters after the demonstrations.

Dozens were arrested at the protests in Melbourne and Sydney; hundreds of others were issued violations for breaching the stay-at-home public health order.

“As a result of the protest, a police officer received lacerations to the head after being assaulted by an individual who was in attendance,” Victoria Police said in a statement.

The statement continued, “Our investigations into this protest will continue, and we expect to issue further fines once the identity of individuals has been confirmed.”

Australian Broadcasting Corporation (ABC) quoted one woman at the Shrine of Remembrance who said, “there’s no epidemic — it’s just a pretext to keep us in lockdown.”

Reuters reported several other protests in Sydney and one in Byron Bay in the state of New South Wales. All demonstrations were in breach of local restrictions on large gatherings, which prompted local police to respond with riot police units.

Lockdown anger has erupted with protesters violently clashing with the riot squad in wild scenes across the city. Police promised a swift and firm response, and they delivered, in a show of force rarely seen in Melbourne. https://t.co/AVvaWLotVs@paul_dowsley#7NEWSpic.twitter.com/A4bdaxR88v

Many anti-lockdown protesters were concerned that stay-at-home orders have become a form of control that restricts people from living their lives. Others were worried that the latest restrictions would result in a more profound decline in the economy.

“Our economy is going to crash because if we don’t start opening up borders and letting people have freedom of choice to do what they want to do, how are we going to exist?” one protester told ABC.

Australia officially entered a recession at the beginning of Sept., the first time in three decades, as deep economic scarring and soaring unemployment rate could result in a much slower recovery.

Tony Abbott, the former Australian prime minister, was heard Tues. (Sept. 1) as saying virus “hysteria” and draconian lockdowns are perpetuating the economic slowdown and have created a “something for nothing mindset” among younger generations living on furlough.

“Much of the media has indulged virus-hysteria with the occasional virus-linked death of a younger person highlighted to show that deadly threat isn’t confined to the very old or the already-very-sick or those exposed to massive viral loads,” Abbott said.

Abbott accused Andrews of being a ‘health dictator’ by placing five million Melburnians under “house arrest.” He said politicians need to stop acting like “trauma doctors” and start adopting the mindset of “health economists” – as reckless money printing to sustain the country’s economy during lockdowns isn’t sustainable.

“From a health perspective, this pandemic has been serious. From an economic perspective, it’s been disastrous,” he said.

So the question we ask readers is what could incite further unrest? Well, it could be mandatory coronavirus vaccinations.

This all comes just days after massive anti-lockdown protests in Germany. A backlash to the latest increase in restrictions in the US could be just around the corner.

via ZeroHedge News https://ift.tt/2F4J4H4 Tyler Durden