While Americans Sacrifice To Survive The Pandemic, CEO Compensation Has Barely Changed Tyler Durden

Sat, 08/08/2020 – 14:05

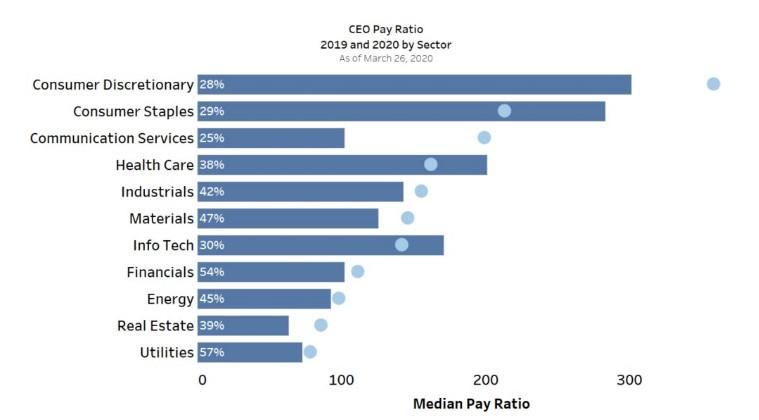

It looks as though we are in the midst of another recession where those in the C-suite are little affected; and in some cases where the Fed has stepped in, doing better than they were financially before the pandemic. And the “shared sacrifice” from most company’s CEOs – many of whom took pay cuts to show “solidarity” with employees – has actually been far less than imagined.

A new survey from the NY Times shows that out of 3,000 public companies, these cuts have come in the form of salary reductions that paled in comparison to CEO’s total pay, which is often made up of stock awards and bonuses.

It was “only a small percentage” of companies that even cut salaries for their senior executives to begin with, the Times notes. Among the ones who cut, about 66% of CEOs took reductions that were equivalent to only 10% or less of their total 2019 compensation. Companies in this group include Walt Disney Company, Delta Air Lines, United Airlines and Marriott International.

Companies last year paid executives an average of 264 times their median worker salary. It’s another example of how the pandemic has disproportionately affected the middle and lower class. The Fed’s response to the crisis, has also served as a monumental example of this.

Liz Shuler, secretary-treasurer of the A.F.L.-C.I.O. said: “These salary cuts were more window dressing than anything else.” Next on the chopping block this year would be bonuses and stock option awards, but it is unclear whether or not Board of Directors will implement such measures.

And not all CEOs have escaped major pay cuts. Glenn Kelman, CEO of Redfin, took a pay cut equivalent to $284,000, the Times reports. He said: “The reason we did it is because we had to furlough or lay off more than a thousand people. It’s not just about the pay cut; it’s about the general sense that capitalism is not working for everyone.”

Out of the 3,000 companies surveyed in the Russell index, 419 of them had disclosed details about salary cuts and only about 10% of those companies cut salaries by more than 25% of the executive’s total realized compensation.

United Airlines said its executives salaries were to “lead by example”, since the company will likely have to furlough 36,000 workers on October 1. The company’s executive chairman, Oscar Munoz, did not draw a salary between March 10 and June 30, amounting to a $610,000 pay cut – but it amounts for less than 3% of the $22.2 in total compensation he took home in 2019.

United’s new chief executive will forego about $790,000 in salary this year, which amounts to about 9% of the total compensation he received last year. United says it is “extremely unlikely” there will be bonuses paid in 2020.

Delta chief executive Ed Bastian took a salary cut of about $714,000, which amounts to about 5.35% of the compensation he received in 2019. The company is also asking its pilots to take pay cuts in order to keep their jobs.

Disney’s Robert Iger gave up his salary from the end of March until the end of 2020. The $2.25 million he is surrendering amounts to about 3.3% of what he earned in 2019.

Mariott, which has also been laying off and furloughing workers, saw its CEO take a salary cut that was less than 2% of the $66 million in total compensation he received in 2019.

Other companies simply deferred their salary payments instead of making cuts. GM, for example, deferred 30% of CEO Mary Barra’s salary. The deferrals will end on August 1 and executives will continue to defer 10% of their salaries going forward. The deferrals started in April and were supposed to last 6 months.

When the company was asked about why they ended early, they stated: “The business demanded that we conserve cash and it is recovering faster than we expected.”

Great, so we should expect nothing but blowout results from General Motors for the rest of the year.

via ZeroHedge News https://ift.tt/3a6iVmm Tyler Durden

Mass media throughout the western world are uncritically passing along a press release from the US intelligence community, because that’s what passes for journalism in a world where God is dead and everything is stupid.

The press release, from the Office of the Director of National Intelligence and authored by National Counterintelligence and Security Center Director William Evanina, claims that Russia wants Donald Trump to win re-election in November and is pushing to advance than goal, while China and Iran are doing the same with Joe Biden.

China

“We assess that China prefers that President Trump — whom Beijing sees as unpredictable — does not win reelection,” the press release reads. “China has been expanding its influence efforts ahead of November 2020 to shape the policy environment in the United States, pressure political figures it views as opposed to China’s interests, and deflect and counter criticism of China.”

Russia

“We assess that Russia is using a range of measures to primarily denigrate former Vice President Biden and what it sees as an anti-Russia ‘establishment,’” the press release claims. “Some Kremlin-linked actors are also seeking to boost President Trump’s candidacy on social media and Russian television.”

Iran

“We assess that Iran seeks to undermine U.S. democratic institutions, President Trump, and to divide the country in advance of the 2020 elections,” says the press release. “Iran’s efforts along these lines probably will focus on on-line influence, such as spreading disinformation on social media and recirculating anti-U.S. content. Tehran’s motivation to conduct such activities is, in part, driven by a perception that President Trump’s reelection would result in a continuation of U.S. pressure on Iran in an effort to foment regime change.”

Great, if Biden wins they’ll blame China and if Trump wins they’ll blame Russia

U.S. Intelligence: China Opposes Trump Reelection; Russia Works Against Biden https://t.co/6MwxGIUDgR

What this completely unsubstantiated narrative means, of course, is that no matter who wins in November America’s opaque government agencies will have already primed the nation for more dangerous escalations against countries which have resisted being absorbed into the blob of the US-centralized empire.

If Trump wins we can expect his administration to continue its escalations against Russia in retaliation for its 2020 “election interference”, and if Biden wins we can expect his cabinet of Obama administration holdovers to ramp up escalations against China in the same way while Joe mumbles to himself off to the side as his brain turns to chowder.

There is never a legitimate reason to believe any unproven claim made by unaccountable spook agencies about US-targeted governments, but even if everything in this press release were true it’s an incredibly stupid thing to care about. The influence that Russia, China or Iran could exert over public opinion in the United States is a tiny fraction of that which is exerted by the unaccountable US billionaire media every single day, which already has its own factions pushing for Biden over Trump and Trump over Biden. Adding some foreign social media operations into the mix would change literally nothing.

Secondly, as the press release itself acknowledges, the US is openly pushing regime change in Iran. It is already engaging in various acts of economic warfare against all three of the named governments, and it openly interfered in Russia’s elections in the nineties to a far greater extent than anything it has even accused Russia of doing. The US government’s own data shows that it is the very worst election meddler in the world by an extremely wide margin, which would make it a perfectly legitimate target for election interference by any nation on earth.

Lastly, the dumbest thing about believing foreign nations are interfering in American democracy is believing America has any democracy to interfere with. The integrity of US elections ranks dead last among all western democracies, public opinion is constantly manipulated by the media-owning plutocratic class which has a vested interest in maintaining the status quo which keeps them rich and powerful, and it’s a two-headed one party system where both corporate-owned parties advance the same establishment agendas.

Imagine believing that foreign leaders are looking at the dumpster fire that is the United States and thinking:

“I know how we can hurt them! We’ll sow division by saying mean things about their presidential candidates on social media!”

It’s the dumbest thing in the world.

Yet all the establishment narrative managers are jumping on this intelligence community press release as a real thing that we should all be excited about.

The fact that the left isn’t outraged and calling for immediate investigations into China & Iran interfering in our election to HURT Trump is proof that the Russia hoax was never actually about “election integrity”

If they didn’t have double standards they would have none at all

“If you want to know why Donald Trump will not confront Vladimir Putin about these allegations of bounties on U.S. soldiers — well there you go,” Rep. Swalwell says of the ODNI report on foriegn interference in the election. https://t.co/m3jDqjY290

All this hand-wringing and arm-waving about foreign interference on social media comes as social media itself makes policy changes to ensure that only western governments are allowed to conduct propaganda on its platforms, with Twitter instituting a new policy of labeling accounts from unabsorbed governments as “state-affiliated media” while placing no labels or restrictions on any accounts with extensive western government ties.

The overall message in all this is that only western government agencies and oligarchs may conduct propaganda on those who live in the US-centralized empire. It should enrage us all that these unaccountable abusers feel so entitled to insert their rapey fingers in our minds and manipulate how we think, act and vote that they get all chest-thumpy about the idea of anyone else getting a word in edgewise. They do this because they understand that whoever controls the narrative controls the world, and there is no amount of evil they won’t do to ensure that they continue to control the world.

The reason sociopaths are able to insert themselves so easily into positions of power and influence in human civilization is because highly manipulative people with no empathy quickly learn that society is dominated by narrative, while the rest of us do not understand this.

This must change before we will be able to create a healthy world.

* * *

Thanks for reading! The best way to get around the internet censors and make sure you see the stuff I publish is to subscribe to the mailing list for my website, which will get you an email notification for everything I publish. My work is entirely reader-supported, so if you enjoyed this piece please consider sharing it around, liking me on Facebook, following my antics on Twitter, throwing some money into my tip jar on Patreon or Paypal, purchasing some of my sweet merchandise, buying my books Rogue Nation: Psychonautical Adventures With Caitlin Johnstone and Woke: A Field Guide for Utopia Preppers. For more info on who I am, where I stand, and what I’m trying to do with this platform, click here. Everyone, racist platforms excluded, has my permission to republish, use or translate any part of this work (or anything else I’ve written) in any way they like free of charge.

“Huge Increase” – Americans Renouncing Citizenship Surges To Record Level Tyler Durden

Sat, 08/08/2020 – 13:15

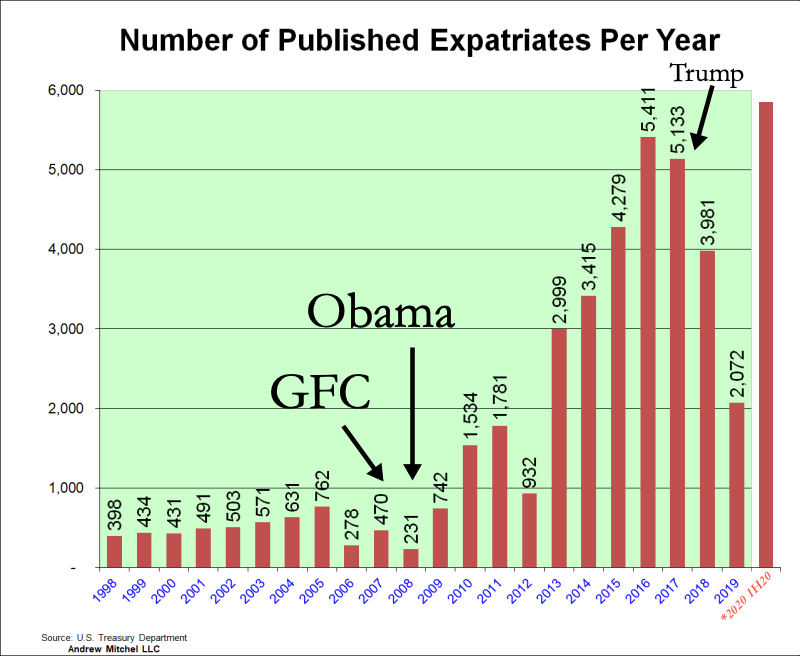

Readers may recall, for almost a decade, we have tracked a troubling trend of more and more Americans renouncing their citizenship. Now, amid a virus-pandemic, crashed economy, months of social unrest, and depressionary unemployment levels, that number has surged to a record high.

Bambridge Accountants New York notes 5,816 Americans renounced their citizenship in 1H20, a 1,210% increase over the prior six months ending in December 2019. In all of 2019, about 2,072 Americans gave up their citizenship.

“It seems that the pandemic has motivated U.S. ex-pats to cut ties and avoid the current political climate and onerous tax reporting,” said the New York-based accounting firm specializing in the U.S. ex-pat taxes.

Worldwide, there are an estimated 9 million U.S. ex-pats. Since the financial crisis, a decade ago, Americans giving up their citizenship has grown. In the last couple of years, the trend lost momentum. Still, as soon as the virus pandemic crashed the economy and triggered widespread social unrest, the number of folks leaving the country has gone parabolic.

After all, it makes perfect sense, who wants to be a citizen of a country that is imploding from within, where the federal government and Federal Reserve are clueless in solving the financial crisis, as officials continue to debase the dollar and bailout mega-corporations and Wall Street.

Has any other country spent a third of their GDP responding to Covid? What are we doing?

At the same time, the bottom 90% of folks are left in financial ruin. Deep economic scarring is developing, one where years of socio-economic crisis will plague the country. We noted last week the U.S. output gap as a percentage of GDP might not return to 2019 levels until 2030.

The financial crisis in 2008 triggered the first wave of Americans renouncing their citizenship. Then was supercharged during the Obama regime following his plan to raise taxes, “spread the wealth around,” and pursue a socialist agenda.

Then in 2016, celebrities threaten to leave the country if Donald Trump was elected. Many have since backtracked.

The number of expatriates peaked in 2016, then slumped from 2017-2019 as the Trump administration injected the economy with fiscal stimulus and sent the stock market to new highs, as it created a false sense of America economically roaring back to greatness.

Now the country is imploding. Smart Americans are getting the hell out of dodge, and they see what’s coming, or what has already transpired in 1H20. A socio-economic bomb exploded over failed liberal cities, police are being defunded, inner-city crime is erupting, and city-dwellers are fleeing for the countryside.

Keep in mind, we altered the chart below to realize 2020 figures on a 1H20 basis, as for full-year, the number could be enormous.

Alistair Bambridge, the partner at Bambridge Accountants New York, explains:

“The huge increase in U.S. ex-pats renouncing from our experience is that the current pandemic has allowed individuals the time to review their ties to the U.S. and decide that the current political climate and annual U.S. tax reporting is just too much to bear.”

So far this year readers have learned city-dwellers are fleeing metro areas for rural communities, now folks are denouncing citizenship at record numbers, all while the country implodes from within.

via ZeroHedge News https://ift.tt/2PDndYZ Tyler Durden

You may have noticed that a lot of people get offended by what I write. It is not something that I am purposely setting out to do, and I actually endeavor to get along with everyone as much as I can. But it is undeniable that my articles about our ongoing economic collapse directly contradict a lot of the narratives that are constantly being pushed by the mainstream media and many of our political, business and religious leaders.

There are so many people out there that want to believe that the future is going to be exceedingly bright, and even though 2020 has been a horrific economic catastrophe so far, there are a lot of optimists that believe that it is just a temporary blip on the road to tremendous prosperity.

It would actually be wonderful if they were right.

But they aren’t.

At this point, everyone should be able to clearly see that we have entered a new economic depression. And I wish that I could tell you that a “recovery” was right around the corner, but I can’t.

On Thursday, we got yet another sign that this downturn is here for the long haul. According to the Labor Department, approximately 1.2 million Americans filed new claims for unemployment benefits last week…

Four months after the COVID-19 pandemic largely shut down the economy and left millions of Americans out of work, employers continue to lay off workers at a historic pace.

About 1.2 million people last week filed initial applications for unemployment insurance – a rough measure of layoffs – the Labor Department said Thursday, down substantially from 1.4 million the previous week and the lowest level since March.

Initially, I thought that this was good news.

1.2 million is still a catastrophic number, but at least it appeared to be an improvement over last week’s level of 1.4 million.

Unfortunately, there is more to the story.

As Wolf Richter has pointed out, when you look at the unadjusted numbers and you include all state and federal programs, the number of continuing unemployment claims increased by a whopping 1.3 million last week…

The total number of people who continued to claim unemployment insurance under all state and federal unemployment programs jumped by 1.3 million from the prior week to 32.12 million (not seasonally adjusted), the Department of Labor reported this morning. It was the second highest ever.

That would seem to indicate that unemployment is dramatically surging, and that is really bad news for an economy that is already deeply suffering.

Overall, more than 55 million Americans have now filed initial claims for unemployment benefits over the past 20 weeks. That is a number that should be almost theoretically impossible, but this is actually happening.

Prior to this year, the all-time record for new unemployment claims in a single week was just 695,000, and now we have been above a million for 20 consecutive weeks.

Up until recently, a weekly $600 unemployment supplement from the federal government had been helping tens of millions of unemployed Americans pay their bills, but now that supplement has expired and Congress has not yet agreed to another one.

An unemployed makeup artist with two toddlers and a disabled husband needs help with food and rent. A hotel manager says his unemployment has deepened his anxiety and kept him awake at night. A dental hygienist, pregnant with her second child, is struggling to afford diapers and formula.

Around the country, across industries and occupations, millions of Americans thrown out of work because of the coronavirus are straining to afford the basics now that an extra $600 a week in federal unemployment benefits has expired.

Over the past couple of months, I have been hearing from a lot of people that believe that all of those unemployed workers should just get off their couches and go get new jobs.

I wish that it was that easy. Good jobs are becoming increasingly scarce, and the competition for those jobs is only going to get more fierce because a “second wave of layoffs” has now begun. The following comes from Fox Business…

A second wave of layoffs is hitting American workers during a surge in coronavirus cases nationwide, and a Congressional stalemate over stimulus relief, according to a new survey by Cornell University and RIWI.

The researchers conducted the survey between July 23 and Aug. 1, and found that 31% of workers who had been placed back on payrolls after initially being laid off have now been laid off for a second time. Additionally, 26% of rehired workers say they’ve been told that they may be laid off again.

I know that I included that quote in yesterday’s article, but I wanted to share it again because it is so important for people to understand what is really going on out there.

Millions of jobs that were lost in the first wave of layoffs are never coming back, and now millions of jobs that actually came back are being lost again.

In other words, instead of witnessing a “recovery” we are witnessing an “unraveling”.

I know that a lot of people don’t like when I talk like this.

But I am not here to make you feel good. I am here to tell you the truth.

We are in the midst of an economic nightmare, and even Bloomberg is admitting that conditions in the U.S. are becoming a lot more miserable…

The US is projected to undergo the biggest increase in economic misery across 60 countries as the nation grapples with heightened unemployment and fresh coronavirus hotspots.

Bloomberg’s Misery Index, which ranks major economies by inflation and unemployment expectations, shows the country sinking to rank 25 from rank 50 in 2020. Venezuela, Argentina, and South Africa held their spots as the world’s most miserable economies.

And every day more businesses are shutting down, more workers are being laid off and more dreams are being shattered.

The consequences of literally decades of incredibly foolish decisions are catching up with our nation, and this economic depression will ultimately get a whole lot worse.

So instead of sticking your head in the sand and hanging on to the delusion that everything is going to be just fine somehow, I would very much encourage you to work very hard to get prepared for the nightmarish years that are ahead of us.

via ZeroHedge News https://ift.tt/3kqOZX6 Tyler Durden

Post-Pandemic World: Homebuilder KB Homes Is Now Including Built-In Office Space In New Homes Tyler Durden

Sat, 08/08/2020 – 12:25

Capitalism is, once again, the solution.

At least that is the case with the housing industry which – like all other industries – is working to adapt to what life is going to be like in a post-pandemic world. For KB Homes, that means acknowledging that less people will be going into the office on a daily basis and including new, built-in offices in homes that they sell.

The KB Home Office, as it’s being called, is “is a dedicated room that delivers comfort, function and aesthetics,” the company said in a press release. “In this private workspace, homeowners can host online presentations or small in-person meetings and boost their productivity,” it continued.

In the press release, KB acknowledges that the shift to work-from-home inspired the new office concept: “The pandemic has served to accelerate the trend of working from home. During the past few months, Americans have accepted makeshift workstations despite challenges and frustrations, because they have been viewed as temporary. Now, as many companies shift to working remotely for the foreseeable future, and for some, perhaps permanently, homeowners are seeking to optimize their work-from-home experience.”

The new KB Home Office includes:

Built-in workstation with generous counter and cabinet space

Large open shelving for displays, books, files and other accessories

Upgraded electrical package, including receptacles, ultra-fast USB charging outlet and additional data/teleport

Jeffrey Mezger, Chairman, President and Chief Executive Officer of KB Home, commented: “Our homes have taken on even greater significance in our lives. Many people are now working from home, which has made home offices more desired and essential than ever before.”

He continued: “We have redesigned our floor plans to meet the needs of today’s homeowners and are pleased to offer the KB Home Office, a dedicated room our customers can easily personalize for the way they work, at a price that fits their budget.”

Homebuyers also have the option of personalizing the office by selecting different options available by the manufacturer. Options include enhanced soundproofing/insulation packages, tailored lighting, ceiling fans, window treatments and a beverage center.

The concept is set to be rolled out nationwide in coming months.

via ZeroHedge News https://ift.tt/3fKhPxL Tyler Durden

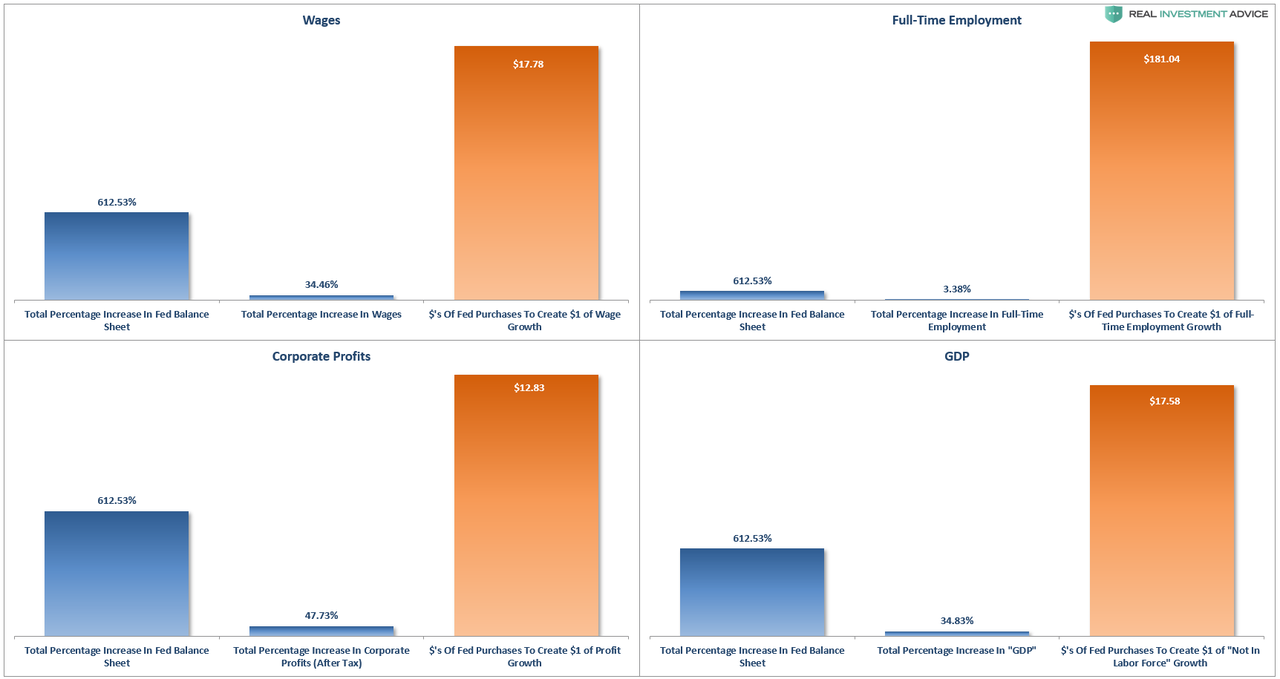

A recent CNBC article states the Fed will make a major commitment to ramping up inflation. How is this different than the past decade of promises for higher inflation? More importantly, while the Fed may want inflation, their very actions continue to be deflationary.

The Fed Has A Plan

“In the next few months, the Federal Reserve will be solidifying a policy outline that would commit it to low rates for years as it pursues an agenda of higher inflation and a return to the full employment picture that vanished as the coronavirus pandemic hit.

Recent statements from Fed officials and analysis from market veterans and economists point to a move to “average inflation” targeting in which inflation above the central bank’s usual 2% target would be tolerated and even desired.

To achieve that goal, officials would pledge not to raise interest rates until both the inflation and employment targets are hit.” – CNBC

Such certainly sounds familiar.

“The Federal Reserve took the historic step on Wednesday of setting an inflation target that brings the Fed in line with many of the world’s other major central banks.

In its first-ever ‘longer-run goals and policy strategy’ statement, the U.S. central bank said an inflation rate of 2 percent best aligned with its congressionally mandated goals of price stability and full employment.”– Reuters Reporting On Ben Bernanke’s Fed Policy Statement January 26, 2012

The Unseen

Over the last decade, the Federal Reserve has engaged in never-ending “emergency measures” to support asset markets and the economy. The stated goal was, and remains, such actions would foster full employment and price stability. There has been little evidence of success.

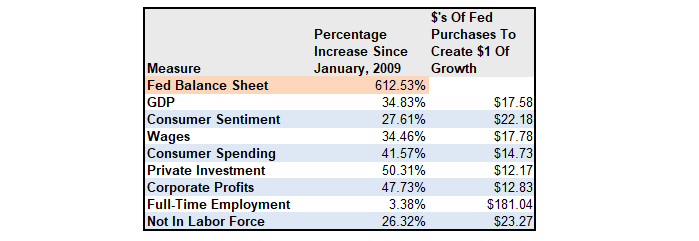

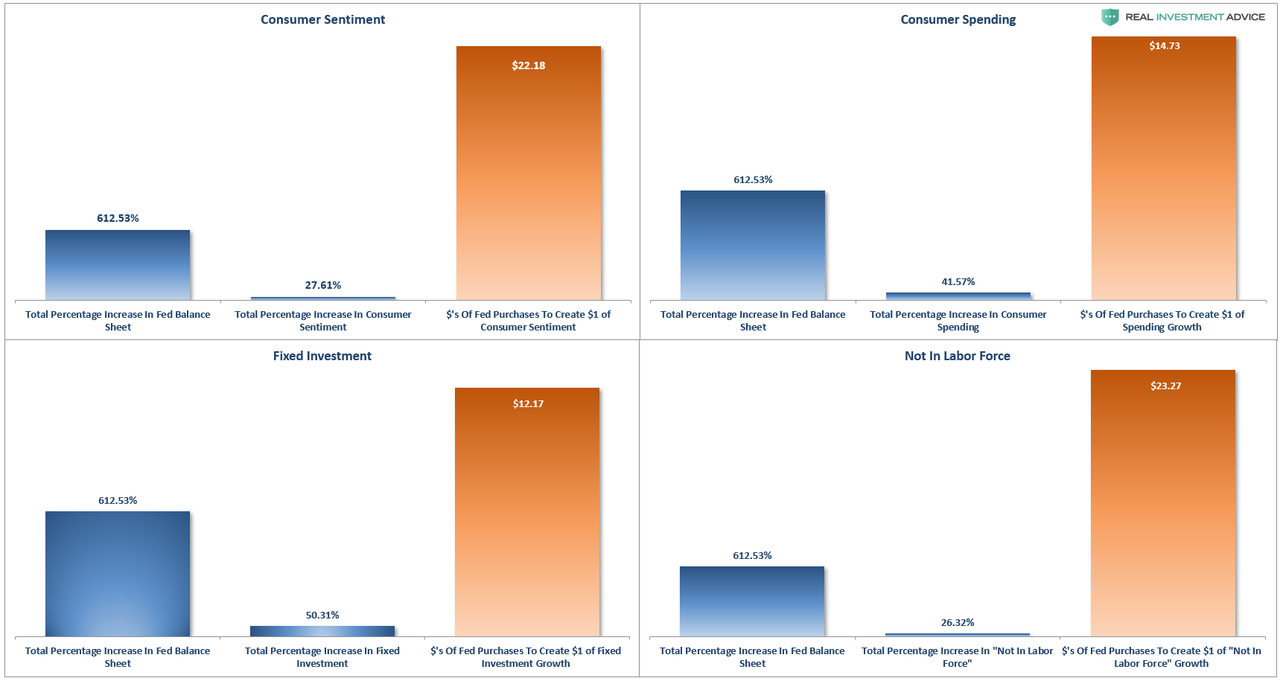

The table and charts below show the Fed’s balance sheet’s expansion and its effective “return on investment” on various aspects of the economy. For example, since 2009, the Fed has expanded its balance sheet by 612%. During that time, the cumulative total growth in GDP (through Q2-2020) was just 34.83%. In effect, it required $17.58 for every $1 of economic growth. We have applied that same measure across various economic metrics.

No matter how you analyze it, the “effective ROI” has been lousy.

These are the unseen consequences of the Fed’s monetary policies.

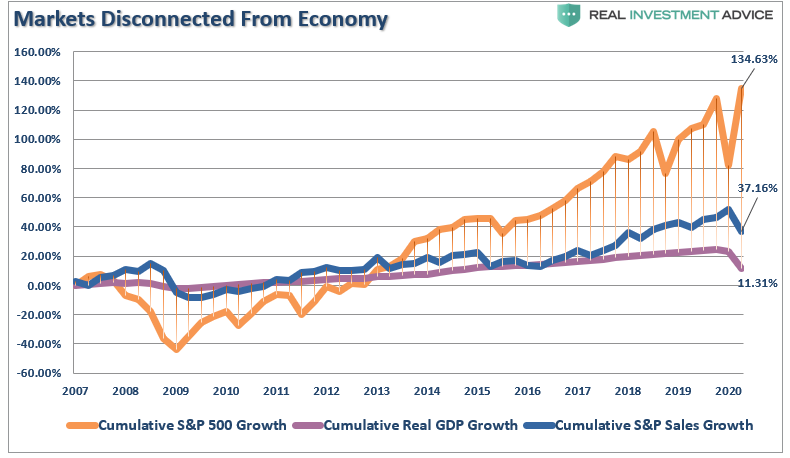

The Seen

The only reason Central Bank liquidity “seems” to be a success is when viewed through the lens of the stock market. Through the end of the Q2-2020, using quarterly data, the stock market has returned almost 135% from the 2007 peak. Such is more than 12x the growth in GDP and 3.6x the increase in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not AS subject to manipulation.)

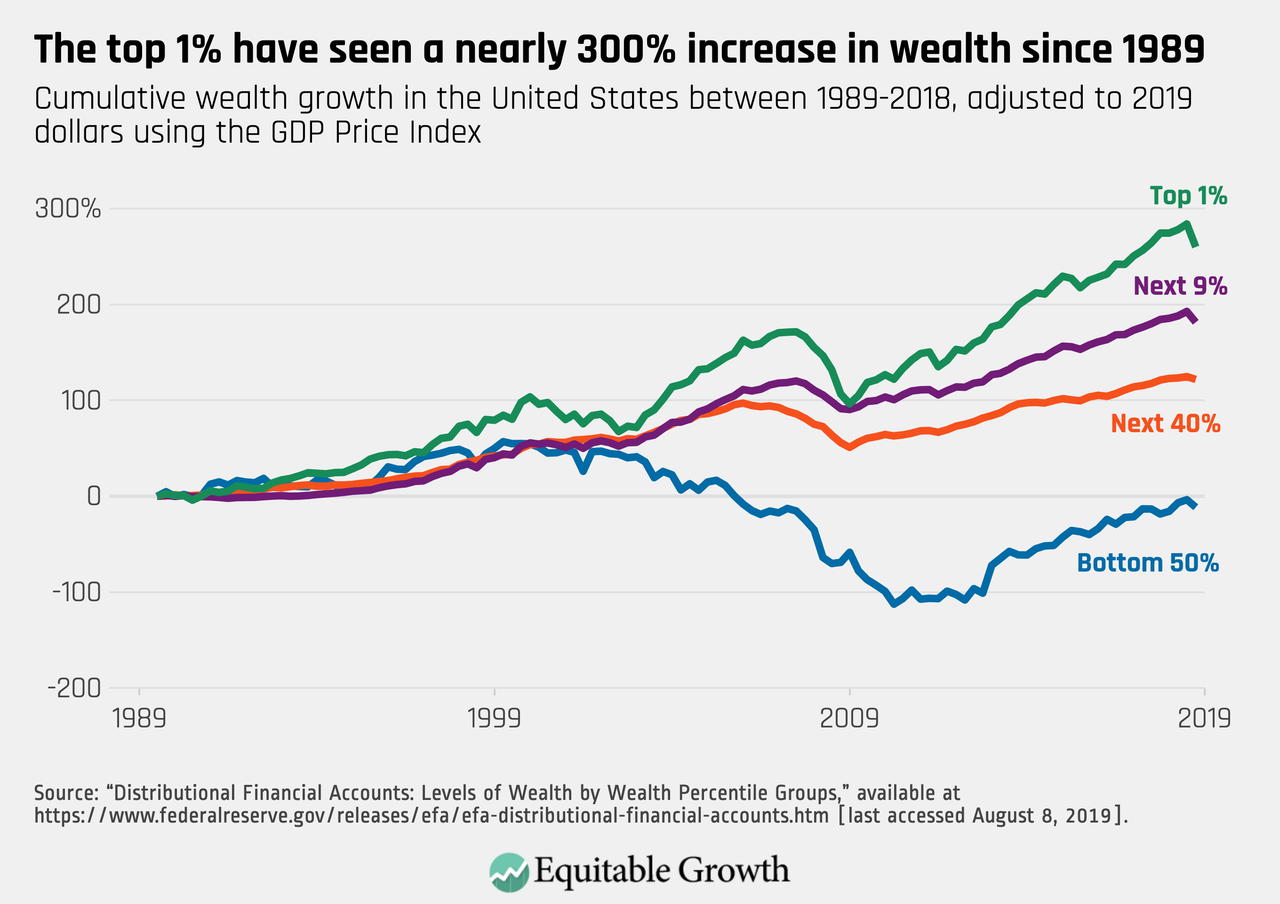

Unfortunately, the “wealth effect” impact has only benefited a relatively small percentage of the overall economy. Currently, the Top 10% of income earners own nearly 87% of the stock market. The rest are just struggling to make ends meet.

While in the short-term ongoing monetary interventions may appear to be “risk-free,” in the longer-term, the Fed has now reached the “end game” of monetary policy.

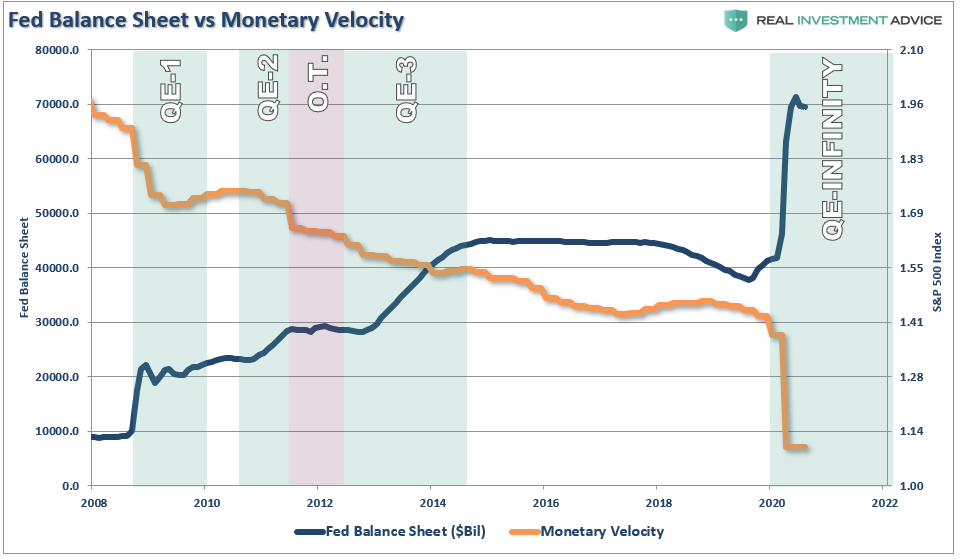

Fed’s Actions Are Deflationary

What the Federal Reserve has failed to grasp is that monetary policy is “deflationary” when “debt” is required to fund it.

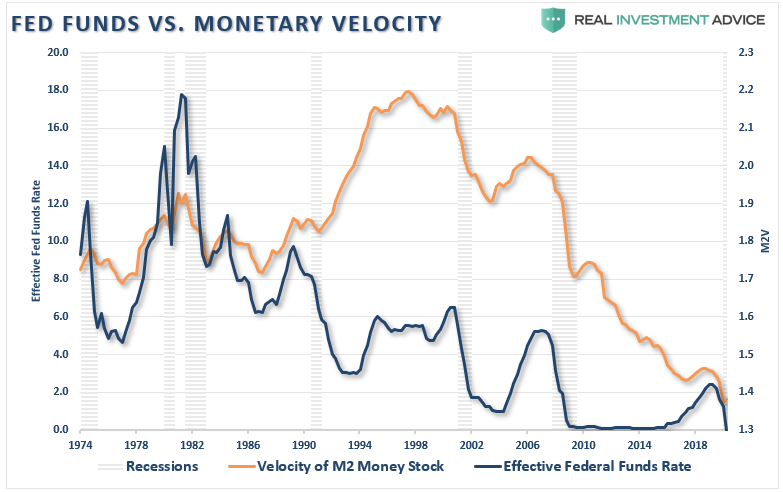

How do we know this? Monetary velocity tells the story.

What is “monetary velocity?”

“The velocity of money is important for measuring the rate at which money in circulation is used for purchasing goods and services. Velocity is useful in gauging the health and vitality of the economy. High money velocity is usually associated with a healthy, expanding economy. Low money velocity is usually associated with recessions and contractions.” – Investopedia

With each monetary policy intervention, the velocity of money has slowed along with the breadth and strength of economic activity.

However, it isn’t just the expansion of the Fed’s balance sheet which is undermining the strength of the economy. It is also the ongoing suppression of interest rates to try and stimulate economic activity.

In 2000, the Fed “crossed the Rubicon,” where lowering interest rates did not stimulate economic activity. Instead, the “debt burden” detracted from it.

To illustrate the last point, we can compare monetary velocity to the deficit.

To no surprise, monetary velocity increases when the deficit reverses to a surplus. Such allows revenues to move into productive investments rather than debt service.

The problem for the Fed is the misunderstanding of the derivation of organic economic inflation

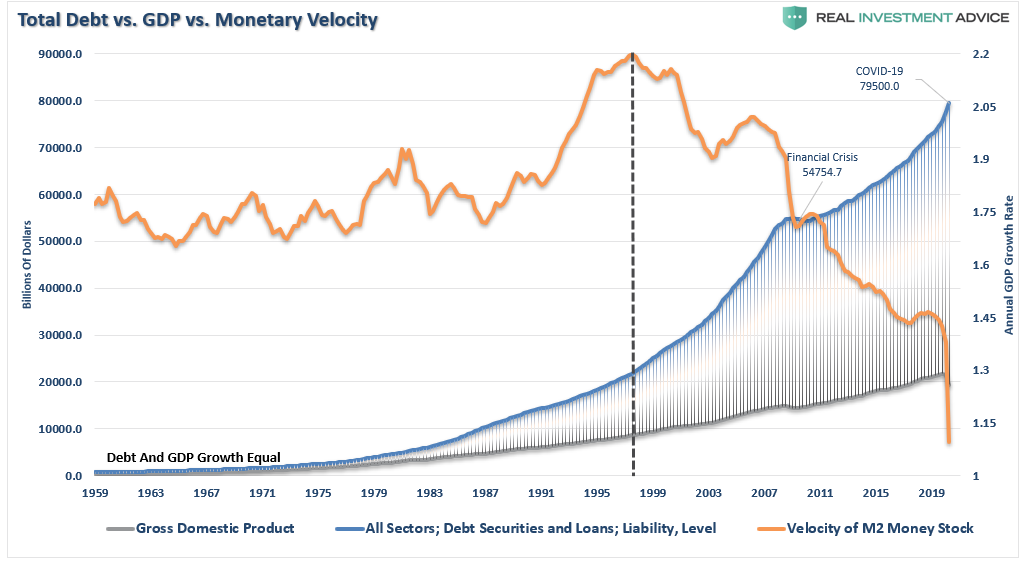

It’s The Debt

It isn’t just the Federal debt burden that is detracting from economic growth. It is all debt. As stated, the belief that lower interest rates would spur more economic activity was correct, to a point. However, as shown, once the debt burden because to consume more than it produced, the lure of debt turned sour.

You will notice that in 1998, monetary velocity peaked and began to turn lower. Such coincides with the point that consumers were forced into debt to sustain their standard of living. For decades, WallStreet, advertisers, and corporate powerhouses flooded consumers with advertising to induce them into buying bigger houses, televisions, and cars. The age of “consumerism” took hold.

However, while corporations grew richer, households got poorer, as growth in the economy and wages remained nascent.

The problem for the Federal Reserve, is that due to the massive levels of debt underlying the meager economic activity it generates, interest rates MUST remain low. Any uptick in rates quickly slows economic activity, forcing the Fed to lower rates and support it.

Economic Inflation

For the last several years, the Fed’s belief has been inflating asset prices would lead to a rise in economic prosperity and inflation. As noted, the Fed did achieve “asset inflation,” which led to a burgeoning “wealth gap.”

What monetary policy did not do was lead to “general fluctuations in price levels.”

Despite the Fed’s annual call of higher rates of inflation and economic growth, the realization of those goals remains elusive.

The problem for the Fed is that monetary policy creates “bad” inflation, without supporting the things that lead to “good” inflation.

Good Inflation

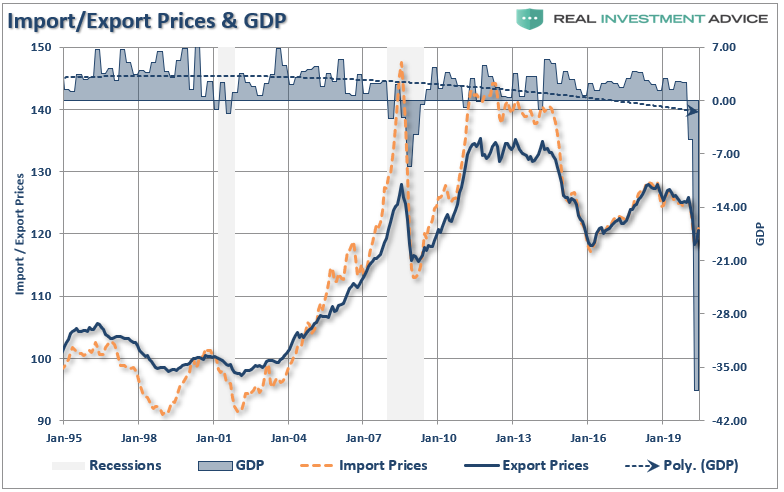

The Fed believes the rise in inflationary pressures is directly related to an increase in economic strength. However, as I will explain: Inflation can be both good and bad.

Inflationary pressures can be representative of expanding economic strength if reflected in the more robust pricing of imports and exports. Such increases in prices would suggest stronger consumptive demand, which is 2/3rds of economic growth and increases in wages allowing for the absorption of higher prices.

That would be “the good.”

Bad Inflation

The bad would be inflationary pressures in areas which are direct expenses to the household. Such increases curtail consumptive demand, negatively impacting pricing pressure, by diverting consumer cash flows into non-productive goods or services.

If we look at import and export prices, there is little indication that inflationary pressures are present.

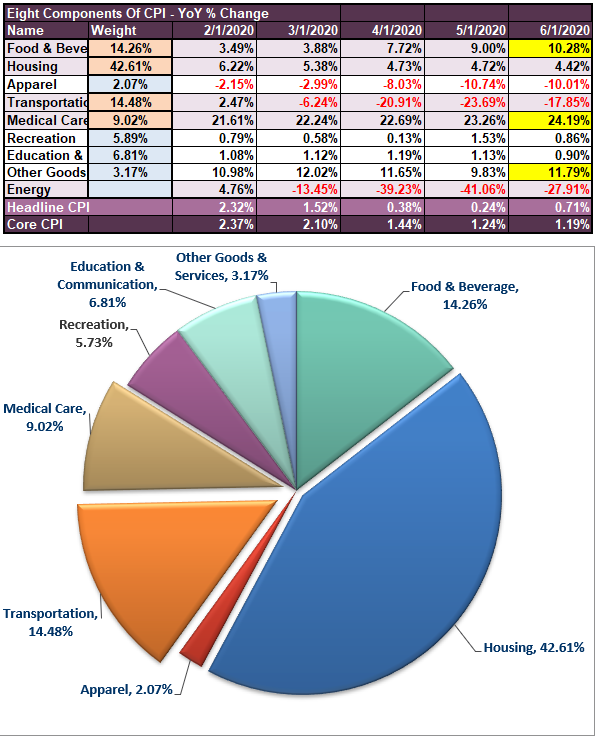

This lack of economic acceleration is seen in the breakdown of the Consumer Price Index below, which shows where inflationary pressures have risen over the last 5-months.

(Thank you to Doug Short for help with the design)

As is clearly evident, the surge in “healthcare” related costs, due to the surging premiums of insurance, pushed both consumer-related spending measures and inflationary pressures higher. Unfortunately, higher health care premiums do not provide a boost to production but drain consumptive spending capabilities.

[Housing costs, a very large portion of overall CPI, is also boosting inflationary pressures. But like “health care” costs, rising housing costs and rental rates also suppress consumptive spending ability. It is the same for Other Goods and the cost of “food,” which is stripped out of the core calculation, but eat away at disposable incomes.]

“For the middle-class and working poor, which is roughly 80% of households, rent, energy, medical and food comprise 80-90% of the aggregate consumption basket.” – Research Affiliates

The Fed’s problem is that by trying to push inflation higher, which will also drive interest rates higher to compensate, will immediately curtail increases in economic activity.

Such is why the Fed remains caught in a liquidity trap.

“When injections of cash into the private banking system by a central bank fail to lower interest rates or stimulate economic growth. A liquidity trap occurs when people hoard cash because they expect an adverse event such as deflation, insufficient aggregate demand, or war.

Signature characteristics of a liquidity trap are short-term interest rates remain near zero. Furthermore, fluctuations in the monetary base fail to translate into fluctuations in general price levels.”

Pay particular attention to the last sentence.

As discussed through the entirety of this article, every aspect of a liquidity-trap has been checked:

Lower interest rates fail to stimulate economic growth

People hoard cash because they expect an adverse event (economic crisis).

Short-term interest rates near zero.

Fluctuations in monetary base fail to translate into general price levels.

Importantly, the issue of monetary velocity and saving rates is critical to defining a “liquidity trap.”

“It is hard to overstate the degree to which psychology drives an economy’s shift to deflation. When the prevailing economic mood in a nation changes from optimism to pessimism, participants change. Creditors, debtors, investors, producers, and consumers all change their primary orientation from expansion to conservation. Creditors become more conservative, and slow their lending. Potential debtors become more conservative, and borrow less or not at all.

As investors become more conservative, they commit less money to debt investments. Producers become more conservative and reduce expansion plans. Likewise, consumers become more conservative, and save more and spend less.

These behaviors reduce the velocity of money, which puts downward pressure on prices. Money velocity has already been slowing for years, a classic warning sign that deflation is impending. Now, thanks to the virus-related lockdowns, money velocity has begun to collapse. As widespread pessimism takes hold, expect it to fall even further.”

Deflationary Spiral

Such is the biggest problem for the Fed and one that monetary policy cannot fix.

Deflationary “psychology” is a very hard cycle to break.

“In addition to the psychological drivers, there are structural underpinnings of deflation as well. A financial system’s ability to sustain increasing levels of credit rests upon a vibrant economy. A high-debt situation becomes unsustainable when the rate of economic growth falls beneath the prevailing rate of interest owed.

As the slowing economy reduces borrowers’ ability to pay what they owe. In turn, creditors may refuse to underwrite interest payments on the existing debt by extending even more credit. When the burden becomes too great for the economy to support, defaults rise. Moreover, fear of defaults prompts creditors to reduce lending even further.”

For the last four decades, every time the Fed has taken action trying to achieve their goals of “full employment and stable prices,” it has led to an economic slowdown, or worse.

The relevance of debt growth versus economic growth is all too evident. Over the last decade, it has taken an ever-increasing amount of debt to generate $1 of economic growth.

In other words, without debt, there has been no organic economic growth.

While the Fed has been diligently working on its next program to achieve the long-elusive 2% inflation target, it will result in the same outcome as the last decade.

The problem is the debt, and you can’t solve a debt problem with more debt.

At some point, you have to stop digging.

via ZeroHedge News https://ift.tt/2F8x8nH Tyler Durden

Florida Cases, Fatalities Bounce Back After Hurricane As US Deaths Top 160,000: Live Upates Tyler Durden

Sat, 08/08/2020 – 11:33

Summary:

US deaths top 160k

Florida reports another 187 deaths, cases climb

NY cases top 700

Hong Kong cases top 4,000

Germany “R” rate hits highest in 10 days

Denmark says may asks citizens to wear masks more frequently

* * *

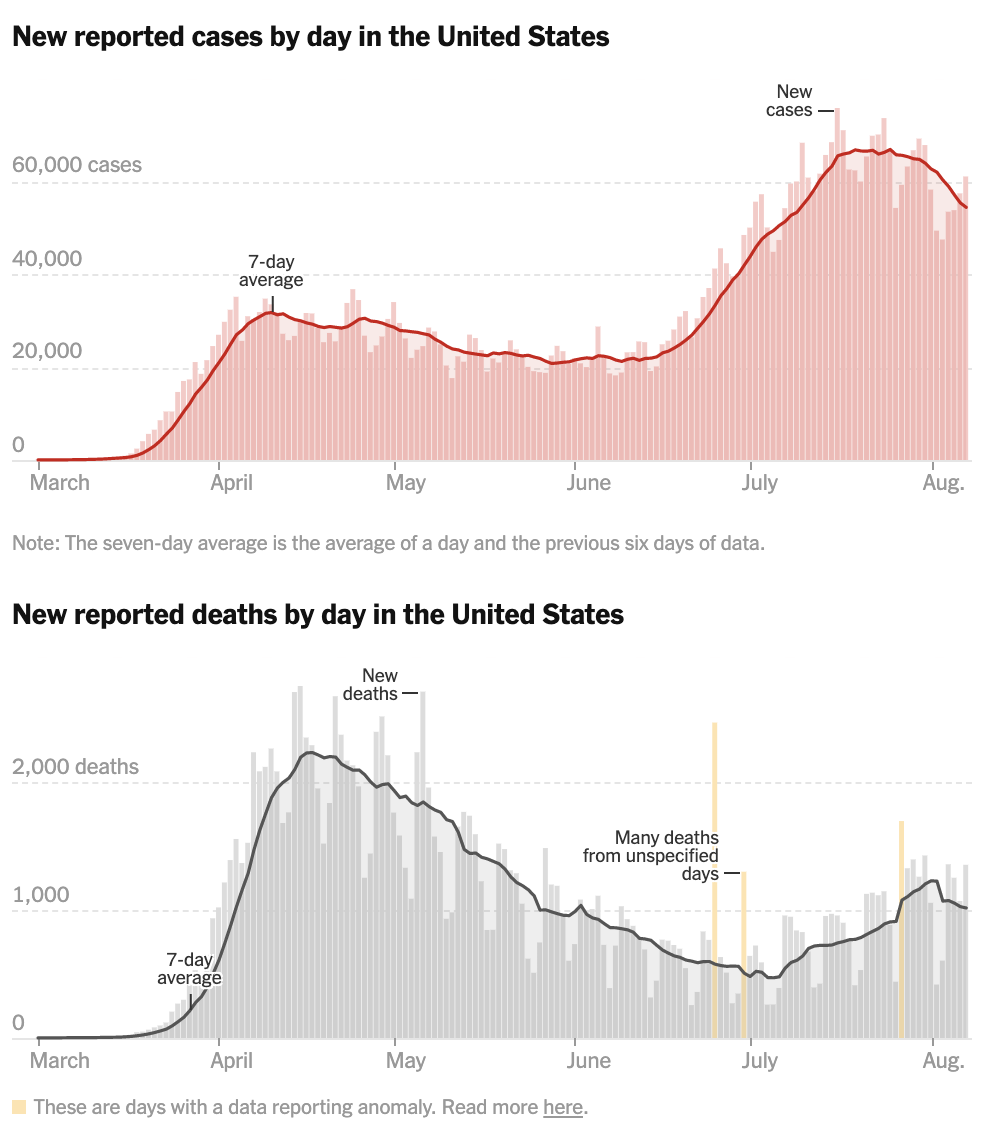

It’s official: The US has passed 160,000 confirmed deaths, according to figures reported by state health authorities and catalogued by Bloomberg, Johns Hopkins and other data providers. According to BBG & JHU, the US added 59,202 new cases (+1.2% ), on par with the average daily over the previous seven days. Some 1,256 deaths were reported yesterday, the fourth consecutive day with more than 1,000, but fewer than the 1,842 reported the previous day. America has now confirmed 4,941,635 cases (plus thousands more logged as ‘probable’ ones, and potentially millions of “asymptomatic” cases that will never be documented) and 161,347 deaths (plus thousands that have probably gone uncounted).

Of course, every time US deaths pass a big, round number, progressives come out with the pitchforks and conveniently try to “remind” indoctrinate the public to believe these deaths are Trump’s fault, and his alone.

Country club members booed because a reporter asked Pres Trump why they were not wearing masks as they watched Trump’s press conference.

Trump said the club members were engaged in a “peaceful protest.” Crowd cheered.

Note: More than 160K Americans have died from COVID.

One day after Gov Andrew Cuomo bucked the national Democratic trend and declared that schools in New York would be allowed to reopen, New York reported 703 new cases, a 0.2% rise, which is in line with the average increase from the prior weeks (and months). NY’s state of spread has more or less plateaued at between 500 and 750 cases per day, with few exceptions. Additionally, the state reported five more deaths, the same number as the day before. Total hospitalizations in the state that had been the center of the U.S. outbreak remained low, at 573.

Today’s update on the numbers:

Of the 74,857 tests reported yesterday, 703 were positive (0.93% of total).

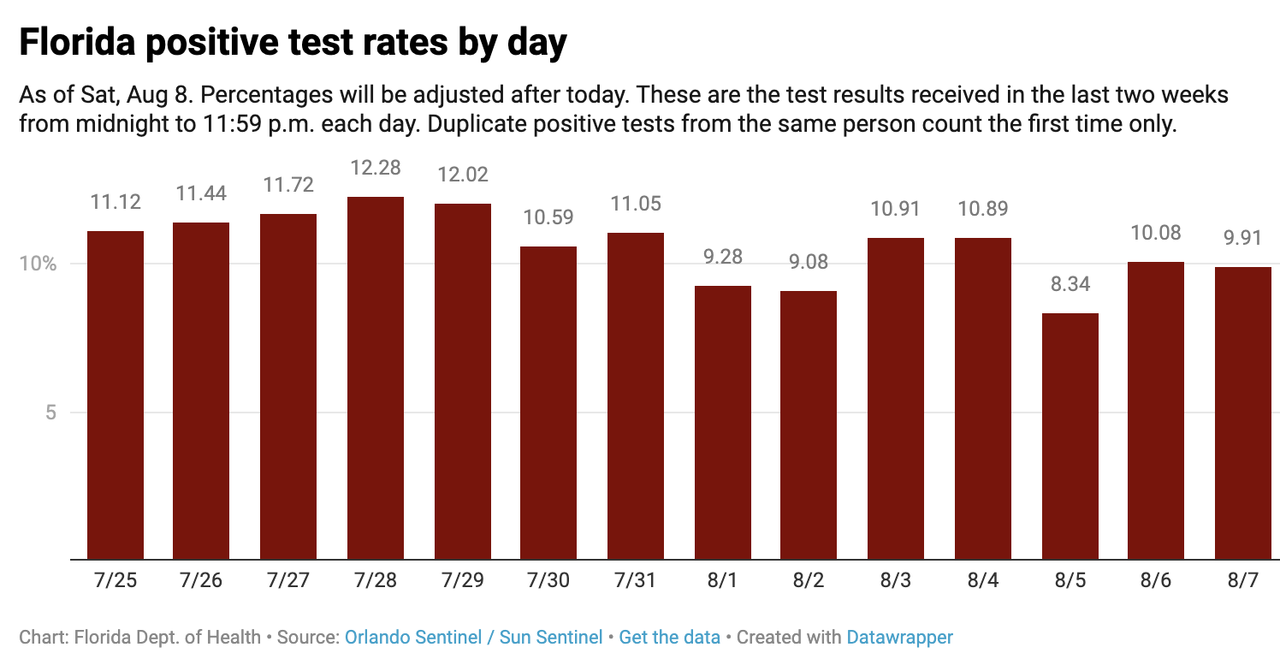

In Florida, health officials reported 187 COVID-19 deaths on Saturday, along with the highest single-day total of new cases in a week with 8,502 cases, though the 7-day average for cases continued to move lower.

Now, 8,238 people have died and 526,577 people have been infected with the virus. The state’s positivity rate declined slightly, but was mostly steady at 9.9.

It’s been three consecutive days of increases in both COVID-19 cases and deaths as both seem to bounce back after the hurricane (though we sincerely doubt the hurricane’s tour stopped people from succumbing to the virus).

Florida reported a record 257 deaths on July 31, when the state’s outbreak appeared to peak.

As we await case and death data from the rest of the US, here’s what else is happening in COVID-19 news world-wide.

Vietnam’s health ministry reported 21 new cases Saturday, of which 20 cases were linked to the coastal city of Danang, and one case was imported. After a lengthy stretch of no infections and deaths, the country has confirmed 353 infections tied to the Danang July 25 outbreak. Vietnam has a total of 810 cases with 10 deaths.

Amid a non-stop flurry of vaccine news out of the US, Europe, China and Russia, Tianjin-based CanSino Biologics, one of the most closely-watched (in the west, and China) Chinese vaccine projects. The company said Saturday it may test its coronavirus vaccine on pregnant women to study its ability to protect groups most vulnerable to virus. The Chinese company, which was the first in the world to start human testing of vaccines against the virus in March, “may include pregnant women and look at the shot’s ability to protect” young people during future clinical trials, said CanSino founder Yu Xuefeng during a webinar hosted by Hillhouse Capital on Saturday.

More signs of slowdown in Iran after deaths and cases surged in the country’s latest wave: single-day deaths fell to the lowest in six weeks with 132, with the number of new cases at a month-low of 2,125. Iran now has 18,264 confirmed deaths and 324,692 infections, with many, many more of both suspected.

Belgium, which has emerged as a hotspot in Europe’s nascent “second wave”, said on Saturday that 768 more infections have been detected, after 858 the day before. Five more deaths were reported, bringing the total number of fatalities to 9,866.

Hong Kong reported 69 new cases Saturday, pushing its total north of 4,000. Indonesia posted 2,277 new infections, lifting its tally above 123,500.

Meanwhile, in Denmark, where the country’s committee of experts leading its response have disagreed on the efficacy of masks, said the country likely won’t reopen nightclubs – as it had planned – due to an increase in cases. Prime Minister Mette Frederiksen said Danes may also have to get used to wearing face masks in public (at the moment, they are not mandatory, though Danes are asked to wear them on public transit).

Starting Saturday, Germany will test all returning travelers as the country’s “R” value climbs to 1.16 on Friday, its highest level in a week-and-a-half.

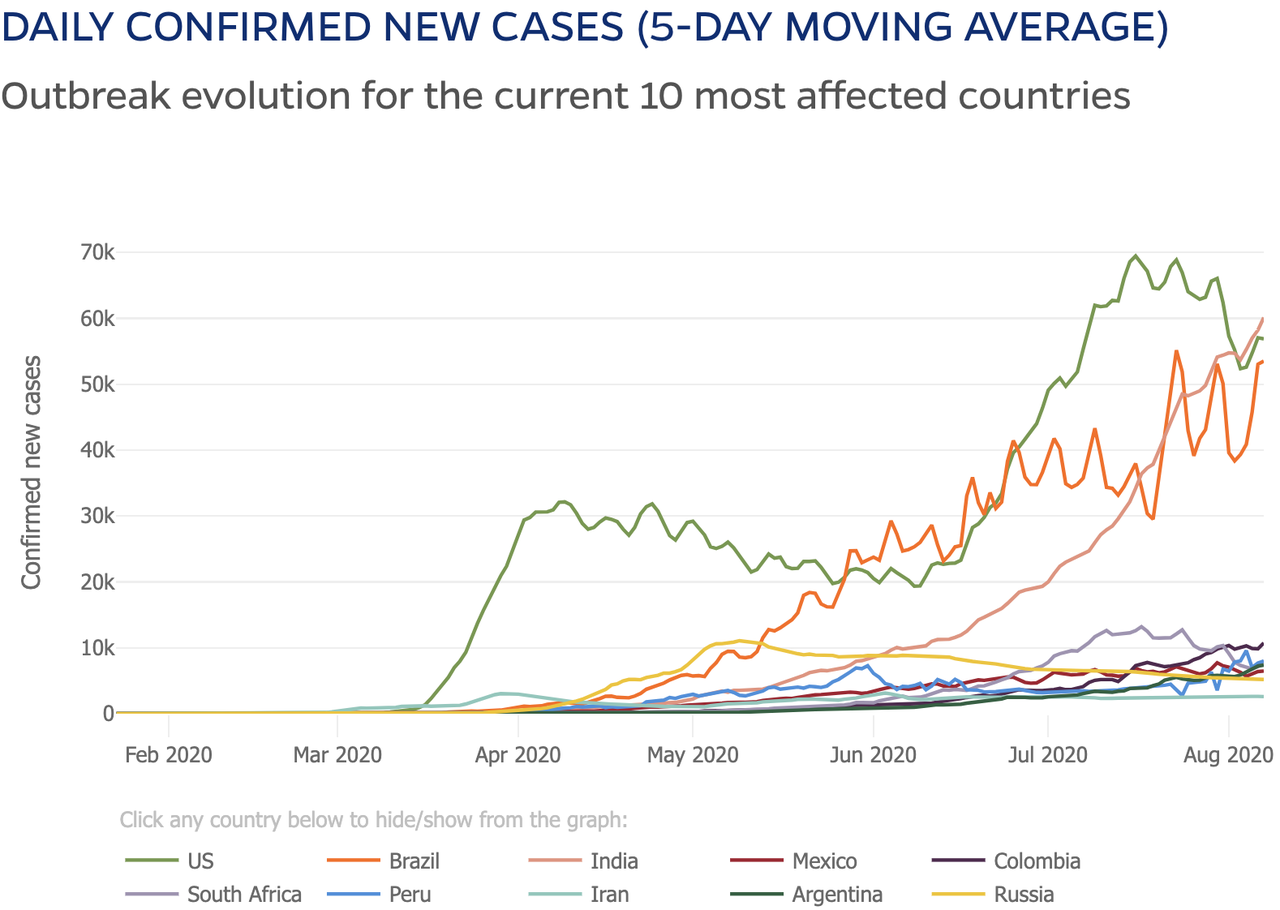

Here’s how the worst outbreaks in the world are progressing, per JHU:

via ZeroHedge News https://ift.tt/2XEqdJi Tyler Durden

Fauci Warns COVID-19 Vaccine May Only Be “50% Or 60%” Effective Tyler Durden

Sat, 08/08/2020 – 11:20

Dr. Anthony Fauci, the top U.S. infectious diseases expert (and untouchable purveyor of all that is true and holy in ‘science’ today), told a Brown University panel on Friday that probabilities of a highly effective COVID-19 vaccine “are not great.”

“We don’t know yet what the efficacy might be. We don’t know if it will be 50% or 60%. I’d like it to be 75% or more,” Fauci said (quoted by Reuters).

“But the chances of it being 98% effective is not great, which means you must never abandon the public health approach.”

Fauci reiterated that the public must abide by these six fundamental principles to flatten the pandemic curve:

Universal wearing of a mask

Physical distancing

Avoiding crowds

Outdoors is “better” than indoors

Washing your hands

Staying away from bars

Interestingly, Fauci inched towards the idea of herd immunity and humans’ own natural defense mechanisms (which of course, in political circles is frowned upon since one more death from COVID is too many).

“We know the body is capable of making a good response and the reason we know is because we have so many people who clear the virus and do well,” he said.

“So the goal of a vaccine is to do as well or hopefully better than natural infection when inducing a good response.”

Once a vaccine is proven and mass-produced, he said it would be prioritized to healthcare workers, elderly, and those with underlying health conditions.

“The thing you can do now is to make sure that resources are concentrated geographically to those demographic groups that are clearly at higher risk of infection so they can get immediate testing, immediate results, immediate access to healthcare,” Fauci said.

He said Moderna Inc’s COVID-19 vaccine, currently in clinical trials, could produce definitive data sometime in 4Q20.

Fauci told Reuters that millions of doses could be available by early 2021, and hundreds of millions by the end of the year.

His latest comments come after he also recently questioned the “durability” of the vaccine, adding that it may not shield someone from the infection on a long-term basis.

Readers may recall pharmaceutical companies developing COVID-19 vaccines will beexempt from liability claims if adverse effects are seen. In other words, if an experimental vaccine, mass-produced for the public accidentally kills folks, big pharma will not be held accountable.

Meanwhile, the world’s asset-gatherers and commission-rakers (and the Trump administration) is hyping vaccines with the most optimistic forecast ever, indicating Thursday the country could have vaccines before the election.

Fauci’s comments are certainly at odds with the optimism that seems widespread among many talking heads that “everything can return to normal once we have a vaccine.”

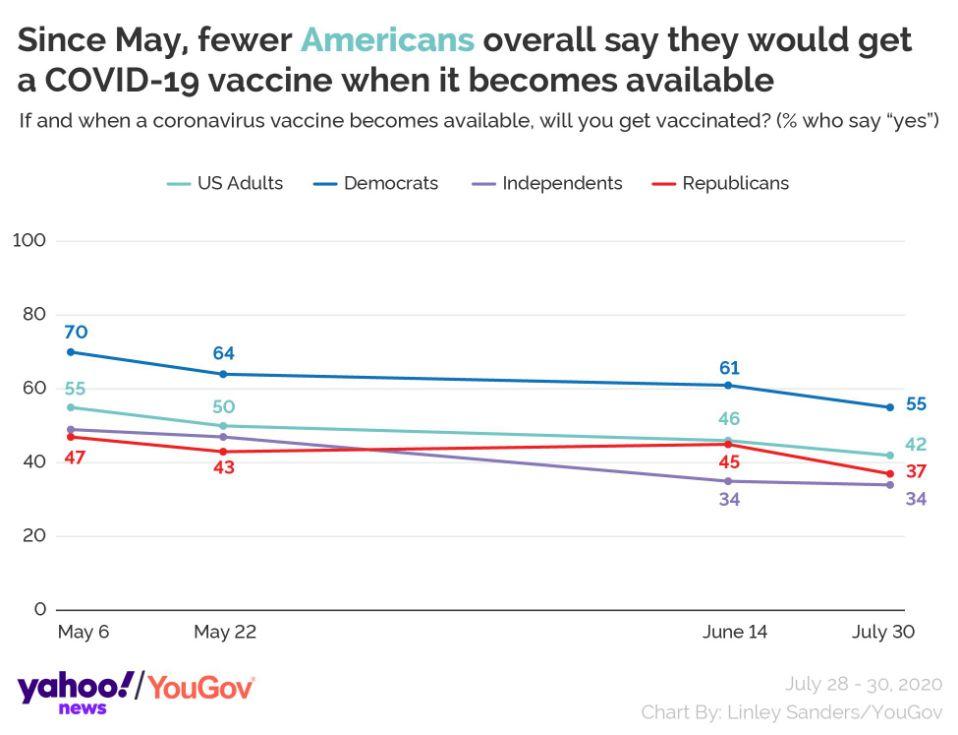

Additionally, as we noted previously, a new Yahoo News/YouGov poll has found that just 42 percent of Americans say they plan to get a coronavirus vaccine when it becomes available.

The figure represents an all time low, having fallen from 55 percent in early May, 50 percent in late May, and 46 percent in July.

When asked “If and when a coronavirus vaccine becomes available, will you get vaccinated?” many fewer Americans across the political spectrum answered in the affirmative.

Only a majority of Democrats now plan to get vaccinated, with 55% saying they will still take the jab.

Among Republicans, only 37% say they are willing to get vaccinated, with even fewer independents, 34%, willing to take the vaccine.

Here’s the full conversation:

via ZeroHedge News https://ift.tt/3ipeNB8 Tyler Durden

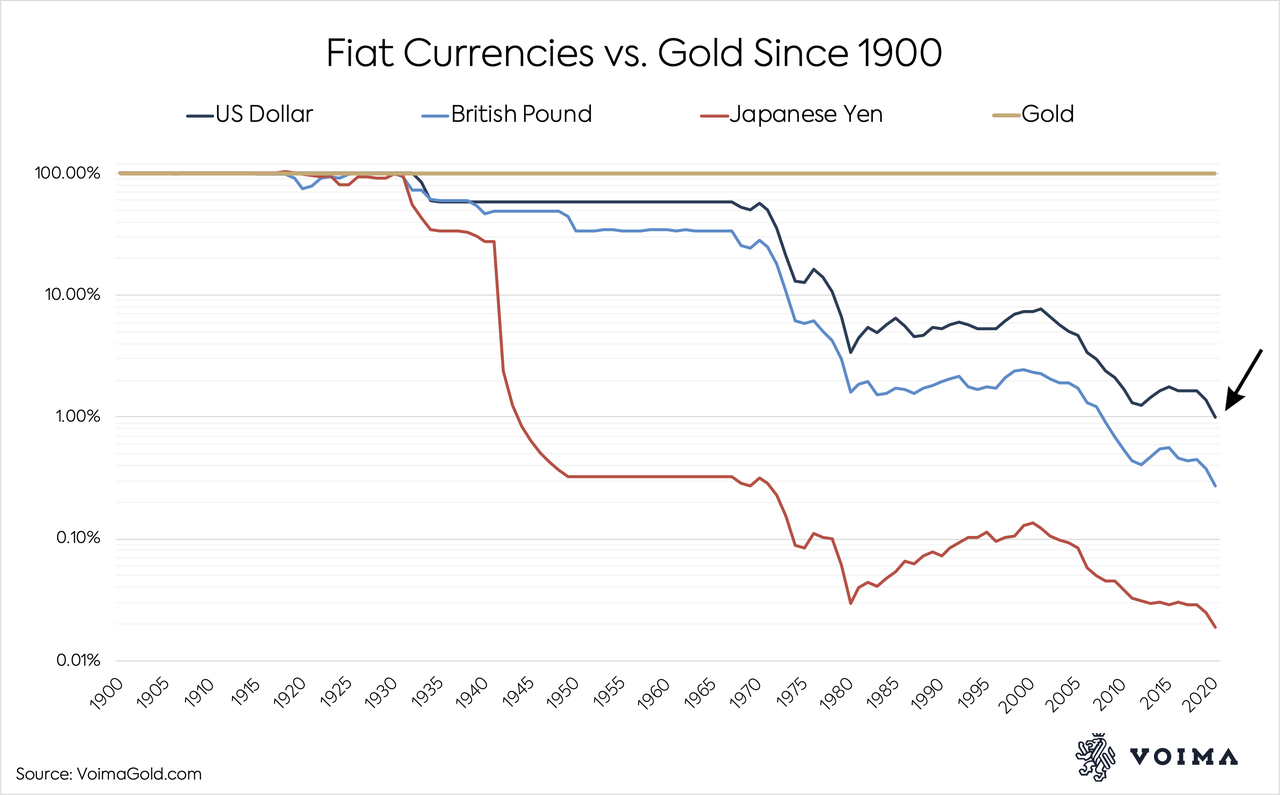

A world reserve currency is supposed to be superior in storing value, but through boundless money-printing the U.S. dollar hasn’t been able to compete with gold by a long shot…

In 1932 the gold price was $20.67 dollars per troy ounce, today it crossed $2,067 dollars.

That’s a 99% decline in value of the dollar against gold. Other reserve currencies such as the British pound and Japanese yen have done even worse. The yen has lost 99.98% of its value against gold in 100 years. Note, the chart below has a log scale.

Gold doesn’t yield, if you don’t lend it, but it’s the only globally accepted financial asset without counterparty risk. Because of its immutable properties gold sustained its role as the sun in our monetary cosmos after the gold standard was abandoned in 1971. Central banks around the world kept holding on to their gold, despite its price reaching all-time highs such as now. This is due to Gresham’s law, which states “bad money drives out good.” If the price of gold rises central banks are more inclined to hoard gold (good money) and spend currency that declines in value (bad money).

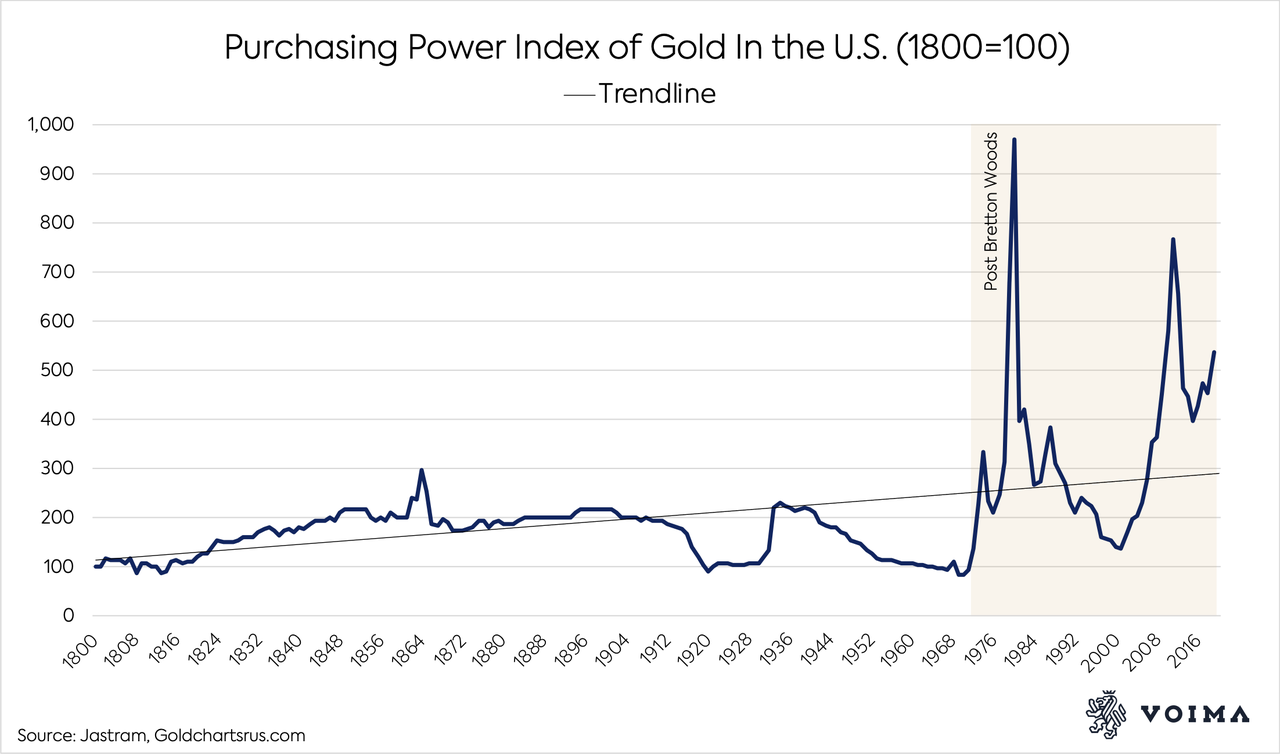

In the chart below you can see that gold’s purchasing power is remarkably stable. As the gold price rises through time it mainly compensates for fiat currencies being devalued versus goods and services. In other words, the price of gold goes up by the same amount that consumer prices rise. Gold even shows a tendency of increasing in purchasing power, which might reveal inflation numbers published by governments are too low. Another theory is that sound money, like gold, should rise in purchasing power as technological development makes goods increasingly cheaper to produce.

You might think that dollars with interest, for example U.S. government bonds (Treasuries), would have outperformed gold since the gold standard was abandoned in 1971. But this isn’t true. Gold has performed better than Treasuries.

In my view, the gold price will continue to rise and will be incorporated in a new international monetary system. The current all-time high in dollar or euro terms is just a nominal measure. When taking into account inflation gold is not at an all-time high, more importantly I’m expecting central banks to debase their currencies way more in the years ahead because the world has never been this much in debt. The debt levels around the world are completely unsustainable and can only be lowered through debt relief or inflation. The Federal Reserve and other central banks are communicating they choose inflation. A few months ago the President of the European Central Bank, Lagarde, said: “We should be happier to have a job than to have our savings protected.” That is a clear admission that (in this case) euro savings will be wiped out.

The Fed is expected to make a major commitment to ramping up inflation soon https://t.co/kFjh8yCw01

After the Second World War the U.S. government capped interest rates at very low levels while boosting inflation. The results were deeply negative real interest rates (nominal rates minus inflation).

Owning physical gold stored outside the banking system offers protection of your purchasing power from currency debasement.

via ZeroHedge News https://ift.tt/2DzjCsv Tyler Durden

Berkshire Bounces Back From Record Loss, But Shares Still Lag Despite Buffett’s $5.1BN Buyback Surprise Tyler Durden

Sat, 08/08/2020 – 10:30

Was DDTG founder Dave Portnoy on to something when he suggested earlier this year that Warren Buffett, the “Oracle of Omaha”, might be past his prime?

Berkshire’s Q2 earnings certainly don’t make a strong case to the contrary.

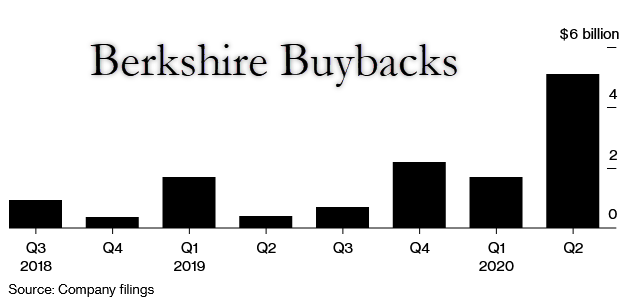

Released on Saturday morning (as per tradition), Berkshire reported that it spent a record $5.1 billion of the proceeds from cashing out its airline stocks, and others, during the March selloff buying back its own shares. While Bloomberg and other financial media focused on the $5.1 billion record buyback angle. BBG dared to ask its readers, in the opening paragraph of its earnings story, whether the great “Oracle of Omaha”, in placing so much confidence in his own company’s relatively unloved shares, might simply be one step ahead of the crowd once again.

Shares of Berkshire Hathaway Inc. were left out of the stock market rally in the second quarter. Warren Buffett clearly thought the disconnect wasn’t warranted.

They suggest this, despite Berkshire’s streak of decidedly “un-oracular” performance, and despite the fact that such deference would sound more like sycophancy if it were directed at another financier. But as always, “the Oracle of Omaha”, the folksy progressive defender of the “potential” of American capitalism.

Shares of Berkshire Hathaway Inc. were left out of the stock market rally in the second quarter. Warren Buffett clearly thought the disconnect wasn’t warranted.

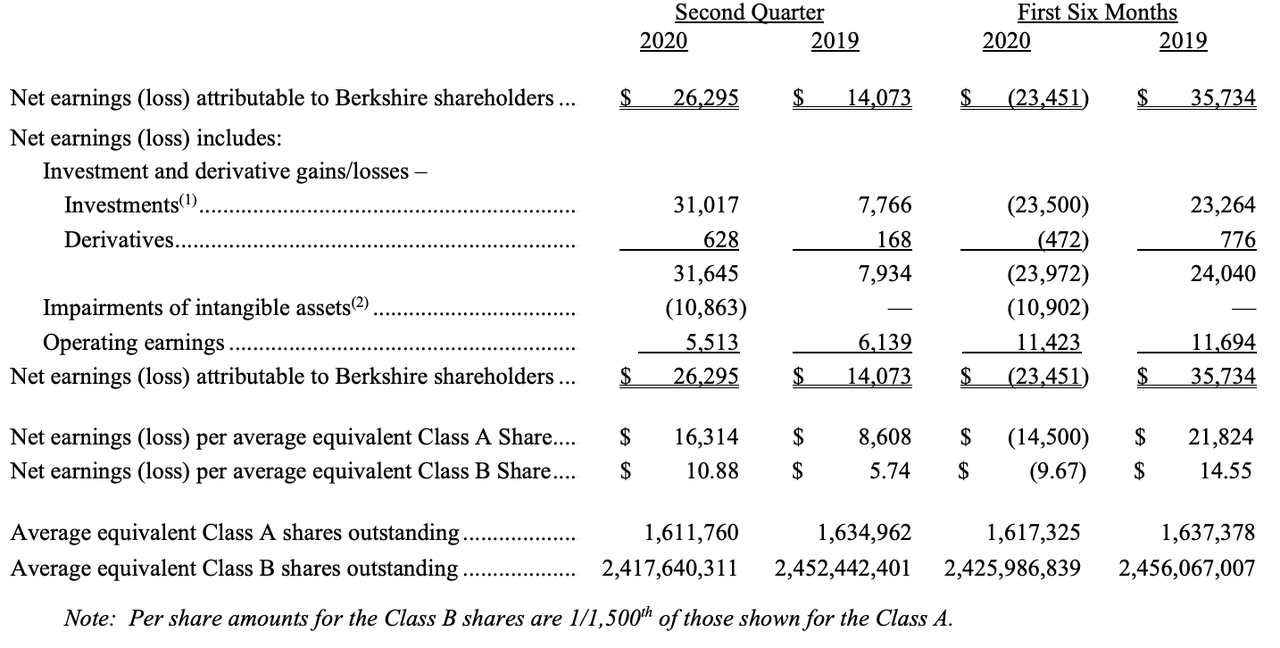

Although Berkshire bounced back to an operating profit after booking a record quarterly loss last quarter…

…its shares have still lagged.

Even with the massive infusion of capital provided by Buffett himself in the open-market buybacks…

…Berkshire’s shares largely lagged both the S&P 500 and a popular index of airline stocks, and the conglomerate’s cash pile, which has grown alongside perceptions of Buffett’s indolence, has reached its own record high of $146.6 billion.

Buffett refrained from dumping all of the $13 billion in cashed-out shares back into Berkshire, perhaps because Buffett told the public a few months ago that this wasn’t a particularly compelling time to buy back shares.

The famed investor spent a record $5.1 billion buying back Berkshire’s own stock in the second quarter, more than double the amount he’d ever purchased before. That came as he unloaded almost $13 billion of other companies’ shares, including airline stocks and some financials, in what was Buffett’s biggest selling quarter in more than a decade.

Buffett has shown signs of buying appetite in recent weeks, but the second-quarter results show those are a new phenomenon as the Covid-19 pandemic has slammed the economy but failed to put a permanent dent in stock-market valuations. Buffett’s been building up cash this year even as other investors have sought to seize on opportunities amid the turmoil, and the pain Berkshire’s own businesses are feeling may inform his thinking.

“Our operating business groups are preparing for reduced cash flows from reduced revenues and economic activity as a result of Covid-19,” Berkshire said Saturday in a regulatory filing. “We currently believe our liquidity and capital strength, which is extremely strong, to be more than adequate.”

Buffett’s cash pile surged to a record $146.6 billion at the end of June, in part from dumping all of his airline shares in April. He’s been more active lately, striking a deal for natural-gas assets in July and snapping up at least $2 billion of Bank of America Corp. stock in recent weeks through Aug. 4.

Berkshire’s Class A shares, which fell in line with the S&P 500 in the first three months of the year as the pandemic spread in the U.S., fell another 1.7% last quarter while the broader index rallied 20%. Buffett said in early May that repurchases weren’t more compelling than at previous times, but the buybacks in the quarter suggest his thinking shifted.

The company’s stock has rallied in July and August, but still is underperforming in 2020. Berkshire Class A shares were down 7.4% for the year through Friday’s close, compared with the 3.7% gain in the S&P 500.

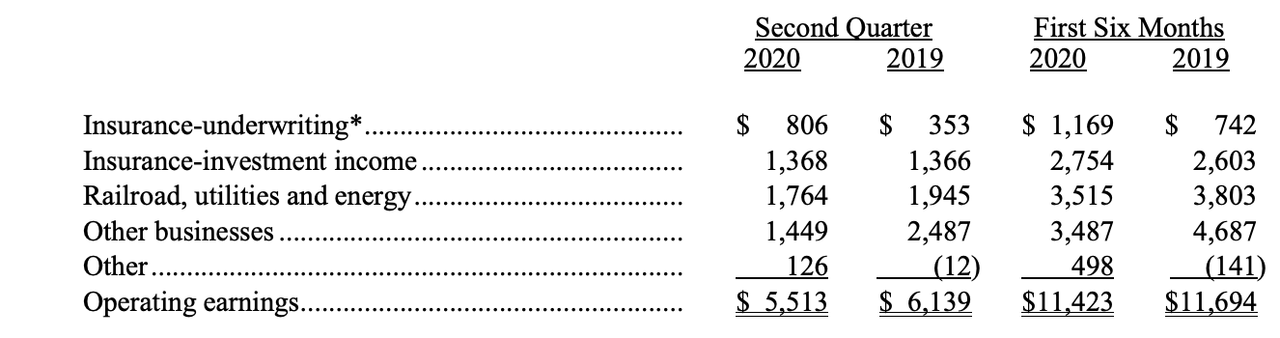

An analysis of Berkshire’s operating earnings follows (dollar amounts are in millions).

Heaping more injury upon injury, Berkshire also announced a $10 billion impairment charge stemming from one of Buffett’s biggest and most recent deals, the purchase of Precision Castparts, a maker of airplane parts and engine components.

The company also took $10 billion of impairment charges related to its Precision Castparts unit. Berkshire bought Precision Castparts in 2016 in a transaction valued at $37.2 billion, making it one of Buffett’s biggest deals. Now the maker of jet-engine blades and aircraft structural components is bracing for lean times as Boeing Co. and Airbus SE cut jetliner production and less air travel reduces the need for replacement parts.

That’s forced the aerospace-parts maker to undergo “aggressive restructuring,” with the company cutting its workforce by about 10,000 employees during the first half of 2020.

“We believe the effects of the pandemic on commercial airlines and aircraft manufacturers continues to be particularly severe,” Berkshire said in the filing. “In our judgment, the timing and extent of the recovery in the commercial airline and aerospace industries may be dependent on the development and wide-scale distribution of medicines or vaccines that effectively treat the virus.”

Here are the other key takeaways from the quarter, courtesy of BBG:

Unrealized gains and losses in Berkshire’s massive stock portfolio count toward the bottom line. So the S&P 500’s rally in the second quarter pushed net income to $26.3 billion.

Insurance underwriting profit more than doubled to $806 million in the period. That was helped by gains at auto insurer Geico as fewer accidents benefited the business.

Berkshire warned that Geico might be hurt in the next three quarters by a program that’s giving drivers a credit on their premiums.