An eventful week in markets and the economy as the month and quarter are coming to a close next week.

The broader market peaked on June 8th on the heels of unprecedented central bank intervention but has since failed to make new highs other than the Nasdaq. Any subsequent efforts by the Fed to stave off any market sell off via the announcement of individual corporate bond buying 2 weeks ago or this week’s announcement to relax the Volcker rule for banks have produced nothing but short lived bounces in markets leading to lower highs and further selling in equities.

Fundamentals and reality are making their presence felt. The reopening of the US economy is hampered by violent spikes in coronavirus infections in some part of the US leading to delayed reopening in some cases raising questions about the veracity of any V shape recovery in the economy as lay off announcements keep mounting globally.

The realization that jobs will not come back to anywhere near February levels may take time to sink in as does perhaps the inconvenient truth that the Fed’s intervention efforts may be hitting a point of diminishing returns.

In this week’s episode of Straight Talk we discuss the market’s technical battle line for control, the state of the banks and their message to markets, the gnawing threats on big cap tech, specifically on Facebook as advertisers are pulling out in droves in the midst of political backlash, the going forward political risk of big cap tech having reached quasi monopoly status in their respective fields, the ongoing threat of the virus resurgence to the V shape recovery narrative, the political risks to markets due the upcoming presidential election and possible impacts of tax policy and much more:

For reference a couple of charts relating to what we discussed in the video above:

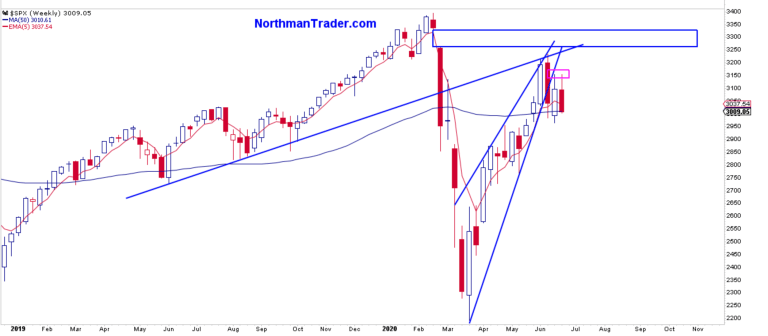

$SPX, following peaking June 8th when it tagged a key trend line has now reversed lower and has closed the week below its weekly 5 EMA for the first time since the March lows following the break of the rally trend earlier in the month:

This could be signaling a trend shift. But also note $SPX closed right at its weekly 50MA and just below its daily 200MA:

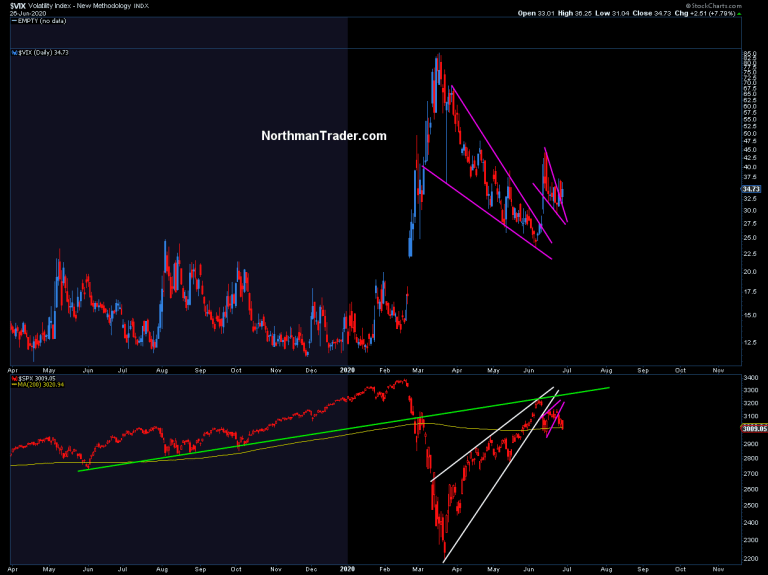

Note also the consecutive breakouts in volatility since the June 8th peak.

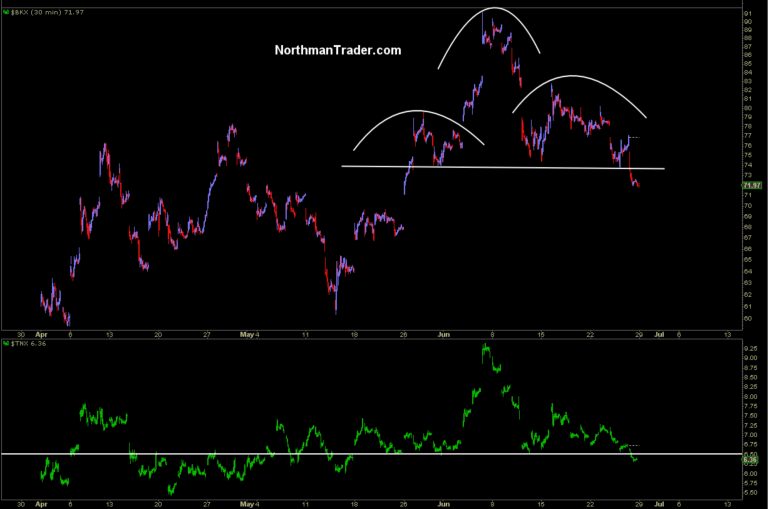

Put in context the horrid action in the banking sector, even this week’s loosening of the Volcker rule lead the resulting bounce to be sold. Worse for banks potentially here is that the chart suggests a potential head and shoulders pattern that could signal much lower prices ahead in context of the 10 year again dropping lower as well:

Since the June peak, $SPX is down 7%, small caps are down over 10% and the banking index is down over 20%. These are sizable moves to the downside and tech is increasingly under threat as well and its strength came on ever weakening internals.

I’ve outlined the reasons why the historic rally may have been still nothing but a bear market rally fueled to extremes by unprecedented liquidity injections and why the Fed looks increasingly busted in trying to defend this market without being able to prevent what the banks and bond market are already signaling: We’re staring at the prospect of a protracted downturn.

Markets are a journey and the day to day back and forth may well distract from the bigger picture, hence it is critically important to keep a close watch on the technical charts and evolving macro data. My primary view: There are plenty opportunities to trade the long and the short side as the battle between artificial liquidity interventions and the fundamental/valuation picture rages on in the months to come. But be clear: In June the broader market made a lower high and the path to a full economic recovery does not look anything like a clear V at all while valuations remain at unprecedented levels during a recession.

* * *

I’ll be posting a separate Market Video focusing on the latest technical implications later today (For those not already signed up for these videos please see link to register). For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2ZkbYJo Tyler Durden

“Disturbing Parallel To HIV”: COVID-19 Can Cause Depletion Of Important Immune Cells, NY Times Admits Tyler Durden

Sat, 06/27/2020 – 17:30

Once again, it looks as though what was once being peddled as Covid-19 “conspiracy theory” on our site appears to have turned out to have been accurate news reported months before the mainstream media. Go figure.

As far back as February 1, 2020, when the pandemic was only starting to attract attention and the China-influenced mainstream media was politically inclined to minimize the severity of the disease before pulling a sharp U-turn and now going full bore with a narrative of just how dangerous it is to reopen the economy, we published an article referencing an Arxiv pre-print which found that the Covid-19 genome contained “HIV Insertions”, stoking fears that the virus was an artificially created bioweapon.

While the mere suggestion that this virus was man-made – nevermind sharing discrete segments of its genetic structure with HIV – sparked outrage among the well-paid mercenary enforcers of the First Amendment known as “fact-checkers” who are employed by such biased organizations as Twitter and Facebook to stifle any line of inquiry that runs contrary to whatever dominant narrative has been blessed by the Zuckerbergs and Dorseys of the world, it was none other than the man who discovered the HIV virus back in 1983, that confirmed our suspicions saying that “the virus was man-made.”

We then reported in April that Professor Luc Montagnier, the 2008 Nobel Prize winner for Medicine, claimed that SARS-CoV-2 is a manipulated virus that was accidentally released from a laboratory in Wuhan, China, and added thatthe Wuhan laboratory, known for its work on coronaviruses, tried to use one of these viruses as a vector for HIV in the search for an AIDS vaccine.

This is the same conclusion we explored months before the mainstream media when we suggested that COVID-19 may have emerged from a lab in Wuhan instead of being man-made. For being early in what is increasingly looking like a very accurate assertion, a Buzzfeed journalist wrote a hit-piece about Zero Hedge that resulted in us being banned from Twitter.

But here we stand, months later. We have since been reinstated on Twitter and the journalist in question has been fired for plagiarism after BuzzFeed‘s new editor-in-chief, Mark Schoofs, published “A Note To Our Readers” detailing eleven instances where he lifted content from other publications without attribution going back to 2013, including his hit-piece against Zero Hedge.

Our lab origin “conspiracy theory” has gained widespread support and is the focus of several international investigations into the CCP lab. And just this week, we found out that and the HIV link that we first reported on months ago, and followed up on last month, continues to only get stronger.

As the mainstream media desperately plays catch-up, The New York Times released a piece yesterday called “How the Coronavirus Short-Circuits the Immune System” and said that “In a disturbing parallel to H.I.V., the coronavirus can cause a depletion of important immune cells, recent studies found.”

“Now researchers have discovered yet another unpleasant surprise. In many patients hospitalized with the coronavirus, the immune system is threatened by a depletion of certain essential cells, suggesting eerie parallels with H.I.V.,” the article says.

The assertions could explain why few kids get sick and why a “cocktail” of treatments may be needed to bring the coronavirus under control, similar to how H.I.V. is treated.

Dr. John Wherry, an immunologist at the University of Pennsylvania said that research now points to “very complex immunological signatures of the virus.” The NY Times wrote:

In May, Dr. Wherry and his colleagues posted online a paper showing a range of immune system defects in severely ill patients, including a loss of virus-fighting T cells in parts of the body.

In a separate study, the investigators identified three patterns of immune defects, and concluded that T cells and B cells, which help orchestrate the immune response, were inactive in roughly 30 percent of the 71 Covid-19 patients they examined. None of the papers have yet been published or peer reviewed.

Researchers in China have reported a similar depletion of T cells in critically ill patients, Dr. Wherry noted. But the emerging data could be difficult to interpret, he said — “like a Rorschach test.”

“It is hard to separate the effects of simply being critically ill and in an I.C.U., which can cause havoc on your immune system,” Wherry continued.

The researchers found that the immune system could actually become impaired because it overreacts to the virus, as happens in sepsis patients. They found that in Covid-19 patients, there was a marked increase in a molecule called IP10, which sends T cells to where they are needed in the body. Patients with coronavirus, as well as SARS and MERS, see a level of IP10 molecules that go up and stay up, which can create “chaotic signaling” in the body.

Dr. Adrian Hayday, an immunologist at King’s College London said: “It’s like Usain Bolt hearing the starting gun and starting to run. Then someone keeps firing the starting gun over and over. What would he do? He’d stop, confused and disoriented.”

This causes some T-cells, usually prepared to destroy the virus, to become confused and act “abberrantly”. Recovery becomes tougher for those over 40 because the thymus gland, which is responsible for creating new T-cells, becomes less efficient. In kids, the thymus glad works much better.

An overreaction of the immune system, causing things like a cytokine storm, may also be able to be treated by blocking a molecule called ID6, which helps organize immune cells.

“There clearly are some patients where IL-6 is elevated, and so suppressing it may help. But the core goal should be to restore and resurrect the immune system, not suppress it,” Hayday said.

Hayday believes an antiviral treatment may make the most sense, given the newfound information: “I have not lost one ounce of my optimism. A vaccine would be great. But with the logistics of its global rollout being so challenging, it’s comforting to think we may not depend on one.”

Recall, we had previously written that the South China Morning Post reported a study by Chinese scientists found that the novel coronavirus uses the same strategy to evade attack from the human immune system as HIV. Specifically, both viruses remove marker molecules on the surface of an infected cell that are used by the immune system to identify invaders, we noted.

The researchers warned that this commonality could mean Sars-CoV-2, the clinical name for the virus, could be around for some time, like HIV.

We wrote in May:

And here is where things gets very messy for the frauds known as “fact-checkers” who – without any actual facts or knowledge – threw up all over our February report that the coronavirus shared genetic material with HIV: while the mainstream media did everything in its power to censor any suggestions that Covid and HIV having genetic similarities (after all who wants to be threatened by an airborne version of AIDS) now it is none other than the South China Morning Post which writes that “earlier studies found the spike protein of the new coronavirus had a structure that allowed it to enter many types of human cells and bind with them. The same structure was also found in HIV, but not in other coronaviruses found in animals such as bats and pangolins.”

At this point, the New York Times and the SCMP appear to have pointed out all the exact same facts – that the coronavirus not only shares genetic material with HIV, but also evades and cripples the immune system in a similar way to HIV – that got the “highly respected” StatNews to accuse Zero Hedge of spreading an “infodemic.”

As we said last month:

“We wonder if StatNews author John Gregory will append his “analysis” now that actual “facts” have emerged showing that it’s not the infodemic we should be afraid of, but the censordemic.”

via ZeroHedge News https://ift.tt/2NzZxnp Tyler Durden

Europe On Alert After Unknown Radioactivity Spike Detected Over Baltic Sea Tyler Durden

Sat, 06/27/2020 – 17:00

Almost a year ago Russia admitted to releasing significant amounts of radiation into the air that triggered warning alerts in the region of the far north Arctic Circle port cities of Arkhangelsk and Severodvinsk, after a failed weapons test involving a “small-scale nuclear reactor” that killed Russian scientists – which was believed connected to Russia’s hypersonics program.

We can’t help but recall that incident now with new reports of radiation sensors based in Scandinavia again picking up abnormal radioactivity levels in the air. Perhaps there’s some further failed weapons tests happening somewhere in the region?:

“Radiation sensors in Stockholm have detected higher-than-usual but still harmless levels of isotopes produced by nuclear fission, probably from somewhere on or near the Baltic Sea, a body running a worldwide network of the sensors said on Friday,” Reuters reports.

22 /23 June 2020, RN #IMS station SEP63 #Sweden🇸🇪 detected 3isotopes; Cs-134, Cs-137 & Ru-103 associated w/Nuclear fission @ higher[ ] than usual levels (but not harmful for human health). The possible source region in the 72h preceding detection is shown in orange on the map. pic.twitter.com/ZeGsJa21TN

The Comprehensive Nuclear-Test-Ban Treaty Organization (CTBTO) confirmed the higher than normal activity.

Its ultra-sensitive networked sensors set up across Europe and the world are capable of picking up nuclear weapons testing when it occurs anywhere around the globe.

As Reuters reports further, the Stockholm monitoring station “detected 3 isotopes; Cs-134, Cs-137 & Ru-103 associated with Nuclear fission at higher than usual levels,” according to CTBTO chief Lassina Zerbo, who made the announcement on Friday.

The additional particles were picked up by the sensors last Monday and Tuesday, and confirmed by the nuclear monitoring organization. Zerbo pointed out, however, that it wasn’t at levels harmful for human health.

Russian nuclear plant in Saint Petersburg, AFP via Getty.

“These are certainly nuclear fission products, most likely from a civil source,” the CTBTO said in a statement. “We are able to indicate the likely region of the source, but it’s outside the CTBTO’s mandate to identify the exact origin.”

The organization further speculated that the source could have come from anywhere spanning from western Russia to Baltic countries to parts of Scandinavia.

via ZeroHedge News https://ift.tt/2ZjAWJb Tyler Durden

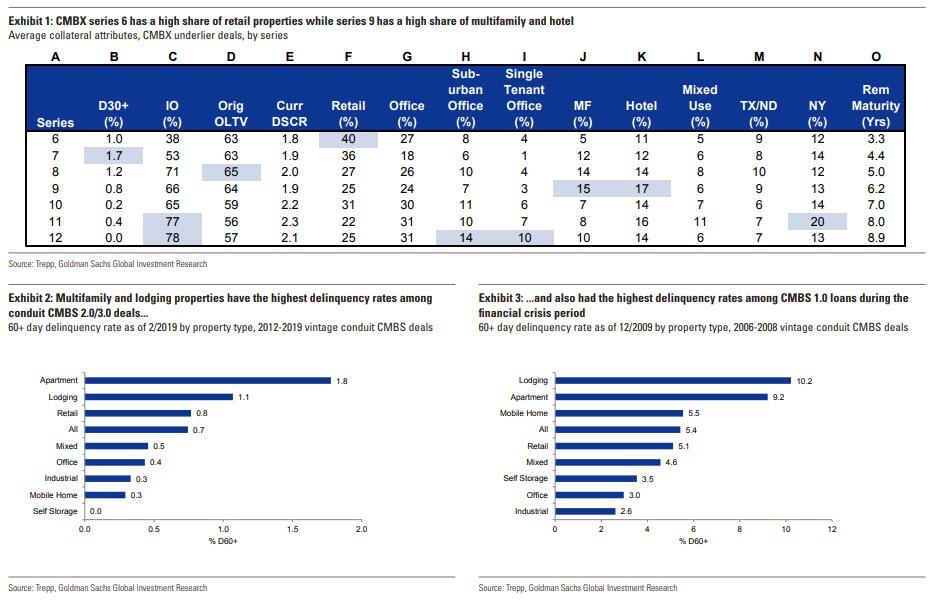

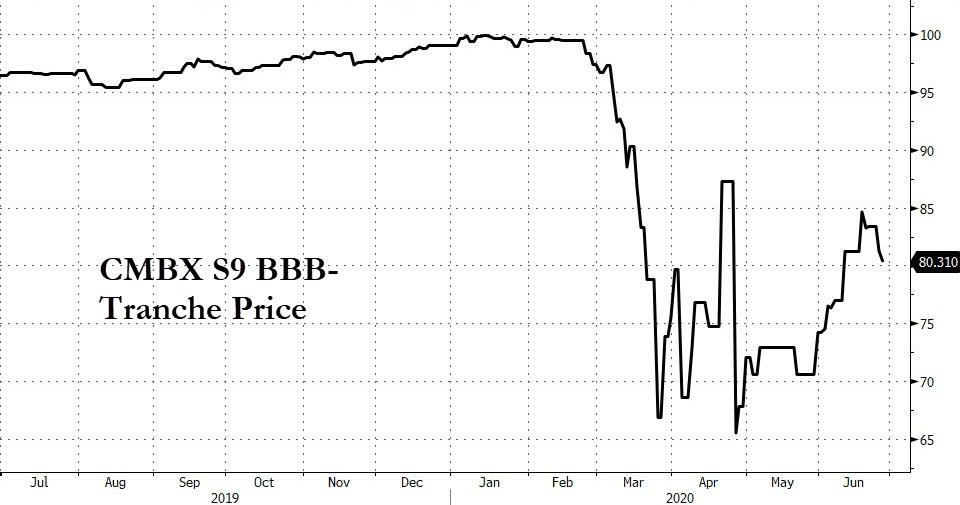

As we reported previously, with commercial real estate failing to benefit from the rebound in overall risk over the past 3 months as a result of a tidal wave of retail bankruptcies, CMBX Series 6 – which back in March 2017 was dubbed the “Big Short 2.0” trade due to its substantial exposure to malls which were hurting long before the arrival of the pandemic…

… and especially the BBB- tranche has been stuck in purgatory, and after surging to 75, is back to where it was in mid-April as investors signal that the worst is yet to come for commercial real estate.

Of course, all of this is well-known by now, and it is safe to say that the riskier tranches of CMBX S6 are now fairly priced for even a downside scenario among retail outlets. But what about other CMBX issues, and is there another “Big Short” lurking among the various tranches, especially in the aftermath of the coronavirus shutdowns which will cripple not just retail outlets but everything from restaurants, to multi-family housing (as city renters flee for the suburbs), to offices and hotels.

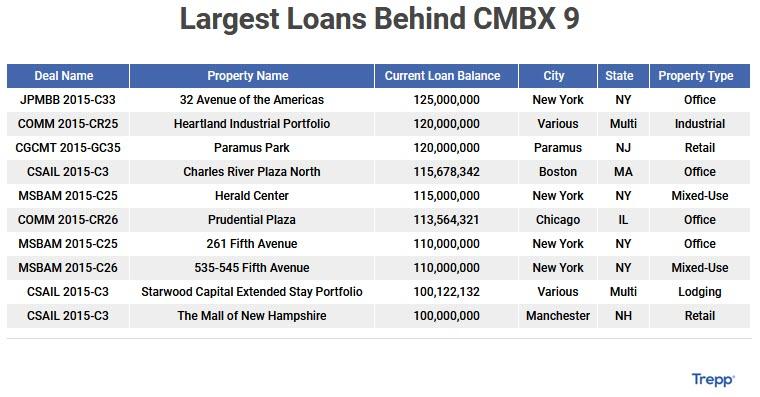

In our view, the answer to all those seeking the next Big Short is CMBX 9. This is what we wrote +:

… with CMBX 6 now done, keep a close eye on CMBX 9. With its outlier exposure to hotels which have quickly emerged as the most impacted sector from the pandemic, this may well be the next big short.

As Trepp’s Manus Clancy writes in a blog post on Friday, “the COVID-related volatility over the last three months has resulted in growing interest over CMBX as a way to take positions on US commercial real estate. This week we are back to hone in on CMBX 9.“

Below are some of the reasons why CMBX 9 – which so far is off-limits to the Fed’s blatant bailouts of most, but not all, asset classes – may be the cleanest and safest way to bet on the devastation resulting from the coronavirus pandemic. Courtesy of Trepp:

What Makes CMBX 9 Unique?

For one, it’s the only CMBX index backed by 2015 deals. Before the COVID-19 crisis began, the last meaningful hiccup in CMBS lending came in early 2016. In late 2015, volatility in the US equity markets picked up considerably and oil prices fell to under $30 a barrel. The sharp price decline in black gold led investors to fear a wave of forthcoming bankruptcies from energy companies.

That fear led to a sharp repricing of credit in the leveraged loan market and that widening had a gravitational pull on CMBS, dragging spreads wider over the course of two months. That widening in CMBS led to an abrupt pause to CMBS lending leading to a standstill in issuance in Q1 2016.

The 2015 CMBX 9 reference obligations consist of deals issued before any of that drama emerged. (The 2016 oil downturn in CMBS also led to several defaults of hotel and multifamily loans backed by “man-camps” in the shale regions of North Dakota and elsewhere.)

Other Attributes of CMBX 9?

It has the highest concentration of multifamily loans of any CMBX series with 14.7%. (The only other series that is close is CMBX 13 with 14.1%.)

CMBX 9 also has the highest concentration of hotel loans with 16.7%. (CMBX 11 is next with 13.8%.) In terms of protection premiums, CMBX 9 BBB- costs about 725 basis points to insure. That’s well inside of the 925 basis points for CMBX 8 BBB- but wider than the 675 for CMBX 10 BBB-. (Those spread levels are from IHS Markit).

For comparison purposes, CMBX 9 BBB- ended 2019 with a spread of 310 basis points. So there has been about 400 basis points of widening since the beginning of the year.

As of June 2020, 9.8% of the collateral behind CMBX 9 is 30 or more days delinquent. That puts the index slightly ahead of the average CMBS delinquency rate as of June.

Another 6.6% of the loans behind CMBX 9 missed their June payment, but were not yet 30 days late – so there is room for the delinquency rate to move higher over the summer. (Those percentages include defeased loans in the denominator of the calculation.)

The pool of defeased loans totals 4.5% by loan balance. In addition, 23% of the collateral pool is on servicer watchlist and another 5.1% of the collateral pool is with the special servicer.

CMBX Background

For background, CMBX is a set of indexes administered by Markit Partners. There are 13 separate indexes – the first five were launched prior to the Great Financial Crisis of 2008.

When the markets are functioning, a new series is rolled out every 18 to 24 months by Markit. Each series allows an investor to buy protection (“go short”) or sell protection (“go long”) on a bucket of 25 separate tranches. An investor can go long or short on AAA, AA, A, BBB- or BB. To buy protection, a buyer pays a fixed premium each month – the premium level is set when the index is launched. If selling protection, the seller is committing to “insuring” the buyer of protection against any bond writedowns.

The price of the index fluctuates up and down – up when the perceived likelihood of losses is low and down when perceived creditworthiness is low. Since the COVID-19 crisis began, prices have been trending lower. The lower down the credit stack, the bigger the price drop.

Within a series – say, CMBX 13 – the same 25 deals are represented across all ratings classes. (So for the CMBX 13 AAA index, it will be the AAA tranches from 25 deals that serve as “reference obligations.” For the CMBX 13 BBB-, it will be the BBB- tranches from the same 25 deals.) All deals that serve as reference obligations are US conduit deals.

For historical reference, for many of the deals used for reference obligations in 2006 and 2007 saw meaningful losses, with some deals seeing losses erase even the AA classes of some deals. (The ABX indexes got most of the attention during the GFC, but those that “shorted” CMBX BBB- from some of the pre-crisis CMBX indexes made out handsomely as well.) In fact, for CMBX 5 BBB-, 22 of the 25 reference tranches suffered 100% losses.

* * *

Finally, for those asking, yes there is a lot of potential downside for CMBX Series 9 BBB-. In fact, if the hotel world suffers a perfect storm of pent up defaults coupled with a second wave of covid which send the hotel industry into another tailspin, the potential downside here could be even greater than for Series 6.

via ZeroHedge News https://ift.tt/2Vlb3Hy Tyler Durden

The lockdown of the economy by government order is proving to be a blunder of epic proportions. Coronavirus is still on the loose. Yet, as a result of the lockdown, the economy’s been destroyed.

Take the housing market, for instance. According to a report from Black Knight, 4.3 million U.S. borrowers were more than 30 days late on a mortgage payment in May. What’s more, over 8 percent of all U.S. mortgages were either past due or in foreclosure.

The succession is real simple.

First, the economy was shut down by government order.

Second, about 47 million people filed for unemployment claims over a 14-week period.

Third, people stopped paying their mortgage.

Here in the ‘land of fruits and nuts’ the trend is also moving in the wrong direction. In May, 6.85 percent of California mortgages were estimated to be “non-current.” This troubled-loan category is composed of mortgages with missed payments plus those formally in the foreclosure process.

When the year started, only 2.1 percent of California mortgages were non-current. Thus, in just six months, the rate of non-current mortgages has jumped 228 percent. Nationally, 7.76 percent of mortgages are non-current.

The housing market’s difficulties typify the consequences of an overleveraged economy. With vast numbers of people up to their eyeballs in debt, all it took was a brief pause in cash flows and the debt structure broke down. To add insult, this is a government sponsored problem…

What Comes Next?

Through the wheelings and dealings of Fannie Mae and Freddie Mac, two government sponsored enterprises, lenders have an endless demand for mortgages. Fannie and Freddie buy up the mortgages from lenders and either hold them in their portfolios or package them up into mortgage-backed securities (MBS).

If you recall, Fannie and Freddie were given a several hundred billion dollar bailout during the 2008-09 financial crisis. Now, just over a decade later, the fermentations of another bailout are brewing. The CARES Act was merely the warm up.

As noted above, mortgage payment fundamentals have rapidly turned negative. Over the next several months the progression will advance from late and missed payments to mortgage defaults and foreclosures.

Without question, there will be another monster bailout. But this bailout is bigger than just Fannie and Freddie or even the big banks. This bailout is about a futile attempt to paper over American homelessness and poverty. But what comes next?

Almost no one has considered the consequences of another monster bailout. Will it be inflationary? What will it do to the economy? What will it do to the stock market? How will it influence the price of gold or the yield on the 10-Year Treasury note?

These questions are not met with obvious answers. We’ve been contemplating them for years without coming to any satisfying conclusions. The best we can do is draw from the past, consider what’s different about the present, and make interpolations and guesses about impacts to the future.

Using this methodology, we offer the following ruminations…

How the Bottom Up Bailout Will Impact the Future

The 2008-09 mortgage bailout marked the start of a major bull market in U.S. stocks. This was partly because the Fed pushed the federal funds rate to zero and swapped cash for the trash toxic assets of securitized mortgage debt. This flooded the financial system with liquidity.

The future is now approaching. But what will the future bring? Namely, what type of bailout will the Fed, in concert with the Treasury, deliver? Will it be another top down bailout similar to 2008-09? Or will it be something entirely different?

We contend that it will be something dramatically different. This time around it’s no longer politically expedient for only the government sponsored enterprises and the big banks to get a bailout. The people are on to the Fed’s money games and demand a bailout too.

By this, the bailout will be from the bottom up. The Treasury will provide cash stimulus check payments – or directly credit bank accounts – to renters and homeowners so they can share in the spoils of a bailout.

Fannie and Freddie already have CARES Act programs to help those affected by the COVID-19 pandemic…including a moratorium on foreclosure and eviction until at least August 21, 2020. What you may not know is that this moratorium date has already been extended twice. Perhaps it’ll continue to be extended until ample government stimulus checks are beings sent out to the American populace on a monthly basis.

Our guess is that this sort of bottom up bailout will be less bullish for stocks. Though it will have a much more dramatic effect on consumer price inflation. In other words, the dollar will lose purchasing power against real goods and services. And eventually it’ll buckle, along with American living standards.

Moreover, the fantasyland world where the government pays everyone’s rent and mortgage, along with free school, free drugs, and free food, will be less sublime than what’s advertised.

Countless governments have tried throughout the ages. Without fail, these pursuits of miracles and purple fairy dust solutions always end in tears.

via ZeroHedge News https://ift.tt/2YDNGet Tyler Durden

More Adults Than Ever Live With Parents Or Grandparents Tyler Durden

Sat, 06/27/2020 – 15:30

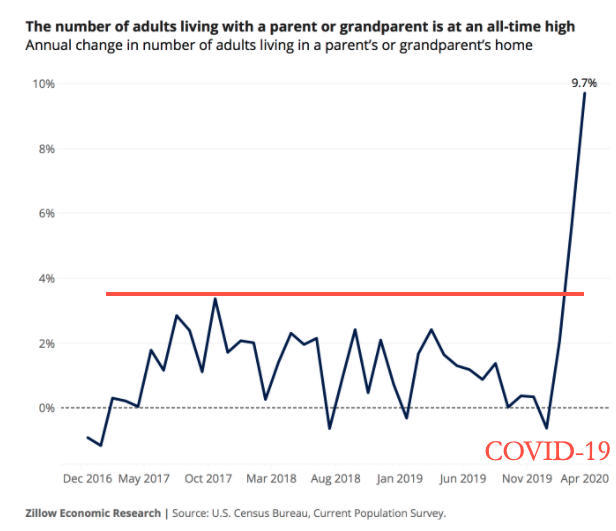

An absolutely shocking, new report via Zillow this month estimates 2.7 million adults moved in with a parent or grandparent in March and April as virus pandemic lockdowns crushed the economy.

The Zillow analysis shows 32 million adults lived with a parent or grandparent as of April, or about 10% of the entire population lives in their parent’s basement, the highest on record.

Many of those who moved back home in March and April, 2.2 million, were jobless millennials:

Employment and living situations among this young age group are generally the most in flux even in normal times, and the added uncertainty of the pandemic and future employment prospects makes this group even vulnerable to volatile swings in job and housing markets. Normally, the living arrangements of the 18-25 age group is quite seasonal (because of college terms and/or seasonal work), with a smaller share living at home in the spring months than in the summer months: Typically, 53%-to-55% of these adults live at home in April, compared to 55%-to-57% in July. But this April, that share surged as high as 61%, an unprecedented level.

But while students returning home after the nationwide closure of college campuses this spring is undoubtedly driving some of this surge, young adults were overwhelmingly driven back home by the major labor market swing in the wake of COVID-19. The number of employed young adults (aged 18-25) fell by more than 25%, or 5.9 million, in March and April. Roughly 60% of these workers that became unemployed in these months continued to look for employment, but more than 2 million were officially counted as no longer in the labor force. And while recently unemployed young people moved back home at roughly the same rate as usual (about 60% of them typically live with parents) the total number of them is bigger than ever.

Its not just newly jobless young Americans that are moving back home. Before the pandemic, almost half (46.5%) of employed young adults already lived in a parent’s home; by this April, the share had risen to 49%. Those who ceased looking for work altogether or were not in the labor force already, including a large number of students, were even more likely to move back home, adding another million-plus young adults to the ranks of homeward-bound movers. – Zillow

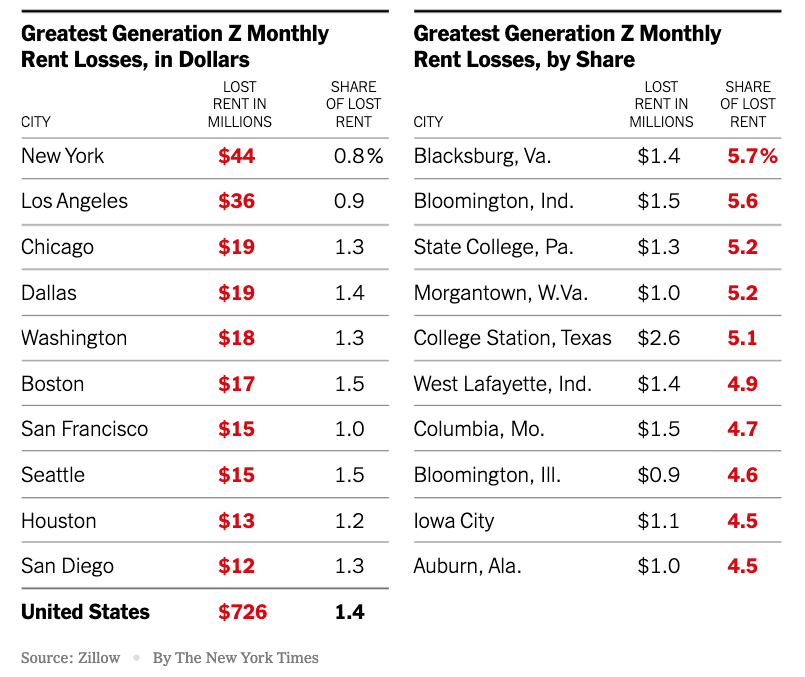

The great migration home, more precisely, to their parent’s basement, has been a major headache for landlords who now face lost rent. Zillow said Gen Zers who returned home in March and April represent lost rental income of $726 million a month.

The New York Times used Zillow data to show rental market losses by geographic area due to folks moving back home during the pandemic.

The trend of broke millennials moving home began well before the pandemic but has since been supercharged by the economic crash.

Over the years – we’ve noted the growing population of basement-dwelling millennials:

With no economic recovery in sight, maybe not until 2023 – expect more adults to move back home. This will have severe impacts on the economy – as consumption will slow – and the rental industry will flounder. The socio-economic collapse of this country will lead to years of slow growth and high unemployment.

via ZeroHedge News https://ift.tt/3eGhqNp Tyler Durden

The system is hurtling towards breakdown. Protect yourself now…

As you may know, I was one of the very first voices publicly reporting on covid-19, issuing an alert that the virus was a significant pandemic event on Jan 23rd, 2020.

This was long before most media outlets even managed to write their first “It’s just the flu, bro!” article.

Using the same logic and scientific methodology I was trained in as a PhD, I was able to “predict” things well in advance of nearly every official or mainstream news source.

I’m using quotation marks around the word “predict” because it’s not really a prediction when you’re just extrapolating trends that are already underway.

Just as it’s not really a “prediction” to estimate where a thrown pitch will travel, it wasn’t much of a prediction to state that a novel virus with an R-Naught (R0) of well over 3 would be extremely difficult to contain once it arrived in a country. Note that I didn’t say impossible — South Korea, Australia, New Zealand, Thailand, Taiwan and Vietnam all get high marks for containment — but certainly difficult.

The US and the UK proved this in spades, as they’re both led by below-average ‘managers’ rather than leaders.

Leaders make tough decisions based on imperfect information. Managers dither and hedge and only make up their minds after the facts are already in and events well underway. Naturally, the US/UK managers were simply no match for the exponential rate that the Honey Badger Virus (aka Covid-19) spreads at.

I call it the Honey Badger virus because of its incredible ability to evade quarantine, as eagerly and easily as Stoeffle, as seen in this short enjoyable video:

Such a determined foe as covid-19 cannot be reasoned with, halted by decree or – much to the puzzlement of the central banks – resolved by printing more thin-air money.

It simply operates by natural laws and rules. Which, by the way, makes it rather easy to predict.

Much more difficult to predict, though, is when we humans will truly wake up to our true plight and begin making better decisions. And I’m not just talking about the coronavirus here. I’m talking about the dangerous levels of social inequity that the Federal Reserve is responsible for creating, both pre- and post-covid-19.

Given the enormous difficulty in getting whole swaths of the managerial and retail classes to grasp such simple and obvious logic as “Everyone should wear a mask!”, it seems thoroughly unrealistic to expect these same folks to thoughtfully tackle the hazards of runaway monetary and fiscal policy.

But they really need to.

Why?

Because the current monetary and fiscal trajectory society is on has been well-trod throughout history. We know where it ends — no place we want to be.

Commerce gets destroyed. Households fail. Government and social order fall apart. Fairness and freedoms are lost as it becomes difficult to distinguish between official policies and overt looting.

Real leaders know this history and would both think and act differently in order to avoid the worst risks. But managers? They just keep operating from the same manual, mindlessly repeating the same steps while hoping for a different result.

The Fed’s Dangerous Gamble

I’ve referred to the Federal Reserve as a bunch of psychopaths engaging in cultural vandalism. This is unfair to both psychopaths and vandals.

After all, the most ambitious of them don’t victimize more than several dozen in their lifetime. Maybe a few hundred, tops.

But the Fed? It’s ruining hundreds of millions of lives and livelihoods — both today and in the future.

Sadly, the Federal Reserve has been doing this — unchecked — for a very long time. Here’s a snippet I wrote for MarketWatch.com 6 years ago. Every word remains as true today as it was then:

The academic name for the Fed’s current policy is financial repression. But a more apt name would be “Throw granny under the bus,” because the program boils down to taking from savers and fixed-income recipients and transferring that purchasing power to other entities.

The cornerstone element of financial repression is negative real interest rates, of which the Federal Reserve is the prime architect and owner.

From the start of the Fed’s post-crisis intervention through 2013, the total cost of these negative real interest rates was over $750 billion just to savers alone. The loss of income to fixed-income investments (such as bonds held in pensions and money markets) was even larger.

But here’s the rub. That loss of income and purchasing power didn’t just vanish. It was transferred from pocket A to pocket B.

It magically appeared again in record Wall Street banking bonuses, in shrinking government deficits (due to lower than normal interest rates), in rising corporate profits (mainly benefiting the already rich), in record stock buybacks (ditto), and in rising wealth inequality.

More directly, when the Fed buys financial assets with printed money and — by definition — drives up the price of those assets, it cannot then act mystified why the main owners of financial assets have grown wealthier. Doing so simply insults our intelligence.

Federal Reserve Chair Alan Greenspan, then Ben Bernanke, then Janet Yellen, and now Jay Powell have all operated as mere managers (not leaders) choosing predictably safe plays from the Federal Reserve cookbook. It prescribes a gruel-thin routine of actions the main ingredient of which is printing currency out of thin air.

Each Fed Chairman has dutifully cooked up unhealthy dishes seasoned with hefty amounts of social corrosion, structural unfairness, elitism, and without even a whiff of historical context.

With no leadership on display and cheered on by a compliant press unable to formulate a single critical question, the Fed is now too deep into its cookbook to do anything besides see the process out to its inevitable conclusion.

The Fed has long pretended to be mystified by the rising inequality its policies are obviously causing. Jerome Powell recently and (in)famously declared during Q&A after a speech that the Fed “absolutely does not” contribute to inequality. That bold-faced lie is infuriating to those who realize just how socially and culturally unfair and damaging the Fed’s actions really are.

When things become too unfair, people stop participating. If laws are too one-sided and rigged, people stop following them. If new hires receive a higher salary for equivalent work, the veteran employees stop working as hard. If students know that their classmates are cheating and getting good grades, they’ll begin to cheat, too.

It’s just how we’re wired. An aversion to unfairness is in our social DNA.

Peak Prosperity readers know I’m a huge fan of this short video. It explains everything about the rising tide of social rebellion in America (and features cute monkeys, to boot!):

By unfairly accelerating the wealth gap between the top 1% and everyone else, the Fed is playing with fire. Seemingly with the same level of ignorance to the consequences as a chimpanzee with a magnifying glass on the tinder-dry savannah.

Money is our social contract.

When that contract is broken, that’s when things really go south for a nation. Zimbabwe, the Weimar Republic, Venezuela and Argentina are all past (and some current again, sadly) examples of just how badly the standard of living can plummet when a nation’s money system breaks down.

The Inevitable

It’s much harder to predict exactly WHEN the Fed’s efforts will end in disaster as easily as I can predict that they will.

History is crystal clear: there has to always be a balance between money, which is a claim on thing, and the things themselves. Too many claims vs money and we get inflation. Too few and we get deflation.

The Fed and the other world central banks have always (always!) erred on the side of “too many claims” in this story. When in doubt, they print more currency.

And that process is now on hyperdrive. The post-covid economy is in a very bad state, and so the money printing at the heart of the “rescue” efforts by the central banks is the biggest ever in history. By a long shot.

So claims go up and up and up, while the economy shrinks. Leaving us with a LOT more money chasing a LOT less “stuff”.

This also applies to financial assets, like stocks and bonds. Printing makes the markets go higher in price and makes investors increasingly dependent on more money printing to support these prices. Eventually, like the era we’re in now, the Fed must keep injecting liquidity on a permanent basis or else the markets will immediately crash.

So, the money printing just keeps happening.

And as a side benefit, those closest to the Fed get stupendously rich from all that fresh money flooding into the world. These are the same Wall Street firms who hire Fed staffers at the end of their tenure there, thanking them with plush jobs that have little responsibility and huge salary.

But, out in real America, there are hundreds of millions of us angry monkeys watching the Fed stuff grapes into the already full bellies of the elites. Eventually wide-scale pushback against the Fed’s injustice will erupt. Protests will become larger and more violent. The police weill realize that they’re protecting the wrong people and switch sides. Then things should start getting really messy.

My strong preference in life is to avoid unnecessary pain and suffering. Why wait for the Fed to ruin everything for us? I’d prefer we get pro-active here to avoid a full-blown crisis. If don’t we’ll be forced to repeat history, whether we want to or not.

Sadly, repeating history and preserving the status quo is exactly what the national managers in the US are intent on doing. Most of the public still thinks of the Fed as the hero in this story instead of the villain it truly is, and so too much of the populace cheers the Fed along. The EU and the UK are more or less in the same boat.

All of which means that, just as I warned people to prepare for the covid-19 pandemic before it hit with full force, you need to prepare now for the coming Fed-created economic/social crisis.

In Part 2: Into The Light: 8 Steps For Surviving What’s Coming, in attempt to be as informative as possible, I share a tremendous volume of the critical data points I’m currently closely monitoring to determine where we are on the timeline to crisis and what’s most likely to happen next. I then provide my eight recommended steps for protecting your wealth, loved ones, and property through the challenges to come.

Minneapolis City Council Members Enjoy Costly Private Security Detail As Push To “Defund The Police” Continues Tyler Durden

Sat, 06/27/2020 – 14:30

A “veto-proof” majority of the Minneapolis City Council recently voted to abolish the city police department. And if it wasn’t for the opposition for the city’s Democratic mayor, Minneapolis would soon be sending social workers to investigate murder scenes.

But when it comes to their own protection, council members apparently aren’t embracing the second amendment, like many other liberals in solid-blue states, and instead are relying on the city to hire expensive round-the-clock security after members of the council received multiple death threats. Currently, the protection is costing taxpayers $4,500 to hire security for three council members.

Over the past three weeks, the bill for the city has come to more than $60,000.

The City of Minneapolis is spending $4,500 a day for private security for three council members who have received threats following the police killing of George Floyd. A city spokesperson said the private security details have cost the city $63,000 over the past three weeks.

The three council members who have the security detail – Andrea Jenkins (Ward 8), and Phillipe Cunningham (Ward 4), and Alondra Cano (Ward 9)– have been outspoken proponents of defunding the Minneapolis Police Department.

Unsurprisingly, council members didn’t want to discuss the arrangement with the press.

Councilmember Phillipe Cunningham declined to discuss the security measures.

“I don’t feel comfortable publicly discussing the death threats against me or the level of security I currently have protecting me from those threats,” said Cunningham in a text message.

Another councilmember, Andrea Jenkins, told Fox 9 that she has been pushing for a security detail since she was sworn in?

Why? Jenkins says the “large number of white nationalists in our city” and several “threatening communications” have given her reason to fear for her life.

Councilmember Andrea Jenkins said she has been asking for security since she was sworn in. She said current threats have come in the form of emails, letters, and posts to social media.

“My concern is the large number of white nationalist(s) in our city and other threatening communications I’ve been receiving,” wrote Jenkins in an email.

Councilmember Cano did not return messages seeking comment.

So, once the police department is gone, and Minneapolis is being policed by packs of taser-toting social workers, who is going to decide which residents deserve “protection” at city expense, and which won’t. While the mayor is typically given a security officer who is also his driver, the council members aren’t afforded similar protections.

Minneapolis mayors have traditionally had a security detail provided by a Minneapolis Police officer who also functions as the mayor’s driver. The thirteen council members are not given the same protection.

Asked why Minneapolis Police are not providing security services to the three council members, a city spokesperson said MPD resources are needed in the community. The hourly cost of private security is similar to the cost for a police officer, the spokesperson added.

A spokesperson for Minneapolis Police told FOX 9 the department does not have any recent police reports of threats against city council members. It is possible a report could have been filed confidentially.

Jenkins said she has not reported the threats to Minneapolis Police because she has been preoccupied with the dual crisis of the “global pandemic and global uprising” over the killing of George Floyd.

Jenkins added that the threats she has received have attacked her over her ethnicity, gender and sexuality.

Andrea Jenkins

Instead of being provided by the city police department (for politicians, optics always come first), the security detail is being provided by two firms, Aegis and BelCom. Fortunately, contracts like these must be approved by the city council, so the same politicians working to dismantle public security protections for ordinary citizens will likely enjoy stepped-up round-the-clock “protection” at taxpayer’s expense. Perhaps, when the councilmembers are ensconced in their chambers, hard at work on some pressing public business, these ‘security agents’ can be ‘repurposed’ to fetch coffee and dry cleaning.

via ZeroHedge News https://ift.tt/2YBorcK Tyler Durden

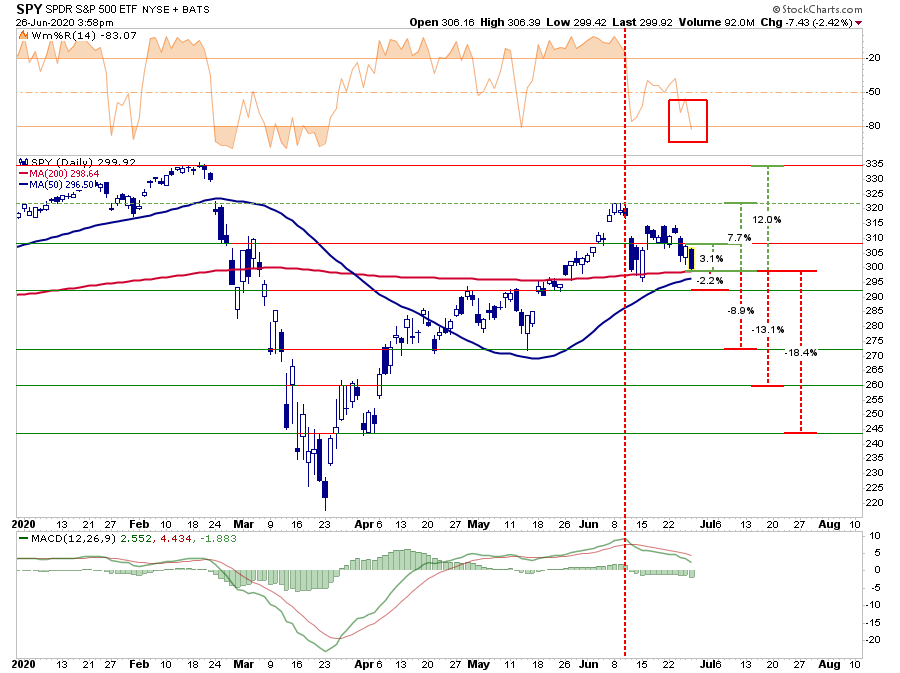

Three overriding catalysts were driving the correction this past week:

The market had gotten a good bit ahead of fundamentals.

The surge in COVID cases is undermining the V-Shaped recovery narrative.

End of the quarter portfolio rebalancing, which managers postponed in March.

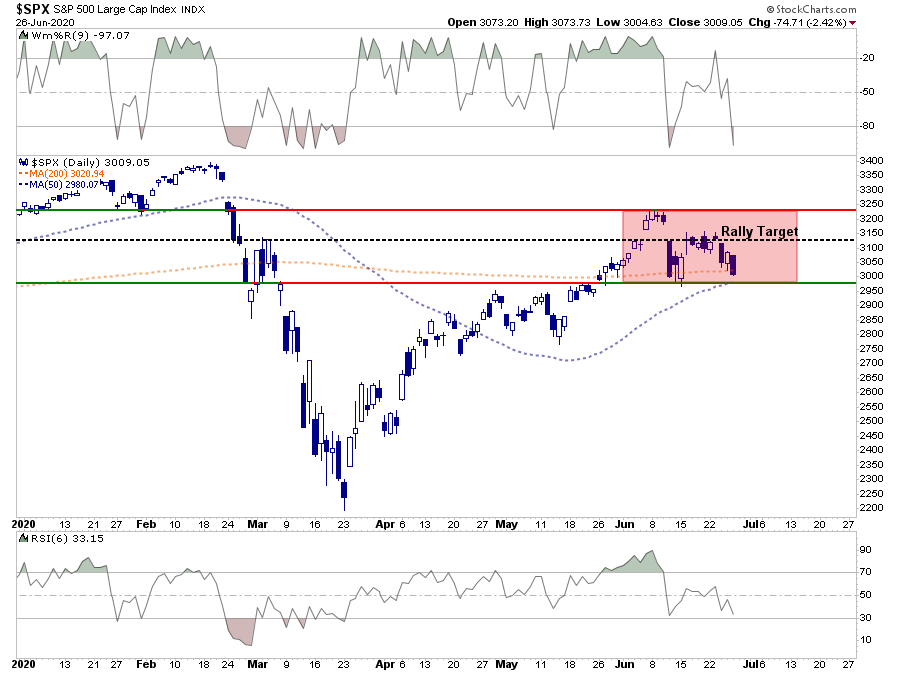

We will go through each of these in more detail. However, let’s start with where we left off last week and update our risk/reward ranges.

Currently, the risk/reward dynamics have become slightly less favorable. The good news is that the 50-dma and 200-dma are so close there is strong support short-term. Such should give the bulls a bit of optimism. However, a breakdown below that level and things will get ugly quickly.

-2.2% to consolidation highs vs. +3.1% to the top of the current downtrend. (Positive)

-8.9% to previous consolidation lows vs. +7.7% to previous rally peak (Negative)

-13.1% to March bounce peak vs. +12% to all-time highs. (Negative)

-18.4% to April 5th lows vs. +12% to all-time highs. (Negative)

As shown, with the sell-off on Friday, the short-term oversold condition, a reflexive rally next week would not be surprising. Given that COVID concerns are escalating, it may be wise to use any rally to reduce risk further and increase hedges.

The Market Is Well Ahead Of Fundamentals

Part of the correction over the last two weeks is coming partially from the realignment of stocks back to reality. We specifically mentioned some of the more visible issues last week, but it was interesting to watch the “Daytraders Favorites” crash back to Earth (No pun intended.)

“Furthermore, given the depth of the economic crisis, 49-million unemployed, collapsing wages and incomes, and a resurgence in the number of COVID-19 cases, estimates are still too high. During previous economic downturns, earnings collapsed between 50% and 85%. It is highly optimistic, given the current backdrop, that earnings will only decline by 20%.”

6 Downside Risks

With States now beginning to back off of reopening plans, it is highly likely current earnings estimates will need to be guided lower over the next couple of months.

The most significant risk to investors currently is a “reliance on certainty” about future outcomes, when, in reality, there is no certainty at all. As Mike Shedlock pointed out just recently, there are numerous risks still present.

Six Downside Risks

The future progression of the pandemic remains highly uncertain.

The collapse in demand may ultimately bankrupt many businesses.

Unlike past recessions, services activity has dropped more sharply than manufacturing—with restrictions on movement severely curtailing expenditures on travel, tourism, restaurants, and recreation and social-distancing requirements and attitudes may further weigh on the recovery in these sectors.

Disruptions to global trade may result in a costly reconfiguration of global supply chains.

Persistently weak consumer and firm demand may push medium- and longer-term inflation expectations well below central bank targets.

Additional expansionary fiscal policies— possibly in response to future large-scale outbreaks of COVID-19—could significantly increase government debt and add to sovereign risk.”

Again, the market is trading well ahead of underlying fundamentals. While the “Fed Put” may indeed put a “floor” below stocks, that doesn’t mean they can’t correct to realign with economic and fundamental realities.

COVID Makes A Second Appearance

As we discussed previously, the market rallied from the March lows based on 4-underlying premises:

There would be no second-wave of the virus.

There would be a vaccine available by year-end.

The economy would fully recover back to pre-pandemic levels.

And, of course, “The Fed.”

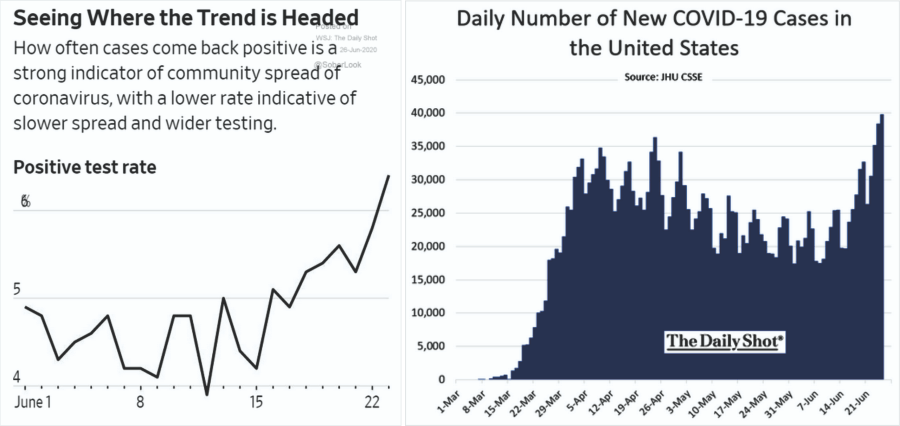

While the bullish fantasy indeed prevailed over the last couple of months, suddenly, the world has shifted. The hope was that cases in the U.S. would slow into the fall before the potential onset of a “second wave” during a more traditional “flu season.” Unfortunately, the spike in cases in the still ongoing “first wave” will delay economic recovery longer.

In Texas, where I live, the Governor has shut-down bars again, is keeping businesses at reduced capacity, and potentially will reverse more if needed.

My wife went to the doctor recently for a test, and she received the “ole’ swap up the nose.” While the test came back negative. The doctor told my wife that COVID lives in the lungs and not the nasal cavity. Therefore, while her test was negative, it could be a false negative. If the doctor is correct, the real numbers of infected could be 10x higher. Such confirms a recent Reuters article:

“Government experts believe more than 20 million Americans could have contracted the coronavirus, 10-times more than official counts, indicating many people without symptoms have or have had the disease, senior administration officials said.

The estimate, from the Centers for Disease Control and Prevention, is based on serology testing used to determine the presence of antibodies that show whether an individual has had the disease, the officials said.”

If true, the ramifications could substantially impair the bullish thesis.

Timing Couldn’t Be Worse

Without a bill to extend more Federal Aid via Payroll Protection Programs and increased unemployment benefits, the ongoing restriction on trade will likely lead to a further surge in bankruptcies and layoffs.

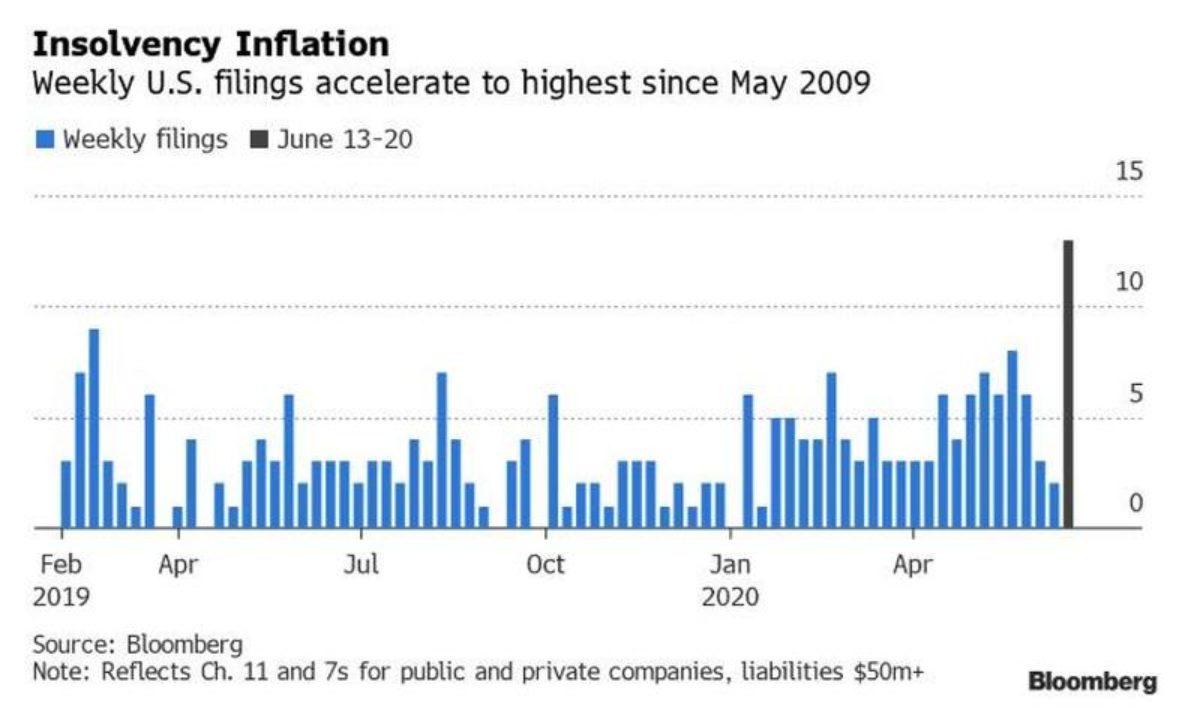

“According to Bloomberg data, no less than 13 U.S. companies sought bankruptcy protection last week, matching the global financial crisis’s peak. The filings, led by the perennially weak consumer and energy sectors, were the most for any week since May 2009.”

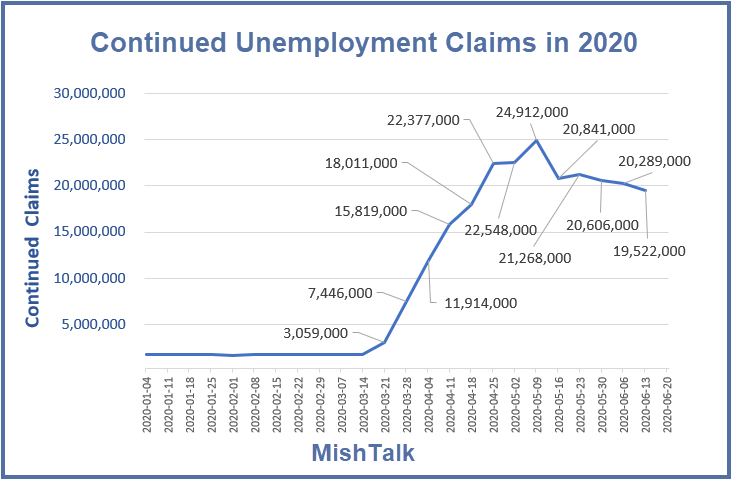

There is a virtual spiral between job losses and bankruptcies. As more individuals lose their jobs, they have less to spend. Since consumption is what drives earnings for businesses, they have to lay off workers to stay in business. Pay attention to the “continuing claims,” which will tell the story of the economic recovery. (That doesn’t look like a “V”)

End Of The Quarter Rebalancing

There was one other factor which has weighed on stocks this past week, which was noted recently by Zerohedge:

“When adding all the other possible sources of the month- and quarter-end forced rebalancing, the total amount ‘for sale’ soars to an unprecedented $170 billion according to calculations by JPMorgan.

In the latest Flows and Liquidity report from JPM’s Nikolas Panagirtzoglou, writes that after correctly pointing out at the market lows on March 23rd that there is a massive $1.1 trillion in rebalancing flow into equities, all of that has since balanced out, and three months later, we are looking at a substantial outflow of about $170BN before month-end, resulting in a ‘small correction.’”

This rebalancing of portfolios was postponed by pension and mutual funds in March as they did not want to sell at market lows. That decision worked out well then, but now they need to rebalance portfolios by selling equities and buying bonds. We can see this action by looking at the performance between the S&P 500 index and Treasury Bonds over the last two weeks.

This rotation is either likely close to completion, or will complete early next week. As we stated previously, this is why we hedge our equity portfolios with fixed income. The risk offset reduces downside volatility and allows the portfolio to weather tough patches in the market.

With the market very oversold short-term, it would not be surprising to see a reasonably decent reflexive rally into the start of July. However, that rally will likely be an excellent opportunity to rebalance risk and rethink exposures accordingly.

Portfolio Positioning Update

As stated last week, with our portfolios almost entirely allocated towards equity risk in the short-term, we remain incredibly uncomfortable.

Our positioning in fixed income and gold has hedged the portfolio against the latest decline in the very short-term. Still, with the market getting very oversold short-term, as shown below, we expect a reflexive rally off of current support next week.

Most likely, we will use any counter-trend bounce to reduce equity risk a bit, rebalance exposures, and focus our attention on capital preservation for the next couple of months. With the virus resurfacing, the potential risk of disappointment to the earnings and economic recovery story has risen.

While it is easy for the mainstream media to write articles and post comments about the markets, it is an entirely different matter when you manage money. Currently, there is a battle raging between the fundamental and “hope” driven narratives.

On the one hand, it’s easy to see the fundamental problems in the market and the economy, which argues for much less risk exposure. However, on the other, you have the Fed and a Government, ready to throw money at, and “jawbone,” the markets at a moment’s notice.

Trying to navigate the two is like trying to thread a needle, in a moving car, on a bumpy road, with your eyes closed. Given we aren’t prescient, we will have to resign ourselves to doing the best job we can for our clients with the information we have available.

That is a fancy way of saying, “we are going to give it our best guess.”

The goal remains the same as always, protect our client’s capital, reduce risk, and try to come out on the other side in one piece.

Sometimes, however, it just gets messy.

via ZeroHedge News https://ift.tt/2CEjKWT Tyler Durden

Below is my column in The Hill on the ongoing destruction of memorials and statues. After this column ran, I learned that one of the iconic busts of George Washington University had been toppled on my own campus. I did not learn that from our university, which was conspicuously silent about this destructive act at the very center of our campus. There is something eerily familiar in the scenes of bonfires with police watching passively as public art is destroyed. Such acts are akin to book burning as mobs unilaterally destroyed images that they do not want others to see. There are valid issues to address on the removal of some public art but there is no room or time for debate in the midst of this spreading destruction. The media has largely downplayed this violence, including little comparative coverage of an attack on the Democratic state senator who simply tried to videotape the destruction of a statue to a man who actually gave his life fighting against slavery in the Civil War. As discussed earlier, history has shown that yielding to such mob rule will do little to satiate the demand for unilateral and at times violent action. People of good faith must step forward to demand a return to the rule of law and civility in our ongoing discourse over racism and reform.

The scenes have played out nightly on our television screens. In Portland, a flag was wrapped around the head of a statue of George Washington and burned. As the statue was pulled down, a mob cheered. Across the country, statues of Christopher Columbus, Francis Scott Key, Thomas Jefferson, and Ulysses Grant have been toppled down as the police and the public watch from the edges. We have seen scenes like this through history, including the form of mob expression through book burning.

Alarmingly, this destruction of public art coincides with a crackdown on academics and writers who criticize any aspects of the protests today. We are experiencing one of the greatest threats to free speech in our history and it is coming, not from the government, but from the public. For free speech advocates, there is an eerie candescence in these scenes, flames illuminating faces of utter rage and even ecstasy in destroying public art. Protesters are tearing down history that is no longer acceptable to them. Some of this anger is understandable, even if the destruction is not. There are statues still standing to figures best known for their racist legacies.

Two decades ago, I wrote a column calling for the Georgia legislature to take down its statue of Tom Watson, a white supremacist publisher and politician who fueled racist and antisemitic movements. Watson was best known for his hateful writings, including his opposition to save Leo Frank, a Jewish factory manager accused of raping and murdering a girl. Frank was taken from a jail and lynched by a mob enraged by such writings, including the declaration of Watson that “Frank belongs to the Jewish aristocracy, and it was determined by the rich Jews that no aristocrat of their race should die for the death of a working class Gentile.”

Yet today there is no room or time for such reasoned discourse, just destruction that often transcends any rationalization of history. Rioters defaced the Lincoln Memorial in Washington and a statue of Abraham Lincoln in London. Besides attacking those monuments to the man who ended slavery, rioters attacked statues of military figures who defeated the Confederacy, like Grant and David Farragut, who refused to follow Tennessee and stayed loyal to the Union. In Boston, rioters defaced the monument to the 54th Massachusetts Infantry, the all black volunteer regiment of the Union Army. In Philadelphia, the statute of abolitionist Matthias Baldwin was attacked, despite his fight for black voting rights and his financial support for the education of black children.

This systematic destruction of public art is now often rationalized as the natural release of anger by those who have been silenced or marginalized. Even rioting and looting has been defended by some as an expression of power. However, a far more extensive movement is unfolding across the country, as people are fired for writing in opposition to these protests. In Vermont, Windsor School principal Tiffany Riley was placed on leave for questioning protest rhetoric on Facebook, where she posted, “While I understand the urgency to feel compelled to advocate for black lives, what about our fellow law enforcement?” She was denounced on social media as “insanely tone deaf” and is being forced to retire.

At the University of Chicago, there is an effort to fire Harald Uhlig, who is a professor and senior editor of the prestigious Journal of Political Economy. His offense was questioning the logic of defunding the police and other messaging from the protests. Writers like Paul Krugman of the New York Times denounced him, and he was accused of the unpardonable sin of “trivializing” the Black Lives Matter movement. Professors across the country are being targeted because they object to aspects of these protests or specific factual claims. Students also face punishment.

Syracuse University student journalists at the Daily Orange have fired a columnist for writing a piece in another publication that questioned the statistical basis for claims of “institutional racism” in police departments. Adrianna San Marco discussed a study published last year by the National Academy of Sciences that had found “no evidence” of disparities against Blacks or Hispanics in police shootings. Such a view could be challenged on many levels. Indeed, this once was the type of debate that colleges welcomed. Yet San Marco was accused of “reinforcing stereotypes.”

The merging of journalism and advocacy is evident in academia, where intellectual pursuit is now viewed as reactionary or dangerous. Many opposed a recent recognition given by the American Association of University Professors to an academic viewed by many as antisemitic. I disagreed with the campaign against the professor as a matter of free speech. However, I was struck by the statement that she “transcends the division between scholarship and activism that encumbers traditional university life.” That “encumbrance” was once the distinction between intellectual and political expression. As academics, we once celebrated intellectual pluralism and fiercely defended free speech everywhere.

However, we now increasingly join the mob in demanding the termination or “retraining” of academics who utter opposing views. In my 30 years of teaching, I never imagined I would see such intolerance and orthodoxy on campuses. Indeed, I have spoken with many professors who are simply appalled by what they are seeing but too scared to speak up. They have seen other academics put on leave or condemned by their fellow faculty members. Two professors are not only under investigation for criticizing the protests but received police protection at home due to death threats. The chilling effect on speech is as intentional as it is successful.

Such cases are mounting across the country as academics and students enforce this new orthodoxy on college campuses. What will be left when objectionable public art and academics are scrubbed from view? The silence that follows may be comforting to those who want to remove images or ideas that cause unease. History has shown, however, that orthodoxy is never satisfied with silence. It demands speech.

Once all the offending statues are down, and all the offending professors are culled, the appetite for collective suppression will become a demand for collective expression. It is a future that is foreshadowed not in loud cries around the bonfires we see every night on the news. It is a future guaranteed by the silence of those watching from the edges.

via ZeroHedge News https://ift.tt/3g3A0z7 Tyler Durden

{kind=link}