Get Ready For Disinfected Dice As Vegas Plans Reopening Tyler Durden

Sun, 05/24/2020 – 23:00

Nevada’s gaming industry could reopen as soon as June 4, Gov. Steve Sisolak stated Friday. The Nevada Gaming Control Board will meet next week with health officials to determine which sanitation protocols are needed at casinos before reopening.

“The board is firmly aware of its statutory duty to protect the public health and welfare of the Silver State’s citizenry while allowing the gaming industry to flourish through strict regulation,” Sisolak said in a statement.

Additionally, the Gaming Control Board will meet Tuesday & will consider any action necessary with regard to reopening. Pending the evaluation of trends in our data and results of this meeting, I have set a target date of June 4, 2020, for reopening Nevada’s gaming industry.

Casinos are expected to submit reopening safety plans to the board next week. When gamblers step inside the casino floor, they will be immediately greeted by staff and screened at temperature check stations. All employees and patrons will be required to wear masks. Table games will have reduced capacity, for instance, there could be three players per blackjack table instead of six. Also, one could expect sanitation stations across the entire property — a move to limit the spread of the virus.

While playing games, dice will be disinfected between shooters, chips, and cards will be routinely swapped out. Resort guests at some casinos will go all-digital via their smartphone — this means phones will be used for touchless check-in, used as room keys, and even used to read menus at the facility’s restaurant(s).

“You’re going to see a lot of social distancing,” Sean McBurney, GM at Caesars Palace, told AP News. “If there’s crowding, it’s every employee’s responsibility to ensure there’s social distancing.”

Wynn Resorts properties and The Venetian will deploy thermal cameras on gaming floors to intercept people with feverish conditions.

Bill Hornbuckle, CEO and president of MGM Resorts International, said his company is losing $10 million per day during the shutdown. He said only 2 of its 10 Strip properties would open first: Bellagio and New York-New York.

Hornbuckle said because of social distancing and new rules, and there will be a lot “fewer people, by control and by design” in his casinos.

Caesars Entertainment is expected to reopen Caesars Palace and the Flamingo Las Vegas, then Harrah’s Las Vegas and the casino floor at The LINQ hotel-casino.

Robert Lang, executive director of the Brookings Mountain West, a think tank at the University of Nevada, said large crowds are not expected to return quickly to the Vegas strip.

Lang is correct, just like the airline industry – which Boeing CEO’s Dave Calhoun recently warned air travel growth might not return to pre-corona levels for several years – the same should be noted for Vegas.

With Vegas imploded, and 1 in 3 jobs in the state tied to the resort industry, Nevada’s unemployment rate has jumped to almost 30% in nine weeks, the worst-ever unemployment rate in state history and the highest in the country.

Getting back to normal, or merely revisiting 2019 growth rates, for the Vegas casino industry and or the economy as a whole, will take several years or more.

via ZeroHedge News https://ift.tt/2zrsoqz Tyler Durden

China Sets Yuan Fix At Weakest Since 2008 Tyler Durden

Sun, 05/24/2020 – 22:32

Just hours after China’s Foreign Minister Wang Yi warned that “some” in America were pushing relations to a “new Cold War”, Beijing made it clear how it intends to retaliate in this new paradigm: by doing the one thing that infuriates Trump more than anything, devaluing its currency.

After the PBOC fixed the yuan at 7.0939 on Friday, the PBOC set the Monday USDCNY midpoint at 7.1209, which was not only weaker than the expected fix of 7.1205 but the weakest fixing since 2008.

Zooming in on the past 10 days shows the sharp bounce in the past three days in both the fixing, the onshore and the offshore yuan, the last of which is now just shy of the lows hit during the March crash, if still below the all time lows hit on Sept 2, 2019 when the USDCNH spiked as high as 7.1940 in response to the escalating trade war.

That said, some – such as Bloomberg – had a different expectation for the fixing, which they saw as 7.1220, which would in turn mean a stronger than expected fixing, and one suggesting that the PBOC has activated its countercyclical buffer to slow the drop of the onshore yuan as the offshore yuan slumps. Their conclusion, which is counter to sellside expectations, is that this marks a shift in the PBOC’s countercyclical adjustments and “could be seen as a warning shot toward speculators betting on a weaker yuan.”

Whether Bloomberg’s fixing model is correct, or consensus expectations for a stronger fix are right, remains to be seen however if indeed it is China’s stance to devalue the yuan in response to the sharp deterioration in Sino-US relations then expect the offshore yuan to take the lead and to keep sliding, giving the PBOC cover for further devaluation and telegraphing how it plans on responding to the “cold war” and any future escalations by the US.

Ironically, the very same Bloomberg, in a different report, notes that “the spread between spot USD/CNH and USD/CNY is likely to become more volatile in coming days, driven by a widening bias. A combination of U.S.-China political tension and unrest in Hong Kong will provide a negative feedback loop into the offshore yuan.”

The PBOC can be expected to maintain a tight grip on the daily yuan fixing and enforce the 2% fluctuation range. But there is no such constraint for the offshore yuan, which is free to roam, only being pulled back into line by FX arbitrageurs or in response to speculation about central bank intervention.

As author Mark Crankfield writes, “the CNH forwards curve can also be expected to see an upward trajectory. The spread spiked to more than 10 big figures several times during previous periods of yuan turbulence. A similar outcome is likely in the near term, as investors consider what the threat of a new cold war will mean for risk assets.“

One thing to note: the last time the offshore yuan was here, the S&P was at 2,300.

Finally, here is a reminder from Rabobank’s Michael Every why in the current environment of escalating hostility between the US and China, the only thing that matters is the Yuan, and why in the not too distant future, the Chinese currency may have a 10-handle in front of it.

This time last year, when we were all still going abroad regularly (right now just ‘outside’ is becoming a psychological barrier if I am honest) I was traveling with a presentation titled “Clause is Cause”. This argued that from a geostrategic ‘Von Clausewitz’ perspective, not a neoliberal “Let’s assume world peace” version, the US would at some point realise the USD/Eurodollar was a weapon it could wield vs. China, and when it did we would see three key strings cut: trade; tech; and then capital flows. The first was evident during the trade war – which has not been concluded is likely to get far worse soon; the second is also abundantly clear on a variety of fronts, much to Silicon Valley’s chagrin; and potentially, now we see the start of that third step – because if the US does block this first USD50bn going in, other such steps will follow, just as they did on the previously unthinkable idea of US tariffs on China.

CNH is right to be selling off, albeit in a traditionally limited fashion, because if you don’t buy from China and you don’t help China up the value-chain and you don’t invest in China then China is not going to be getting much USD liquidity at all. The US hawks probably don’t get the Eurodollar iron logic there; they are likely just pressing buttons in anger. The outcome would be the same nonetheless.

I can hear the market bulls and technocrats of the world saying “But China has USD3 trillion in reserves!” Perhaps. Most think it’s far lower than that. And not earning USD means you have to dig into that stockpile. And when you do, the PBOC either has to contract the local money supply (because every USD is backed by 7.xx CNY on the other side of the balance sheet) or it just creates new CNY anyway and supply-demand sees CNY move sharply lower – as we have been seeing in all other EM FX. Looking at the drop in BRL, ARS, ZAR, TRY, etc., or even THB,this would be how we would get to the ‘unthinkable’ 8 (9? 10?) handle in CNY. That would also crush those other EM crosses in tandem – and AUD and NZD, as the former tries to navigate its own geopolitical spat with Beijing.

And so with the Fed having taken over most US capital markets which have now lost most if not all of their discounting and signaling capabilities, keep an eye on that USDCNH: ironically, it may be the last true market stress indicator left.

via ZeroHedge News https://ift.tt/2zrxK5c Tyler Durden

Gun Battle Unfolds At Residential Complex Near Moscow Tyler Durden

Sun, 05/24/2020 – 22:05

A gun battle unfolded at a residential complex called “Yasny” in the south region of Moscow on Sunday, reported TASS News. Residents saw men firing AK-47s and other weapons on the streets below their windows.

“On the territory of Yasnoy, unidentified people opened fire on each other. At present, the police put on the wanted list cars that are supposedly hiding the incident participants – Mercedes, Ford, Toyota,” a law enforcement agency spokesperson told TASS.

The spokesperson said at least eight people were involved in the shootout.

“They shot at each other with traumatic pistols and, presumably, from the Saiga and Vepr hunting rifles.”

So far, the incident has resulted in “no casualties, and a police search has been launched for at least eight people,” said RT News. Police have yet to release a motive behind the gun battle.

via ZeroHedge News https://ift.tt/2ZxWKlT Tyler Durden

Countries across the world have been in lockdown for months in response to the coronavirus pandemic. The costs of the policy are enormous – in terms of life, liberty and the economy. But is it worth it to save lives?

Yoram Lass was once the director-general of Israel’s Ministry of Health. Lass is a staunch critic of the lockdown policy adopted in his native Israel and around the world. He has described our response to Covid-19 as a form of hysteria. spiked caught up with him to find out more…

spiked: You have described the global response to coronavirus as hysteria. Can you explain that?

Yoram Lass:It is the first epidemic in history which is accompanied by another epidemic – the virus of the social networks. These new media have brainwashed entire populations. What you get is fear and anxiety, and an inability to look at real data. And therefore you have all the ingredients for monstrous hysteria.

It is what is known in science as positive feedback or a snowball effect. The government is afraid of its constituents. Therefore, it implements draconian measures. The constituents look at the draconian measures and become even more hysterical. They feed each other and the snowball becomes larger and larger until you reach irrational territory. This is nothing more than a flu epidemic if you care to look at the numbers and the data, but people who are in a state of anxiety are blind. If I were making the decisions, I would try to give people the real numbers. And I would never destroy my country.

spiked: What do the numbers tell us, in your view?

Lass:Mortality due to coronavirus is a fake number. Most people are not dying from coronavirus. Those recording deaths simply change the label. If patients died from leukaemia, from metastatic cancer, from cardiovascular disease or from dementia, they put coronavirus. Also, the number of infected people is fake, because it depends on the number of tests. The more tests you do the more infected people you get.

The only real number is the total number of deaths – all causes of death, not just coronavirus. If you look at those numbers, you will see that every winter we get what is called an excess death rate. That is, during the winter more people die compared to the average, due to regular, seasonal flu epidemics, which nobody cares about. If you look at the coronavirus wave on a graph, you will see that it looks like a spike. Coronavirus comes very fast, but it also goes away very fast. The influenza wave is shallow as it takes three months to pass, but coronavirus takes one month. If you count the number of people who die in terms of excess mortality – which is the area under the curve – you will see that during the coronavirus season, we have had an excess mortality which is about 15 per cent larger than the epidemic of regular flu in 2017.

Compared to that rise, the draconian measures are of biblical proportions. Hundreds of millions of people are suffering. In developing countries many will die from starvation. In developed countries many will die from unemployment. Unemployment is mortality. More people will die from the measures than from the virus. And the people who die from the measures are the breadwinners. They are younger. Among the people who die from coronavirus, the median age is often higher than the life expectancy of the population. What has been done is not proportionate. But people are afraid. People are brainwashed. They do not listen to the data. And that includes governments.

spiked: Do the lockdowns have any positive effect on people’s safety?

Lass:Any reasonable expert – that is, anyone but Professor Ferguson from Imperial College who would have locked down everybody when we had swine flu – will tell you that lockdown cannot change the final number of infected people. It can only change the rate of infection. And people argue that by changing the rate of infection and ‘flattening the curve’, we prevented the collapse of hospitals. I have shown you the costs of lockdown, but this was the argument in favour of it. But look at Sweden. No lockdown and no collapse of hospitals. The argument for the lockdown collapses.

spiked: Why have some countries suffered so much more than others from Covid-19?

Lass: For example, you can compare Italy to Israel. In the Middle East, this virus is not really working. There are two reasons. One is that there is a very young population, and the other is that the climate is different. In the latitude of 50 degrees, which is Europe, and 40, which is the north-eastern United States, the virus is much more viable. Italy has the oldest population in the world apart from Japan. Italians are also are heavy smokers and very social people – they keep hugging and kissing. If you look at the numbers, in 2017, 25,000 Italians died from flu complications. Now you have around 30,000 dying from coronavirus. So it is a comparable number. You should not ruin a country for comparable numbers.

spiked: What has it been like in Israel?

Lass: In Israel, we have two layers of fear. The hysteria is similar to the rest of the world. However, we have a prime minister who has been resuscitated by coronavirus by adding another layer of fear. I do not think there is any other prime minister who has spoken about coronavirus in terms of the medieval Black Death, the Holocaust and the end of humanity in this way. Did Boris Johnson mention the Black Death? I do not think so. That is the special situation in Israel.

spiked: How does coronavirus compare to past pandemics?

Lass:If you look at the 1950s, we had the Asian flu. In the 1960s, there was the Hong Kong flu. These were worse than this pandemic. Also, look at the story of swine flu in 2009, which began exactly the same as coronavirus. A new virus originated in Mexico. There was no vaccine so it was very frightening. It spread all over the world. It infected one billion people. A quarter of a million people died. But there was no lockdown, no Ferguson, nothing – people were far more interested in the economic crisis that hit a year before in 2008. They did not have time to give attention to this nonsense.

spiked: Will the pandemic be over soon?

Lass: The virus, like the influenza virus, is saying farewell to western Europe for sure. The same in the Middle East. In the United States, we do not know yet, so we should talk in a month from now. But nothing can justify this destruction of people’s lives. It is unbelievable.

via ZeroHedge News https://ift.tt/2ZxUcUT Tyler Durden

The Fed Is Now The Proud Owner Of Bankrupt Hertz Bonds Tyler Durden

Sun, 05/24/2020 – 21:27

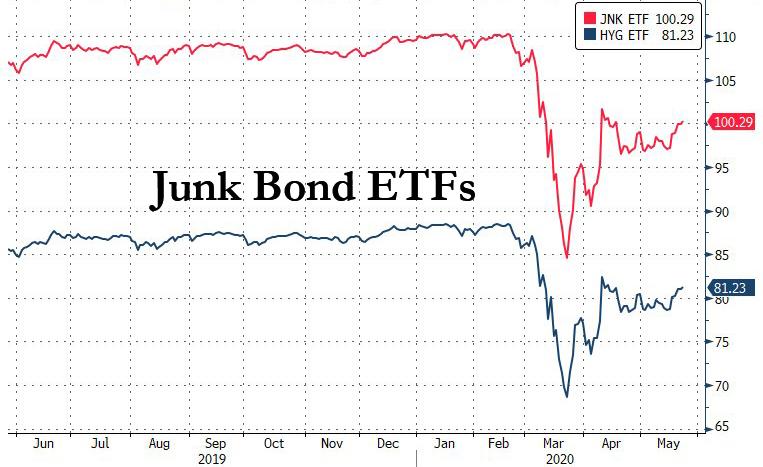

On March 23 – the day the S&P dropped to its cycle low of 2,237 – the Fed stunned capital markets when it announced it would purchase investment grade corporate bonds, traversing a Rubicon into secondary market intervention that not even Ben Bernanke had dared to cross. A few weeks later, on April 9, the Fed doubled down by announcing it would purchase not only junk bonds from “fallen angel” issuers (an announcement which came just days after a quarter in which a record $150BN in investment grade bonds were downgraded to junk, starting the long awaited tsunami of “fallen angels”), but would also buy junk bond ETFs such as HYG and JNK.

This is what the Fed’s Secondary Market Corporate Credit Facilities term sheet said on this topic:

The Facility also may purchase U.S.-listed ETFs whose investment objective is to provide broad exposure to the market for U.S. corporate bonds. The preponderance of ETF holdings will be of ETFs whose primary investment objective is exposure to U.S. investment-grade corporate bonds, and the remainder will be in ETFs whose primary investment objective is exposure to U.S. high-yield corporate bonds

Naturally, the news was enough to send junk bonds ETFs such as JNK and HYG soaring.

One month later, following a surge in inquiry including from the bond king Jeff Gundlach as to when the Fed would actually start buying corporate bond ETFs, the Fed realized it would not be able to jawbone markets any more and would have to put its money where its term sheet was, and on May 11 the NY Fed said it would “begin purchases of exchange-traded funds (ETFs) on May 12.”

And while the central bank said the focus of its ETF purchases would be on IG-focused ETFs, the New York Fed also disclosed it would start buying junk bonds ETFs as well:

As specified in the term sheet, the SMCCF may purchase U.S.-listed ETFs whose investment objective is to provide broad exposure to the market for U.S. corporate bonds. The preponderance of ETF holdings will be of ETFs whose primary investment objective is exposure to U.S. investment-grade corporate bonds, and the remainder will be in ETFs whose primary investment objective is exposure to U.S. high-yield corporate bonds.

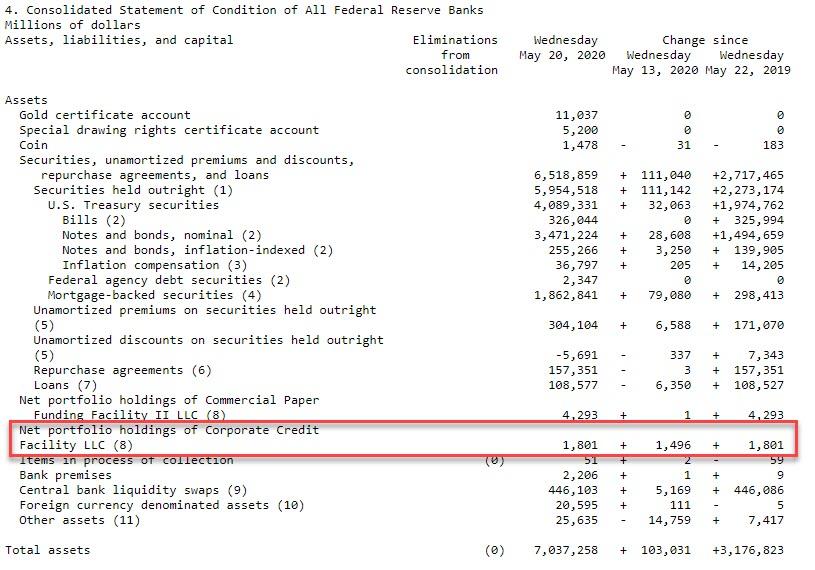

Then, last Thursday, we reported that as part of the Fed’s record balance sheet, which for the first time ever surpassed $7 trillion, the Fed disclosed that it also held $1.8 billion under Corporate Credit Facility holdings, the line item that include purchases of both investment grade (LQD) and junk bonds ETFs (HYG, JNK, etc).

This came two days after Powell defended the Fed’s program to buy junk bonds during his testimony before the Senate Banking Committee, which asked how purchases of junk bonds is “helping folks on Main Street.” Powell flagged that the Fed allowed for buying bonds from so-called “fallen angels” to ensure there is “no cliff” between the two lending markets (even though as we pointed out previously, a clear cliff has formed), saying “we don’t want to have a cliff there to where investment grade markets are working well, but the leveraged markets are not, non-investment grade markets are not.”

He then added that “we made a very limited, narrow set of actions to support market function in these markets, including buying ETFs, and that’s had an effect to improve market function there.”

Powell concluded by saying “we’re not buying junk bonds generally across the board at all,” which of course is correct: he is merely buying ETFs that have junk bond constituents.

And this is where the Fed’s first major test of directly manipulating and intervening in market functioning is about to take place.

While the Fed’s H.4.1 statement does not breakdown how much of the $1.8 billion in ETF holdings is allocated to investment grade and how much is junk, it is safe to say that at least $1 dollar of that amount has been allocated to purchases of Junk ETFs.

That will be a problem for Powell, because a quick scan of the holdings of both HYG and JNK reveals that these junk bonds ETFs own, among the hudnreds of other securities, several bonds from the just defaulted rental giant, Hertz.

Here are HYG’s holdings of HTZ bonds: they amount to just over $50MM in face value across 4 bonds (out of a total of $23.3BN in holdings across just over 1,000 bonds).

And here is JNK: just under $$30MM in notional across 3 CUSIPs out of a total of $11.55BN in total assets in the ETF.

And yes, for those asking, both ETFs hold that infamous Hertz bond that was issued last November and that will default before paying a single coupon.

To be sure, we can only extrapolate but it is safe to say that the Fed’s holdings of both these ETFs are modest for the time being, and we assume that the bulk of ETF purchases have targeted the investment grade, LQD ETF; still the fact is that as of this moment, the Fed is a holder, via BlackRock and via HYG and JNK, of bonds which are in default, and which make the Fed a part of the Hertz post-petition equity once it emerges from bankruptcy!

This means that unless the Fed somehow manages to divest of Hertz bonds that comprise its HYG and JNK holdings, the US central bank is as of this moment a stakeholder in the Hertz bankruptcy process, and assuming there is no liquidation, will end up owning a pro-rata stake of the post-petition equity once the company emerges from bankruptcy in the not too distant future.

What happens then nobody knows: will the Fed take a vocal position in the company’s future? Can the Fed even own equities via a debt-to-equity swap? What happens when hundreds of other junk bonds default and the Fed ends up owning billions in post-petition equity pro forma for equitization?

We don’t know; we doubt anyone on Wall Street or in Congress knows. And we are certain that the Fed itself doesn’t know, because in its scramble to stabilize the bond market, it forgot that once companies file for bankruptcy (certainly there is no discussion in the Fed’s term sheets of what happens once its corporate bond holdings default) the Fed will – sooner or later – end up being an equityholder.

As a reminder, the ECB was faced with a similar scandal in Dec 2017 when it ended up holding bonds of insolvent Steinhoff, but back then Mario Draghi quickly liquidated the bonds and the market pretended nothing ever happened. The problem for Powell is that one look at the HYG and JNK holdings reveal dozens if not hundreds of companies which will file for bankruptcy within months if not weeks, suggesting the Hertz debacle is just the start of a bankruptcy flood in which the Fed will emerge as a key actor in bankruptcy court and Powell will have to explain away why it is now an equity stakeholder of bankrupt companies.

We eagerly look forward to Powell answering all these questions, hopefully as soon as this Friday when the Fed chair holds yet another video conference.

via ZeroHedge News https://ift.tt/2ZtwxVE Tyler Durden

Young People Are Rushing To Leave Big Cities In Favor Of “Less Infected” Suburbia Tyler Durden

Sun, 05/24/2020 – 21:15

There’s no doubt that the long-lasting impact of the coronavirus pandemic will include a major shift in how consumers look at homebuying. In fact, have already reported here on Zero Hedge about how many are leaving the city in favor of life in the suburbs, since the virus has spread faster in city areas.

Now, it looks as though the younger generation is following the cues of the older generation and doing the same. The effects could be pronounced, especially since the younger generation was responsible for the boom in many U.S. cities over the last decade.

That includes people like Desiree Duff, who Bloomberg highlighted late last week. A former NYC bartender, she has left her apartment in Brooklyn to move back in with her parents in South Carolina. She is currently using unemployment to pay her part of the rent and says that she is stuck “rethinking” the appeal of living in the big city.

She said: “Not knowing what my future there looks like does make me reconsider. Maybe after my lease is done I should move elsewhere, to a smaller city that was less infected, as much as that breaks my heart.”

Duff/BBG

Her move is a microcosm of a larger shift for the younger generation, which is leaving apartments empty in cities across the U.S.

Deniz Kahramaner, the founder of data-driven real estate brokerage Atlasa said: “The draw of the city is the social life, the dating scene, bars, restaurants, the ability to do fun things on the weekend. Without those attractions, it makes a lot of sense to just abandon ship and go back to your parents.”

Charley Goss, government and community affairs manager at the San Francisco Apartment Association said: “It’s a really hard time for the renter, but it’s a really hard time for the housing provider, too.”

Goss conducted a survey and found that 17% of landlords in the San Francisco area have had tenants break leases or give 30 day “move out” notices.

Another example is Alexa Lewis, a 24 year old that was living in San Francisco when the city locked down. By the end of April, her roommates had left and she was all alone. She was stuck with a $4,900/month rent bill and no clue what to do. “There were a lot of calls with my family to talk out everything and ask for advice/cry,” she said. She was able to negotiate temporary concessions with her landlord.

And the rental market is expected to stay soft even as the economy recovers. “People won’t need to be in a job center if they can work from home. I would expect to see less demand and that corresponds to lower rents,” Goss said. Rents are even expected to decline in places like New York City.

A new StreetEasy report stated: “Residents moving out of the city, even temporarily, could drive rents across the city down.” The report referenced a 10% decline in rents during the 2008 crisis.

Jonathan Miller, president of appraiser Miller Samuel Inc. said the difficulty of breaking leases could slow the pain in starter apartments. He also said that he expects rental activity in the suburbs to tick higher.

Atlasa’s Kahramaner said about the San Francisco market: “People are leaving San Francisco to try to buy a house in Marin or East Bay. People have a renewed interest in the suburban life.”

Daniel Chandross, a 23 year old that works for Google, is paying rent on an empty apartment after moving back with his family in the Midwest. Their lease is ending soon and it doesn’t look like they will renew. “We’re throwing around the option of moving our stuff into a storage facility. No reason to waste money on rent if we can live/work at home,” he concluded.

via ZeroHedge News https://ift.tt/2yvxxNZ Tyler Durden

Donald Trump has finally won a war. It’s a war he’s uniquely suited to fight, a propaganda war, and he’s successfully waged it on China through his command of Western media.

Stating this doesn’t imply any kind of judgment on my part as to whether he should or should not have waged this war with China. He has and he has emerged victorious, thanks to his reframing the threat from COVID-19 as an evil Chinese plot to kill millions of people.

Now, I’m convinced that the circumstances surrounding COVID-19 were a plot by evil people to kill millions of people and usher in a bleak, authoritarian nightmare they’ve had legislation and action plans written to execute for years. I’m just not convinced it was China that was wholly behind it.

In fact, my fundamental problem with Trump’s China propaganda war vis-à-vis COVID-19 is that it lets the real culprits for how it unfolded around the world off the hook. But, ultimately, that’s a different discussion.

Today’s discussion is about where things stand between the U.S. and China and what’s on tap for the future. Why do I think Trump has won his war against China?

Simple, the numbers.

A recent poll by Bloomberg found that 78% of Americans are willing to spend more for products made in “Not China” than in “China.” Moreover, that poll goes onto say that 40% of Americans now say they won’t buy anything at all from China.

I can tell you that more people I talk with personally here in the U.S. are at this point. I’m not one of them. While, personally, I’d prefer my food, clothing and basic necessities be made as close to home as possible it has nothing to do with antipathy with China or Chinese people.

To me that’s just wise, defensive living. In times of crisis, basic necessities should have supply chains as short as possible. Honestly, I would say the same thing about stuff made in California or Idaho. But economic reality is that Idaho is better at growing potatoes and California almonds than Florida is and therefore those supply chains aren’t likely to change much.

That doesn’t mean, however, my wife isn’t growing potatoes this year or that I’ll miss them if my local Winn-Dixie is out of them because the truck was late or the harvest poor.

It’s called comparative advantage and it is the basis for all productive economic interactions. And in some areas of the economic sphere China is superior to the U.S. currently, and until the dynamic changes people will complain about “Made in China” but they will still buy what they need, especially in a country with 40+ million people out of work being acutely price-sensitive.

But that said the poll numbers found by Bloomberg will rise over the next couple of years because things will get that desperate here in the U.S. and people want to work and be willing to work for less.

That can only happen, however, if the barriers to local commerce are lifted. And that lies at the feet of government at all levels, which are, by definition, funded by the private sector. Like it or not, folks, government has no money of its own. Everything it has it has after taking it through taxes.

Trump is clearly pursuing policies to decouple the U.S. and China’s economy to as great an extent as possible to help the U.S. economy regain its domestic productive capacity. And he’s been very systematic about it. This propaganda war and his attacks on China over their handling of COVID-19 are just the next stage of this.

He began the process with his tax cut plan which cut corporate taxes as well as small business and self-employment taxes, reversing decades of ruinous policy designed to destroy the American middle class and offshore U.S. productive capacity. He’s quietly been slashing federal department budgets and staff and lifting mandates on states.

That process is slow, very slow, during normal operations.

But that wasn’t nearly enough and now he’s faced with the next task, which is to cut taxes again and incentivize the onshoring of manufacturing. His Chief Economic Adviser Larry Kudlow floated that idea last week. Republicans in Congress didn’t like it. And one has to wonder why?

It’s not like the current budget looks anything like what tax receipts are going to total this year or next. The deficit will be above World War II levels. More likely they would rather dole out checks of funny money than not collect the money in the first place. That way the power continues to flow through D.C. rather than go back to the people themselves.

Never let a crisis go to waste right? Well, the Democrats are pushing for a China-esque total surveillance state and Green New Deal all rolled into one $3 trillion monstrosity, which, if passed, would only make the U.S. even more uncompetitive and hasten its demise.

Trump is finally doing the same thing, by going in the complete opposite direction.

The key to reversing China’s comparative advantages over the U.S. is removing the barriers to commerce which make local production unattractive. It’s that simple. And with oil prices now very low and low for a long time to come, Trump is now fighting lower shipping costs from overseas.

The U.S. maintains an extravagant government at not only the federal level but state and local as well. The American people can follow Trump blaming China all they want, but China is the symptom, government is the disease.

To solve this problem they have to look at themselves and admit this addiction to government itself is the barrier to them getting back to productive, happy lives.

I generally lay that blame for this extravagance at the feet of the cozy relationship between the Federal Reserve and the Treasury department creating money like crazy and allowing Congress and Presidents for two generations now to bribe voters with handouts from our future.

That future is now here.

And as individuals we have to face that.

I’ve said for a long time that anywhere from 20-40% of U.S. GDP is a phantasm born of fake money. It is waste and sloth within a system designed to hollow out the middle class and roll wealth up to an international oligarch class. Remove it and you get a better sense of what GDP and the cost basis for production truly is.

The same thing goes for China, by the way. Strip out the financialization and how much real economy is left?

That oligarch class just pulled the plug on that portion of the U.S. economy and I have no doubt that China had a hand in helping that along. It would be in their strategic interest to do so.

Thanks to Trump’s ham-fisted propaganda the American people now get this in the broadest terms.

And he’s willing to do both great and terrible things to change the dynamic. This much he has shown in spades. This war with China he’s waging has only just begun. He has the American people on his side, now he just has to convince the chattering class in D.C. that the old way of doing things is over.

via ZeroHedge News https://ift.tt/2Tye1aK Tyler Durden

Summer Vacation Spending Is Expected To Plunge 66% This Year Tyler Durden

Sun, 05/24/2020 – 20:25

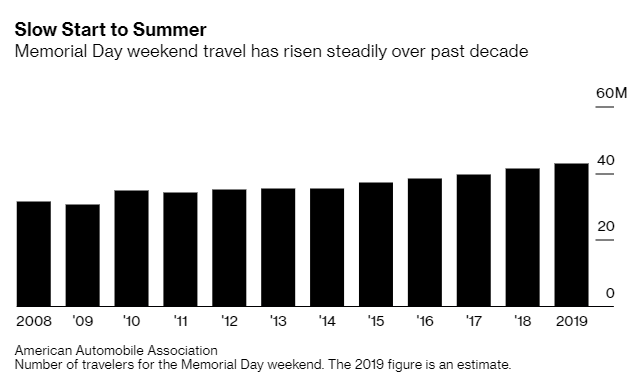

Memorial Day weekend not only kicks off the start of summer but also, for many Americans, kicks off travel and vacation season. But this year will obviously be different, with millions stuck sheltering in place at home, due to the global coronavirus pandemic.

As a result, travel spending for the weekend is expected to fall 66% to $4.2 billion, according to Bloomberg.

Even though some areas are starting to see small upticks in traffic, tourism officials say that most travel won’t come until later in the season. Domestic air travel is expected to still be sparse and “almost everyone” who travels will be expected to drive.

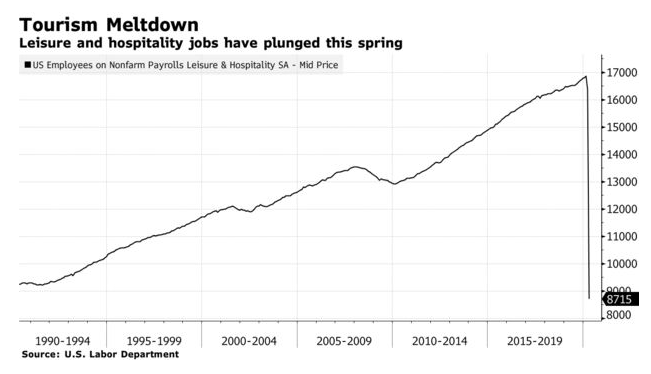

Additionally, seasonal hiring is also expected to plunge more than 75% from a year ago. The younger European workers that staff many U.S. resorts for the summer are expected to stay home. Visa processing for U.S. work and travel visas has “basically shut down everywhere” except for farmwork.

Since the beginning of the pandemic, almost half of all leisure and hospitality employees have lost their jobs.

Areas that are accessible by car are expected to be popular destinations this summer. That includes places like the Florida panhandle, the Carolina coasts, Oregon and Washington. Even parts of Wisconsin and Michigan are expected to be destinations for American road trips.

Camping is another alternative that vacationers may try this year. Judson Gee’s, who has a vacation rental home in Wrightsville Beach, North Carolina, said: “People are absolutely dying to get out of their house and more comfortable to be outdoors than in crowded spots.”

Just 32% of hotel rooms were occupied as of the week ending May 16. This is despite hotel bookings improving in recent weeks. As of May 14, more than 3,000 hotels remained closed.

Federal Reserve Chairman Jerome Powell told Congress earlier this week: “It will take some time for the public to regain confidence and adapt to the new world and start traveling, taking vacations.”

Places like Broadway and Disneyworld, popular tourist destinations, remain closed. Fred Dixon, the president and chief executive of NYC & Company, which promotes tourism said: “When restrictions are lifted, there is a lot of pent-up demand. At the same time, people will be more cautious now, just generally about how they make decisions to travel.”

But places like Myrtle Beach, South Carolina are starting to get busier and restrictions have begun lifting, allowing hotels to take new reservations.

Heather Baker and her husband, from Wilkesboro, North Carolina, said: “The beaches were packed. Myrtle Beach is a great mini-vacation. It’s only a four-hour drive for us, which makes for a nice little getaway.”

While June bookings are down more than 25% from last year, the shortfall is expected to narrow as summer progresses. Vacation Myrtle Beach, which operates 14 hotels and condo properties in the area, has hired less than 100 seasonal employees this year compared to the 700 they hired last year.

Bloomberg economist Carl Riccadonna concluded: “Certain businesses with a relatively short ‘high season’ may not be able to reopen in time to salvage their business for the year. If your year is really 3-4 months in the summer, then a lost few months really means a lost year–and in many cases a failed business.”

via ZeroHedge News https://ift.tt/2TA6hoV Tyler Durden

“The Comments Are Highly Important”: China’s Xi Reportedly Indicated Desire To Avoid Strong Stimulus Tyler Durden

Sun, 05/24/2020 – 20:15

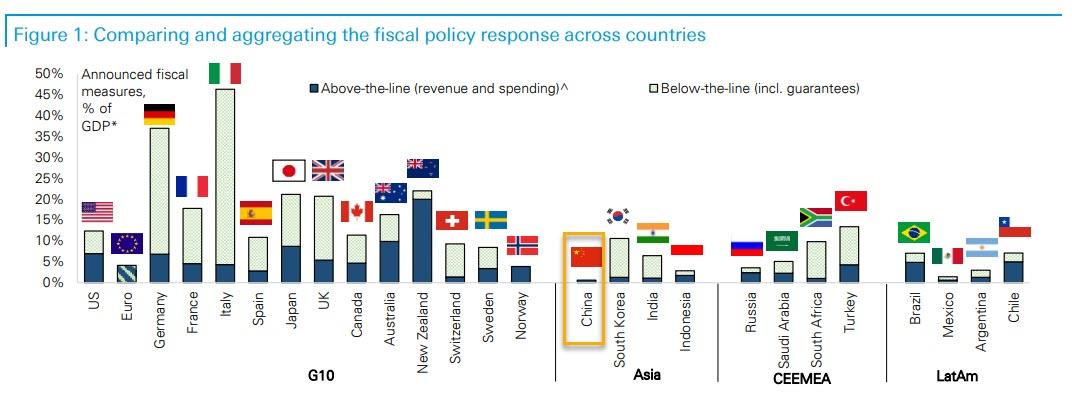

One of the more remarkable aspects of the global policy response to the coronavirus crisis has come out not out o the G10, where virtually every nation has unleashed an unprecedented stimulus, both fiscal and monetary, but rather out of China – the country which following the global financial crisis launched an unprecedented debt-fueled reflation and stimulus, yet which this time has done very little if anything at all, as the following chart comparing the fiscal response across countries demonstrates.

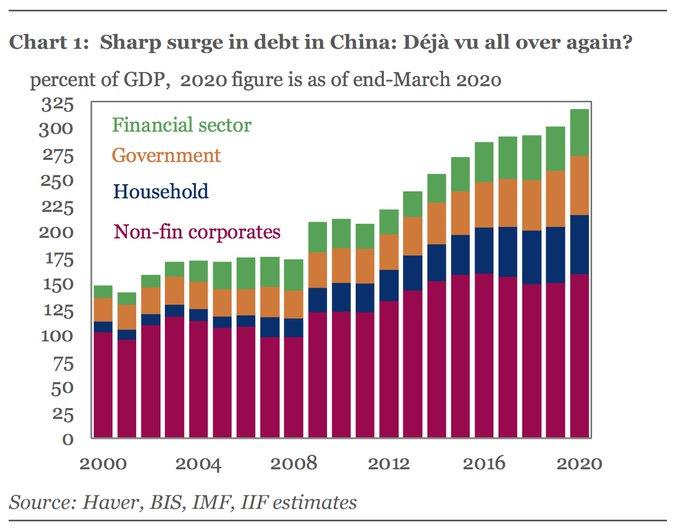

This should hardly come as a shock: after all, according to the IIF, China’s total debt/GDP as of March 31, 2020 is now a record 317%, the highest in history, and up 17% in just the past quarter and nearly double what it was in 2008, suggesting the country is basically out of room to layer on even more debt leaving far less space for a major new fiscal stimulus push.

Overnight, Goldman confirmed as much, writing that President Xi participated at group discussions at the Two Sessions on Friday, with some of his comments reported on Saturday. Notably he said if it were not because of the pandemic, the growth target would be set at around 6%. He added that a global recession is guaranteed, and given this, if a numerical target (implicitly at a relatively high level) was set, it would require a strong stimulus and the focus of the government would be on the growth rate. He said the focus should instead be on the “six stabilities” and “six guarantees” in six areas — the pursuit of these goals will indirectly contribute to GDP growth but the latter should not be the focus of the government, according to the report.

“The comments are highly important”, according to Goldman because they both explain some past policy decisions and will have significant future policy implications. While this is the first report publicly quoting President Xi on the issue of the GDP growth target, it is probably not the first time he has made this kind of comment, Goldman’s Yu Song goes on to note. If he indeed made similar comments non-publicly, possibly to small groups of senior officials, it would have affected the behavior of government officials and could explain the relative lack of aggressive stimulus measures relative to China’s past stimulus and relative to that of many other economies (as shown in the top chart). One example might be the relatively small MLF and LPR adjustments compared to market expectations. Such decisions had been subject to extensive discussions and debates and had to be signed off by President Xi because they were presented to the National People’s Congress.

President Xi’s comments will likely have implications for the behavior of officials. The doves at both central and local levels who have been advocating a growth target for fear of disappointing market expectations may well find it harder to argue their cases. While it is true that the “six stabilities” and “six guarantees” goals will contribute to GDP growth, they are much less specific. Some methods of achieving those goals may not contribute much to overall economic growth as measured by GDP. For example, to ensure employment stability, companies may find themselves under more pressures not to lay off workers. This often leads to cuts in pay for a broader group of employees. While having the burden more widely shared is arguably socially more desirable, its contribution to economic growth is likely to be limited and also often not sustainable.

Non-governmental economic agents such as companies and individuals may become more cautious with their plans as well.

Lastly there probably will be less pressure on data reporting (read fudging economic numbers for which China is notorious). While on the surface this is a good thing, as it tends to reduce distortions, it also boosts the likelihood of a lower level of reported GDP growth.

Earlier on Friday NDRC Director He Lifeng stated the performance of high frequency indicators since the beginning of May has been encouraging. If GDP growth in 2020 is 3%, then the level of income will be 1.95 times that in 2010. (The longer-term policy goal of doubling income over the decade is not precisely defined, but implicitly Goldman thinks a 1.95 level should be good enough to be rounded up to 2.)

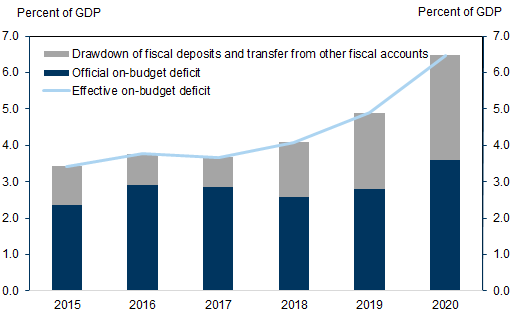

Separately, Minister of Finance Liu Kun revealed the government will transfer around 1 trillion RMB from the SOE fund to central government fiscal spending. If so, this means the actual fiscal loosening is meaningfully larger than the apparent fiscal deficit target of 3.6%. In fact, according to Goldman calculations, the effective deficit which is a more relevant indicator to measure the on-budget fiscal stance by taking financing through drawdown of fiscal deposits and transfers from other fiscal accounts into account, will increase even more, by 1.6pp to around 6.5% this year, according to the budget report released on the MOF website over the weekend.

That said, as Goldman also notes, the 1tr RMB of central government special bond quota (primarily 10-year tenor) is significantly lower than the bank’s pre-NPC expectation of Rmb 2tr. And here an interesting observation from the bank:“Recently there have been debates on whether PBOC should monetize the issuance (i.e., PBOC buys directly), and as suggested by the budget report, the issuance of these bonds would be market based. This will put pressure on interbank market liquidity, so PBOC needs to provide liquidity support (e.g., through RRR cut; 50bp of RRR cut could release liquidity of around Rmb 800bn).” In short: even with a rather limited fiscal stimulus, is the PBOC setting the stage for its own QE?

In any case, going back to Goldman, the bank estimates that the augmented fiscal deficit would increase by around 5.5% this year, slightly higher than the bank’s previous forecast of 5.3%, pointing to a slightly stronger fiscal stimulus, but still notably smaller than that in GFC.

In other words, whereas it was China that managed to pull the world out of the depression triggered by the global financial crisis with an unprecedented surge in debt creation (something we discussed back in 2013), this time around – whether due to political reasons, or purely based on balance sheet limitations – it will be up to every developed and emerging nation to restore its historical growth rate. While that explains the speed, and lack of discussions, with which helicopter money was adopted by the entire world, it begs the question: can the global economy rebound without China’s help this time?

via ZeroHedge News https://ift.tt/2WXE5Oz Tyler Durden

Global Anger Builds As Elites Worldwide Break Quarantine Rules Tyler Durden

Sun, 05/24/2020 – 20:00

“One rule for me, and another for thee” appears to be the politically-prone mantra rapidly spreading around the world.

Opposition parties take shots at one another with America‘s left decrying President Trump’s maskless-golfing escapades…

…and the right exposing Virginia Governor Northam’s recent non-socially-distanced, maskless-beach visit.

Japanese authorities are also under pressure with Japanese Prime Minister Shinzo Abe’s cabinet approval rating fell 4 ppts to 29%, lowest since the start of his second administration in Dec. 2012, after a wave of condemnation involving a man that his administration took great pains to defend: Hiromu Kurokawa, head of the Tokyo High Public Prosecutor’s Office. On Thursday, Kurokawa stepped down after a tabloid expose said he had gambled on mahjong with journalists twice this month despite the state of emergency requesting that nonessential outings be avoided.

Defying a growing clamor from public and politicians, AP reports that Johnson said Dominic Cummings had acted “responsibly, legally and with integrity” when he drove 250 miles from London to Durham, in northeast England, with his wife and son at the end of March.

Cummings said he traveled to be near extended family because his wife was showing COVID-19 symptoms, he correctly thought he was also infected and he wanted to ensure that his 4-year-old son was looked after.

However, as AP notes, critics of the government expressed outrage that Cummings had broken strict rules

Labour leader Keir Starmer said Johnson’s defense of Cummings was “an insult to sacrifices made by the British people.”

“The prime minister’s actions have undermined confidence in his own public health message at this crucial time,” he said .

Former Labour lawmaker Helen Goodman, whose father died in a nursing home during the outbreak, said Cummings’s behavior was “repellent.”

Whether you’re repelled or not, most ironically, Cummings “is the inventor of these three-word slogans: ‘Stay at Home,’ ‘Protect the NHS’ and ‘Save Lives.'”

As a reminder, elsewhere in Britain, so-called epidemiologist Neil Ferguson stepped down as government scientific adviser earlier this month after a newspaper disclosed that his girlfriend had crossed London to stay with him during the lockdown. In April, Catherine Calderwood resigned as Scotland’s chief medical officer after twice traveling from Edinburgh to her second home.

Still, it seems the elites’ ongoing belief in ordering the “better safe than sorry” lockdown of entire nations is facing a breaking point among the stuck-at-home, increasingly welfare-dependent average joe around the world.

via ZeroHedge News https://ift.tt/3gnwWiy Tyler Durden

{kind=link}