There is a growing trend where people are feeling compelled to deny their opinions and remain silent. This is because we are seeing a blatant disregard for the opinions of others by both those on the left and the right. Democracy as a form of government is far from perfect. Its greatest weakness is rooted in the ability of a vocal minority to force their opinions on others.

Governments Are Adding To The Fear

This growing fear of speaking out is not limited to America, we are seeing it in countries that claim to be free across the world. The tech giants, governments, and extremist groups are all throwing fuel on the fire and adding to the feeling retaliation is a fair response to speaking our mind. The tech giants’ effort to closely watch, silence, and censor those not marching in line with their desired narrative is a dagger in the heart of free speech. This effort is also apparent when we hear about groups threatening to block highways, shut down ports, and occupy state capitols if things fail to go their way. It even extends to harassing elected officials, we are hearing more threats from groups vowing to hound and badger members of Congress at their own homes. Another sign of intolerance is seen in the mass arrest of nonviolent protesters by governments.

Vandalism Like This Is A Sign Of The Times

Consider what we are witnessing as a sign of the times. Above is a picture showing a sign that vandals wrote curse words on, they also egged the house where it was displayed. This started several years ago and ramped up when the term “politically correct” moved front and center. In the minds of some individuals if you say anything that they consider “incorrect” it justifies a harsh response.

In such an environment it is little wonder that many people have become less vocal and afraid to speak their mind. This could help explain why so many people doubt the recent political polls showing Joe Biden leading President Trump by a large margin. Ironically, it is the Democrats that continue to demand the President disavow violence and those associated with it. The cornerstones of democracy are freedom of assembly and speech, inclusiveness and equality, membership, consent, voting, right to life, and minority rights. When these are trampled upon for any reason, the system is in danger of being cast aside.

Boy In Picture Assaulted Over MAGA Hat

In one of the most disgusting acts occurring in an election year, some Joe Biden supporters shoved and stole the hat of a young boy. The reason they assaulted Riley was that he was wearing a MAGA hat. His mother, Abbey Wigton, 27. Said “We were standing outside peacefully minding our own business,” she continued.

“Suddenly, two Joe Biden supporters began to yell political epithets at my child. They ripped the sign from my arms and assaulted my seven-year-old son.

“The Joe Biden supporters laid hands on my child and ripped his “Make America Great Again” hat from his head while cursing at him and pushing him over.”

She went on to say, “The two Joe Biden supporters verbally and physically assaulted my child. My 7-year-old child was sobbing and screaming.” Riley, was distraught following the incident because learning how absolutely hideous people can be at an early age can be difficult to handle. The boy wanted to call the police. He wanted his hat back. He wanted the evil people who attacked him to apologize. While the police can do little and the chance of getting an apology very slim, at least one of his wishes is coming true as he has a replacement hat on the way. He found this out when the White House called to tell him.

But this article is not about a small boy being assaulted, it is about how most people are now thinking twice before saying what they think. This article is about the ability of a vocal minority to make people so uncomfortable they become silent. It is about how we should be appalled by those that justify violence, aggression, and force towards those that simply disagree with them. It is about how the threat you may be demonized if you say what you feel tends to breed silence. Watching this unfold is leaving a sickening feeling in those valuing free speech.

A recent survey of 2,000 Americans by Cato Institute/YouGov found most Americans say “the political climate these days prevents them from saying things they believe because others might find them offensive”. The survey indicated 52% of Democrats, 59% of independents, and 77% of Republicans now say they have political opinions they are afraid to share. Most people do not enjoy confrontations or being harassed and as a result, are self-censoring themselves. With the free exchange of opinions and ideas being the foundation of a free and healthy democracy the signpublic discourse is being destroyed does not bode well for our continued freedom.

Joe Biden and Donald Trump at the September 30 presidential debate.

If you’re a libertarian like me, elections in the US two-party system often come down to choosing the lesser of two evils. This one is no exception. Both major-party candidates have serious flaws. But Democratic candidate Joe Biden is far preferable to Donald Trump. And that’s true based entirely on ideology and policy—without having to consider Trump’s corruption, his tweets, or his awful personality. Judged from the standpoint of promoting liberty, justice, property rights, and human welfare, the choice is clear. Trump has the edge on a few issues, but they are greatly outweighed by the ones where he doesn’t.

But those who do choose to vote have an obligation should try to make at least a reasonably informed choice. And, at least in most cases, they should vote for the least-bad alternative among those with a realistic chance to win. I defend the morality and rationality of lesser-evil voting in some detail here.

To briefly summarize, Biden has significant advantages over Trump when it comes to immigration, trade, property rights, government spending, and maintaining relationships with liberal democratic allies. These readily outweigh Trump’s edges on judicial appointments and certain types of taxation and regulation. Though I won’t cover it here, Trump’s undermining of liberal democratic norms is also a menace, even if it hasn’t yet led to many concrete policy actions. I explained why in a 2018 post.

This piece admittedly comes late in the election process; I admit I would have done better to write it sooner. But many millions of people still haven’t voted. And I suspect that may include a disproportionate percentage of undecided voters. For those who have already voted, I hope this work might still have value in terms of understanding where the two major parties stand from a libertarian perspective.

The costs to human liberty here are enormous. Trump’s expanded immigration restrictions forcibly consign hundreds of thousands of people to lives of poverty and oppression, simply because they made the mistake of being born to the wrong parents or in the wrong place. They also impose huge economic costs on both immigrants and natives. Immigrants make major contributions to American economic growth and innovation. The scale of economic harm caused by the administration’s immigration restrictions greatly outweighed any possible benefit from its deregulatory actions elsewhere—even before the former was ratcheted up during the pandemic.

Nor can these moves be rationalized by analogizing the US government to the owner of a private house who has a right to keep people out for whatever reason he wants. Such analogies are deeply flawed, and—if taken seriously—would justify draconian restrictions on natives’ liberty, no less than that of immigrants. No libertarian—or any kind of liberal—should accept the dangerous idea that the state is entitled to such sweeping power.

Biden is far from perfect on immigration issues. But he plans to reverse pretty much all of Trump’s new immigration restrictions, plus promote further liberalization, such as increasing the refugee cap to 125,000. The latter move alone will save over 100,000 people per year from poverty, oppression, and sometimes death. Freeing over 100,000 per year from a lifetime of oppression is enough to outweigh a multitude of sins elsewhere.

Moreover, virtually all of Trump’s immigration actions are the product of unilateral executive action. Therefore, Biden could reverse them without getting any new legislation through Congress. And, obviously, the odds of immigration liberalization getting through Congress are clearly higher if Biden wins than if Trump is reelected. In the latter case, there would be virtually chance at all.

What is true of immigration is also true of trade. On this quintessential libertarian issue, Trump is the worst president of modern times. In addition to his trade war with China, Trump has also picked trade wars with numerous US allies, including Canada, Mexico, the European Union, and South Korea, among others. The costs include some $57 billion in annual added expenses for American consumers, and massively reduced the value of American businesses, to the tune of hundreds of billions. And, once again, these costs greatly outweigh any plausible estimate of benefits from Trumpian deregulation elsewhere, which even the administration itself estimates at only about $50 billion for Trump’s entire term (thus, about $12.5 billion per year).

Like his immigration restrictions, Trump’s trade wars are almost entirely the result of executive action. Thus, Biden could very easily undo them—though joining TPP would require congressional ratification.

It was in some ways predictable that the Republicans might become an anti-immigration party, and perhaps even that they would turn against free trade. But, a decade ago, I would never have expected them to become worse than the Democrats on property rights. Yet, under Trump, that’s exactly what they have done.

Biden and the Democrats are far from ideal on property rights issues. But Biden would terminate the awful wall-building project. He is also likely to restore Obama-era constraints on asset forfeiture (though it would be preferable to go further than that). On zoning, liberal Democrats have pushed through valuable reforms in several states and localities, with more potentially on the way. Biden would provide some modest federal incentives to facilitate that. At the very least, unlike, Trump he wouldn’t actively oppose deregulation in this vital area.

In fairness, however, things could be even worse if Biden is able to push through all the additional new spending he advocates. However, he might have difficulty doing that. We know from much recent history that congressional Republicans only work to constrain federal spending when there is a Democrat in the White House, as they did under Clinton and Obama. If Biden wins the election, there is a high likelihood that the Democrats will have only a very narrow majority in the Senate, or even (less likely) that the GOP will retain control in that chamber. Working with moderate Democratic swing-voters, the GOP can constrain Biden’s spending plans, and will have every incentive to do so. Indeed, even the mere prospect of Trump’s leaving office has already led Senate Republicans to regain some of their fiscal religion, as they have rejected both Trump’s and the Democrats calls for a massive new $2 trillion “stimulus” package.

I don’t want to paint a rosy picture here. Regardless of who wins, there are likely to be major spending increases, and an exacerbation of our already severe fiscal crisis. But this will be incrementally better if at least one major party works to limit the damage, perhaps in cooperation with moderates from the other. That is more likely to occur with Biden in the White House than Trump.

Biden may not be able to fix all of this. But he would at lest end most of the trade wars, treat the allies with greater respect, and curb many of the Trumpian policies that most damage America’s image. That should matter for libertarians (and liberals of any stripe) because want liberal ideals to advance around the world, not just in one country. And it is important that brutal authoritarian regimes stop gaining influence at the expense of more liberal ones.

The harm Trump causes goes beyond the details of specific policy issues. Hostility to immigration, protectionism, gargantuan spending, damaging relationships with allies, and even undermining property rights, are all facets of the more general trend towards big-government nationalism in the GOP. If Trump wins reelection, we can expect that trend to solidify and continue. Should Trump’s approach succeed politically even in the midst of a dire economic and public health crisis, other Republican politicians (and perhaps even some Democrats) will continue to imitate him. We can expect more of the same from the GOP for years to come.

By contrast, if Trump is defeated and repudiated, there is a real chance the GOP will have to reconsider its approach, and retreat from some of his awful policies. At the very least, that’s more likely in the event of a Trump defeat than if he beats the odds and wins.

On the other hand, a defeat for Biden is unlikely to improve the Democratic Party. To the contrary, it would probably give a boost to the more extreme “democratic socialist” faction led by Bernie Sanders, and others, whom Biden defeated in the 2020 primaries. Defeat for Biden would lend credence to their notion that there is no political payoff for moderation, and that the only way to combat Trumpian right-wing populism is the left-wing version of the same.

Where Trump is Better – And Why it’s Not Enough

While I think a Biden victory is preferable, overall, there are undoubtedly some areas where Trump is better. The two most significant are economic regulation in areas unrelated to immigration and trade, and judicial appointments.

While, for reasons noted above, his achievements in this area have been overstated, there is no doubt Trump has achieved some useful deregulation in some fields. The best—and severely underappreciated—example is Trump’s executive order permitting a wider range of expense compensation for kidney donors, which could save thousands of lives.

By contrast, Biden, if he wins, has a long list of new regulations he would like to enact. Among the worst are a $15 minimum wage (which would destroy thousands of jobs), and a nationwide version of California bill AB 5, which severely restricts “gig economy” employment by forcing Uber, Lyft, and other similar businesses to classify their workers as “employees” rather than independent contractors. Sadly, Trump has said he might support a $15 minimum wage, as well, though he is probably less likely to be serious about it than Biden.

As already noted, Trump’s deregulatory accomplishments pale in comparison to the harm he has done in other areas, such as immigration and trade. Even if Biden undoes all of the former, and adds significant further regulatory burdens, it will still be outweighed by his plans to undue Trump’s immigration and trade policies. Moreover, the more extreme Biden regulatory policies—including the minimum wage increase and a nationwide AB 5—would require legislation to enact. And it is unlikely that swing-vote Democratic senators like Manchin (West Virginia), Kirsten Sinema (Arizona) and Hickenlooper (Democratic candidate in Colorado) would support them, given the vast damage they would do to their respective states (which are heavily dependent on sharing industries and—especially in West Virginia’s case—low-cost labor). By contrast, Biden could probably undo Trump’s horrible immigration and trade policies through executive action alone.

What is true on regulation is also true on taxation. The 2017 tax bill passed by the GOP Congress with Trump’s backing includes some useful provisions, such as limiting corporate taxes, restricting the mortgage interest deduction, and constraining deductions for state and local taxes. Biden’s tax proposals would only partially reverse these measures, but would move us in the wrong direction, nonetheless. However, this too would have to get through Congress, which might moderate it. And the net negative effect is still much smaller than that of Trump’s immigration and trade policies.

As for the more general tax cuts in the 2017 plan (which Biden would repeal for those earning over $400,000 per year), they are—sadly—likely to be negated by irresponsible deficit spending. So long as that continues, if we don’t pay more now, that just means we (and our children) will pay more later (along with accumulated interest). Overpending will probably be a serious problem regardless of who wins. But for reasons already noted, it is likely to be even worse if Trump gets reelected.

Finally, there is the issue of judicial appointments. Here, I have to acknowledge Trump has made substantially better appointments than I expected back in 2016. Some have proven outstanding, like Gorsuch on the Supreme Court, and Judge Don Willett on the Fifth Circuit. Most of the others are, at least, no worse than we could expect from a conventional GOP administration. Essentially, Trump has accomplished this by delegating judicial selection to more conventional conservatives, as opposed to seeking judges who reflect his own distinctive nationalist agenda (as I thought he might do, back in 2016).

Conventional GOP judges are by no means flawless, from a libertarian point of view. But with the extremely important exception of immigration-related constitutional cases, they do tend to better than Democratic-appointed judges in terms of both judicial philosophy, and positions on specific issues (e.g.—property rights, federalism, gun rights, campaign finance restrictions, and some others).

If Trump continues in the same vein in a second term, his appointees would likely be better than those Biden is likely to choose. That said, there are several important caveats, that diminish this advantage.

Second, while Trump has been content to appoint conventional conservatives to the judiciary so far, that can change over time. Already, his most recent Supreme Court list includes several dangerous big-government nationalists deeply hostile to civil liberties, such as Senators Josh Hawley and Tom Cotton. Recent appointee Amy Coney Barrett is not of the same ilk. But her appointment clearly offers more hope to social conservatives and perhaps nationalists than libertarians.

More generally, over time judicial appointments come to reflect a party’s overall ideological priorities. The more big-government nationalism, with an admixture of social conservatism, comes to dominate the GOP, the more that will eventually be reflected in judicial appointments. Even if it doesn’t happen under Trump, it is likely to come to fruition under the next nationalist GOP president, who could easily be either Hawley or Cotton! As discussed above, this dangerous development is more likely to be avoided if Trump is defeated and repudiated.

Even a small chance of court-packing should be taken seriously. But it’s not enough to outweigh all the evil done by Trump. Not even the best possible Supreme Court justices can do enough good to outweigh the hundreds of thousands of lives blighted by Trump’s immigration and trade policies.

I will not try to deal with Biden and Trump’s respective approaches to the Covid crisis. Suffice to say that I am not as confident as many Biden supporters that his policies will work better than Trump’s. At the same time, they can hardly be worse than that of a president who often tries to deny the problem even exists. Ultimately, the best way to end the crisis is to accelerate the development and deployment of a vaccine. I see no reason to think Biden will be worse on that front than Trump, and some reason to hope he might be better. For example, a less nationalistic and xenophobic administration might be more willing to cooperate with allies on vaccine development and distribution.

We end where we began. The election presents with a choice of evils. But Biden is by far the lesser evil of the two. In some key areas, he could even be a positive good. And, as promised, I have defended that conclusion entirely without reference to Trump’s personal behavior, his corruption, or his Tweets. Getting that out of the White House would just yet more icing on cake!

from Latest – Reason.com https://ift.tt/3kKQTBo

via IFTTT

Democratic Gov. Gavin Newsom’s ability to dictate the conditions of reopening California’s economy is being challenged in a new lawsuit by small business owners who claim that the governor’s pandemic restrictions have endangered their livelihoods—as well as representative government in the state.

“We’ve been shut down since mid-March and that’s been completely devastating,” says Daryn Coleman, owner of Ghost Golf, who is currently suing Newsom. “I have bills racking up. I have balances building on everything.”

Coleman’s business, a ghost-themed miniature golf and family entertainment center in Fresno, California, was forced to close, alongside all other nonessential businesses in mid-March, when Newsom first issued his emergency declaration.

Since then, he’s been at the mercy of reopening conditions set by the governor and the California Department of Public Health (CDPH), which has kept Ghost Golf closed but for a few days in early June.

The state’s latest reopening criteria don’t give Coleman much hope of being able to open his doors again soon, let alone turn a profit.

The state’s latest Blueprint for a Safer Economy places counties in one of four color-coded tiers based on their number of new cases (case rate), and percent of COVID-19 tests coming back positive (positivity rate). The higher a county’s case and positivity rates are, the fewer businesses and social activities are permitted.

Fresno County is in the second-most-restrictive purple tier. That means Coleman’s Ghost Golf, like all amusement parks in the county, is closed. Gyms, dance studios, and aquariums can open at limited capacity and under certain conditions.

Coleman will have to wait until his county is admitted into the next least-restrictive tier before being allowed to open. Even then, he’ll only be allowed to operate at 25 percent capacity. That could be too little, too late for Ghost Golf.

“I honestly don’t know if I will survive even if I am allowed to reopen,” says Coleman, pointing to those capacity restrictions and the fact that business closures have already cost him busy summer months and the Halloween rush. “We’re a haunted-themed place and I lost October, which is usually a really good month for us.”

On Thursday, Coleman and Nieves Rubio, a restaurant owner in Bakersfield, California, sued Newsom, California Attorney General Xavier Becerra, Acting State Public Health Officer Erica Pan, and CDPH Director Sandra Shewry. Their lawsuit argues Newsom’s business closures are a usurpation of law-making powers reserved for the state’s Legislature.

“The governor is essentially making law. He has no authority to do that,” says Luke Wake, an attorney with the Pacific Legal Foundation (PLF), which has filed the case on behalf of Coleman and Rubio. “We’re now seven months into what is really autocratic rule, one-man rule.”

Newsom’s orders have invoked the state’s Emergency Services Act, which enables the governor to declare a state of emergency, and gives him sweeping powers to craft regulations and direct state agencies’ actions when responding to an emergency.

While this law consolidates executive power in the hands of the governor, argues Wake, it doesn’t create new executive powers that haven’t already been approved by the state legislature.

“The Emergency Services Act allows the Governor to coordinate all aspects of the executive branch of the state and to exercise all powers already granted to any executive agency of the state,” reads the lawsuit. “It does not grant the Governor the authority to take actions not otherwise authorized by the California Constitution or by statute.”

The legislature, Wake notes, has passed several bills related to the COVID-19 pandemic while contenting themselves to let the governor and public health officials set the pace of the state’s reopening.

The lawsuit PLF has filed on behalf of Coleman and Rubio is asking the court to declare the governor and CDPH exceeded their authority by ordering business closures and to strike down the entirety of the state’s Blueprint for a Safer Economy as unlawful.

During coronavirus, the courts have generally have been loath to strike down lockdown orders and business closures in response to plaintiffs claiming their individual rights have been violated, citing a 1905 U.S. Supreme Court case which upheld a mandatory vaccination law as a constitutional exercise of state’s police powers.

Lawsuits alleging that state governors and public health authorities have unjustly assumed powers reserved for state legislatures have proven more successful. State supreme courts in Wisconsin and Michigan shot down their governors’ respective business closure orders for violating the separation of powers.

Every day, Coleman says he gets numerous emails and phone calls asking if his business is open yet. He hopes that this lawsuit will undo the restrictions keeping him from serving these customers, restrictions he considers arbitrary as well as financially ruinous.

“I can go work out at a gym. I can go get a massage if I want. I can go to a movie theater,” he says. “but playing laser tag or indoor miniature golf is too great a risk?”

from Latest – Reason.com https://ift.tt/3oJAIXq

via IFTTT

Libertarian Party (L.P.) state House candidate Bethany Baldes of Wyoming came just 53 votes away from winning a seat in 2018, in a race with fewer than 3,300 total votes cast. She was so close she’d been reported as the actual winner, over longtime Republican incumbent David Miller (then the House majority leader), before absentee ballots came in.

That’s one reason why Apollo Pazell, an L.P. political operative working the Wyoming races, says in a phone interview today that they began their ground operation in Wyoming this year well before absentee ballots were first cast.

Pazell sees the strong possibility of an actual victory for both Baldes and another state House candidate, Marshall Burt, based on surveying done by their door-knockers who are interacting with voters daily, including hitting all relevant houses at least four times. (Their door-knockers are masked and frequently tested, though Pazell says citizens often tell the canvassers to “take off the stupid mask.”)

Burt is facing one Democratic challenger, Stan Blake, in House District 39. Blake has held the office since 2007 and generally runs unopposed.

The L.P. has pursued a more active than usual set of tactics in Wyoming, following a long-term Pazell strategy of targeting elections with a small number of total voters needed to win and only one major-party rival. The state does present unique ground game problems, though: One of the districts the L.P. is vying to win with candidate Lela Konecny has roughly 3,000 voters spread out over a region “the size of Massachusetts,” he says.

“We have six canvassers on the ground traveling the state, and a half-dozen to dozen phone banking volunteers all years long,” notes Pazell.

Outside organizations, including Wyoming Gun Owners, have been helping promote Baldes as well, attacking her Republican opponent Ember Oakley for Oakley’s concern over immunity provisions for citizens under the state’s “stand your ground” law that dissatisfied the hardcore gun rights group.

Pazell today talked up his team’s efforts for four L.P. candidates running for the Wyoming House against only one other major-party opponent, which increases their chances of big results or even a win. The fourth is Shawn Johnson in District 38, running against Republican incumbent Tom Walters, who won his last election with only 1,017 total votes. Johnson is also the state L.P.’s chair.

Johnson said the national party has been taking an unprecedented step to provide resources to the party this year and potentially help establish a third-party presence here.

This year might present the perfect opportunity for that to happen. As Democrats work to capture as many moderates as possible from the state’s Republican supermajority, Libertarians seek to tap into the state’s already massive wellspring of conservative voters who are potentially fed up with the current disarray of the Wyoming GOP, which has been plagued by infighting and anemic fundraising efforts over the past year.

The Libertarian Party has also sought to avoid debates over hot-button social issues like abortion and same-sex marriage that have long been a lightning rod within the state GOP and exacerbated tensions among the party’s ranks.

Baldes has received some endorsements from local Republicans over her opponent. Baldes told the Star-Tribune that “The two parties that are in place right now have been pushing the idea of taxes down our throat to the point where constituents have this idea that there’s no way forward without raising taxes….Having Libertarians in office will allow us to keep Republicans honest. They no longer can hide behind a name and talk about non-conservative ideas.”

The L.P. candidates are pushing economic issues mostly, Pazell says. “Wyoming is in a very drastic economic situation,” he says, between COVID-19 and a collapse in the state’s mineral industry. Other politicians, he says, are quick to call on more corporate, sales, and income taxes as a solution, which the Libertarians are not. “We have a detailed plan involving improving [the state’s] investment portfolios and cutting costs in a responsible way.”

from Latest – Reason.com https://ift.tt/35Kod5k

via IFTTT

Biden Advisers Sound Red Alert Over Black, Latino Turnout Tyler Durden

Fri, 10/30/2020 – 17:20

Senior Biden campaign officials are ‘becoming increasingly worried’ over low turnout among black and latino voters in key states such as Pennsylvania and Florida, according to Bloomberg, citing people familiar with the matter.

Despite record early-vote turnout around the country, there are warning signs for Biden. In Arizona, two-thirds of Latino registered voters have not yet cast a ballot. In Florida, half of Latino and Black registered voters have not yet voted but more than half of White voters have cast ballots, according to data from Catalist, a Democratic data firm. In Pennsylvania, nearly 75% of registered Black voters have not yet voted, the data shows. –Bloomberg

“I would like to see turnout increase – and yes, we need improvement,” said Biden super PAC president, Steve Schale in a Tuesday blog post.

According to the report, top campaign leaders are confident that blacks and latinos will show up on election day, however some Biden advisers have expressed concerns about a lack of participation – and are urging the campaign to spend more money to target minority voters in the final stretch.

Perhaps minorities found out that Biden didn’t want to raise his children in a racial jungle when he opposed desegregation?

Or that he drafted the 1994 crime bill, which sent tens of thousands of black men to prison for minor crimes, something Biden has expressed pride over.

Or that Biden said blacks ‘aren’t black‘ if they don’t vote for him.

Biden told black people who didn’t support him that they were race traitors. Very uniting. Much healing. https://t.co/1kuzHpfIIC

Or that his ‘guide and mentor’ was an ‘Exalted Cyclops’ in the KKK (who renounced his racist ways when it became a political liability he saw the light.)

FLASHBACK: 10 years ago today Joe Biden delivered a eulogy for Senate segregationist and former KKK “Exalted Cyclops” leader Robert Byrd.

He called him a “mentor,” a “guide,” and a “friend.”

— Trump War Room – Text TRUMP to 88022 (@TrumpWarRoom) July 2, 2020

Or that he equates being poor to being black.

Or that rapper 20 cent endorsed Trump (until his ex-girlfriend Chelsea Handler yanked his leash), while Lil’ Wayne, Kanye and Ice Cube have thrown their support behind Trump, or at least a new ‘platinum plan’ intended to help the black community.

Biden campaign spokeswoman Symone Sanders (who mocked a white Trump supporterwho was beaten in Chicago, and is apparently OK with all of the above) – says Bloomberg’s sources are trippin’.

“No campaign in American history has devoted this level of resources that we have to outreach to voters of color, and we’re deeply proud of it,” said Sanders, adding “In community-specific advertising alone, we’ve dedicated tens of millions of dollars to each community, with a total into 9 figures. And we’ve committed tens of millions on in-person GOTV programs unique to communities of color. Earning the support of diverse voters is the beating heart of our operation. We’re also the most diverse general election campaign in American history, including at senior levels, and all of our strategic decisions are driven by our diverse leadership team.”

The anonymous advisers, however, fear the Biden campaign has become overconfident – especially after weak turnout among people of color for Hillary Clinton in 2016, and she had hot-sauce on her side.

via ZeroHedge News https://ift.tt/37ZTyng Tyler Durden

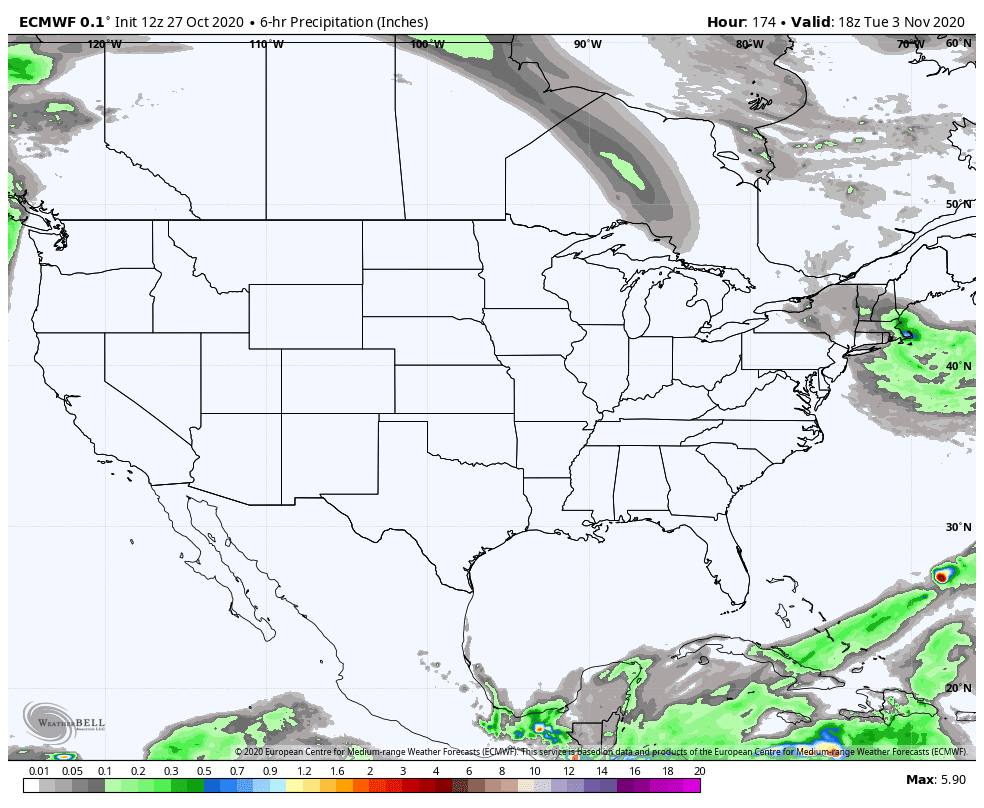

I got a call today from a political science professor from California: he wanted to know how to get reliable weather forecast information for next week because weather can favor one party over another.

I helped him, but this got me thinking about the weather on election day, particularly since we are now close enough in time to have some skill.

I was familiar with a number of studies that have been done on this subject, and their suggestion that bad weather favors Republicans (see an example below).

So what do the latest and best model forecasts predict for election day?

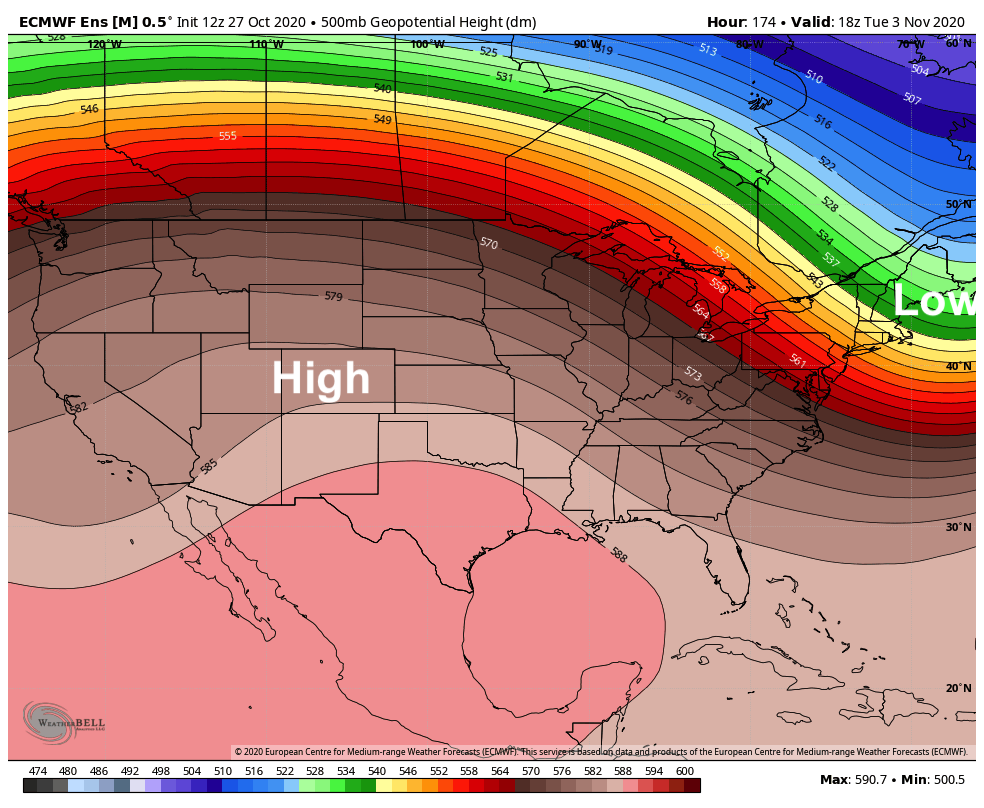

Since my blog readers deserve the best, I examined the world-leading guidance from the European Center model.

The forecast for election day over much of the U.S. is extreme….. extremely pleasant, with minimal storminess and precipitation.

To give you the best possible forecast let’s examine the European Center ensemble model predictions in which they run their model 51 times, each slightly differently, The average or mean of these ensemble forecasts is usually a good prediction.

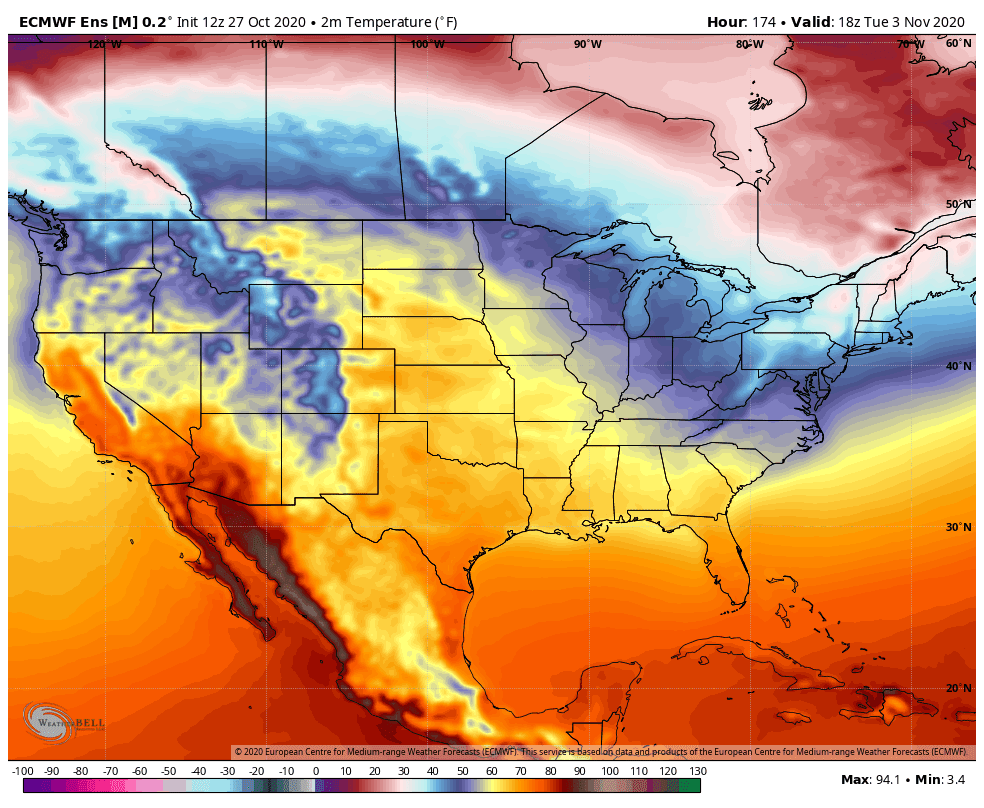

The ensemble-mean upper level (500 hPa, about 18,000 ft) weather map for 11 AM PDT shows a HUGE area of high heights/pressures dominating nearly the entire U.S., while a trough of low pressure/height is offshore. Such a pattern will bring warmer than normal and dry condition for the western two-thirds of the U.S.

To show his, there are the temperatures forecast for the same time. Toasty in California, the southwest, the central and southern Plains states, the Gulf Coast and Florida. The only locations that will be below freezing will be northern New England and New York.

Precipitation that day? Almost nothing except for a few sprinkles in New England. Even Seattle will be dry

Considering this forecast, the classical papers, such as the one noted above, would suggest an enhancement of Democratic voting.

But I suspect there are some surprises ahead. How will the COVID pandemic and huge numbers of mail-in ballots change the story? The percentage voting on election day will be much smaller than normal.

Trump supporters are probably different that the Republican voters of 20-30 years ago. And can one really trust telephone-based polling? Many people are solely using smartphones and conservative voters may well be fearful of expressing their honest views to someone that calls their home out of the blue.

One thing is for certain: the weather this weekend looks quite pleasant here in the Northwest–a perfect time enjoy the fall colors.

A pleasant way to forget the election for a few hours.

via ZeroHedge News https://ift.tt/34EKD8O Tyler Durden

Shops Boarded Up In San Francisco Ahead Of Anticipated Election Night Unrest Tyler Durden

Fri, 10/30/2020 – 16:40

The Nov. 03 presidential election is just a few days away – and for weeks – we’ve outlined security consultants, insurers, contractors, and even employees of retailers confirmed businesses are boarding up shops and increasing security measures ahead of Tuesday night.

Earlier this week, the looting and social unrest in Philadelphia following the fatal police shooting of a black man could be an eye-opener of what’s to come after the elections. Demonstrations started peacefully on Monday and Tuesday but quickly went downhill as mobs of people looted stores in the city.

The fact that law enforcement officials across the nation have been preparing for widespread violence on election night and after should be troubling to ordinary business owners with brick and mortar presence in metro areas.

For more color on the rising fears of social unrest next week, Harmeet Dhillon, a civil rights attorney and former California Republican Party vice chairwoman, tweeted that shops in San Francisco “are boarding up this week in anticipation of opportunistic rio-looting. Some thugs got started early at Coach earlier this week, which was boarded up today.”

Shops in San Francisco’s now-joyless shopping destination, Union Square, are boarding up this week in anticipation of opportunistic rio-looting. Some thugs got started early at Coach earlier this week, which was boarded up today. pic.twitter.com/LJteTo1t72

On Wednesday, the San Francisco Business Times posted a photo of the Salesforce Tower, which was also boarded up.

“Bracing for potential violence after next week’s election, several landlords near Salesforce Tower and Union Square freshly boarded up their storefronts this week,” the Times said.

Marc Intermaggio, executive vice president at BOMA San Francisco, who represents businesses in the metro area, said owners who have already boarded up their shops are just taking “precautionary” action ahead of the election.

“Just pre-election precaution against any civil unrest,” Intermaggio told the Times. “Protecting private property.”

Many businesses in the downtown and Union Square area were boarded up during the virus pandemic and George Floyd protests, but recently had plywood boards removed as reopening plans were beginning. However, much of that could be in reverse with virus cases surging and threats of unrest next week are elevated.

“Given the heightened attention and emotion around this year’s election, many businesses out of an abundance of caution are boarding up their entrances and windows in case of public unrest or protests across the political spectrum,” said Karin Flood, head of the Union Square BID. “Given events of this past spring and summer, it is not an unexpected precaution.”

via ZeroHedge News https://ift.tt/3jIj4zQ Tyler Durden

In the wake of the police killing of George Floyd in May, activists and criminal justice reform advocates suddenly had momentum and mainstream attention on previously niche issues like qualified immunity, no-knock warrants, and public access to police misconduct records.

State lawmakers responded to these nationwide demands for reform by introducing hundreds of bills. But how much of that momentum translated into concrete changes in American policing?

A database created by the lobbying firm MultiState and shared with Reason shows that, of the 283 policing reform bills introduced since May that the firm has tracked, 35 have passed.

The National Conference of State Legislatures (NCSL), a nonpartisan association of sitting state legislators, maintains a wider database of policing bills introduced since the death of George Floyd. Of the 653 bills tracked by the NCSL, 57 have passed.

“We’ve seen so much activity on policing reform at the state level since the end of May,” Chris Mattox, a senior policy analyst at MultiState, says, “even in a year when many states’ legislative sessions were interrupted or cut short by the COVID-19 pandemic. Given what we’ve seen so far, I expect to see a lot more legislation coming out of the statehouses when they reconvene next year.”

Those databases give a fairly comprehensive view of what happened in summer/early fall 2020, but not the whole picture.

This month, Virginia passed legislation banning no-knock raids, barring police from initiating searches during traffic stops if they allegedly smell marijuana, expanding civilian oversight of police departments, and making it easier to decertify officers found guilty of crimes or other misconduct.

California passed measures to ban chokeholds, require the state attorney general to investigate fatal police shootings of unarmed civilians, and increase oversight of county sheriffs. However, police unions managed to kill other proposals, such as one that would have given the state a way to decertify police officers. California currently has no power to permanently strip an officer’s badge, allowing problem cops to bounce from department to department.

The New York legislature repealed a law that made police misconduct records in the state totally secret, a stinging defeat for police unions that had successfully defended and expanded the law for four decades.

Similarly, Hawaii passed a bill in July that will make suspensions and firings of police officers public record. The new law also allows the state’s law enforcement standards board to revoke officer certifications.

The Minnesota legislature passed a compromise bill that bans chokeholds and warrior-style training for police officers and creates a new office to investigate police killings and allegations of sexual assault committed by police.

New Mexico will now require every police officer in the state to wear a body camera.

However, civil liberties and criminal justice advocates didn’t see many of their highest priorities pass, let alone make it into bills.

“Overwhelmingly, the legislation we saw introduced in the wake of George Floyd’s murder was honestly pretty weak,” says Paige Fernandez, policing policy adviser at the American Civil Liberties Union.

Fernandez says most of the bills that were introduced were “backstop bills” that focused on what happens after police violence has occurred, rather than stopping them from happening in the first place.

One of the more common provisions passed by state legislatures was restricting police from using chokeholds like the kind that killed George Floyd. Delaware, for instance, created a new crime, “aggravated strangulation,” that applies to police officers. Utah and Iowa also restricted the use of chokeholds. The latter was one of the few bills introduced by a Republican. The vast majority of bills were introduced by Democrats.

The Department of Justice also announced this week that restricting chokeholds would be one of the certification requirements for police departments under a White House executive order issued in June.

The MultiState and NCSL databases do not include internal policy changes at police departments: The Omaha Police Department and the Las Vegas Metropolitan Police Departmentannounced changes to their use-of-force policies to limit neck restraints. The Memphis Police Department announced it would no longer execute no-knock search warrants.

City councils were active as well. In San Francisco, police will no longer respond to calls involving non-criminal matters. Louisville, where Breonna Taylor was killed by police, banned the use of no-knock warrants. Atlanta Mayor Keisha Lance Bottoms issued executive orders in June requiring police to use de-escalation tactics before using force, and requiring officers to intervene if they see another officer using excessive force. In Wisconsin, the Madison City Council voted to create a civilian review board and an independent auditor to oversee its police department.

Cities and school boards also wrestled with proposals to eliminate or shrink the presence of police in schools, which civil liberties groups have long argued contribute to the so-called school-to-prison pipeline. Several major cities—Minneapolis, Portland, Denver, Seattle, Oakland—eliminated school resource officer programs, while Chicago slashed its school police budget by more than half.

But there was backlash as well. The Georgia legislature, for instance, passed a “peace officers bill of rights” that increased procedural protections for police officers. The legislation, opposed by civil liberties groups, seals records of unfounded complaints against officers and substantiated complaints that do not result in discipline. It also increases procedural protections for officers under investigation and creates a new crime for attacks against police or law enforcement property.

In September, Republican Florida Gov. Ron DeSantis announced legislation to increase penalties for crimes associated with protests and to block state funding to cities that cut police department budgets.

“The concern that I have, and I think a lot of advocates in policing reform work have,” Fernandez says, “is that in the 2021 legislative session, a lot of legislatures will try to absolve themselves of responsibility and say, ‘Look, we passed this package in emergency session in the summer of 2020 following the murder, George Floyd, we did our part.’ But they didn’t, and they have a long way to go.”

from Latest – Reason.com https://ift.tt/382hMxr

via IFTTT

In the wake of the police killing of George Floyd in May, activists and criminal justice reform advocates suddenly had momentum and mainstream attention on previously niche issues like qualified immunity, no-knock warrants, and public access to police misconduct records.

State lawmakers responded to these nationwide demands for reform by introducing hundreds of bills. But how much of that momentum translated into concrete changes in American policing?

A database created by the lobbying firm MultiState and shared with Reason shows that, of the 283 policing reform bills introduced since May that the firm has tracked, 35 have passed.

The National Conference of State Legislatures (NCSL), a nonpartisan association of sitting state legislators, maintains a wider database of policing bills introduced since the death of George Floyd. Of the 653 bills tracked by the NCSL, 57 have passed.

“We’ve seen so much activity on policing reform at the state level since the end of May,” Chris Mattox, a senior policy analyst at MultiState, says, “even in a year when many states’ legislative sessions were interrupted or cut short by the COVID-19 pandemic. Given what we’ve seen so far, I expect to see a lot more legislation coming out of the statehouses when they reconvene next year.”

Those databases give a fairly comprehensive view of what happened in summer/early fall 2020, but not the whole picture.

This month, Virginia passed legislation banning no-knock raids, barring police from initiating searches during traffic stops if they allegedly smell marijuana, expanding civilian oversight of police departments, and making it easier to decertify officers found guilty of crimes or other misconduct.

California passed measures to ban chokeholds, require the state attorney general to investigate fatal police shootings of unarmed civilians, and increase oversight of county sheriffs. However, police unions managed to kill other proposals, such as one that would have given the state a way to decertify police officers. California currently has no power to permanently strip an officer’s badge, allowing problem cops to bounce from department to department.

The New York legislature repealed a law that made police misconduct records in the state totally secret, a stinging defeat for police unions that had successfully defended and expanded the law for four decades.

Similarly, Hawaii passed a bill in July that will make suspensions and firings of police officers public record. The new law also allows the state’s law enforcement standards board to revoke officer certifications.

The Minnesota legislature passed a compromise bill that bans chokeholds and warrior-style training for police officers and creates a new office to investigate police killings and allegations of sexual assault committed by police.

New Mexico will now require every police officer in the state to wear a body camera.

However, civil liberties and criminal justice advocates didn’t see many of their highest priorities pass, let alone make it into bills.

“Overwhelmingly, the legislation we saw introduced in the wake of George Floyd’s murder was honestly pretty weak,” says Paige Fernandez, policing policy adviser at the American Civil Liberties Union.

Fernandez says most of the bills that were introduced were “backstop bills” that focused on what happens after police violence has occurred, rather than stopping them from happening in the first place.

One of the more common provisions passed by state legislatures was restricting police from using chokeholds like the kind that killed George Floyd. Delaware, for instance, created a new crime, “aggravated strangulation,” that applies to police officers. Utah and Iowa also restricted the use of chokeholds. The latter was one of the few bills introduced by a Republican. The vast majority of bills were introduced by Democrats.

The Department of Justice also announced this week that restricting chokeholds would be one of the certification requirements for police departments under a White House executive order issued in June.

The MultiState and NCSL databases do not include internal policy changes at police departments: The Omaha Police Department and the Las Vegas Metropolitan Police Departmentannounced changes to their use-of-force policies to limit neck restraints. The Memphis Police Department announced it would no longer execute no-knock search warrants.

City councils were active as well. In San Francisco, police will no longer respond to calls involving non-criminal matters. Louisville, where Breonna Taylor was killed by police, banned the use of no-knock warrants. Atlanta Mayor Keisha Lance Bottoms issued executive orders in June requiring police to use de-escalation tactics before using force, and requiring officers to intervene if they see another officer using excessive force. In Wisconsin, the Madison City Council voted to create a civilian review board and an independent auditor to oversee its police department.

Cities and school boards also wrestled with proposals to eliminate or shrink the presence of police in schools, which civil liberties groups have long argued contribute to the so-called school-to-prison pipeline. Several major cities—Minneapolis, Portland, Denver, Seattle, Oakland—eliminated school resource officer programs, while Chicago slashed its school police budget by more than half.

But there was backlash as well. The Georgia legislature, for instance, passed a “peace officers bill of rights” that increased procedural protections for police officers. The legislation, opposed by civil liberties groups, seals records of unfounded complaints against officers and substantiated complaints that do not result in discipline. It also increases procedural protections for officers under investigation and creates a new crime for attacks against police or law enforcement property.

In September, Republican Florida Gov. Ron DeSantis announced legislation to increase penalties for crimes associated with protests and to block state funding to cities that cut police department budgets.

“The concern that I have, and I think a lot of advocates in policing reform work have,” Fernandez says, “is that in the 2021 legislative session, a lot of legislatures will try to absolve themselves of responsibility and say, ‘Look, we passed this package in emergency session in the summer of 2020 following the murder, George Floyd, we did our part.’ But they didn’t, and they have a long way to go.”

from Latest – Reason.com https://ift.tt/382hMxr

via IFTTT

This “capitalism” is only attractive to parasites, predators, kleptocrats, legalized looters, embezzlers, fraudsters and all those insiders whose palms get greased along the way.

Back of the envelope definition of classical capitalism:

1. Transparency in markets, including pricing, information on quality and reliability of products, sellers and buyers, and of rules of conduct and rights governing all participants;

2. Risk is tightly bound to reward, i.e. everyone has skin in the game, those who lose are forced to absorb the entire loss.

3. Open competition, i.e. no monopolies or cartels limiting supply or setting prices;

4. Free flow of capital and labor;

5. Everyone pays the same rates of taxes, duties and fees on every transaction.

Needless to say, what is presented as “capitalism” in America today is not actually capitalism; it is monopoly-state-socialism for the wealthy, a kleptocracy incompetently cloaked by a rigged simulacrum market in which risk and losses are transferred to the debt-serfs and tax donkeys and the “socialism for the rich and powerful” is enforced by a pay-to-play simulacrum democracy and kleptocratic, totalitarian central bank, the Federal Reserve.

In this winner take most, anything goes if you’re rich casino, the weaker players are ruthlessly stripmined and exploited and those enterprises without political protection are cannibalized by rapacious, predatory monopolies and cartels.

Parasitic elites take a skim from every table: student loans over here, state junk fees over there; everyone gets clipped by self-serving insiders and entrenched interests.

Transparency is an illusion.Complexity thickets protect monopolies and cartels, and the fine print… try getting a set price for healthcare services. (You must be joking.) Sign the form for the $30 oil change and come back to an $800 bill for “work you authorized.” (You didn’t read the fine print? Too bad.)

Quality has gone downhill across the board but there’s no recourse or competition. All the items regardless of brand come from the same factory in China. So what if your new oven turns on by itself randomly (true story, happened to me); the once-proud American brand’s warranty is only one year, so tough luck, bucko, the repair bill for the defective $5 sensor will cost you as much as a new range.

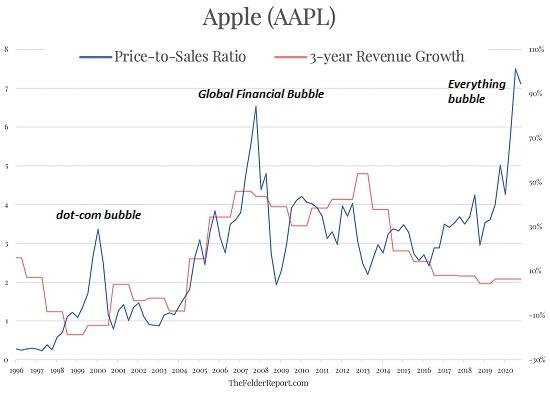

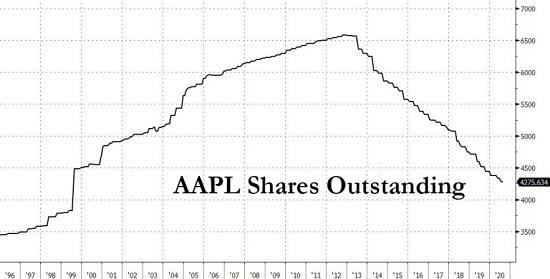

In American “capitalism,” the name of the game is scale up with cheap debt supplied by the Federal Reserve, use the “Fed free money” to buy up any potential competitors and then start buying back your own shares, jacking your share price even as sales and profits stagnate. (Charts of Apple below).

Once you’re too big to fail or jail, then you can gamble to your heart’s content because all the winnings will be yours to keep and if you lose big, the Fed or the Treasury will step in and transfer the losses to the debt-serfs and tax donkeys.

In America, as Warren Buffett jacks up the price of Sees candy, etc. to maximize his profits and add more billions to his net worth, and Amazon uses its quasi-monopoly power to relentlessly jack up the price of Prime membership, nobody asks Warren or Jeff “don’t you have enough already?”

The answer is “no”. It’s never enough, because as long as the Fed and federal government enforce, enable or allow your monopoly, quasi-monopoly or cartel to kill transparency and competition, and offer you limitless “Fed free money” while students pay 8% on their loans, then why not add another $10 billion to your personal wealth?

Go ahead and lie, cheat, embezzle, rig markets, commit fraud, collude–everything is allowed if you’re a powerful corporation because all your execs have get out of jail free cards from the Department of Justice. Nobody in Corporate America ever goes to prison no matter how egregious the fraud or theft. And you get to keep all the loot, other than a wrist-slap fine if you’re caught. But that’s just a modest cost of doing business in American “capitalism.”

If this “capitalism” was actually attractive to capitalists, why would everyone pile into the same six Big Tech monopolies? Is that really the only opportunity left to “create shareholder value,” to pour hundreds of billions of dollars in “Fed free money” into a handful of Big Tech monopolies?

Paraphrasing the late Immanuel Wallerstein, “Capitalism” is no longer attractive to capitalists. This “capitalism” is only attractive to parasites, predators, kleptocrats, legalized looters, embezzlers, fraudsters and all those insiders whose palms get greased along the way.

If you think this “capitalism” is sustainable, the future holds a big surprise.

{kind=link}