Christmas is no time to be given the old heave-ho. This is a time of celebration, redemption, and excess libation. A time to shop ‘til you drop; the economy depends on it. Don’t get us wrong. There really is no best time to receive the dreaded pink slip. But Christmas is the absolute worst. Has this ever happened to you?

The verdict: Orange man bad! [PT]

Well, believe it or not, this is precisely what House Speaker Nancy Pelosi and her Democrat degenerates in the House did this week with their partisan impeachment of President Trump. Not even Ebenezer Scrooge had a cold enough heart to fire Bob Cratchit on Christmas. In fact, Scrooge gave Cratchit Christmas day off – with pay.

For the record, Trump is a repulsive fellow. He chows Big Macs in bed and bloviates sulfurous gas back at the boob tube. After that, he feeds his resentments over a phone call with Sean Hannity. Then he uncorks on twitter. The sequence repeats every night and rolls into the morning like clockwork.

Perhaps this sort of behavior is beneath the stature of an esteemable President. But so what? It’s remarkably entertaining.

His eminence, God Emperor, Field Marshal & Stable Genius, Donald “Real” Trump, POTUS, fount of endless high quality entertainment and greatest troll in the world. [PT]

All the while, the Democrats – and Anderson Cooper – say The Donald is below the salt. The real question, though, is: Does he deserve to be impeached? To this day, no one – including Adam Schiff – actually knows.

House Democrats may have voted yes on their two articles of impeachment. But they failed to prove Trump guilty of these high crimes and misdemeanors. They bypassed American traditions of due process and a fair trial. In other words, Nancy Pelosi reduced the legislative branch of government to a kangaroo court.

Russian Bots

Make no mistake: Trump will come out of this fake impeachment in better shape than he started. He will be acquitted by the Senate. However, this assumes Pelosi transmits the articles of impeachment to the Senate; if she doesn’t, Trump isn’t technically impeached.

Regardless, House Democrats have gifted thousands of rounds of live ammo to Trump that he can fire back at his presidential challengers. What’s more, the most enduring political target of all time may be about to step into the clearing.

God may have created all creatures great and small. And who are we to second guess the lord’s handiwork? But there are certain creatures that improve the world with their absence.

Hillary Clinton, the political class’ incarnation of ringworm jock itch, is now scratching at another uncomfortable flare up. Year after year, decade after decade, she refuses to go away. Still, we’ve learned to make the best of it.

For instance, rather than getting agitated when seeing Clinton’s smug mug on the nightly news we marvel at what a fright her face has become. We can’t quite tell what in the world has happened. But whatever it is… the ugliness is cockadoodle awful.

Operation: Hopeless. [PT]

According to a recent Harvard-Harris presidential poll, Clinton is the top choice for registered Democrats for the party’s 2020 presidential candidate. She hasn’t thrown her hat in the ring just yet. However, when push comes to shove, Clinton will be compelled to run by Russian bots. You can count on it!

Real High Crimes and Misdemeanors

Of course, the fake impeachment and the upcoming presidential election are a great big distraction. The real high crimes and misdemeanors, the one all three branches of government and both parties are ignoring, is that Americans are compelled under legal tender laws to use unconstitutional money.

If you recall, Article I, Section 8, of the U.S. Constitution empowers Congress – not the Federal Reserve – to coin money and regulate its value. In addition, Article I, Section 10, specifies that money be coined of gold and silver and cannot be bills of credit – such as debt based legal tender notes.

By this, the dollar, in its present form, is illegal money on two counts. First, the dollar is issued by the Federal Reserve. Second, the dollar is a bill of credit with no ties to gold or silver.

The US dollar – then and now: From gold certificate to irredeemable Federal Reserve note [PT]

What gives? Isn’t the U.S. Constitution the supreme law of the land? Alas, this is only true so long as it’s politically expedient.

The fact is, government officials have failed to uphold their obligations. They’re operating in dereliction of duty. And until the high crime of illegal money is abolished, everything else is a great big farce.

Look, we don’t like it one bit. There are many creative ways for a nation to self-destruct. The corruption of money underlies them all. We’re doomed!

SEC Investigating BMW For Using “Sales Punching” To Potentially Inflate Sales Numbers

While Tesla continues to waltz around regulators, breaking any and all securities laws it wants to, underreserving its warranty liabilities and allowing its self-driving cars with human beta testers to slam into inanimate objects before bursting into flames, regulators have decided to instead pay attention to BMW.

It was reported yesterday that the SEC has now opened an investigation into whether BMW’s sales figures have been manipulated, according to the Wall Street Journal. On a side note, there’s been no word on whether or not BMW counts its “factory gated” vehicles in its press releases.

Instead, the SEC is looking at whether or not the automaker has engaged in “sales punching”, a practice that encourages dealers to register cars despite them not being sold.

BMW acknowledged they were being investigated, stating: “We have been contacted by the SEC and will cooperate fully with their investigation.”

BMW also faces litigation by European authorities on allegations of colluding with rivals to manipulate prices and control emissions. BMW has vowed to fight the case and took a $1.1 billion charge as a result in April.

The company has also faced headwinds due the U.S./China trade war’s effect on its Spartanburg, S.C. factory exports.

The SEC investigation comes as U.S. officials are reportedly pursuing other car companies suspected of engaging in the same practice.

Fiat paid a $40 million fine in September to settle claims by the SEC that the company had paid dealers to report exaggerated sales numbers. But don’t worry, the company has said it “reviewed and refined its sales reporting procedures and was committed to maintaining strong controls.”

We feel better.

Fiat was also forced to revise several years of sales results, nullifying a streak of 75 months of sales increases. Using the revised numbers, the streak ended in September 2013.

Regulators also found that VW had defrauded U.S. consumers and the U.S. government in 2015 by rigging their cars to cheat emissions tests.

As a reminder, the investigation into BMW comes at arguably the peak of the auto bubble – as well as the peak of auto regulator apathy. We recently reported that only 7% of incomes had been verified on new auto loans since 2017 and, despite these ongoing investigations into other companies, the name we see as the industry’s main offender, Tesla, has been mostly left alone by regulators.

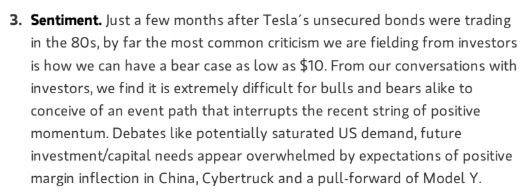

…Morgan Stanley felt as though it was necessary to make a joke of their own, by issuing an update note (for some reason) on its Tesla target, which we had previously reportedwas located somewhere in the gaping hole between $10 and $500.

The investment bank’s previous stance on the company was summed up in this exceptionally vague chart pointing out that Tesla stock could go – well, anywhere – over the next 12 months.

…and third, Jonas points out that the most “common criticism” he is fielding is how he could have a bear case as low as $10, while maintaining a bull case at $500.We wonder why…

But when it boils down to brass tacks, Jonas makes the admission (in bold print, no less) that “We are not bullish on Tesla longer term, especially as, over time, we believe Tesla could be perceived by the market more and more like a traditional auto OEM; we are prepared for a potential surge in sentiment through 1H20 but question the sustainability.”

Tesla being viewed as a traditional OEM would likely collapse the company’s share price, as the market is notorious for valuing low margin, capital intensive auto companies with minuscule earnings multiples. Additionally, Tesla doesn’t even have consistent earnings, so even applying a crippling P/E to the company in this case could prove difficult.

However, like any good analyst with a $490 spread between their bull and bear case, Jonas closes his note with some backhanded reasons for optimism:

We believe 2020 offers a strong event path for the stock; there are a number of catalysts over the next year, whether it be China milestones, Model Y, or new technology announcements that would allow Tesla to potentially test the upper bound of our admittedly wide bull-bear skew. We still see Tesla as fundamentally overvalued, but strategically undervalued.

When people tick off the components of the “everything bubble” they usually omit US housing, for a couple of reasons.

First, bubbles don’t normally recur immediately in the same asset class, because memories of past carnage need to fade before investors can be seduced back into irrational optimism. Since housing was the epicenter of the last boom/bust cycle, no one is looking there for evidence of new bubbles.

Second, the action in housing has been more gradual than in the 2000s, so it hasn’t generated a lot of breathless headlines about speculators making killings with other people’s money.

But this expansion has gone on for such a long time that even modest annual price gains have taken home prices back into bubble territory. And now the news is starting to reflect it. From today’s DollarCollapse.com “Real Estate” links list:

To recap, home prices are above their 2007 bubble peaks in many places while the wages of potential homebuyers have barely risen, which is squeezing ever-larger numbers of people out of the market.

Yet somehow the buying continues. This may not qualify as a mania, but it’s definitely looking dysfunctional, because where can a sector go from “record low affordability” if it wants to keep rising?

Going forward, one of two things has to happen.

Either buyers go on strike, as they (and their mortgage lenders) recognize that houses are a bad deal at current prices and mortgages written at those prices are unlikely to be paid off.

Or the government tries to keep the party going by lowering interest rates to make future mortgages easier to manage.

Since a dramatic slowdown in the housing market would take the rest of nominal GDP down with it, that will of course be seen as unacceptable, leading calls for lower rates, a weaker dollar and various other kinds of stimulus like tax cuts paid for with bigger deficits.

Put another way, even if housing doesn’t crash, the need to keep prices elevated is one more impetus for what looks like a tidal wave of monetary ease coming our way.

As we head into year-end, Goldman Sachs continues its tradition of taking stock of Top of Mind themes and highlighting what to look for next year.

On the heels of a 2018 characterized by solid growth and poor asset performance, 2019 has delivered the reverse. Indeed, growth has slowed considerably over the past year with our global current activity indicator (CAI) currently running around 2.6% versus 3.4% on average in 2H 2018. Meanwhile, a simple US 60/40 portfolio had one of the best risk-adjusted returns since the 1960s.

The strong asset performance was driven in large part by the Fed’s dovish pivot early in the year. With other central banks around the world following suit, easier monetary policy pushed rates globally down to or beyond historical lows. These shifts marked a decisive turn in the equity market cycle with equity markets—feeling somewhat comforted by the so-called “Powell put”— reaching new highs. In fact, equities had one of their best years since the initial recovery from the Global Financial Crisis, but almost all of the gains came from multiple expansion rather than profit growth, which was close to flat or even negative across the major economies.

This large market disconnect – with bond yields at or near all-time lows and equity indices at all-time highs—raised questions about how markets were viewing the growth outlook, and whether that view differed between bonds and equities—with equities just more optimistic. Our short answer: no. That’s because, scratching under the surface, equities were pricing their fair share of growth concerns as reflected, for example, in the outperformance of defensive sectors for much of the year.

Indeed, growth concerns prevailed for most of 2019 owing largely to the ongoing US-China trade war, which escalated further when President Trump imposed new tariffs on China in September and threatened additional tariffs slated for later in a “currency manipulator” following a sharp depreciation in the Yuan, which has helped to somewhat offset the impact of the trade war on the Chinese economy. As a result, currency wars became a new front in the ongoing trade war. And this development has evolved beyond US-China relations; President Trump recently announced his intention to impose tariffs on metals imports from Argentina and Brazil in response to the large depreciation in those countries’ currencies, which he argues is harming US farmers that compete with South American producers (but no official action has been taken.)

Beyond trade-related tensions, geopolitical risk also flared elsewhere later in the year, with Brexit uncertainty rising as the October 31st deadline for the UK withdrawal from the EU approached with no clear way forward, and a drone attack on Saudi Arabia’s Abqaiq oil processing facility—the largest such facility in the world—led to the single-largest disruption in global oil supply in history.

But looking ahead to 2020, we believe that some of these political/policy uncertainties that loomed over economies and markets this year are set to fade. In recent days, the US and China agreed to a “Phase 1” trade deal in which China has committed to large purchases of US goods and services as well as structural changes in areas ranging from intellectual property to currency policy in exchange for a cancellation of the next tranche of US tariffs and some rollback of existing tariffs. In our view, this likely marks the end of tariff escalation in the current US-China trade war.

And, just as the good trade news hit, the Conservatives won a decisive victory in the UK general election, finally clearing the path for an orderly withdrawal of the UK from the EU. This major hurdle for Europe was overcome in a year in which European elections led to critical leadership transitions on the continent that—despite fears of a growing populist influence— largely saw outcomes consistent with policy continuity.

Overall, we expect this decline in political uncertainty— combined with a positive impulse from financial conditions, a resilient consumer and some fiscal expansion in places like Europe (though likely not as much as they need) to lead to a sequential growth pickup in 2020, with global growth rising to 3.4% (from about 3.1% this year), led by the US and the UK.

We believe this sequential improvement should provide a broadly supportive environment for risky assets in 2020. That said, in recent months, markets have already begun to price a better growth outlook, which has been reflected, for example, in a sharp rotation towards pro-cyclical assets, and which has already pushed risky assets to relatively rich levels. And we don’t think monetary policy will provide a similar tailwind to markets this year given our expectation that the Fed—as well as the ECB and the BOJ—will keep interest rates on hold despite continued White House pressure for easier monetary policy. Although this pressure continues to raise concerns about central bank independence, with the Fed nevertheless recently pausing rate cuts, fears of political influence in central bank decision making doesn’t seem to be playing out so far (although we still view the bond markets as an indirect channel for such influence.)

In our view, all of the above suggests positive but lower returns across assets in 2020, with total equity returns across the major regions ranging from the mid-to high-single digits, US 10yr Treasury yields rising modestly above 2% and the Dollar index remaining relatively rangebound in the near term before weakening moderately on signs of improving global growth.

But while the growth and policy outlooks provide some reasons for mild optimism, of course political uncertainty is not entirely behind us. There is little doubt that the 2020 US presidential election in particular will be a major market focus throughout the year with policies on everything from taxes, to trade, to healthcare to buybacks (where we’ve still seen a fair amount of Congressional attention but no legislative action) all in question. But here we continue to emphasize that the outcome of the Congressional elections will likely be just as important as the presidential election in terms of material policy changes in most of these areas (save trade!).

In the words of the wise

“Central banks should have constrained missions centered on maintaining monetary system stability…The more they stray into other areas, the greater the distributional effects, and so the greater the temptation-or even the need-to re-politicize them by the back door.”

– Sir Paul Tucker, Former Deputy Governor, Bank of England

“People underestimate how reliant on liquidity the global financial system has become; at almost 40% of GDP, global liquidity is crucial.”

– Rick Rieder, CIO of Global Fixed Income, BlackRock

“There is now only a limited amount of stimulant left in the bottle, and the sooner we use it, the sooner it will run out.”

– Ray Dalio, Founder and Co-CIO, Bridgewater Associates

“Fundamentally…not much has changed… it’s just that the market swung from looking at things optimistically to looking at them pessimistically.”

– Howard Marks, Co-founder and Co-Chairman, Oaktree Capital Management

“It is crucial to have a group of people who analyze the economy with respect to the long-run goals of economic policy…politicians have a much shorter timeframe in mind than is consistent with achieving these goals.”

– Donald Kohn, Former Vice Chair, US Federal Reserve

“There is no shortage of things to worry about. I would simply say…that as the US continues to pull back, its alliances grow weaker, and international institutions fail to keep up with new challenges, instability is likely to go up in the world. So the future is likely to be far more turbulent than the recent past.”

– Richard Haass, President, Council of Foreign Relations

“At the ELB—when monetary policy is constrained—the case for fiscal policy to support demand and help maintain output at potential becomes compelling.”

– Olivier Blanchard, former Chief Economist, IMF

“Given the behavior of the past several years, I would not rule out additional [ECB] policy mistakes, such as a rate hike even if it is unwarranted…there seem to be other factors-legal challenges, politics-that influence [ECB] decisions.”

– Athanasios Orphanides, former member, ECB Governing Council

“ If a company buys back stock for the wrong reasons and good investments are turned down, that is troubling. But addressing that problem requires a scalpel not a bludgeon.”

– Aswath Damodaran, Professor, NYU Stern School of Business

“Trapping resources in larger and older businesses not only inhibits the overall size of the pie…but also tends to reinforce the unequal distribution of the pie.”

– Steven Davis, Professor, The University of Chicago Booth School of Business

“The reality is that the EU is a challenging project. But even today the forces of integration are stronger than the emboldened forces of disintegration.”

– Jose Manuel Barroso, fmr. President of European Commission

“The US is underestimating the influence of the hardliners, or hawks, in China and the degree to which Chinese nationalism and anti-American sentiment has grown since the early 1990s. This is the biggest mistake we have made over the last several decades.”

– Michael Pillsbury, Director for Chinese Strategy, Hudson Institute

“While I don’t think the Fed is cutting rates because the White House is telling them to, you can’t completely separate the politics from the market signals feeding into the Fed’s decision-making.”

– Jan Hatzius, GS Chief Economist

“ The complexity for the US is that the more the US intensifies the trade war, the more pressure there is for a weaker Yuan. And the challenge for the world is that if China tries to offset weak trade with the US with a weaker Yuan, that puts more pressure on other economies to depreciate their currencies in order to avoid losing out to China.”

– Brad Setser, Senior Fellow, Council on Foreign Relations

“Trump’s actions have led to a more unified nationalist resentment of the US-and a view that not just Trump, but American society, is trying to contain China’s rise.”

– Susan Shirk, Chair, 21st Century China Program

“The likelihood that President Trump wakes up and says it’s time to go to war with Iran is probably zero. His lack of desire for another war in the Middle East is one of the few positions he’s maintained consistently from the get go.”

– Richard Nephew, Senior Research Scholar, Columbia University

“I think we should keep a longer-term perspective. Yes, interest rates are low, and they may be low for a while, but they won’t be low forever. And when they rise of course the cost of debt will increase again.”

– Alberto Alesina, Professor, Harvard University

“Just because manipulation is a smaller concern today doesn’t mean it will stay that way. I worry that it will be a problem in the next recession.”

– Joseph Gagnon, Senior Fellow, Peterson Institute for International Economics

Revisiting 2019 Themes… Crossword Style

Source: Goldman Sachs

Across:

2. This treaty that was implemented in 2009 gave expanded powers to the European Parliament (Issue 78).

7. According to Richard Haass, President of the Council on Foreign Relations, the Middle East matters for many reasons beyond just _____ resources (Issue 83).

11. After rate cuts and quantitative easing programs, the financial world is now often described as awash with _____ (Issue 80).

12. Athanasios Orphanides, fmr. member of the ECB Governing Council, believes that the _____ guided inflation too low by not allowing its balance sheet to expand sufficiently after the global financial crisis (Issue 76).

13. In 2014, government purchases of _____ currencies declined significantly as the global economy recovered (Issue 82).

14. Ray Dalio, Founder and Co-CIO of Bridgewater Associates, is concerned that _____ policy will be dangerously low on power in the next few years (Issue 80).

15. Michael Pillsbury, Director for Chinese Strategy at the Hudson Institute, argues it is imperative that China earn its way out of _____—a view that President Trump has consistently held (Issue 79).

21. Steven Davis, Professor at the University of Chicago Booth School of Business, believes that buybacks don’t affect the level of _____ in the economy; they only affect its distribution (Issue 77).

22. The Federal Reserve does not have a mandate to target the _____ rate (Issue 82).

24. With markets performing well after the Fed’s dovish pivot, some observers have suggested that there is “a _____ put” on the S&P 500 (Issue 76).

25. Howard Marks, Co-Founder and Co-Chairman of Oaktree Capital Mgmt., believes that over the past two years, markets were excessively _____ (Issue 75)

26. Joseph Gagnon, Senior Fellow at the Peterson Institute for International Economics, worries that currency _____ will be a problem in the next recession (Issue 82).

27. Given substantial evidence of a large tax _____, Alberto Alesina, Professor of Political Economy at Harvard University, believes that any fiscal expansion should focus on cutting taxes rather than on increasing spending (Issue 84).

28. The notion that debt accumulation reduces capital formation is only true when the economy is at full _____ (Issue 84)

29. _____ took out an ad in the NY Times in 1987 to discuss how the US was being disadvantaged by foreign countries in the trade area (Issue 79).

30. Support for _____ parties has increased significantly across Europe (Issue 78).

Down:

1. The Trump administration’s policy toward Iran included pulling out of the 2015 _____ agreement (Issue 83).

3. The Federal Reserve set itself an inflation target under the chairmanship of _____ (Issue 81).

4. Buybacks have been the single largest source of US _____ demand each year since 2010 (Issue 77).

5. Over the past several years, rising _____ were the main drivers of global equity returns (Issue 75).

6. Historically, the Federal Reserve has had to cut rates by roughly_____ percentage points on average during recessions (Issue 80).

8. This country has the largest amount of seats in the European Parliament (Issue 78).

9. The Federal Reserve ended its balance sheet _____ sooner than expected (Issue 76).

10. Olivier Blanchard, fmr. Chief Economist of the IMF, does not blame fiscal or monetary policy for weak growth in Japan, instead saying it has to do with _____ (Issue 84).

16. Aswath Damodaran, Professor at the NYU Stern School of Business, thinks of buybacks as _____ dividends, in that they can vary from year to year depending on how much cash a company has (Issue 77).

17. US economic recoveries have never lasted more than this many years (Issue 75).

18. Susan Shirk, Chair of the 21st Century China Program at UC San Diego, believes that _____ technologically from China will ultimately weaken US technological innovation (Issue 79).

19. Sir Paul Tucker, fmr. Deputy Governor of the Bank of England, regards central banks as the _____ pillar of unelected power (Issue 81).

20. US sanctions imposed on Iran over the past two years have included a demand that oil exports effectively go to _____ (Issue 83).

23. Donald Kohn, fmr. Vice Chair of the US Federal Reserve, believes that central bank independence is still important today despite an environment of low _____ (Issue 81).

* * *

Finally, here’s Howard Marks

“I don’t believe that we’re in a bubble, and I don’t think we’re going to have a crash…But for an investor, I think the next five years simply aren’t going to be as good as the last ten.”

– Howard Marks, Co-Founder and Co-Chairman, Oaktree Capital Management

As a busy 2019 in the oil and gas industry ends, analysts are busy issuing predictions about next year and what they would mean for oil markets and prices.

This year saw a mix of some of the more predictable events – such as OPEC and Russia extending their cooperation pact, twice – and a ‘black swan’ such as the September attacks on Saudi oil facilities which cut off 5 percent of daily global oil supply for weeks.

As black swans are, by definition, unpredictable, analysts focus on predicting the ‘knowns’ in the market for 2020 as they see them at the end of 2019.

There are many factors to watch in oil markets next year, both in the U.S. and globally.

For the sake of simplicity, here are 10 of the most important predictions and factors to watch in the oil and gas industry in the United States and worldwide.

Independent energy analyst David Blackmon has summed up some predictions, concerning mostly the U.S., for Forbes.

And these are:

1) U.S. shale production will continue to grow

U.S. shale growth is slowing down, but all analysts and organizations still expect oil supply from the United States to continue to rise in 2020. Growth may be slower, due to reduced capex from drillers, but U.S. will still be the main contributor to non-OPEC supply growth next year.

2) Rig count will remain stable

Despite the fact that the U.S. oil and rig count declined by more than 250 units this year to December 20 compared to the same time last year, the number of active oil rigs last week saw an increase of 18 rigs—the first double-digit growth since the beginning of April, according to Baker Hughes data.

3) U.S. oil and LNG exports will continue to rise

Exports of U.S. oil and liquefied natural gas (LNG) are expected to grow with the increase in infrastructure capacity in 2020.

The United States exported more crude oil and petroleum products than it imported in September 2019—the first month in which America was a net petroleum exporter since monthly records began in 1973, the U.S. Energy Information Administration (EIA) said earlier this month.

Total U.S. crude oil and petroleum net exports are expected to average 570,000 bpd in 2020 compared with average net imports of 490,000 bpd in 2019, according to EIA’s latest Short-Term Energy Outlook (STEO).

4) Oil and gas prices will remain range-bound in 2020

Rising production from non-OPEC nations not part of the OPEC+ deal, driven by the U.S., Brazil, and Norway, is expected to keep a lid on oil prices, while OPEC+ cuts and an expected pick-up in global economic and oil demand growth will keep a floor under prices.

5) Sudden supply outages will have smaller impact on oil prices

Due to the growing non-OPEC supply, unexpected and short-lived outages are likely to have a smaller impact on oil prices than they would have on markets five or ten years ago, analyst Blackmon says.

Case in point—the mid-September attacks on critical Saudi infrastructure sent oil prices soaring—with WTI Crude touching a five-month high of $62.90 a barrel—but just for one day, as slowing demand growth and a protracted trade war weighed on prices.

6) Bankruptcies in the U.S. shale patch are set to grow

The number of bankruptcies and companies seeking protection from creditors is expected to rise in 2020, continuing the trend from 2019.

Haynes and Boone estimated at end-September that the U.S. oil and gas industry had 33 filings year to date in September, more than the number of filings in each of 2017 and 2018, at 24 and 28 filings, respectively.

With reduced capital availability in equity and debt markets, more of the smaller companies could struggle through the next year.

7) U.S. oil and gas mergers & acquisitions are poised to rise

A growing number of distressed U.S. oil and gas firms and few funding options could mean that the ‘smaller guys’ could be acquired by bigger shale players or the smaller guys could team up to scale operations and cut costs.

Signs of consolidation in U.S. shale have already started to emerge, and the wave is expected to continue in 2020.

Shareholders of Callon Petroleum and Carrizo Oil & Gas approved an all-stock merger last week.

Two months ago, Parsley Energy and Jagged Peak Energy announced that Parsley would buy Jagged Peak in an all-stock transaction valued at US$2.27 billion, including Jagged Peak’s debt.

“The inevitable consolidation in the Permian has started and Jagged Peak made a decisive move to team up with the right partner,” said S. Wil VanLoh, Jr., a Jagged Peak director and the founder and CEO of Jagged Peak’s controlling shareholder, Quantum Energy Partners.

In its Q3 2019 Oil & Gas deals insights, PwC said:

“In the quarters ahead, we expect to see more companies merging to create scale, companies continuing to focus on generating positive cash flows and shareholder value, while struggling companies will become more amenable to being acquired or seeking restructuring through bankruptcy.”

Internationally, the key factors to watch in oil markets will be:

8) How oil demand growth will fareas the U.S.-China trade dispute de-escalates

Oil prices hit a three-month high on December 13 amid growing optimism of a phase-one trade deal. In the days following the announcement that a phase-one deal had been reached, China removed six chemicals and oil derivatives from its list of tariffed U.S. imports.

9) How OPEC+ cooperation will proceed after March 2020

Another key factor to watch is what OPEC and its Russia-led non-OPEC partners will do after March 2020, when the current agreement for deeper cuts expires. The next move by the cartel and its allies will largely depend on how oil demand growth will fare in the typically low-demand growth season in Q1. The move will also depend on how much oil OPEC and friends will have managed to withhold from the market compared to plans—that is, whether all members will have fallen in line and stopped cheating.

10) Sudden supply outages in restive regions

Oil market participants will continue to monitor developments in Libya and Iraq, which could suddenly tighten the market more than anyone had intended to.

After yesterday’s dismal 2Y auction, which printed at the lowest bid to cover since 2008, few were looking forward to today’s 5Y auction which would come in an environment of even worse liquidity coupled with a continued selloff across the Treasury complex this morning.

Yet to everyone’s surprise, the sale of $41 billion in 5Y notes was nothing short of stellar, with the high yield coming in at 1.756%, which while above last month’s tailing stop of 1.587%, stopped through the When Issued 1.772% by a whopping 1.6bps, the biggest stop through since February 2016!

Also unlike yesterday’s disappointing 2Y auction, the internals today were quite impressive, with the bid to cover virtually unchanged from November’s 2.50, at 2.49, the second best since July 2018, and well above the 2.38 six auction average.

Finally the takedown was also on the strong side, with Indirects taking down 62.4%, above the recent average of 59.9%, and with Directs taking down 16.1%, the most since August 2019, Dealers were left holdings 21.5%.

In kneejerk response to the stellar 5Y auction, yields have tumbled across the curve which was to be expected for an illiquid session, yet the 10Y rate plunging from 1.94% just before the auction to a sub 1.90% print shows just how little liquidity there is in the bond market at this moment.

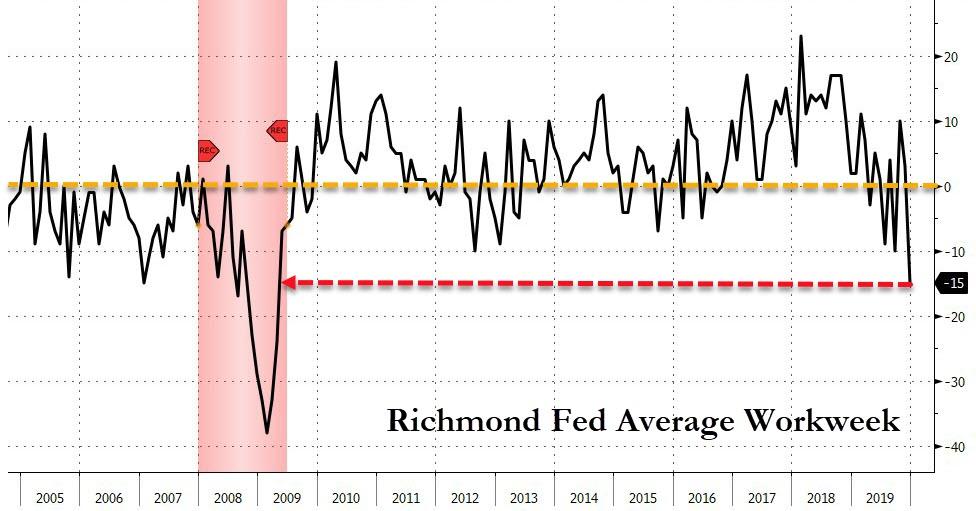

Richmond Fed Tumbles Into Contraction, Confirms Regional Fed Survey Slump

Confirming the pessimistic plunges in Kansas City and Philadelphia, The Richmond Fed’s Manufacturing Survey disappointed, tumbling to -5 from -1 last month (and expectations of a bounce to +1).

Source: Bloomberg

Under the hood was more worrisome:

Shipments fell to -6 after -2 the prior month

New order volume slowed to -13 after -3 the prior month

Order backlogs were unchanged at -11 after -11 the prior month

Capacity utilization slowed to -12 after 2 the prior month

Inventory levels of finished goods increased to 22 after 15 last month

Inventory levels of raw goods rose to 21 after 20 last month

So, inventories up, new orders and shipments tumbling?! Doesn’t sound like a renaissance in America to us.

And the average workweek crashed to its worst since April 2009…

Source: Bloomberg

Of course, as long as the PMIs are rebounding no one will pay attention to this… yet

House Democrats may conduct a second impeachment of President Trump, according to lawyers for the Judiciary Committee.

In a Monday court filing reported by Politico, House Counsel Douglas Letter argued that they still need testimony from former White House counsel Don McGahn, which may uncover new, impeachable evidence that Trump attempted to obstruct the Russiagate investigation (of a crime he didn’t commit).

“If McGahn’s testimony produces new evidence supporting the conclusion that President Trump committed impeachable offenses that are not covered by the Articles approved by the House, the Committee will proceed accordingly — including, if necessary, by considering whether to recommend new articles of impeachment,” reads Letter’s filing.

Underscoring this point, House lawyers say if McGahn’s testimony yields more evidence of obstruction it could lead to “new articles of impeachment.” pic.twitter.com/DXiEl0KXwL

The Democrats also argue that “McGahn’s testimony is critical both to a Senate trial and to the Committee’s ongoing impeachment investigations to determine whether additional Presidential misconduct warrants further action by the Committee,” adding that McGahn’s testimony may also be relevant to future legislation which may stem from the details of Trump’s conduct.

And while DOJ lawyers acknowledged in a Monday brief that the legal fight over McGahn isn’t moot, the fact that the House Judiciary Committee moved forward with impeachment on a completely different matter removes the urgency to resolve their case.

“The reasons for refraining are even more compelling now that what the Committee asserted — whether rightly or wrongly — as the primary justification for its decision to sue no longer exists,” wrote lawyers for the DOJ. The agency also argues that the Mueller impeachment investigation is over, when House lawyers and lawmakers have described it as ongoing and active, according tothe report.

McGahn’s participation in House impeachment proceedings was blocked by the White House, which claimed “absolute immunity” for advisers.

President Trump chimed in over Twitter followingthe Monday court filing, quoting “Fox and Friends” host Brian Kilmeade, who said “now all of a sudden they are saying maybe we’ll go back and visit the Mueller probe, which is absolutely unbelievable, and shows they don’t care about the American public’s tone deafness…”

….the American public’s tone deafness – & it should be intolerable, because the American people have had it with this.” @kilmeade@foxandfriends The Radical Left, Do Nothing Democrats have gone CRAZY. They want to make it as hard as possible for me to properly run our Country!

DOJ attorneys argued that the upcoming Senate trial is yet another reason for the judicial branch to refrain from the case.

“If this Court now were to resolve the merits question in this case, it would appear to be weighing in on a contested issue in any impeachment trial,” wrote DOJ lawyers. “The now very real possibility of this Court appearing to weigh in on an article of impeachment at a time when political tensions are at their highest levels — before, during, or after a Senate trial regarding the removal of a President — puts in stark relief why this sort of interbranch dispute is not one that has ‘traditionally thought to be capable of resolution through the judicial process.’”

“This Court should decline the Committee’s request that it enter the fray and instead should dismiss this fraught suit between the political branches for lack of jurisdiction,” they added.

{kind=link}