A new Zogby poll shows President Trump beating all the potential Democratic candidates in a hypothetical 2020 run off.

The numbers show that Trump beats Biden 46-45%, he’s ahead of Warren 47-43% and also beating Bernie 47-45%.

The figures also show that amongst college educated Americans, Trump performs even better when up against the farthest left candidates, beating Warren and Sanders 50-45%.

“Trump is winning with union voters (Trump leads 48% to 42%) and consumers-NASCAR fans (Trump leads 63% to 32%), weekly Walmart shoppers (Trump leads 54% to 37%), and weekly Amazon shoppers (Trump leads 54% to 43%),” reports Zogby.

The numbers are particularly impressive given the onslaught of attacks and negative media coverage Trump has received.

“The scale of media involvement in the 2020 election will likely be the most massively biased propaganda effort in the history of U.S. media manipulation,” comments Conservative Treehouse.

“Together with the big tech effort from control operatives in social media, the scale of unified effort is likely to exceed Orwellian proportions.”

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Virginia is the latest state to consider sweeping state-level housing reform. A new bill would legalize duplexes on residential land statewide, making the Old Dominion the third state, after Oregon and California, to essentially abolish single-family zoning.

Urbanists have praised the bill as a great way to produce more (and more affordable) housing in high-demand areas. Some conservative critics meanwhile warn that legalizing two-unit homes is just the opening shot in the war on suburbia.

“Across the country, there is a shortage of affordable units that is putting a squeeze on working families and contributing to rises in rents for existing units,” tweeted Del. Ibraheem Samirah (D–Fairfax), the duplex bill’s author. “Unfortunately, the kind of dense ‘middle housing’ that could be built to alleviate the shortage is banned on most lots.”

Samirah’s legislation, H.B. 152, is pretty straightforward. It would require Virginia’s local zoning ordinances to allow two-family homes on all land that’s currently zoned to permit only single-family homes. Localities would also be forbidden from demanding that new duplexes obtain special use permits or meet other conditions that aren’t also required of single-family dwellings.

The bill still allows counties and cities to determine setback, design, and environmental standards for new housing. It explicitly states that it would not prevent local authorities from permitting new single-family homes—they just can’t outlaw duplexes.

H.B. 152 is part of a package of housing bills introduced by Samirah, including one, H.B. 151, that would legalize accessory dwelling units (ADUs)—sometimes known as in-law suites or granny flats—on single-family lots as well.

California passed a bill this year that allows homeowners statewide to build up to two ADUs on their property, effectively eliminating single-family zoning. An Oregon bill similarly made it legal to build duplexes on single-family-zoned land in cities of 10,000 or more people, and four-unit dwellings on single-family plots in cities of 25,000 or more.

Legalizing duplexes across the state could see some especially high-cost areas add a lot of new housing, says Emily Hamilton, a housing policy researcher at George Mason University’s Mercatus Center.

“I think it will have the biggest effect in localities where a lot of single-family homes are being torn down and replaced by fancier, new, larger single-family homes,” says Hamilton, citing the Northern Virginia communities of Arlington, McClean, and Falls Church as examples. “In many, or perhaps most cases, rather than build a new very expensive single-family home, we’d see those [duplexes] built as homes.”

Building a duplex or townhome could allow a developer to sell each unit for less than a single-family home while still making more on the lot as whole, she points out.

Two-unit homes in high-demand areas would still be pretty expensive, Hamilton tells Reason. But they’d nevertheless be adding housing supply to these desirable neighborhoods, freeing up housing in less desirable areas for lower-income renters and homebuyers.

Supporters of the bill have touted other possible progressive outcomes from H.B. 152.

Alex Baca, a housing program organizer for Greater Greater Washington, toldCityLab that zoning has been “a tool for wealthy white communities to maintain segregated neighborhoods” and that eliminating single-family zoning would be a boon to racial equity.

Samirah himself has called single-family zoning the modern equivalent of “redlining“, arguing the kind of middle housing his bill would legalize would be more affordable to lower-income people and people of color.

He has also pitched his duplex bill as an environmental measure, writing that “upzoning would make it easier to cluster around environmentally-friendly transit options.”

Some Republican officials and conservative media have seized on such statements to paint H.B. 152 as an assault on the suburban lifestyle.

Samirah’s bill amounts “a power-grab to take away the ability of local communities to establish their own zoning practices…literally trying to change the character of our communities,” Fairfax County Republican Committee Chairman Tim Hannigan told the Daily Caller.

That Caller article, written by Luke Rosiak, warned that H.B. 152 will “quickly transform the suburban lifestyle enjoyed by millions, permitting duplexes to be built on suburban lots in neighborhoods previously consisting of quiet streets and open green spaces.” In subsequent comments on Twitter, Rosiak denounced “soy boy urban (central) planners” who failed to appreciate either the “nature” and”rugged individuality” that current single-family zoning enables.

At Vox, Matt Yglesias chalks up the conservative reaction to Samirah’s bill to the left-wing language the delegate has used to pitch it.

“Rhetorical strategies designed to overcome left-wing opposition to useful market-oriented policies can backfire by provoking conservative opposition to them,” writes Yglesias. “It’s an example of how almost all politics is, at some level, identity politics.”

That kind of talk, he says, might be suitable for selling upzoning to Bay Area progressives, but it’s counterproductive in more purple Virginia.

It’s an interesting idea, but I’m not sure it’s right, given how readily people of all ideological stripes have seized on the “our communities are under siege” line to oppose legislation that increases density.

Berkeley Mayor Jesse Arreguín, no one’s idea of a conservative, has dubbed California’s state-led upzoning efforts “a declaration of war against our neighborhoods.” Activists from San Francisco to Seattle have fought density-increasing bills on the grounds that they would allegedly displace, not help, low-income people of color.

Sometimes conservative-leaning upzoning opponents will even adopt progressive talking points to argue against greater density. Beverly Hills’ Republican mayor, for example, has called state-level upzoning proposals “a flawed Reaganomics trickle-down theory of market economics.”

That’s because self-interest, not ideology, explains most opposition to housing reform.

Local governments, whether controlled by Team Red or Team Blue, don’t like losing power. Homeowners who have a financial stake in limiting new housing supply don’t like to see land use decisions removed from a part of the government that they have more influence over.

If H.B. 152 were intended as a weapon to destroy Virginians’ cherished suburban lifestyle, Hamilton notes, it wouldn’t be a very good one.

“I don’t think the bills would be an effective war on suburbia,” she says. “It won’t make sense to tear down single-family homes in the vast majority of cases. It’s limited to very expensive localities where this makes sense.”

Indeed, by preserving design and setback regulations, Samirah’s legislation will leave localities with a lot of tools to thwart new duplexes and ADUs from being built.

But the bill’s potential to add more housing supply, and to enhance landowners’ property rights, still makes it a worthwhile effort. It’s also a sign that sensible housing reforms first adopted by a few select states may be starting to go national.

from Latest – Reason.com https://ift.tt/2spJB0d

via IFTTT

Here Is The Last Ever Gartman Letter, In Which Dennis Shares Lessons Learned… And A Warning

Today is a historic day: not only is the last day of a fascinating, tumultous decade, it also marks the end of a three decade tradition: the daily publication of The Gartman Letter. As we reported last month, today the final edition of Dennis Gartman’s iconic newsletter will hit client inbox one last time, after which the 69-year-old “world-renowned commodity guru” is done waking up at 1am every morning to tell you what the market will do (or won’t, as the case may have been more often than not in recent years) and will shift “to a totally different and much less rigorous life… perhaps producing a biweekly commentary and a podcast or two each week as we deem it necessary.”

But as Dennis goes, if only to return shortly in some abbreviated media format, he has one last warning to the bulls, pointing out that most asset classes today have unappealing long-term expected returns, and that stocks are “either overvalued or extremely overvalued right now.”

However, as Barron’s Mark Hulbert who recently interviewed Gartman writes, instead of merely stretched fundamentals, Gartman’s pessimism derives from deeper place: namely, what he perceives to be the absence of fear among market participants and a pervasive lack of experience. And with an entire generation or two having never witnessed a sharp market drawdown, Gartman warns that the coming bear market will “do real and perhaps severe damage to portfolios everywhere.”

… we are quite certain that when this bull market ends it shall end very badly for such markets always do end badly. The buyers have enjoyed having the investment winds at their backs. But those winds will eventually shift course and when they do shift, they shall swamp everyone… the reckless neophytes as well as the conservative, sophisticated investors alike. When the next bear market comes… and IT WILL COME!… those who out-perform will be those who lose the least for when the market does fall 25-30% in some twelve-month period the manager who is down “only” 9% will be the hero of the age.

Thus these all-too-easily-made profits enjoyed so readily by the neophytes will evaporate with these inevitably changing investment winds just as the profits of 1999-2000 evaporated into the thinnest of air in 2001—2002 and just as the profits of 2005-2007 evaporated in the collapse of ’08-’09.

As Hulbert adds, to Gartman the current environment as a “kids market,” relying on a phrase introduced in the 1960s by George Goodman, in his classic book The Money Game. Goodman used the phrase to refer to an investment environment in which the traders making the most money are those too young to remember the last bear market.

Gartman – who in January 2016 famously predicted that he “won’t see $44 crude in my lifetime” only for oil to soar just a few months later – describes today’s “kids” as “young, brash, utterly naive, ill-educated, egregiously overconfident, neophyte-yet-fearless ‘investors’.” And with kids taking over, “market veterans” such as Gartman are left to do little more than stand on the sidelines, “fearful yet envious” of the kids’ profits.

That said, this isn’t the first “kids market” Gartman has encountered in his career, and as he points out, all have ended badly, as will this one. When it does, the “all-too-easily-made profits [of today’s] kids” will evaporate,” echoing a warning finance experts handed out to bitcoin billionaires who had to be put on waitlist for Lambo purchases back in early 2018 before the crypto market tumbled.

To Gartman, who invokes the vivid imagery created by Dante who needed Virgil as a skilled guide to take him across the circles of hell, avoiding this boom-to-bust cycle requires a wise advisor with the battle scars of having lived through a bear market, because as Gartman says, “no amount of education can substitute for that experience.” That’s why he doesn’t trust “a 26-year old who has just gotten his M.B.A. and has no experience.” His advice: “Don’t follow anyone who hasn’t been around for at least an entire cycle.”

Unfortunately for Gartman, and with the blessing of the Fed whose mission has mutated into making sure idiots appear as market geniuses in an artificial market that will never drop, it is the 26-year-olds that have the last laugh for now. To be sure, Dennis remains patient and fully acknowledges that the stock market may continue rising for a while longer before eventually succumbing to a bear market. But even if it does keep rising, he told Barron’s that its potential reward relative to its potential downside is far less attractive than it is for agricultural commodities, which is currently Gartman’s favorite asset class, as it is “unbelievably inexpensive right now.”

We leave it to 2020 to validate or disprove Gartman’s prediction (if his track record in retirement is similar to his professional one, the market may very well never crash), however since we commiserate with Gartman who clearly was caught offside by last decade’s centrally-planned market in which nothing makes any sense any more, we wish to convey some of Gartman’s lessons learned over more than 30 years of watching various markets, which he published in the final edition of the Gartman Letter and which we republish below for the benefit of the next generation of traders:

WHAT HAVE WE LEARNED: This being the final edition of The Gartman Letter as we drift off to a far less onerous schedule producing a bi-weekly written commentary and doing pod-casts on an as yet undecided upon schedule, we need to leave our friends/clients/readers around the world some thoughts on what we have learned about the markets and so we are today doing exactly that.

Firstly and perhaps most importantly we’ve learned that the single most import Rule of Trading is to never, ever, ever add to a losing trade. As our old friend, Paul Tudor Jones, says “Averaging losers is for losers.” If one buys a stock at $50/share and it goes to $45, why are you buying more when the market is telling you that your decision was the wrong on? You may simply be early but early in our business is the same as being wrong; or you may have the trade/investment thesis entirely wrong and the stock is headed toward much lower prices or even perhaps to bankruptcy. Enron was a highly touted stock at nearly $91/share; it was bankrupt two years later! Better it is to wait until the stock in question is profitable for then the market is telling you that you are right; that your thesis is the correct one; that the investment wind is at your back and that the investment coast is clear.

We have learned this the hardest of ways, by having broken the rule; having averaged down and having almost always suffered even greater losses than we had originally suffered. Indeed, the market’s gods are wily enough to entice you into averaging down once or twice and for that to have proven profitable, only to trap you into the third time when the market moves materially and seemingly relentlessly against you in a career ending collapse.

Secondly, we have indeed learned that as Lord J.M. Keynes and Dr. A. Gary Shilling told us, the markets can remain illogical far longer than we can remain solvent. Our investment corollary to that is that the market will return to rationality the moment you have been rendered insolvent and then shall turn on the proverbial dime and move in the other direction. It happens all the time. It will happen again; count on it!

Thirdly we have also learned that as Keynes said, “When the facts change, I change.” That is, when the market and/or the fundamentals as we had understood them turn against us it is best to admit that the facts of the investment in question have changed and that holding on is an illogical and almost always a very costly decision.

We have learned that markets move in very large cycles and that what is very popular now will inevitably become unpopular and that what is manifestly unpopular now shall become popular again. As Ecclesiastes tells us, “To everything there is a season” or as Caesar’s servant reminded him “Ubi sunt qui ante nos fuerunt?”… Where are they now? We have learned too that trying to anticipate the turn from popular to un-popular and from un-popular back to popular is a mug’s game for as noted above, illogic can obtain for a very, very long while.

We have learned to listen to those who have in the past been the wisest for wisdom is a God-given talent and rarely is lost. The Wise of years past will likely remain the Wise of coming years. The Keyneses, Shillings, Wesburys, Kasses, Perrys, Tudor Joneses, Grants, Williamses, Coxes, and Buffetts et al were wise in the past and will be wise in the years ahead because they have all been battle tested and have survived.

We have learned that bad things happen far more quickly than do good things and that bear markets are far more severe and swift and terrifying than are bull markets. As the late economist, Rudiger Dornbusch, once so wisely said, “In economics, things take longer to happen than you think they will and then they happen faster than you thought they could.” This is especially true in the transmission from bullish to bear markets and from economic expansion to recession.

We have learned that economic news doesn’t matter until it matters and then it matters… a lot.

We have learned again and again and yet again that markets that won’t go up on bullish news are not bullish markets or have finished their previous bullish run; conversely, markets that won’t go down on bearish news are not bearish or have finished their bearish run.

We have learned that friends mean a lot in the business of trading/investing… perhaps more than anything else and we acknowledge all of the men and women who’ve been friends over the years too many to mention but who shall not be forgotten [Ed. Note: Steve, you’re #1.].

Finally we have learned that we’ve been involved… and will remain involved… in the greatest of all businesses that allows us to match wits with geniuses on a daily basis. There is nothing quite like it, really. We count ourselves blessed and very, very lucky to have staked out a position in the capital markets and that we’ve perhaps even added a bit to the accumulated wisdom incumbent therein. And above all, we’ve been lucky to report to the greatest of all CEOs… our lovely bride of 30+ years, Margaret, who kept us focused when times were rough and even when times were great. We’ve been fortunate. Thanks to everyone! We mean that sincerely. THANKS TO EVERYONE!

2019 Greatest Hits: The Most Popular Articles Of The Past Year And A Look Ahead

One year ago, when looking at the 20 most popular stories of 2018, we admitted that perhaps as a result of too many conflicting narratives and storylines that emerged in 2017 and earlier in the decade, it was difficult to find a coherent theme to the key events that shook the world, and which you, our readers, found most interesting and notable.

Indeed, we said that “it is difficult to say that 2018 provided much needed closure to many of the themes and narratives that emerged in the previous year and earlier, most of which played out in the political arena, where for the first time in decades the non-establishment president of the world’s biggest superpower, a manifestation of the “protest vote” that had built up over the past decade, shook to the core everything that the world had taken for granted, setting the stage for a dramatic revulsion from widely accepted norms and principles.”

As we had warned for years, the vast if silent majority, feeling snubbed and neglected by the political oligarchy and the world’s central bankers, decided to take the power back which they did within the confines of the democratic process, sending the establishment reeling, by rejecting years of legacy narratives by replacing decades of a failed, and flawed, political regime in the US with something… different. And yet, looking back over the past 12 months, and in fact past decade, it remains to be seen if these changes will be successful and bear fruit, or if they will be a change for the worse.

However, amid this confusion, some clarity did emerge: as we look back at the past year, and past decade for that matter, the one thing that becomes clear amid the constant din of markets, of politics, of social upheaval and geopolitical strife, in fact a world that is so flooded with constant conflicting newsflow and changing storylines that some say it has become virtually impossible to even try to predict the future in a world bombarded with a relentless stream of flashing red headlines, that despite the people’s desire for change, for something original and untried, the world’s established forces will not allow it and will fight to preserve the broken status quo at any price, which is perhaps why it always boils down to one thing – capital markets, that bedrock of Western capitalism and the “modern way of life”, where control, even if it means central planning the likes of which have not been seen since the days of the USSR, and an upward trajectory must be preserved at all costs, as the alternative is a global, socio-economic collapse.

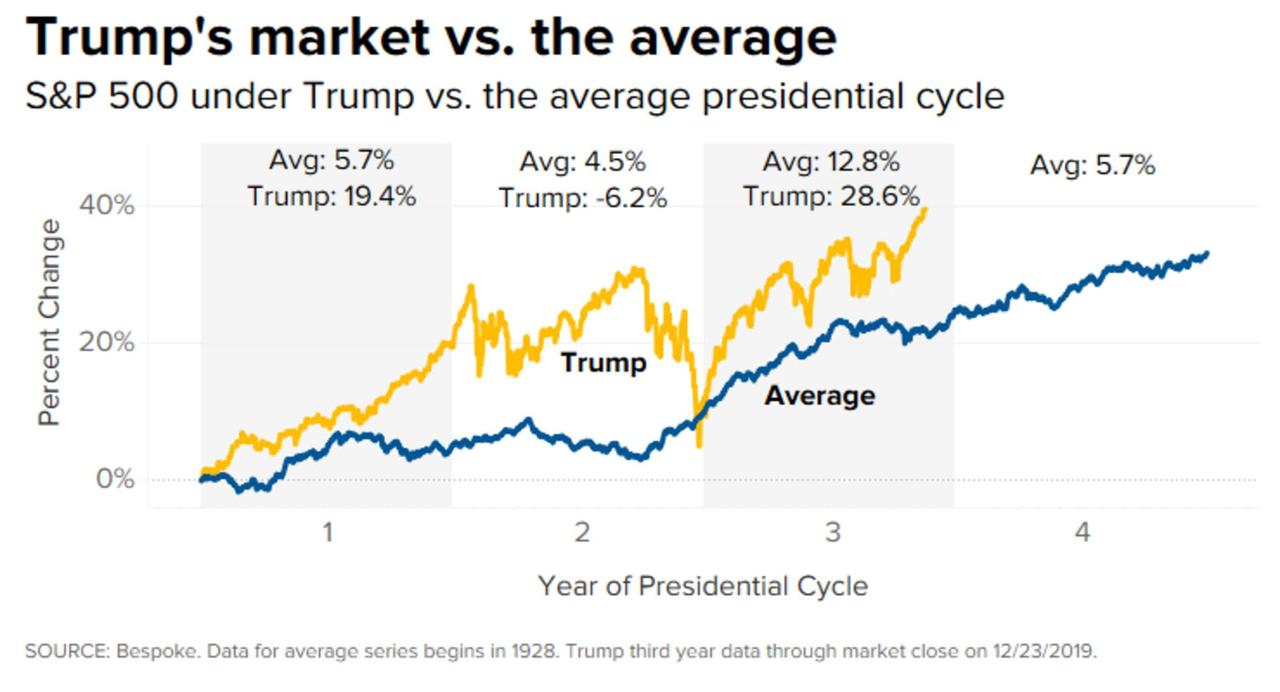

And since it is the daily gyrations of stocks that sway popular moods – and explains why none other than the US president is now tweeting almost daily on how the S&P closed on any given day to boost his approval rating and bolster his credibility – the interplay between capital markets and politics has never been more profound or more consequential. Indeed, in a historic moment when the president was impeached by the House (if not the Senate), Trump’s natural response was to point to the record high hit that very day in the S&P500. To be sure, so far Trump has been successful – although the correct word is lucky – in that the stock market cooperated in 2019 when it returned an impressive 28.50%, just shy of the best annual return in the past 22 years when it posted a slightly higher return in 2013. Indeed, the S&P has returned more than 50% since Trump was elected in 2016, more than double the 23% average market return of presidents three years into their term.

The more powerful message here is the implicit realization and admission by politicians, not just Trump but also his peers and challengers, that the stock market is now seen as the consummate barometer of one’s political achievements and approval. Which is also why capital markets are now, more than ever, a political tool whose purpose is no longer to distribute capital efficiently and discount the future, but to manipulate voter sentiments far more efficiently than any Russian election interference attempt ever could.

Which brings us back to 2019 and the past decade, which is best summarized by a recent Bill Blain article who said that “the last 10-years has been a story of massive central banking distortion to address the 2008 crisis. Now central banks face the consequences and are trapped. The distortion can’t go uncorrected indefinitely.“

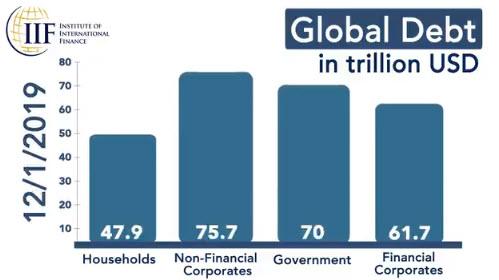

That, in a nutshell, is what every decade introspective boils down to (or should): we had a decade in which the excesses of the past were not only not corrected, but swept under the rug… and under a mountain of debt. Because the tradeoff of pulling years if not decades of growth from the future means that we ended 2019 with global debt of a record $255 trillion, up from $185.4 billion at the start of the decade, and a staggering 330% of global GDP, a level which not even the most liberal economists harbor any belief will have a happy ending.

And while helicopter money, or MMT, is likely the next and final stop for a world careening into the fiat money abyss, for now the music is playing and everyone must dance, to quote Chuck Prince.

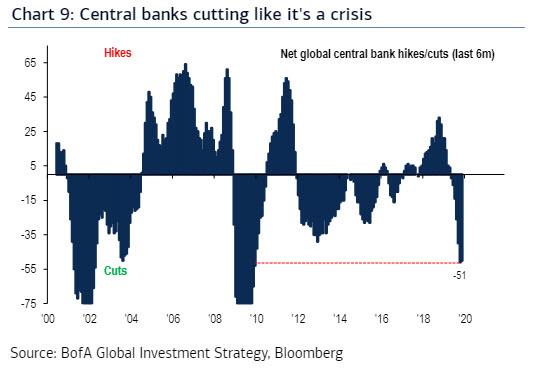

Which, in turn, brings us back to the point why 2019 tied a lot of loose ends: you see, in many ways the transition from 2018 to 2019 was a neat recapitulation of some of the core themes of the past decade. When the S&P briefly entered a bear market – one which literally lasted just a few seconds on Dec 24, 2018 – central banks threw in the towel on any attempt to renormalize monetary policy. As a result first the Fed, then all of its central bank peers, proceeded to ease massively in order to avoid a catastrophic market crash, one which would undo a decade of central bank interventions and the injections of over ten trillion in newly-created liquidity, and went all in on perpetuating a failed status quo. The best summary of this came from Bank of America which in a moment of striking honesty, said that “central banks are cutting like it’s a crisis” and indeed, the number of rates cuts into late 2019 matched those last seen during the 2008/2009 financial crisis when the global financial system was on the verge of collapse. And yet, this time the global economy was growing at a solid, if not stellar pace (or so we were told), there was no imminent crisis on the horizon with global stocks already trading near all time highs.

Amusingly, it was in our year-end recap from last year published exactly one year ago when we said that “the question we have: how far will the tide be allowed to recede before central banks step in again.” We now know the answer: it was just a few months.

What happened? Simple – in late 2018 central banks panicked that they had lost control – and credibility – and they not only reversed all their “renormalization” success, with the Fed going from predicting two rate hikes in Dec 2018 to cutting three time in the summer of 2019, while also launching QE4 (under the pretext of fixing a repo system which was brought to its knees by none other than JPMorgan, which just happens would benefit greatly from a new round of QE), even as the ECB both cut rates deeper into negative territory as it also restarted its own QE less than a year after it ended it.

One explanation for this “crisis” response: China, which over the early part of the past decade had emerged as the world’s emergency economic kickstarter, has by now accumulated too much debt to provide the spark needed to reflate the global economy, and drowning under a mountain of (increasingly bad) debt, Beijing was relegated to the economic sidelines unable to trigger another massive debt injection into the domestic economy already suffering from record debt defaults and bank failures, and forcing the Fed and other central banks to take its place. Ironically, the Fed did so even though as former NY Fed president (and ex-Goldman Sachs economist) Bill Dudley admitted in an scandalous op-ed in August, that the Fed could effectively crash the market to secure a recession and prevent a Trump re-election, and it should think hard and deep if it shouldn’t do just that. In the end, however, Powell – who had emerged as the target of Trump’s angry tweets about the market and economy, sparking debate whether Trump would tell him “You’re fired” next – picked kicking the can, even it meant 4 more years of Trump.

And so, with the Fed fully behind Trump and helping the S&P return nearly 30% in 2019, 4 more years of Trump is now virtually assured (barring some unexpected calamity in 2020) because while Nancy Pelosi’ crusade to impeach the president ended up being a massive dud, one which has backfired spectacularly with Trump only benefiting from even more moderate support as a result ahead of an inevitable acquittal in the Senate, it was the impressive market performance and resilient economy that won Trump the 2020 re-election one year before the vote even took place. And no, the outcome of the 2020 presidential election has nothing to do with the motley crew of Democratic presidential candidates, ranging from ultra-billionaires to raging socialists who literally are pushing for helicopter money and MMT, or the endless noise that was the “made for popular consumption and flashing red headlines” trade war spectacle between the US and China that bored traders for over 560 days (as the two sides had long ago agreed on the “trade war’s” amicable resolution behind closed doors). So for all those Democrats tearing their hair out why Trump is an odds-on favorite to win next year’s presidential election, the answer is simple: the Fed, and the Fed’s realization that it must capitulate on its renormalization ambitions if it wishes to preserve the artificial levitation of US and global capital markets.

In other words, going back to what we said above, 2019 helped crystalize the realization that politics is now markets, and markets have become political weapons, and why the past decade was, as Bill Blain put it, “a story of massive central banking distortion to address the 2008 crisis.” The problem is that this distortion has only made the mess even greater, and the only hope central banks have – in their own words – is if government fiscal stimulus takes over where monetary stimulus ends. Only there is just one problem, or rather 255 trillion problems as shown above, because whereas one could argue that fiscal stimulus is a credible option if the world’s wasn’t drowning in debt, when global debt to GDP is 330%, it is tantamount to saying that only more debt can fix a debt crisis. Which is effectively what the world’s smartest people are saying.

That said, whether the story of 2020, and the next decade for that matter, is one of fiscal or monetary stimulus is of secondary importance: what is key, and what we learned in the past decade, is that the status quo will throw anything at the problem to kick the can. And while many already knew that, the events of 2019 made it clear to a fault that not even a modest market correction can be tolerated going forward. That in turn may explain why the last quarter of 2019 was a mirror image of events from the fourth quarter of 2018. After all, if central banks aim to punish all selling, then the logical outcome is to buy everything, and investors, traders and speculators did just that armed with the clearest backstop guarantee from the Fed in the form of both rate cuts and QE 4.

Meanwhile, for all those lamenting that relentless coverage of politics in a financial blog (which sadly also includes every tweet from Donald Trump), why finance appears to have taken a secondary role, and why the political “narrative” has taken a dominant role for financial analysts, the past year showed vividly why that is the case.

Ironically, if there was one event in 2019 that threatened the status quo, it had nothing to do with capital markets, Trump, the Fed’s balance sheet, or the repo market, and everything to do with the repeat arrest of Jeffrey Epstein. Having been unexpectedly arrested for the second time for his involvement in a giant child prostitution ring, one which threatened to take down some of the world’s most powerful people, Epstein’s incarceration proved extremely uncomfortable to those same people… and then Epstein simply “committed suicide” despite constant surveillance. And just like that the risk that he may name names disappeared forever.

What about China? After all when looking ahead last year, we said that “another assumption that will be tested in the coming year is whether “China no longer matters” for US markets, something which was certainly not the case in 2018.” We added that we “have a nagging suspicion that whether or not the US manages to avoid a recession in 2019 any global shock will ultimately come out of Beijing, regardless of whether Trump and Xi manage to find a common language and put the trade war between the two nations aside.” The answer is that despite much speculation that 2019 would be the year that China’s economic and financial bubble (at $40 trillion, the country’s financial system is double that of the US) finally bursts, Beijing managed to once again avoid a hard landing. Ironically, it did so on the back of the trade war with Trump, which provided Xi Jinping with just the right amount of scapegoating on which to blame not only China’s economic slowdown, but the complete failure of its credit impulse to rebound from cycle lows, and the sharp spike in both bank failures and record corporate defaults. After all, who will pay much attention to the underlying Chinese economy is Beijing can blame the US trade war for all its ills? And that’s precisely what happened in 2019, a year when China blamed Trump for all its woes, even if in reality China’s slowdown started years ago, and will only accelerate in the coming year, especially if much of the “trade war” is now resolved.

Ironically, as China’s Xi Jinping blamed trade war with Trump for its slowdown, Trump in turn used the buoyant US economy and record US stock market to redirect public attention from the 3-year long attempt by democrats to overthrow the sitting US president. As a reminder, 2019 was the year when the Mueller probe into Trump “collusion” with Russia crashed and burned to the chagrin of much of the liberal “fake news” propaganda; however, just months later the narrative was reborn when a “whistleblower” triggered in a carefully staged script which saw Trump become only the third US president to be impeached by the House over what Democrats claimed was an illegal attempt to force Ukraine to “interfere with US democracy.” The end result was twofold: the House, where Democrats have had a majority since the midterm elections, impeached Trump and… the nation yawned, realizing that the GOP-controlled Senate would nullify the impeachment especially since the Democrats failed in their primary mission: to convince moderate voters that Trump indeed deserves to be thrown out.

And yet, with the 2020 elections looming, it is certainly true that anything can still happen, only as with all true “black swans”, it won’t be what anyone had expected. And so while many themes, both in the political and financial realm, did get some closure, dramatic changes in 2019 persisted, and will continue to manifest themselves in dramatic, often violent and unexpected ways – from the unprecedented obsession with everything Trump does, says and tweets, to “populist” upheavals in Europe and around the developed world, to China’s fight with soaring food inflation in a time when the central bank desperately needs to ease financial conditions.

As always, we thank all of our readers for making this website – which has never seen one dollar of outside funding (and despite amusing recurring allegations, has certainly never seen a ruble from the KGB either, although now that the entire Russian hysteria episode is over, those allegations have finally quieted down), and has never spent one dollar on marketing – a small (or not so small) part of your daily routine. Which also brings us to another amusing topic: that of fake news, and something we – and others who do not comply with the established narrative – have been accused of. While we find the narrative of fake news laughable, after all every single article in this website is backed by facts and links to outside sources, we find it a dangerous development, and a very slippery slope that the entire developed world – is pushing for what is, when stripped of fancy jargon, internet censorship under the guise of protecting the average person from “dangerous, fake information.”

To preserve its counter-establishment aura, it goes without saying that the current administration should overturn this blatant attack on the First Amendment, and let people decide for themselves what is and isn’t fake news. If anything, it is the conventional, mainstream media, most of which is owned by a handful of corporations with extensive ties to the government, that demonstrated on many occasions not only in 2019 but in the past decade that it is the primary creator and distributor of “fake news”, something which has not escaped the broader US population the majority of which no longer trust conventional news media.

In addition to the other themes noted above, we expect the crackdown on free speech to accelerate in the coming year, especially as the following list of Top 20 articles for 2019 reveals, many of the most popular articles in the past year were precisely those which the conventional media would not touch out of fear of repercussions, which in turn allowed the alternative media to continue to flourish in an orchestrated information vacuum and take significant market share from the established outlets by covering topics which the public relations arm of established media outlets refused to do, in the process earnings itself the derogatory “fake news” condemnation.

We are grateful that our readers – who hit a new record high in 2019 – have realized it is incumbent upon them to decide what is, and isn’t “fake news.”

* * *

And so, before we get into the details of what has now become an annual tradition for the last day of the year, those who wish to jog down memory lane, can refresh our most popular articles for every year during our no longer that brief, almost 11-year existence, starting with 2009 and continuing with 2010, 2011, 2012, 2013, 2014, 2015, 2016, 2017 and 2018.

So without further ado, here are the articles that you, our readers, found to be the most engaging, interesting and popular based on the number of hits, during the past year.

In 20th spot, with just over 400,000 reads, was a question or rather “7 Unanswered Questions About Epstein’s Death That The Mainstream Media Is Not Talking About“ and for good reason: with few media outlets daring to touch the “Jeffrey Epstein” topic when he was alive, it only emerged after his death that at least one major network, ABC News, spiked a piece on Epstein’s potential ties with the top echelons of American power. As TV anchor Amy Robach was heard saying on a hot mic, “Do I think he(Epstein) was killed? 100% I do…He made his whole living blackmailing people. There were a lot of men on those planes. A lot of men who visited that island. A lot of powerful men who came into that apartment.” The spiking of the Epstein story came around the time it emerged that NBC deliberately suppressed evidence that Michael Avenatti lied about Brett Kavanaugh and fabricated a false accusation against him. In light of so many attempts by America’s mainstream press to keep the population in the dark, is it any wonder that trust in media institutions has collapsed and that Americans increasingly seek out alternative venues of information?

In 19th spot of the year’s most popular articles, we received another vivid reminder that in US society a handful continue to be “much more equal” than everyone else, and the only thing that really matter is the size of one’s bank account. Over 401,000 readers were shocked to learn that “Feds Arrest Dozens, Including Actresses and Ex-Pimco CEO, In “Largest College Admissions Scam Ever Prosecuted. ” While most Americans’ children had to fight tooth and nail, study countless hours and dedicate even more time to extracurricular and charitable activities to get into the college of their choosing, the kids of a more than a handful of rich Hollywood parents and financial oligarchs had found a short cut – their parents paying bribes to fast track their admission into top universities across the land. And yet, even here the elite remained “more equal” – while a handful of prison sentences have been handed down, the longest one so far was a mere 6 months, with most parents getting a few token days in jail or some community service. It remains to be seen if college bribery has been snuffed out, although if that is the full extent of the deterrence we seriously doubt it.

in 18th spot, with nearly 403,000 reads, was our report on the Fed’s emergency response to what some had predicted would be a year-end repo market crisis. Just days after Credit Suisse and former NY Fed repo guru, Zoltan Pozsar predicted that the Fed would be forced to unleash hundreds of billions in liquidity in the form of QE4 to avoid a lock up of the repo market following the September repo market fireworks which briefly saw the overnight repo rate soar as high as 10%, the Fed did just that, only instead of launching QE4, the US central bank unveiled that it would backstop up to $500 billion in liquidity in the one month period following mid-December to prevent another repo market crisis as we explained in “Massive… Huge… Largest Ever”: Fed Will Flood Market With Gargantuan $500 Billion In Liquidity To Avoid Year-End Repo Crisis.” The result was a remarkable surge in the Fed’s balance sheet which soared by $400 billion since its late August nadir, in the process unleashing an unprecedented year-end stock market meltup which helped send stocks soaring to new all time highs just in time for the 2019 holidays which in turn translated into record online spending as US consumers were delighted to see the value of their brokerage accounts and 401(k)s hit all time highs. The question now is whether – and if – the Fed will be able to drain all of this freshly created liquidity as we enter the new year.

In 17th spot was a bizarre twist in what was part of the biggest political scandal of 2019 – Trump’s impeachment – which was started after second-hand “whistleblower” accused Trump of threatening to withhold funding to Ukraine unless former VP Joe Biden, and Trump’s current democratic challenger for the 2020 elections, was investigated for corruption. And while by now the identity of the “secret” whistleblower, who appears to have been an ideologically biased, never-Trump CIA officer, is known 405,000 readers were surprised to read that he had gotten cold feet about testifying after revelations emerged that he worked with Joe Biden, former CIA Director John Brennan, and a DNC operative who sought dirt on President Trump from officials in Ukraine’s former government. In the end, Trump was impeached in the House, although with impeachment in the Senate impossible and with moderate voters increasingly appalled by Nancy Pelosi’s tactics, it appears that this gambit backfired dramatically for the Dems.

We were not the only one surprised to receive an email from a Fed staffer in August seeking more information on an article we had written which not only predicted the September repo fireworks, but also explaining why the Fed would soon be forced to launch QE: over 408,000 readers agreed with us that “When You Get An Email Like This From The Fed, It May Be Time To Panic.” As we wrote in the article, which came out a full month before the Sept 11 repo crisis and two months before the Fed’s restart of QE, “based on the Fed’s email, we wonder if it means the Fed is now seriously contemplating [QE4], and if so, does the market crash first, or is it about to price in QE4 and soar. We expect to find out very soon.” We did: one month later the repo market tanked, sparking a mini stock market swoon, which immediately gave way to a massive liquidity injection by the Fed, and as stocks priced in QE4, they indeed soared. incidentally, as we also predicted earlier in August, the Fed indeed launched QE4 in early October. The rest is record stock market history.

In 15th spot, and going back to the propaganda front that is US mainstream “media”, we quoted a CBS News reported who said “I’m Committing Professional Suicide” after admitting that “Mostly Liberal” Journalists Are Now “Political Activists.” Nearly 420,000 readers heard CBS reporter Laura Logan admitting that “the media everywhere is mostly liberal, not just the U.S.,” adding that it was nearly impossible for viewers to decipher if they were being told the truth at any given time. She also admitted that journalists today are more or less lobbyists for liberal interests, adding that the weight of the liberal media machine overwhelms “the other side” unless people actively seek outlets such as Breitbart. With more and more lies emerging from the mainstream, it is hardly a surprise that that’s precisely what people are doing.

Shifting back from media to central banks, the 14th most read article of the year involved a stunning warning by the Dutch Central Bank whose Freudian slip that “if the system collapses, the gold stock can serve as a basis to build it up again” amazed nearly 430,000 people. In additional to admitting that systemic collapse is not only possible, it may be just a matter of time, the bank also added that “gold bolsters confidence in the stability of the central bank’s balance sheet and creates a sense of security.” The bank’s admission that “a bar of gold retains its value, even in times of crisis. This makes it the opposite of “shares, bonds and other securities” all of which have inherent risk and prices can go down” sounded like the pitch from a gold ad which is why it was especially surreal and prompted question if there is more to the wholesale gold repatriation among European nations than meets the eye.

From central bank printers of money, to printing money with the world’s oldest profession, in 13th spot and seen by over 443,000 readers was our question “Why Are So Many Top-Tier College Girls Turning To ‘Soft Prostitution‘?” The question, in retrospect, was rhetorical and undoubtedly linked to the country’s $1.5 trillion student debt problem. Still, it poses some unpleasant social questions if 15,277 female students at Georgia State, nearly one in ten girls at the college, were willing to whore themselves out to websites such as Sugar Babies.com in order to make ends meet.

And from prostitution to pedophilia, in 12th spot we go back to Jeffrey Epstein, whose death left far too many questions unanswered. Which is why the emergence of his ‘tapes’ was a matter of great public interest and why over 443,000 readers tuned in to listen to the “Epstein Tapes: Dead Pedophile Describes His Lifestyle In Unearthed Recordings.” The tapes, the remnant of an Epstein 2003 interview, offered his thoughts on subjects ranging from mathematics, to exorbitant wealth, to the important of prenuptial agreements. Alas, there was no hint who may have “suicided” Epstein himself some 16 years later. More importantly, this was most likely the last time we’ll ever hear from Epstein, as dead pedophiles tell no tales.

In 11th spot, 445,000 readers got a vivid reminder that the “science” behind global warming can be as “scientific” as the propaganda behind mainstream media. As we reported in “Glacier National Park Quietly Removes Its “Gone By 2020” Signs“, officials at Glacier National Park had begun quietly removing and altering signs and government literature which told visitors that the Park’s glaciers were all expected to disappear by either 2020 or 2030. Why? Because GNP’s most famous glaciers such as the Grinnell Glacier and the Jackson Glacier have been growing – not shrinking – since about 2010. Of course, don’t ever let facts stand in the way of good propaganda narrative, something which 16-year-old anti-global warming crusader Greta Thunberg and her fame and limelight hungry parents discovered at roughly the same time.

When it comes to politics, 2019 wasn’t just about the collapse of the Russia collusion narrative in the first half of the year, and Trump’s impeachment in the second: the “other” big story throughout the year was the (seemingly endless) field of Democratic presidential candidates, yet where one name was missing: that of Hillary Clinton. Which is why in September we asked “Is Hillary Gearing Up For Late-Stage Do-Over Against “Corrupt Human Tornado” Trump?” in which we cited bookies’ bets and a few recent actions, which sparked fresh speculation that Hillary Clinton may be about to enter the Democratic Party presidential nominee race. So far such speculation has not materialized, although just like Mike Bloomberg, Hillary may merely be waiting for her competition to tear itself apart before she makes her glorious entrance, culminating with a repeat of the 2016 presidential election.

And from politics back to capital markets, where as more than 475,000 people learned there was no more market moving report than the one published on December 9 by Credit Suisse repo guru Zoltan Pozsar, titled “Countdown to QE4”, in which the former Fed and Treasury staffer predicted that “It’s About To Get Very Bad”, and that the Fed would lose control of the repo market into year end due to a massive liquidity shortage resulting in an imminent market crash, and only another massive liquidity injection in the form of QE4 could prevent a crisis. In the end, the Fed did not launch QE4 – after all it had already started QE4 back in October (the expansion from T-Bills to coupons will happen some time in early to mid-2020), however the Fed’s massive, $500 billion year-end liquidity injection and backstop would almost certainly not have happened without the Pozsar report sparking a mini panic within the Fed. As such while Pozsar did not correctly predict the Fed’s reaction, his lucid explanation of the faults within the repo system prevented what could have been a dire year-end crisis (which we assume earned the Hungarian a Christmas Card from the Trump administration).

It may come as a surprise to some that Central banks are not only in the market rescuing and money printing business: they are now active agents when it comes to fighting climate change. And since the past decade has demonstrated that any gospel accepted by central banks as fact is almost certainly a lie, we were not shocked to learn, although it did comes as a surprise to over 530,000 readers that in a “Bombshell Claim: Scientists Find “Man-made Climate Change Doesn’t Exist In Practice. ” The study, which resulted in our 8th most popular article of 2019, and which has yet to be featured by any mainstream media, has crippled flawed fundamental assumptions underlying controversial climate legislation after scientists in Finland found “practically no man-made climate change” after a series of studies. “During the last hundred years the temperature increased about 0.1°C because of carbon dioxide. The human contribution was about 0.01°C”, the Finnish researchers bluntly state in one among a series of papers. Or, as Greta Thunberg would say, “how dare they.”

In 7th spot, with over 540,000 reads, was the surprise news that bizarrely, and for no reason at all, in mid-March Facebook decided to ban Zero Hedge. In some ways we were lucky: unlike other websites, only a tiny fraction of our inbound traffic originates at Facebook, with most of our readers arriving here directly without the aid of search engines or referrals. And while after several days of vocal complaints by our readers about the ban, Facebook reversed the ban, we are confident it is only a matter of time before Facebook – and other social media sites – bans a “conspiracy theory” site like Zero Hedge for good. Which reminds us that it is time to start thinking of Plan B.

In 6th spot, with over 575,000 views was a reminder that even as the US economy continues to grow, for millions of student-debt borrowers life remains unbearable. And so, as we wrote in “Debt-Laden Americans Flee Country To Escape Crushing Student Loans “, faced with crushing student loans and little ability to repay them, some Americans have taken to fleeing the country in order to escape their debt. “It’s kind of like, if a tree falls in the woods and no one hears it, does it really exist?” said 29-year-old Chad Haag, a millennial who – like millions of his peers – is about to find out the hard way that one can’t just pick up and disappear from his problems.

In 5th spot was a surprising report from the Rand corporation, according to which the US better not escalate its trade war with China into something more “kinetic.” 687,000 readers learned that during simulated World War III scenarios, the U.S. lost against both Russia and China: “In our games, when we fight Russia and China, blue gets its ass handed to it.” Of course, the report had a simple, ulterior motive: to boost the defense budget with more taxpayer money: “$24 billion a year for the next five years would be a good expenditure” to prepare the military for World War III.

Over 708,000 people tuned in, shocked to learn in August that despite being placed in a maximum security holding cell, and having been on suicide watch, pedophile millionaire Jeffrey Epstein managed to kill himself by chocking himself with a bed cover. Of course, nobody believed it, which is why “Outrage Surged Over Epstein’s Mysterious Suicide. ” Alas, with the video camera recording Epstein mysteriously broken, and with a lengthy probe into the guards who were supposed to keep Epstein safe only just beginning, the likely outcome is that one that Epstein’s killer wanted: to shut the pedophile with the massive rolodex for good.

Something odd happened on June 2: for a few minutes that dayGoogle Cloud went offline, an outage which adversely affected Gmail, YouTube, SnapChat, Instagram, and Facebook. And while over 812,000 people wondered alongside us if “the Government Just Test The Internet Kill Switch”, making this the 3rd most popular post of the year, even a more innocuous explanation left many questions unanswered, namely if just one cloud service going offline can cripple the key nodes of the modern internet, what will happen during the next major cyberattack on US soil, and will US economic productivity finally jump at that moment?

Not one year passes without Deutsche Bank somehow making its way into the Top 20 article, and 2019 was no exception. Over 1.1 million readers tuned in to ask and debate whether “A Bank With $49 Trillion In Derivatives Exposure Is Melting Down Before Our Eyes.” One look at Deutsche Bank’s stock price and the answer becomes self-evident.

Finally, in what was a surprise to us, the most read post of the year with 1.4 million hits, had nothing to do with capital markets, with politics, or with the latest failed CIA coup in some middle-eastern nation. Instead, it was a report exposing the hypocrisy of those “greens” who buy electric cars to virtue signal, yet are unaware that doing so results in far worse environment consequences as we wrote in “Electric Car-Owners Shocked: New Study Confirms EVs Considerably Worse For Climate Than Diesel Cars.” We can only hope that our conclusion that “maybe Elon Musk’s plan to save the world with electric cars is the biggest scam of our lifetime” will prompt at least one or two readers to think again before splurging on that brand new Model S.

* * *

With all that behind us, and as we wave goodbye to another bizarre if exciting yet and a truly surreal decade, what lies in store for 2020, and the next decade?

We don’t know: as frequent and not so frequent readers are aware, we do not pretend to be able to predict the future and we don’t try despite endless allegations that we constantly predict the collapse of civilization: we leave the predicting to the “smartest people in the room” who year after year have been consistently wrong about everything, and never more so than in the last three years, which destroyed the reputation of central banks, of economists, of conventional media and the professional “polling” and “strategist” class forever. We merely observe, try to find what is unexpected, entertaining, amusing, surprising or grotesque in an increasingly bizarre, sad, and increasingly crazy world, and then just write about it.

We do know, however, that after $16 trillion in liquidity has been conjured out of thin air by the world’s central banks, as QE makes a triumphal return to both the US and Eurozone, and as interest rates are once again sliding to unprecedented lows, the entire world is floating on an ocean of excess money, which in 2019 once again succeeded in masking just how ugly the truth beneath the calm surface is.

We are confident, however, that in the end it will be the very final backstoppers of the status quo regime, the central banking emperors of the New Normal, who will eventually be revealed as fully naked. When that happens and what happens after is anyone’s guess. But, as we have promised – and delivered – every year for the past ten, we will be there to document every aspect of it.

Finally, and as always, we wish all our readers the best of luck in 2020, with much success in trading and every other avenue of life. We bid farewell to 2019 with our traditional and unwavering year-end promise: Zero Hedge will be there each and every day – usually with a cynical smile – helping readers expose, unravel and comprehend the fallacy, fiction, fraud and farce that the system is reduced to (ab)using each and every day just to keep the grand tragicomedy going for at least one more year.

Watch: Apache Gunships Attempt To Disperse Mob As Kataib Hezbollah Flags Erected Over Embassy Walls

Dramatic footage over the US embassy in Baghdad as enraged protesters continue to encircle the compound with US Marines still inside, and reportedly with more Marines on the way from nearby Kuwait:

VIDEO: AH-64 Apaches protect @USEmbBaghdad. 🚁“We have taken appropriate force protection actions to ensure the safety of American citizens…and to ensure our right of self-defense. We are sending additional forces to support our personnel at the Embassy.”~@EsperDoD 🇺🇸🇮🇶 pic.twitter.com/amABHBAOcL

— OIR Spokesman Col. Myles B. Caggins III (@OIRSpox) December 31, 2019

The Pentagon announced that a pair of AH-64s Apache helicopters would be used to attempt to disrupt and disperse protests. The US coalition in Iraq spokesman released video of low flying Apaches making aggressive maneuvers and releasing flares on the crowds below.

“We have taken appropriate force protection actions to ensure the safety of American citizens… and to ensure our right of self-defense. We are sending additional forces to support our personnel at the Embassy,” Col. Myles B. Caggins said in an official statement.

This was hours after the Pentagon announced the US will send additional troops to Baghdad specifically to protect the US Embassy in Iraq. According to the statements this is to include about 100 Marines sent from nearby Kuwait. According to one defense official cited by Bloomberg, the Marines will likely fly to the embassy area in V-22 Ospreys.

But the tactics don’t appear to be working given the mob has set the embassy compound walls on fire, including the main gate and security pass through reception area.

Crucially, in a stunning image sure to send shockwaves through the US administration, multiple Kataib Hezbollah flags have now been erected along the walls of the US embassy.

Likely the Apaches will continue encircling the area through the night as things look to get worse before they get better.

All of this portends that the potential for even greater escalation and confrontation is in the air as Trump continues to call on Iranian proxies to leave Iraq.

As the new year comes around, it’s a perfect time to look at what legacies we leave behind us. What glories of the past year can we proudly point out to friends and family? What milestones in our journey can we single out and say “that’s what got me here”? Here we present a few of the more prominent milestones and markers of the political left on their own journey of discovery through 2019.

I’ve Got The (White) Power

Did you know that if you flash the OK finger gesture, you are really asking, “Where’s the nearest Klan meeting?” Yep. Anytime someone gives you the OK sign that person is conveying to you a clandestine message that you belong to a brotherhood of white supremacy culture. Well, at least that is the paranoia emanating from the Anti-Defamation League (ADL), which updated its list of hate symbols. What was a seemingly innocuous gesture that dates back to 18th-century Britain has now metastasized into a symbol that has leftists clutching their pearls and searching for the nearest hate crime officer to file a complaint of racism.

What’s next? A childhood game that will now be condemned as perpetuating white power? Oh, wait…

Kids These Days

Do you remember the Circle Game from when you were a kid? You make a circle with your fingers and place it below your waist. You must convince another person to look at the shape. If he or she does, then that individual gets a punch to the shoulder. Unfortunately, the fun police are not amused, and now anyone who participates in this game shall be punished for life because it is a calling card for the Ku Klux Klan.

Case in point, a few West Point Cadets and U.S. Naval Academy midshipmen flashed the upside-down OK finger gesture during a live broadcast of the Army-Navy football game. Years ago, reasonable people would have viewed it as a bunch of young people having fun. But the population of reasonable folks is diminishing, so, of course, the Circle Game now requires investigations to satisfy the perpetually perturbed. Naval Academy and West Point announced that they will be probing the matter.

Sigh…

Honoring ISIS And Insulting MAGA Kids

There they go again. The left-leaning mainstream media’s blatant bias was exposed by fake news and story suppression. It was another ugly year for the fourth estate.

The media seemingly honored the killed ISIS leader, Abu Bakr al-Baghdadi, as an “austere religious scholar” and attempted to diminish the successful mission because Trump was president at the time. An agenda-driven press attacked a bunch of white Catholic high schoolers for allegedly blocking the path of a Native American, which turned out to be fake news. It was learned that ABC News stopped a story involving Jeffrey Epstein because the network feared it would no longer land interviews with Will and Kate. A legacy media delivering their news on President Donald Trump with a 90% negative slant.

It was a typical year for an industry that is losing trust of the people.

Drag Queens Twerk And Strip

One of the oddest fads forming across North America is something called Drag Queen Storytime. This involves men dressed in women’s clothing – oftentimes the frightening attire will trigger nightmares – reading children’s stories at public libraries. Over the last 12 months, some footage has been released showing that they really are not reading classic Dr. Seuss tales or Peter Rabbit books.

Instead, these drag queens are twerking and performing stripteases in front of pre-schoolers. The key question that should be asked is: Where the heck is the police and why is nobody getting arrested?

Go Back Where You Came From

Hate hoaxes were prevalent in 2019. Actor Jussie Smollett claimed that a couple of white guys attacked him on a bitterly cold Chicago evening by tossing a noose around his neck and declaring that this is MAGA country. The story seemed implausible from the very beginning. Firstly, it was unlikely that any residents of MAGA country even know who Smollett is. The second is an obvious question: Who carries a noose around with them at 1 a.m.?

Erica Thomas, a Georgia lawmaker, accused a man at a supermarket of telling her to “go back where you come from.” The incident occurred after she went to the express checkout lane and had several more items than what was accepted. She captured national attention and the narrative was that white people are racists and President Trump is inciting these acts. Well, the whole thing turned out to be a hoax and Thomas, who had initially cried in front of the cameras, then pivoted by telling a reporter:

“I don’t know if he said ‘go back,’ or those types of words… I don’t know if he said ‘go back to your country’ or ‘go back to where you came from,’ but he was making those types of references is what I remember.”

These were the most prominent cases of hate hoaxes, but they were common throughout 2019, committed mostly by people with an agenda. Ostensibly, universities have turned into “hate-crime hoax mills,” writes the City Journal. Yet the mainstream media continue to believe the boy who cried wolf without any skepticism or additional reporting. Shame.

A Hostile Climate

You could say that 2019 has been the year of climate action. Thanks to some random Swedish teenager who was propelled to the spotlight because of the mainstream media, protests have been held all over the world to demand the government confiscate a greater share of our money and regulate our lives even more. One of the more common types of demonstration involves professional activists taking to the streets and blocking traffic. This results in motorists not only being late to work but also their cars are sitting idly by emitting pollutants into the air. The irony seems to be lost on the climate activists.

That’s gold, Jerry. Gold!

Left Cannot Find Salvation

For more than 150 years, the Salvation Army has been one of the greatest organizations on the planet for operating shelters to help the homeless, delivering humanitarian assistance to developing countries, and providing disaster relief to the people impacted by severe weather events. The organization does a lot of good for local communities and impoverished nations. What should be a celebrated institution is now a target for the left. Why? They have just learned it is a religious institution.

Facing pressure from left-wing mobs over its donations to what they call anti-LGBTTQQIAAP initiatives, Chick-fil-A announced that it would no longer be contributing to Christian non-profit groups, including the Salvation Army. The left is so militaristic and hellbent on forcing everyone to cave to their whims that they want to slash funding for a charity.

It is similar to the left protesting the Koch brothers’ $100 million gift for a new wing at New York-Presbyterian Hospital in 2014.

Blame Russia!

On the left, it is all Russia, all the time. Anytime something does not go according to plan, the left will immediately blame Russia. Don’t believe it?

When Prime Minister Boris Johnson and the Conservatives enjoyed a resounding electoral victory in the U.K., it was somehow the fault of Moscow. Because Representative Tulsi Gabbard (D-HI) voted “present” on articles of impeachment, it was evidence she is a puppet for Russia. Alberta wanting to secede from Canada? Russia. President Donald Trump slapping new sanctions on Moscow? Russia. Oh, wait. Never mind. Scratch that one from the record!

This paranoia would make Joseph McCarthy’s face turn red. Wait a minute. Red? As in the red scare? Was a secret code just transmitted to President Vladimir Putin? Putin asset confirmed!

An Antifa Embarrassment

And then there was Antifa. This group never ceases to amaze any person who has little gray cells. All year long, Antifa has spent its time destroying property, attacking individuals from all walks of life, and proving that its foot soldiers do not possess much of a vocabulary. They injured journalist Andy Ngo so badly that he suffered a brain hemorrhage.

They bullied and intimidated an elderly lady because she wanted to attend a Maxime Bernier event in Hamilton, ON. They attacked a senior citizen in his car in Portland, OR. And, about as predictable as the sun rising in the east and setting in the west, they prevented invited guests from speaking on college campuses.

Making A Hard Left In 2020

As Arthur Fleck from Joker said, “Is it just me or are things getting crazier out there?”

Over the years, we have witnessed the left howl at the sky, perform odd dances to fight climate change, and mirror the behavior of a crazy man on a street corner predicting the end of days in 12 years (or is it 10 now?). The left has ostensibly veered further to the cusp of insanity, incrementally extinguishing the last vestiges of sensibility. There are many theories as to what triggered this descent into madness, such as college indoctrination and mainstream media programming. All we know is that the left is now actively fighting against their rights. What the heck is happening? We might be living in some toxic concoction of Brave New World, Nineteen Eighty-Four, Metamorphosis, and The Trial.

‘Smart Camera’ Data Leak Exposes Personal Data Of 2.4 Million Users

A massive data leak by smart home device manufacturer Wyze revealed the personal details of 2.4 million users for over three weeks, according to the Daily Mail, citing the December 26 discovery by consulting firm Twelve Security. The find was confirmed by video surveillance authority IVPM.

Wyze, based in Seattle, was founded by former Amazon employees. The company produces inexpensive smart cameras, light bulbs, plugs and security devices.

Compromised data includes usernames, email addresses, Alexa tokens, and information specific to people’s wireless home networks.

Also exposed (albeit for just 140 users) were health stats – including weight, height and gender for the company’s upcoming smart scale product.

“We are confirming that some Wyze user data was not properly secured and left exposed from December 4th to December 26th,” wrote Wyze co-founder and chief product officer Dongsheng Song in a December 27 forum post.

“We copied some data from our main production servers and put it into a more flexible database that is easier to query. This new data table was protected when it was originally created,” he added. “‘However, a mistake was made by a Wyze employee on December 4th when they were using this database and the previous security protocols for this data were removed.”

“We are still looking into this event to figure out why and how this happened.”

According to Wyze, the compromised information did not include any passwords, nor personal financial data, physical addresses or ‘government-regulated’ personal information.

Mr Song denied Twelve Security’s report that the compromised information included the bone density and daily protein intakes of the smart scale testers — and the claim that Wyze was sending user data to the Alibaba Cloud in China.

He also refuted the allegation that the firm had experienced a similar data breach earlier this year.

‘We’ve often heard people say, “You pay for what you get,” assuming Wyze products are less secure because they are less expensive. This is not true,’ Mr Song added. –Daily Mail

“We’ve always taken security very seriously, and we’re devastated that we let our users down like this,” said Song.

The company has secured the exposed database and forced users to reset their account passwords, along with their Alexa and/or Google assistant connections.

Climate alarmists think they are always right, and when they aren’t… they just move the goalposts ahead 10 years. Our friend Willis Eschenbach calls it “serial doomcasting“.

Some perspective:

“What historians will definitely wonder about in future centuries is how deeply flawed logic, obscured by shrewd and unrelenting propaganda, actually enabled a coalition of powerful special interests to convince nearly everyone in the world that CO2 from human industry was a dangerous, planet-destroying toxin.

It will be remembered as the greatest mass delusion in the history of the world – that CO2, the life of plants, was considered for a time to be a deadly poison.” ~ Richard Lindzen

What follows are climate predictions forecast to come true during the 2010s – one for each year.

A few timely missed predictions for 2020 are also added as a bonus feature.

Trump Encourages Iraqi “Freedom” Uprising Against Iran; Esper Sends More Troops To Embassy

President Trump just called for a mass “freedom” uprising not in Iran, but in Iraq of all places, at a moment the US embassy in Baghdad continues to be encircled by enraged protesters bent on expelling the Americans after US airstrikes killed dozens of Iran-backed Iraqi militia over the weekend.

Trump’s provocative tweet, coming after an hours long embassy standoff that has reportedly trapped the Marine guard inside, anxiously awaiting a defusing of the tense situation, further implies that it is ultimately Iran that’s running the show inside Iraq. He blamed Iran for orchestrating the current mayhem. The country, though invaded and occupied by US forces since Bush’s war in 2003, is “dominated and controlled by Iran” the president said.

To those many millions of people in Iraq who want freedom and who don’t want to be dominated and controlled by Iran, this is your time!

However, by all appearances it’s the Americans that have fallen out of favor. Naturally, Iraqis across the religious and political spectrum don’t like seeing their country bombed repeatedly by both the US and Israel multiple times over the past months.

Meanwhile, the Pentagon has announced it will be sending additional forces as security to protect US facilities. Defense Secretary Mark Esper announced the US will send additional troops to Baghdad specifically to protect the US Embassy in Iraq.

The breaking details, via Bloomberg, will include about 100 Marines sent from nearby Kuwait and two AH-64s Apaches which will fly over the embassy in a show of force. According to one defense official cited by Bloomberg, the Marines will likely fly to the embassy area in V-22 Ospreys.

But now the question remains: will the bulk of the Iraqi population join the Shia militias’ calls to expel the ‘foreign occupiers’ and thus intensify pressure on American forces to leave?

Or will Iraqis actually head President Trump’s call to rise up against those leaders in Iraq who are ‘tainted’ by their links to Iran?

As Ron Paul noted this week, the greatest threat to peace in 2020 now looks to be a possible disastrous Iraq War 3.0.

Remember the Kansas police officer who claimed that McDonald’s employees had written “fucking pig” on his coffee cup? Welp, it was a hoax: The officer wrote the message himself.

Herington Police Chief Brian Hornaday did not reveal the 23-year-old officer’s name, but did say that the individual has been fired, according to KSNT.

“Now, this is absolutely a black eye on law enforcement,” said Hornaday. “I truly hope that the former officer of the Herington Police Department that did this, I hope he understands the magnitude of the black eye that this gives the law enforcement profession from coast to coast. None of us can be excluded from that.”

The incident should remind everyone not to immediately succumb to knee-jerk outrage when they read news stories like the initial one about the coffee cup. Not every hateful incident is exactly what it appears to be, or even real. It’s always prudent to wait for more details, since in manycasesthesekindsof things turn out to be hoaxes—and the police are perfectly capable of spreading misinformation.

from Latest – Reason.com https://ift.tt/2F6DIHS

via IFTTT