The global stock rally that took all US assets, including stocks, investment grade and junk bonds, to all time highs while sending gold and Treasuries soaring on Thursday, fizzled as world stocks fell on Friday amid worries about a U.S. military strike against Iran, while the ongoing US-China trade conflict took the edge off the central bank-induced rally from earlier in the week.

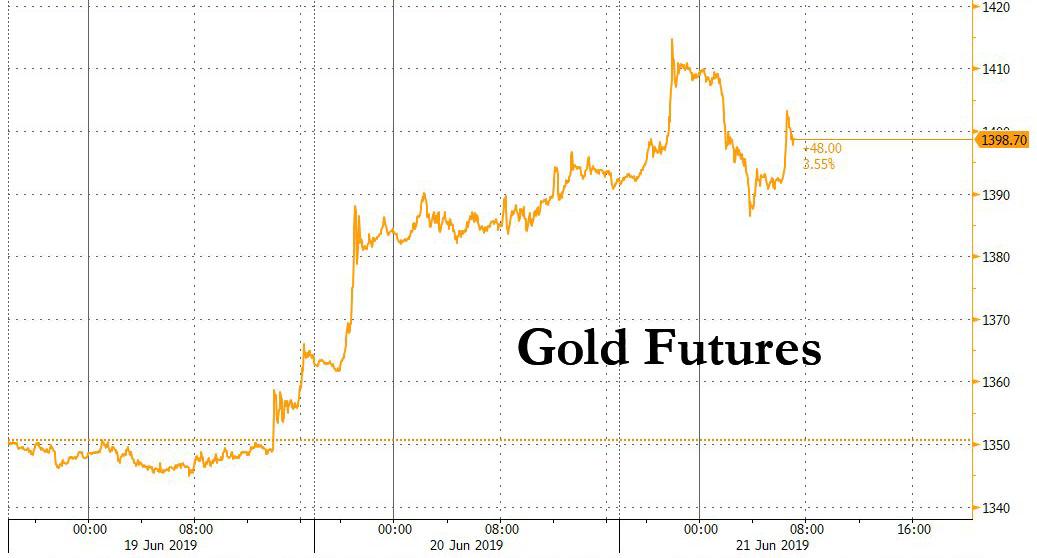

The scramble for anything that wasn’t nailed down, pushed Gold futures above $1,400 an ounce for the first time since September 2013 on Friday and Treasuries were steady.

After closing at a record on Thursday, the S&P 500 was set to open slightly lower, as Europe’s Stoxx 600 Index was weighed down by media companies. Asian markets were mixed, with Japanese, South Korean and Australian shares declining as Chinese shares rose.

Investor sentiment was rattled after the New York Times said late on Thursday that President Trump had approved military strikes against Iran on Friday in retaliation for the downing of an unmanned surveillance drone, then pulled back from launching the attacks. Iranian officials told Reuters on Friday that Tehran had received a message from U.S. President Donald Trump through Oman warning that a U.S. attack on Iran was imminent.

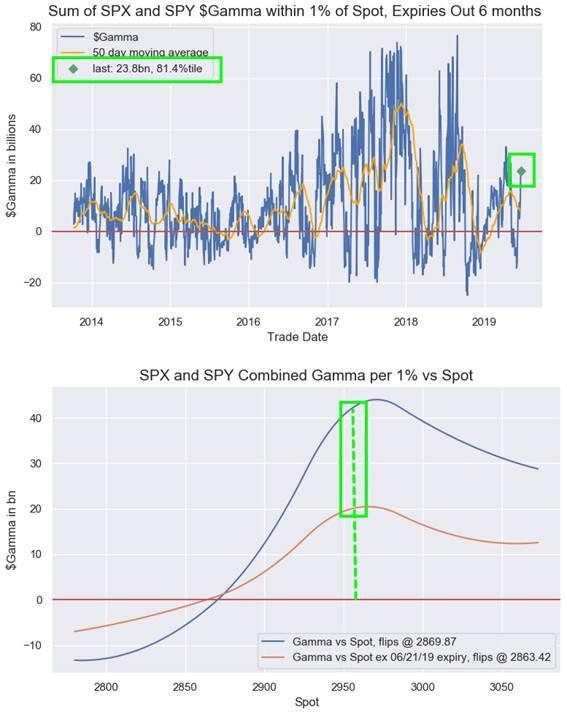

Friday is also quad-witching option expiration, when “strange”, and often unexplained things happen in the market as volumes soar and traders are caught flat footed. As a reminder, there is a major option “pin” around around 2,950 in the S&P, so it is quite likely that any major moves away will be difficult to achieve, but if the S&P starts moving, it may accelerate rapidly in either direction.

Meanwhile, worries about a possible mid-east war persist, and the MSCI world equity index fell from a seven-week high, driven mostly by weakness in Asian stocks. A rally by European stocks also faded, with the pan-European index sliding in the red.

“ … Market risk hasn’t been switched off, it’s merely gone dim,” said Vanguard’s Stephen Innes. “However, it does appear equity markets are tired and may be suffering from a bit of a hangover after partying it up to post FOMC.”

MSCI’s broadest index of Asia-Pacific shares outside Japan lost 0.15%. The index was still up nearly 4% on the week – its biggest weekly gain since January reaching its highest level since May 8. Markets in the region were mixed, with Japan and India retreating and China advancing. Health care and consumer staples were among the worst-performing sectors. The Topix gauge fell 0.9%, driven by SoftBank Group and Sony, as Japan’s key inflation gauge edged lower. The Shanghai Composite Index rose 0.5% before the first phase of A-share inclusion in FTSE Russell’s global indexes, which will take effect at the June 24 market open.

European stocks added to early gains after Eurozone, German and France flash composite PMI readings for June all came in stronger than consensus, suggesting that the worst of the European storm may now be over. The German June Flash Manufacturing PMI printed at 45.4, above the estimated 44.6 as New Orders rose to 44.2 vs 42.7 in May, their ninth consecutive month of contraction; in France, the June Flash Manufacturing PMI rose to 52 from 50.6, also above the 50.8 estimate and in line with the 52.5 print a year ago.

The news of a possible bottom in European manufacturing sent German yields higher across the curve, with the 10-yr Bund yield +2bps at -0.3%, still ~4.5bps lower on the week.

In US rates, Treasury yields were steady to 1bp higher in 2-yr through 10-yr tenors, with 10-yr yield down ~5bps this week, and unchanged on Friday at 2.02%.

As tensions remain elevated and concerns about collapsing global rates are rising, gold advanced to a six-year high of $1,410.78 an ounce on Friday, boosted by the geopolitical tensions and the prospect of a U.S. rate cut. At one stage, gold was up nearly 5% on the week.

“While lower real rates in the U.S. and globally make gold more attractive, the metal is being increasingly viewed as a cardinal asset to hedge against the scrim of unpredictability like the fear of recession and war,” Innes said.

Separately, China and the United States are set to resume trade talks before Presidents Donald Trump and Xi Jinping meet next week in Japan. Hopes of an agreement grew after the two leaders talked by telephone call, but neither side has signaled a shift from positions that led to an impasse last month. According to a real-time index of favorable trade deal odds from Goldman Sachs, the probability of a positive outcome is only 20%.

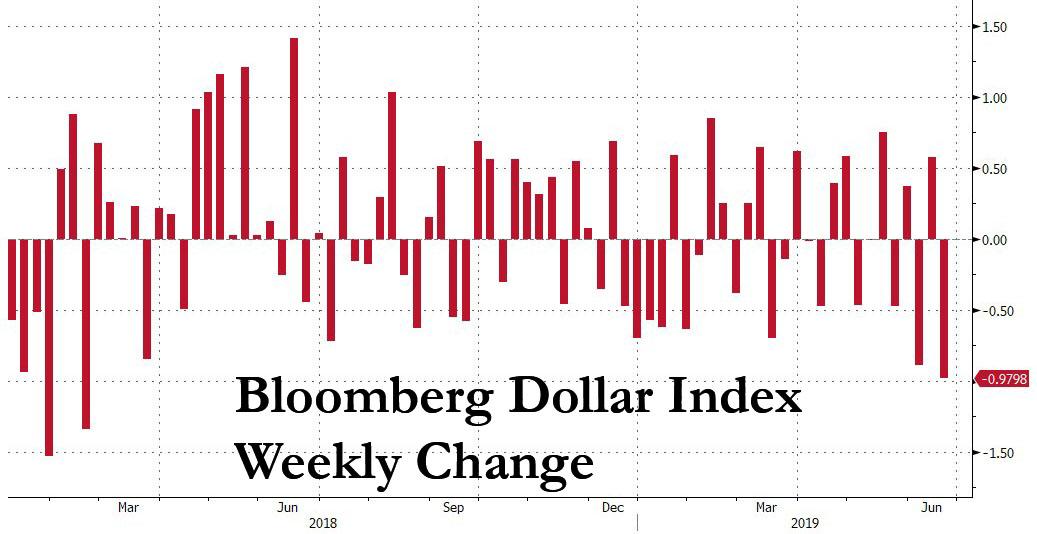

In FX, the Bloomberg USD index +0.1%, with NZD and GBP leading losses in the G-10 space, SEK leading gains. The Bloomberg dollar index steadied as investors trimmed short exposure into the weekend yet it was headed for its worst week since February 2018, after the Fed signaled that a rate cut is coming, which also pushed gold above $1,400 for the first time since 2013.

Elsewhere, the EURUSD gains as much as 0.2% to 1.1316 after the positive PMI surprises from France and Germany, even as the overall Euro-area manufacturing PMI reading at 47.8 missed estimate of 48 amid concern the region is sliding closer toward stagnation. The USDJPY reverses losses, rises 0.2% to 107.53 high, after dropping to 107.05, weakest since Jan. 3 flash crash. The USDCHF was up 0.2% to 0.9839; it slid Thursday to 0.9792, lowest since since Jan. 10; pair down 1.6% this week. GBPUSD slid 0.3% to 1.2656, off 1.2725 day high as the contest for the leadership of the Conservative Party enters its final stage as Brexiteer Boris Johnson will fight former remainer and current Foreign Secretary Jeremy Hunt to become Britain’s next prime minister. Cable is still up 0.7% on the week, as it built on broad dollar weakness, even as money markets now see a more than 50% chance of a rate cut by November 2020. Finally, down under, AUDUSD dropped 0.1% to 0.6916; while NZDUSD was down 0.3% to 0.6565 low as antipodeans lose traction after the London open; the kiwi led losses in G-10.

In commodities, gold was little changed, with both Brent ($64.76) and WTI (57.21) slightly higher on the session as traders awaited next steps in the Iran escalation. They had surged more than 5% the previous day after Iran shot down the U.S. drone.

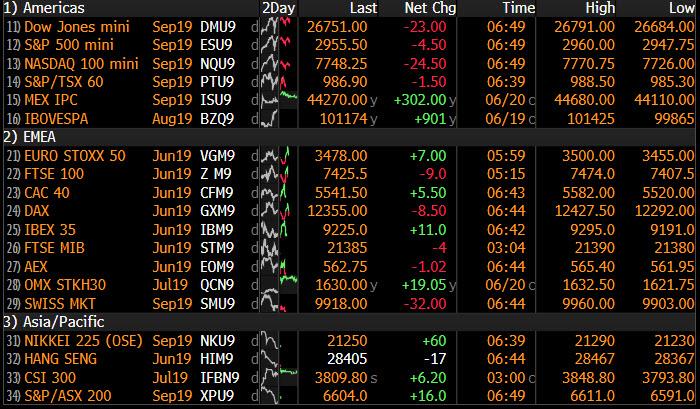

Market Snapshot

- S&P 500 futures down 0.1% to 2,952.75

- STOXX Europe 600 up 0.09% to 386.49

- MXAP down 0.4% to 159.44

- MXAPJ down 0.2% to 524.97

- Nikkei down 1% to 21,258.64

- Topix down 0.9% to 1,545.90

- Hang Seng Index down 0.3% to 28,473.71

- Shanghai Composite up 0.5% to 3,001.98

- Sensex down 1% to 39,200.52

- Australia S&P/ASX 200 down 0.6% to 6,650.78

- Kospi down 0.3% to 2,125.62

- German 10Y yield rose 2.1 bps to -0.297%

- Euro up 0.1% to $1.1306

- Italian 10Y yield rose 3.5 bps to 1.782%

- Spanish 10Y yield rose 1.1 bps to 0.403%

- Brent futures up 0.7% to $64.88/bbl

- Gold spot little changed at $1,388.66

- U.S. Dollar Index little changed at 96.64

Top Overnight News from Bloomberg

- The euro-area economy showed some signs of stabilization in June, but it may not be enough to comfort the European Central Bank. A pickup in a measure of activity was tempered by weakness in sentiment, which was at a five-year low, according to surveys of purchasing managers

- The last glimmer of positive yields on German bonds is in danger of being snuffed out. Thirty-year yields turning negative would be a first among major bond markets, with a global rally already having sent all of Germany’s out to 20 years below zero

- The U.S. called off military strikes against Iran on Thursday night that were approved by President Trump, according to an administration official, abandoning a move that would have dramatically escalated already high tensions between the two countries

- BOE Governor Mark Carney said the U.K. can’t avoid tariffs with the EU if it leaves the bloc without an agreement, refuting a position defended by Boris Johnson, the front-runner to be Britain’s next prime minister

- Hong Kong protesters, including student groups, resumed demonstrations in the city center Friday to demand Chief Executive Carrie Lam step down. Historic protests in the past few weeks prompted Lam to suspend the extradition bill indefinitely and apologize to the city’s 7.5 million people

Asian equity markets traded mostly lacklustre as the FOMC-fuelled momentum began to wane in the region despite the strong lead from Wall St where the S&P 500 rallied to fresh all-time highs and the energy sector outperformed on further oil advances. ASX 200 (-0.6% ) and Nikkei 225 (-1.0%) were both lower although downside was stemmed for most the session by strength in energy and commodity-related stocks after WTI gained around 6% and gold broke above USD 1400/oz for the first time since September 2013, while South32 was among the notable gainers in Australia after it received a couple of bids for its coal assets. Chinese markets were mixed with the Hang Seng (-0.3%) subdued after further disruptions from protesters discontent the extradition law wasn’t fully withdrawn by their set deadline and who also demanded that all charges against those involved in last week’s protests are dropped. Conversely, the Shanghai Comp. (+0.5%) bucked the trend and rose above the 3,000 level after the PBoC’s liquidity efforts resulted to a net injection of CNY 285bln for the week and with US-China trade negotiating teams said to meet as early as Tuesday. Finally, 10yr JGBs were higher and briefly broke above 154.00 amid the subdued risk tone in Japan and BoJ presence in the market for JPY 1.23tln of JGBs in 1yr-10yr maturities, while yields continued to decline in which Japanese 10yr yields fell to the lowest since July 2016.

Top Asian News

- Slow Monsoon Progress Threatens Dry Spell for India Agro Stocks

- FTSE Index Rebalancing Triggers Moves in These Asia Stocks

- China Says Within Rights to Control Foreign Visits to Hong Kong

- UBS Expects Asia IG and HY Bond Spreads to Widen Amid Trade War

European equities are mixed [Eurostoxx 50 Unch] as the region received a lacklustre handover from Asia on quadruple witching day. The European cash open was relatively uninspiring with most bourses flat/lower before receiving some impetus from encouraging French and German flash PMIs, albeit the EZ metrics were mixed. Sectors are now mostly in the red but energy names lead the gains amid the this week’s price action in the complex. In terms of individual movers, Natixis (-4.0%) shares fell amid a downgrade at HSBC. On the flip side, Elior (+4.3%) shares are bolstered due to a positive broker move at Goldman Sachs. Elsewhere, Telecom Italia (+1.6%) shares rose amid reports that the Co. signed a non-disclosure agreement to start talks regarding a TIM and Open Fiber network integration. Finally, looking at analysis from Nomura Quant, the bank believes that dips in stocks ahead of G20 pose good buying opportunities as it sees signs of increased equity exposures by speculators , “Judging from the pattern of market sentiment and supply-demand among hedge funds, we still expect the risk rally to sustain into July”, Nomura says.

Top European News

- Euro-Area Output Makes Subdued Improvement in June, PMI Shows

- Salvini Tax Cut Demand Squeezes Conte’s Room for EU Negotiations

- Telecom Italia Starts Talks to Combine Grids With Open Fiber

- Goldman Says Global Dovishness Will Delay East Europe Rate Hikes

In FX, the EUR has gleaned support from above forecast French and German preliminary PMIs that appear to have offset weakness elsewhere in the Eurozone and underpinned the pan prints to an extent. However, Eur/Usd has stalled well ahead of major resistance in the 1.1347-50 area where 200 WMA and DMAs reside as the Greenback attempts to stabilise following its Fed induced sell-off and the DXY holds just above 96.500 vs 96.492 lows. Note also, hefty 2.5 bn option expiry interest at the 1.1300 strike is keeping the headline pair contained, while Eur/CHF remains top heavy and technically bearish around 1.1100 even though the Franc is fading vs the Buck within a 0.9808-38 range.

- CAD/SEK – Also relative G10 outperformers as the Loonie holds above 1.3200 against its US counterpart and looks towards Canadian retail sales data for more independent direction, while the Swedish Krona seems to be benefiting from Scandi cross flows as its Norwegian peer loses some Norges Bank momentum, with Eur/Sek hovering just above 10.6100 and Eur/Nok rebounding from the low 9.6500 region to 9.6850+ at one stage.

- NZD/AUD/GBP/JPY – All weaker vs the recovering Usd, as the Kiwi fails to sustain gains above 0.6600 and Aussie wanes ahead of 0.6950 alongside a pull-back in the Yuan after a strong PBoC midpoint fix overnight. Meanwhile, Cable has been unable to retain grip of the 1.2700 handle yet again after topping out close to yesterday’s 1.2727 high for the week so far and the Yen has pulled up short of 107.00 with decent expiries between the figure and 107.05 (1.4 bn) adding to psychological resistance, as Japan’s monetary authorities monitor currency moves closely. On the flip-side, 1.3 bn options at 107.50 and a further 2.8 bn from 107.70-80 may well keep Usd/Jpy in check into the NY cut, if not beyond.

- EM – Widespread declines as the Dollar regains a degree of composure, and with the Lira also wary about the weekend election rerun in Istanbul following all the rumpus after the first vote. Usd/Try is back over 5.8000, while the Rand and Rouble are also handing back a chunk of their recent gains but not quite to the same extent, with Usd/Zar and Usd/Rub straddling 14.4100 and 63.1000 respectively. Note, MS has reportedly shorted the latter pair at 63.3000, looking for 60.0000 and placing a stop at 65.0000.mitigation.

In commodities, WTI and Brent futures continue to advance as tensions in the Middle East escalate, with NYT reporting that the Trump administration considered a strike in Iran following the downing of the US spy drone yesterday. Furthermore, officials stated that US President Trump delivered Iran a warning of an imminent attack, with the message noting “we do not want war but talks” and gave Tehran a deadline to start discussions. Brent is poised for it biggest weekly gain since April and inches closer to the USD 65/bbl level ahead of its 100 WMA at 67.10. Meanwhile, WTI futures reclaimed the USD 57.00/bbl handle before hitting resistance close to USD 58.00/bbl. ING believes “oil prices will trend higher over the second half of the year” due to the flaring tensions in the Middle East, coupled with expectations for an OPEC+ extension. Elsewhere, gold topped USD 1400/oz in Asia trade (albeit now back below the figure) and reached a high of USD 1411/oz, levels last seen in September 2013. Upside in the yellow metal has been driven primarily by the dovish tilts in major central banks, a weakening Buck and fears of potential war between the US and Iran. Gold remains near to the top of this week’s 1333-1411 range thus far. Elsewhere, copper pared some of yesterday’s gains as the FOMC-led momentum waned overnight, although the red metal is off lows. Finally, Dalian iron ore futures continued to advance as concerns persisted over tight supply, strong demand and declining shipments from Rio Tinto.

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 50.5, prior 50.5; US Services PMI, est. 51, prior 50.9; US Composite PMI, prior 50.9

- 10am: Existing Home Sales, est. 5.3m, prior 5.19m; MoM, est. 2.12%, prior -0.4%

DB’s Jim Reid concludes the overnight wrap

Welcome to the longest day of the year here in the Northern hemisphere. It’s all downhill to winter from here folks! Sadly it’s been a long night at home as Maisie is having withdrawal symptoms on her second night without a dummy. We’ve been up a few times and as I type this I can hear “I want my dummy” in the background. Sigh. I hope it doesn’t put me off my stride for the below. That’ll be more dolls house furniture we need to buy this weekend.

Markets continue to party on the central banks’ decisions this week, with the ECB and Fed having managed to ensure that rates, equities and credit are all prospering with the S&P 500 at all time highs last night even if markets are consolidating a bit in the Asian session. Also a late US rates sell-off last night dented the run a little too. It’s not clear what caused it but it could have been a delayed reaction to the strongest day of the year for oil (+5.38%) with Iran tensions mounting. Anyway its been mostly reversed in Asia as 10yr USTs hover around 2%.

There is one more big test left for markets this week and that is the release of the flash June PMIs today. We’ve already had the Japan manufacturing print which came in at 49.5 compared to 49.8 last month with accompanying commentary from IHS Markit reading that “a soft patch for automotive demand and subdued client confidence in the wake of US-China trade frictions were often cited by survey respondents”, as a reason for a further loss in momentum. In Europe this morning, the consensus expects modest improvements for both the manufacturing (48.0 vs. 47.7 last month) and services (53.0 vs. 52.9 last month) readings for the Euro Area with manufacturing prints for Germany and France also expected to improve. We’ll also get the data for the US this afternoon where no change is expected for the manufacturing print at 50.5 and a 0.1pt rise for the services reading to 51.0. All evidence of trade war interference will be carefully assessed around the globe.

The highlights yesterday included a new all-time high for the S&P 500 (+0.95%) which came only 13 sessions after hitting a 12-week low earlier this month (+7.64% higher from these lows). The NASDAQ (+0.80%) and DOW (+0.94%) are back to within 1.55% and 0.74% of their respective all-time highs as cyclical sectors led the charge yesterday. The dollar declined another -0.48% as the fallout from yesterday’s Fed meeting continued, with EM currencies advancing +0.33% to an 8-week high. That included a +0.55% gain for the Turkish Lira following a bit of a whipsaw day after President Erdogan advocated for lower rates and retributions for US sanctions.

There was a swoon around lunchtime in the US, with all the major US indexes paring almost all of their gains, as the tension between the US and Iran notched up another several gears. Iran apparently shot down a US reconnaissance drone in international airspace, though the leader of the Revolutionary Guard Gen. Hossein Salami suggested it had broached Iranian airspace. He went on to say that “we are fully ready for war” though he does not desire conflict with anyone. President Trump responded by tweeting that “Iran made a very big mistake!” and telling reporters that “you’ll soon find out” if the US would respond militarily. He also invited Congressional leaders from both parties to attend a briefing in the White House Situation Room, a relatively rare occurrence. Markets nevertheless bounced off their lows when Trump clarified that he finds it “hard to believe it was intentional” by Iran. Still, WTI oil prices rose +5.38% – their biggest daily gain since 26 December – and gold reached a five-year high (+2.16%) as investors digested the implications of the elevated geopolitical risks. Overnight, the New York times has reported that President Trump approved military strikes against Iran in retaliation for the downing of the drone, but pulled back hours after approving them. The report further went on to add that it is unclear whether the attacks might still go forward. So certainly one to watch.

In Europe, the STOXX 600 posted a +0.36% gain while cash HY spreads in Europe and the US were -15.0bps and -11bps tighter respectively. In CDS markets the CDX IG index in the US is trading at the tightest level in 15 months while iTraxx Main is at the tightest level since last May. As for rates, 10yr Treasuries yields edged +0.5bps higher with the late day sell-off, though they had earlier slipped below the 2% level for the first time since the US presidential election in November 2016. Meanwhile 2yr yields were +4.2bps higher, causing the curve to flatten -3.7bps to 24.5bps. Across the curve, inflation breakevens rose, likely as a result of climbing oil prices, while real yields actually continued to slide, with the former outweighing the latter overall. For the Fed, that divergence is likely the ideal policy outcome. Yields in Europe were broadly 2-4bps lower with 10y Bunds in particular rallying -3.0bps to -0.318% and back to the lows once more. BTPs underperformed, selling off +3.7bps as Italy sent a reply letter to the Commission about its budget. The initial reports suggest that the document is light on details, potentially raising the odds that ECOFIN opts to open an EDP against Italy at its July 9 meeting.

This morning in Asia markets are trading mixed with the Nikkei (-0.58%), Hang Seng (-0.26%) and Kospi (-0.27%) all down while the Shanghai Comp (+0.61%) is up. The Japanese yen advancing to 107.08 (+0.21% this morning), the strongest level since April 2018, is likely to be weighing on the Nikkei. Meanwhile, yields on 10y JGBs are down -0.9bp to -0.185%, thereby trading very close to the lower target bound of -0.20%. However, the BoJ Governor Kuroda said in his presser yesterday that markets should think of the target range flexibly. Elsewhere, futures on the S&P 500 are down -0.28%. In terms of other overnight data releases, Japan’s May CPI came in line with consensus at +0.7% yoy while core-CPI came in one-tenth above expectations at +0.8% yoy. Staying in the region, it’s worth noting that yesterday Chinese President Xi said that China is willing to play a “positive role” in the denuclearisation of the Korean peninsula. So that might be an added element to upcoming US/China trade talks.

Moving on and after an epic central bank week, the baton was passed to the BoE yesterday. As expected, there was no policy change in what was a unanimous decision. Since MPC members Haldane and Saunders had indicated that they were prepared to raise rates in coming meetings in comments prior to yesterday, this was at the margin dovish. Language around global growth was downgraded, while language on domestic growth was also softer, with the forecast for GDP in Q2 downgraded to 0.0% from +0.2%, albeit closer to what the market expects. Sterling had been trading stronger prior to the meeting but gave up some gains after the statement was released to finish +0.52% on the day. Our UK economists described the meeting as a steady as she goes type of message and also noted that the overall tone was slightly dovish. See more here .

Staying with central banks, amazingly we can list one as being hawkish this week with the Norges Bank yesterday hiking rates 25bps (albeit as expected) to 1.25%. The statement and forward guidance was a lot more hawkish than expected though, including signals that there are more hikes to come and it helped the NOK rally +1.83% and the most of any major currencies yesterday.

In the UK, politics continued to consume a lot of attention. The final two candidates for the Conservative party leadership contest are now set; it will be Boris Johnson versus Jeremy Hunt. The bookmakers certainly favour Johnson (per the Telegraph), with current odds implying that he is a 90% favourite to win the vote amongst the 160,000 Tory party members. The winner will be announced on 22 July, leaving 3 days before Parliament’s planned summer recess, which is set for 25 Jul-3 Sep. That will leave a three day window for either Johnson to announce a general election or possibly for the opposition to table a no confidence motion.

As for the US data, a pretty awful looking headline June Philly Fed reading (0.3 vs. 10.4 expected and 16.6 in May) was partially offset by better underlying details and also a consensus reading which appeared far too optimistic in the first place given the latest empire reading. Indeed the ISM-adjusted series (constructed from components similar to the ISM) actually rose by 0.4pts to 55.0. As for claims, they fell 6k last week to 216k and thus reinforced the strong labour market message. The other data yesterday came from the UK where retail sales excluding fuel fell -0.3% mom in May, slightly less than expected.

Finally to the day ahead, which this morning includes those flash June PMIs in Europe and May public finances data in the UK. In the US we’ll also get the flash PMIs followed not long after by May existing home sales. It’s also a busy day for Fed speak with Brainard and Mester taking part in a Fed Listens Event this evening, while Daly is due to speak later on. The BoE’s Tenreyro is also due to speak this afternoon. The other potentially important event is the latest results of the Fed’s stress tests. The results are due in two stages with the first results due today which will reveal the hypothetical losses banks would face under the Fed’s calculations.

via ZeroHedge News http://bit.ly/2L6CO2e Tyler Durden