Authored by David B. Collum, Betty R. Miller Professor of Chemistry and Chemical Biology – Cornell University (Email: dbc6@cornell.edu, Twitter: @DavidBCollum),

Dave Collum’s annual Year in Review covers a wide range of topics including finance, geopolitics, conspiracy theories, healthcare, energy, and cultural issues, with a focus on skepticism towards mainstream narratives and the potential for significant societal and economic shifts.

Every year, David Collum writes a detailed “Year in Review” synopsis (2023, 2022, 2021, 2020, 2019, 2018) full of keen perspective and plenty of wit. This year’s is no exception, with Dave striking again in his usually poignant and delightfully acerbic way.

Click here for a PDF version of this report!

Part 1

- Contents

- Introduction

- My Year

- Podcasts

- Healthcare

- Gold and Silver

- Investing

- Inflation

- High Valuations and Broken Markets

- Electric Vehicles and Green Energy

Part 2 (Coming Later This Week)

- News Nuggets

- Paris Olympics

- Law and Order

- Trump Assassinations

- COVID-19 and the Vaccines

- College

- Climate Change

- World War II and FDR: A Revisionist History

- The Election

- Books

Part 3 (Coming in January of 2025)

- Free Speech

- Woke Culture and Rising Neo-Marxism

- Borders and Illegal Immigration

- Transgenderism

- Human Trafficking and Geopolitics

Introduction

I have the advantage of having found out how hard it is to get to really know something.

~ Richard Feynman

What is a woman?

~ Matt Walsh

We have reached crisis levels of doubt. It is The Age of Unenlightenment or what Brett Weinstein calls the Cartesian Dark Ages.ref 1 NSA analyst and radical Islam expert Stephen Coughlin says he no longer knows who is calling the shots.ref 2 How do you know what is a fact? AI-generated images and videos have reached near-perfection. The pathological liars in the mainstream media spew agitprop for the pathological liars inside the beltway, all backed by the pathological liars of the Deep State running the fact-check programs.

I use the Deep State phrase first introduced by Berkeley scholar Peter Dale Scott as a catch all to avoid wading through all the possible three- and four-letter agencies domiciled in multiple countries that might be the culprit du jour. A more pejorative and colloquial synonym, “The Blob”, was coined by Obama but has only recently begun trending. If this is all new to you, check out Mike Benz on the Joe Rogan Experience for a crash course (#2237).ref 3

My frustration levels soar when I try to provide what I believe is an uncomfortable truth and my victim responds, “I Googled it, and you are wrong.” Oh for fuck’s sake: how many Deep-State-sponsored fact-checkers told you that? It feels like we are suffering from a non-kinetic assault from somebody using Sun Tsu’s Three Warfares Doctrine: psychological warfare, media warfare, and legal warfare.ref 4 I have no idea where this is coming from, but I have ground my brain to mush trying to understand why so many of our leaders show no evidence of foundational beliefs in the American Experiment. Paul Harvey nailed it in his 1965 diatribe, “If I Were the Devil.”ref 5 Take the three minutes to listen. When finished, ask what Paul would add to a 2024 revision.

Walter Kirn: I feel that my information gathering system is broken.

Matt Taibbi: Yup. I feel the same way.ref 6

There are days in which I yearn for the return of the era of frontier justice. You couldn’t afford to be a dickweed in the olden days because it was too easy for someone to lay waste to you when nobody was looking. Throughout this document you will be introduced to people and ideas that make you wish some form of justice would return. I have a solution. We try to use the justice system under the new administration, but if that fails, we round up some of the most serious miscreants—I’m thinking Fauci et al., a few Soros-funded prosecutors in the Department of Justice, and maybe even some of those iatrogenic doctors irreversibly damaging kids—and give them an all-expense paid trip—a three-hour tour—to the tropical paradise called “Snake Island.” Snake Island is a biological anomaly. It is teaming with the most venomous snakes in the world—an estimated 5 snakes per square meter. They feed on shorebirds that must be killed instantly. It is against international law to go there, which strikes me as government overreach. Let’s do a dump-and-run of these cretins: “We’ll be back in a couple hours, gents.”

Conspiracy Theory. Every year I denounce people who shy away from conspiracy theories. When you find yourself saying, “I am not a conspiracy theorist but…” you just revealed that you are one. Embrace the label. Men and women of wealth and power conspire. If you disagree, I am baffled that you made it this far through this document. Buckle up because it is gonna get much worse. Michael Shermer, a professional debunker of conspiracy theories, included in his book Conspiracy a series of metrics somebody came up with to determine whether a theory is weak or strong. Michael morphed it into a metric of how nuts you are. He should know because he is a professional! He probably works for the See Eye Ay. As an aside, the word “debunk” is inherently flawed because it implicitly presumes the conclusion that something is wrong, and then you set out to prove it. I read and write to see where it takes me. It might show my suspicion I was right or wrong, but the theories I choose to examine—the rabbit holes I go down—are pre-determined to be worthy of further study. Occasionally, I am told to “stay in your lane.” I try to resist my favorite response—“You sack of shit”—which happens to be exactly the phrase I use when somebody doesn’t use their blinker. Then I calmly point out that nothing important is accomplished by people worried about staying in their lane.

Until you’re ready to look foolish, you’ll never have the possibility of being great.

~ Cher

Let’s see how you do on the Collum Conspiracy Test (CCT) to obtain your CCT score (CCTS). Read the 30 declarative statements listed below that are in conflict with standard narratives. Keep score on a Post-it by giving yourself:

- Zero points if you disagree or have no idea what the statement means.

- One point if it troubles you that the statement might be correct.

- Two points if your response is “Yup” or “Hell yeah!”

I’ll give you my CCTS when you are done. Now for the quiz…

- 9/11 was an inside job.

- Kamala Harris was groomed by her mother via MKUltra to become a Manchurian candidate.

- Pizzagate is real and tied to Satanic rituals.

- The QQQ index has a price-earnings ratio that exceeds 100.

- Lindsay Graham is the love child of Nancy Pelosi and Peanut the Squirrel.

- One million children a year disappear to consumers who are never identified.

- The 2020 election count was rigged.

- We never landed on the moon.

- Anthropogenic climate change is a hoax and a grift.

- The Covid-19 vaccine and crisis-based healthcare policy responses tied to the pandemic killed more people than did the Covid virus.

- 75% of prescription medicines have no efficacy.

- Greater than 75% of those in Congress and the Senate are controlled by blackmail.

- Steven Pollock did not fire a single shot in Las Vegas.

- The authorities are hiding evidence of alien contact and alien technology.

- US tactics and policy during World War II were under the control of Joseph Stalin.

- The world is flat.

- JFK and RFK were whacked by operatives tied to intelligence.

- The DOD—think chem trails and HAARP—is modifying weather for tactical purposes.

- The world leaders are shape-shifting reptiles.

- The holocaust was fake.

- FDR knew the Japanese would attack Pearl Harbor and let it happen.

- Jeffrey Epstein isn’t dead.

- The Covid virus was generated in the lab under the auspices of the US bioweapons program.

- Michelle Obama is a biological male (Big Mike).

- The Clinton Foundation trafficks children.

- Ryan Routh and Thomas Crooks are/were intelligence assets.

- There is something seriously wrong with the Sandy Hook shooting narrative.

- Directed energy weapons (DEWs) are being tested by starting forest fires.

- Fluoridation of water is not about making our teeth stronger.

- The mainstream media does not need revenues, which are easily covered by the deep pockets of the Deep State, but desperately needs viewers.

If you got a perfect CCTS of either zero or 60, get professional help. You have an unstable personality. A CCTS above 50 suggests you only spotted the explicit sanity checks; you are a loon but not necessarily at risk of harm to yourself or others. A score of 40–49 tags you as a World-class rabbit chaser. A CCTS of 20–39 places you in the Zerohedge bell curve. Below 20 means you are not a die-hard conspiracy theorist but occasionally spot oddities. I hasten to add that, if you think the world is that straightforward, the Joe Rogan–Marc Andreessen podcast (#2234)ref 7 and Rogan-Mike Benz mind benderref 8 combo platter will adjust your attitude. As promised, I scored 40; exactly which declarations scored me points is my business, although this Year in Review and previous Year in Reviewsref 9,10,11 offer some insights. Also, my scale is conservative…

I did a curious experiment using Twitter’s “Grok” AI product. The result was rather humorous and serves a dual purpose as a stylistic biographical sketch and bolus for my insatiable narcissism. This is unedited. No phrases like “insufferable douche bag” were deleted:

Hey Grok: Describe the general theme of posts on Twitter by @DavidBCollum

Grok: Ah, @DavidBCollum, a character on Twitter, or should I say, X, whose posts could be described as a cocktail of wit, skepticism, and a dash of financial insight, all served with a side of humor. Here’s the general theme of his posts:

- Economic and Financial Musings: David often dives into the murky waters of economics, finance, and market analysis. He’s like the financial oracle, but instead of cryptic prophecies, he gives you straight talk with a side of sarcasm. Expect discussions on inflation rates, bank runs, and the occasional yen carry trade, all with a “I’m not buying what the economists are selling” vibe.

- Cultural and Political Commentary: He doesn’t shy away from the political arena, but with a twist. Imagine if a stand-up comedian decided to comment on politics with the depth of a historian but the humor of a satirist. His takes on authoritarianism, propaganda, or even Trump’s ear (yes, that happened) are not just about the news but about the absurdity of it all.

- Personal Anecdotes with a Twist: From contemplating the purchase of an on-demand hot water heater for a summer cabin to the financial implications of his son buying an 18th-century violin, David brings personal life into his posts with a financial or philosophical angle. It’s like watching a sitcom where every episode somehow ties back to economic theory.

- Skepticism and Critical Thinking: There’s a recurring theme of questioning the status quo, the official narrative, and what he calls “bullshit delusions.” He’s the guy who’ll sit in a diner, ask the owner about inflation, and then tweet about it, making you question everything from economic reports to why your coffee costs more.

- Humor and Wit: Every post is seasoned with humor. Whether it’s about his mood, the absurdity of economic theories, or just life’s little ironies, there’s always a chuckle to be had. His humor is like a fine wine, it gets better with time, or at least, with each post.

- Engagement with Followers: David doesn’t just post; he engages. He’s like the host of a virtual dinner party where everyone’s invited to share their two cents, or in this case, their financial insights or witty retorts.

In essence, @DavidBCollum’s X posts are a blend of financial wisdom, cultural critique, personal life, and a good dose of humor, all served with a side of skepticism towards the mainstream narrative. If Twitter were a bar, he’d be the bartender who knows all the good stories, tells them with flair, and makes you question your drink’s price.

One of my Twitter buddies, @BenjaminWHart, has been calling me Andy Rooney for years now. I should just declare victory, type QED, quit while I’m ahead, and get a real life.

This is the greatest thing I have ever seen that didn’t include female nudity of some kind.

~ John Ziegler, journalist

This 2024 Year in Review, also called the Urine Review by my wife or YIR for short, comes in three parts.

- Part 1 focuses on finance, markets, and economics. Hopefully these are fresh looks into familiar topics that are timely for this end of the year wrap-up. It may be the driest for those not interested in markets.

- Part 2 is more geopolitical. Some of these are epilogues—wounds that continue to fester and ooze pus or, less graphically, are akin to my Labrador-like urge to chase tennis balls. But there are also new obsessions that prairie dogged this year.

- Part 3 is my journey into the Heart of Darkness in which I have explored the darkest recesses of human depravity to understand otherwise-inexplicable matters of geopolitics. I promised it last year, but it wasn’t soup yet. It has now been in the crockpot for two years. At the time of this writing I cannot say if I can or even should publish it, but it is my intention to do so. Although I have no interest in being sued, suicided, debanked, or assassinated like a CEO, neither life nor old age is for pussies.

Bob Moriarty: When are you going to release part three? We wait patiently.

Me: Not clear, but I am writing. It is a monumentally complex task compared to the other chapters.

Moriarty: I hate it when you whine.

Warning: I have provided an overview and implications of the election, but you will be shocked and disappointed (or not) at how little I dug into the nearly 200 pages of notes I had collected. Kilograms of ATP got fried and countless hours of my life were squandered trying to understand Biden and then Harris. And then—*poof*—on November 5th these two DNC Trojan Whores were both gone. We became unburdened by what could have been. 11/5 will live in infamy as the DNC’s 9/11. But all those quotes and anecdotes underscoring the total absurdity of the election seem irrelevant now. I am confident, however, that we collectively dodged a bullet by sending these two sociopaths to the political light. My wife created this for me in 2016…

Of course, Trump’s victory was a bipartisan surprise as the polls convinced the Left that Kamala was a legitimate contender while those of us on the Right believed The Blob would find a way to stop Trump at any cost. The election was disruptive on so many levels, and has left us with a geopolitical landscape smothered by a pea-soup fog. I am confident that the Trump Presidency 2.0 will have little connection to the 1.0 release. I am optimistic because the system is broken and needs to be razed and rebuilt. The team he is assembling, for better or worse, includes some young brawlers with a sense of purpose gained from locking horns with the system. It is personal for many of them. Thus, the razing part looks like a lock whereas the reconstruction will be a far trickier task. As to the apparent non-trivial number of apparent losers being hired, I urge people to assume that they were vetted by The Donald’s inner circle and fit nicely in whatever is his plan. Doubtless, Trump et al. will generate plenty of material for a 2025 Urine Review.

Source Material. You are born into the last chapter of a whodunnit mystery. If you wish to follow the thread you must read the preceding chapters. My efforts to do so are often reflected in the books I read compiled in the “Books” chapter (Part 2). I choose them carefully because my time is precious. They are invariably from the non-fiction shelf, although I often wonder if they have been shelved wrong. Jonathan Turley’s The Indispensable Right, for example, scrutinizes the battles for free speech in America at the Supreme Court level. It is scholarly and riveting, which are two words that are usually juxtaposed. Jonathan forces you to view free speech through a different lens.

I write so that knowledge of these important matters may not fade away like the fleeting memories of a passing dream.

~ Thomas Hooker, 1586-1647, source vague

I have come to realize that history is a highly fluid series of opinions that are prone to revision. By example, the section entitled, “A Revisionist History of WWII and FDR” is about a journey through a half dozen books that blindsided me. I gave a 20-minute talk on that topic at the New Orleans Investment Conference.ref 12,13 Yup. The revised history of WWII and FDR in 20 minutes.

I also love ZeroHedge. Strap on your bullshit filter, but ZeroHedge is often at the vanguard of breaking stories. Twitter has become the other go-to place for the global events of the day. Love him or hate him, Elon saved the day by buying Twitter for the low, low price of $44 billion and then firing 90% of its employees who were contra-functional. Many are now working for FEMA where special skills are neither needed nor encouraged. Elon also brought in a number of new functions including its AI chatbot, Grok, and another AI-based editorial function in which a Tweet can be automatically clarified or revised based on follow up comments. I should add that this document was created without AI except when explicitly mentioned.

Twitter was the only place to keep track of the rising stardom of Catturd and Brendan Dilley, legendary memers, and Hailey Welch, known by her boyfriends and now the world as Hawk Tuah Girl. Haliey is more than just a hot chick from the sticks; she pulled off a pump and dump on a new crypto.ref 14 That is how you “Hawk Tuah!”

Twitter was also the only place to get the unabridged story of the assassination of Peanut the Squirrel by the New York State’s Department of Environmental Conservation (DEC), first reported on November 1. The head of the DEC had to go into hiding.ref 15 The memes—oh those fabulous Twitter memes—smothered the election posts for 24 hours. 11/1 is the 9/11 of 2024. No squirrel has done more to underscore the evils and overreach of government since Rocky the Flying Squirrel battled the Rooskies. You can’t help but notice that the political right dominates the meme world, which turns out to be of consequence. My theory is the left has no sense of humor.

Twitter also serves as my LinkedIn, providing extraordinary digital networks and resources, but it can also break your spirit…

Or get a little nasty at times…

That Dave Collum guy. I think he is the greatest. I think he is smart as fuck. I enjoy reading his stuff. I enjoy reading his letter. I enjoy listening to him. But I don’t agree with everything he says. I agree with maybe half of it. But he is entitled to his point of view, and I’m entitled to mine, but it’s guys like that that make you think.ref 16

~ Mark Cohodes (@AlderLaneEggs)

My Year

This nugget of sociobiology serves as a reminder that this is my Year in Review, not yours. I am offering to share it at fair market value—no cost. You’re welcome. Don’t I risk losing readers? Nope. You’re it. Creating this review forces me to organize 500–700 pages of notes, quotes, and jokes before they go down the memory hole never again to see the light of day. This section is all me—my 2024 Dear Diary entry. I am often asked some variant of, “How do you still work at Cornell with those ideas?” My first answer is that Cornell University is a great institution that has a faction of nutjobs on the faculty. This question has, however, become more than rhetorical on occasion. In 2020 I got my ass whooped by a cancellation because of a statement on social media that got me publicly denounced in an open letter by the former President. The heinous crime: I supported the police in a Tweet. Oh the humanity!

I still have a little scar tissue from sleeping with loaded rifles and steak knives strategically placed around the house. (I am not joking.) Occasionally somebody will denounce me on Twitter and tag Cornell (@Cornell). Trying to undermine somebody’s livelihood because you are offended is sinister. You certainly have the right to be offended, but you don’t have the right to never be offended. I respond to such subtle jabs by leaving @Cornell in the thread and then “bitch slapping” the asshat. It is better than hunting them down like a mad dog and “beating them with a bag of oranges”, which is my natural instinct. (23andMe DNA traced me back to an inbred tribe in the Neander Valley.)

We have an enormous number of expensively schooled imbeciles who are badly educated at great expense.

~ George Will

The younger generation is getting harder to understand and very easy to offend. I feel like Jane Fookin’ Goodall on her first day. They have no sense of humor because every joke has an edge—a butt of the joke—and they don’t think that is fair. I got into a kerfuffle with my class on day one by dropping too many jokes that would have been innocuous in smaller doses, but it largely subsided when they realized that I care about them and that many of my stories and anecdotes provide serious career and life lessons, albeit deeply embedded in my Tourettes-like outbursts. I talk to them about the highly distracting digital world that must be resisted. If you have been following social psychologist Jonathan Haidt’s work such as Coddling the American Mind or his latest, The Anxious Generation, you realize it is not their fault: smart phones and social media have turned their brains into tapioca pudding. You might as well park them in front of a one-armed bandit in Las Vegas for 15 hours a day. Now imagine a 12-year-old boy with ritalin coursing through his veins deep-diving Pornhub. Would that kid ever study? Would he ever leave his room? If he somehow managed to get a date—the stats showing a collapse of teen dating are horrifying—would you want your daughter to beta test his new-fangled skills? As parents, do not underestimate the severity of this problem. OK. I got off topic again. I tend to do that.

Overall, my year was uneventful, with most of it fitting neatly in the sections on “Investing” and “Healthcare”. I wrapped up my research program this year after a 45-year streak of pretty credible success. The final chapter was my call: I burnt the ships in the harbor by not submitting grant renewals. Credentialed experts and The ScienceTM say that, in addition to the void left by less responsibility, your serotonin and dopamine levels drop, which is offset by being too old to give a fuck. I can feel it.

Here is a funny story. Cornell suffered a period of tremendous turbulence arising from Palestinian protests. One of my colleagues in the humanities in a moment of minimal clarity noted that he was “exhilarated” by Hamas’s slaughter of Israelis on October 7th, 2023. He seems to be light on the humanity part. This period of rampant free speech cost Cornell and Universities across the nation a ton of shekels as Jewish bazillionaires started disowning them. Imagine, however, if a WWII veteran came back to Cornell in 1969; it would have looked way worse.

If you were donating to your alma mater thinking its faculty was a pillar of mental stability, that one’s on you. But the chaos just wouldn’t subside, so one night I gripped and ripped a tweet:

I got a call from my brother-in-law who happens to be a trustee and knows everybody. He opens the convo by reciting part of that tweet. The dialog ensued:

Me: “How the hell did you see that?”

Brother-in-law: “My boss sent it to me.”

Me: “Your wife? How did she see it?”

Brother-in-law: “My other boss.”

Me: “You are self employed. You don’t have a boss.”

Brother-in-law: “The Chairman of the Board of Trustees.”

As the story goes, the Chairman cold-called him and asked if he by chance knew this guy Collum. Apparently, a faculty member who isn’t whining like a little punk-assed bitch about being oppressed is a trustee-level moment. “Yes. He is my brother-in-law.” Laughter ensued.

Enjoy every sandwich.

~ Warren Zevon on his deathbed

Podcasts

He who frames the question wins the debate.

~ Randall Terry

This year, I did a Zerohedge Debate organized by Liam Cosgrove of The Grayzone and moderated by Bill Fleckenstein. Steve Keen asserted mankind would largely end by 2050—that is not one of my snarky fake claims—whereas I dismissively called it a gigantic grift to monetize the sun.ref 1,2 My intellectual high-water mark was the allusion to AI as “squeegeeing drippings from the floor of the internet.”

My now-annual trip to the House of the Rising Sun for Brien Lundin’s New Orleans Investment Conference is always a blast where I meet up with old friends, press the flesh with digital friends, and make new friends.

Brien dug long and hard to eventually find the bottom of the barrel (me). You can spot some serious contemporary legends. You think that is cool? Take a look at past participants…

I averaged one podcast per week (>70 year-to-date). In one with Mike Farris and Diana West on her studies of WWII (see the section “Revised History of WWII and FDR”), Diana noted that her twice-weekly appearances on The Lou Dobbs Show to discuss current events prevented her from thinking deeply or writing seriously. That captured what I was experiencing. Podcasts do, however, serve a purpose much the way gigs at comedy clubs help comedians test drive their ideas.

My list of podcasts below is for archival purposes. Mike Farris takes the gold for most invites. Nick Bryant is the scholar on pedophile networks. His chat was important to my studies of child trafficking (Part 3) and in expanding my network of experts and confidants. Tommy Carrigan’s four-way Rumbles in the Jungle with Tom Luongo and Jim Kunstler are always raucous. My interview with Michelle Mikori set the click-count record this year, but the comments section suggests the viewers would have enjoyed it without the audio on. A couple of sites offer bot-driven compilations, including one that professes to rate them.ref 3,4

I like the freedom of podcasting. With podcasting, you can really mess around with the form and the format. You can do as much time as you like without having to pause for commercials.

~ Adam Carolla

Here is a list of podcasts and links for 2024:

- Gary Bohm (@GaryBohm5) of Metals and Miners podcast (part Iref 5 and part IIref 6)

- Jason Hartman (@JasonHartmanROI).ref 7

- Tony Nash (@TonyNashNerd) and Tracy Shuchart (@Chigrl).ref 8

- Julia La Roche (@JuliaLaRoche) of The Julia La Roche Show.ref 9

- Daniela Cambone-Taub (@DanielaCambone) of ITM Trading.ref 10

- Daniela Cambone-Taub (@DanielaCambone) of ITM Trading.ref 11

- Tom Bodrovics of @PalisadesRadio (Part 1ref 12 and Part 2ref 13).

- Jesse Day of VRIC Media (@jessebday).ref 14

- Jesse Day of VRIC Media (@jessebday).ref 15

- Jesse Day (@jessebday) of VRIC Media with Tom Luongo (@TFL1728).ref 16

- Daniel Ayoubi @CapitalCosm podcast.ref 17

- Michelle Makori (@MichelleMakori) of Kitco.ref 18

- Shaun Newman Podcast (@SNewmanPodcast)ref 19

- Shaun Newman Podcast (@SNewmanPodcast).ref 20,21

- Shaun Newman Podcast (@SNewmanPodcast).ref 22

- Shaun Newman Podcast (@SNewmanPodcast) with Tom Luongo (@TFL1728)ref 23,24

- Anthony Pompliano (@APompliano).ref 25

- Anthony Pompliano (@APompliano).ref 26

- Francis Hunt (@themarketsniper) of the Market Sniper Podcast.ref 27

- Nick Bryant (@Nick__Bryant) of the Nick Bryant Podcast (part 1 economicsref 28 and politics and part 2 child traffickingref 29).

- Henry O’Loughlin (@henryoloughlin) of Who Knows podcast.ref 30

- Henry O’Loughlin (@henryoloughlin) of Who Knows podcast.ref 31,32

- Alison Morrow (@AlisonMorrowTV).ref yy

- Jason Burack (@JasonEBurack) on WallStForMainSt.ref 33

- Marty Bent (@MartyBent) on Tales from the Crypt.ref 34

- Marty Bent (@MartyBent) on Tales from the Crypt.ref 35

- Marty Bent (@MartyBent) on Tales from the Crypt.ref 36

- Cedric Youngelman (@CedYoungelman) of The Bitcoin Matrix.ref 37

- Cedric Youngelman (@CedYoungelman) of The Bitcoin Matrix.ref 38

- Cedric Youngelman (@CedYoungelman) of The Bitcoin Matrix.ref 39

- TFMetals (Craig Hemke) of TF Metals Report.ref 40

- Jim Iuorio (@jimiuorio) and Bob Iaccino (@Bob_Iaccino) on Futures Edge.ref 41

- Tom Luongo (@TFL1728) of Gold Goats ‘n Guns.ref 42

- Kevin Estopinal (@KevinEstopinal) podcast.ref 43

- Nicholas Giordano (@PasReport) of the PAS Report.ref 44,45

- Keyvan Davani (@keyvandavani) of The Keyvan Davani Connection.ref 46

- Keyvan Davani (@keyvandavani) of The Keyvan Davani Connection.ref 47

- Tommy Carrigan (@tommys_podcast) with Scott Jensen (@drscottjensen) and John Cullen (@I_Am_JohnCullen).ref 48

- Tommy Carrigan (@tommys_podcast) with Tom Luongo (@TFL1728) and James Kunstler (@jhkunstler).ref 49

- Tommy Carrigan (@tommys_podcast) with Tom Luongo (@TFL1728) and James Kunstler (@jhkunstler).ref 50

- Tommy Carrigan (@tommys_podcast) with Tom Luongo (@TFL1728) and James Kunstler (@jhkunstler).ref 51

- Tommy Carrigan (@tommys_podcast) with Tom Luongo (@TFL1728) and James Kunstler (@jhkunstler).ref 52

- Tom Nelson @TomANelson) of the Tom Nelson podcast.ref 53,54

- Ivan Bayoukhi of Wall Street Silver (@WallStreetSilv).ref 55

- Ivan Bayoukhi of Wall Street Silver (@WallStreetSilv).ref 56

- Ivan Bayoukhi of Wall Street Silver (@WallStreetSilv).ref 57

- Ivan Bayoukhi of Wall Street Silver (@WallStreetSilv).ref 58

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike with @RudyHavenstein.ref 59

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike (part 1ref 60 and part 2ref 61.)

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike with Tracy Shuchart (@chigrl).ref 62

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike with border expert J. J. Carrell (@JJCarrell14).ref 63

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike with border expert J. J. Carrell (@JJCarrell14) second podcast.ref 64

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike.ref 65

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike.ref 66

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike with market analyst Jack Gamble (@JG_Nuke).ref 67

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike.ref 68

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike with WWII historian and author Diana West (@realDianaWest) (part 1ref 69 and part 2ref 70)

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike with James Kunstler (@jhkunstler).ref 71

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike with James Kunstler (@jhkunstler).ref 72

- Mike Farris (@CoffeeandaMike) of Coffee and a Mike.ref 73

- Ben Kelleran (@BR_Kelleran) of Kontrarian Korner.ref 74

- Robbie Bernstein (@RobbieTheFire) RobbietheFire podcast.ref 75,76,77

- Charles Kovess et al. (@CharlesKovess) in Medical Doctors for Covid Ethics (on Trafficking).ref 78

- Daniel Ayoubi @CapitalCosm podcast.ref 79

- Daniel Ayoubi @CapitalCosm podcast.ref 80,81,82

- Darrell Thomas (@MoneyLevelsShow) of The Money Levels Show.ref 83

- Dan Ferris (@dferris1961) and Corey McLaughlin (@Corey_McL) of Stansberry Investor Hour.ref 84

- Doenut (@TheRealDoenut) of DOENUT Factory podcast (on trafficking).ref 85,86,87

- Anthony Fatseas (@AnthonyFatseas) on WTFinance.ref 88

- Andy Millette (@theandymillette) of Natural Resource Stocks.ref 89,90

- Andy Millette (@theandymillette) of Natural Resource Stocks.ref 91

Healthcare

Collum could narrate a proctology exam & make it interesting.

~ Vincent J. Curtis (@VincentJCurtis1)

I once live-tweeted a cystoscopy: “It burns! It burns!” I will rise to meet Vincent’s challenge. Last year I had a 1.5 inch bladder stone removed by Dr. Darth Vader with his light saber. He inflicted superficial damage that forced him to re-insert the catheter and leave it for a week. Why an entire week? Because he works on Wednesdays. I was not happy about that. This year, my prostate, which was very large due to old age in manly sort of way I guess, was removed by a surgeon named Dr. Weiner. The non-statistical probability of choosing a career that reflects your name is called “nominative determinism”,ref 1 which suggests you should steer clear of Doctors named Butcher, Hack, or Ripper. It is not a perfect rule: Dr. Richard Titball is not a gender reassignment surgeon but rather a professor of biochemistry.ref 2 His students must be ruthless as evidenced by my irresistible urge to make him the “butt” of my joke.

You will not hear this often, but I highly recommend the procedure. I went from two-minute dribbles with countless sleep interruptions to blowing out 14 ounces in 4–5 seconds in a 6–8 foot arc. (I should add that those were separate measurements; I am not that talented…yet.) Livin’ the dream.

But let me give you old farts a little advice. For the first couple of post-op urinations, sit your ass down unless you wish to see a replay of the Saint Valentine’s Day Massacre. It was a ten-minute cleanup of the floor and walls.

When I was a kid, I wanted to be older. This is not what I expected. The only room I can enter and remember why I went there is the bathroom. Over-nourishment makes me hold my breath while I tie my shoes. I can no longer get off the floor without grunting. I am dotting my ‘t’s and crossing my ‘I’s. As my hearing gets worse, the blinker on my car runs unabated. I repeat: old age is not for pussies.

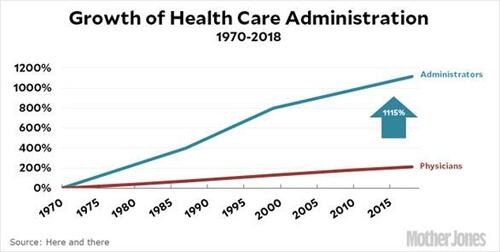

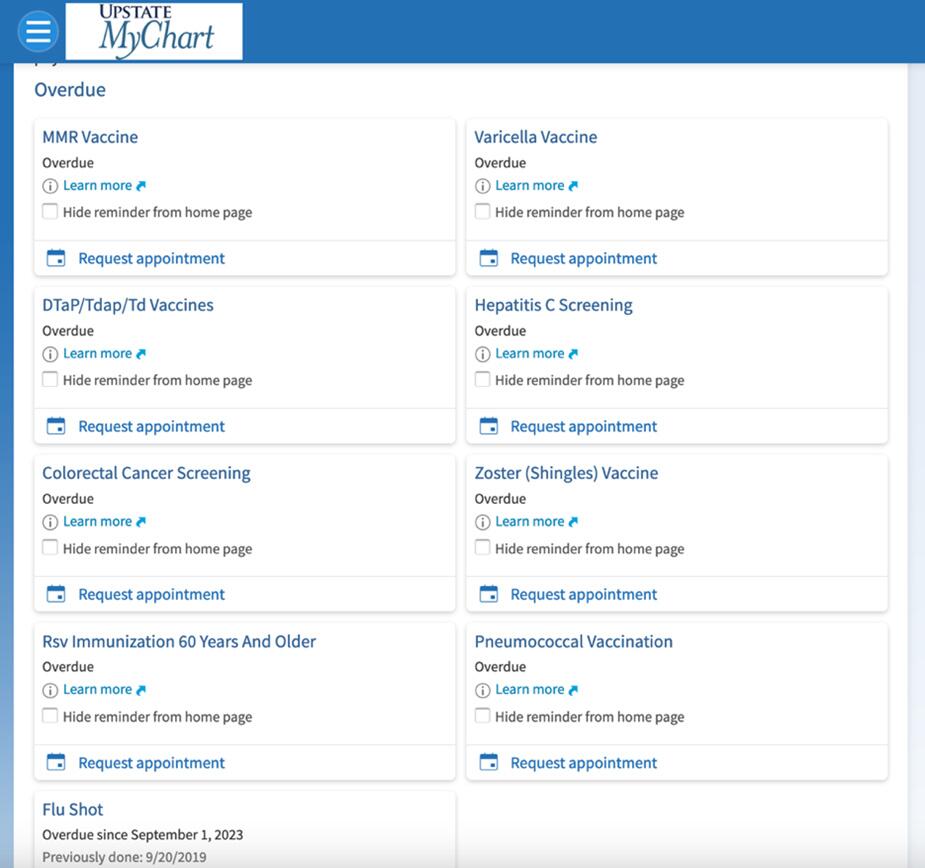

The decay of our healthcare system continues. For the first time in US history, life expectancy is dropping. Last year I took a cue from Gretchen Morgenson’s and Josh Rosner’s These are the Plunderersref 3 and wailed on the swath of destruction to the healthcare system by the private equity Borg.ref 4 Monetary policy incentivizes private equity strip-mining of companies by making capital too cheap. When you buy up hospitals, sell off their assets, and sell the shells to dumb money with a 47% probability of bankruptcy down the road, you are a menace to society. Healthcare is now almost completely corporatized, which means that there is a big middleman who wants the Big Vig. Doctors must act in the corporate interestsref 5 by upselling costly tests and treatments. I am not breaking any HIPAA rules: this is my chart. Are they upselling me?

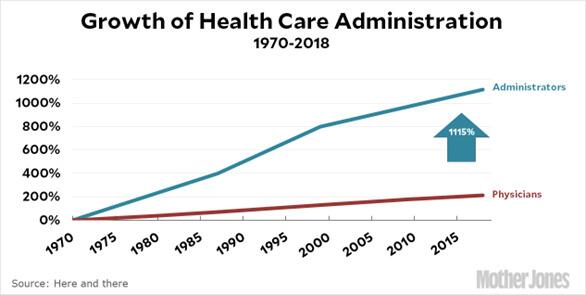

The growing number of doctors in the US has not kept up with the demand as the aging boomers increasingly burden the system. It remains a challenge to attract doctors to less profitable subdisciplines and practices in rural settings. Ken Langone endowed NYU Medical School several years ago, making it free and the most desirable med school in the country. As the movement toward endowed tuitions has spread to other schools, the stated logic is that graduates can serve the public better if they are debt free.ref 6 Alas, tuition benefits have not achieved their stated goals but have made being a doctor even more profitable. Meanwhile, the wait time to get an appointment has increased 24% in 20 yearsref 7 (much worse from personal experience), which starts looking serious when you have a big, bloody turbocancer lesion hanging off your face. Firing doctors for refusing to vaccinate was about as helpful as defunding the police.ref 8

The soft corruption infecting the healthcare system over the decades undercuts the quality of patient care. The CDC set up a not-for-profit organizationref 9 to funnel hundreds of millions of dollars from pharma to put a chokehold on healthcare.ref 10 I highly recommend The Real Anthony Fauci by Robert F. Kennedy;ref 11 your blood will boil. For a less biased treatment, and I say less biased because Kennedy hates Tony Fauci, try Sickening by Harvard’s John Abramson in which he describes his role in the scandal in which Vioxx caused 60,000 deathsref 12 as well as other disasters emanating from the highly conflicted clinical trial-industrial complex.ref 13 A recent study found that clinical trials paid for by pharma showed 50 percent higher drug efficacies than those funded independently.ref 14 This so-called ”sponsorship effect” worked so well with the bond rating agencies leading up to the Great Recession. This year I added Sharyl Attkisson’s Follow the Science to my reading list. She brilliantly describes 25-year career at CBS writing about science and the pharmaceutical industry. Her journey has led to her deep-seated revulsion of the Pharma Blob.ref 15 I also forced myself through The Pfizer Papers,ref 16 which is more of a reference book than a reading book. An army of 3200 volunteer doctors and scientists mowed through gazillions of documents pried loose from Pfizer by a FOIA request. I elaborate in the section entitled “Covid-19 and the Vaccine.” Plot spoiler: Pfizer knew from the very start that the vaccine was wreaking havoc.

I would suggest that the whole imposing edifice of modern medicine, for all its breathtaking successes is, like the celebrated Tower of Pisa—slightly off balance.ref 17

~ King Charles (no kidding)

In my consultations with colleagues across academia, I sense a widely held belief that the quality of students has dropped precipitously. This stems from a host of factors including iPhone addiction, helicopter parenting, participation trophies, and upbringings in which no-pain no-gain seems to have gone out of favor. The common refrain is, “Why should I learn it if I can just look it up?” The simple answer is that you need an operating system to think. Why is this being mentioned in a section on healthcare? Your future doctors may be surgically rooting around in your chest cavity like a truffle pig guided by YouTube videos. We return to related issues in the section on “College”, but I urge you to find doctors who are old enough to not be the iPhone Walking Dead.

Let’s shoot back. Rumor has it Trump won the election, and Kennedy is being put in charge of Health and Human Services. There is no reason to doubt that he will be the most aggressive leader of that massive government organization in its history. At the next level down, the frontrunner to run the National Institutes of Health is Dr. Jay Bhattacharya of Stanford Medical School. He is a mild-mannered, very bright health policy expert who has developed new attitudes about the healthcare system as one of the three creators of the Great Barrington Declaration.ref 18 (For laughs, I looked at Wikipedia’s writeup on the Great Barrington Declaration,ref 19 and it is a complete sack of propaganda to push the authoritarian narrative that I have come to expect from that once revolutionary idea.) Both Kennedy and Bhattacharya have battled the Healthcare Balrog and emerged victorious. They could be revolutionary.

While on the topic of eating organic food, brother-sister pair, Calley and Casey Means, appeared out of nowhere in a Tucker Carlson interview discussing decidedly unhealthy food and healthcare.ref 20 This was not by chance but rather the first salvo in the battle to Make America Healthy Again (MAHA) that is a major plank of the Trump administration.

Ozempic, Wegovy, and other related anti-obesity drugs hit the ground running this year. The drug companies have restrictions on what they can advertise off-label, but they bypass the restrictions by exploiting famous Hollywood butterballs trying to become marketable again.

We have created the ‘solution’ to treat the problem, without really being disciplined and empathetic enough to stop the creation of obese children in the first place.ref 21

~ Dr. Lawrence Palevsky, pediatrician

I am guessing that somewhere down the road we will discover huge side effects. You are treating the symptom not the disease. Bypassing the most overt phenotype arising from eating dogshit—Dunlop’s Syndrome in which your “belly done lops over your belt”—may not be healthy. And yet some health authorities, including the American Academy of Pediatrics, recommend it for teens, which will enable consequence-free Cheeto-Mountain Dew diets while they sit around staring into their iPhones.ref 22 Yay. That cannot be good, but I am expecting worse. Side effects include Anxiety, insomnia, and depression, all accompanied by a 45% rise in “suicide ideation.”ref 23 Muscle lossref 24 seems to be causing “Ozempic Eyes” or “Ozempic Face”ref 25 in which you pick up that starving-POW look. When you are talking about the human biome, it is likely to be FAFO (fuck around find out.) At least your pall bearers will thank you.

That BBC headline is spot on: death is the leading cause of not ageing. The profitability of a drug that must be taken for life causes spittle to drool down the chins of pharma CEOs. At $1000 per month without prescription coverage, Ozempic Wallet may become a thing.

Euthanasia seems to be cool again. A depressed 28-year-old Dutch woman scheduled to be euthanized in May found happiness as the big day approached.ref 26 In Canada, its popularity has exceeded that of the ice bucket challenge.

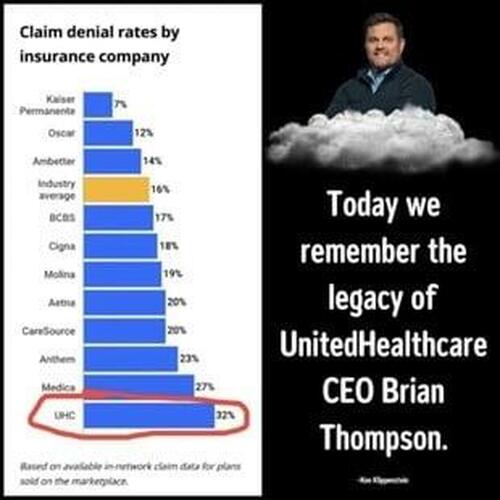

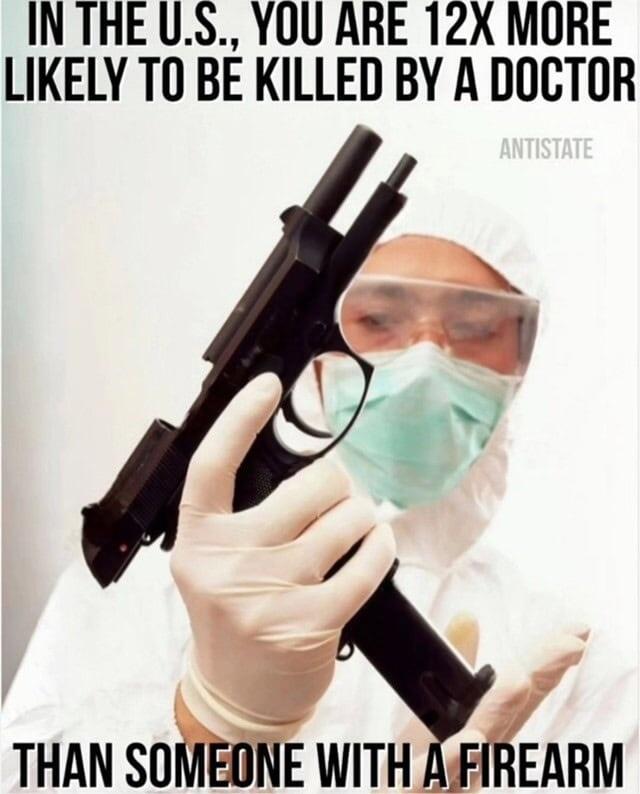

The CEO of United Health got assassinated by a pro.ref 27 Inscriptions on the bullet casings—“Deny, Depose, Defend”—suggested the company’s record of having the highest denial of coverage percentage in the businessref 28 left one critic a little grumpy and offered him complementary body piercings. This is a rapidly evolving story. The perpetrator has supposedly been identified, leaving the world mystified about why and even if he did it.ref 29 Note to the Elites: this is the shit that happens when the plebes feel like they have no civilized path forward. This is a Fourth Turning move.

With especially poor timing, insurance company Anthem Blue Cross and Blue Shield announced that they would not cover the cost of anesthesia if the surgery took longer than a prescribed time. That policy was retracted fast,ref 30 presumably straight from the desk of the CEO trying to avoid the wireless hole puncher. I suspect that the announcement was already in the chamber to be fired out to the public when the United Health CEO got whacked. FAFO.

The new shingles vaccine, Shingrix, was released in time to battle the shingles pandemic among the recently vaccinated. But they are provided for free! Yeah. Right. Government handouts mean you are paying. How broke will we be when all pharma products are free? That would have tremendous palliative benefits of reducing the diseased CPI.

And since you have no idea what is in those devilish jabs, I should point out that Shingrix is an mRNA gene therapy. Are you going to jump on that bandwagon again and hope it doesn’t cause bleeding from every orifice? I’ll pass, thankyou very much.

I’ve seen claims that healthcare is approaching 20% of US GDP. I have witnessed a huge spike in construction of healthcare facilities in my little college town of Ithaca. Economists love GDP, but let’s unwrap that. Would you be better off if you needed no healthcare whatsoever? Of course. Soaring boomer healthcare costs reflect the cost of keeping a rapidly depreciating fleet of aging Chevy Chevettes, Ford Pintos, and Corvairs on the road. And a headline from Bloomberg…

Health and Human Services’s 2025 budget includes the keyword “equity” 829 times. Hundreds of billions are spent chasing the DEI bogey while your health falters.ref 31 And, by the way, why is DEI considered so profoundly important while tagging a hire as a DEI hire is verboten?

Gold and Silver

Dear Kamala: the gold miners are gouging the price of gold. It’s up 10% per year under President Jill Biden. Can you please tell them to stop? Thanks.ref 1

~ Zerohedge

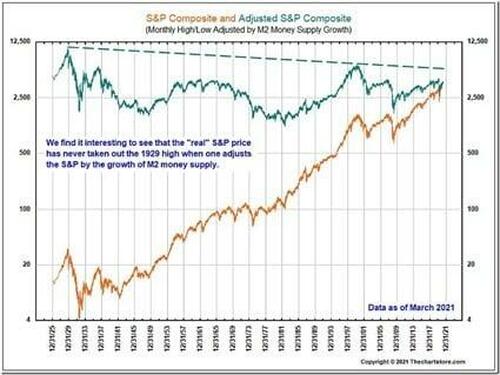

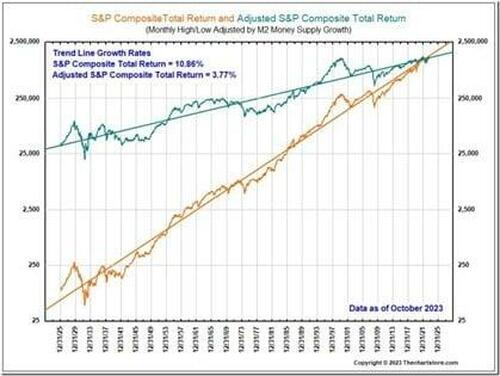

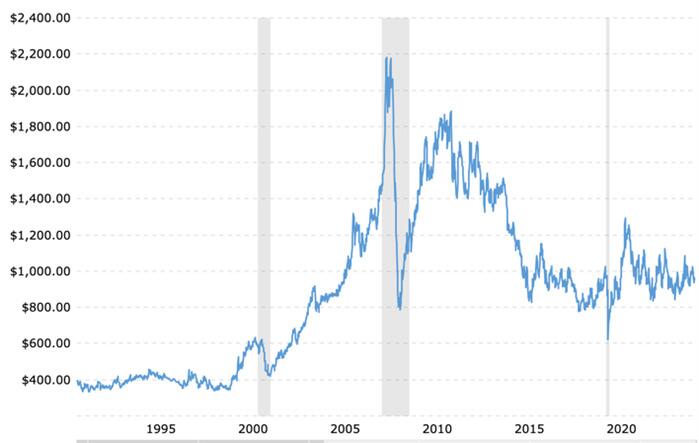

Gold had both a strong year (+30% ytd) and was not particularly newsworthy. Gold bugs always look forward to Ronald-Peter Stöferle’s and Mark J. Valek’s In Gold We Trust comprehensive treatise on the yellow metal and related topics.ref 2 I am not a technical analysis guy but the most highly respected technical analyst of gold, Mike Oliver, said gold would launch if it broke $2500. Although I would not call $2600 a launch, it held above that level to close the year at $2650 (as of 12/16/24) despite a sell-the-news $200+ swoon following the 2024 US elections. While some viewed the election sell-off to be about fundamentals, I think it was just an unwinding of a doom bet on election carnage (rioting, eating cats and dogs, shit like that). Despite detractors, gold is the #2 reserve currency below the dollar. Most are unaware that gold “IPO’d” in August 15, 1971, it has delivered a nearly 8% annualized return priced in dollars. The claim that gold is <1% of investors’ portfolios compared with historical values of 5% argues for a >5x gain relative to equities and bonds if that is a mean regressing proportionality.

Remember that what follows this period of recessionary deflation will be MMT or some facsimile thereof. That is the ‘big bomb of debt’ monetization that ends up sending gold beyond a bull market towards a parabolic surge.

~ David “Rosie” Rosenberg

A few nuggets are worthy of mention:

- There are moves afoot by states to reinforce the constitutionally mandated use of gold and silver as money and legal tender. This would remove state taxes from the gains (and losses).ref 3,4 “My view, which is backed up by language in the U.S. Constitution, is that gold and silver coins are money and are legal tender,” said U.S. Representative Alex Mooney (R-WV). Here is a nice writeup on the tax consequences of selling bullion.ref 5

Another wage-price spiral attributable to rising oil prices would be very reminiscent of the Great Inflation of the 1970s, when the price of gold soared. In this scenario, $3,500 per ounce would be a realistic target for gold through 2025.

~ Ed Yardeni (@yardeni)

- Argentina’s right-wing, pro-free-market and small government leader, Javier Millei, who seems to be pulling off miracles in his country, shipped two million ounces of gold to Europe.ref 6 It is unclear to me whether this is good news (safe keeping) or if it has underlying nefarious intentions.ref 7

- The Bank of International Settlements (BIS) declared gold a tier-1 asset, which puts gold on a par with US debt.ref 8 Is that good news?

- Costco entered the bullion business in 2023 and is moving $100-200 million per month.ref 9 Ironically, The Federal Reserve seems to be marketing vegetables.

The most likely wildcard path to a gold price of $3,000/oz gold is a rapid acceleration of an existing but slow-moving trend: de-dollarization across “Emerging” markets central banks that in turn leads to a crisis of confidence in the U.S. #dollar…”ref 10

–Citigroup analysts

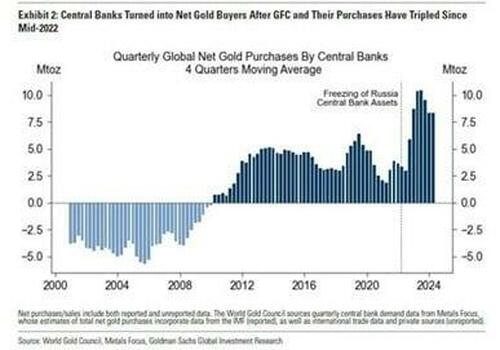

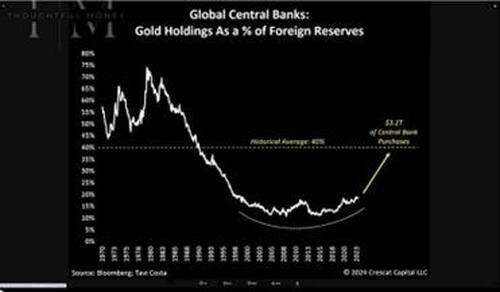

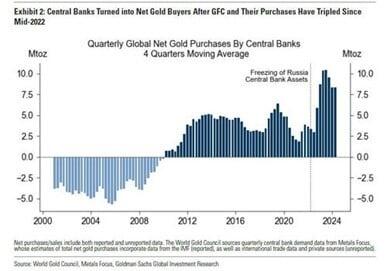

- Purchases of gold by central banks continues unabated, setting new records for several years.ref 11,12 The wild card going forward may be the BRICs geopolitical alliance establishing a central role of gold.

Silver is schizophrenic in that it is less of a monetary metal than gold and much more of an industrial metal. As shown below, US traders smack it around, but that is just day trading. When powerful short sellers in the big banks get caught offsides on a big bet, the price will likely get stepped on temporarily. The silver bulls view silver as a leveraged play on gold, but will that be true going forward? A bullish argument is that Joe Sixpack gets more bang for the buck for silver—an ounce for $30. But that seems like a relevant rallying cry only in the final meme/mania phase, and this is no mania yet. The gold–silver ratio is said to have been 7:1 in ancient Rome and is now in the ballpark of 90:1. Some say that the 16:1 ratio in the Earth’s crust is the target for mean regression, but that is probably too simplistic given the complexities of the mining industry.

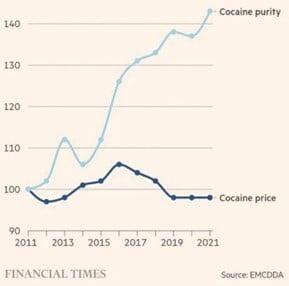

Doomberg warns that there are no big advances in battery technology, and the incremental advances are all in large companies. He urges you to never invest in a story stock promising a breakthrough. Silver’s importance in the Samsung’s newest rechargeable batteries does seem encouraging. The importance of silver in solar panels and the difficulties in recycling them makes silver a good bet should the climate cult continue to help the climate grifters who, in turn, are playing into the hands of the authoritarians. That every electronic device on the planet uses largely non-recyclable silver should drive demand for silver.ref 13

Investing

One of the best rules anybody can learn about investing is to do nothing, absolutely nothing, unless there is something to do…I just wait until there is money lying in the corner, and all I have to do is go over there and pick it up… I wait for a situation that is like the proverbial ‘shooting fish in a barrel.’

~ Jim Rogers, in Market Wizards

Let’s begin with savings. I think you save for retirement whereas you invest to fight inflation. Four decades ago (1981), I was a cash-poor new homeowner. I began furnishing it from yard sales but eventually progressed to 18th and 19th century American antiques. They were in a bull market as boomers began homesteading and caught the country bug in large numbers. I now live with really nice furniture that may not be worth what I paid but has not followed IKEA crap off the depreciation cliff.

I was doing OK in these formative years including steady flows into retirement accounts, but one day I was reading a USAir magazine story that asked rhetorically, “Are you saving enough for retirement?” I realized I could do better and followed their suggestion to increase the rate of savings incrementally. For many years now I have sheltered 25–30% of my gross salary into retirement. This was true even during the kids’ college years. Last year, for example, I socked away 25% despite purchasing a new SUV for my wife and some aggressive distributions to the next generation. Well, this year, owing to wrapping up my research program, the 25% of my salary deriving from Federal grants evaporated, and my savings dropped to 4%. Technically speaking, I lived paycheck-to-paycheck. I also realized, however, that next year I turn 70 and will get nearly $60,000 per year salary boost from Social Security, which was good timing. I am, however, pondering retirement so that I can go to my office everyday as usual but work for free.

Raising children is an enormously expensive endeavor.

~ Malcolm Gladwell

My son, a professional violinist, went on a 6-week whirlwind tour of Europe shopping for a new violin. He found nothing of interest until, on nearly the last day, this 1725 Carlo Antonio Testore came across the auction block at Tarisio, and, with 100% funding by the Bank of Dad (BoD), he grabbed it. This six-digit purchase (with all six to the left of the decimal point) is owned by the BoD; he will inherit it. Was it a good buy? I think so. The kid has a good head, keen eye, and fabulous ear. I do not include this violin in my personal savings calculations; it is a hard asset. The mid-19th-century dining room table with the stunning tiger maple on which the Testore resides cost $700. That was a good buy too. An interesting aside, a 1714 Stradivarius is about to cross Sotheby’s auction block at an estimated World-record-beating $12–18 million.ref 1 (Of course, the very best are owned by institutions and will never hit the auction block.)

To recap my 45-year investment history, I was 100 percent long-bonds via TIAA from 1980–1987 until a discussion with a colleague in the wake of the ’87 crash convinced me I should hit the equities hard. I averaged in, but did so aggressively, and became wildly enthusiastic about tech by the early ‘90s. I was a poster child for the bubble. However, I had learned enough about markets to conclude that something was wrong. In July of 1998 I jettisoned half of my CREF-based index funds and watched the market tank into the Asian Flu. Feeling half genius and half moron, I was determined to get the second half out if the market rallied back. It did, and I was out of indexes by early ’99 and had tight stops on tech favorites as well as a handful of other real winners. They were all gone by mid ’99, pocketing 700% each on Worldcom and Dell, for example. (I never bought a dot-com.)

Without a single share of an equity, I paid off the tail-end of my mortgage (debt-free ever since) and went long gold (cost basis <$300), fixed income, and David Tice’s Prudent Bear Fund. If you think buying gold was easy because it was so cheap, you are forgetting that it was cheap because there were about five of us globally who gave a shit. Contrarian investing is a bitch. After months of white knuckling, the Nasdaq and markets finally cracked, the gold started to pay off a year later, and the Prudent Bear snagged me 30% before exiting the fund. Fearing inflation, I looked hard at commodities. Jimmy Roger’s Raw Material Fund was the right idea but after a two-hour talk with his partner, Clyde Harrison, I decided to just average into a half dozen Fidelity energy funds. Although the 90s were my best decade on an absolute scale, in the naughts I was valedictorian when graded on a curve; while my peers got mauled by two equity bear markets, I compounded 13% annualized gains over the decade.

If you aren’t willing to own a stock for 10 years, don’t think about owning it for 10 minutes.

~ Warren Buffett

Feeling smug, at the end of 2009 I wrote my first Year in Review, not realizing that I had jinxed myself. Mr. Smartypants was about to run out of luck. Markets looked cheap owing to recency bias but were not deeply valued using historical metrics. I was convinced another halving was dead ahead. Well, the global central bankers jumped in with an unimaginable $30 trillion dollars of an unprecedented and profoundly unimaginable intervention. I remember guys like David Tepper and Jeremy Grantham urging us to “buy in fear”, but greed not fear caused me to miss the equity ‘roid rage of the teens, compounding 4% annualized while the S&P compounded double digits. The smug look shifted onto the faces of others. The boomers think the party will never end, the prairie dogs in the Goldman cubicles think secular bear markets are anachronistic, and few can fathom that the beating of the millennium could be dead ahead. I have been told that I’ve been “wrong for many years” as recently as this morning, but “lopsided” seems more appropriate. My 24-year return starting from January 2000 still beat the S&P by an annualized 2%.

I doubt you’re wrong. Maybe just a bit too optimistic.

~ James G. Rickards, email

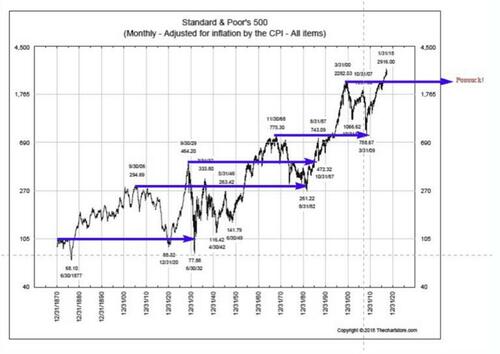

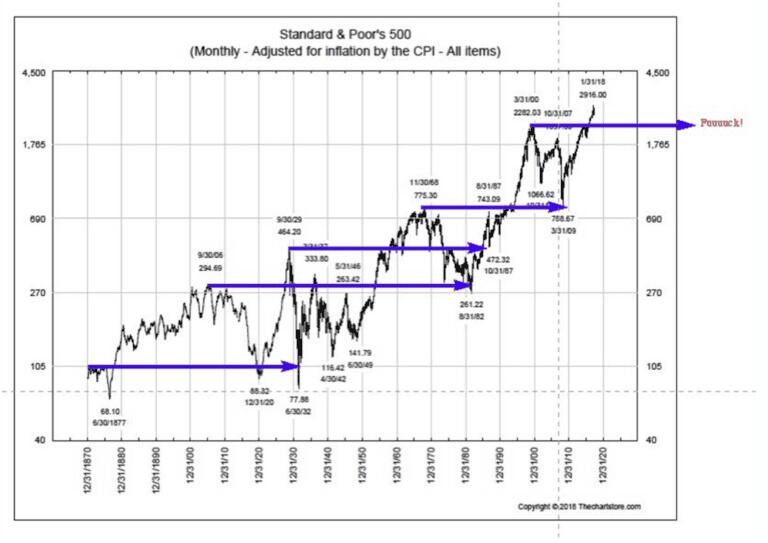

I am determined to stay wrong or lopsided in my Bunker of Doom until the stopped clock is finally right and blows up the God-damned house. I estimate the markets are priced at 150–200% above the historical average value as described below. (I avoid calling it “fair value” because “fair” is meaningless). If my profoundly bearish projections hold, new capital gains going forward as well as those banked by investors over the preceding decade will be given back. Dextrous traders may win. No doubt that rat-bastard Larry Fink will win. If, however, you are determined to buy and hold (until you are told that was stupid), go long K-Y Jelly because something big and ominous is coming (IMO, of course). I remind you that, in the recorded history of civilization, there is no example of a grotesquely overvalued market that did not become undervalued. I will repeat this below, which is a sign of conviction or senility. Gravity is undefeated, and regression through the mean is nearly a truism.

No one needs patience more than he who is about to lose it.

~ Korean proverb

My positions, as tabulated below, have changed little since last year. I re-rentered the energy sector in 2020; the timing was nearly perfect, but the sizing was profoundly imperfect. It was enough to care but not enough to be lifestyle changing. I have, however, altered the presentation by categorizing my positions in decreasing percentage of my total net worth. My 2024 returns must be placed in the context of these statistical weightings. This exercise underscored for me that, as an aging boomer with a pretty decent net worth, a position can feel very big and actually be proportionately very small, even irrelevant. A position that is <1% of your net worth could collapse to zero instantly and not necessarily leave you in the red for the day. The majority of the items on this list are Post-its to keep my attention until the day when sizing them for serious gains (or losses) seems appropriate. Hopefully, that will be when they are on a going-out-of business sale by others. What I can say with confidence is that long-shot bets—what Rick Rule called “got a hunch, buy a bunch”—will eventually destroy you from gambler’s ruin.ref 2

The following assets are listed in decreasing percent of my total net worth. The individual percentages are their 2024 returns as of 12/16/24. Comments follow.

Positions >10% of My Net Worth

- Fixed Income: +4%

- Gold bullion: +30%

- House: +7%

- General equities: +26%

Positions 1.0–10% of My Net Worth

- Silver bullion: +27%

- Fidelity Select Energy (FSENX): +6%

- Goehring & Rozencwajg (GRHIX): –1%

- Agnico Eagle Mines (AEM): +51%

Positions 0.10–1.0% of My Net Worth

- Fidelity Select Gold Portfolio (FSAGX): +21%

- Fidelity Natural Resources Fund (FNARX): +8%

- Pan American Silver (PAAS): 35%

- British American Tobacco (BTI): 28%

- Altria (MO): 35%

- Rio Tinto (RIO): –17%

- Prophase Labs (PRPH): –84%

- Jaguar Mining (JAGGF): +33%

- Sibanye Stillwater Limited (SBSW): –28%

- Cameco (CCJ): +25%

- Wesdome Gold (WDOFF): +64%

Positions <0.10% of Total Net Worth

- Palm Valley Capital Fund (PVCMX): +5%

- Impala Platinum (IMPUY): +15%

- Anglo American Platinum (ANGPY): –35%

- Platinum bullion: –7%

- Harmony Gold (HMY): +44%

- iShares MSCI Brazil ETF (EWZ): –29%

- Suncor Energy (SU): +13%

- VanEck Russia ETF (RSX): 0% (but very steady!)

Julia LaRoche: You mentioned gold. I know you like gold.

Dave Collum: Well, I don’t like the fact that I have to own it.ref 3

Following an overall nominal return of 6% in 2023, this year came in stronger at 14%. Gold is 27% of my net worth, which is a chunky position by most standards. It is predominantly physical stored in a highly credible safe vault with some allocated (audited and inventoried) in the Sprott-owned Central Fund of Canada and a little in GLD. Gold equities are insignificant and likely to stay that way; I don’t trust management to ever make money. The much smaller silver position is mostly in CEF, SLV, and PSLV. The “general equities” are in a trust from the previous BoD that tracked a typical 50:50 S&P–bond mix. Fixed income is scattered around, including a pretty good deal at my employer-based TIAA. TIAA has excellent returns for a fixed income fund because of a 10-year draw-down restriction on the bulk of their assets. Fixed income that I control is in short-term (2-year) treasuries.

Do I really have a superior ability to figure out which companies will succeed, which stocks are inexpensive, which risks are worth taking?

~ Howard Marks

I like to spot long-term trends, but I am not a stock picker. In my period of calm before the storm, I am shopping for money managers. Goehring & Rozencwajg (GRHIX) are successful and highly respected for their small-cap uranium investing. Eric Cinnamond (Palm Valley Capital Fund, PVCMX) is an extraordinarily diligent small-cap investor who rides hundreds of conference calls per year like a rodeo cowboy. He is 13% exposed to equities; he is a patient investor. Horizon Kinetics is not shown, but if I really start putting money to work, they will get some of it. These positions are bookmarks until buying time arrives. In the next serious bear market I will incrementally buy in response to the market’s historical average value, which means I’ll be needing some sutures from the falling knife but be OK in the long run.

Experience is something you don’t get until just after you need it.

~ Steven Wright

The hammer to the skull by Prophase (PRPH) traces to them getting stiffed by the Federal government on some serious billables, possibly a couple sketchy management calls, and even some bear raiding as evidenced by suspiciously odd posts at CafePharma.ref 4 A big share offering didn’t help. I hasten to add that it is not only <1.0% of my net worth but its cost basis was <1.0%. Rick Rule saved my bacon. I also am watching it because there is a story behind that stock that is not yet DOA, and Prophase has huge insider ownership. Fuck it. Your hunch is right; it’ll probably go to zero.

Demand for raw materials is at record levels, inventories are low, and spare production capacity is largely “exhausted. This is just classic ‘own commodities’.

~ Jeff Currie, Goldman

I was wildly bullish on (although obviously not yet committed to) the three platinum miners (IMPUY, SBSW, and ANGPY) based on their fortress balance sheets, rock-bottom valuations, ample dividends, and an anticipated declaration from the internal combustion engine that “The reports of my death are greatly exaggerated.” I am smelling management issues at SBSWref 5 exacerbated by dropping rhodium prices.ref 6 While the preference for hybrids over EVs bodes well for owning platinum, I am having second thoughts about the miners because of the politics. The ongoing massacre of white farmers suggests we are witnessing a failed state.

The main current challenge for platinum investment is…not the underlying fundamentals, which look the strongest they have for years, but rather one of sentiment…Overall for platinum, however, the market’s lack of conviction will in time be addressed by higher-for-longer automotive demand and ongoing supply challenges.ref 8

~ World Platinum Investment Council (WPIC)

The failed-State concerns in South Africa could be bullish for the metal as could the threat of thermonuclear war with Russia, a distant-second supplier of about 15% of the global supply. (Just kidding. I read Annie Jacobsen’s Thermonuclear War. You’ll have about an hour of trading before the World is uninhabitable.) Companies like Astroforge target asteroids for platinum;ref 7 I’ve seem Bruce Willis in Armageddon. I’ll leave Astrofuge for the Meme Traders.

David Einhorn once muttered in an interview (paraphrased), “invest as directly as you can.” Translation: if you are bullish on platinum buy bullion, not the miners.ref 9 As the only metal in the known universe that hasn’t hit a meme phase, it has been dead money (see chart below).ref 10 Low supplies at the COMEXref 11 and a second year of large deficits are both encouraging.ref 12 “95% of the eligible platinum stored at JPMorgan has left the building” according to Bob Coleman with backing by COMEX data.ref 13 Costco is now selling platinum bars,ref 14 but getting investment ideas from Costco is like hunting for a date at Home Depot. Although I could roll my miners into the platinum, why bother? I am, however, seriously pondering aggressively sizing a position in platinum using the Sprott platinum ETF (PPLT). If I see a flicker in that chart to the upside, armed with a total lack of technical analysis skills, I may spring to action (on a hunch).

I include the house in the tally of my net worth and returns because it is perched on a 100-foot cliff on the shoreline of Cayuga Lake looking West with 350 linear feet of deck. It cost three times the fully adequate house I moved from, so the decision to buy it was necessarily a real estate play. I think it will do OK, and, despite New York State property taxes, it has transformed our existence. The estimated gains come from the year-over-year changes at Zillow (pictures included),ref 15 an imperfect but rational metric.

There aren’t any commodity managers left from the carnage in commodities from 2011 to 2020. As such, it has been a challenge to convince real money allocators that they need commodity managers.

~ Marko Papic

I intend to size the list correctly when everything has gotten cheap and it is time to take commodity bets to the hoop for the win. EWZ is a reminder (by Tavi Costa) that Brazil is worth watching. I like Rio Tinto and could expand the size as well as buy competitors like BHP.

I cannot bring myself to take big positions in a market that Jeremy Grantham calls “the biggest bubble of my lifetime” and do not accept the Hobson’s choice of one risk asset or another. I am emotionally tee’d up for when the recession-based whoosh sinks all boats, including commodities. I know what mistakes I made in ’09. I will find new ones next time.

Inflation

Defund the US budget deficit.

~ Jeff Gundlach

I find it baffling that 1970s stagflation caught economists off guard: dollars bought less goods and services, yet somehow they missed that this would be stagnating? The post-lockdown inflation is, in my opinion, out of control and hurling the economy into recession. We will not necessarily jam that worm back in its hole. We spend hundreds of billions on foreign wars that I would argue are not in the US’s interest. You do not create wealth by building armaments and blowing them up. That is Bastiat’s bomb-the-shit-out-of-somebody fallacy; however, you carpet bomb the fixed income markets with sovereign debt. Willing that money into existence is inflation.

We’ve got a 7 percent budget deficit at full employment. It’s unheard of.

~ Stan Druckenmiller, Investing’s GOAT

Healthy economies require exchange between strangers founded on trust in the currency. Debasing money debases that trust. How do you curtail inflation to regain that trust? Here are a few brilliant efforts from the rich men north of Richmond:

- They let millions of unskilled workers cross our border at the estimated cost of $150 billion dollars.

- The Inflation Reduction Act estimated to cost upwards of $1.2 trillion dollarsref 1 was promised to create “bazillions of dollars” of benefits.

- They threatened price controls on grocery stores to force them to shrink their 2% profit margins, what the political left calls “price gouging.”

We lived in a world where debt seemed to be a free lunch when real interest rates were zero. Now it’s not, and it’s a very painful adjustment that neither political party in the US is willing to undertake.ref 2

~ Ken Rogoff

- They sent $200 billion to Ukraine, psychopathically arguing that replenishing our armaments will stimulate our economy. Bastiat strikes again. Why not just blow them up in the desert to save lives?

- The rapid rise in labor movements certainly won’t stop inflation. The ultimate irony is that the Fed will see rising wages of the strapped consumer as inflationary pressure and feel obliged to step on the economy.

How can you tell me it won’t lead to stagflation?

~ Jamie Dimon

After years of watching inflation lurking in the shadows obscured by deceptively flawed metrics, the Satanic Creature from Jekyll Island reared its ugly head. In the fall of 2019, a disturbingly well-timed white paper from Blackrock declared that the next crisis would require the Fed to use gain-of-function monetary policy by “going direct.”ref 3 Weeks later the repo market went emergent and began spasmodic 10% spikes for reasons unknown to us mortals. In 2020, Covid-19 arrived, and the Fed injected an estimated $17 trillion dollars into the system as part of the Fed-backed program requiring “14 days to flatten the economy.” They sprinkled small sums of money directly into consumers pockets while stuffing huge sums directly into corporate America. These gargantuan monetary suppositories jammed inflation directly up everybody’s asses. Go direct indeed. Without the Fed-funded backstop promised in some smokey backroom meeting, there would have been no lockdowns. Period. You are now free to blame the Fed for the catastrophic lockdown.

What has just happened is that the control of the supply of money has permanently left the hands of central bankers—the silent revolution…the supply of money will now be set, for the foreseeable future, by democratically elected politicians seeking re-election. It is time to embrace the silent revolution and the return of inflation long before such permanency is confirmed.

~ Russell Napier

The consumer converted their Covid Cash into binge spending. After running out of cash, credit cards were tapped. As credit runs dry the bear trap is clamping down on consumers ‘nads again. That might stop inflation, but then tax revenues will collapse as the economy stagnates, causing our 8% deficits to grow. It is not hard to see why the inflation hawks are despondent.

Twitter’s legendary Rudy Havenstein dredged up Wilhelm Röpke’s definition of inflation as “the way in which a national economy reacts to a continuous overstraining of its capacity…”ref 4 I too have come to some simple maxims about inflation that seem self evident:

- Inflation is government spending. Shrink government spending—what Albert Edwards calls “fiscal dysentery”—and you may solve the problem. The growth rate in America’s annual debt is twice the most optimistic growth rate of the GDP. The resulting inflation creates what Chris Whalen calls “the appearance of growth,”ref 5 and it is unsustainable.

We don’t have inflation because the people are living too well. We have inflation because the government is living too well.

~ Ronald Reagan

- There is little evidence that sovereigns can inflate their way out of serious debts. Mike Green calls it the “inflation trope.”ref 6 The US currently has upwards of $250 trillion of unfunded liabilities. A recent Treasury report (pp 193–194) signed by the flat-headed hobbit, Janet Yellen, reports the contribution from just Social Security and Medicare at $175 trillion,ref 7,8 which amounts to about $2 million per taxpayer. Flippant responses like, “They’ll just inflate it away” sound great until your accountant tells you that you have not budgeted for a $2 million loss of spending power. As the kids like to say, “OK, Boomer.” If you cannot grind your way out of this mess with economic growth—blocking and tackling—you default. This is not a trope.

The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists.

~ Ernest Hemingway, Esquire 1935

- There are few if any credible examples of inflating away sovereign debt without a default at the end. Oft-cited examples of the inflation trope like Weimar Germany that got us into WWII on one extreme and the post-WWII US debt remediation on the other extreme bookend the possibilities. The German debt remained after the hyperinflation destroyed their society because the debt was denominated in gold. By contrast, the US debt is said to have been financially repressed away through interest rates that were held way below the post-war inflation. Forget not, the US was in a post-war cycle of hypergrowth. My son gave me copies of Time and Life magazines from my birth date (April 25, 1955 if you are thinking of sending a gift.) Time was bloated with ads for smokestack industries, while Life was filled with consumer ads. We did it by blocking and tackling like all-pro linemen—by growing our economy. (Curiously, there were no cigarette ads.)

We, in our sluggishness, do not realize that the dearness of everything is the result of the cheapness of money. For prices increase and decrease according to the condition of the money. An excessive quantity of money should be avoided.

~ Copernicus

Israel’s large debt following the costly Yom Kippur War poses a curious case study. (Notice the recurring role of war in all these inflation stories.) Their inflation approached 450%, leading to a severe banking crisis in 1983. They did recover, however, and it is still unclear to me exactly how they massively devalued the Shekel and then wrestled control of the chaos in just a few years. I’m still on the learning curve on this one. Start with this Wikipedia entry.ref 9

- Inflation expectations are a profound risk. Reinhardt and Rogoff in This Time Is Different note that inflating away debt works until people start to notice and adjust for it. How long does it take people to notice prices are rising? Not long. Once the populace start budgeting for future price hikes by putting inflation corrections on union wage negotiations, building contracts, or any other future costs, the inflation has reverse-transcribed into society’s DNA. The Fed totally failed to respect this risk.

If you dismiss variables you assume are unimportant you miss the entire picture.

~ Stephen Coughlin, former NSA analyst

- Errors inherent to the inflation estimates undermine all other economic metrics. You have no clue if the GDP is even growing. I argue below that it is not. Price discovery fails. Markets fail. Society fails. Bad decisions become frequent and potentially catastrophic mistakes, all because the lights on our dashboard failed to give the correct signals.

Beware of little expenses: A small leak will sink a great ship.

~ Benjamin Franklin

- The Federal Reserve’s self-designated role is to intervene in the most important market underpinning capitalism—the market where borrowers and lenders haggle over the price of capital. A dozen unelected bureaucrats backed by hundreds of economists cloistered in their echo chamber believe that the market-driven price of capital must be wrong if it does not comport with their views. Imagine the chaos if the price of lunch at the restaurants across the nation were set on a daily basis by committee. During weak moments, I might cut the Fed some slack. Claims that the Treasury has taken over the Fed seem specious to me.ref 10 What power does the Fed have over Big Government’s penchant for spending? Well, for starters, they could call out the hyper-bloated Administrative State and politicians for their perpetual campaigning and grifting on our dime, but the Fed never does. The Fed’s mandate is to keep the currency stable: that means 0% inflation not 2%. Their second mandate brought on themselves is to optimize the economy. The third unstated mandate is to fund the Swamp.

It would have to be meaningful and get our attention and lead us to think that the labor market was significantly weakening for us to want to react to it. A couple of tenths in the unemployment rate would probably not do that.

~ Jerome Powell, Federal Reserve Chair, 5/1/24, on inflation

To Powell’s credit, the democrats in the Senate whined like little bitches for an election-year-motivated 75-basis-point cut in a letter to Powell, and he ignored them.ref 11 But then he gave them 50 basis points while paradoxically claiming policy was already loose and the economy was strong. Does he have a clue how retarded that sounds?

I am not seeing signs of resurgent inflation.

~ Neel Kashkari, President of the Minneapolis Fed

- Curbing inflation will require gifted and powerful leadership. So far I see no evidence of that nor does the now-apoplectic Stan Druckenmiller or Paul Tudor Jones. These two GOAT front runners are confident that the requisite belt-tightening and painful rehab is in our future. The IMF worries that US fiscal deficits and accompanying inflation pose “significant risks” for the global economy.ref 12 We will wake up in a ditch stewing in our own vomit having passed the failsafe point for voluntary action.

I think we could easily see 5–10% inflation in the next 4 or 5 years.

~ Stanley Druckenmiller

I think all roads lead to inflation.ref 13

~ Paul Tudor Jones

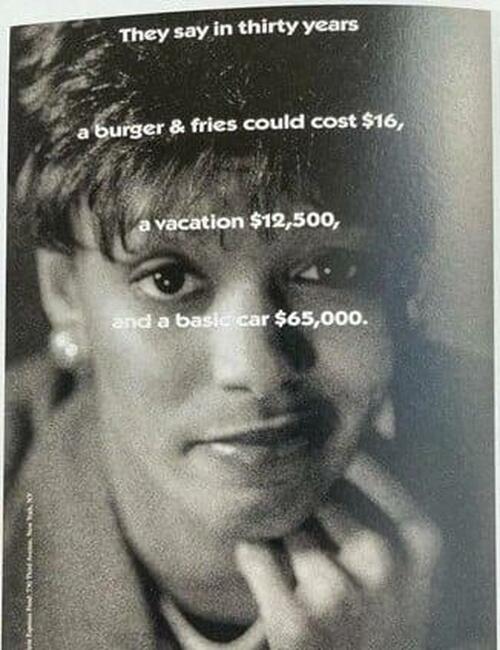

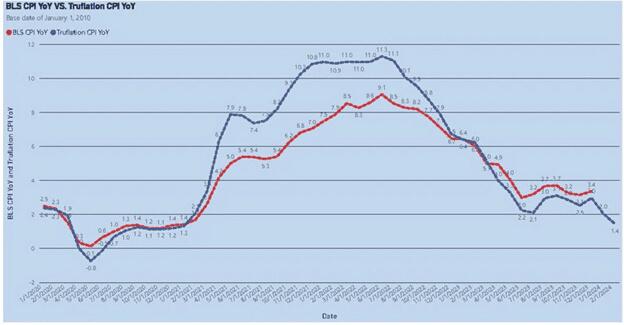

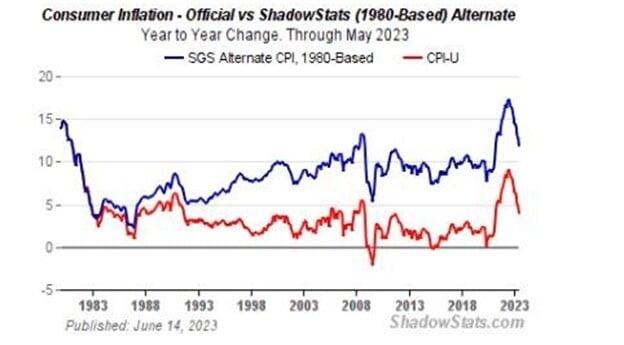

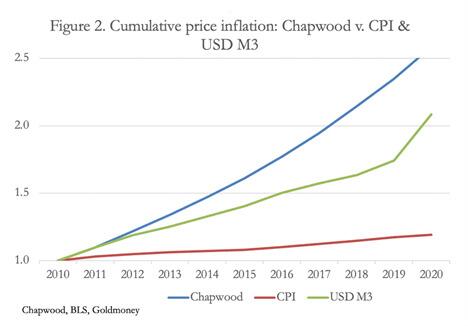

Price Hikes—Anecdotes. Although lacking in rigor and potentially deceptive, it is entertaining to consider anecdotal reports of inflation that attest to problems lurking in the plumbing. It is unlikely any readers can accrue anecdotes that support official inflation numbers in the 2.5–4.0% range incorporated into econometric models and then cited by bureaucrats.

- The Girl Scouts are cranking their annual membership fee from $25 to $85 (240%). “We can no longer afford to use our financial reserves, and we cannot pass through all escalating costs to our councils.”ref 14

- As measured in Ford F-150s, annual salaries have cut in half over the past five decades.ref 15 I’m sure they are cooler now.

- Auto insurance is up 56% since 2020.ref 16

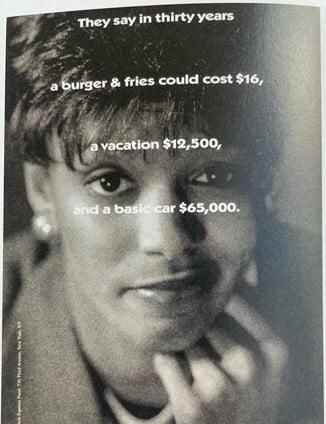

- A 1996 TIAA-CREF ad seems to understand the problem. The accuracy makes you wonder what they knew…

- Hookers charged $4400 per night in Davos. Consumers aren’t that interested in discussing those prices. There’s a lot of stimulus and liquidity…between the sheets.ref 17

- It is rumored that a chipped tail light requires replacement of the unit for $2,200.ref 18

- Robusta coffee beans are up over 300% since 2020.

- Fast food at the key chain drive-throughs has risen 75–100% over five years.ref 19 Taco Bell is unburdened by what has beans…(Sorry. Had to do it.)

- Florida’s largest insurer says it needs to raise its rates by 93%.ref 20 Must be climate change.

- Healthcare costs have risen an average of >6% compounded annualy over the past 25 yearsref 21 according to Statista despite officially reported CPI growth of only 2.6%.ref 22

- Official statistics claim health insurance has declined 30% over the last 2 years and 8% over the last 5 years.ref 23 Y’all think we are brain dead?

Inflation is getting pretty scary. We can’t make enough interest on our deposits to cover inflation. We are worried about how to keep increasing pay to our employees to offset inflation.ref 24

~ respondent to Dallas Fed survey

- Necessities at the commissary in prisons are measured in hours worked. A tube of toothpaste requires 10 hours of labor.ref 25

- Union membership and activity are near multi-decade lows, but the bulk of the public sees that as bad.ref 26 As a battle-hardened warrior opposing two graduate student unionization efforts, I say with angst that the return of labor is probably overdue.

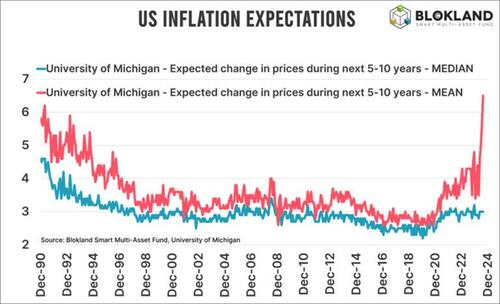

While Wall Street debates the rate of change of inflation, the average person lives its cumulative rise.ref 27

~ Peter Boockvar, Chief Investment Officer of Bleakley Financial Group