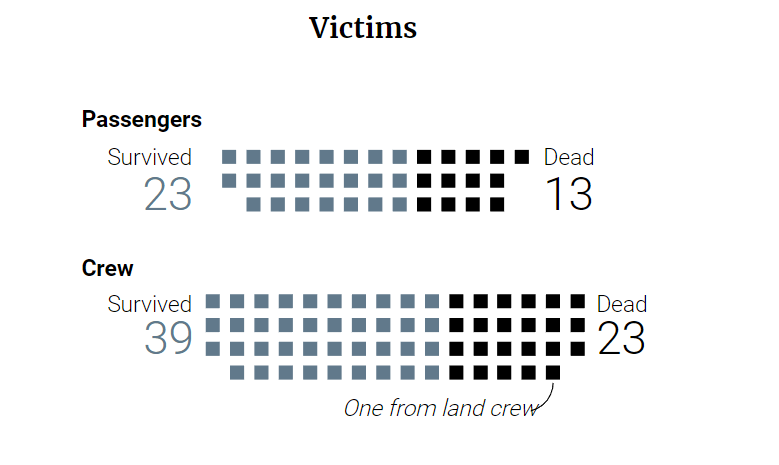

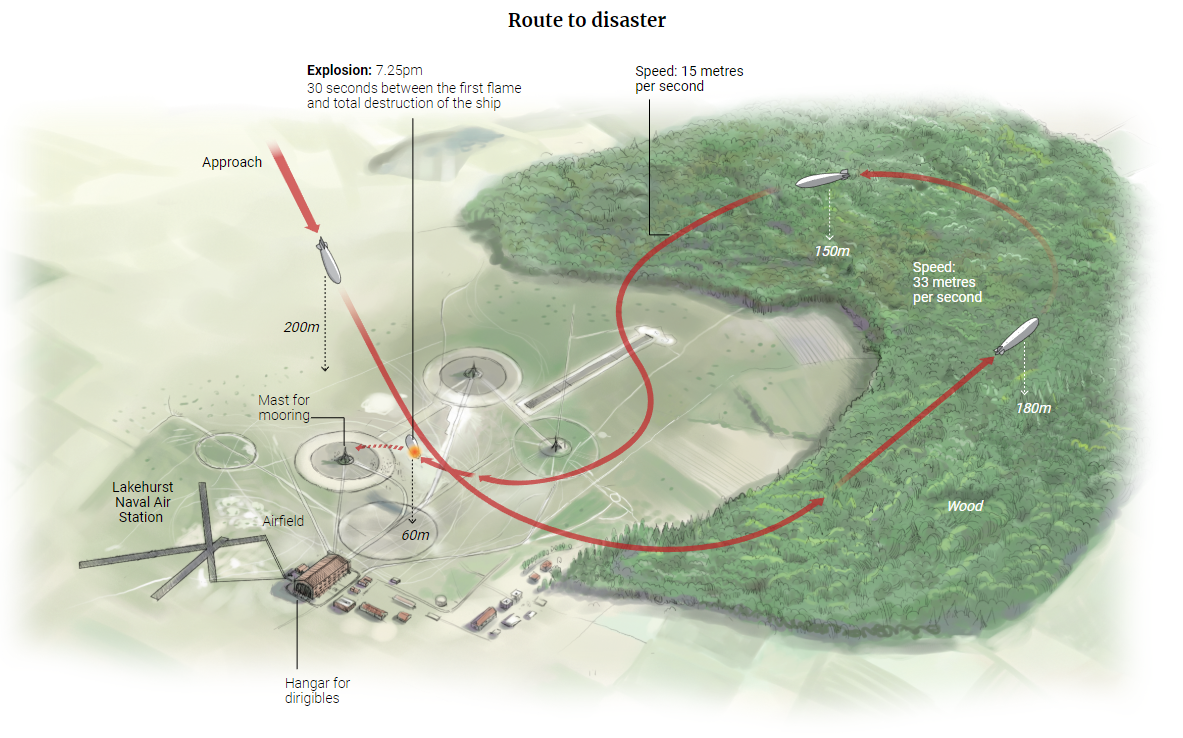

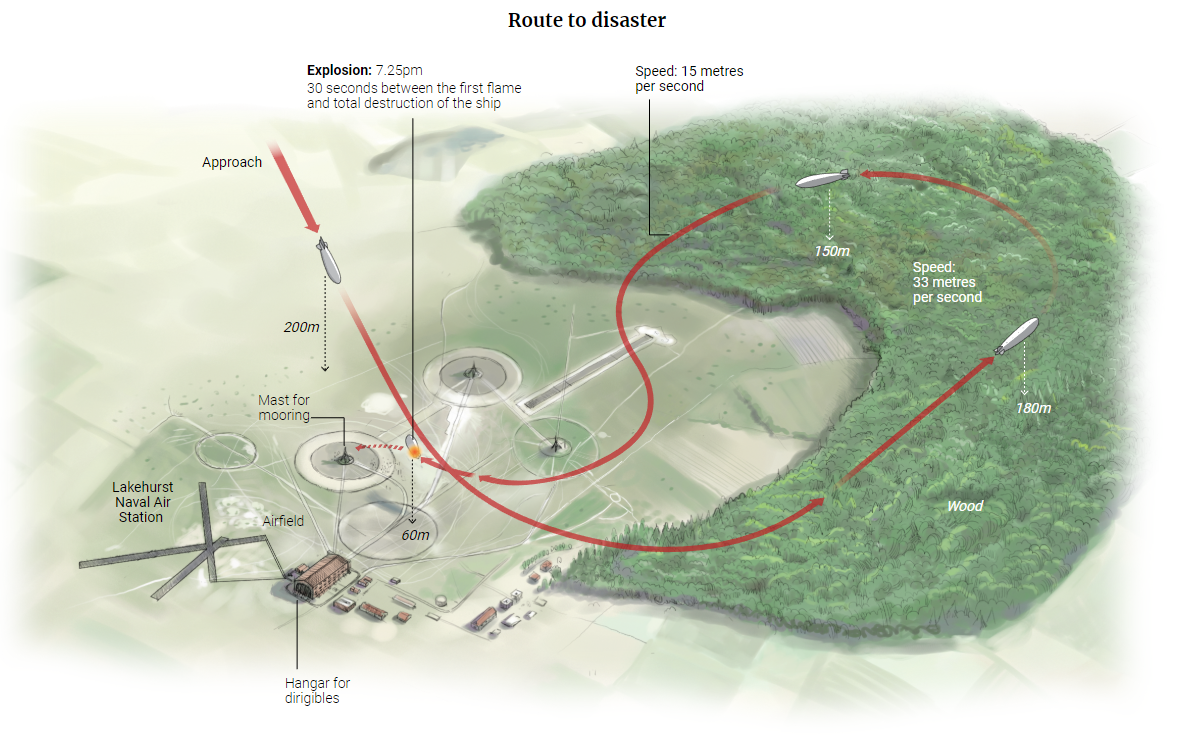

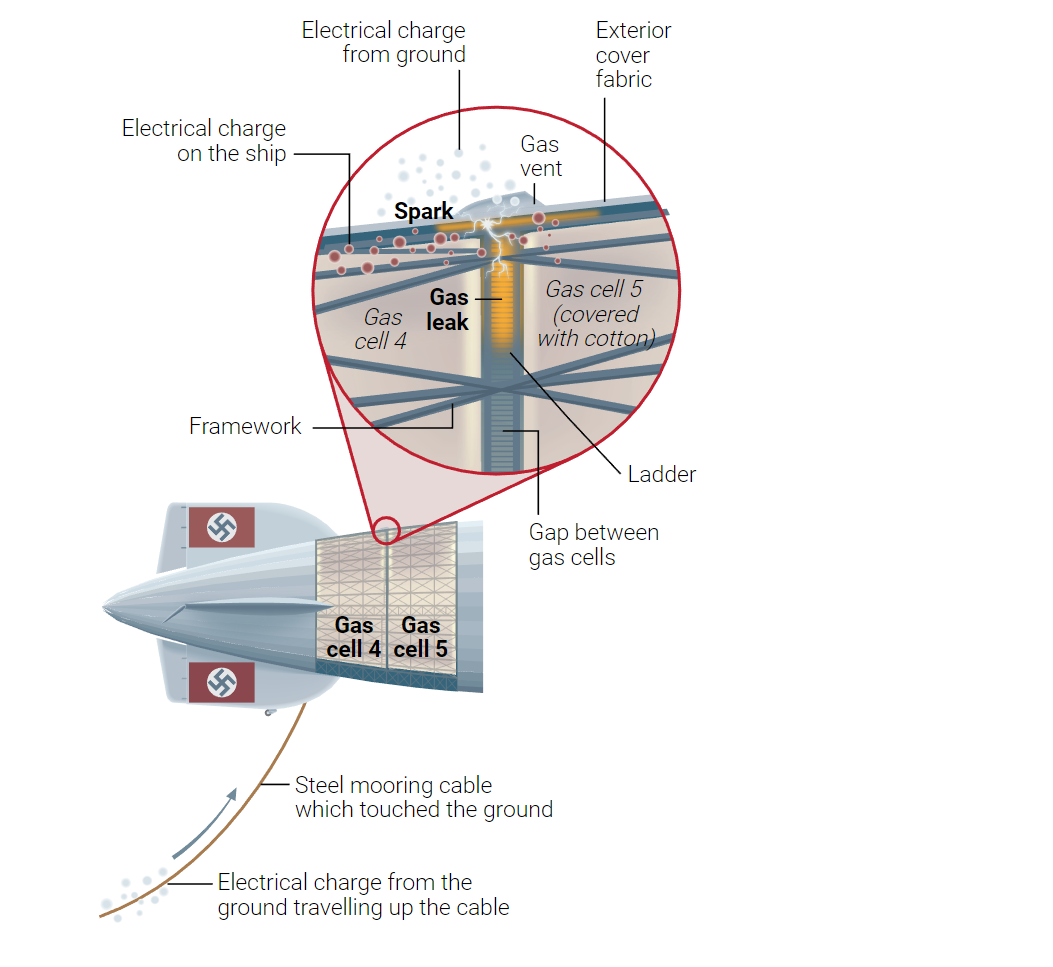

On May 6, 1937, the German airship LZ129 Hindenburg caught fire during its landing in Manchester Township, New Jersey, killing 36 people out of 97 total on board after departing from Frankfurt, Germany two days prior.

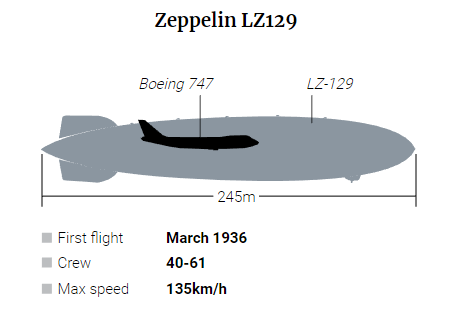

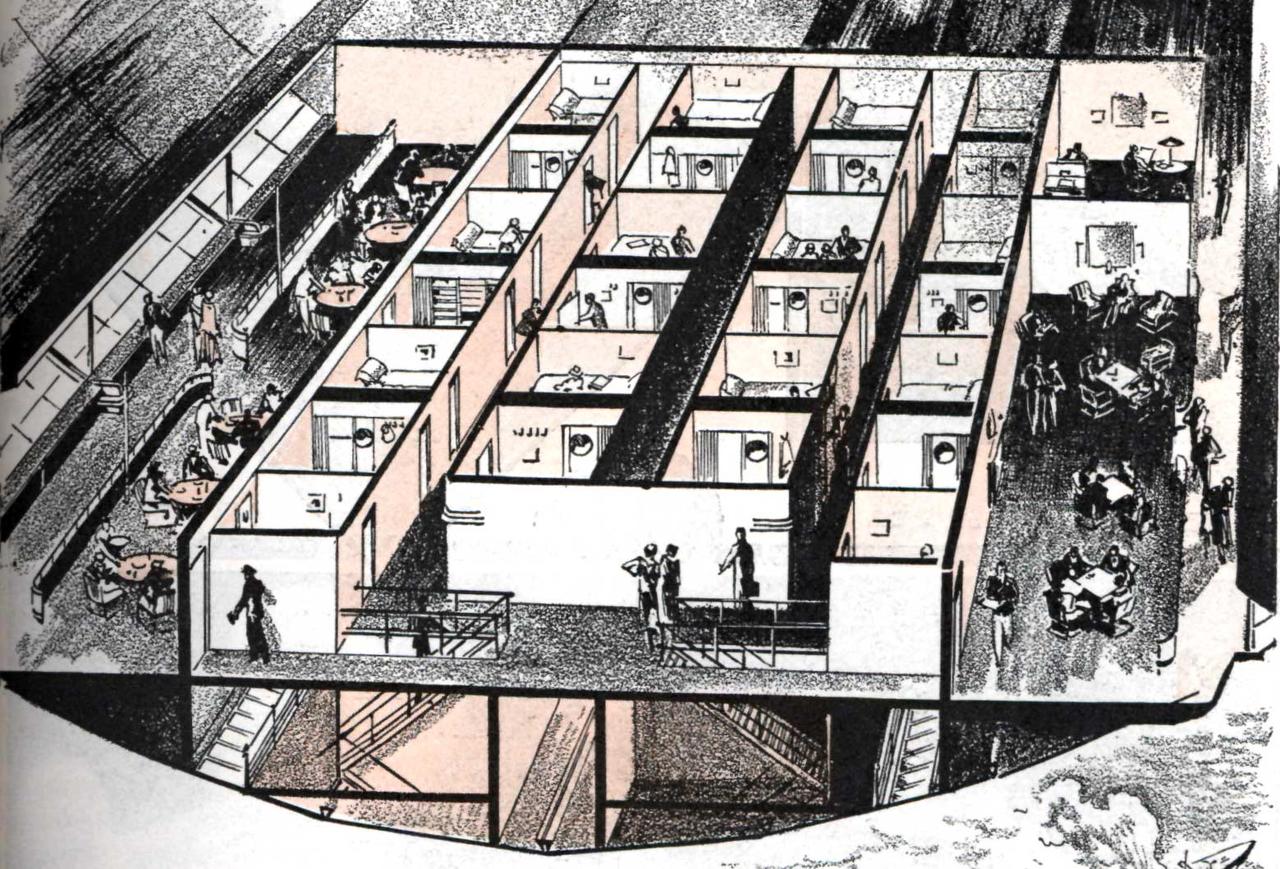

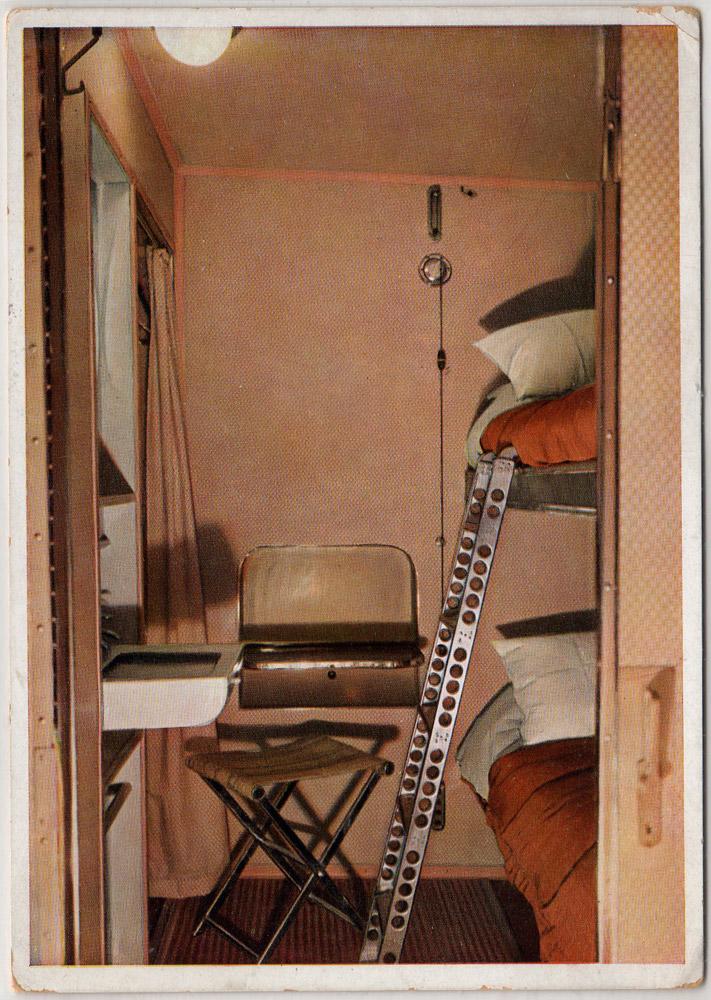

The Hindenburg was 803.8 feet long and weighed approximately 242 tons. It’s metal frame was filled with hydrogen, which was vented as the dirigible descended. It contained sleeping quarters, a dining area, a library and a lounge, and was able to cruise along at just over 80 miles per hour.

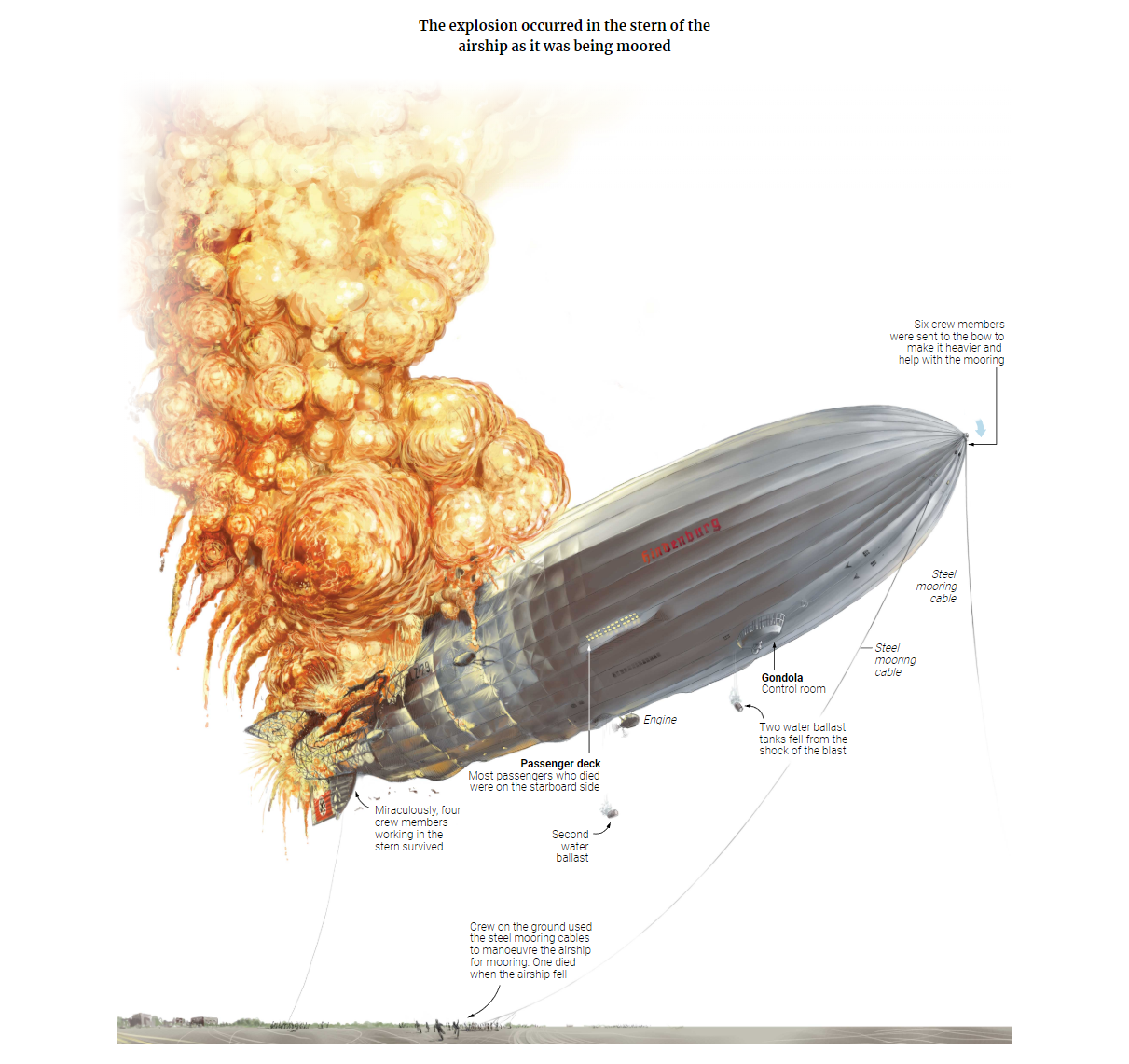

Once the Hindenburg caught fire, it rapidly spread throughout the dirigible’s gas cells until it was destroyed. The disaster at Naval Air Station Lakehurst, which was spectacularly caught on camera, marked the end of the rigid airship era of travel.

Via SCMP

While the newsreel footage was shot by Pathé News, Movietone News, Hearst News of the Day, and Paramount News – perhaps the most famous audio broadcast of the disaster was Herbert Morrison’s live radio report for WLS Chicago.

In Germany, media coverage of the disaster was suppressed – while newsreel footage was not released in the country until after World War II.

What brought it down?

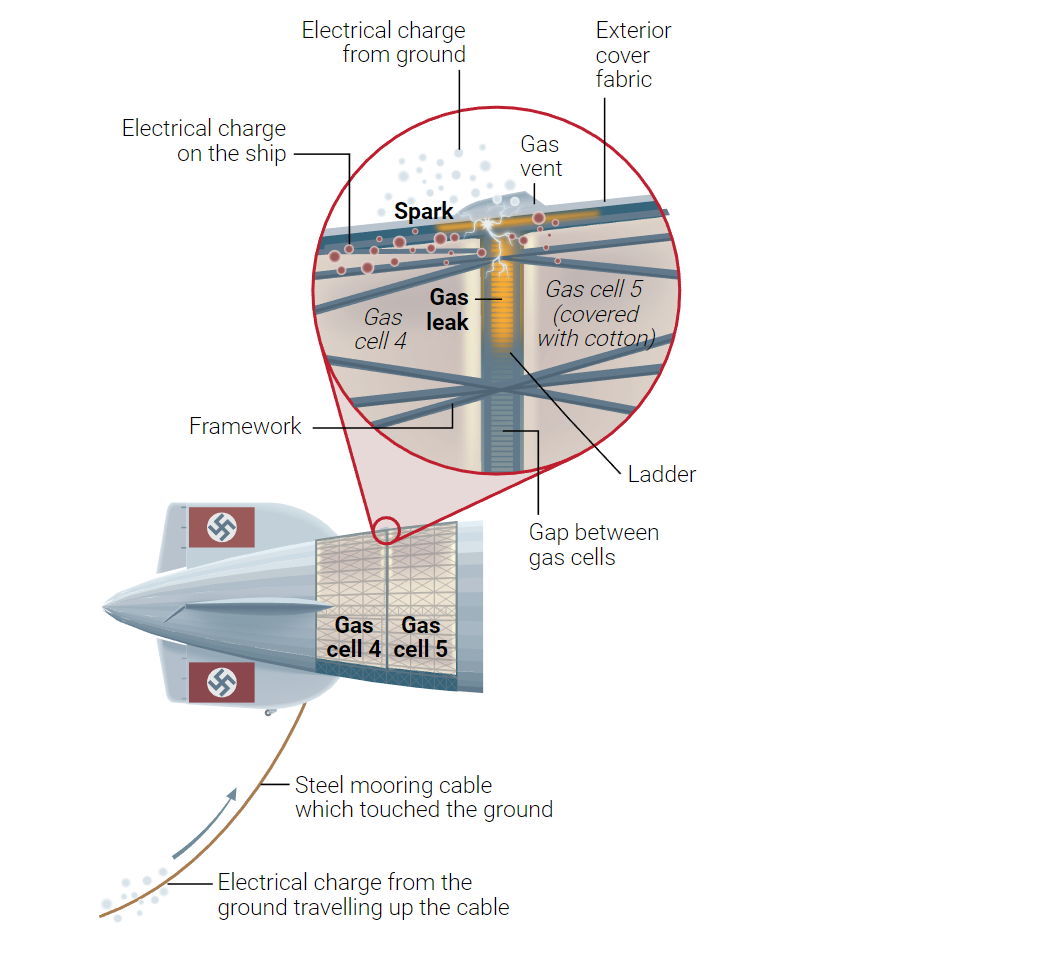

At the time of the catastrophe, the two most common theories as to what caused the fire were sabotage or a lightning strike as the dirigible vented gas upon approach. Hugo Eckener – former head of the Zeppelin Company, came to believe that static discharge was the cause.

Max Pruss, who commanded the Hindenburg throughout most of the airship’s career, told Columbia University in 1960 that it was likely sabotage – as early dirigible travel was safe, and they were frequently struck by lightning along the popular route between Germany and South America.

There’s an entire game of Clue’s worth of suspects who were onboard the Hindenburg before the crash – ranging from a German acrobat, to crew members, to a theory that Adolf Hitler himself gave the order.

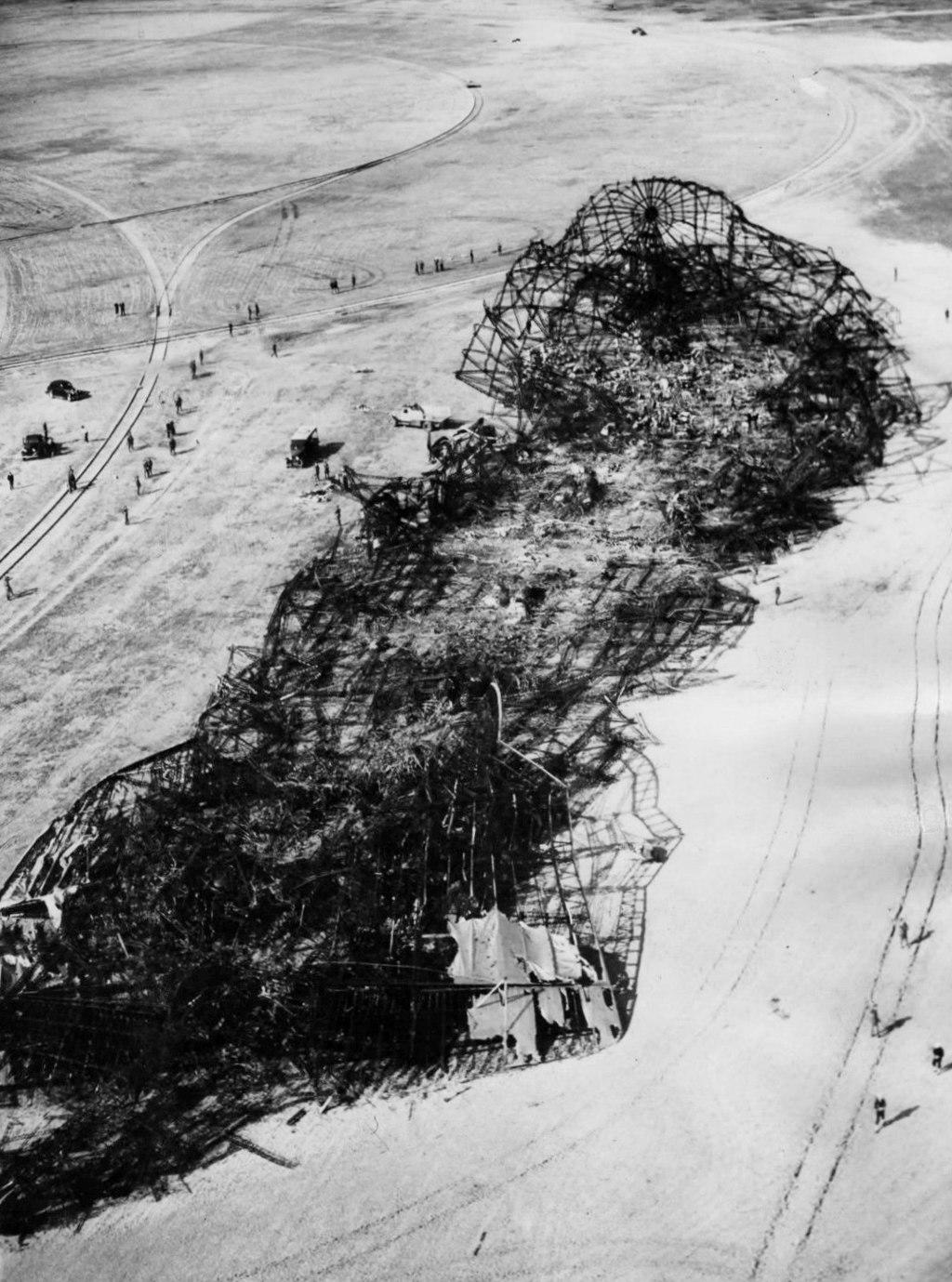

This is all that was left:

via ZeroHedge News http://bit.ly/2DS2J9I Tyler Durden

There was a note of caution among investors, business leaders and policymakers at this year’s Milken conference in California.

Despite near all-time highs in public markets and unemployment continuing to fall, investors were apprehensive. The rise of populism, trade tensions, inequality, tech disruption, or the $10 trillion of negative-yielding bonds in Europe and Japan are sowing seeds of doubt.

As we approach the longest U.S. expansion on record in July, the dominant topic for investors was how late in the economic cycle—and bull market—are we? Where are the vulnerabilities? And what does this mean for policies and portfolios?

Behind the scenes, I found three big themes with special relevance to finance.

1. The late-cycle investing playbook

How to position portfolios for late cycle investing was the biggest conversation in the corridors and private sessions.

Investors are casting their net for unappreciated secular growth which could outride a slowdown. The biggest hit was the focus on businesses geared to healthy eating and longevity. At a dinner of private equity investors, when I asked about their current favorite investment, over half were on health—from clean food ingredients to supplements to life sciences.

There is a growing focus on sustainability across all conversations. While the catalyst was often to better risk manage a concentrated portfolio, there is growing interest in measuring sustainable factors to help make better decisions.

But investors at Milken are also starting to buy some protection. For some this was a modest short position in parts of U.S. commercial real estate debt. For others it was looking to protect against potentially higher volatility in Europe.

2. Big Tech Versus Big Finance

There is a growing anxiety about how big banks will keep pace with big tech.

Financiers used to think that the post-crisis regulatory burden would make banking less appealing for new entrants. But increasingly they fear that non-banking rivals will target more profitable areas and skim the cream in areas such as payments or direct lending.

At Milken, financiers looked in awe at the scale and pace of innovation in combination with the large platforms networks. Take China’s Ant Financial which now has more than one billion customers across payments, investments and insurance without a single branch. Or closer to home Visa,PayPal and Mastercard , which have together created more value than the FAANGs [ Facebook , Apple , Amazon, Netflix and Google] in the last three years.

So the focus was, “How to catch up?”

It’s no longer “friend or foe” with fintechs and platforms anymore. I saw a big inflection as firms look to form partnerships and leverage platforms to help catch up on innovation.

Banks are stepping up their tech spending considerably. Many were surprised by the pace of cloud adoption in the US. One tech CEO said he expects nearly 50% growth in cloud usage by banks in the next 12 months as they want a better platform for innovation and borrow tech firms’ scale to invest. There will be rich seams of opportunities for to mine for tech firms across cloud, cyber and machine learning automation.

This said, despite seeing the success of large tech platforms or the Chinese financials, it was striking how few banks appeared to have an offense game plan to complement the defensive catch up.

3. The rise and rise of private assets

The rise and rise of private assets was a big theme.

At least $2.4tn was raised privately in the US in 2017 while $2.1 trillion was raised publicly, according to the Milken Institute. The thirst for yield, desire to access to fast growing companies and opportunities to disintermediate banks are bringing in even larger allocations. Fundraising for direct lending funds in the first quarter is already up 67% on 2018, according to Preqin, although Europe lags. The heady pace of growth is giving some pause for thought about the longer term implications for public markets and any collateral effects of persistent low rates.

But for the firms, the economics are clear: last year 43% of investment management fees already went to alternative managers, according to BCG. Given intense price deflation in exchange traded funds and core investment products as technology reshapes the sector, alternative assets are likely comprise more than half of all fees paid by investors even sooner than forecasters predict.

The Milken consensus is normally a much better barometer of markets than Davos. As I left, I asked an old friend for their takeaway from the conference. She said: “Invest with a little extra caution.”

via ZeroHedge News http://bit.ly/2DQTu9q Tyler Durden

Those curious who is more impacted by the sudden re-escalation in trade hostilities between the US and China can get a quick answer by looking at the market reaction to Sunday’s unexpected news: while the S&P is down barely 1%, overnight Chinese stocks plunged nearly 6%, their biggest drop in over three years, indicating just how much more sensitive to every twist and turn in trade relations Chinese stocks are.

Of course, one can counter just how smaller – and far less relevant – the Chinese stock market is in comparison to the S&P500, which is also the basis for the vast majority of household net worth for Americans, and global investors (whereas in China, it is the local housing that is far more critical and accounts for roughly 70% of household net worth).

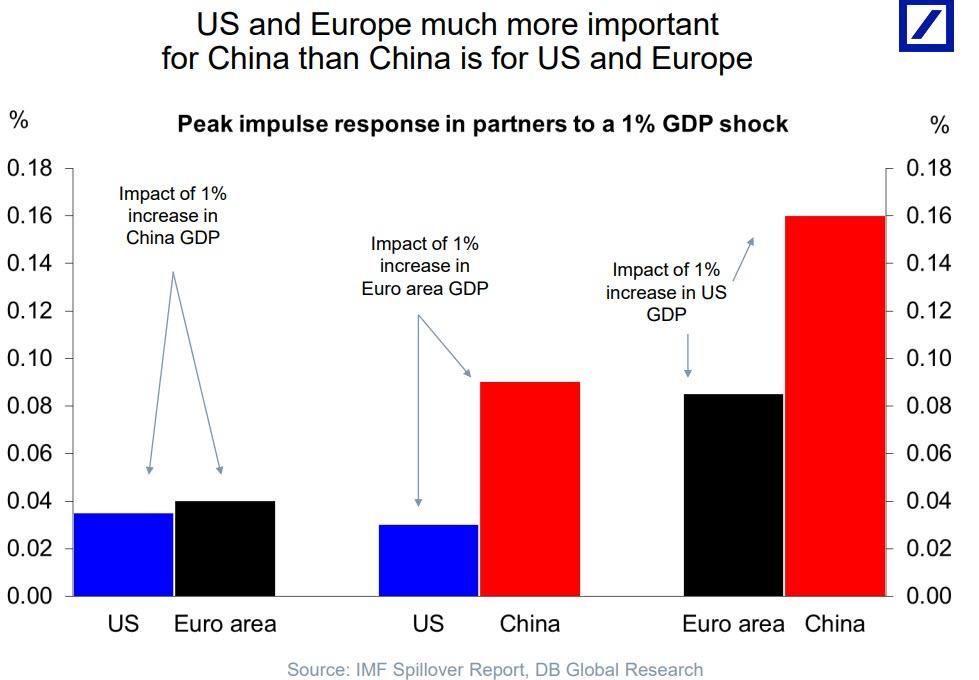

But it’s not just the stock market that shows why China should tread very lightly in its ongoing negotiations with Trump, or why the US president has decided suddenly to re-escalate. Below we lay out [ ] charts showing just why the US indeed continues to have the upper hand in negotiations with China, starting with the relative importance of the US and European economies to China rather than vice versa.

As the first chart below from Deutsche Bank shows, the US and Europe are “much more important for China than China is for US and Europe” as China remains the nation with the highest beta, or the highest relative impact, from a 1% move in either direction for either the US or the Euro area.

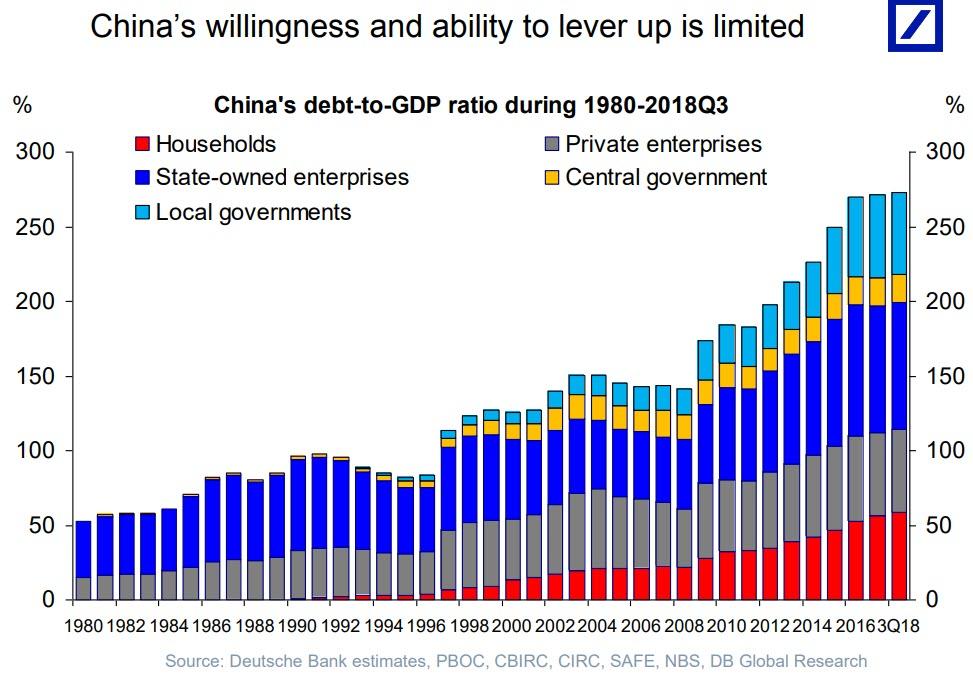

Second, whereas the US is now actively contemplating the launch of MMT, and exploding the US twin deficit by issuing virtually unlimited amounts of debt – which it ostensibly can do as long as the US Dollar is the world’s reserve currency – China is already near its leverage peak. In fact, as shown in the chart below, both China’s willingness and ability to lever up is now quite limited according to Deutsche Bank’s Torsten Slok.

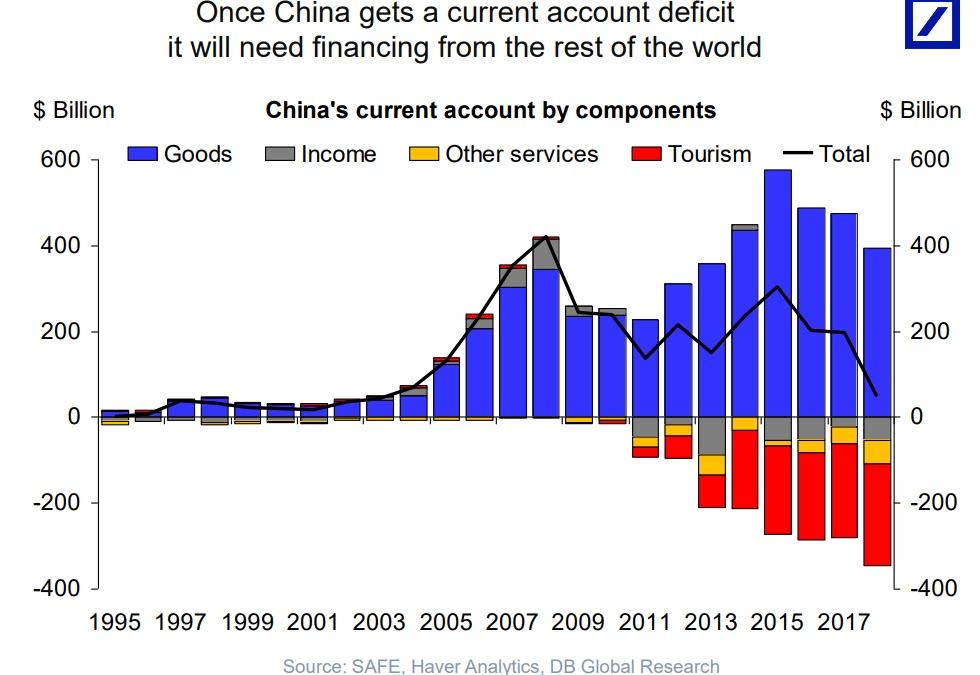

Last, and certainly not least, is what we said back in January represented a “tectonic shift” in China’s economy, when we observed that this year, for the first time in history, China’s current account deficit will turn negative meaning that China will henceforth need financing from the rest of the world, and specifically the US. Which is why, as we said five months ago, it is not Beijing that has leverage over the US, but rather the US whose ability – and desire – to allocate capital to China could mean all the difference for China’s economic growth, or lack thereof.

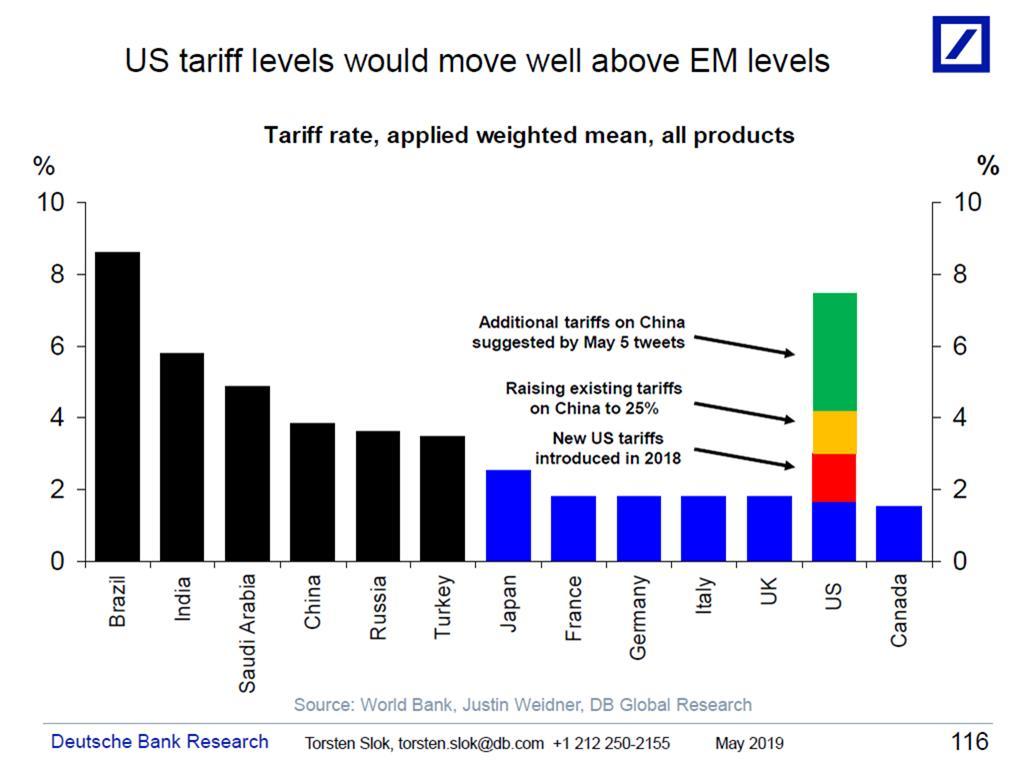

Finally, and tangentially, assuming trade talks collapse and Trump follows through on his threat of hiking taxes on Chinese imports, it would, as Torsten Slok shows in his latest chart, push US tariffs – which are already higher than most advanced economies – higher than many emerging market countries making the US one of the leading protectionist countries in the work.

That alone would cripple China’s economy, and is perhaps the main reason why Trump decided to once again flex his muscles, if so far only on twitter.

via ZeroHedge News http://bit.ly/2V3TxEP Tyler Durden

$7 trillion investment firm Fidelity will reportedly roll out bitcoin trading for institutional clients in the coming weeks, Bloomberg reported on May 6.

Citing a source who asked to remain anonymous, the publication revealed Fidelity’s cryptocurrency-focused spin-off, Fidelity Digital Assets, would be adding to the existing range of services.

The subsidiary launched in October 2018 and has offered cryptocurrency custody from March this year ahead of planned over-the-counter (OTC) trading.

Now, the trading side will go live for Fidelity’s users in as little as several weeks, the source said, and will primarily target large-volume traders like other OTC offerings.

While Fidelity itself did not confirm the time frame, the company hinted that its future direction would only involve more integration with the bitcoin space.

“We currently have a select set of clients we’re supporting on our platform,” spokeswoman Arlene Roberts told Bloomberg. She added:

“We will continue to roll out our services over the coming weeks and months based on our clients’ needs, jurisdictions, and other factors. Currently, our service offering is focused on Bitcoin.”

The report comes on the back of a survey Fidelity conducted last week that revealed consistent appetite for bitcoin among its target market.

Specifically, 22% of the over 400 institutional investors who responded said they already owned the cryptocurrency as part of their portfolio. Almost half were sympathetic to including it.

“More institutional investors are engaging with digital assets, either directly or through service providers, as the potential impact of blockchain technology on financial markets — new and old — becomes more readily apparent,” Fidelity Digital Assets president Tom Jessop commented in an accompanying press release.

via ZeroHedge News http://bit.ly/2J5tE5N Tyler Durden

Robert Mueller’s 448-page “Investigation into Russian Interference in the 2016 Presidential Election” contains at least two major omissions which suggest that the special counsel and his entire team of world-class Democrat attorneys are either utterly incompetent, or purposefully concealing major crimes committed against the Trump campaign and the American people.

First, according to The Federalist‘s Margot Cleveland (a former law clerk of nearly 25 years and instructor at the college of business at the University of Notre Dame) – the Mueller report fails to consider whether the dossier authored by former MI6 spy Christopher Steele was Russian disinformation, and Steele was not charged with lying to the FBI.

The Steele dossier, which consisted of a series of memorandum authored by the former MI6 spy, detailed intel purportedly provided by a variety of Vladimir Putin-connected sources. For instance, Steele identified Source A as “a senior Russian Foreign Ministry figure” who “confided that the Kremlin had been feeding Trump and his team valuable intelligence on his opponents, including Democratic presidential candidate Hillary Clinton.”

Other supposed sources identified in the dossier included: Source B, identified as “a former top-level Russian intelligence officer still active inside the Kremlin”; Source C, a “Senior Russian Financial Officer”; and Source G, “a Senior Kremlin Official.” –The Federalist

As Cleveland posits: “Given Mueller’s conclusion that no one connected to the Trump campaign colluded with Russia to interfere with the election, one of those two scenarios must be true—either Russia fed Steele disinformation or Steele lied to the FBI about his Russian sources.”

…Trump’s victory does not negate the reality that, assuming Steele truthfully relayed to the FBI and the media the intel his Russian sources provided, Russia interfered in the election by feeding Steele false intel about Trump.

Yet in the special counsel report, Mueller identified only two principal ways Russia interfered in the 2016 presidential election: “First, a Russian entity carried out a social media campaign that favored presidential candidate Donald J. Trump and disparaged presidential candidate Hillary Clinton. Second, a Russian intelligence service conducted computer-intrusion operations against entities, employees, and volunteers working on the Clinton Campaign and then released stolen documents.”

Surely, a plot by Kremlin-connected individuals to feed a known FBI source—Steele had helped the FBI uncover an international soccer bribery scandal—false claims that the Trump campaign was colluding with Russia would qualify as a “principal way” in which Russia interfered in the 2016 presidential election. The Russia social media campaign to disparage Hillary Clinton wasn’t a patch on the plot the Kremlin launched to destroy Trump: It resulted not only in bad press, but also an investigation into the Trump campaign and the use of court-approved surveillance exposing campaign communiques.

Even though Mueller was authorized, as he put it in the special counsel report, to investigate “the Russian government’s efforts to interfere in the 2016 presidential election,” the report is silent of efforts to investigate Russia’s role in feeding Steele misinformation. –The Federalist

Meanwhile, the only lawmaker to even mention this possibility has been Sen. Chuck Grassley (R-IA), who raised the issue with Attorney General William Barr last week:

“My question,” said Grassley, “Mueller spent over two years and 30 million dollars investigating Russia interference in the election. In order for a full accounting of Russia interference attempts, shouldn’t the special counsel have considered whether the Steele dossier was part of a Russian disinformation and interfere campaign?“

Barr replied that he had yet to “go through the full scope of [Mueller’s] investigation to determine whether he did address or look at all into those issues,” but that he would “try to assemble all the existing information out there about it, not only for the Hill investigations and the OIG, but also to see what the Special Counsel looked into. So I really couldn’t say what he looked into.”

Meanwhile, Barr said that he has assembled a DOJ team to examine Mueller’s investigation, findings, and whether the spying conducted by the FBI against the Trump campaign in 2016 was improper.

Mueller’s second major oversight – which we have touched on repeatedly – is the special counsel’s portrayal of Maltese professor Joseph Mifsud was a Russian agent – when available evidence suggests he may have been a Western agent.

Weeks after returning from Moscow, Mifsud – a self-described Clinton Foundation member – ‘seeded’ the rumor that Russia had ‘dirt’ on Hillary Clinton with Trump campaign adviser George Papadopoulos on April 26, 2016, according to the Mueller report.

As Rep. Devin Nunes (R-CA) noted on Fox News on Sunday, “how is it that we spend 30-plus-million dollars on this, as taxpayers and they can’t even tell us who Joseph Mifsud is?”

“…this is important, because, in the Mueller dossier, they use a fake news story to describe Mifsud. In one of those stories, they cherry- pick it,” Nunes added.

BARTIROMO: Then he’s working for Trump. So how come somebody from Britain, Australia, Italy, they’re all reaching out to him? And, by the way, how come this London Center of International Law reached out to Papadopoulos on LinkedIn to go work there, after Ben Carson withdrew?

NUNES: And I think a better question is, is that — so, Papadopoulos claims that he was quitting this London Center.

So how many companies or agencies that you know of, when you say, hey, I’m quitting, and they say, hey, what about a free four-to-five-day vacation in Rome? We’re going to fly you there. We’re going to put you up for free. We’re going to give you food… And all you have to do is meet this guy Mifsud, right… We’re trying to get to the bottom of Mifsud. So, as we talked about it on the last segment, this guy originates the investigation. We know that the Mueller team wrote this Mueller dossier. They used a lot of these news stories that, in fact, sometimes were generated by leaks from the FBI.

Now, I don’t think the American people expect 20 DOJ lawyers and 40 FBI agents to write a 450-page report that’s built off of news stories that in many cases they generated.

Why I particularly have a problem with this is — with one of the stories is because they pick a news story, and then they cherry-pick from it. So they use it partly to describe where Mifsud worked, but then they fail to say in that same story that they have given support to by using it in the Mueller dossier, they cherry-pick it. -Via RealClearPolitics

As conservative commentator and former US Secret Service agent Dan Bongino notes of Mifsud, “either we have a Russian asset who’s infiltrated the highest echelons of friendly Intelligence Services, or we have a friendly who was setting up George Papadopoulos.”

“So either we have a Russian asset who’s infiltrated the highest echelons of friendly Intelligence Services, or we have a friendly who was setting up @GeorgePapa19 – That’s the real scandal. This was not spying, this was entrapment.” pic.twitter.com/wGnV8HHur1

Perhaps Mueller’s reportedly scheduled testimony next week will shed more light on why he failed to question the possible role of Russian disinformation with the Steele Dossier, and why he didn’t flush out who Joseph Mifsud really is.

via ZeroHedge News http://bit.ly/2vFZ6yO Tyler Durden

Wells Fargo is reportedly in talks to hire Bridgewater Associates co-CEO Eileen Murray – one of the most powerful women on Wall Street, if not the most powerful – to take the open CEO job, according to WSJ. If the bank succeeds in recruiting Murray, it would both fulfill Charlie Munger’s and Warren Buffett’s urging to hire its next CEO from outside the Wall Street banking milieu, while also potentially neutralizing the bank’s arch-nemesis, Elizabeth Warren, who has successfully scalped the bank’s last two leaders.

Wells, which is still subject to a cap on its balance sheet imposed by the Fed and is still reeling from its infamous cross-selling scandal – where an ‘insane incentives regime’, as Munger described it during a Monday morning interview on CNBC, inspired branch managers to open millions of fraudulent accounts – as well as a string of other abuses, has been searching for a new CEO since Tim Sloan abruptly quit in March after Warren demanded he resign during a Congressional hearing.

Per WSJ, Murray has had conversations with several people inside the firm about leaving – in keeping with Bridgewater’s ‘radical transparency’ ethos, she has been fully forthcoming – though the prospect of her departure has reportedly filled her co-CEO David McCormick with dread.

In a sign of just how exhausting Bridgewater’s culture can be, WSJ reports that Murray has grown ‘weary’ of leading the world’s largest hedge fund, and has discussed jumping ship several times in the recent past. Companies with which she has reportedly been in talks with include Uber, MetLife, BNY Mellon and Northern Trust, among others. Even Murrray, one of Bridgewater’s top executives, has shared that according to the firm’s internal ranking system she has scored high on creativity, but poorly on organization.

Wells is still in the early stages of its CEO search, but Murray’s background would make her an ideal candidate. In addition to being a powerful woman on Wall Street, Murray boasts an inspiring rags-to-riches background, having grown up one of nine children in a NYC public housing project. She majored in accounting at Manhattan College before embarking on a storied Wall Street career.

Murray has increasingly taken on duties like meeting with top clients as Bridgewater founder Ray Dalio has shifted his focus to promoting his books and – oh yeah – trying to save the American capitalist system from itself.

Should Murray jump ship, Dalio might once again need to step in and help steer the firm on a day-to-day basis, something he was forced to do a few years back after another leadership shakeup.

via ZeroHedge News http://bit.ly/2DUPSDv Tyler Durden

Now that the market has digested the initial shock following Trump’s surprise threat to raise the 10% tariff on $200BN of Chinese goods to 25% on May 10 in what BofA has called a “major escalation”, traders and investors are focusing on three follow up questions: i) why did Trump do what he did, ii) is he serious and iii) is the possibility for a trade deal with China now dead?

First, looking ahead, RaboBank’s Michael Every writes this morning that Trump’s pivot “puts chief negotiator Liu He in a very awkward position. While it may be Trump’s style to be impulsive in the final stages of a deal, the Chinese government will lose face if they cave in to his demands following a public threat on Twitter. It could be perceived as a breach of trust and the Chinese may conclude that the US have been negotiating in bad faith after all. But only when they decide to walk away and announce their retaliation, will we truly know Trump’s intentions. Is he really willing to cancel trade talks, and to put the recent rally of his beloved stock market at risk? And this with just 18 months left before the US elections? Or will he somehow regain control over his emotional intelligence and still find a way around this strong 10 May deadline?”

So while the future remains murky, and the ball is now in China’s court, a better answer may come from analyzing another, just as important question: how did we get here in the first place? According to BofA, the answer is that “economic and market strength has reduced both sides’ incentives to compromise.“

And while that may sound intuitive, when policy is very responsive to markets, the policy/markets equilibrium can be elusive. The result is increased volatility.

So what to expect? Below is the latest primer from Bank of America’s global economist Aditya Bhave, explaining “what happened to the trade deal” and what to expect next.

Countercyclical protectionism

Soon after the Xi-Trump summit in Buenos Aires last December, we highlighted an interesting relationship between policy and markets. At the time we argued that weaker markets were pushing policymakers towards a more benign outcome on trade. But we flagged the risk of an extended period of uncertainty: if the markets started to price a positive outcome, the urgency to reach a deal would reduce.

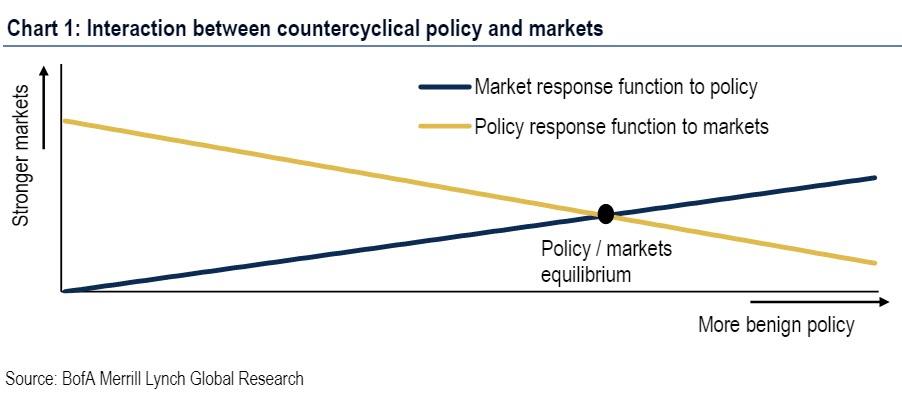

Now, with the S&P 500 basically at its all-time high, President Trump has unexpectedly threatened to increase the tariffs against China on Friday (May 10). This is the most significant escalation of the US-China trade war to date. We take this opportunity to explore our theory in more detail. The interaction between trade policy and markets shown in Chart 1 below is conceptually similar to countercyclical traditional (fiscal or monetary) policy, with policy measures mitigating shocks in either direction.

But there are two key differences:

First, traditional policy typically responds primarily to economic shocks. By contrast the current US administration has been very sensitive to the markets. We think this could lead to more frequent policy shifts because markets are more volatile than the underlying economy.

Second, the markets understand the traditional policy response function and price it in before the fact. But if countercyclical policy shocks are not fully anticipated, as has arguably been the case with trade policy, very responsive policy increases market volatility. We show that in this case markets and policy tend to spiral away from equilibrium until the markets learn to internalize the policy response function.

The immediate market response suggests that the latest escalation of the trade war was a complete surprise to investors. This means that markets could be in for a bumpy ride before a trade deal is reached.

Detour ahead?

We have been calling for a benign outcome on the US-China trade war. Our view has been that a full-blown trade war would be avoided because pain in the markets, the economy and in public opinion polls would force policymakers to compromise. But importantly this sort of pain is not just sufficient to incentivize a trade deal, it is also necessary. This is why our mantra has been “no pain, no deal.” The implication is that there are likely to be speed bumps along the path to an agreement: improvements in market sentiment or economic fundamentals might prompt policymakers to dig their heels in and negotiate harder.

The latest news might not just be a speed bump. If President Trump acts on his threat to raise the 10% tariff on $200bn of Chinese goods to 25%, that would represent a detour, at the very least. There are several reasons why the threatened tariff increase would be the most significant escalation of the trade war to date.

First, assuming no FX or price adjustments, it would amount to an additional $30bn tax on US consumers and firms, representing the largest single round of tariff increases since the trade war began.

Second, this round of tariffs includes more consumer goods-nearly a quarter-than prior rounds, which focused more on capital and intermediate goods.

Finally, it will be difficult for currency markets to offset the effect of the latest threatened tariffs. FX has been playing the role of shock absorber in the trade war: when the trade war looked to be getting worse last fall, the renminbi was down nearly 9% against the US dollar.

This move almost negated the effect of the 10% tariffs. Since then news of reconciliation has caused the currency to appreciate. With Chinese policymakers looking to prevent large currency moves, we think it is highly unlikely that they would allow the renminbi to depreciate enough to offset a 25% tariff.

Why the sudden escalation of tensions while negotiations are ongoing? President Trump cited the lack of sufficient progress in trade talks. The latest threat is undoubtedly an attempt to speed up negotiations, and perhaps to extract more compromises out of China, which so far does not appear to have conceded ground on any major issues. But it is hardly a coincidence that the threat comes with equity markets around their all-time highs and with the Fed having taken a very dovish turn. The markets are now better buffered than they were last fall against a negative surprise on trade. Equally we would not be surprised if Chinese negotiators have hardened their stance in response to improved domestic data.

A simple framework

Here we develop a simple framework to explore the relationship between policy and markets. In Chart 1, the upward-sloping line is the market response to policy: the markets respond positively to benign policy and negatively to less friendly policy. The downward-sloping line is the policy response to markets. Weak markets motivate friendly policy and strong markets do the opposite. Markets and policy are in equilibrium where the two lines cross.

This framework is not entirely new. It is conceptually similar to traditional countercyclical monetary and fiscal policymaking. For example, markets are stronger when they expect a dovish Fed, but strong markets (and a strong underlying economy) tend to make the Fed more hawkish. But there are a couple of important differences between traditional countercyclical policy and countercyclical protectionism.

The first is that monetary and fiscal policy are typically more responsive to economic fundamentals than market gyrations. Since the markets are more volatile than economic data, traditional policy does not change course very often. By contrast, the current US administration appears to keep a close eye on the markets. This results in more frequent swings in trade policy. As an aside it is somewhat ironic that trade policy has become countercyclical after a large procyclical tax cut and a somewhat procyclical turn in monetary policy.

The second difference between current trade policy and standard monetary policy is that the latter is well understood by the markets and gets priced in before the fact. For example, equity markets respond positively to good economic news, but there is also some financial tightening because rates increase in anticipation of a more hawkish Fed.

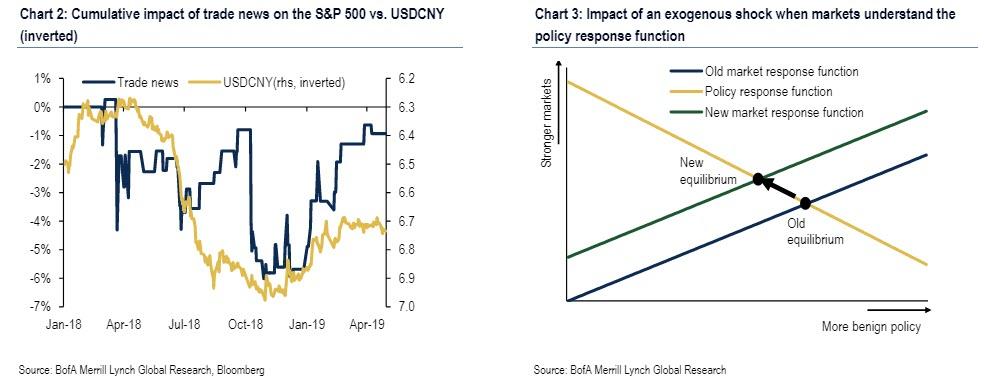

Chart 3 below shows the impact of a positive exogenous shock. For example, the recent upside surprise in Euro area GDP has likely moved the market response function upwards: for a given policy stance, the markets will be stronger than they would have been if the Euro area data had been softer. A countercyclical policy response to the exogenous shock implies slightly tighter / less-market-friendly policy. If the markets understand the policy response function, they will converge quickly to the new equilibrium, with stronger markets despite less friendly policy.

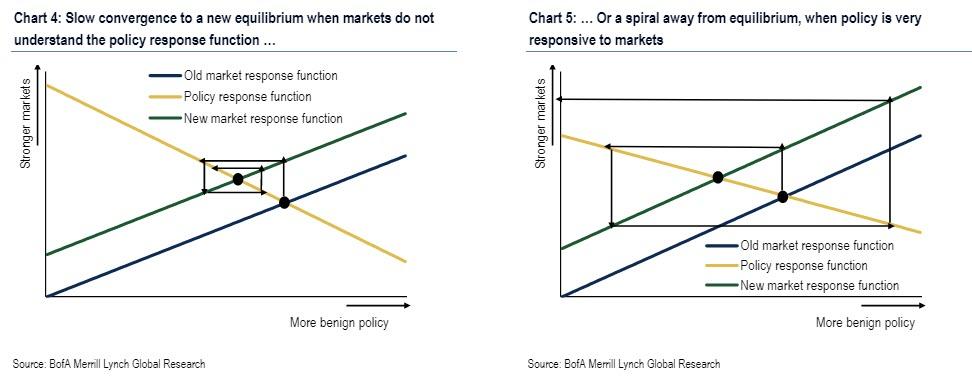

What if the markets do not understand how policymakers will respond? Then Chart 4 shows in our view how the new equilibrium might be reached. Stronger markets lead to less friendly policy, which weakens the markets, which leads to more benign policy, and so on. In other words, markets will gyrate on the path to the new equilibrium.

But there is an even more concerning possibility. What if, instead of converging to a new equilibrium, markets and policy spiral away from it, as in Chart 5? That is, what if each move in the markets causes an increasingly larger policy response, and vice versa? In that case we think market volatility will be exaggerated, and equilibrium will only be reached when the markets “learn” the policy response function.

The difference between Chart 4 and Chart 5 is the responsiveness of the policy function. It is precisely when policy is very responsive to markets that we might spiral away from equilibrium instead of converging to it.

Fasten your seatbelt and don’t hold your breath.

What does our framework say about the outlook? The good news is that the markets seem to be coming to grips with the US administration’s policy response function. That is arguably why markets were volatile last year but have been less responsive to news out of Washington, good or bad, in recent months.

The bad news is that the latest escalation of the trade war was completely unexpected, despite the strength of the economy and the markets. This is evident from the immediate negative reaction of US equity futures to the news. However we cannot rule out the possibility that President Trump does not plan to act on his threat, which might have been made simply to raise the profile of an imminent deal. It is also possible (though very unlikely in our view) that China will suddenly make a major compromise, triggering a deal and precluding the tariff hike. However, given that trade policy has proven to be even more responsive to the markets than was generally believed, our framework makes a strong case against complacency. We believe we might be in for a long, bumpy ride before a trade deal is finally reached.

Source: BofA

via ZeroHedge News http://bit.ly/2Jj6kB2 Tyler Durden

After a week of street demonstrations that left four dead and hundreds injured, the Venezuelan people are growing weary of opposition leader Juan Guaido’s attempts to win military support for an ant-Maduro insurrection.

And that weariness started to show this weekend, when many questioned the wisdom of returning to the streets on Saturday when Guaido called for another day of street protests, according to the FT. On Twitter, many of Guaido’s supporters slammed him for offering up the Venezuelan people as “cannon fodder.”

Perhaps sensing the waning support for his campaign, Guaido told the BBC in an interview Monday that he was considering asking the US for support in the form of a boots-on-the-ground military intervention. Speaking to the BBC’s Nick Bryant, he said he would “evaluate all options” to finally depose Maduro, while the US has hinted that it “all options are still on the table,” hinting that an invasion of Venezuela remained a possibility.

Guaido’s intensifying rhetoric makes sense considering his efforts to convince members of the military to defect have been largely unsuccessful, and even his own supporters are now accusing him of “fighting bullets with whistles and placards.”

“When are you going to march until? Enough!,” tweeted Nangel Medina, a graphic designer from hard-hit Zulia state in the west of the country. “People have already protested and the world knows that we’re in the majority but we’re fighting bullets with whistles and placards.” “Stop offering us up as cannon fodder and making martyrs out of us in vain,” added María Hernández, another of Mr Guaidó’s 2m twitter followers. “We need concrete actions.”

But Guaido thanked the US and President Trump for the “decisive” support, in what might be an attempt to butter up the US, even after Trump on Friday spoke with Vladimir Putin and claimed that Russia isn’t trying to interfere in Venezuela.

“I think President [Donald] Trump’s position is very firm, which we appreciate, as does the entire world,” he said.

Saturday’s march, as Guaido envisioned it, was supposed to win over the military as peaceful demonstrators had planned to hand over copies of a letter reminding the military of their constitutional duties to the Venezuelan people. But fearing violent retribution, few citizens followed through.

Instead, many battle-weary Venezuelans took advantage of the time to stock up on supplies as some complained about the military and government-backed militias taking the fight to the housing complexes where many poor Venezuelans live.

“These haven’t been easy days and things are still tense,” said 62-year-old Magaly Uzcátegui as she shopped for fruit and vegetables at a market in the El Paraíso district of the capital. “It was brutal this week. The military police fired a lot of shots. In the tower block where I live loads of windows were broken and the colectivos [motorbike gangs that support the government] turned up. We’re just surviving.” “We don’t know what’s going to happen next,” added 54-year-old Rafael Rojas as he queued to buy tomatoes. “It’s out of our hands.”

To be sure, Guaido might have another motive in ratcheting up his calls for US military intervention: Following the three days of street clashes last week, where Guaido appeared outside a military base in Caracas flanked by defectors, it appears the Venezuelan government might finally be preparing to arrest him, despite the US’s implicit threats that it would treat Guaido’s arrest as an unprecedented provocation.

The military largely stood firm behind Mr Maduro, who said he had defeated a coup attempt orchestrated by the US. On Friday, his chief prosecutor Tarek William Saab said he had issued 18 arrest warrants for “civilian and military conspirators”. Until now, the government has refrained from arresting Mr Guaidó. Washington has said it will act swiftly and firmly if it does and insists that “all options remain on the table”, including military intervention.

Since last week’s riots, Maduro has been making the rounds, visiting military bases and thanking cadets and officers for their continued support since Guaido first declared himself the legitimate ruler of Venezuela back in January, a claim that has been recognized by more than 50 countries.

Then again, as Ron Paul recently pointed out, it’s certainly possible that Guaido might be worth more to the US dead than alive.

via ZeroHedge News http://bit.ly/2Vm6MWj Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}