After February’s surprising slowdown, US factory orders were expected to rebound in March and rebound they did.

US factory orders had fallen for 4 of the last 5 months ahead of today’s March data but against expectations of a 1.6% rise, order spiked 1.9% MoM – the most since Aug 2018…

On a year-over-year basis, US Factory Orders hovered at 2.0% YoY – near the weakest since Nov 2016

Core factory orders also rose in March (up 0.8% MoM) – the best since April 2018 – as non-defense capital goods shot up 6.5% MoM with Transportanation durable goods orders up 7.0% MoM.

Is this the inventory build that spiked Q1 GDP? And, as Jay Powell might ask “is is transitory?”

Following the publication of his ‘capitalist manifesto’ where he called for drastic reforms of the American capitalist system to redistribute wealth and resources more equitably – something he followed up with an unprecedented $100 million donation to the public schools in his home state of Connecticut, putting his money where his mouth is, so to speak – Ray Dalio’s self-published LinkedIn essays have been garnering a lot more attention. It probably didn’t hurt that Dalio’s essay appeared to set off a wave of wealthy capitalists talking about how “capitalism is broken”, placing him at the forefront of a trend that could have profound implications for American politics as Wall Street struggles to confront the rise of populism on the right and the left.

And so it is that late on Wednesday, Dalio published a follow-up where he expanded on a proposal that, as we noted at the time, sounded suspiciously similar to Modern Monetary Theory.

This time around, Dalio argued that, whether we like it or not, the US will eventually be forced to embrace MMT, this has become “inevitable,” he said. Central banking as we know it (which, thanks to rampant money printing in the post-crisis paradigm, has already moved closer to the MMTers ideal) is doomed to eventually collapse under its own weight and unpopularity. In other words, sooner or later, the people will demand MMT, once inequality gets bad enough.

Once the public has accepted that money printing and interest-rate cuts aren’t doing enough to distribute wealth more equally (as we’ve pointed out many times, the Fed’s unprecedented post-crisis easing has been the primary driver in the expansion of economic inequality that Dalio finds so troubling), policy makers will be forced to accept “monetary policy 3” – or MMT.

To me the most important engineering puzzle policy makers around the world have to solve for the years ahead is how to get the economic machine to produce economic well-being for most people when monetary policy does not work. I don’t mean that monetary policy won’t work at all; I mean that it won’t work hardly at all in stimulating economic prosperity in the ways that we are used to having it stimulate economic activity, which are through interest rate cuts (what I call Monetary Policy 1) and through quantitative easing (what I call Monetary Policy 2). That is because it won’t be effective in producing money and credit growth (i.e., spending power) and it won’t be effective in getting it in the hands of most people to increase their productivity and prosperity. Hence I believe we will have to go to Monetary Policy 3, which is fiscal and monetary policy coordination that is of a form that we haven’t seen before in our lifetimes but has existed in various forms in others’ lifetimes or faraway places. It is inevitable that this shift will happen because it is inevitable that central bankers will want to ease when interest rates are pinned at 0% and when quantitative easing will be ineffective in achieving the goal. I recently refreshed my prior exploration of past cases and future possibilities of such coordination, which I will share below.

In the policy prescriptions he introduced during his previous essays, Dalio recommended a closer collaboration between fiscal policy and monetary policy. Now, he’s taken that a step further and advocated placing the monetary policy reins into the hands of elected officials (one of the key tenents of MMT).

For what it’s worth, Dalio acknowledges that this could present a conflict, and that if we embrace MMT, it will need to be done in a way that limits the control of politicians to enact self-serving policies (something that, as far as we can tell, would be extremely difficult)

The big risk of this approach arises from the risks of putting the power to create and allocate money, credit, and spending in the hands of politically elected policy makers. In my opinion, for these MP3 policies to work well, the system would have to be engineered in a way that decision making would be in the hands of wise, not politically motivated, and highly skilled people. It’s difficult to imagine how the system will be built to achieve that. At the same time it is inevitable that we are headed in this direction.

Ultimately, Dalio would favor a version of MMT with automated policy prescriptions to control taxes and stimulus depending on what’s happening with the business cycle, to limit the influence of politics (effectively marrying MMT with a kind of hybrid Taylor Rule).

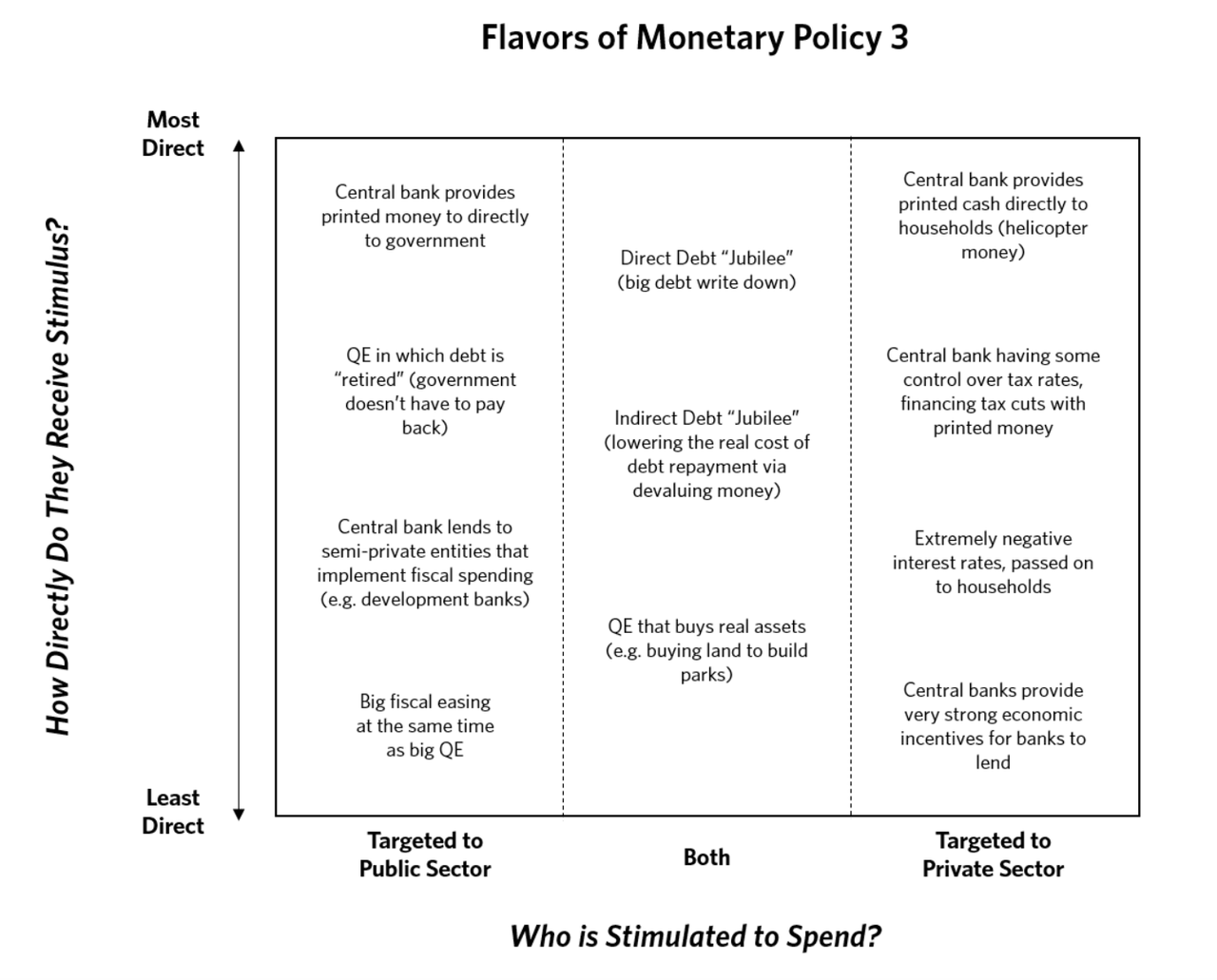

For anyone who is unfamiliar with MMT, Dalio created this handy chart to explain the different ‘flavors’ of the policy.

Of course, Dalio isn’t the only Wall Street luminary to come out in favor of MMT. But will he stick to his guns after the inevitable backlash? Or will he eventually change his mind like Carl Icahn?

via ZeroHedge News http://bit.ly/2Vaai6i Tyler Durden

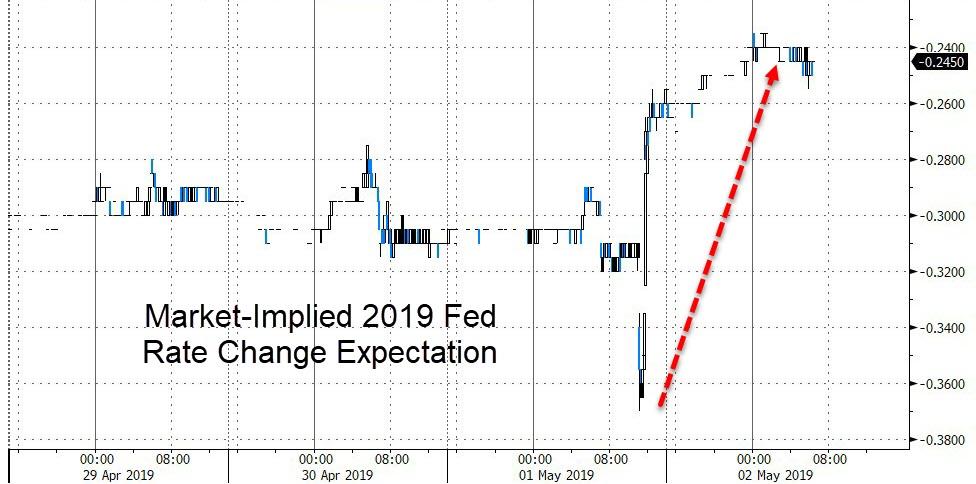

A “transitorily” hawkish Fed, which saw the market’s Fed rate change expectations tighten by 13bps, has prompted dollar gains and sparked selling in the precious metals.

And as the dollar rallied, gold sank…

Holding (for the second time in just over a week) at its 200DMA…

At the same time, Silver has dropped to its lowest since 12/3/18…

via ZeroHedge News http://bit.ly/2PIMHn8 Tyler Durden

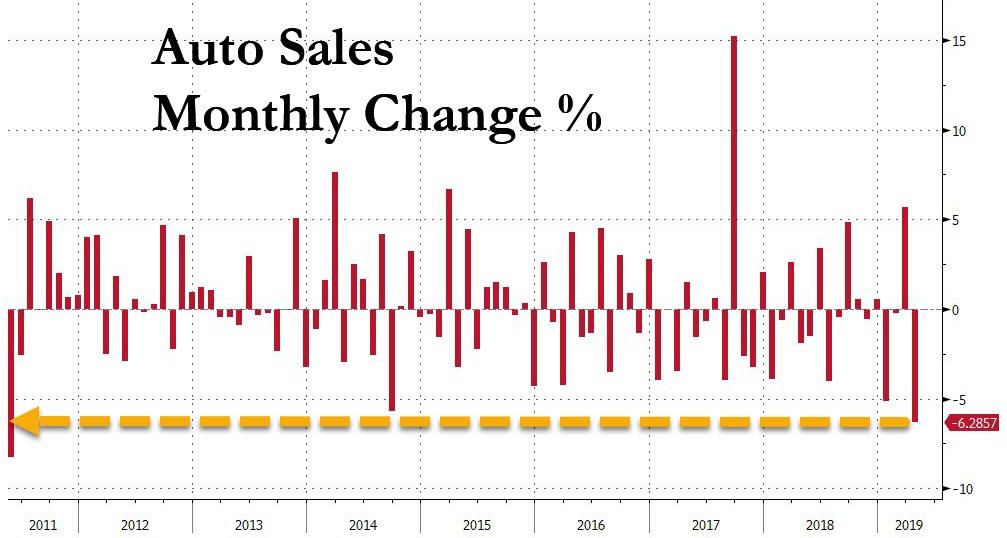

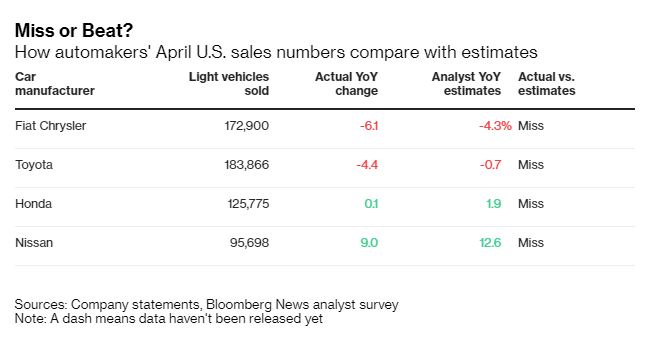

It was yet another dismal month for US auto sales in April, continuing a recessionary trend that has been in place not only in the US, but globally, for the better part of the last 12 months and certainly since the beginning of 2019. The nonsense-excuse-du jour for this month’s disappointing numbers is being placed on the weatheron seasonality on rising car prices, which easily pushed away an overextended, broke and debt-laden U.S. consumer.

In a nutshell, US auto sales in April tumbled by 6.1% – the biggest monthly drop since May 2011 – to just 16.4 million units, the lowest since October 2014. Aside for an incentive-boost driven rebound in March, every month of 2019 has seen a decline in the number of annualized auto sales. Furthermore, as David Rosenberg notes, the -4.3% Y/Y trend is the weakest it has been for the past 8 years.

Adding “fuel to the fire”, the average price of a new car in April came in at $36,720, the highest ASP so far this year, according to The Detroit News. It comes at a time where interest rates remain above 6% on average, further pressuring sales.

Edmunds analyst Jessica Caldwell said: “April sales were a bit dampened by the harsh financing conditions we’ve been seeing in the new-car market. Shoppers are really starting to feel the pinch as prices continue to creep up and interest rates loom at post-recession highs.”

Brian Irwin, Accenture Plc’s managing director for North American automotive, said simply: “We are disappointed with how sales turned out.”

Across the board, almost all major names missed estimates, especially as passenger vehicle sales continued to collapse. Nissan was the one manufacturer that was able to buck the trend for the month. Some additional details, according to Bloomberg:

Ford’s U.S. sales fell 4.7 percent, according to Automotive News. That was steeper than the 4 percent drop predicted by analysts. The Ford brand fell 4.7 percent, while Lincoln dropped 6.2 percent, the publication reported.

Fiat Chrysler deliveries fell 6.1 percent, its third straight monthly U.S. sales decline. Chrysler sales fell 37% while Dodge slipped 24%. FCA’s Fiat brand saw a 34% dip in sales last month while Alfa Romeo was down 14%.

Honda eked out a gain of 0.1 percent, as the new Passport sport utility vehicle helps offset declines for cars including the Accord sedan. Honda’s passenger car sales fell 2.4%, driven down by an 11.5% drop in Accord deliveries.

Toyota sales fell 4.4 percent, while the Corolla sedan saw a 32.8% drop in deliveries and its Camry fell 2.1%.

Nissan, whose total sales rose 9 percent, credited cut-rate financing offers with helping boost its redesigned Altima sedan in April, and the automaker is expanding that program to its Rogue SUV this month.

Nissan’s success came from offering a better rate, proving that much of what is keeping the consumer away has been a financial burden. Billy Hayes, a division vice president for Nissan North America, said: “Offering a special rate has done well for us.”

On top those poor results, another one of Detroit’s “Big Three” has said that it will no longer be reporting sales on a monthly basis. FCA said Wednesday it will switch to quarterly sales reports, following the lead of both Ford and General Motors. It said it would begin quarterly reports on October 1 and will provide monthly reports up until that time.

FCA’s Chief Communications Officer Niel Golightly said: “A quarterly sales reporting cadence will continue to provide transparency of our sales results while at the same time aligning with where industry practice is heading.”

More transparency from less reporting – got it. We’re sure it has nothing to do with the fact that FCA’s year-to-date sales are down 4%.

FCA’s U.S Head of Sales Reid Bigland, who has been making excuses for the automaker’s sluggish sales all year, said: “April marks the start of the spring selling season and we anticipate strong consumer spending as we move through May. The industry may be shaking off the first-quarter sluggishness, but shoppers are coming into showrooms and buying.”

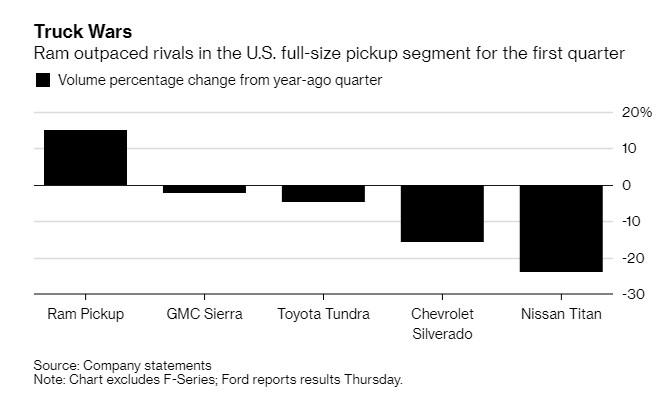

FCA’s Ram truck brand was one of the only six brands to post an increase in sales last month, up 25%. The Ram pickup posted a 25% gain with 49,106 units sold and is up 22% for the year. Jeep sales were lower by 8% in April, catalyzed by a 25% drop in Wrangler sales and a 13% drop in Cherokee sales. Ram had also bucked the trend last month:

And it’s no coincidence that the biggest failsafe for auto sellers – fleet sales – which can sometimes allow sellers to stuff the channel to meet numbers, have finally cooled.

Zo Rahim, an analyst for Cox Automotive said: “Fleet sales in April appear to have cooled from their impressive run in the first quarter. With overall sales down and fleet moderating, softness in vehicle sales still stems from weakness in the retail market. Affordability concerns coupled with attractive supply in the used-vehicle market might suggest retail sales might not bottom out for the foreseeable future.”

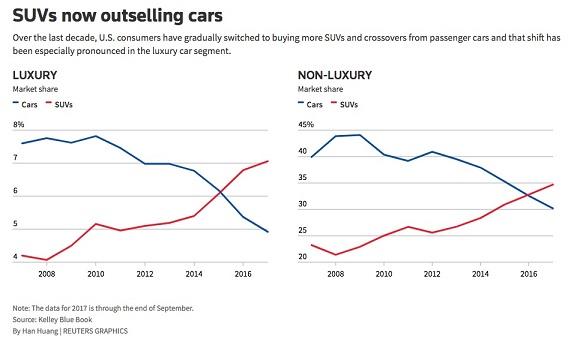

In February, auto sales plunged to 18 month lows as SUV demand hit a brick wall. SUVs were, until this February, one of the sole remaining bright spots in the rapidly slowing U.S. auto market. Despite the fact that they were crippling traditional sedan sales, Americans’ transition to SUVs was seen as a silver lining, prompting many automakers to make infrastructure changes to account for the change in demand. That silver lining looks to have all but completely disappeared at this point.

In January, auto companies set the tone for the year, starting 2019 just as miserably as 2018 ended, with major double digit plunges in sales from manufacturers like Nissan and Daimler.

via ZeroHedge News http://bit.ly/2DLi0J4 Tyler Durden

The further we get from her historic electoral defeat at the hands of President Trump, the more unhinged Hillary Clinton becomes.

Case it point: it appears the former secretary of state has moved on from endlessly blaming everybody but herself and her campaign staff for the many miscalculations made along the way (many have joked that Clinton probably couldn’t point out Wisconsin on a map), to actively soliciting enemies of the US to interfere on behalf of the Democrats in 2020.

Of course, there’s still plenty of evidence that Russia did exactly that back in 2016 (this thread was explored in more detail during AG Barr’s Wednesday hearing before the Senate Judiciary Committee).

But that didn’t stop Clinton from publicly asking China to step in and give the Democrats a boost against Trump during the 2020 race during an appearance on – where else? – the Rachel Maddow Show. Specifically, she asked the Chinese to steal Trump’s tax returns, which the Democrats have been having more trouble obtaining than they had probably expected.

“Imagine, Rachel, that you had one of the Democratic nominees for 2020 on your show, and that person said, you know, the only other adversary of ours who is anywhere near as good as the Russians is China,” Clinton told Maddow. “So why should Russia have all the fun? And since Russia is clearly backing Republicans, why don’t we ask China to back us?”

“And not only that, China, if you’re listening, why don’t you get Trump’s tax returns?” I’m sure our media would richly reward you.”

Clinton, clearly sore about Mueller’s findings, said China’s interference (which, according to the Trump administration, is already happening) could be part of a ‘great power contest’.

“Let’s have a great power contest, and let’s get the Chinese in on the side of somebody else,” she added. “Just saying, that shows how absurd the situation we find ourselves in.”

She added that the No. 1 thing she learned from reading the Mueller report was that the Russians interfered in the 2016 race to boost Trump, and that they haven’t been held accountable (that is, except for all the sanctions, and the indictments and the…well, you know).

Asked for her thoughts on the Barr hearing, Clinton said she thought Democrats on the Senate Judiciary Committee did a “good job” exposing Barr as “the president’s defense lawyer” (note: WSJ’s editorial board has offered plenty of evidence to the contrary).

“I think that the Democrats on the committee did a good job today in exposing that he is the president’s defense lawyer,” Clinton said. “He is not the attorney general of the United States in the way that he has conducted himself.”

Of course, Clinton’s comments were intentionally meant to mimic Trump’s now-famous campaign-era ‘joke’ that Russia steal Clinton’s missing emails and hand them over to the Republicans.

We now wait for Clinton to clarify that she, too, was ‘just kidding.’

via ZeroHedge News http://bit.ly/2Ja322P Tyler Durden

“If you can walk away, it’s a good landing. If you can use the airplane the next day, it’s an outstanding landing!”

What’s not to like about current markets?

A strong US economy – the strength of last week’s 3.2% growth rate data will likely be bolstered by a strong Jobs number tomorrow and ongoing solid economic releases through this month.

A US President determined to pump-prime an economic boom ahead of election year – who will do anything to avoid a downturn.

Theresa May finally doing something decisive and sacking a minster for indiscipline might suggest political firmness on the way, and maybe even a deal with Labour on Brexit?

A compliant(ish) Fed showing no sign of tightening policy. (Some analysts put it another way – the Fed rejecting Trump by not cutting rates…)

The same Fed perceiving no concerns on inflation, painting a picture of a US economy on a “healthy path”.

Signals Trump wants the China Trade deal signed asap – and even prepared to “compromise” on the key content – could provide another market booster.

US Oil production reaching record levels.

Apple surging 5% – despite falling sales – because it announced another stock buyback. (See link to a very interesting Bloomberg note on Apple’s failure to fill the looming iPhone “crater”.)

Maybe global trade is not a bad as we feared – has anyone noticed the Baltic Dry Index (an index showing global shipping costs) is up 54% in the last month?

Second quarter corporate results were expected to be poor – lower because of the global trade fracas and overstretched. Instead they’d generally been stronger than expected, hinting at a much firmer base.

Q2 Reporting across the Tech sector – the sector many think most vulnerable to a correction – has been solid. Aside from Alphabet’s lacklustre numbers, most Tech did well. Facebook was supposed to be the one that would cost us all dear because of on-going privacy issues and regulation. Nope. FB has seen a massive gain!

All in all, its not a bad picture. Economic growth, low rates, strong corporate performance, global trade not dead, and smiles all round. Or is it a bit complacent? I reckon the rosy picture I’ve painted above is somewhat distorted – it’s a dangerous reflection of deeper underlying issues with markets.

I am concerned about the bond market. Why? Because in the bond market lies the truth.

It’s very difficult to invest sensibly in the bond market at present. Rates remain distortedly low. Much of Europe is back in negative yield territory. US rates have not normalised either. Its an investment truth you can’t survive on 2.5% 10-year Treasury Yields, and corporate bond yields at spreads so tight they don’t properly reflect risk. Treasuries are supposed to be the zero-risk rate – but when the discount rate they provide is simply wrong, then it effects every other investment – distorting the risk/return equation.

Fixed Income Investors are left with the option of idiosyncratic plays – looking for value in thin illiquid markets. Over the past few days I’ve been speaking to clients about a whole raft of bond ideas to generate above market returns, but it’s difficult to focus on making 6% by taking extremely clever and complex synthetic European Sov risk when the stock market is touching new highs each and every day.

There are smart bond market plays out there – but overall markets seem focused on yield tourism again. When bond rates are too low to care about, money is looking for unconstrained returns that can’t be found in the dull boring predictable bond markets. When bond yields are so artificially low and stock prices look to have another leg up, then it difficult to ignore them!

Remember Blain’s Market Mantra no 1: “The Markets only objective is to inflict the maximum amount of pain on the maximum amount of participants.” Feels to me its setting itself up to catch as many bond market refugees as possible, and fleece them in stocks…

Call me Cassandra, but I don’t think this ends well..

One interesting snippet to note.. I note Warren Buffet has made a big bet on Dubai property (which is down 25% in last few years..) What does he know that we don’t? We’ve been talking about the likelihood of increased volatility and potential instability in the region, rather than it finding a firm base.. Hmmm. Must consider foundations in sand.

via ZeroHedge News http://bit.ly/2GXbqzY Tyler Durden

Good news America – productivity is surging at its fastest rate in nine years

Bad news America – it’s on the back of lower labor costs

Theoretically, they are close to the mirror of one another in a stable world (a rise in one necessarily means the inverse in another) and US productivity in Q1 soared 3.6% QoQ – the biggest QoQ rise since Q3 2014

Driven by the fact that Unit labor costs fell 0.9% in 1Q vs. up 2.5% prior quarter (Output rose 4.1% in 1Q vs. up 2.6% prior quarter, Employee hours rose 0.5% in 1Q vs. up 1.3% prior quarter, and nominal compensation rose 2.6 percent, the least in three quarters).

On a year-over-year basis, productivity rose 2.4% – the largest rise since Q3 2010…

…While labor costs advanced 0.1%, the least since 2013.

Blooomberg notes that it will still probably take more time to determine whether productivity is enjoying persistent increases after relatively slow gains throughout the current expansion, with an average of 1.3 percent from 2007 to 2018. Fed Chairman Jerome Powell on Wednesday brushed aside pressure for an interest-rate cut and said productivity is partly driven by technology developments and very hard to predict.

Today’s report showed output rose at a 4.1 percent pace, while hours worked increased 0.5 percent; that gain was last slower in 2015.

via ZeroHedge News http://bit.ly/2VaOUxt Tyler Durden

Joe Biden became the latest presidential contender to demand that AG Barr resign following a 5-hour-plus hearing on Wednesday where Democratic members of the Senate Judiciary Committee howled, mostly without evidence, that Barr was improperly trying to cover for President Trump, that he had deliberately watered down Mueller’s findings and that he was, in effect, acting as a mole within the DOJ feeding information on the 14 ongoing investigations to the White House.

Given his treatment at the hands of the Senate, it’s hardly a surprise that Barr declined to appear before the House Judiciary Committee on Thursday, which is stocked with even more bloodthirsty Democrats who will all need to defend their seats in 18 months time. And while Democrats will inevitably portray this as Barr shirking responsibility, as WSJ points out in an editorial published in Thursday’s paper, Barr’s treatment at the hands of the Judiciary’s Democrats was nothing short of reprehensible – and the coordinated ‘leak’ of the Mueller letter on the eve of the hearing was a blatant attempt to discredit an Attorney General who had done nothing wrong.

As WSJ explains, Mueller’s complaint that Barr’s summary of the 448-page report’s findings “lacked context” was likely an exercise in ass-covering. How could Barr be expected to distill the full sweep and scope of such a lengthy report’s findings in just four pages. In the same letter, Mueller affirmed that Barr’s summary was accurate – and, more tellingly, that he had been moved to write the letter following “public confusion” about his findings (i.e. Republicans’ trumpeting of ‘no collusion, no obstruction’, which probably angered Mueller’s many fanboys and fangirls in the #resistance).

As Lindsey Graham interjected following Marie Hirono’s bombastic questioning, where she effectively labeled Barr a liar and a traitor, the AG has been subjected to vicious slander at the hands of the Democrats simply for doing his job honestly and properly.

And the calls for his resignation are merely the cherry on top.

If Barr’s actions should be contrasted with anyone’s, the most fitting example would be former AG Loretta Lynch. Lynch “cowered” before James Comey and bowed to partisan interests by refusing to make a prosecutorial judgment after the Clinton investigation.

Did the Democrats demand that she resign?

Read the full editorial below:

Washington pile-ons are never pretty, but this week’s political setup of Attorney General William Barr is disreputable even by Beltway standards. Democrats and the media are turning the AG into a villain for doing his duty and making the hard decisions that special counsel Robert Mueller abdicated.

Mr. Barr’s Wednesday testimony to the Senate Judiciary Committee was preceded late Tuesday by the leak of a letter Mr. Mueller had sent the AG on March 27. Mr. Mueller griped in the letter that Mr. Barr’s four-page explanation to Congress of the principal conclusions of the Mueller report on March 24 “did not fully capture the context, nature, and substance” of the Mueller team’s “work and conclusions.” Only in Washington could this exercise in posterior covering be puffed into a mini-outrage.

Democrats leapt on the letter as proof that Mr. Barr was somehow covering for Donald Trump when he has covered up nothing. Hawaii Sen. Mazie Hirono, the Democratic answer to Rep. Louie Gohmert, accused Mr. Barr of abusing his office and lying to Congress, and demanded that he resign. The only thing she lacked was evidence.

Mr. Barr’s four-page letter couldn’t possibly have covered all the nuances of a 448-page report. It was an attempt to provide Mr. Mueller’s conclusions to Congress and the public as quickly as possible, while he took the time to work through the entire document to make redactions required by law and Justice Department rules.

This is exactly what he promised to do in his confirmation hearing.Even Mr. Mueller’s complaining letter admits that Mr. Barr’s letter wasn’t inaccurate, a fact Mr. Barr says Mr. Mueller also conceded in a subsequent phone call. The Mueller complaint, rather, was that there was “public confusion about critical aspects” of his investigation. Translation: Republicans were claiming vindication for Donald Trump, and Mr. Mueller was taking hits in the press for not nailing the worst President in history. Having been hailed for months as a combination of Eliot Ness and St. Thomas More, Mr. Mueller and his team of prosecutors seem to have been unnerved by some bad press clips.

Mr. Barr told the Senate Wednesday that he offered Mr. Mueller the chance to review his four-page letter before sending it to Congress, but the special counsel declined. Mr. Mueller worked for Mr. Barr, and that was the proper time to offer suggestions or disagree. Instead, Mr. Mueller ducked that responsibility and then griped in an ex-post-facto letter that was conveniently leaked on the eve of Mr. Barr’s testimony. Quite the stand-up guy.

Mr. Barr has since released the full Mueller report with minor redactions, as he promised, and with the “context” intact. Keep in mind Mr. Barr was under no legal obligation to release anything at all. Mr. Mueller reports only to Mr. Barr, not to the country or Congress.

Mr. Barr has also made nearly all of the redactions in the report available to senior Members of Congress to inspect at Justice. Yet as of this writing, only three Members have bothered—Senate Judiciary Chairman Lindsey Graham, Senate Majority Leader Mitch McConnell and ranking House Republican on Judiciary Doug Collins. Not one Democrat howling about Mr. Barr’s lack of transparency has examined the outrages they claim are hidden.

Democrats are also upset that Mr. Barr concluded that Mr. Trump did not obstruct justice regarding the Russia probe. But in that decision too Mr. Barr was behaving as an Attorney General should. Mr. Mueller compiled a factual record but shrank from a “prosecutorial judgment.” Mr. Barr then stepped up and made the call, however unpopular with Democrats and the press.

* * *

Contrast that to the abdication of Loretta Lynch, who failed as Barack Obama’s last Attorney General to make a prosecutorial judgment about Hillary Clinton’s misuse of classified information. Ms. Lynch cowered before the bullying of then FBI director James Comey, who absolved Mrs. Clinton of wrongdoing while publicly scolding her. That egregious break with Justice policy eventually led Mr. Comey to re-open the Clinton probe in late October 2016, which helped to elect Mr. Trump.

All of this shows again the risks of appointing special counsels. They lack the political accountability that the Founders built into the separation of powers. Mr. Mueller, in his March 27 letter, revealed again that like Mr. Comey at the FBI he viewed himself as accountable only to himself.

This trashing of Bill Barr shows how frustrated and angry Democrats continue to be that the special counsel came up empty in his Russia collusion probe. He was supposed to be their fast-track to impeachment. Now they’re left trying to gin up an obstruction tale, but the probe wasn’t obstructed and there was no underlying crime. So they’re shouting and pounding the table against Bill Barr for acting like a real Attorney General.

via ZeroHedge News http://bit.ly/2JicNML Tyler Durden

During the first hearing in what’s expected to be a protracted legal battle over the US’s extradition request, Wikileaks’ founder Julian Assange told a British judge that he wished to fight extradition, and the hearing was concluded with the next court date set for May 30.

Assange, whom the US has charged with conspiring with Chelsea Manning to break into a government computer, a charge that carries a maximum prison term of 5.5 years, appeared on screen wearing a sports jacket. He wasn’t handcuffed. And when asked if he would consent to surrender to the US, he replied that he did not wish to do so, according to CNN.

Assange, speaking from Belmarsh prison, was wearing a sports jacket and was not handcuffed.

Asked by Judge Michael Snow if he wished to consent to surrender himself for extradition, Assange said: “I do not wish to surrender myself for extradition for doing journalism that’s won many, many awards and affected many people.”

His appearance came a day after another judge slapped him with a 50-week sentence for skipping bail back in 2012.

As we previewed last night, Wikileaks editor-in-chief Kristinn Hrafnsson said Wednesday that the extradition process is where ‘the real battle begins’ for Assange.

Speaking to CNN after Assange’s bail violation sentencing on Wednesday, WikiLeaks’ Editor-in-Chief Kristinn Hrafnsson said he was “shocked and appalled by this decision to sentence Julian to two weeks short of the maximum sentence for not showing up in court.”

He added that the US extradition claim is “where the real battle begins.”

Assange’s legal team has yet to publicize its defense strategy, but most expect them to argue that the request is politically motivated. Meanwhile, Hrafnsson declared that it’s Wikileaks’ view that the charges cited by the US in the extradition request are merely a ruse, and that Assange will be charged with violating the 1970 Espionage Act once he’s safely on American soil – a charge that could carry the death penalt.

“Everything in this case seems to indicate that what is being established is a violation of the espionage act of 1970 which carries the death penalty,” Hrafnsson explained. “Although the extradition is based on a lower level of offenses, we think that is basically a snaring strategy to get him to United States where additional charges will be added.”

As CNN explained, to extradite Assange, a court must agree that his alleged violations would also constitute criminal conduct in the UK. Afterward, the UK’s home secretary would still have final say on whether Assange is handed over.

Extradition requests to the UK from outside the European Union are governed by Part 2 of the Extradition Act 2003. When reviewing the US extradition claim, it will not be for the UK courts to determine culpability. A judge only determines whether the US request satisfies the “dual criminality” legal requirement – meaning that the alleged crime is illegal in both countries. The judge would also consider if granting extradition would breach his human rights.

If satisfied that the claim meets procedural conditions, the case would be sent to the British home secretary for a final decision on ordering the extradition.

Protesters gathered outside the courthouse before the hearing (during which Assange participated by video link; he was being held in a high-security prison).

Supporters of WikiLeaks founder Julian #Assange protesting outside Westminster Magistrates Court at US extradition hearing: “US, UK – Hands off Assange!” pic.twitter.com/x0Ros0OuCs

— Socialist Equality Party (Britain) (@SEP_Britain) May 2, 2019

And crowds waited to hear from Assange’s lawyers after the hearing had concluded. Some even blocked a nearby road in a gesture of protest.

Outside the court waiting for Assange legal team to speak. Extradition matter back in court again May 30. pic.twitter.com/9oypAJs3MY

Tesla’s need for cash has finally slipped beyond the point where CEO Elon Musk can continue to pretend to ignore it, and instead has been given a violent thrust into urgent, as the company filed this morning to offer about 2.7 million shares (~$650 million in stock) and $1.35 billion in convertible notes one week after Musk said there was merit to the cash-crunched company raising more capital. Shares popped on the news in the pre-market session on news Musk would participate in the offering:

The entire financing seeks to raise about $2. The converts will add another maturity to the company’s nearly $11 billion in debt it already carries and, by our back of the envelope calculations, the equity issuance will dilute current shareholders by approximately 1.25%. The senior convertible notes will be due in 2024.

To put a lipstick on the dilution pig, CEO Elon Musk has indicated his “interest” in purchasing up to about 42,000 shares, or a paltry $10 million of the offering. This equates to about 0.045% of Musk’s reported $22 billion net worth. According to FinTwit regular @bgrahamdisciple, Elon Musk is the only executive officer or director who has purchased shares in the last 12 months. Other executive officers and directors have executed 41 sales in the past 12 months.

Goldman Sachs, Citigroup, BofA, Deutsche Bank, Morgan Stanley, Credit Suisse, Soc Gen and Wells Fargo will be handling the offering. As Mark Spiegel points out, the lead underwriter on the stock has a “sell” rating on the name and a $200 price target.