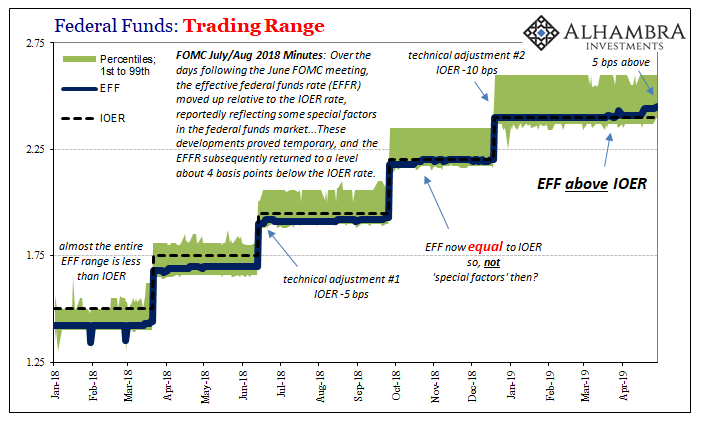

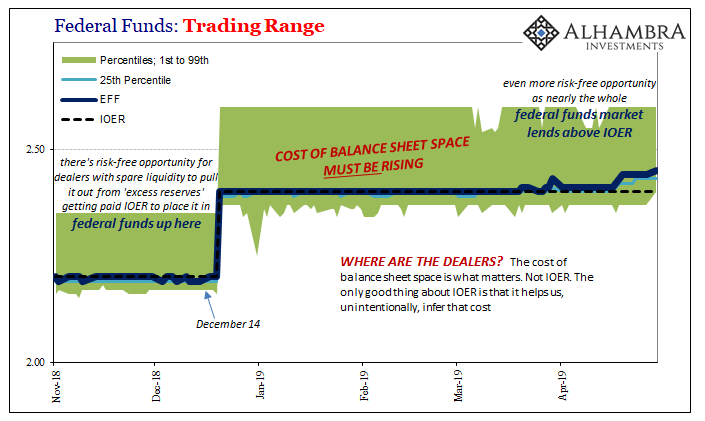

Federal funds is up again. As of yesterday, the 29th, the effective rate (EFF) is now 5 bps above IOER. That takes it to within 5 bps below the top of the Federal Reserve’s policy range. According to FRBNY, the 1st percentile in yesterday’s session was 2.40%, meaning that almost the entire federal funds market is paying more than IOER. Where are the dealers?

If a scramble for liquidity shows up here, what is it like everywhere else where it does matter? The federal funds market is nothing more than leftover pocket change of the FHLB’s. But with these rates, there should be more than that going on. There is opportunity for any enterprising dealer to take advantage of risk-free spreads, to make something more than what it is.

And the profit opportunities just sit there.

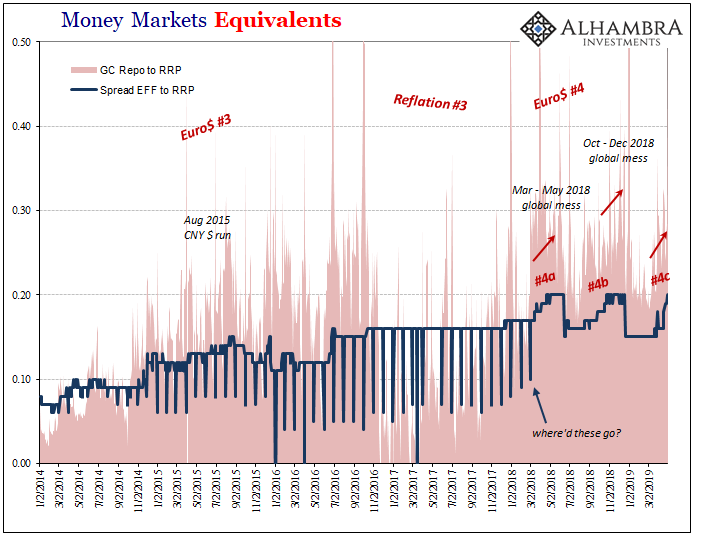

It’s not just here where the dealers publicly demonstrate their hoarding. If EFF is up you pretty much know what’s going on in the repo market. There is no obvious reason why month-end in repo should be so dry. We’ve become accustomed (though only during these Euro$ squeeze periods) to quarter-end runups in the GC rates. Month-end is something else.

That’s just what happened yesterday. The final trading day of a middle month in Q2 2019 for some reason became extra special hard in terms of repo market liquidity. It’s not nearly the insanity experienced at the very end of 2018, but the GC rate for UST collateral was fixed today at 2.807% (DTCC). That’s nearly 56 bps above RRP (literally off the chart below), and a lot more than yesterday’s 2.534%. The GC rate for MBS was even higher, 2.915%.

The few who do notice these vitally important indications will keep talking about T-bills or some other technical-sounding excuse. Meanwhile, going back to the original outbreak last year, the world keeps coming apart. The global economy’s minus signs keep piling up and proliferating.

If you are a big leveraged player, meaning just about every large financial entity on the planet, you can’t afford to be so sanguine or to keep your head stored so firmly, deeply in the sand. As illiquidity escalates with these warnings, the chance of the most dreaded phone call in finance rises.

The collateral call creeps ever closer, the one that can terminate your career and your firm if due care is not exercised. The lingering lesson of Bear.

Given this situation, it doesn’t matter one bit that you might agree with Economists. Let’s say you are ultra-positive on the economy. The unemployment rate in the US is the true picture of the domestic situation, inflation has to therefore rise. The world isn’t going to keep buying all the US federal debt, not with the economy on the rise and demand for UST’s dropping against that rising supply.

It’s going to be really bad for especially duration (meaning long end UST holders) – at some point.

Those factors, however, don’t mean a damn thing today. All that does matter is EFF and repo (and interest rate swaps, as well as FX). Liquidity is primary over everything. The more these “benign” problems continue forward and intensify, the less relevant those other parameters will be. The bond market massacre can easily wait. A long time.

And that’s if you actually believe Economists.

They are thinking something else because they don’t get bonds. CNBC’s chief Economist Steve Liesman sent out a survey to a lot of others like him. Guess what? Surprise of all surprises, the Economists almost uniformly believe that Economists are right and the bond market must be wrong.

Almost two-thirds of them. 63% are still forecasting another Fed rate hike by the end of this year. Whereas bond and money markets continue to betting trillions on a cut perhaps more, not these guys. They are sticking with their econometric models where the unemployment rate cannot possibly be so faulty (again).

“The markets are irrationally pessimistic about the future. There is no recession coming,” wrote Chris Rupkey, chief financial economist at MUFG. “Cutting rates for low inflation at this time is ill-advised…The Fed should restart its gradual pace of rate hikes later on this year.” [emphasis added]

For them, green shoots and an overblown growth scare. It doesn’t matter that, according to the same survey, these same Economists had last year expected the 10-year UST yield to rise to 3.5% or more but now only expect 2.75% by the end of 2019. The difference is just transitory stuff. China trade tensions that will go away when a trade deal is done.

But that’s the thing. Here we are one-third of 2019 in the books already and EFF keeps showing up Jay Powell; repo keeps doing remarkably disruptive things. And the economic data continues to follow the obviously illiquid nature of global money – as do bond yields. Even the US economy’s biggest (purported) boom in a long time has proved vulnerable, pulling up especially lame recently in all the key components (income most of all).

We’ve been here before, of course. What I wrote in May 2014could’ve easily been written today:

That sets up another “titanic” struggle between economists and money markets – academic models against those with actual money positions. The economist side sees taper as a signal that the economy is going to take off (as intended under the Bernanke scenario of influencing expectations), whereas the credit and dollar markets may be coming around to taper as optimal control, preserving policy margins ahead of economic turbulence.

We know which side stocks are betting on.

Stocks didn’t care, outside of seven months starting August 2015, that Economists got it wrong for the third time in the last almost twelve years dating back to Bill Dudley’s first ugly encounter with the curves in 2007. There was no recovery and acceleration in 2015, no big liftoff as had been planned by Economists and central bankers in 2014.

Bonds were right. Euro$ #3 pushed the US economy very, very close to recession while the rest of the world suffered a variably intense nightmare. The way the markets are positioned now, that’s actually the upside to today’s confirmed Euro$ #4, the least worst case. If bonds are specifically right about rate cuts, that’s more of a downside still.

Then again, Economists and their models could just get lucky for once. That’s about all they have going for them at this point. When does it ever just work out great once all the biggest financial institutions in the world, despite what the Economists working for them say, all pile in on liquidity preferences? Pretty much never, especially when the reasons they are and have been are right there in front of everyone.

via ZeroHedge News http://bit.ly/2DJ2EEW Tyler Durden

After March’s gravely disappointing miss (well below the March rebound in non-farm payrolls), ADP employment was expected to rebound to its somewhat flat forecast of 180k in April.

After last month’s +129k miss, ADP played catch up this month with a massive +275k (and upward revision to +151k for March) with Services adding 223k and Goods producers up 52k

“April posted an uptick in growth after the first quarter appeared to signal a moderation following a strong 2018,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute.

“The bulk of the overall growth is with service providers, adding the strongest gain in more than two years.”

Information and Natural Resource jobs declined…

Mark Zandi, chief economist of Moody’s Analytics, said,

“The job market is holding firm, as businesses work hard to fill open positions. The economic soft patch at the start of the year has not materially impacted hiring. April’s job gains overstate the economy’s strength, but they make the case that expansion continues on.”

Soaring GDP and employment data – and yet the market still expected 30bps of rate cuts in 2019? Something is wrong here!

via ZeroHedge News http://bit.ly/2WpBxpG Tyler Durden

It’s no secret that Beijing has chafed at American audacity to try and dictate whom Chinese refineries can and can’t buy oil from. And in the latest example of just how aggravating the decision to end waivers for Iranian crude imports has been for the world’s second-largest economy, Reuters reported that some 20 million barrels of Iranian crude have been languishing at the northeastern port of Dalian for months, but because of the US’s decision to re-impose sanctions on Iran back in November, nobody wants to touch the oil.

Even when the waivers were in effect, Chinese refineries couldn’t secure financing and insurance that would allow them to purchase the oil because of the uncertainty surrounding the future of the waivers.

Iran sent the oil to China via the National Iranian Tanker Company before the sanctions were imposed as Iran struggled with a backlog of oil that had exhausted the country’s domestic storage capacity. So Beijing, the largest buyer of Iranian oil, allowed the NTCC to store some oil in so-called bonded storage tanks situated in the Dalian port. The oil has yet to go through Chinese customs.

China filed a formal complaint with the US over its decision to end the waivers, but the US has refused to consider any exceptions to its plans to reimpose full sanctions.

As one analyst told Reuters, no Chinese company will touch the oil unless specifically instructed to do so by the Chinese government.

The oil is being held in so-called bonded storage tanks at the port, which means it has yet to clear Chinese customs. Despite a six-month waiver to the start of May that allowed China to continue some Iranian imports, shipping data shows little of this oil has been moved.

Traders and refinery sources pointed to uncertainty over the terms of the waiver and said independent refiners had been unable to secure payment or insurance channels, while state refiners struggled to find vessels.

The future of the crude, worth well over $1 billion at current prices, has become even more unclear after Washington last week increased its pressure on Iran, saying it would end all sanction exemptions at the start of May.

“No responsible Chinese company with any international exposure will have anything to do with Iran oil unless they are specifically told by the Chinese government to do so,” said Tilak Doshi of oil and gas consultancy Muse, Stancil & Co in Singapore.

To be sure, Reuters says, some of the oil was apparently purchased by a Sinopec refinery. But the bulk of the stock remains untouched.

Some Iranian oil sent to Dalian has moved, according to a ship tracking analyst at Refinitiv.

Dan, a supertanker owned by NITC moved 2 million barrels of oil from Dalian more than 1,000 km (620 miles) to the south to the Ningbo Shi Hua crude oil terminal in March, according to Refinitiv data.

Ningbo is home to Sinopec’s Zhenhai refinery, one of the country’s largest oil plants with a capacity of 500,000 barrels a day and a top processor of Iranian oil.

The headache for Beijing will likely only get worse, because shipping data show more Iranian crude is heading for Chinese ports.

For now, more Iranian oil is heading to China, with the supertankers Stream and Dream II due to arrive in eastern China from Iran on May 5 and May 7, respectively, Refinitiv data showed.

Some of this crude may be from Chinese investments into Iranian oilfields, a sanctions grey area.

Eventually, this could create incentives for non-compliance that are just too powerful for Chinese companies to ignore, particularly companies that have investments in Iranian oilfields. Some companies might try bartering for the oil, while others resort to illegally forged documents.

Whether China will keep buying oil from Iran remains unclear, but analysts at Fitch Solutions said in a note “there may be scope for imports via barter or non-compliance from … China.”

Muse, Stancil & Co’s Doshi said the only way to get the Iranian oil out of Dalian now was by cheating.

“Only rogue parties might try to cheat the system and try to pass the Iranian oil at Dalian as something else via fraudulent docs. But I doubt this is easy or can amount to much in terms of volume.”

Regardless of what happens to the oil, the incident serves as a reminder of the many annoyances that US sanctions create for its geopolitical rivals. Every barrel of China has sitting offshore that its refineries can’t touch is one more reason for Beijing to pursue the creation of an alternative payments channel that’s outside of American control…and more incentive for Chinese refineries, at the government’s behest, to push exporters to accept payment in yuan, something that the Shanghai-traded, yuan-denominated oil futures have already incentivized.

The US should acknowledge the perverse incentives for de-dollarization that its own policies have created – something that one of America’s favorite boogeyman has labeled a “colossal strategic mistake.”

via ZeroHedge News http://bit.ly/2GUMNp5 Tyler Durden

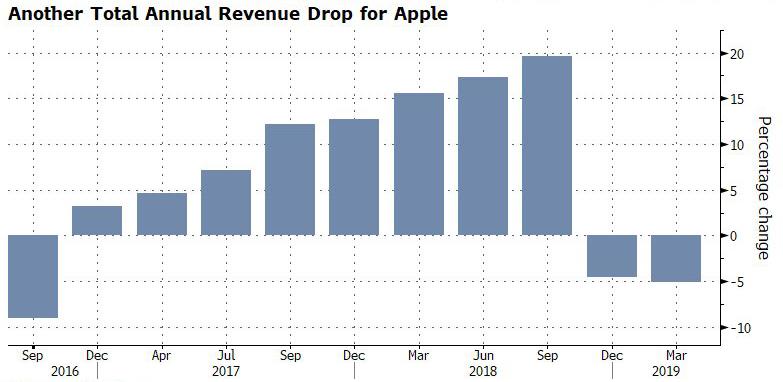

The tremors unleashed by Google’s earnings debacle and China’s disappointing PMIs just over 24 hours ago are now long forgotten as trader focus shifts to Apple’s strong guidance (if not 17% drop in iPhone sales and 22% plunge in China revenues), helping push the global rally into a fifth month and US equity futures to a fresh record high, even as potential disappointment looms should the FOMC come out more hawkish than expected. At least there will be fewer traders to be disappointed: most of Asia and Europe was shut for the May day holiday. Meanwhile, out of equities, bonds continue to disagree with the algos’ optimism as treasury yields slumped below 2.50% again, while the dollar dipped ahead of the Federal Reserve’s policy decision.

The MSCI world equity index was up 0.1% in early trading after rising to its highest since early October, although May Day holidays across Asia and Europe meant trading was thinner than usual with China, Hong Kong, India, Japan, Singapore, South Korea and Taiwan all shut, and only the UK and Denmark open in Europe.

In a sign of the growing appetite for riskier assets, Australian shares ended just shy of an 11-year peak and London’s blue chip FTSE 100 was up 0.2 percent after solid earnings from supermarket chain Sainsbury’s.

Apple’s strong guidance which came against a disappointing background of the second consecutive revenue decline…

… helped rally US index futures and Apple’s global suppliers and pointed to a rebound for American technology shares, which had slumped in the wake of Google’s revenue miss. Stocks in the U.K. turned lower after data showed manufacturing growth slowed in April, though the pound held gains. Australian equities climbed, while the New Zealand dollar fell after unexpectedly weak labor data. In the UK, Pearson fell after US textbook peers McGraw-Hill Education and Cengage Learning were said to plan a merger. The pound rose to fresh gained to fresh 2 week highs against the dollar.

For those traders who did make it to work today, there is plenty to keep them busy: Beijing and Washington began their latest talks aimed at ending a bitter trade war and Fed chairman Jerome Powell was due to speak later following the central bank’s two-day policy meeting.

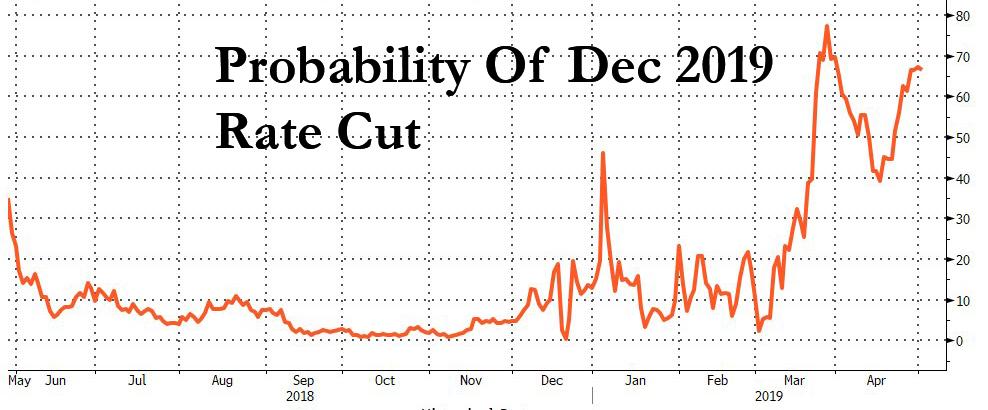

Indeed, all eyes turn to the Marriner Eccles building at 2pm today, and Powell’s subsequent press conference following the U.S. rate decision. “The risk for this Fed meeting is that, unless the FOMC meets the market’s dovish expectation for their stance, we would expect another leg higher in USD,” Mizuho strategists said in a note. As we previewed last night, the Fed expected to leave US rates unchanged amid a “goldilocks” economy, although there is a modest chance of an IOER cut. That said, the market remains convinced a rate cut is coming by December 2019.

A call from U.S. President Donald Trump for a cut in interest rates will likely be unheeded when the results of the Fed’s two-day meeting are released, but the unorthodox comments made on Twitter will increase focus on Powell at his press conference shortly after.

“We expect the Fed to reiterate their still patient stance, as they announced at the start of the year,” Stifel chief economist Lindsey Piegza told Bloomberg TV. “We also expect the Fed to re-characterize their expectation for growth at a somewhat tempered level, but still very positive.”

Corporate earnings and developments in the trade conflict between America and China are also on the radar, with U.S. Treasury Secretary Steven Mnuchin calling the latest round of meetings “productive.” Bullish investors are looking for fresh reasons to push the S&P 500 Index higher after it closed Tuesday at another record.

Additionally, with the whole “sell in May” mantra at their backs, trader caution is building ahead of the summer lull with investors questioning how much longer the rally across global equities can last with better economic data and a stabilization in earnings priced in. “Historically the more difficult half of the year starts today,” said Ian Williams, economics and strategy research analyst at Peel Hunt. “The next six months will present plenty of geo-political challenges.”

In FX, the U.S. dollar was down slightly, trading in a tight range after hitting a one-week low ahead of the Fed news. The Swiss franc and pound led gains among G-10 currencies as the dollar reversed an earlier advance ahead of the FOMC decision. Moves were muted as many markets in Europe and Asia were closed for holidays and traders were in a holding pattern before the Fed. The New Zealand dollar fell after weaker-than-forecast labor-market data caused investors to increase bets on an interest-rate cut as soon as next week.

Elsewhere, commodities were mixed with base metals prices rising on hopes of a breakthrough in the U.S.-China talks, while crude oil prices eased as data showed a rise in U.S. inventories. Brent crude oil futures were at $71.55 per barrel, down 0.8 percent, while U.S. West Texas Intermediate (WTI) crude futures were down 1.1 percent at $63.23 per barrel.

The Federal Reserve’s policy decision is due, along with manufacturing data from ISM and Markit. Scheduled earnings include Qualcomm, CVS Health and Estee Lauder.

Market Snapshot

S&P 500 futures up 0.4% to 2,959.25

STOXX Europe 600 up 0.09% to 391.70

MXAP up 0.2% to 162.60

MXAPJ up 0.3% to 539.76

Nikkei down 0.2% to 22,258.73

Topix down 0.2% to 1,617.93

Hang Seng Index down 0.7% to 29,699.11

Shanghai Composite up 0.5% to 3,078.34

Sensex down 0.09% to 39,031.55

Australia S&P/ASX 200 up 0.8% to 6,375.89

Kospi down 0.6% to 2,203.59

German 10Y yield rose 1.0 bps to 0.013%

Euro up 0.1% to $1.1227

Brent Futures down 0.8% to $71.48/bbl

Italian 10Y yield fell 2.9 bps to 2.184%

Spanish 10Y yield fell 1.2 bps to 1.001%

Brent Futures down 1.8% to $71.48/bbl

Gold spot down 0.2% to $1,281.13

U.S. Dollar Index down 0.04% to 97.44

Top Overnight Highlights

The latest round of U.S.-China talks wrapped up in Beijing, with U.S. Treasury Secretary Steven Mnuchin calling the meetings “productive” in a tweet. Negotiations will continue in Washington next week, Mnuchin said after Wednesday’s round concluded slightly later than scheduled

Fed policy makers may decide Wednesday that falling inflation reinforces a message of caution on interest-rate moves, rather than bowing to President Donald Trump’s demands for drastic action to boost the U.S. economy

U.S. Attorney General William Barr will face new scrutiny from lawmakers on Wednesday after a revelation surfaced that he misrepresented Special Counsel Robert Mueller’s findings about whether Trump obstructed justice

The U.K.’s main opposition Labour Party predicted Prime Minister Theresa May will have to accept a customs union with the European Union as the price for getting her Brexit deal ratified in Parliament

New Zealand hiring unexpectedly fell in the first quarter and wages rose at a slower pace, adding to signs that the jobs market isn’t generating significant inflation pressure

A quiet tone was observed in Asia-Pacific amid closures in nearly all the major regional bourses for Labour Day, although US equity futures were underpinned after-hours following Apple earnings in which the tech giant beat on top and bottom lines, authorized an additional USD 75bln share repurchase and raised its dividends by 5%. ASX 200 (+0.8%) was positive with the index led higher by tech on contagion from Nasdaq futures and with financials buoyed as ANZ shares rallied nearly 3% after its H1 results, while reports that the US dropped a key demand regarding cyber theft in an effort to accelerate a trade deal with China also added to the optimism although most of the region failed to capitalize with China, Hong Kong, India, Japan, Singapore, South Korea and Taiwan all shut.

Top Asian News

Mnuchin, Lighthizer Conclude ‘Productive Meetings’ With China

Japan’s New Emperor Naruhito Ascends World’s Oldest Monarchy

China Further Opens Financial Industry on Eve of Trade Talks

Qantas CEO Alan Joyce Commits to Three More Years at the Helm

Mass closures in Europe have extended the quiet tone seen across Asia, with only UK and Danish markets open today in the EU. The FTSE 100 (-0.1%) is relatively flat with sectors also showing no clear standouts. In terms of movers, Sainsbury’s (+4.7%) rose to the top of the index amidst optimistic revenue and profit numbers, alongside a net debt reduction which is ahead of target. To the downside, Persimmon (-1.8%) shares suffer after fire issues were found in houses developed by the company, the company is addressing the issue. State-side, Apple reported earnings aftermarket wherein the tech giant topped estimates on both top and bottom line, whilst Q3 guidance was also above analyst consensus, despite a sharp drop in Q2 iPhone sales. Apple shares spiked higher in excess of 5% post-earnings.

Top European News

Lloyds Gets Capital Relief From Bank of England Risk Change

Sainsbury Gets Boost as CEO Clings On After Asda Failure

U.K. Mortgage Approvals Decline, Consumers Rein In Borrowing

U.K. Manufacturing Growth Slows as Firms Reduce Stockpiling Pace

In FX, Cable extended gains through more chart resistance levels on the way to circa 1.3073, like the 30 DMA (1.3052), a Fib (1.3053) and daily tech formation (1.3065), eyeing 1.3090 next (55 DMA) before the 1.3100 handle. A broadly in line and less stockpile-inflated UK manufacturing PMI amidst mixed BoE mortgage and consumer data was largely shrugged off, but Sterling also eked more upside vs the Euro as the cross eased a bit further below 0.8600 to test bids just ahead of a 50% retracement (0.8583) following more reports about constructive cross party Brexit talks as discussions are put on hold due to Thursday’s local elections. More immediately, focus on the Fed before the BoE tomorrow – see the Ransquawk headline feed for detailed previews of the 2 events. Conversely, weaker than forecast NZ jobs data has raised the stakes in terms of RBNZ rate cut expectations for next week and Nzd/Usd retreated in response through 0.6650, as the Aud/Nzd cross rebounded firmly from around 1.0560 to just over 1.0600. However, the Kiwi has pared some losses since with the probability of an ease still close enough to 50% for reasonable doubt.

CHF – Another major outperformer or rather beneficiary of a deeper pull-back in the Dollar ahead of the FOMC, as the Franc edges towards 1.0150 and DXY slips to 97.359, very close to a 97.355 Fib and nearer the 30 DMA (97.216).

AUD/EUR – Also firmer vs the Greenback as Aud/Usd consolidates recovery gains around 0.7050 and the single currency builds a foothold above 1.1200. Eur/Usd has eclipsed Fib resistance at 1.1217 and is now approaching convergence at 1.1242 (another Fib and 30 DMA) before 1.1250 and 1.1275 (latter roughly coincides with the 50 DMA).

JPY/CAD – Both narrowly mixed vs the Usd, as the Yen attempts to breach the 30 DMA (111.40) and retest Tuesday’s peaks, while the Loonie continues its recovery from yesterday’s post-Canadian GDP lows within a 1.3400-1.3375 range in advance of the manufacturing PMI and more from BoC’s Poloz and Wilkins.

In commodities, the energy market had a stellar performance in April as the benchmarks climbed over 6% amidst intensifying tensions in Venezuela, tightening US sanctions on Iran and ongoing OPEC supply cuts. Ahead of the end of Iranian oil waivers later, oil Journalist Reza Zandi notes that Iranian officials are reportedly discussing three potential Iranian scenarios in OPEC: 1) Iran suspends its membership in OPEC until sanctions are removed, 2) Iran departs from OPEC and 3) Iran continues its membership. In today’s trade, oil prices have reversed a bulk of the April gains following a much wider-than-forecast build in API crude stockpiles (6.8mln vs. Exp. 1.5mln), marking the 4th stock build in April. PVM analysts also highlight the uptrend in US stockpiles which is described as a “deepening pocket of weakness” amid a host of a bullish catalysts. WTI and Brent futures have thus retreated back below/around USD 64/bbl and USD 72/bbl respectively ahead of today’s EIA data wherein the market is geared for a headline build of 1.485mln barrels. Elsewhere, gold remains within a relatively tight range around 1280/oz ahead of the FOMC rate decision (preview available in the Research Suite) whilst copper mirrors the humdrum tone with most the region away on holiday. Finally, aluminium prices remain pressured following on from the weaker-than-forecast Chinese manufacturing data coupled with producers revising down their demand growth estimates for the year.

US Event Calendar

7am: MBA Mortgage Applications, prior -7.3%

8:15am: ADP Employment Change, est. 180,000, prior 129,000

9:45am: Markit US Manufacturing PMI, est. 52.4, prior 52.4

10am: ISM Manufacturing, est. 55, prior 55.3;

10am: Construction Spending MoM, est. 0.0%, prior 1.0%

2pm: FOMC Rate Decision (Upper Bound), est. 2.5%, prior 2.5%

Wards Total Vehicle Sales, est. 17m, prior 17.5m

DB’s Jim Reid concludes the overnight wrap

Welcome to May, a month which traditionally has been associated with the adage of ‘sell in May and go away’. However, with the S&P 500 having not seen a negative May performance since 2012 and the US expansion now only one more month away from matching the longest expansion ever at 120 months, it feels like it would take a brave person to do that now. The first day of a new month also means we have our latest performance review which you’ll find as a separate document to this and in your inboxes a short while ago. Needless to say April was another strong month for risk assets, and it means we’ve now seen the strongest start to a year through the first four months in the post-GFC era.

The end of the month saw the S&P 500 stick to the playbook after advancing a modest +0.10% yesterday despite some earnings headwinds and intensified concerns over trade. However, the NASDAQ did fall -0.81% as Alphabet tumbled -7.50% and the most since 2012 following that softer than expected earnings report late on Monday. That move erased more than $69 billion of Google’s market cap, which is equal to more than 3x the median S&P 500 company. On the other hand, Pfizer had reported earnings and revenue that beat expectations, propelling the stock up +2.58% and helping the DOW gain +0.15%. After markets had closed, Apple reported strong sales and profits as well, with iPhone sales notably healthy after recent concern over the product’s outlook. The company’s shares were nearly +5% higher overnight, helping NASDAQ futures advance +0.73% this morning. That’s all to report this morning with most of Asia not trading due to public holidays. Meanwhile, the STOXX 600 ended yesterday close to flat (+0.01%) with banks partially retracing their rally from Monday (-0.35%). Peripheral equities and bonds outperformed, led by Spain’s IBEX and Italy’s FTSE MIB, which gained +0.56% and +0.43%, respectively.

Not helping sentiment also was a WSJ article suggesting that the US favoured leaving punitive tariffs in place as a way of enforcing any trade deal. During the US session, Acting White House Chief of Staff Mulvaney said that talks “won’t go on forever” and if they can’t reach a deal soon then “you throw up your hands and say ‘this is never going anywhere.’” So things certainly seem to be approaching an inflection point, but to be fair we’ve heard similar rhetoric before. USTR Lighthizer and Secretary Mnuchin are in Beijing today negotiating, with the Chinese team set to return to the US next week to continue talks. In other US political news, congressional Democrats met with President Trump yesterday to discuss an infrastructure deal and agreed to meet again in three weeks to discuss funding options. That will be the key area of disagreement, since Senate Minority Leader Schumer has already called for a partial rollback of Trump’s signature tax reforms, while Majority Leader McConnell has already rejected that idea. The sides at least agreed that $2 trillion should be the target for the overall plan, which would certainly be a positive for the economy if realized.

While that should hover in the background, the good news is that we’ve got the welcome distraction of a Fed meeting to look forward to this evening. No policy change is expected and our US economists anticipate that the meeting statement and press conference will reflect the dichotomy of improving growth prospects and easy financial conditions on the one hand, and softening inflation pressures on the other. As such our colleagues believe patience in assessing any adjustments to the policy stance will remain the order of the day for the foreseeable future. However the wildcards are further announcements about balance sheet normalization and the potential for a cut to the IOER. The latter became a bit more likely after yesterday’s fed funds fixing rose to 2.45%, which takes it within 5bps below the top of the target range. That’s the level which has prompted the Fed to lower the IOER in the past. For what it’s worth, President Trump was vocal about the Fed again yesterday, criticizing them for “incessantly” lifting rates amid “wonderfully low inflation” and suggested that the US economy would soar “like a rocket” if they cut rates by a full point and did more QE. Anyway, you can see our economists’ full Fed preview here.

Coming back to yesterday, where the other story was the contrasting slew of data releases on both sides on the pond. It started in Europe with a better than expected Q1 GDP reading for the Euro Area at +0.4% qoq (vs. +0.3% expected). The unrounded reading was +0.38% qoq with the data getting a boost from country level readings for France, Spain and Belgium before. At the same time the March unemployment rate also ticked down to 7.7% which is in fact the lowest in the current cycle now, having peaked at 12.1% in 2013. For what it’s worth, the 2007 low was 7.3%. So the labour market is seemingly still extremely robust, which as our European economists noted reduces the chances of manufacturing sector weakness being transmitted to services through an income-induced hit to domestic demand. We should note that Italy also reported a +0.2% qoq GDP reading yesterday which officially means it has emerged from recession.

Also generating some airtime yesterday morning were the country level April inflation readings. There wasn’t any great surprises for the data in France, Spain, or Italy, however the big positive surprise came in Germany where the +1.0% mom print smashed expectations for just +0.5%. That left the annual rate at +2.1% yoy compared to +1.4% in March. There was talk of an unusually large increase in prices for packages around the Easter holidays as explaining the upside surprise, which may result in some payback next month. Nevertheless, Bunds got as high as 0.046% intraday before fading slightly to close +0.9bps higher on the session at 0.011%.

In any case, stronger growth and higher inflation is certainly food for thought for the ECB even if the data in Europe remains a bit noisy at the moment. Meanwhile, there was no shortage of data in the US yesterday either. It started with a +0.7% qoq reading for the employment cost index which matched expectations, while the breakdown didn’t reveal any great surprises, however the private wages and salaries component was a little firmer at +0.8%. Overall, another fairly benign inflation reading however. Even softer though was the April Chicago PMI which tumbled -6.1pts to 52.6 compared to expectations for 58.5. That is the weakest reading since January 2017 which perhaps paints some downside risk for the 55.0 consensus for today’s ISM print, though it’s interesting to note that the Chicago reading has moved in the opposite direction as the ISM in every month so far this year.

The other data out in the US yesterday included consumer confidence, which rose +5pts to 129.2, remaining near its cyclical high. Pending home sales rose +3.8% mom versus expectations for +1.5%, which is the second highest rate since 2010, only eclipsed by January’s print. Some further evidence of firming activity in the housing market, though on the other hand an index of US house prices rose only +3.0% yoy, which was its slowest pace since 2012. Since shelter prices make up 40% of core CPI, this will definitely be an area to watch moving forward.

The end result of all that was for 10y Treasuries to trade in a 4.9bps range but ultimately settle -2.4bps lower at 2.503%. Elsewhere, BTPs rallied -3.0bps. Though there wasn’t a clear driver, euro area inflation expectations also repriced notably higher. The 5y-5y forward inflation swap rate rose +7.2bps, its biggest move since 2015, though it remains somewhat depressed at 1.42%. The USD (-0.39%) faded with EM FX ending +0.18% higher. Speaking of EM, there was some focus on Venezuela yesterday after opposition leader Juan Guadio called for the military to join with him to overthrow the Maduro regime. He was reportedly seen with national guardsmen, but Madura said on Twitter that the military remains loyal to him. Brent crude oil spiked as high as +1.71% before ending the session +1.05% higher, however it has since given up most of that move this morning.

Looking at the day ahead, the obvious focus is on the aforementioned Fed meeting tonight however it’s also another busy day of data releases with March money and credit aggregates data due in the UK this morning along with the April manufacturing PMI, before we get the April ADP employment change reading in the US along with the April ISM and manufacturing PMI, March construction spending and April vehicle sales. Away from that we’re due to hear from the ECB’s Guindos while US Attorney General Barr is due to testify before the Senate on the 2016 election and specifically Russian interference. The earnings highlights today include Qualcomm, GlaxoSmithKline and Kraft Heinz.

via ZeroHedge News http://bit.ly/2GYT7fj Tyler Durden

Julian Assange has been sentenced to 50 weeks in a UK prison – close to the maximum sentence – for skipping bail in 2012 to seek refuge in the Ecuadorian embassy, setting off a seven-year showdown with UK law enforcement and the US that ended with his arrest earlier this month, WSJ reports.

After arriving at the Southwark Crown Court on Wednesday, Assange defiantly raised his fist to rally his supporters. A judge declared during an earlier hearing that Assange’s case could warrant the maximum sentence after he was found guilty shortly after his arrest.

Assange skipped bail in 2012 to avoid being extradited to Sweden over an investigation into allegations of sexual assault.

The Wikileaks founder is facng a separate court hearing on Thursday over a US extradition request. If he is extradited, he could face a maximum of 5.5 years over charges that he conspired to break into a government computer.

via ZeroHedge News http://bit.ly/2J4uLSA Tyler Durden

Venezuelan opposition leader and self-proclaimed president Juan Guaido has called for a second day of street protests on Wednesday, but after the Venezuelan government successfully beat back the Guaido-led “popular uprising” – as the vast majority of Venezuela’s military remained loyal to Nicolas Maduro – it’s looks like the Russia- and China-backed socialist regime has resisted this latest challenge to its rule.

The coup attempt was hardly bloodless – there were horrifying incidences of extreme violence – but for all the jawboning from President Trump, Vice President Mike Pence, Secretary of State Mike Pompeo and NSA John Bolton, it appears Guaido’s most prolific attempt yet to force Maduro from power was a spectacular failure. Some members of the military defected, but Maduro by and large retained control over the military and other levers of power. Presenting a surprising lack of confidence in Guaido, opposition supporters celebrated the release of Leopoldo Lopez from house arrest, the former opposition leader immediately sought refuge in the Chilean embassy.

Late on Tuesday, Maduro took to twitter to thank the supporters of his regime who took to the streets to help suppress the rebellion, and the leaders who stood up for the Bolivarian revolution.

Agradezco a todo el pueblo venezolano, su valentía, coraje y conciencia frente a este intento de golpe de Estado frustrado. Han demostrado que un pueblo movilizado es garantía de tranquilidad para la Patria. ¡Venezuela es Territorio de Paz e Independencia! pic.twitter.com/CjOhzxpjH4

Saludo a los líderes, lideresas, gobiernos, movimientos sociales e intelectuales del mundo por sus pronunciamientos, muestras de solidaridad y apoyo a la Constitución, a la democracia y al Gobierno Bolivariano que presido. ¡El Pueblo de Venezuela les Agradece! pic.twitter.com/XAnRvUABJa

Flanked by military leaders, Maduro delivered a speech where he demanded that all opposition supporters who participated in the day’s violent skirmishes must be identified and arrested, and he bragged that the military base at La Carlota resisted a takeover attempt.

Forming an unusual alliance, it appears CNN has joined the Trump administration in spreading disinformation about the events in Venezuela to try and destabilize the regime.

CNN uses picture of pro-Guaido soldiers shooting (note the blue armbands) as proof of Maduro government “mowing down” its own citizens. Standard. https://t.co/kpwwCKI2oP

Still, Guaido hasn’t given up yet, calling for his “Operation Liberty” to continue on Wednesday.

Mañana continuamos con la ejecución de la #OperaciónLibertad. Iniciamos la fase final y estaremos de forma sostenida en las calles hasta lograr el cese de la usurpación.

Meanwhile, Russia’s foreign ministry has said Pompeo’s claim that Moscow had convinced Maduro to resist the coup and cling to power was “fake news”.

Pompeo said Tuesday that Maduro had intended to step down, but Russia had convinced him to stay. “Washington tried its best to demoralise the Venezuelan army and now [has] used fakes as a part of an information war,” Moscow spokeswoman Maria Zakharova told CNN on Wednesday.

As Venezuelans prepare for a second day of unrest, the number of dead and wounded in Tuesday’s clashes hasn’t yet been reported.

via ZeroHedge News http://bit.ly/2XXHACk Tyler Durden

Amid the ruckus of Great Britain’s reckless Brexit saga, one might not have noticed the ongoing environmental battle that could put a sudden end to shale gas development in the UK. While Britain’s energy security does not have any direct links to Brexit – its hydrocarbon production went into decline in 2000 and has been falling ever since, although the mid-2010s evidenced a stabilization of output – the UK High Court decision over the nation’s shale gas projects might deal a painful blow to the little hope British producers had to kick-start something new. All 9 basins of the Greater North Sea are mature and it is only until 2025-2027 that the current output rebound can last, after that Britain’s oil output will plunge Venezuela-style unless additional measures are taken.

There is no scientific consensus on how much shale gas can be recovered across the United Kingdom. We might use the British Geological Survey’s 2013 report as a point of reference, which states that across central Britain (Bowland-Hodder shales) the aggregate shale gas reserves are somewhere within the 164-264-447 TCf interval (P90-P50-P10). Even if it were true, due to the rather difficult lithography of central Britain the actual recoverable volume would be substantially smaller. The USGS has put the total recoverable gas resources in the Midlands area of England at 8.3 TCf. The Weald Basin in southern Britain and Northern Ireland also has shale gas resources, but they are in a less advanced stage of development than shale finds in Lancashire or Nottinghamshire.

Partially motivated by the emotional drain of Brexit and the necessity to present itself as an employment creating party, the Conservative Party (seemingly) made great headway last year in advancing the cause of developing UK shale gas resources and creating the regulative norms required for it. It has promoted a package of reforms that ought to kick-start shale projects across the country by removing needless administrative obstacles and easing operations. For instance, the new set of rules stipulated that no planning permissions would be needed for shale plays as long as fracking is not involved, and classified shale projects as “nationally significant”, meaning that decisions on shale applications were moved away from the local and regional level.

The Conservative minority government also created a new shale-devoted entity, the Shale Environmental Regulator Group (SERG), to create a dedicated authority that would act as a uniting platform and appointed a first-ever commissioner for shale gas matters. Yet unlike most gas producers around the globe (perhaps only excepting continental Europe) shale operators in the United Kingdom have to face a very committed and highly organized opponent, environmental activists. Opponents of shale gas drilling, staging one protest after another and causing disruptions at the sites, led Ineos and Cuadrilla to secure legal protection at their shale sites – the Preston Crown Court even jailed several anti-shale activists for blocking access in late 2018.

Lacking the competence to ban fracking altogether, Local councils in the UK also started to craft new creative ways on how to nip the government’s shale push in its bud – for instance, the mayor of Greater Manchester introduced a so-called “presumption” with regard to new shale gas developments, effectively meaning that the default position of the local council would be to ban new projects in view of Greater Manchester’s grand target of becoming carbon neutral. As Greater Manchester hosts 10 exploration licenses, this is no small feat. Other local councils have taken similar steps to restrict fracking – even the city of London made the case for a “climate emergency” as the mayor Sadiq Khan pushed for a blanket shale gas ban.

The Scottish government, availing itself of the freedom it has on the matter, has prolonged indefinitely its shale moratorium until an already agreed-upon permanent ban is placed in vigor. Similarly, the Welsh government held public consultations throughout last year and thereupon decided to freeze all license issuing procedures for shale oil and gas, regardless of whether fracking is used or not. To a certain extent, the reaction of the populace across Britain is fully understandable – the several shale gas development sites currently in action are considered a cautionary tale of what is to come unless the public does something about it. Cuadrilla, the only company currently fracking in the UK at its Preston New Road site near Blackpool in Lancashire, has had a series of 0.5 magnitude tremors in early December 2018 and was forced to halt it for a longer period after causing a 1.5 magnitude mini-earthquake mid-December.

All this runs counter to the research shale proponents put forward, stipulating that fracking’s impact would be like dropping a melon – in fact the more advanced the stage of the fracking, the more powerful were the earthquakes. Cuadrilla is reportedly looking to drill a second horizontal well at the same site, however, it remains to be seen how expedient would it be under current circumstances. All the more so as the UK’s shale gas commissioner, MP Natascha Engel, resigned last week from her position after a mere 6 months of work. Yet perhaps the biggest obstacle of any further shale gas advances in the United Kingdom would be its own High Court, which has ruled this March that the government’s amendments of the National Planning Policy Framework to speed up shale projects was unlawful.

Here we return to an oft-repeated mistake – the UK High Court has found that the government’s disregard for an environmental study (the “Mobbs Report”) presented by the anti-shale group Talk Fracking was undeniable and that the government indeed underestimated the extent of shale gas emissions arising from fracking, at the same time overestimating Britain’s shale potential. This opens up the possibility for other anti-shale and anti-fracking groups to question the government’s shale policy by means of judicial review. All in all, with a frustrated government, constrained companies and a very organized array of environmental groups, the United Kingdom is just a couple of steps away from giving up on its shale gas altogether.

via ZeroHedge News http://bit.ly/2WgIhGD Tyler Durden

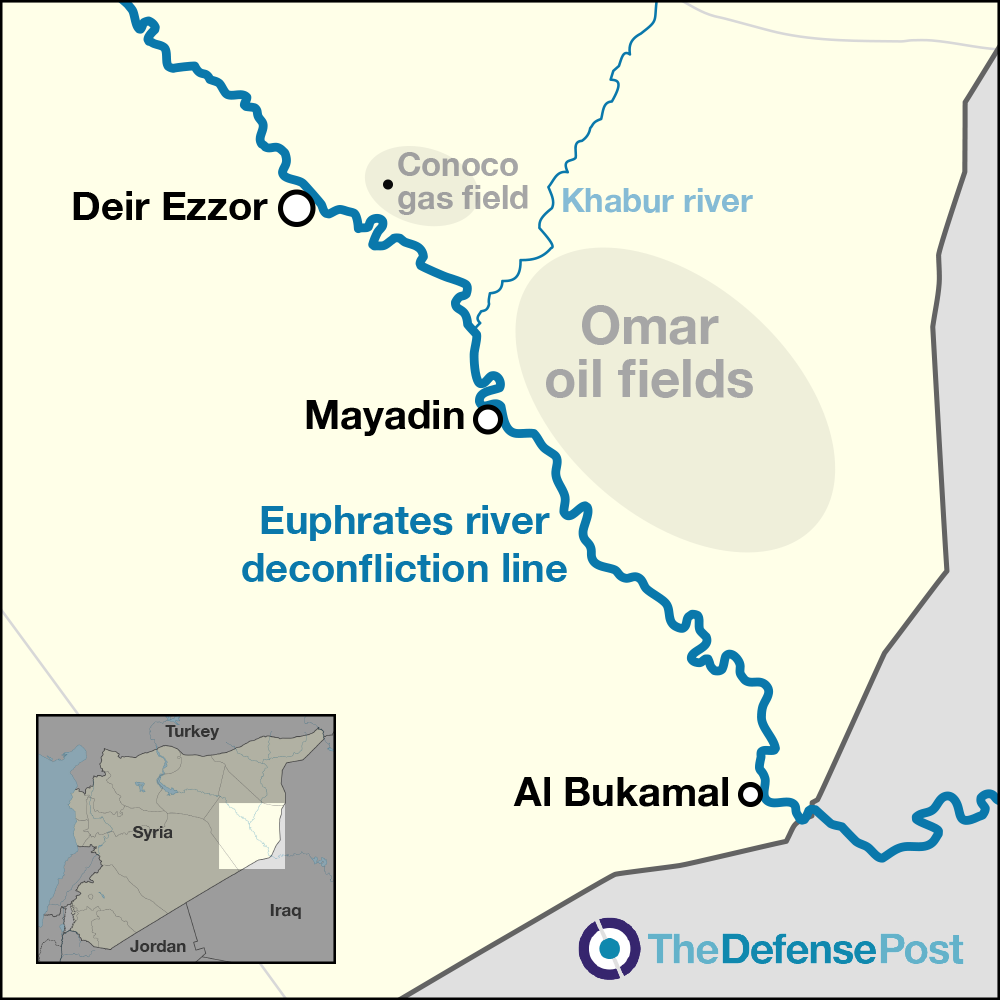

A high level Pentagon official has admitted that US forces will be in Syria for “the long haul” and coupled his statement by declaring the territory contains “a lot of the oil resources and arable land.”

The unusually frank remarks were made this week by Michael Mulroy, Deputy Assistant Secretary of Defense for the Middle East, while addressing a conference at the D.C. based Center for a New American Security (CNAS), months after President Trump appeared to have caved to his advisers, reversing course earlier this year from his stated goal of a full and rapid US troop exit from Syria.

al-Omar oil field in Deir Ezzor, Syria

Mulroy said “we have a very capable partner” — in reference to the primarily Kurdish Syrian Democratic Forces (SDF) — and quickly noted the US-trained SDF happens to occupy key regions in eastern Syria with “a lot of the oil resources and arable land,” and added that, “we are there with them”.

The Pentagon official further vouched for the think tank’s new feature policy recommendations on Syria which call among other things for continuing to “maintain a presence in over one-third of the country.”

Referencing the CNAS’ new policy report entitled “Solving the Syrian Rubik’s Cube,” regional Iraqi media outlet Kurdistan 24 reported:

Nicholas Heras, one of the study’s co-authors, spoke with Kurdistan 24. He explained that of the six scenarios considered in the report, “The option that we supported is that the United States should continue to maintain a presence in over one-third of the country” and “should invest more, both in terms of financial resources and personnel to stabilize” that region of Syria.

U.S. is in Syria for the long haul, says Michael Mulroy, Dep Ass Sec for Def. The US is “not in a bad situation” in Syria, Mulroy said, the country has “ a very capable partner,” & the territory contains “a lot of the oil resources & arable land.” https://t.co/X4ajRef49t

Earlier this month the SDF and western coalition forces declared total defeat over ISIS after fully securing the last ISIS holdout town of Baghouz.

Meanwhile, the majority of Syria’s population is now under the Syrian government, now reeling from the worst fuel shortage in the nation’s history as a result of new oil sanctions targeting Damascus and its ally Iran.

Even with the Islamic State’s territorial caliphate now long gone, major oil and gas sites like al-Omar oil field in Deir Ezzor province in Syria’s east remain controlled by the SDF and its US backers, something which Damascus has repeatedly condemned before the United Nations as an illegal violation of its sovereignty.

via ZeroHedge News http://bit.ly/2GUWG64 Tyler Durden

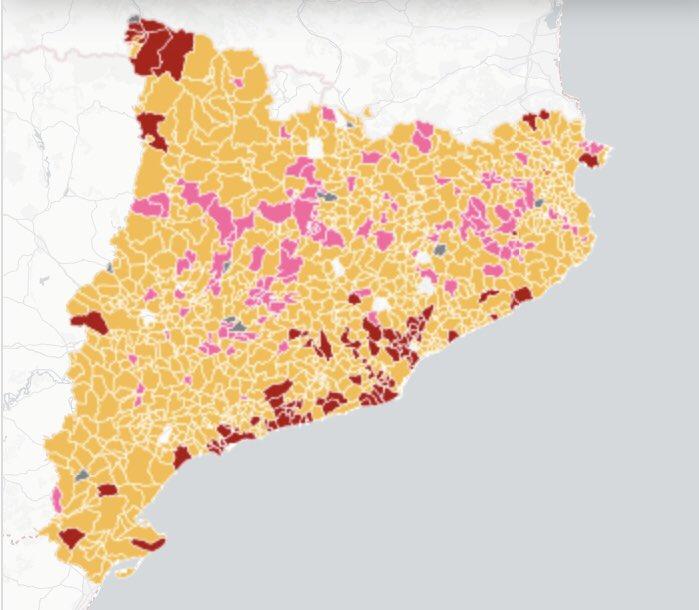

The Spanish General election in Catalonia was a stunning victory for the Catalan Separatists, their best ever election result, achieved despite their leadership being exiled or political prisoners and despite an avalanche of MSM propaganda against them. Four of those elected are currently in jail. The Spanish state has reacted by declaring the two major separatist candidates, Clara Ponsati and Carles Puigdemont, ineligible for the European Parliament elections.

The Catalan Republican Left won the biggest share of the vote, which negates the continued false propaganda being put about Catalonian Independence being a right wing movement. Over 60% of the vote in Catalonia went to avowedly left wing parties.

It is further worth noting that there is a very plain correlation between the geographical location of the 3.6% of the vote that the neo-fascists of Vox gained in Catalonia, and the Spanish occupation garrisons in the country.

You will struggle very hard indeed to learn any of the above facts from British mainstream media; I had to get them all from Catalan sources.

The Guardian has published 55 articles in the last three years boosting Ines Arrimadas, the leader of the Catalan branch of the right wing “Spanish” Citizens Party, including at least three op-eds written by Ines herself. The Guardian has sought relentlessly to portray public opinion in Catalonia as anti-Independence, and Arrimadas as its true representative.

Typical photo from the Guardian of their right wing anti-Catalan pin-up.

Yet in the Spanish General Election, Arrimadas’ party got only 11.6% of the vote in Catalonia. The right wing nationalist Spanish parties, the fascist Vox, the Francoist PP and Arrimadas’ foreign security service promoted Citizens, got a pathetic 20.1% of the vote between all three, in a stunning Catalan rejection of Spanish nationalism.

The Citizens Party started life as an astroturf effort to help counter the left-wing and anti-EU populism of Podemos. To that end it was funded and assisted by the German foreign intelligence service, the BND. It remains a favourite tool of foreign intelligence services, particularly MI6 which of course sees the links between Catalan and Scottish nationalism. Hence the peculiarly active link between Ciudadanos and MI6’s print media mouthpiece, the Guardian.

It is impossible to correlate directly from party results to potential referendum results, as a number of parties including Podemos and the Greens hold ambivalent positions on Independence, and a percentage of voters will have a view on Independence which differs from the party they support. For example a small but significant number of Socialist Party supporters of PM Pedro Sanchez, also support Catalan Independence.

Given the thuggish violence of Francoist paramilitary forces against the ordinary voters in Catalonia’s referendum, given the imprisoning and exile of its peaceful leadership, given the extraordinary Madrid dictated barrage of MSM propaganda, the Catalan nationalist victory in the General Election is a wonderful triumph for the human spirit.

Now you won’t hear that in the MSM.

via ZeroHedge News http://bit.ly/2IQeZLT Tyler Durden

World Health Organization analysis shows the countries in Europe where childhood obesity is most prevalent, revealing, as Statista’s Martin Armstrong points out, that the problem to be most pronounced in Mediterranean nations.

Regardless of gender, Cyprus is home to the largest share of obese 6 to 9 year olds.

{kind=link}