In a clarification that only created more confusion, Boeing said Monday that an alert intended to notify pilots when the plane might be receiving erroneous data from one of the 737 MAX 8’s ‘angle of attack’ sensors wasn’t disabled intentionally, as WSJ reported on Sunday, but that the feature had been disabled because of a previously undisclosed software glitch.

What’s confusing is that Boeing had confirmed WSJ’s story that the aerospace company had neglected to tell the FAA and Southwest, the biggest customer for the 737 MAX 8, that the alert feature had been disabled because it had been made a new ‘optional’ safety feature. The alerts would have warned pilots that the plane’s MCAS system might be about to misfire.

However, the airline appears to have changed its story, offering little clarification as to why. During Boeing’s shareholder meeting in Chicago on Monday, CEO Dennis Muilenburg repeated the company’s claim that the alerts were a ‘non-essential’ feature, however, given the fact that the misfire of Boeing’s MCAS system (which Muilenburg also insisted wasn’t an ‘anti-stall’ system, as it has been regularly described in media reports, but instead characterized it as a safety system) is widely suspected to have caused the crashes of Lion Air and an Ethiopian Airlines flights that together killed nearly 350 people makes this claim difficult to believe.

The company said that it didn’t intentionally deactivate the alerts, and that they had only been disabled because of the software issue.

Boeing is now saying that its engineers, as well as safety regulators at the FAA, either missed or overlooked the software glitch that rendered these alerts inoperable, presumably even on planes where the extra safety features had been paid for. The alerts had been standard on earlier models.

The Monday statement suggests Boeing engineers and management, as well as U.S. air-safety regulators, either missed or overlooked one more software design problem when the model was certified two years ago.Before Monday, neither Boeing nor the Federal Aviation Administration had disclosed that an additional software glitch—rather than an intentional plan by the plane maker—rendered so-called angle of attack alerts inoperable on most MAX aircraft. The alerts warn pilots when there is a disagreement between two separate sensors measuring the angle of a plane’s nose.

Boeing’s disclosure comes as the plane maker scrambles to win FAA and international approval of a software fix for MCAS, making it less potent and less likely to misfire. In addition to the challenges already facing the MAX fleet, revelations of the additional software difficulties are likely to be scrutinized by airlines, passengers and regulators world-wide as Boeing strives to restore their trust and return the MAX fleet to service.

The alerts, intended to tell cockpit crews if sensors are transmitting errant data, had been standard on earlier 737 models. Officials at airlines around the globe, including Southwest Airlines Co., the largest 737 MAX customer, assumed the alerts remained standard until details emerged in the wake of the Lion Air crash. At that point, the industry and FAA inspectors monitoring Southwest realized the alerts hadn’t operated on most MAX aircraft, including Southwest jets.

Ultimately, Boeing’s admission of this glitch could make winning FAA approval to allow the planes to return to the skies even more difficult, and it’s also bound to make international regulators more wary of Boeing’s updated flight software, which the company has said is being designed to make MCAS less powerful, and more quickly identify when a plane’s sensors are feeding it erroneous data.

Despite the bad news, which could further weigh on new 737 orders by prolonging the grounding, Boeing shares traded slightly higher on Tuesday, and remained up on the year.

via ZeroHedge News http://bit.ly/2DFfmo6 Tyler Durden

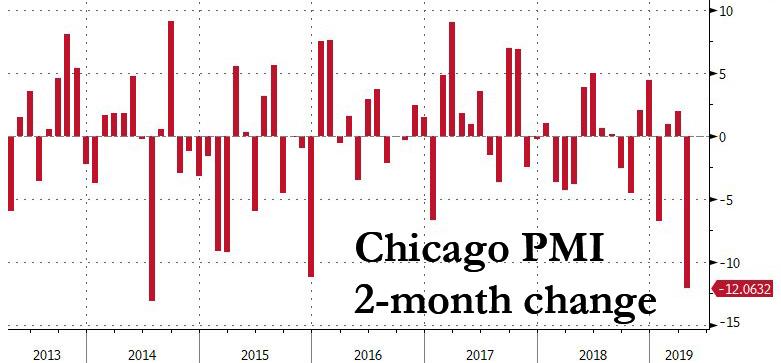

Just hours after China reported disappointing PMI data across the board, with both manufacturing and services surveys posting a drop to levels just above contraction…

… the latest Chicago PMI confirmed that the slowdown is accelerating in the US, as the index tumbled to 52.6 from 58.7, and sharply below the 58.5 estimate. It was also the lowest print since January 2017.

The details:

Forecast range 56 – 62 from 25 economists surveyed

Business barometer rose at a slower pace, signaling expansion

Prices paid rose at a slower pace, signaling expansion

New orders rose at a slower pace, signaling expansion

Employment rose at a slower pace, signaling expansion

Inventories fell at a slower pace, signaling contraction

Supplier deliveries rose at a slower pace, signaling expansion

Production rose at a slower pace, signaling expansion

Order backlogs rose and the direction reversed, signaling expansion

More notably, the two-month plunge in the PMI was breathaking and after printing at 64.7 in February, the index has plunged 12.1 points in the past two months, its biggest drop since mid-2014.

And with all that, it now appears that China’s gargantuan credit injection which was 40% greater than a year earlier, has now been exhausted and the credit impulse tailwind is over.

via ZeroHedge News http://bit.ly/2GUiC17 Tyler Durden

As if the past months of US push for regime change in Venezuela with officials like Elliott Abrams of Iran-Contra conviction infamy at the helm wasn’t bizarre enough, things just got weirder, as Erik Prince has apparently been pitching a plan around Washington to privatize US coup efforts using his latest Blackwater inspired mercenary empire.

According to Reuters, Prince — the brother of billionaire Education Secretary Betsy DeVos who has over the past years since selling his mired-in-controversy Blackwater group (now Academi) revived his mercenary empire in China in the form of Frontier Services Group (FSG) — intends to “deploy a private army to help topple Venezuela’s socialist president, Nicholas Maduro”.

Prior file photo of Prince during Congressional committee hearing, via Getty/NPR

Price has reportedly sought access to Trump administration officials to whom he’s attempting to pitch the whole operation, said to involve some 5,000 soldiers-for-hire to be used by opposition leader Juan Guaido, according to multiple sources who spoke to Reuters. The controversial private security CEO has sought investments from both Trump supporters and wealthy Venezuelan exiles, and reportedly held meetings over the plan as recently as mid-April.

Neither the White House nor Guaido opposition representatives have confirmed they were entertaining such a plan, with the latter denying altogether that Guado’s team had even spoken with Prince or FSG reps.

Reuters’ sources described some of the details of the proposed Venezuela coup plan as follows:

The two sources with direct knowledge of Prince’s pitch said it calls for starting with intelligence operations and later deploying 4,000 to 5,000 soldiers-for-hire from Colombia and other Latin American nations to conduct combat and stabilization operations.

Perhaps the most interesting detail to be revealed is the need for a triggering event that could set a final bid for coup over the top, after a number of small attempts failed to gain enough momentum in the past months.

Reuters’ sources described what Prince called a “dynamic event”:

One of Prince’s key arguments, one source said, is that Venezuela needs what Prince calls a “dynamic event” to break the stalemate that has existed since January, when Guaido – the head of Venezuela’s National Assembly – declared Maduro’s 2018 re-election illegitimate and invoked the constitution to assume the interim presidency.

In 2017, Prince is known to have lobbied the Trump administration for using private contractors to stabilize the Middle East.

He’s made headlines last year after pitching an idea to privatize the wars in Afghanistan and Syria to Trump administration officials, which has reportedly met with little progress, though there were some indicators Trump could be open to the idea.

Iraq-style mercenary occupation of Venezuela? Erik Prince hopes so…

Image source: “Silent Professionals” blog

To the shock and surprise of many, a subsidiary of his Hong Kong-based Frontier Services Group has been allowed to operate in Iraq, showing up in the southern city of Basra, after both Prince and Blackwater were formally barred by Iraq’s government from ever entering the country again following the 2007 Nisour Square massacre.

As for Venezuela, things look to slowly destabilize further as continued total economic collapse fuels an ongoing humanitarian emergency, and on news of more armed uprisings by military defectors backing Guaido come out of Caracas.

via ZeroHedge News http://bit.ly/2Weatdh Tyler Durden

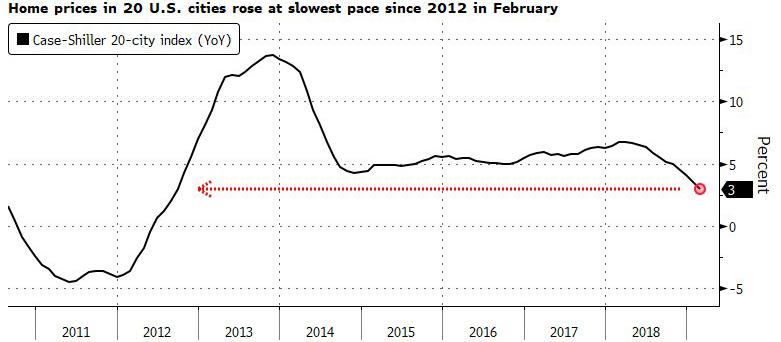

The slowdown in the US housing market is, well, accelerating.

Following last month’s disastrous starts and permits data, the Case Shiller’s home price index was expected to show growth continuing to slow. and it did, considerably worse than expected.

Case-Shiller’s 20-City Composite grew at just 3.00% YoY in January (just above the 2.95% YoY expectation but sharply below March’s 3.51% YoY print). This is the weakest annual growth since September 2012, decelerating for an 11th month in January as buyers held out for more affordable properties. At the national leve, home prices grew at just a 4% rate, the smallest gain since 2012.

“The pace of increases for home prices continues to slow,” said David Blitzer, chairman of the S&P index committee. “Prices generally rose faster in inland cities than on either the coasts or the Great Lakes.”

Some more details:

As has been the case for much of the past decade, all 20 cities in the index showed year-over-year gains, led by a 9.7% increase in Las Vegas and 6.7 percent in Phoenix.

Increases have slowed considerably over the past year in California, with San Francisco, San Diego and Los Angeles all recording annual gains of below 2 percent. Seattle, another previously hot city, showed an advance of just 2.8 percent.

Prices in 17 cities rose from the prior month on a seasonally adjusted basis, led by Tampa.

What is odd is that despite alleged wage gains and lower interest rates and borrowing costs, buyers have still been holding out for more affordable properties.

That said, as Bloomberg notes, price gains may pick up in the coming months amid signs of strength in demand as the latest new home sales report showed the fastest increase since 2017, while applications for loans to buy homes recently hit the highest weekly level in almost nine years.

Meanwhile, keep an eye on pending home sales later on Tuesday for a better sense of momentum in the housing market in the first half of the year. Analysts project contract signings rose for the second time in three months.

via ZeroHedge News http://bit.ly/2UPXUTF Tyler Durden

Albert Einstein once wrote that “the definition of insanity is doing the same thing over and over again and expecting different results.” Were he alive today, he would be repeating the line to anyone who would listen, especially the reporters on cable news channels such as CNBC. He might add that the world’s policymakers always approach oil market disruptions in the same way: predicting there will be no impact on prices.

Einstein would then point out that the policymakers are consistently wrong. A hefty price boost has followed every disruption.

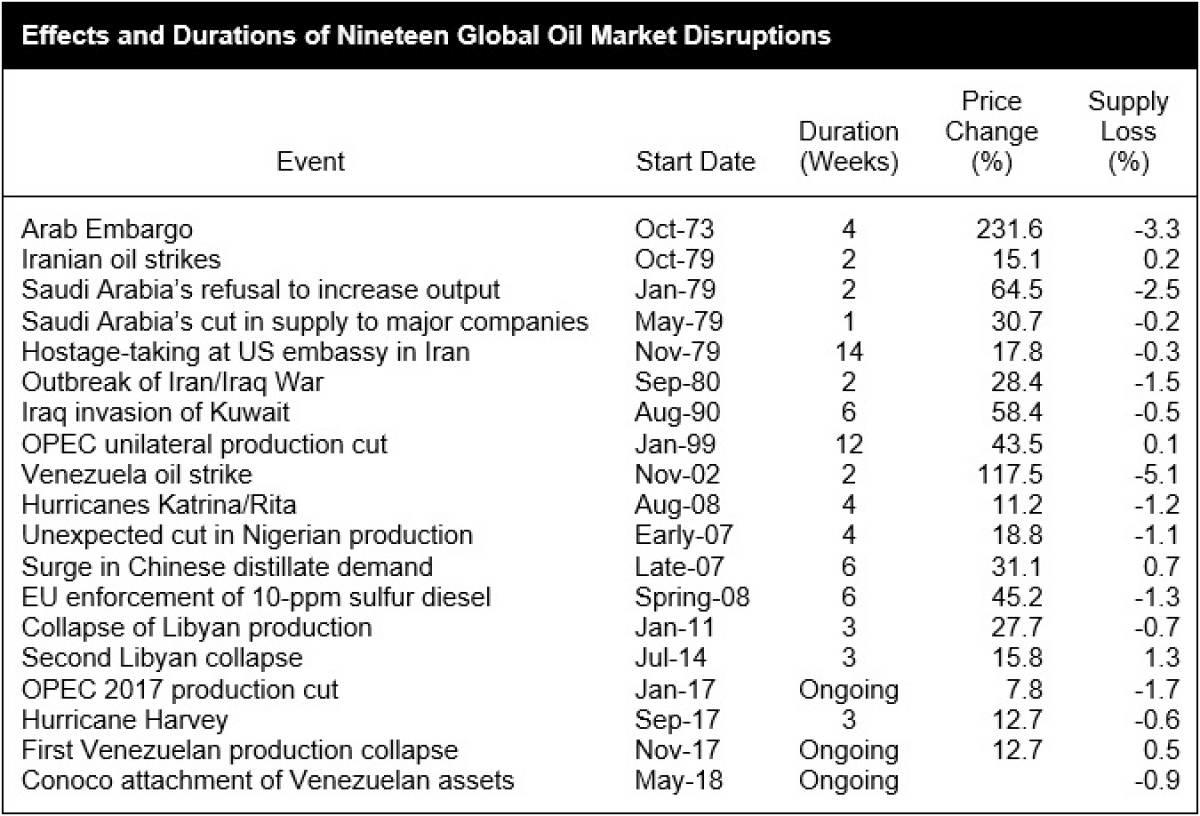

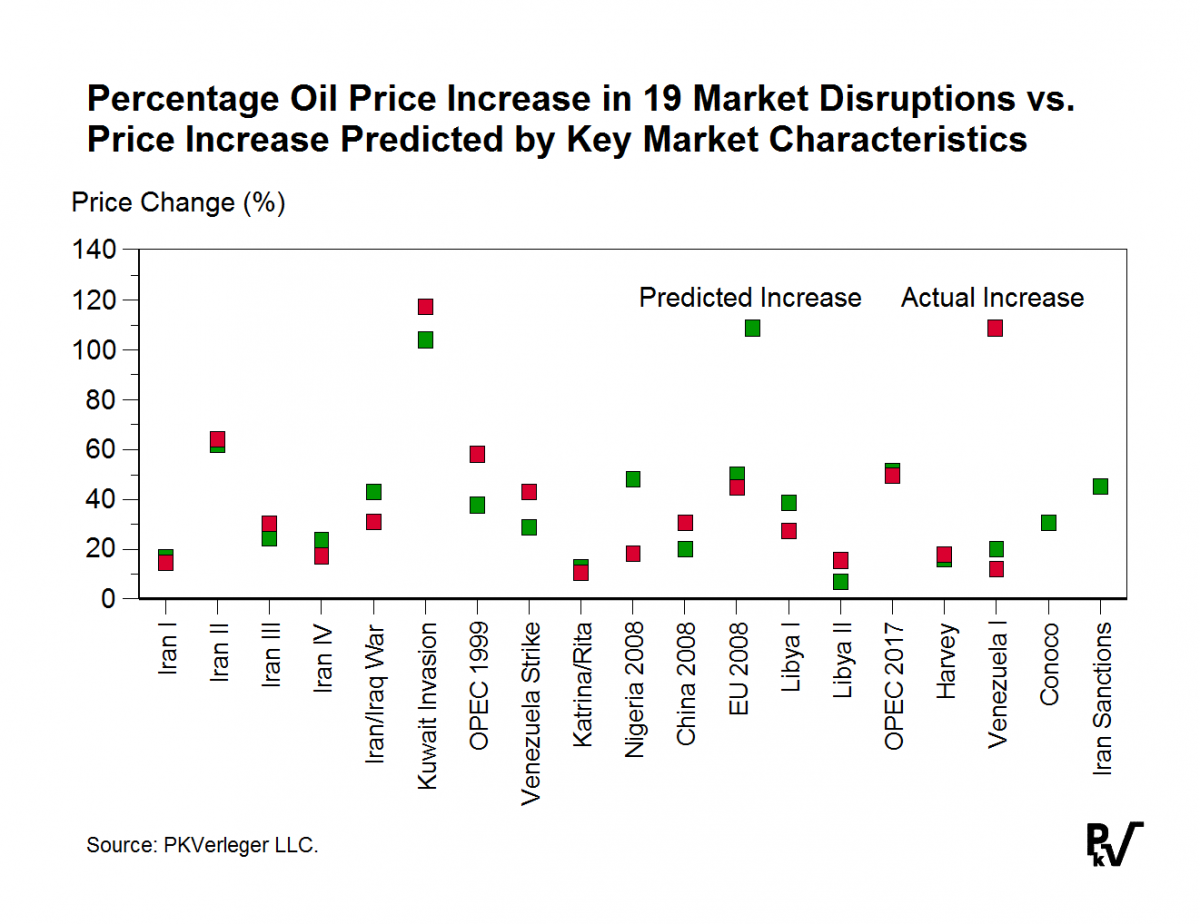

The world has experienced nineteen oil market disruptions over the last forty years. In a paper published in March 2018, I chronicled these events and noted that the maximum price increase was predictable. Last Monday, Secretary of State Mike Pompeo initiated the twentieth disruption. The consequences are projected here.

Start, though, with the energy policy insanity. In each of the disruptions since 1973, I have noted the following regarding government officials.

State Department representatives always say something like “the US Department of State remains in contact with our partners to reduce the risk of supply disruptions. There is sufficient oil supply in the global markets that countries can access.”

OPEC officials always spout some version of “the oil market remains well-supplied, with the recent price driven by geopolitics, not fundamentals.”

Nothing has changed. Last week Reuters offered this quote from the State Department’s Brian Hook, the person running the Iran sanctions program:

“There’s roughly a million barrels per day (bpd) of Iranian crude (exports) left, and there is plenty of supply in the market to ease that transition and maintain stable prices,” said Brian Hook, U.S. Special Representative for Iran and Senior Policy Advisor to the Secretary of State, speaking in a call with reporters.

Meanwhile, Saudi energy minister Khalid al-Falih toldFinancial Times that Saudi Arabia would not boost production immediately, adding that “the market is ‘well supplied’ and inventories continue to rise despite the sanctions against Iran’s oil exports.”

Mark Twain is thought to have said that “history does not repeat, but it rhymes.” In this case, it repeats. Policymakers have learned nothing in forty years.

The table below lists the nineteen market disruptions. I prepared it in 2018 at a time when Conoco had just used an award of $2 billion granted against Venezuela to seize the latter’s assets in Curacao and when production in Nigeria suffered a disruption. For each event listed, the table shows the start date, the duration, the maximum price increase associated with it, and the percentage loss in supply.

(Click to enlarge)

I took these data and developed a model that predicted the price increase associated with seventeen of the nineteen disruptions, excluding the Arab Embargo and the Conoco attachment of Iranian assets. The model explained seventy percent of the price variation. The graph below compares the actual and predicted price changes for each disruption.

(Click to enlarge)

I note here that I based this model on results published in 1982 in Oil Markets in Turmoil, a book I wrote while teaching at Yale. The volume provides a quantitative approach to evaluating oil market disruptions.

The findings from the model indicate that the current disruption will likely cause prices to increase sixty-six percent at their peak. Roughly speaking, Brent will rise to between $114 and $126 per barrel.

This conclusion results from my calculation that the present episode will take roughly two percent of supply from the market.

The reduction will come from falling Venezuelan production, which is also subject to US sanctions, the declining Iranian exports, and a modest cut in Libyan exports.

The latest issue of The Economist warns that “the risk of an oil price shock is increasing.” The editors are correct.

Thinking of the Einstein quote above, I end by paraphrasing the title of a great book by Carmen Reinhart and Kenneth Rogoff: “This time will not be different.”

via ZeroHedge News http://bit.ly/2GSVHmG Tyler Durden

Futures dipped after the Wall Street Journal reported that punitive tariffs exchanged between China and the United States are now posing a major obstacle in ongoing trade talks between the two nations.

US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin resume high-level talks with China on Tuesday – which will be followed next week by their counterparts traveling to Washington next week for another round of talks which officials and business groups say could result in a deal.

That said, “how and whether to remove the tariffs the two governments imposed in the earliest phases of the dispute are now at the forefront of the talks,” according to the Journal, citing people briefed on the negotiations.

At issue is how much of the tariffs the U.S. levied on $250 billion of Chinese goods will be removed, according to the people. The U.S. wants to leave some in place as a tool to enforce the agreement while Chinese negotiators see those tariffs as an affront, and negotiators have batted the issue back and forth for at least a month. –Wall Street Journal

“The tariffs are the leverage to move the deal past the finish line,” said Jake Parker, Vice President of the US-China Business Council in Beijing. “It’s natural the details of drawdown timelines would be among the last items negotiated.”

U.S. Trade Representative Robert Lighthizer, center, arrives at a Beijing hotel Tuesday ahead of the latest round of U.S.-China trade talks. PHOTO: GREG BAKER/AGENCE FRANCE-PRESSE/GETTY IMAGES

Aside from Tariffs, the negotiators are trying to find solutions in other areas – such as persuading Beijing to expand access to China’s cloud computing market and agricultural markets, according to business and farm groups.

Neither Mr. Lighthizer nor Mr. Mnuchin would comment on specifics as they walked past reporters after arriving in Beijing. Mr. Mnuchin said that the focus of this week’s talks is “broad” and that “we’ve made a lot of progress.”

On Monday Mr. Mnuchin told Fox News that the enforcement mechanism still “needs a little bit of fine tuning” and that “if we get to a completed agreement, it will have real enforcement provisions.” –Wall Street Journal

According to people familiar with Beijing, their primary concern is that the US continues to insist on imposing tariffs, while preventing China from retaliating in order to make sure Beijing fulfills commitments in a trade deal.

“Beijing absolutely doesn’t want to give in on this,” said one WSJ source, who noted that the tariffs would be an embarrassment for leadership and a tough sell to Chinese businesses and domestic counterparts. Investors are also taking note.

“The U.S. has already hurt the confidence of the Chinese people,” by initiating a trade war, and should eliminate tariffs immediately upon inking a deal, according to Mei Xinyu – a senior researcher at the Chinese Academy of International Trade and Economic Cooperation – a think tank affiliated with the Commerce Ministry.

“Bringing back tariffs would break any trust even further.”

via ZeroHedge News http://bit.ly/2LeBSL4 Tyler Durden

If ever we needed proof of the expression that “guns don’t kill people, people kill people” look no further than Britain, where families may have to start practicing cutting their steak and bread at dinner with a spoon. This is, of course, because Britain’s politicians have now made the absurdly ridiculous move to call for the banning of what Reason magazine called “the most useful tool ever invented” – the knife.

Reason reported this morning that British politicians have “declared war on knives” and are moving swiftly to try and ban them, since gun laws aren’t working to help stop crime altogether:

Having failed to disarm criminals with gun controls that they defy, British politicians are now turning their attention to implementing something new and different: knife control. Because criminals will be much more respectful of knife laws than of those targeted at firearms, I guess.

“No excuses: there is never a reason to carry a knife. Anyone who does will be caught, and they will feel the full force of the law,” London’s Mayor Sadiq Khan tweeted on April 8.

Not to be outdone, his predecessor, Boris Johnson, currently Foreign Secretary, called for increased use of stop-and-search powers by police. “You have got to stop them, you have got to search them and you have got to take the knives out of their possession.”

The insanity disguised as regulation continues to get worse:

British politicians propose banning home delivery of knivesand police promote street-corner bins for the surrender of knives while also conducting stings against knife vendors. Their goal is to “target not only those who carry and use knives, but also the supply, access and importation of weapons.”

It all sounds all so familiar, doesn’t it? And yet so utterly pointless. If British authorities have been unable to block criminals’ access to firearms—mechanical devices that require some basic mechanical skill to manufacture, or at least a 3D printer—how are they going to cut off the flow of knives, which require nothing more than a piece of hard material that can take an edge?

There are also practical downsides to discouraging the public from possessing knives—one of the oldest and most useful tools ever invented. Poundland, after all, isn’t dropping the sale of combat blades; the company’s move applies specifically to the tools people use to make their meals. The law looks much more likely to inconvenience peaceful people planning to carve a roast than to put off thugs who, push comes to shove, can find a way to sharpen a piece of rebar against a rock.

This nonsense comes in the wake of a growing number of stabbings since Britain outlawed guns altogether. While Britain can now boast, as Piers Morgan famously did in his interview with Alex Jones, that they were only about 30 gun murders in Britain in the year prior, British politicians failed to notice that crime continues to happen, just through different means. It became clear when Britain’s crime stats were put up against those of gun toting New Yorkers. From Reason:

A flurry of recent headlines reveal that London now has a higher murder rate than New York City, a metropolis of nearly identical population and one long considered more vulnerable to crime. “London police investigated more murders than their New York counterparts did over the last two months,” Reuters reported earlier this month. “In the latest bloodshed, a 17-year-old girl died on Monday after she was found with gunshot wounds in Tottenham, north London, a day after a man was fatally stabbed in south London.”

Commentators note that this may be a blip and that New York City’s murder rate for 2017 stood at more than double that for London. In fact, London’s murder rate really hasn’t risen much—instead, New York’s has dropped dramatically. But that still represents a big shift. In her 2002 Guns and Violence: The English Experience, historian Joyce Lee Malcolm noted that “New York City’s homicide rate has been at least five times higher than London’s for two hundred years. For most of that time, there were no serious firearm restrictions in either city.”

New Yorkers didn’t need firearms to exceed the bloodlust of their trans-Atlantic rivals. Even if you removed crimes committed with guns from the comparison, “New Yorkers still managed to outstab and outkick Liverpudlians by a multiple of 3 and Londoners by a multiple of 5.6″ over those two centuries,” wrote the late Eric H. Monkkonen in Murder in New York City, published in 2000.

We detailed this asinine knife ban in a series of articles we’ve been writing, the latest of which came on April 10.

Dr John Crichton, the new chairman of the Royal College of Psychiatrists in Scotland, wants the sale of pointed kitchen knives to be banned to help reduce the number of fatal stabbings.

Dr Crichton, who took on the role of chairman in June this year, is championing a switch to so-called “R”-bladed knives, which have rounded points and are far less effective as weapons.

As The Express detailed, he said that research shows many attacks, particularly in households where there has been a history of violence, involve kitchen knives because they are so easily accessible. Dr Crichton believes a switch from sharp-pointed, long-bladed knives to the new design could save lives.

“This is a public health measure and public health measures are always about society deciding on a self-imposed restriction for the public good.”

As ridiculous as the idea of the knife ban sounds, it hasn’t stopped its advocates from beating the drum even harder over recent weeks. However, let us tell you how this is going to work out, for those that don’t already know. We think that politicians will be shocked to find that similar circumstances take place with the knife ban as they did with the gun ban. Criminals will find a different method to commit violent crimes and those who don’t obey the law to begin with certainly won’t be deterred by more regulation.

However, if you’re a law abiding citizen in Britain preparing dinner for 10 from scratch at your house, you may find things a little more inconvenient in the comfort of your own home. Thanks politicians and regulators!

via ZeroHedge News http://bit.ly/2LsbrSj Tyler Durden

One stock analyst revealed on Monday that flight tracking data showed Occidental Petroleum’s corporate jet had flown to Omaha over the weekend, prompting them to speculate that Oxy might be trying to bring Warren Buffett into the deal to help finance its takeover of Anadarko Petroleum.

As it so happens, that assessment was absolutely spot on.

According to CNBC, a day after Anadarko said it was leaning toward Oxy’s higher bid, Buffett has confirmed that Berkshire is getting involved in the bidding war between Oxy and Chevron. Berkshire has committed to invest $10 billion in Occidental Petroleum contingent on the company completing the takeover of Anadarko.

Buffett’s backing will undoubtedly strengthen Oxy’s hand as its squares off with the much larger Chevron, which could still up its offer for Anadarko. With Buffett backing Oxy, it’s more likely that Chevron will walk away from the deal with the $1 billion breakup fee it would be owed by Anadarko. Though Chevron still has the financial heft to see the deal through if it commits to doing so.

Berkshire will receive 100,000 shares of cumulative perpetual preferred stock with a value of $100,000 a share.

The conglomerate also gets a warrant to purchase up to 80 million shares of Occidental at an exercise price of $62.50 a share.

The preferred stock will accrue dividends at 8% annually.

Oxy CEO Vicki Hollub, who had pledged to sell off some $15 billion in assets to help finance the acquisition, said she was “thrilled” to have Buffett on board.

Berkshire’s involvement in the deal will undoubtedly be widely discussed at Berkshire’s annual shareholder meeting this weekend.

via ZeroHedge News http://bit.ly/2XROngU Tyler Durden

This past weekend, we discussed the breakout of the markets to all-time highs.

The question I asked this past weekend was simply;

“The bull market is back, but can it stay?”

When I was growing up my father, probably much like yours, had pearls of wisdom that he would drop along the way. It wasn’t until much later in life that I learned that such knowledge did not come from books, but through experience. One of my favorite pieces of “wisdom” was:

“Exactly how many warnings do need before you figure out that something bad is about to happen?”

Of course, back then, he was mostly referring to warnings he issued for me “not” to do something I was determined to do. Generally, it involved something like jumping off the roof with a queen-sized bedsheet convinced it was a parachute.

My argument was always that “everyone else is doing it.”

After I had broken my wrist, I understood what he meant.

(What’s funny is that I am having the same conversations with my son today, and he is determined to figure out things the hard way simply because “everyone else is doing it.” Now, I truly understand what I put my Father through.)

Likewise, investors are currently rushing to get back into the market, after bailing out in December, with a near reckless disregard for the consequences.

Simply because “everyone else is doing it.”

So, before you go “jumping off the roof with a bed sheet for a parachute”, there are some warning signs to consider before taking that leap.

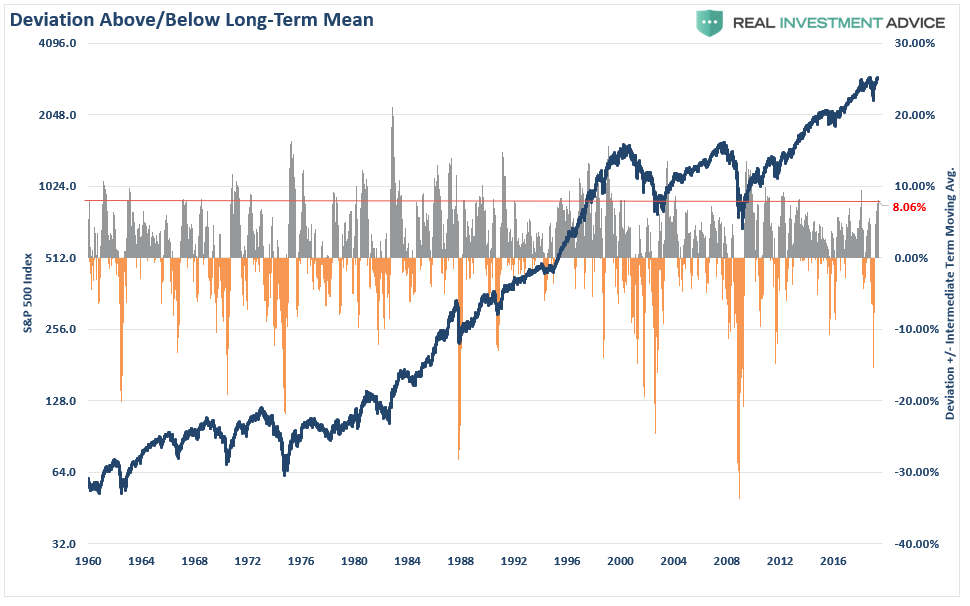

Warning 1: Deviations From The Mean

There is a funny story about a “defensive driving” class where the instructor asks the class how many thought they were “above average drivers.” About 80% of the class raised their hands. The funny thing is that all of them were in the class because of traffic violations or accidents. But more to the point, 80% of drivers cannot be above average. It is mathematically impossible.

Likewise, in investing, prices must be both above and below the “average price” over a set period of time for there to be an average. To many degrees “price” is bound by the laws of physics, the farther from the “average price” the current price becomes, the greater the pull back to, and generally beyond, the average. This is shown in the daily chart below.

Currently, the market is more than 8% above its longer-term daily average price. These more extreme deviations tend not to last an extraordinarily long time. Furthermore, reversions from these more extreme deviations tend to be rather quick.

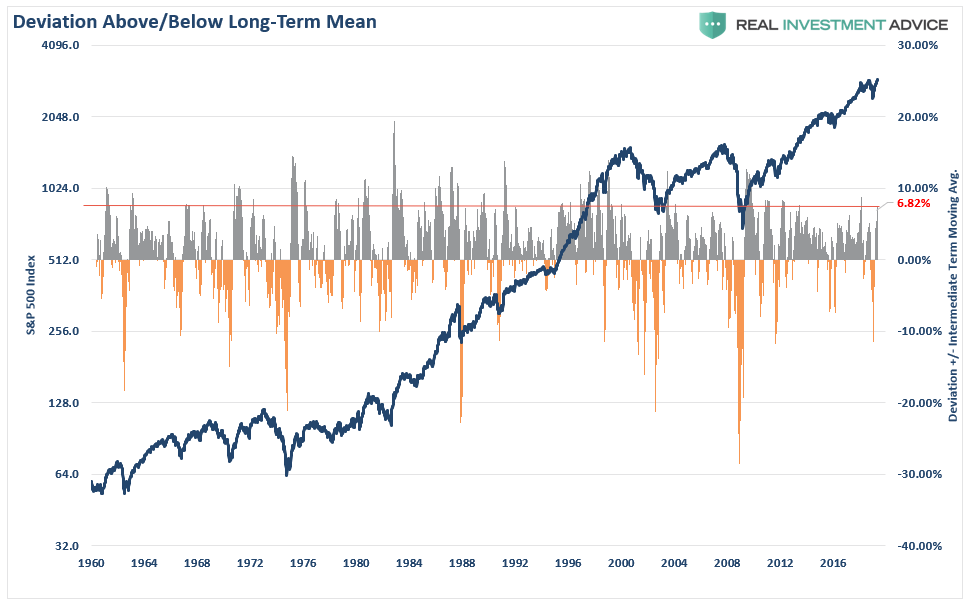

If we step out to a weekly basis, we see the same warning.

At almost 7% above the long-term weekly moving average, the market is currently pushing the upper end of historical deviations.

The important point to take away from this data is that “mean reverting” events are commonplace within the context of annual market movements.

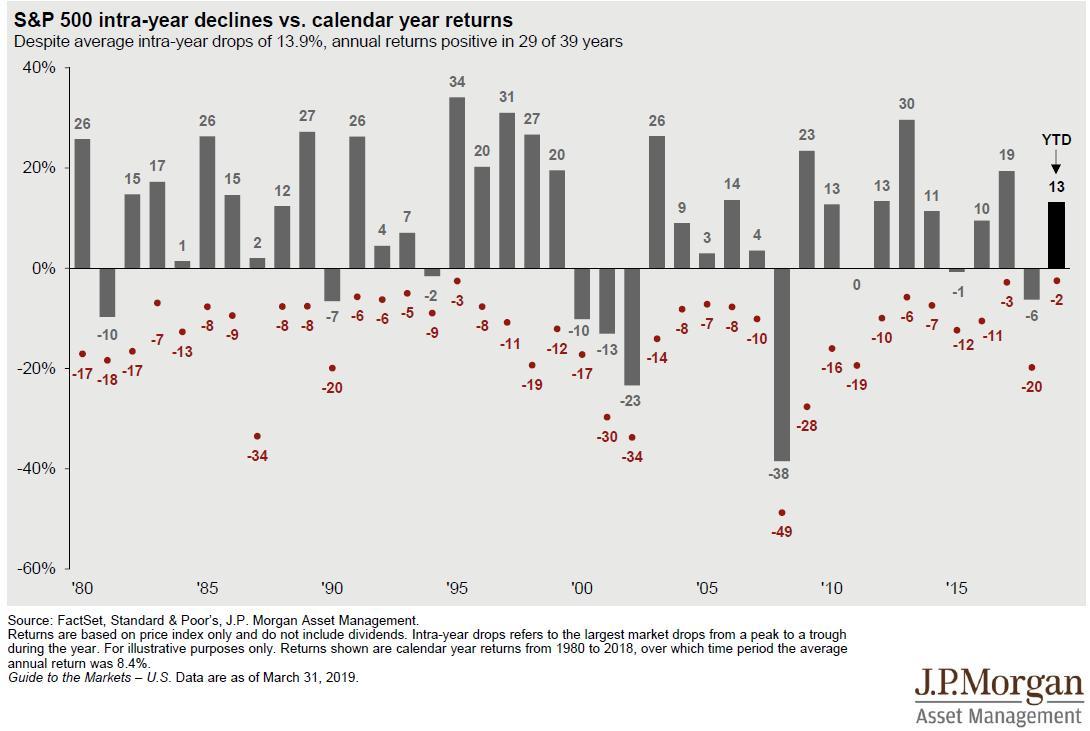

Currently, investors have become extremely complacent with the rally from the beginning of the year and are quick extrapolating current gains through the end of 2019.

As shown in the chart below this is a dangerous bet. In every given year there are drawdowns which have historically wiped out some, most, or all of the previous gains. While the market has ended the year, more often than not, the declines have often shaken out many an investor along the way.

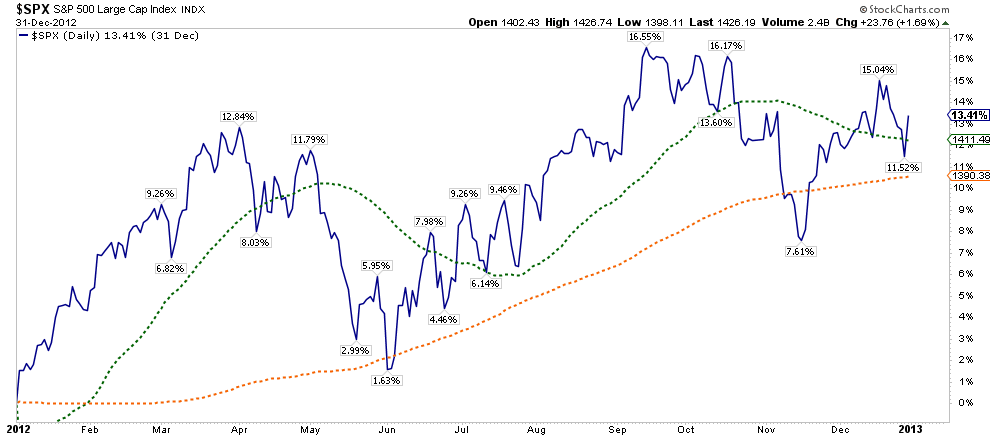

Let’s take a look at what happened the last time the market started out the year up 13% in 2012.

So far, it looks a whole lot like this year.

From a portfolio management standpoint, the reality is that markets are very extended currently and a decline over the next couple of months is highly likely. While, it is quite likely the year will end on a positive, particularly after last year’s loss, taking some profits now, rebalancing risks, and using the coming correction to add exposure as needed will yield a better result than chasing markets now.

Warning 2 – Technical Warnings

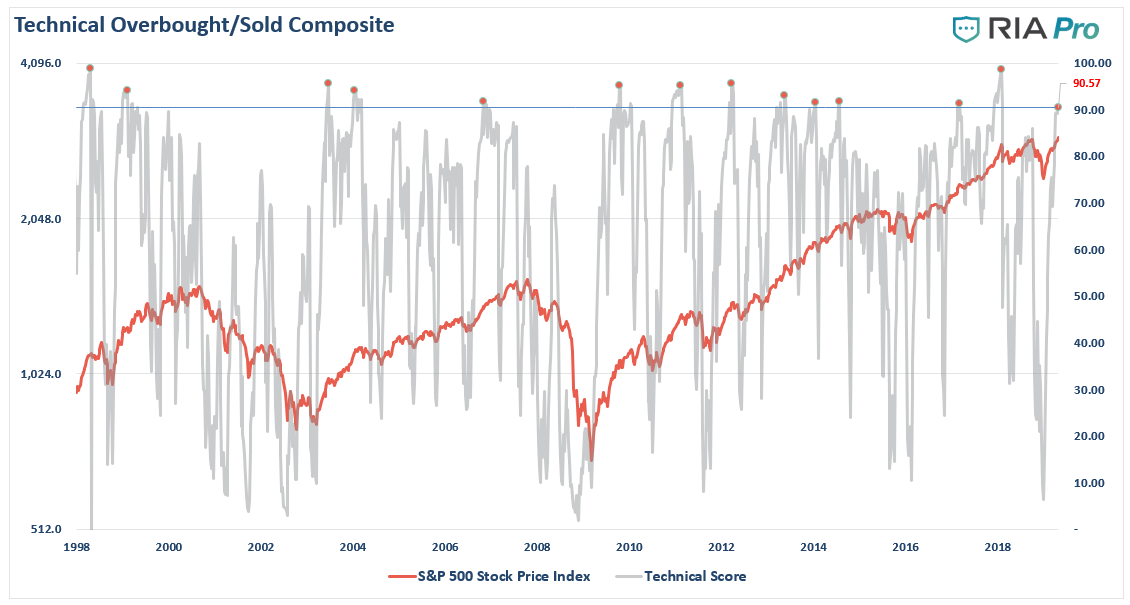

The technical warnings also confirm our concerns about a near-term correction.

Each week, we post the chart below for our RIA PRO subscribers which is a composite index of our weekly technical measures including RSI, Williams %R, Stochastics, etc. Currently, the overbought condition of the market is near points which have denoted more significant corrections.

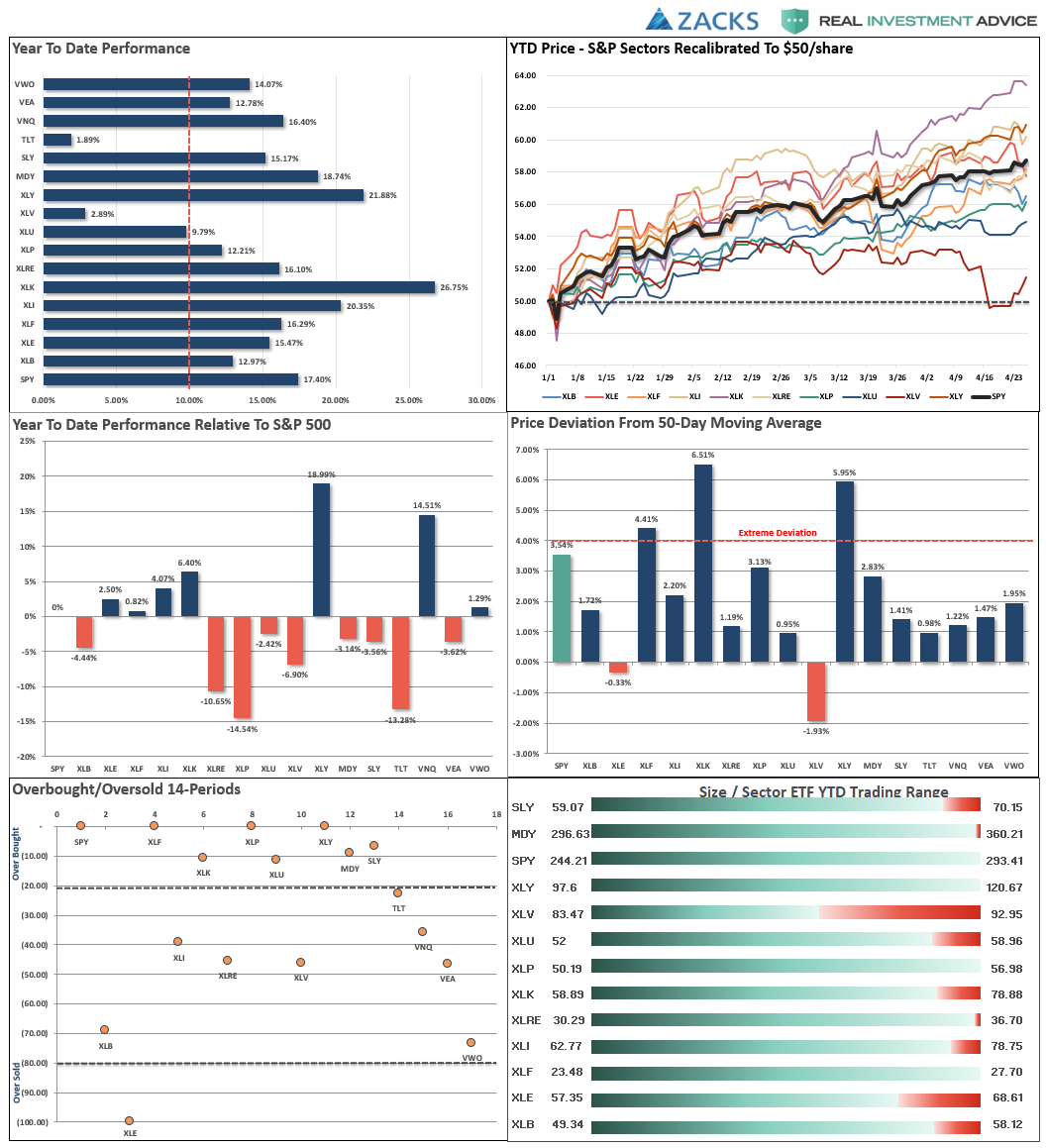

The market/sector analysis, which is also exclusive to RIA PRO members, shows the rather extreme price deviation in Technology, Discretionary, and Financials. Also, relative performance shows that it has primarily been Technology and Real Estate providing a bulk of the “alpha” year-to-date.

These are abnormalities that tend not to last long in isolation and rotations tend to occur rather quickly.

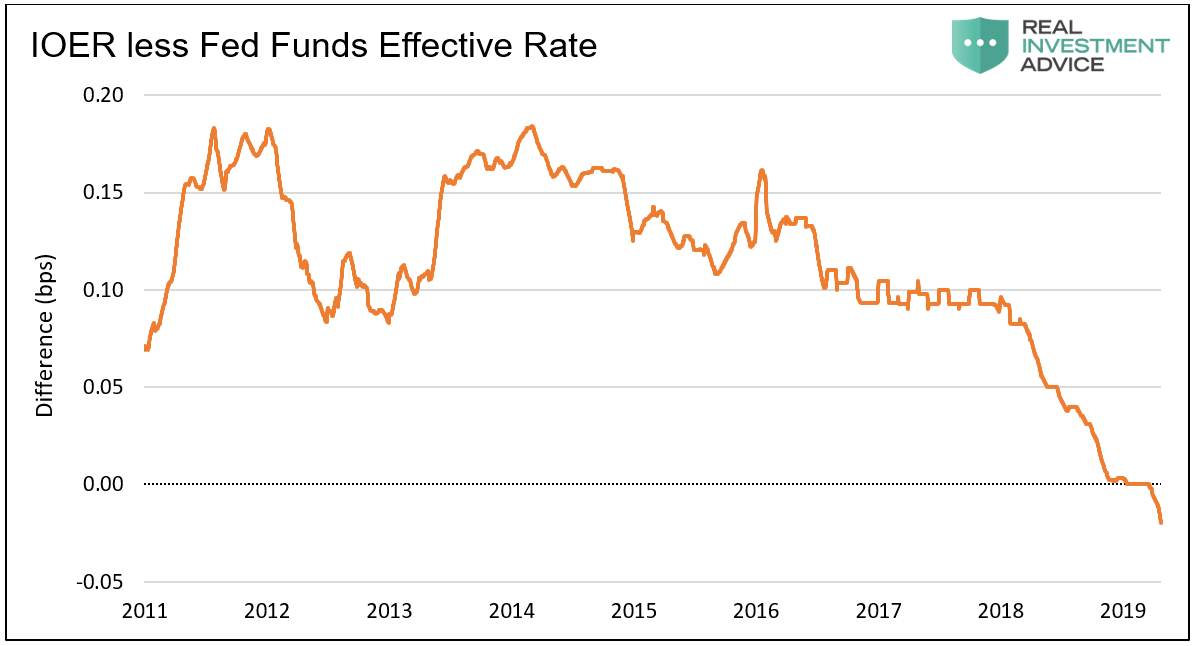

Warning 3 – Dollar Surge/Shortage

One of the lesser known issues with the markets currently was addressed by my co-portfolio manager, Michael Lebowitz, CFA:

When the Fed embarked on QE, they wanted to ensure that the money created to buy Treasuries and mortgages was being held by the banks as excess reserves and not being used to form loans. They also knew that controlling the Fed Funds rate would become problematic given the sharp increase in potential banking reserves. To help them keep the money on the sidelines and better control the Fed Funds rate, the Fed decided to pay banks interest on excess reserves (IOER). The IOER rate was set above the Fed Funds rate (the rate banks lend reserves to other banks on an overnight basis). The thought being that banks would rather collect a higher interest rate and take no risk than lend out money to other banks at a lower interest rate. On the flip side, if Fed Funds rose to the IOER rate, the banks would lend their reserves which should, in theory, provide a cap for Fed Funds.

The IOER premium over Fed Funds served its purpose in keeping excess reserves constant and in capping the Fed Funds rate from 2011 to 2017. However, as shown below, its effectiveness started eroding with the advent of QT in October of 2017

We believe the liquidity drain associated with QT created a shortage of dollars among foreign banks. Given this liquidity shortfall, foreign banks are likely being forced to pay higher interest rates for overnight funding. The Fed Funds rate is now higher than the IOER rate. That was not supposed to happen. Domestic banks either do not have the liquidity to lend or are being precautionary. Regardless of the reasons, a dollar shortage can become a dollar crisis if not addressed.

It is quite possible this situation will cause the Fed to stop QT before the scheduled September 30th end date. More importantly, it also raises the specter that QE, which injects liquidity into the banking system, is not as far off as we think. Watch the IOER/Fed Funds rate differential and the dollar for clues of further liquidity problems.

Warning 4 – Earnings

Lastly, as I discussed in this past weekend’s missive, earnings are not currently as “stellar” as the media makes them out to be. To wit:

“One of the reasons given for the push to new highs, and something we had previously said was highly probable, were the “better than expected” earnings reports coming in.

“Percentage of Companies Beating EPS Estimates (78%) is Above 5-Year Average

Overall, 15% of the companies in the S&P 500 have reported earnings to date for the first quarter. Of these companies, 78% have reported actual EPS above the mean EPS estimate, 5% have reported actual EPS equal to the mean EPS estimate, and 17% have reported actual EPS below the mean EPS estimate. The percentage of companies reporting EPS above the mean EPS estimate is above the 1-year (76%) average and above the 5-year (72%) average.”

Wow…that’s impressive and certainly would seem to be the reason behind surging asset prices.

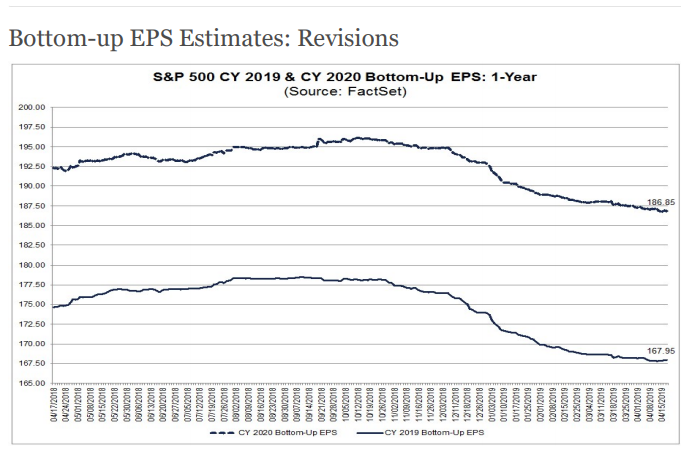

The problem is that “beat rate” was simply due to the consistent “lowering of the bar” as shown in the chart below:”

“As shown, beginning in mid-October last year, estimates for both 2019 and 2020 crashed.

This is why I call it ‘Millennial Soccer.’

Earnings season is now a “game” where scores aren’t kept, the media cheers, and everyone gets a “participation trophy” just for showing up.”

Importantly, the issue of buybacks continues to obscure the issue.

Not surprisingly, stock buybacks create an illusion of profitability.

Once that impact is removed the “soft underbelly” of actual earnings is fully exposed. The risk investors are taking is ultimately paying far too much for every dollar’s worth of earnings given that much of it is manufactured. While it may not matter now, it ultimately will matter.

If They Don’t “Buy & Hold” – Why Should You?

Here is the market for you year to date (via David Rosenberg):

Alphabet +23%

Microsoft +28%

Apple +30%

Amazon +30%

Facebook +46%

(Disclosure: We are long Apple and Microsoft in our equity portfolio.)

These “warning signs” are just that. None them suggest the markets, or the economy, are immediately plunging into the next recession-driven market reversion.

But as David noted:

“The equity market stopped being a leading indicator, or an economic barometer, a long time ago. Central banks looked after that. This entire cycle saw the weakest economic growth of all time couple the mother of all bull markets.”

There will be payback for that misalignment of funds.

Past experience suggests that future returns will be far less than historical averages suggest. Furthermore, there is a dramatic difference between investing for 30-years, and whatever time you personally have left to your financial goals.

While much of the mainstream media suggests that you “invest for the long-term” and “buy and hold” regardless of what the market brings, that is not what professional investors are doing.

The point here is simple. No professional, or successful investor, every bought and held for the long-term without regard, or respect, for the risks that are undertaken. If the professionals are looking at “risk,” and planning on how to protect their capital from losses when things go wrong, then why aren’t you?

via ZeroHedge News http://bit.ly/2GSoxDY Tyler Durden

With the market recently digesting Microsoft’s stronger than expected earnings, pushing its market cap north of $1 trillion and making it the most valuable company in the world for however long, while patiently awaiting today’s Apple earnings after the close, yesterday’s report by the third largest company, Google parent Alphabet, left a decidedly bitter aftertaste in investors’ mouths after it missed across the board while reporting a sharp slowdown in ad revenue growth.

Making matters worse, analysts were left puzzled over the reasons behind Alphabet’sfirst-quarter revenue miss: as Bloomberg explains, a particular source of confusion was product changes in advertising that the Google-parent said led to a slowdown in revenue growth.

A lack of answers on the earnings call led to “frustration” for investors, Jefferies analysts wrote in a note. One concern is whether other online businesses are taking advertising share away from Google, given that paid clicks on Google ads rose at the slowest pace since 2016. Alphabet’s shares are down 7.8% in pre-market trading on Tuesday. The stock had climbed 24% this year and closed on Monday at an all-time high before tumbling.

Courtesy of Bloomberg, here’s what what analysts were saying this morning about Alphabet’s results:

JEFFERIES (Brent Thill); buy rating on Alphabet with a PT of $1,450

1Q results raise “more questions than answers”, with continued lack of transparency “troubling” to investors

While valuation is undemanding, Alphabet will need to rebound in 2Q to show 1Q was not a trend

Otherwise investors may be resigned to the view that Alphabet is a lower growth story, potentially losing share, though Jefferies doesn’t believe that is the case

MORGAN STANLEY (Brian Nowak); overweight recommendation, though lowers PT to $1,425 from $1,500

1Q Websites deceleration and uncertain forward trajectory highlight need for better transparency; this will likely remain key to long-term valuation

Unclear what changes Alphabet made in the quarter that drove the deceleration in growth, and this is something the Street must figure out

Remains positive on Alphabet’s ecosystem and valuation support

CITI (Mark May), buy rating, PT $1,325

Alphabet’s 1Q report was worse than expected, with revenue below consensus due to impact from FX headwinds

Operating income margin and adj. Ebitda margin were better than expected

Despite weak 1Q results, still believes Alphabet can post a 3-year forward CAGR of 18% and generate GAAP EPS of $50 in 2020

{kind=link}

{kind=link}

{kind=link}