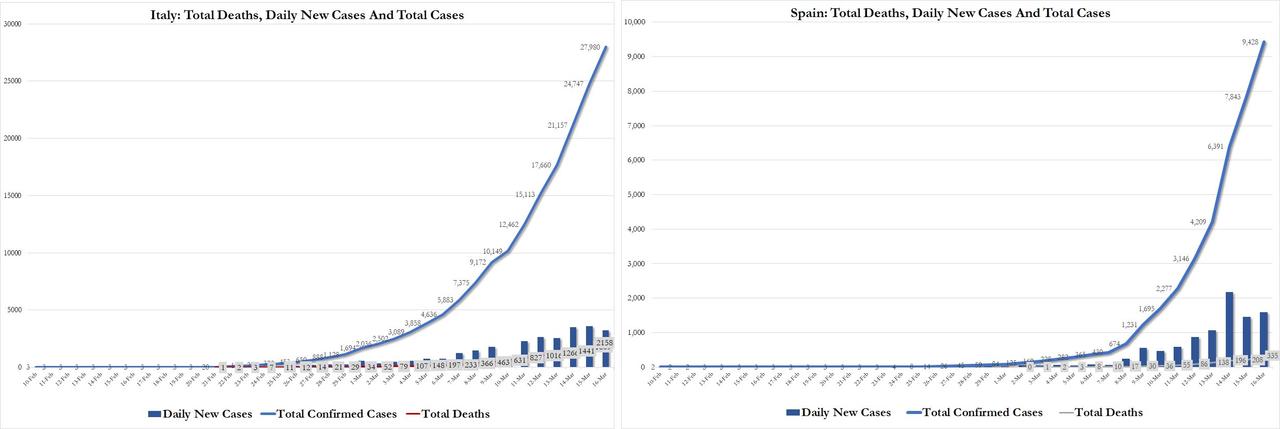

With Europe reeling under the weight of a record number of new coronavirus cases, especially in Italy and Spain, both countries announced today they they are banning short selling for the foreseeable future.

Spain’s stock market regulator CNVM on Monday banned transactions with Spanish shares involving the creation and increase in net short positions at least until April 17 following a steep dive in the market amid the coronaviarus epidemic. The prohibition covers short-selling even when such deals are covered by a securities loan, the CNVM said.

“The measure will enter into force tomorrow, the 17th of March, before the trading session begins and until the 17th of April, after the trading session is closed. It can be extended for additional periods not exceeding 3 months if the current circumstances persist,” it said in a statement.

At roughly the same time, Italy’s market regulator Consob said on Monday it was introducing a new 24-hour short-selling ban as the Milan bourse continued to slide hit by a coronavirus crisis in the country. The ban will apply to 20 stocks on Tuesday and follows a similar measure that was taken last Friday affecting 85 stocks.

Consob said it had also kicked off a procedure which will allow it to adopt further restrictive measures, introducing a more lasting ban on short-selling as envisaged by existing European regulation under exceptional circumstances.

The good news: unlike the Philippines, the two European nations plan on keeping their markets open. The bad news: with covid cases in both countries growing exponentially …

… it may be just a matter of time before both nations have no choice but to shutter their markets indefinitely.

With traders and investors living in a state of near constant panic (while working from home or their parents’ basement in the case of millennials who just got blown up on all their “growth” stocks), virtually nobody has any idea what to do in a market that is either cratering or soaring with no middle ground. And so, to answer pent up question about “how to invest when the world stops”, BofA has published a report which seeks to answer some of the top questions it has received about its market outlook, such as:

1. How have the coronavirus & oil shocks changed our outlook?

We’re very cautious about growth & earnings.

2. Is this like 2008, and what are the biggest risks?

No. The risks are worsening liquidity, credit contagion, layoffs and recession.

3. What can policymakers do to help?

Only a large, coordinated fiscal stimulus package matters now.

4. Why stay invested?

Not staying invested means missing most of the long-term market upside.

5. When will it be time to buy?

Watch our trading rules and watch for signs of a policy panic.

6. What is our asset allocation?

We are bullish on equities, credit, and gold and neutral on government bonds.

7. Where should we invest in equities?

Buy quality companies in defensive sectors like staples and health care.

8. Where should we invest in fixed income?

Rotate out of Treasuries into munis, corporates & mortgage-backed securities.

BofA, whose CIO recently declared that he is operating under the assumption that “we are in a global recession”, then takes a more detailed look at some of these questions, starting with:

1. How have the coronavirus and oil shocks changed our outlook?

BofA states that it is “very cautious about short-term growth & earnings. Markets are trading like a recession is already assured. Our economists Ethan Harris and Michelle Meyer have reduced their 2020 GDP growth forecasts from 3.1% to 2.2% globally and to 1.2% in the US”, something which the Fed’s emergency rate cut to 0% effectively confirmed.

In fixed income, the bank expects 10-year Treasury yields to be volatile before rising to 1.25% by year-end, and while 1.25% may be the right number, the real question is whether it will have a minus sign ahead of it. BofA is bullish on munis, on investment grade bonds and on mortgage-backed securities, all of which have gotten mauled in recent weeks. In equities, BofA’s strategist Savita Subramanian has reduced the S&P 500 year-end price target to 3100 and 2020 EPS from $177 to $169. She will reduce her targets far, far lower before it’s all over.

Why these changes? As BofA explains, “the manageable supply-side disturbance in China became a demand-side shock as the virus spread into Europe & North America. Investor fears have been compounded by the OPEC oil shock and the glacial response from fiscal authorities.”

* * *

2. Is this like 2008, and what are the biggest risks?

Noting that “every recession is different” BofA differentiates the current market crash from the financial crisis noting that in 2008, the big excesses were in household and financial balance sheets; today, household debt is low and the financial system is very well-capitalized. In 2020 the risk is from corporate profitability and the real economy, not systemic solvency (with about $20 trillion in global liquidity injected by central banks, one can only hope no systemic solvency is lurking).

At the same time, “every recession is the same”, and whatever the causes, once confidence falls and markets drop, all that matters is the policy response. The US economy was on relatively stable footing to start the year (low unemployment, rising wages, strong housing), but is now in a recessionary environment now, with concerns about three areas:

Liquidity: in the past 12 months, the key market supports have been net inflows from US households ($160bn) and corporates ($715bn). If investor selling continues just as corporates enter the buyback “blackout period” (late March & much of April), BofA expects even more market dislocations. Indeed, hedge fund liquidity has already vanished, as seen in equity futures and Treasury markets.

Corporate debt: the credit market has shuttered and companies are highly levered, with debt a record 92% of GDP, the share of developed-market “zombie” firms at a post-crisis high of 12%, and US bankruptcies on pace to exceed the 2008 total. The OPEC/Russia oil price war will pressure the energy sector and investors have begun distancing themselves from credit funds ($66bn outflows in recent weeks).

Jobs: BofA’s Consumer Confidence Indicator is tumbling, showing that the pandemic is already affecting consumer behavior. If the virus recession persists without offsetting stimulus, companies may begin laying off workers. In coming weeks watch for initial jobless claims >240k.

* * *

3. What can policy makers do to help?

Fed rate cuts, liquidity measures (QE5), and even lending to non-financial firms can prevent markets from seizing up, although as we saw over the past 24 hours, can no longer prop up stocks, something central banks have been doing for the past decade. At the of the day, “only Congress and the President can help stop the virus or provide support to the real economy.”

Bad news: the market breaks until “whatever it takes”. In 2008-2009, global fiscal stimulus was worth >3.5% of world GDP. Thus far, we have seen a paltry 0.2%, with nothing from the US.

Good news: the US government has a massive amount of fiscal firepower, largely thanks to the dollar’s status as reserve currency. Furthermore, at negative real interest rates across the curve, governments are effectively getting paid to borrow, which is key when $1 of stimulus generates $2 to $2.4 of GDP such as when invested in infrastructure, health care and R&D (Chart 2).

4. Why stay invested?

Here BofA pulls a CNBC, and “explains” that not staying invested means missing most of the long-term market upside…it’s simply too difficult to time the market, and adds that “a strong impulse to hide out in cash is often a sign that a buying moment is near.” On the other hand, few have the stomach, or balance sheet, to survive a 30%, 40% or greater drawdown. And while in theory it is great for everyone to stay invested, in practice it is impossible as one sees years of market gains disappear in a matter of hours.

In any case, here is how BofA urges its clients to never sell:

We know that the best days often follow the worst and this has been the sharpest drop into a bear market in history (Chart 3);

Since 1929, in the 24 months following a bear market, S&P 500 total returns have averaged 20%. Excluding the Great Depression, the average gain was 27% (Chart 4);

Since 1931, an investor who missed the 10 best days of each decade made 91% in equities. Staying invested meant earning 14,962%;

In the 2010s, missing the 10 best days meant gaining only 95% instead of 190%;

Over any 10-year period, the odds of ending with equity losses are just 4%;

* * *

5. When will it be time to buy?

BofA believes that we are near the point of capitulation (we disagree quite vocally), where positioning & technical signals turn bullish:

The BofA Bull and Bear Indicator is at 2.5 (<2 = "buy");

The Global Flow Trading Rule registered a buy signal after big outflows of >1% of global equity assets;

Global Risk-Love sentiment fell to the 5th percentile; the last 5 out of 5 signals saw +20% returns over the next year;

Stephen Suttmeier flags oversold levels in volatility, put/call ratios, and distribution;

SPX broke its 200-week average…2500 & 2350 support levels are key (Chart 5)

Here the bank hedges by noting that most sentiment indicators are designed for a “rational” market environment where mean-reversion dominates. In a momentum-driven, irrational market, conditions tend to get even more extreme than history would imply. Meanwhile, to turn short-term bullish with conviction, the bank would look for a big, coordinated fiscal response from US policymakers.

* * *

6. What is BofA’s asset allocation?

Here BofA surprised us by noting that “the consensus 60/40 allocation model may be enjoying its last hurrah”, and instead BofA is now pitching a 25/25/25/25 model, in which it is bullish on equities & corporate bonds, neutral on Treasuries, bullish on gold, and bearish on oil.

Given year-to-date returns (equities -23%, HY -9%, Treasuries +7%), once markets find their footing a violent rotation is likely out of safe havens. With every passing day, equity & corporate bond valuations are getting more attractive, although at this rate they will likely get even more attractive; At the same time, Treasuries are the most expensive in history, and

“buying them here is like buying all your stocks at 52-week highs.” Yes sure, we have heard that argument every year last decade, and yet bonds continue to outperform stocks.

In any case, 60/40 may lose either way, as “A big policy response can cause yields to painfully overshoot, while bonds have been no hedge at all since the March 9th lows: 10-year yields jumped 48bps, and Treasury volatility is the highest since 2008.”

* * *

7. Where should one invest in equities?

Once markets stabilize – when that happens is anyone’s guess – BofA says to buy quality stocks, especially in defensive sectors like health care, staples, and utilities. Regionally, BofA keeps a US bias and would add to EM ex-China in a rebound, but need evidence of a structural shift in policy to buy Europe & Japan. Some traditionally cyclical industries in the US may prove more resilient here, too:

Cybersecurity has little supply chain exposure with less discretionary revenue;

National defense is not exposed to the economic cycle & outperformed in the last 5 recessions by 13ppt on average;

Homebuilders benefit from record-low mortgage rates, minimal supply chain risk, and demographic tailwinds; and

Banks have already priced-in a recession, pay well-guarded dividends of 5%, and may earn higher multiples once the downturn is over.

For global quality, look for the latest update soon to our Global Best of Breed screen. Many of these sectors & themes are accessible via funds & ETFs, which Eli Lanik ranks.

* * *

8. How about bonds: where should one invest in fixed income?

BofA says that it would rotate out of Treasury bonds and into municipals, investment grade corporates, and mortgage-backed securities (hardly a new take for the bank that has hated TSYs for years, losing greatly in the process). That said, treasuries today yield just 16bp per unit of risk vs. 60bp historically, and every other fixed income sector offers a better risk/reward profile once markets stabilize.

Meanwhile, the ratios of muni bond yields to Treasuries spiked so sharply that BofA’s team suggests “buying the whole curve”.

Finally, mortgage-backed securities are the cheapest since 2008, and attractive on the prospect of the Fed re-entering the market. Finally, our analysts are bullish on investment grade bonds at spreads above 200bps.

Liquidity Panic Reaches Staples: Kraft Heinz To Fully Draw Down $4 Billion Revolver

Last week investors were shocked when a barrage of major US corporations – including Boeing, Hilton, Wynn and a handful of PE portfolio companies – announced their decision to fully draw down on their existing credit lines. That said, for all the ominous banking crisis undertones – many still remember that one of the early symptoms of the global financial crisis was countless companies whose revolvers were pulled by a panicking banking sector – there was a common theme linking all these companies: they were all in sectors (airlines, casinos, lodging, energy) that were directly impacted by either the coronavirus pandemic or the recent oil price war.

Today, that changed when food giant Kraft Heinz – which should be benefiting generously from the recent food hoarding panic – was set to also draw down on its credit facility of as much as $4 billion, even though it faced none of the same coronavirus/oil headwinds as so many other companies that jumped the gun to boost their liquidity while they still could.

“We maintain our $4.0 billion senior credit facility, and subject to certain conditions, we may increase the amount of revolving commitments and/or add additional tranches of term loans in a combined aggregate amount of up to$1.0 billion,” the company said.

Speaking to Bloomberg, which first reported the drawdown of the Buffett-owned company, a Kraft Heinz spokesman said that “the demand for our brands, our cash flow and our balance sheet remain strong,” which is a rather bizarre explanation why it would need billions more in liquidity. “As a matter of practice, we typically maintain a conservative liquidity posture, which is even that much more important as we focus on making sure all our products remain available to the public during these challenging times.”

One possible reason for Heinz’s liquidity problems is that while other sectors have been crippled by the ongoing dual viral-oil shock, the ketchup maker has seen it share of corporate woes in recent years, most recently its downgrade to junk by S&P Global Ratings and Fitch Ratings, when it also warned that the downgrades may limit its access to financing sources such as the commercial paper market, requiring it to use alternative funding sources such as its senior credit facility.

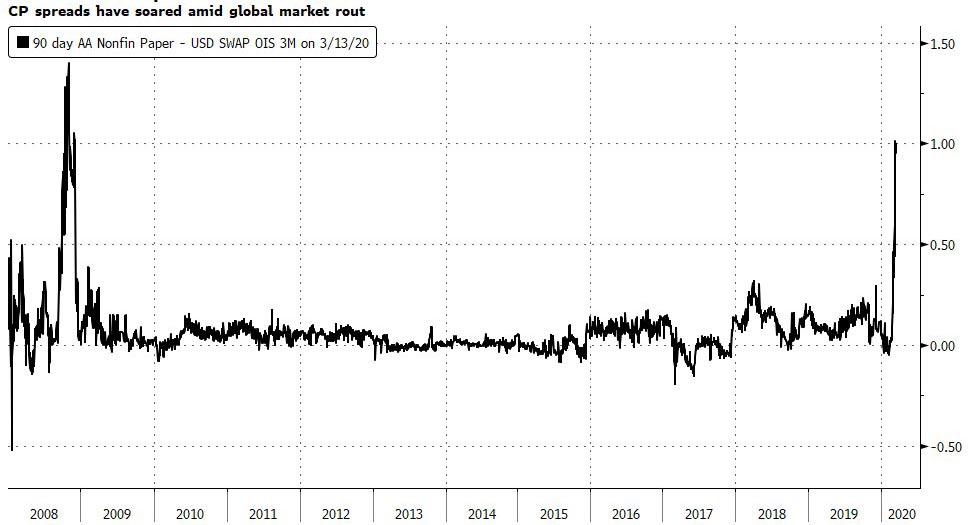

And, as we discussed yesterday, the commercial paper market is starting to freeze up (something the Fed failed to address in its emergency Sunday announcement) which is forcing companies like Heinz to seek alternative, last ditch sources of liquidity.

Indeed, as Bloomberg noted today, issuance of commercial paper dropped to 3,125 transactions on March 13, according to figures released Monday; that’s down 13% from the average daily rate in the week ending March 6 and 18% since February. At the same time, a closely watched CP spread – that between three-month AA rated financial and non-financial commercial paper rates versus overnight index swaps – shows some of the most stress since the financial crisis.

“I am not surprised, liquidity is the lifeblood of these types of programs,” said Scott Kimball, a portfolio manager at BMO Global Asset Management. “When markets lock up like this, interest rates surge to levels that are unsustainable for business.”

Yet what is odd, is that Kraft Heinz said in a regulatory filing last month that it had no commercial paper outstanding at the end of 2019 and that the maximum amount it held during last year was $200 million.

So maybe the company’s rush to its banking syndicate is simply that: a panicked attempt to grab as much cash as it can before it is locked out as banks go into cash conservation mode, something their halt of stock buybacks made quite clear is coming.

Created in a catastrophic merger five years ago orchestrated by Warren Buffett’s Berkshire Hathaway and private equity firm 3G Capital, Kraft Heinz is in the midst of a turnaround as its brands fall out of favor with consumers. Its shares have crashed 16% in the past month, less than the decline of the S&P 500 Index, amid ongoing consumer demand for food and beverages, although today’s revolver news will hardly excite investors.

“So, first of all, let me assert my firm belief that the only thing we have to fear is…fear itself — nameless, unreasoning, unjustified terror which paralyzes needed efforts to convert retreat into advance. In every dark hour of our national life a leadership of frankness and of vigor has met with that understanding and support of the people themselves which is essential to victory. And I am convinced that you will again give that support to leadership in these critical days.”

– Franklin D. Roosevelt – March 4, 1933

Franklin D. Roosevelt spoke these words during his first inauguration at the depths of the Great Depression in 1933. The narrative taught in government schools is how FDR’s words invigorated the nation and inspired the people to show courage in the face of adversity. His terminology was that of a general leading his troops into battle.

What is not taught in government schools or proclaimed by the propaganda spewing fake news media were the dictatorial type actions taken by FDR over the next month after his “inspirational” speech. He was the first Democrat president to not let a crisis go to waste. The day after his inauguration, Roosevelt assembled a special session of Congress to declare a four-day bank holiday, and on March 9 signed the Emergency Banking Act.

What the American people should have feared was the government taking control of every aspect of their lives and threatening them with imprisonment if their dictums were not followed. On March 6, taking advantage of a wartime statute that had not been repealed, he issued Presidential Proclamation 2039 that forbade the hoarding ‘of gold or silver coin or bullion or currency’, under penalty of $10,000 and/or up to five to ten years imprisonment.”

One month later, Roosevelt implemented Executive Order 6102 “forbidding the hoarding of gold coin, gold bullion, and gold certificates within the continental United States”. FDR, like every corrupt politician, overstepped his authority by invoking the Trading with the Enemy Act of 1917, to seize all the gold in the country. The fake reason for the order was that hard times had caused “hoarding” of gold, stalling economic growth and making the depression worse.

As usual, the Federal Reserve created the Great Depression through their recklessly easy monetary policy during the 1920s, creating a stock market bubble and its inevitable crash. The false rationale behind the order was to remove the restriction on the Federal Reserve which prevented it from increasing the money supply during the depression; the Federal Reserve Act (1913) required 40% gold backing of Federal Reserve Notes issued.

Excessive money printing by the Fed to benefit their Wall Street owners and the monied interests is a consistent theme since the Fed’s shameful conception in 1913. They catalyzed the Great Depression Fourth Turning in 1929 and seventy-nine years later created the current Greater Depression Fourth Turing in 2008. Americans should fear what they have done to our country.

Roosevelt used the fears of the American people to elevate the Federal government as the savior and ultimate allocator of dispensations to the masses. This is how politicians used fear in the 1930s to implement more control over our lives. They used the 2008 Wall Street created financial collapse to further confiscate the nation’s resources, while screwing over the little guy.

Now, we are in the midst of another manufactured crisis where government control of every aspect of our lives will be implemented through mandates, quarantines, and ultimately military force. There is nothing to fear but listening to politicians, government apparatchiks, and the hysteria inducing corporate media doing the bidding of their oligarch masters.

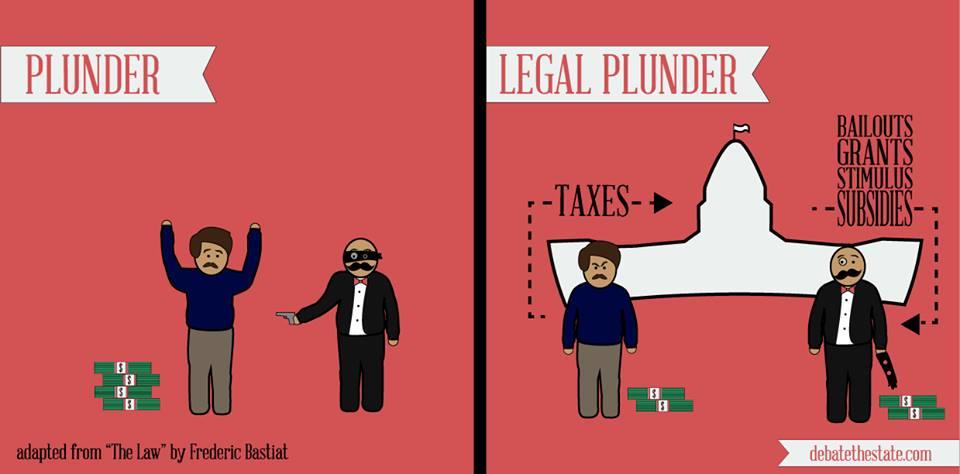

“The politician attempts to remedy the evil by increasing the very thing that caused the evil in the first place: legal plunder.”

– Frederic Bastiat

I’ve followed this entire coronavirus outbreak with a skeptical eye since it first appeared on the radar in January. Knowing that I’m lied to by virtually everyone has made it difficult to comprehend the truth about this ongoing crisis. We know China lied to the entire world about the outbreak in Wuhan. It wasn’t until social media revealed the true extent of the virus and quarantine of a city larger than NYC, that the world began to understand this was serious.

The fact that a military bio-lab in Wuhan somehow contributed to the initial outbreak has been downplayed by the propaganda media. The arrest of a Harvard chemistry professor and two Chinese nationals for trying to smuggle biological vials to China in January is also highly suspicious. A Canadian government scientist at the National Microbiology Lab in Winnipeg made at least five trips to China in 2017-18, including one to train scientists and technicians at China’s newly certified Level 4 lab, which does research with deadly pathogens.

All indications point to this virus being man made, for purposes of biological war. Whether it was released into the world by accident or on purpose is unknown. What we do know is it is now spreading rapidly in every country around the globe. I don’t doubt it is highly contagious and will kill a large number of health compromised people. The growth rate goes exponential, based on what has happened in China, Italy and now countries across the globe. China reports that it has peaked and is in decline. Of course, they lie about everything, so these reports are suspect. If true, it can be attributed to their military lock down of cities and martial law ruthlessly implemented against its people. You can be sure our beloved leaders have noted the cold-blooded use of the military to implement their mandatory confinement. Obey or die.

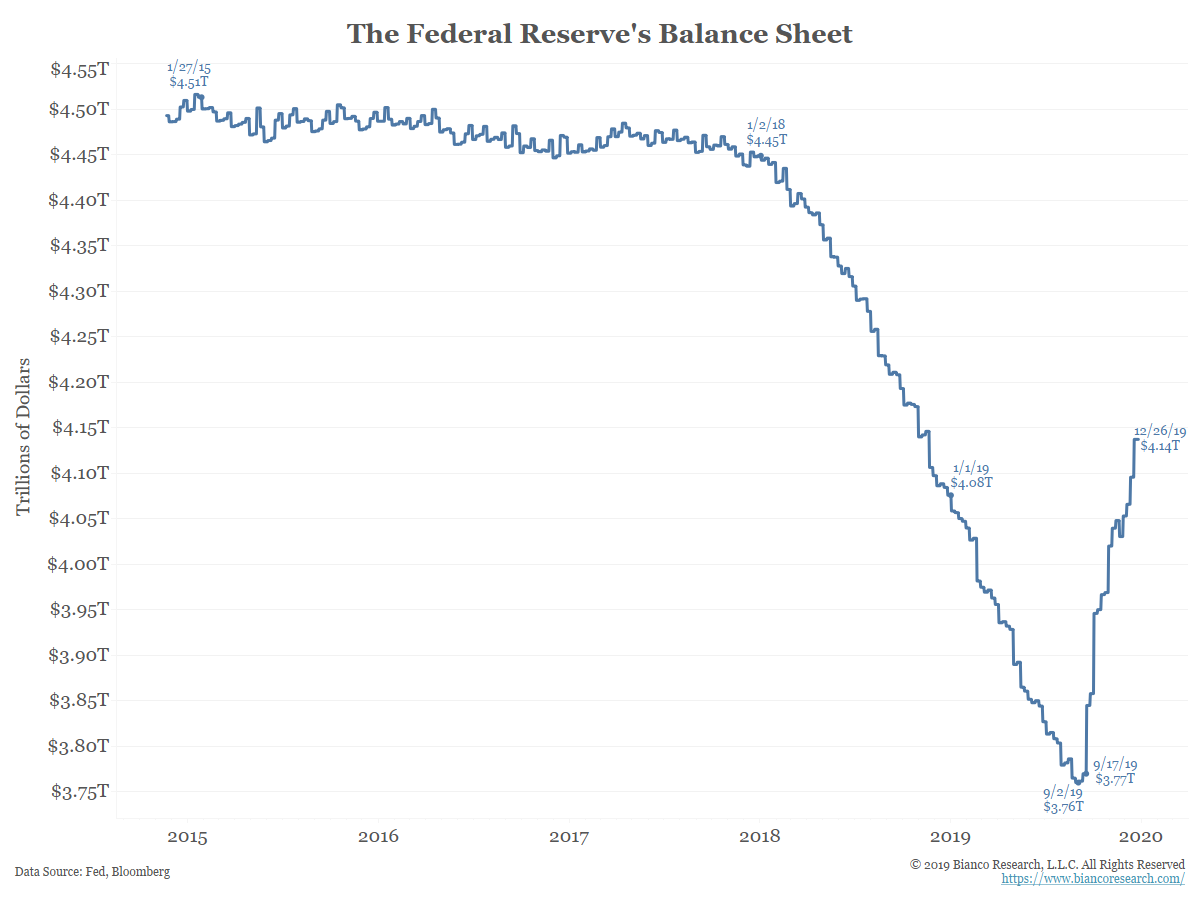

In the middle of 2019, something beneath the surface of our debt based financial system broke. Suddenly, the Fed began to cut interest rates. This was done when the economy was “the best ever” according to Trump. They cut three times during the second half of 2019. The repo market went berserk in September. The Fed began “not QE” in January as the wheels began to fall off. The Wall Street lemmings cheered and bought everything in sight, propelling the market to the most overvalued in history. The Wall Street titans encouraged the public to buy, buy, buy. The Fed balance sheet made a V like “recovery”, skyrocketing by $700 billion in a matter of months. The daily bailing out of Wall Street banks has continued at an increasing level.

There was no fear exhibited by the likes of Dalio, Dimon or Shwarzman. The crash was inevitable. It just needed a catalyst. And that catalyst was the coronavirus. The more than 20% drop in less than two weeks was fastest in history. The Fed has attempted to capitalize on this crisis to further enrich their Wall Street benefactors. Trump was so exhilarated by the 7% bounce on Friday, he signed a stock chart for his sycophant ass kisser Lou Dobbs.

Trump continued to badger his pussified Fed Chairman Powell to slash rates more. Powell cowered under the glare of Trump and his Wall Street puppeteers and went all in on Sunday, slashing rates to zero and officially launching QE5. He has zero bullets left in the chamber. If he can’t reignite the stock market bubble with this recklessly outrageous conduct, then it’s game over and the Greater Depression will commence.

In the past week, politicians, bureaucrats and bankers of all stripes have used this coronavirus crisis, to increase their control and power over our daily lives. They passed another “stimulus package” that was 300 pages and no one in Congress read before voting it through. It’s filled with pork and corporate goodies. Manuchin, another Goldman vampire squid, is doing all he can to keep the net worth of his banker and corporate buddies headed north during this crisis.

Bailouts for airlines, cruise lines, frackers, hotels, and any other favored industry is in the offing. The fact these fake capitalists borrowed at near zero rates and bought back hundreds of billions of their stock in order to boost their stock price and reward themselves with hundreds of millions in bonuses, is water under the bridge in our crony capitalist paradise. It is truly despicable and traitorous to bailout these scumbags after their ten year orgy on the nation’s wealth.

Trump and his minions are following the exact playbook used in 2008/2009. Socialism for the corporate titans when they blow up the financial system, while average Americans lose their jobs and have their 401ks wiped out for the 3rd time in the last two decades. Every action being taken by politicians today is to save Wall Street and the mega-corporations who buy and sell them.

Main Street will be fucked over once again. ZIRP throws senior citizens under the bus. The spreading of irrational fear about this virus by the propaganda media is designed to convince the ignorant masses to beg their government keepers to save their lives. What critical thinking Americans should conclude is how corrupt, incompetent and evil their elected and unelected leaders have proven to be.

This Fourth Turning is really heating up. We have entered the phase where body counts will accelerate. No one knows whether the coronavirus will result in thousands of deaths or millions of deaths. Anyone telling you they know what is going to happen is a liar. If you think your Constitutional rights have been trashed through the mass surveillance being conducted by our government, you haven’t seen anything yet.

Wait until they declare this coronavirus out of control requiring a countrywide quarantine enforced by the U.S. military. When military vehicles are patrolling your streets with the threat of arrest or death if you leave your home, you’ll know the Constitution has been tossed into the trash bin. After decades of government school indoctrination and mass media propaganda, the sheep will passively be led to slaughter.

Our Himalayan mountain of debt is about to come tumbling down. The Federal Reserve has proven to be nothing but a whore for the Wall Street pimps. They have destroyed any semblance of credibility and independence they once had. The economic impact of this global pandemic will drive the entire world into recession. The likely outcome is a global depression as fear replaces greed and debts can’t be repaid. Fiscal stimulus when the national debt is already $23 trillion is like injecting adrenaline into a cancer patient. Small businesses are going to fail and unemployment is going to rise. This farce of a debt ponzi scheme is over.

Once economies across the world implode, with central bankers having failed epically, and citizens angry about how their political leaders have failed them, feckless politicians will do what they always do. They will create a foreign bogeyman enemy to redirect the ire of their citizens. Again, our leaders will exaggerate threats to induce fear into the masses. Will it be China or Russia or both? Some false flag will be utilized to launch another Fourth Turning war.

Millions will be sent to their deaths by foolish egomaniacal leaders. These crisis periods follow the same dynamic, only the specific events and triggers change. The existing social order will be swept away. Fourth Turnings always separate the wheat from the chaff. 2020 is destined to go down in history as the year where decades of lies, corruption, thievery and corporate fascism came crashing down. Who picks up the pieces after the crash will determine our future.

“With the civic ethos now capable of producing civic deeds, a new dynamic of threat and response takes hold.

Instead of downplaying problems, leaders start exaggerating them.

Instead of deferring solutions, they accelerate them.

Instead of tolerating diversity, they demand consensus.

Instead of coaxing people with promises of minimal sacrifice, they summon them with warnings of maximal sacrifice.

A new resolve about urgent public goals crowds out qualms about questionable public means.” – Strauss & Howe – The Fourth Turning

VIX Closes At Record High As S&P Breaks Critical Trendline Support

Just to provide a little focused context on US markets, three major things occurred today:

1) this was the 3rd biggest down day for stocks… ever – Great Depression, 1987 and… now

Source: Bianco Research

2) VIX closed at a record high – higher than the highest close during the Great Financial Crisis…

3) The S&P 500 broke below (and closed below) the 11-year up-trendline from the March 2009 ‘generational low’ for the first time…

And all that amid the most massive monetary intervention ever seen. As we detailed earlier, while this deserves an extended discussion, we will merely point out that each day there a distinct part of the credit and/or funding market is breaking:

One day it is ETF NAV discounts blowing out

The next day the treasury Treasury/Swap basis surges and basis funds suffer a historic VaR crash amid forced liquidations

Day three sees the FRA/OIS explode higher as a massive dollar funding margin call strikes

Then, day four sees the same repo crisis that was supposed to be fixed back in September return with a vengeance, as banks freak out about counterparty risk.

What the Fed needs is the monetary equivalent of Dr. House: someone who can diagnose what is actually wrong with the monetary plumbing, instead of using the same old shotgun approach of shoveling trillions in blunt liquidity into the market, which clearly is not working anymore.

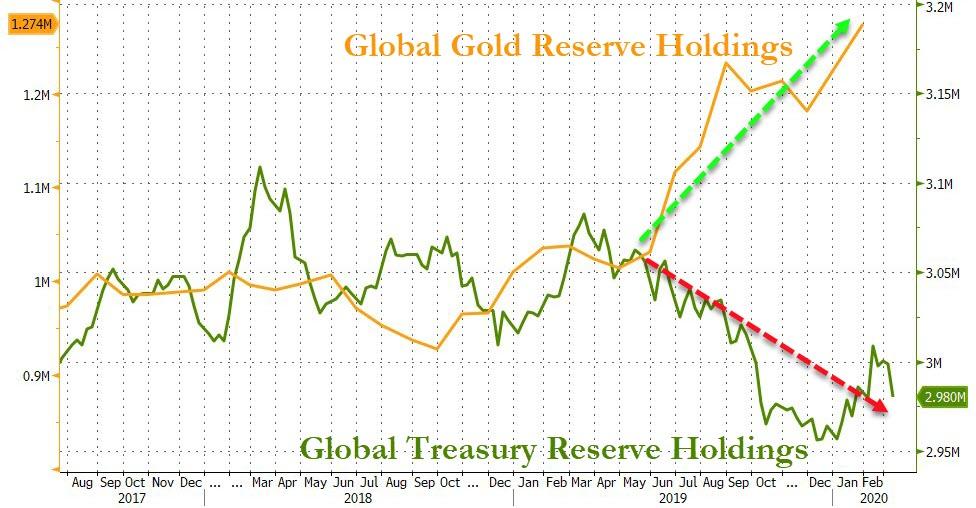

Foreign Central Banks Dump Treasuries For 17th Straight Month, Continue To Hoard More Gold

For the first time since June, China added to its US Treasury holdings in January (the latest month from TIC data).

The total for China — the second-largest holder of U.S. government debt after Japan – rose $8.7 billion in January to $1.08 trillion.

Source: Bloomberg

The coming months’ data will help show if the virus’s blow to China’s economy is starting to pressure central bank officials to sell Treasuries to support the yuan, a step they’ve avoided over the past several years, preferring instead to manage the currency via the daily fixing, says Mark Sobel, former IMF and Treasury official and chair of the OMFIF.

If COVID-19 hit the yuan hard, he said, “China might intervene to cushion any decline.”

Japan remains the largest foreign holder with $1.21 trillion, as the value of its holdings rose $56.8 billion at the start of the year, the data showed.

Source: Bloomberg

Overall, Foreigners were net buyers of US assets excluding corporate debt

Foreign net buying of Treasuries at $25.6b

Foreign net buying of equities at $2b

Foreign net selling of corporate debt at $31.8b

Foreign net buying of agency debt at $32.3b

But foreign central banks dumped US Treasuries for the 17th straight month…

Central bank demand came in at 650.3 tons in 2019. That was the second-highest level of annual purchases for 50 years, just slightly below the 2018 net purchases of 656.2 tons. According to the WGC, 2018 marked the highest level of annual net central bank gold purchases since the suspension of dollar convertibility into gold in 1971, and the second-highest annual total on record.

The World Gold Council bases its data on information submitted to the International Monetary Fund.

Turkey was the leading gold-buyer in January. The Turks added 16.2 tons of gold to their reserves.

Russia continued to stockpile the yellow metal, adding another 8.1 tons to their hoard. Russia’s quest for gold has paid off in a big way. The Russian Central Bank’s gold reserves topped $100 billion in September 2019 thanks to continued buying and surging prices.

The Russians have been buying gold for the last several years in an effort to diversify away from the US dollar. Russian gold reserves increased 274.3 tons in 2018, marking the fourth consecutive year of plus-200 ton growth. Meanwhile, the Russians sold off nearly all of its US Treasury holdings. According to Bank of America analysts, the amount of US dollars in Russian reserves fell from 46% to 22% in 2018.

Mongolia and Kazakhstan both added 1 ton of gold to their reserves in January. The only other buyer was Greece at 0.1 tons.

There were two significant net-sellers – Uzbekistan (2.2t) and Qatar (1.6t).

The People’s Bank of China did not report any gold purchases for the fourth straight month It’s not uncommon for China to go silent and then suddenly announce a large increase in reserves.

January’s net gold purchases represented a 57% decline year-on-year. World Gold Council analyst Krishan Gopaul said it was too early to determine what this could mean for 2020.

World Gold Council director of market intelligence Alistair Hewitt said there are two major factors driving central banks to buy gold – geopolitical instability and extraordinarily loose monetary policy.

Central banks are looking toward gold to balance some of that risk. We’ve also got negative rates and yields for a large number of sovereign bonds.”

“This recent trend shouldn’t be ignored. But nor should we also lose sight of the fact that central banks remain net purchasers, even if at a lower level than we have come to expect to in the last two years.”

The days where the dollar is the reserve currency are numbered and we’re going back to basics. You know, everything old is new again. Gold was money in the past and it will be money again in the future, and central banks that are smart enough to read that writing on the wall are increasing their gold reserves now.”

Amazon Hiring 100,000 Warehouse And Delivery Workers As Coronavirus-Driven Purchases Explode

Amazon will hire 100,000 employees in the US to cope with the surge of Americans turning to online deliveries amid the coronavirus outbreak, according to the Wall Street Journal.

Employees will also earn $2 more per hour through April, along with an additional £2 for UK workers and €2 an hour for workers in many EU countries. The current starting wage is $15 per hour in its fulfillment centers around the US.

“We are seeing a significant increase in demand, which means our labor needs are unprecedented for this time of year,” said semior VP of operations, Dave Clark, in a memo reviewed by the Journal.

With the coronavirus spreading throughout the U.S. and states implementing restrictions on large gatherings, more customers are turning to online shopping for everything from grocery delivery to paper towels, cleaning supplies and daily needs. Amazon, which also owns grocery store chain Whole Foods, was one of the companies President Trump mentioned during his update on the coronavirus on Sunday. Amazon accounts for 39% of all online orders in the U.S., according to eMarketer, and is shouldering a lot of those needs. –Wall Street Journal

Amazon also expanded its sick-leave policy last Wednesday to include part-time warehouse workers. They company has also set up a relief fund with an initial $25 million for drivers and other delivery partners affected by the outbreak.

According to the report, the 100,000 new jobs come at a time when retail is collapsing and retailers are considering widespread closure of physical stores. Nike, Apple and Lululemon have all announced temporary store closures, while people working in the entertainment, restaurant and hospitality industries are facing furloughs as cities and states restrict gatherings in public places.

As one veteran trader exclaimed in FULL CAPS over text: “it’s total f**king global carnage” as wherever you look today there is blood in the streets.

For example:

STOXX EUROPE 600 ENDS DOWN 4.9%, LOWEST CLOSE SINCE MID-2013

SOUTH AFRICA’S FTSE/JSE INDEX FALLS AS MUCH AS 12.2%, MOST EVER

MUNI BONDS EXTEND WORST ROUT SINCE 1987

COPPER SLUMPS AS MUCH AS 5.2% AMID WEAKENING RISK APPETITE

BRENT CRUDE OIL PLUNGES BELOW $30 FOR FIRST TIME SINCE 2016

SILVER PLUNGES TO 2011 LOWS

U.S. WHOLESALE GASOLINE PRICES PLUNGE 21%

HYG WORST DROP SINCE 2008

LQD WORST DROP SINCE 2008

Year-to-date, the long-bond is the best-performing asset with stocks the worst and gold just dipping into the red today…

Source: Bloomberg

Only Dow Industrials is still green from the start of 2019…

Source: Bloomberg

Since Trump’s election, Small Caps and Transports are now down 8% and 12% respectively…

Source: Bloomberg

And to comprehend what just happened, Small Caps and Trannies are down 35% from their highs and the rest of the majors down around 27%…

Source: Bloomberg

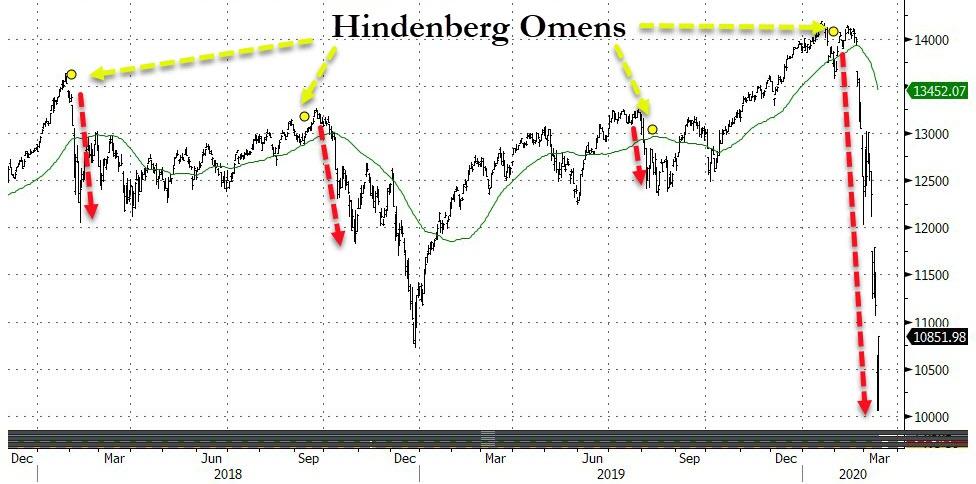

Seems like Hindenberg nailed it again…

Source: Bloomberg

Chinese stocks are starting to awaken from their margin-fueled stupor…

Source: Bloomberg

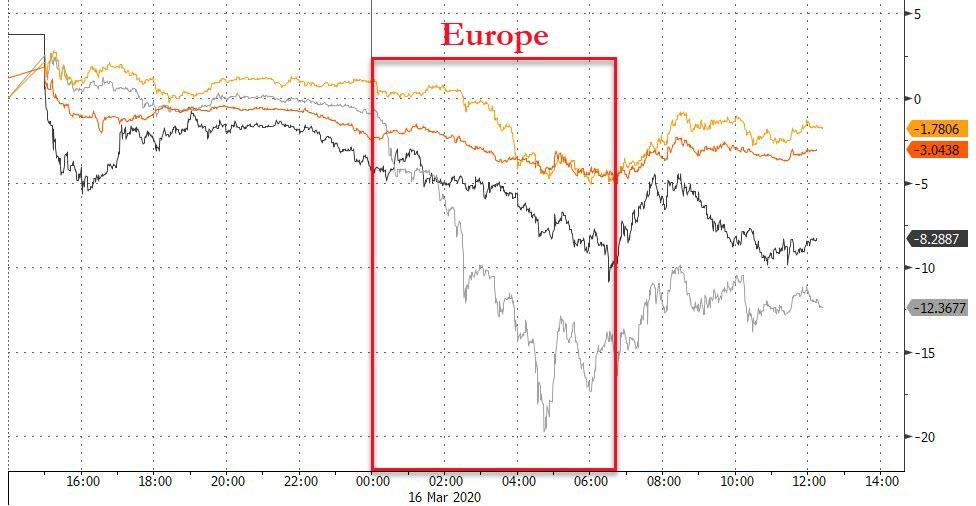

European stocks crashed to their lowest since Nov 2012…

Source: Bloomberg

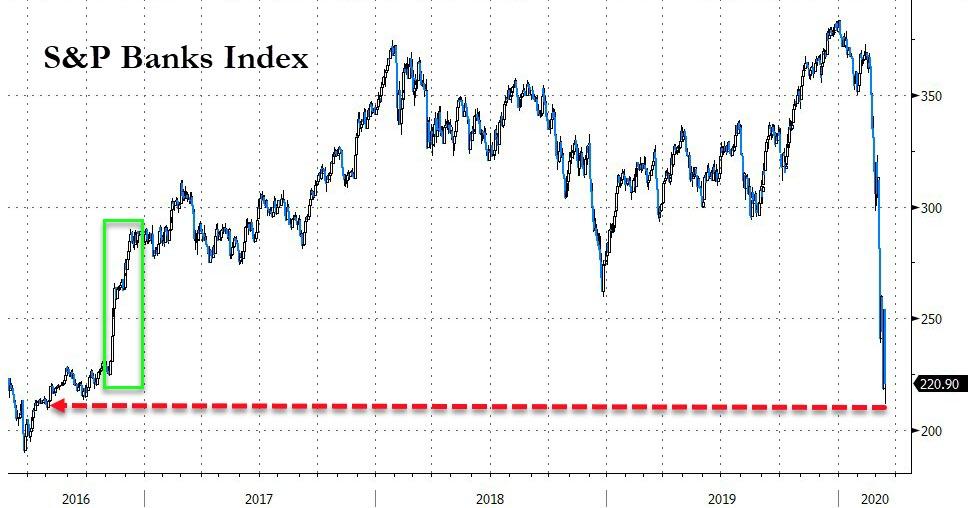

Elsewhere in Europe, banking stocks were a bloodbath, smashed to their lowest since 1987…

Source: Bloomberg

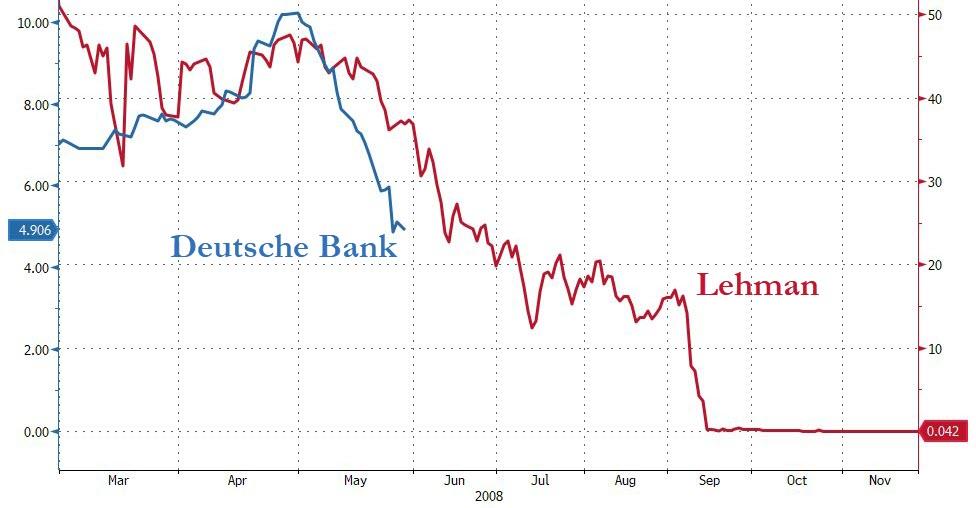

With Deutsche Bank reaching the vinegar strokes, below EUR5 for the first time ever…

Source: Bloomberg

US Futures were halted limit-down overnight, and when cash markets opened, they were halted (down over 7%) before rallying all the way back up to the halted levels before slumping back… Losses accelerated into the close as the White House press conference began…

US Equity ETFs showed the price action a little better (as they were not halted overnight)…

On the cash side, The Dow ended back below 21,000 (crashing 3,000 points today)…

…but Small Caps were the worst hit on the day…

The December 2018 lows are all that matters for now for the S&P 500…

Source: Bloomberg

And the S&P is at key support…

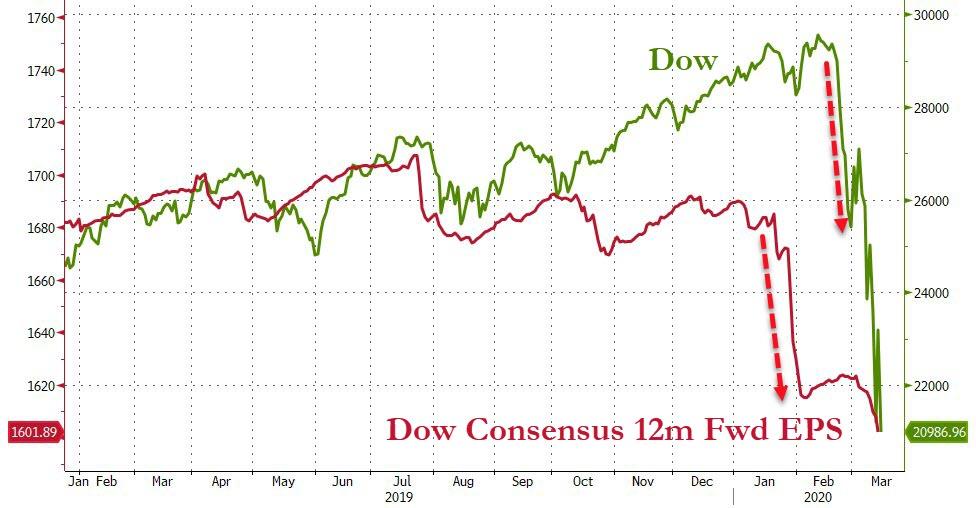

The Dow has caught down to its EPS contraction… but will multiples collapse even more?

Source: Bloomberg

Bank stocks were destroyed today after abandoning buyback plans, erasing all post-Trump-election gains…

Source: Bloomberg

And just when you thought virus-impacted sectors had priced it all in… they plunge another 10-12%…

Source: Bloomberg

It’s been total liquidation…

Source: Bloomberg

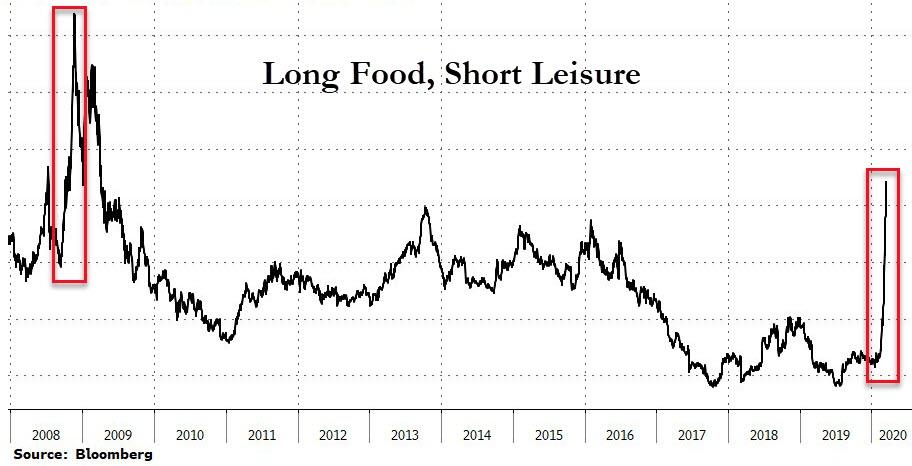

The virus trade continues to play extremely well… Long Food, Short Leisure…

Source: Bloomberg

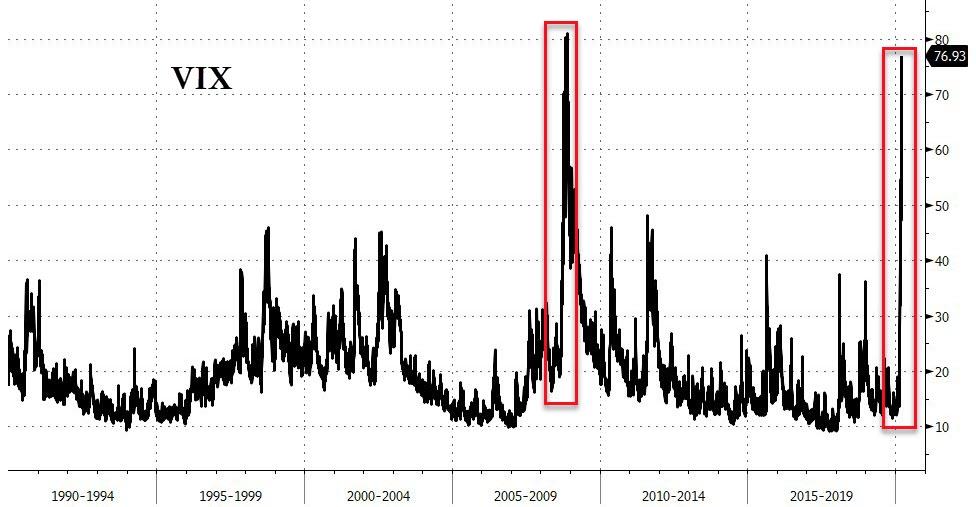

VIX spiked even higher today, within reach of its record highs…

Source: Bloomberg

And systemic event risk is soaring…

Source: Bloomberg

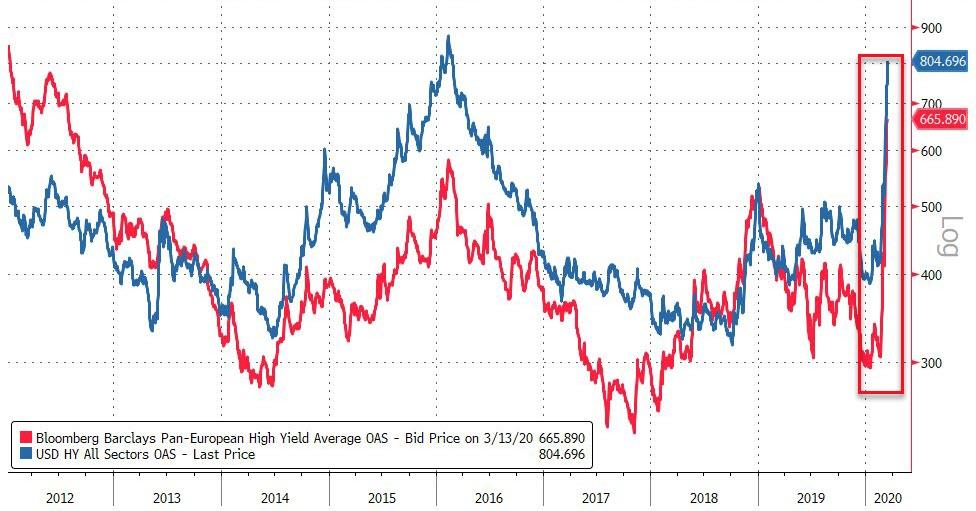

Credit markets suffered more carnage with IG spreads exploding higher…

Source: Bloomberg

As well as HY…

Source: Bloomberg

Treasury yields plunged today, crashing at the open before rising around the European open before being dumped after Europe closed…

Source: Bloomberg

The entire curve was lower but the short-end underperformed…flattening the yield curve.

Source: Bloomberg

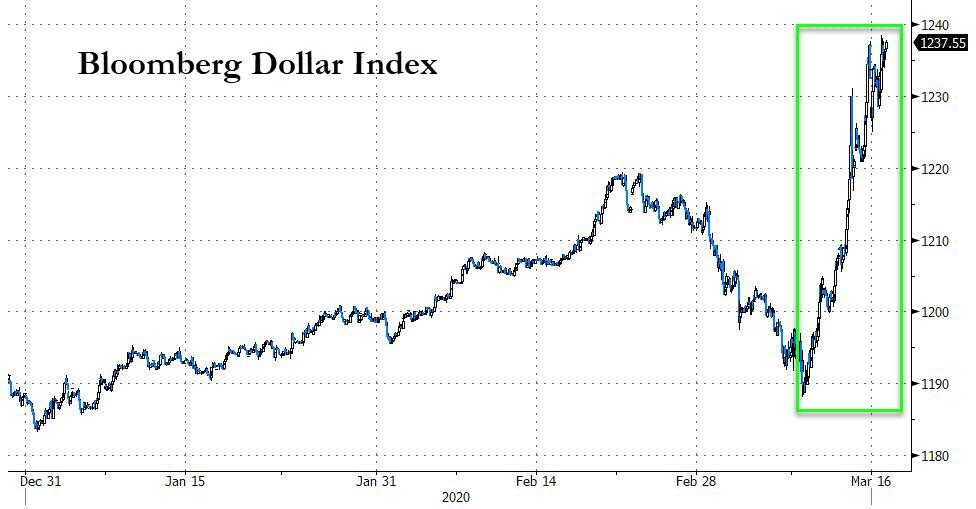

The Dollar surged for the 5th straight day, rallying 3.9% – the biggest 5-day jump since Lehman…

Source: Bloomberg

Cryptos went on a wild roller-coaster in the last 24 hours, crashing 10-2% before ripping back…

Source: Bloomberg

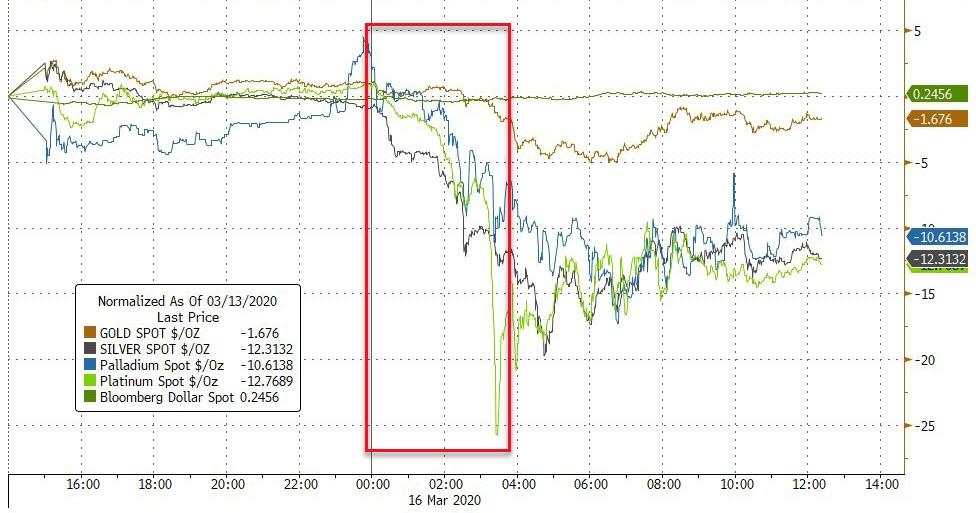

The dollar’s ongoing surge (amid liquidity shortages) prompted further liquidations across commodities with Silver slammed the most…

Source: Bloomberg

Precious metals were broadly pummelled today with gold majorly outperforming (NOTE – the precious metal puke started as Europe opened)…

Source: Bloomberg

Silver puke below $12 today…

Which sent the gold/silver ratio exploding to a record high…

Source: Bloomberg

And WTI busted back below $30…

And finally, despite massive monetary intervention overnight, the global shortage just went to ’11’…

Source: Bloomberg

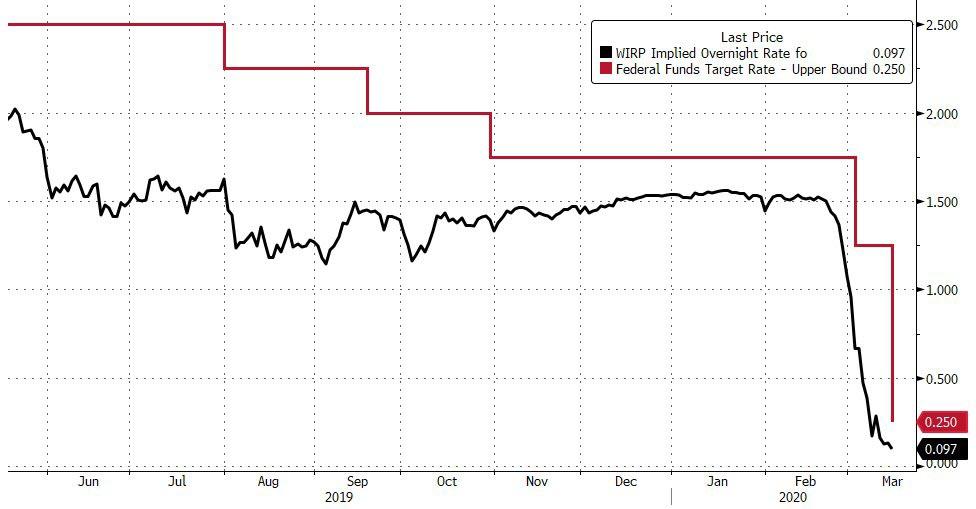

The market got its 100bps cut and is still demanding more…

Source: Bloomberg

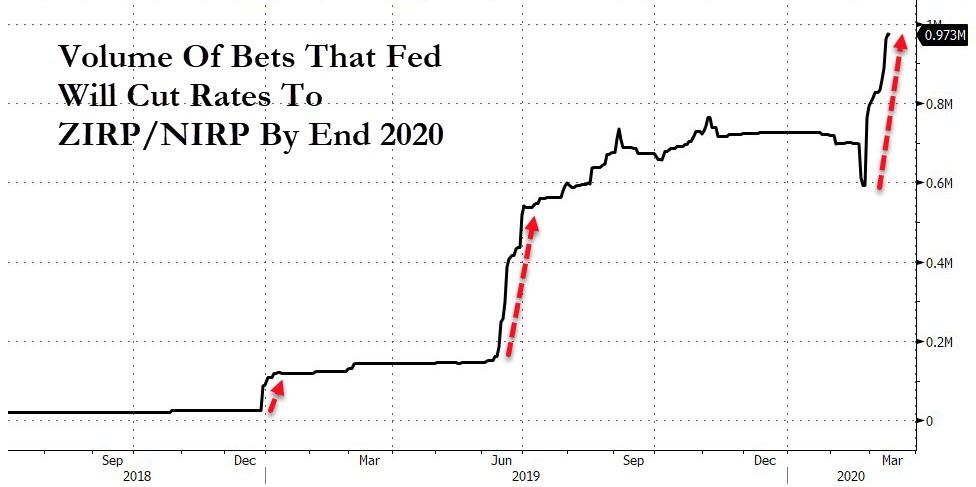

And the number of bets on The Fed going negative are soaring…

Elon Musk To His Workers: “You’re More Likely To Die In A Car Crash Than From Coronavirus”

Elon Musk is telling his workers that they have a higher risk of dying in a car crash than from coronavirus, in what has become the latest in a string of actions Musk appears to be taking to try and downplay the pandemic crisis that the globe now faces.

In a company-wide e-mail on Friday, Musk said that the evidence surrounding the virus “suggests that this is *not* within the top 100 health risks in the United States,” according to BuzzFeed. Musk said in the e-mail that employees who feel ill should stay home.

His e-mail continued: “Isn’t C19 growing so fast that it will soon become a top 100 health risk for people who are otherwise healthy and young to middle-aged? The trends do not support this conclusion. Among other things, the media is using the ‘presumed’ positive number of C19 cases, not the *confirmed* number.”

Musk also added to his pompous diatribe: “As a basis for comparison, the risk of death from C19 is *vastly* less than the risk of death from driving your car home. There are about 36 thousand automotive deaths per deaths [sic], as compared to 36 so far this year for C19.”

That is, of course, unless your “car” is a Tesla on Autopilot…

While other cities and corporations are taking precautions and locking down their employees, Musk’s SpaceX in Hawthorne, California, and Tesla’s offices and factories, remain open.

Amesh Adalja, a senior scholar at the Johns Hopkins University Center for Health Security told BuzzFeed: “It doesn’t make logical sense comparing those types of things. This virus is not a containable virus, and while most people do well with it, there is a proportion that don’t. People may end up dying from this, and we should be focused on trying to limit people’s exposure.”

“Once we saw what happened with the windows of the [Cybertruck], maybe we should be worried about those crashes,” Brandon Brown, an associate professor of epidemiology at the University of California, commented.

It was just days ago that we reported that America’s favorite sociopath CEO had Tweeted out that the coronavirus panic was “dumb”. Just hours after that, he again took to Twitter to double down on his statement and defend his reasoning using a word salad of half-assed smart-sounding terms that amounted to one giant non-sequitur.

Asked by another Twitter user what his reasoning was for calling the panic “dumb”, Musk responded by Tweeting:

“Virality of C19 is overstated due to conflating diagnosis date with contraction date & over-extrapolating exponential growth, which is never what happens in reality. Keep extrapolating & virus will exceed mass of known universe!”

One thing Musk may want to start extrapolating, however, is what happens when a cash strapped money losing company watches its worldwide production and demand simultaneously come to a halt at the time its stock crashes. And, continuing to extrapolate, what happens to its CEO who has loans against all of his shares?

And one more extrapolation: what happens when that company is a key piece in a house of cards that holds up several other business ventures?

$290 Billion Fund’s Advice To Investors: Don’t Look At Markets

112-year-old Scottish fund manager Baillie Gifford has seen market crises come and go before and as Covid-19, an oil-price war and fears of a U.S. recession are slamming global markets, partner Stuart Dunbar has one key piece of advice: Don’t panic.

With $290 billion under management, Dubar explained to Bloomberg (in the following edited and condensed transcript) his firm’s approach and why it’s best not to keep staring at the screens.

What should investors do in times of crisis?

The answer is, fundamentally, don’t panic. If you’re investing in a company on a 10-year view because you think it’s got wonderful opportunities and will grow to be a multiple of its current size, what’s changed in the last two months?

There are all sorts of near-term challenges. About short-term growth, about how companies are operating, about doing the right thing for stakeholders, for staff, for society in general when you’re confronted with a pandemic. Now everyone has an obligation to respond to that in a way that’s socially responsible, including this firm.

That’s what we’re in the midst of. I don’t think it makes a significant difference to whether great companies will be hugely successful in a 10-year view.

How much of the market is noise?

The market is a whole bunch of people speculating with a whole bunch of other people through the medium of share prices. That’s got very little to do with the fundamental progression of great companies. The market went up, the market went down. That’s just some kind of average measure of a bunch of people betting against each other from one day to the next. It’s really not that interesting. What ought to matter is the long term operational progression of the small number of companies that go on to be great.

Investing is capital deployment.

How are Baillie Gifford’s holdings doing?

There will be companies in our portfolios that are going to take a short-term hit on profits and growth because of coronavirus. Does that in some way completely change the long-term prospects for those companies? I can’t think of any cases where it does. Our approach to investing is such that unless the investment case is broken, if this is just noise, we’ll ignore it.

What if markets continue to sink?

If markets halve, we’re not going to sack half our people, we’re just going to make a lot less money for awhile. It’s not in the client’s interests to react in the short term to that sort of stuff. And it’s much easier to do that if you don’t have outside shareholders barking at you to try and hit profit targets every year.

What did you do in 2008?

We did absolutely nothing. Nothing. On the investment side, we took advantage of market falls to buy a bit more of companies that we liked. But I wouldn’t want to give the impression that there was a frenzy of activity. We did nothing that was out of the ordinary. We didn’t do anything in the firm. We didn’t slash costs. We didn’t make anyone redundant.

What about your bottom line?

The partners essentially said, “Even if there are no profits to share that’s okayfor a period of time because this is all about having a decent business in the long run.” It’s about doing the right thing for your staff as well. It’s about that long view. What are you going to do? Fire everyone to cut costs and hire them back 18 months later when you get busy again? I mean, it just doesn’t make sense.

Predictions?

The stock market will show volatility as it does. That’s just people putting a short term price on companies in the stock market. Our view would be — while in no way is this something that we should be dismissive of or not take seriously — that this too will pass.

It always does.

We’ve had SARS, we’ve had flu epidemics. We’ve had 9/11. You name it. You look back at all of these cataclysmic events and with the benefit of 10 years of hindsight, the world keeps going and great companies keep making progress.

Best advice for now?

Compel yourself to not look at what the markets are doing. That’s nearly impossible. And I’ll confess to you, I think I flipped up Bloomberg yesterday just to see if things are going up or down. If you can’t control your impulses, don’t look. If you can control your impulses, by all means look. But don’t do anything.