“Great Slowdown” – Indian Economy Headed Towards ICU, Warns Former Economic Official

The former Indian Chief Economic Adviser Arvind Subramanian warned that the Indian economy is headed for increased financial hardships, reported Business Today.

Subramanian said the country’s current economic slowdown is considered a “Great Slowdown.” He suggested that the economy is headed towards an “intensive care unit,” referencing how the economy is on life support.

He warned that the second wave of twin balance sheet (TBS) crises is crushing the economy, which will develop into an even more massive crisis, expected to unfold in the year ahead.

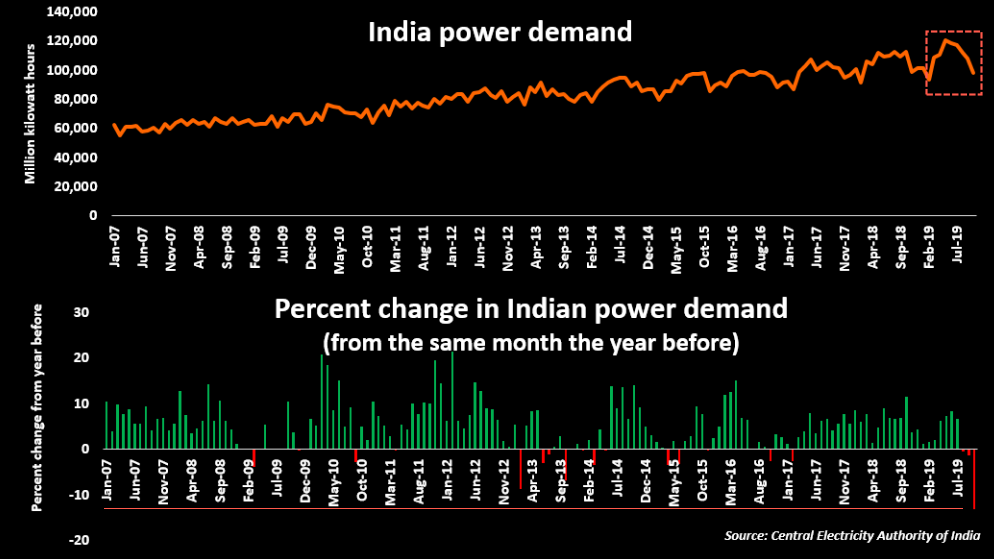

“Look at electricity generation growth, it’s falling off the bottom, and it’s never been like this ever. So this is the sense in which I would say this is not just any slowdown, this is the great slowdown that India is experiencing and we should look at it with all seriousness …and the economy seems headed for the intensive care unit,” Subramanian said during a conference at Harvard University’s Centre for International Development.

Subramanian also warned about the TBS crisis in 2014 when he was Chief Economic Advisor under the Modi government.

TBS refers to the developing problems in corporate debt and increasing non-performing assets have led to difficulties in the country’s banking sector that have weighed on credit growth. This has further slowed the economy and will likely lead to more deceleration through 2020.

Subramanian said IL&FS Ltd, or Infrastructure Leasing & Finance Services crisis in 2018, was a “seismic event” as it triggered panic in banks and raised questions about sustainability.

The TBS problem in India will push the economy much lower into 2020. Already, growth in Q3 stood at its lowest in six years.

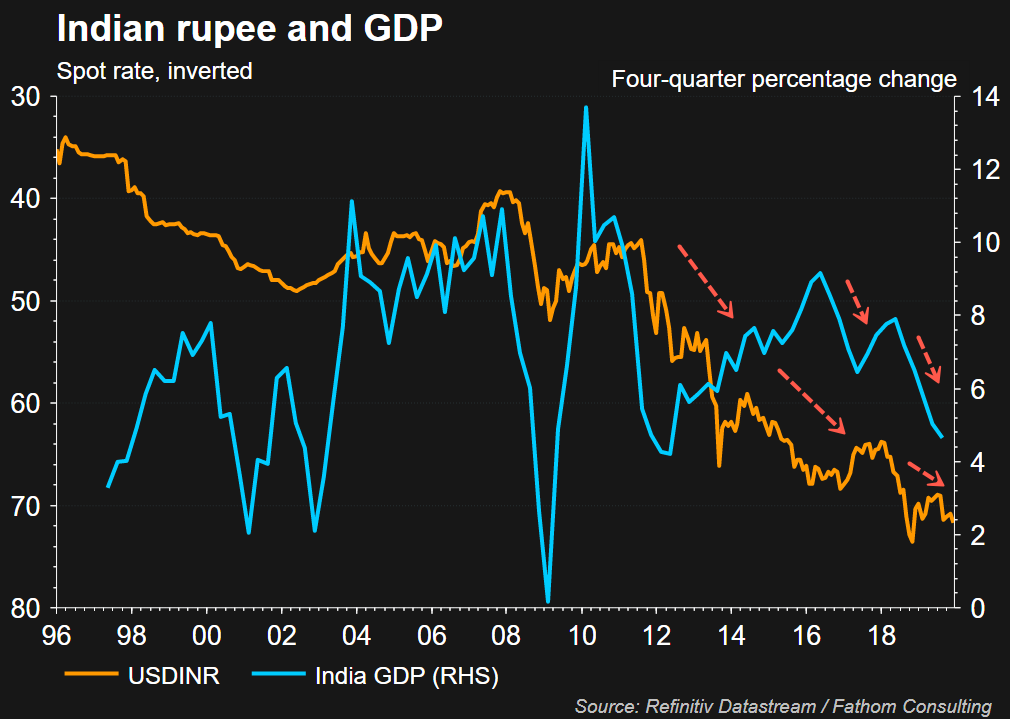

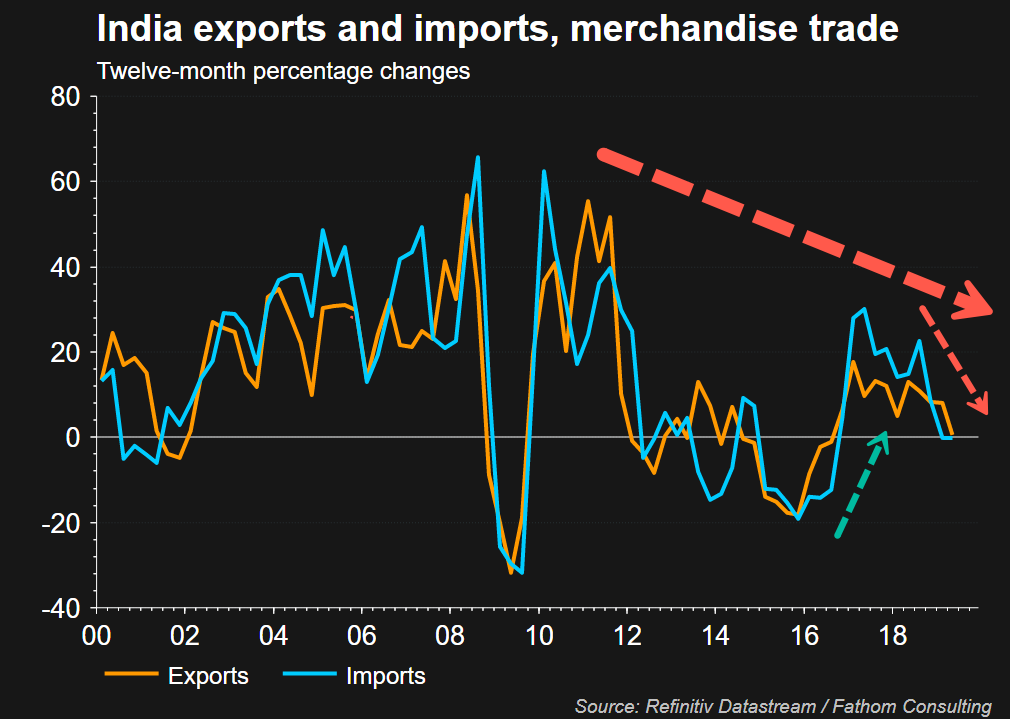

As economic growth rapidly slows, the Indian rupee has tumbled.

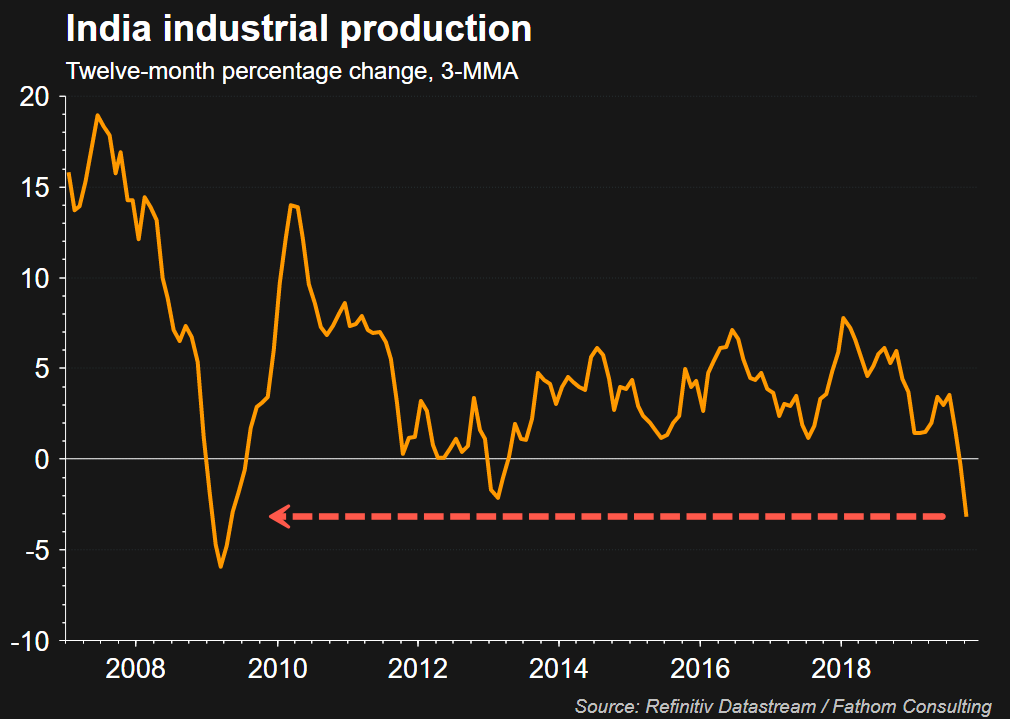

Industrial production growth is at the weakest level in a decade.

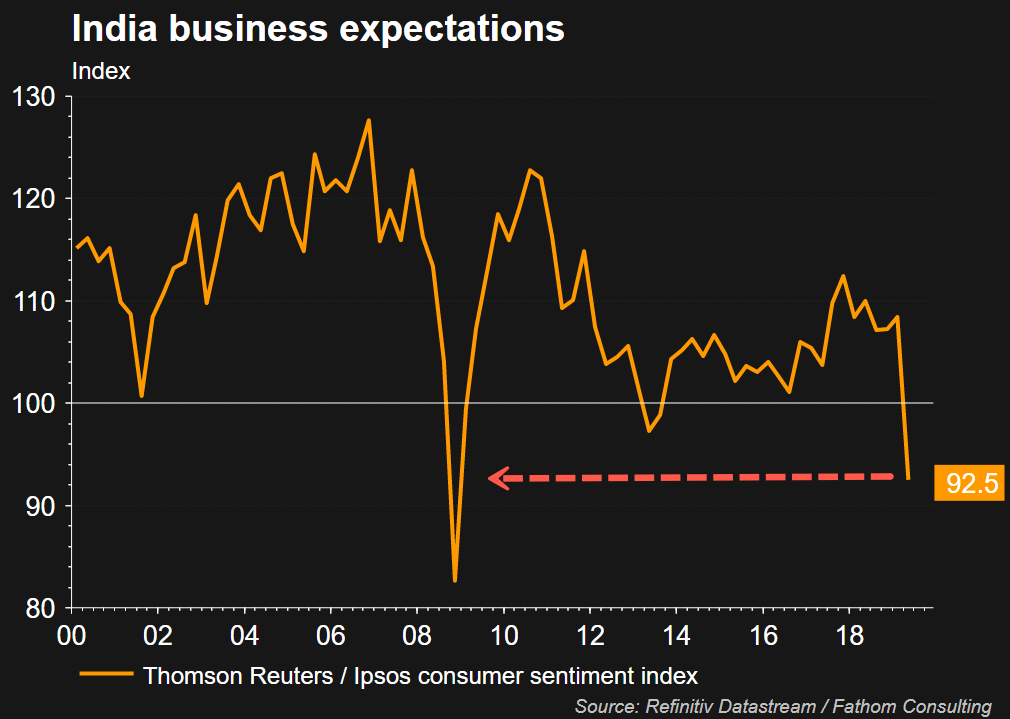

Business confidence has also plunged to decade lows.

And maybe because the 2016 recovery is over, a much longer-term downturn has resumed.

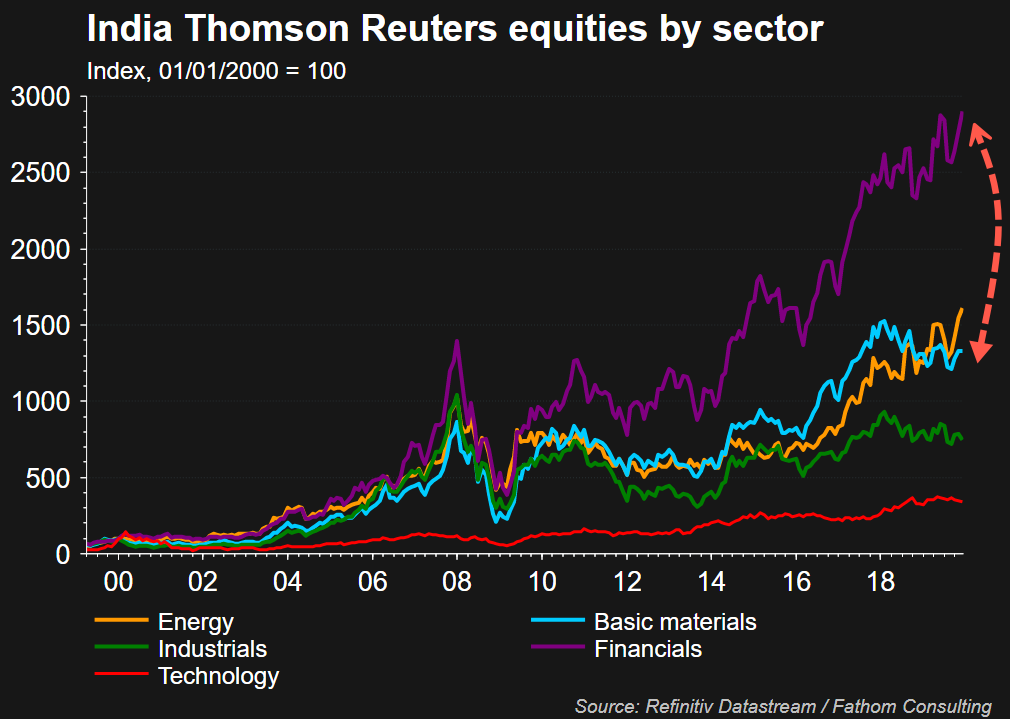

Clearly, the financial sector is the most significant imbalance in the system that could be corrected as the economy continues to decelerate.

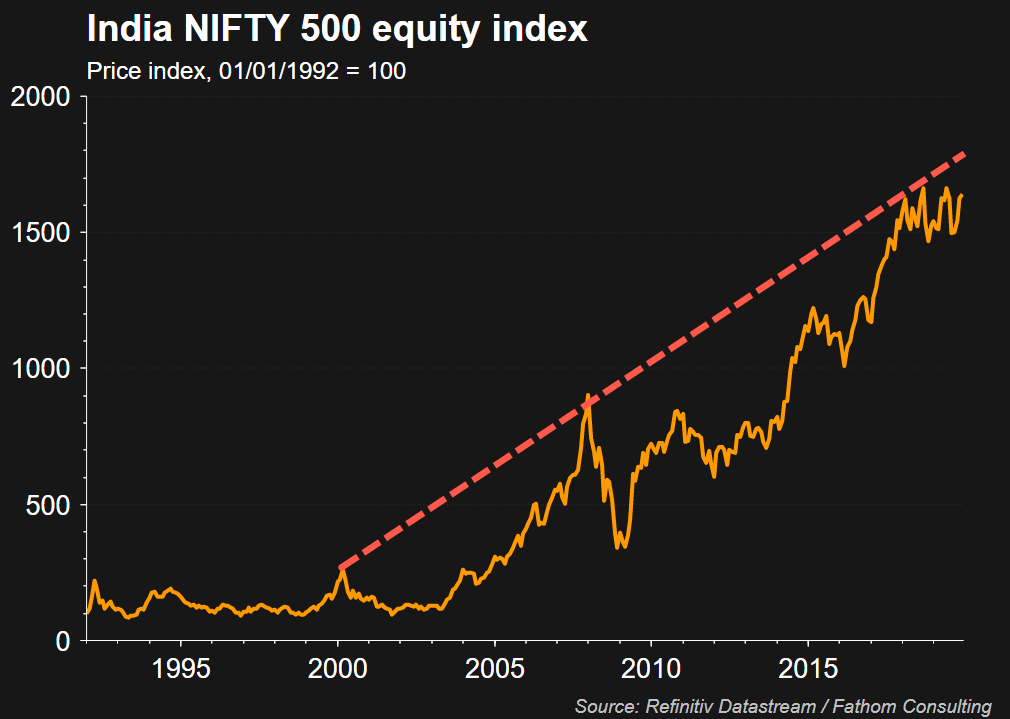

Indian stocks are bumping up against a two-decade diagonal resistance line.

Saxo Bank’s Christopher Dembik, global head of macro research, warned on Twitter earlier this month, that “All the leading indicators point out it will get worse.”

India’s slowdown has certainly been the most under-appreciated aspect of the current global downturn. In Q3 this year, the Indian economy reached a 6-year low at 4.5% YoY, down from 5% in the previous quarter. All the leading indicators point out it will get worse. pic.twitter.com/sGajxI9Q4u

Putting this all together, it means that central banks’ are failing to stabilize the global economy as it seems their policies are becoming less effective than ever before. This also means desynchronization continues to persist in the global economy, and really in manufacturing hubs around the world, indicating that a massive rebound in global growth, already priced in by global equity markets for early 2020, might be a fantasy at the moment.

In the early 1920s, Ludwig von Mises became a witness to hyperinflation in Austria and Germany – monetary developments that caused irreparable and (in the German case) cataclysmic damage to civilization.

Mises’s policy advice was instrumental in helping to stop hyperinflation in Austria in 1922. In his Memoirs, however, he expressed the view that his instruction — halting the printing press — was heeded too late:

Austria’s currency did not collapse — as did Germany’s in 1923. The crack up boom did not occur. Nevertheless, the country had to bear the destructive consequences of continuing inflation for many years. Its banking, credit, and insurance systems had suffered wounds that could no longer heal, and no halt could be put to the consumption of capital.

As Mises noted, hyperinflation in Germany was not stopped before the complete destruction of the reichsmark. To illustrate the monetary catastrophe, one may take a look at the exchange rate of the reichsmark against the US dollar.

Before the start of World War I in 1914, around 4.2 marks would buy 1 US dollar. As soon as war action began, the convertibility of the mark was suspended and paper marks (papiermark) were issued, largely for financing war-related outlays. In 1918, after the end of World War I, 8.4marks bought 1 US dollar. In December 1919, the mark had depreciated to 46.8 per US dollar, and in December 1920 to 73.4 per dollar.

In July 1922, the US dollar cost 670 marks.

When French and Belgian troops occupied the Rhineland at the beginning of 1923, however, the exchange rate of the mark plummeted to 49,000 marks per US dollar.

On November 15, 1923, when hyperinflation reached its peak, the currency reform effectively made 1 trillion (1,000,000,000,000) papiermarkequal to 1 rentenmark, and as 4.2 trillion papiermark exchanged for 1 US dollar at that time, 4.2 rentenmark would equal 1 US dollar.

Increases in the Money Supply

The 20th century saw many hyperinflations, including China in 1949–50, Brazil in 1989–90, Argentina in the late 1980s and early 1990s, Russia in 1992, Yugoslavia in 1994, and, most recently, Zimbabwe in 2006–09. All of these hyperinflations were the direct result of a system of unfettered fiat money under government control — a system that produces money in a non-market-conforming way: the money supply is increased out of thin air by banks simply extending loans (circulation credit) and/or monetizing assets.

Hyperinflation is perhaps the darkest side of a government fiat money regime. Among mainstream economists, hyperinflation typically denotes a period of exceptionally strong increases in overall prices of goods and services, thus denoting a period of exceptionally strong erosions in the exchange value of money. Some people consider a rise in overall prices of 10 percent per month (which implies an annual rate of price increases of around 214 percent) as hyperinflation; others indentify hyperinflation as a monthly price rise of at least 20 percent (which implies an annual increase in prices of nearly 792 percent).

However, any such numerical definition can be criticized, as it refers to the symptom rather than the root cause of the accelerating loss of the purchasing power of money. Economically speaking, hyperinflation is the inevitable consequence of an ever-greater rise in the amount of money. And this is exactly what the monetary theory of the Austrian School of economics teaches: In fact, Austrian theory shows that inflation is the logical consequence of a rise in the money supply, and that hyperinflation is the logical outcome of ever-higher growth rates in the money supply.

According to the Austrian school, money is, like any other good, subject to the irrefutably true law of diminishing marginal utility. It is this law, which is implied by the axiom of human action, which is at the heart of Mises’s praxeology. As it relates to money, the law of diminishing marginal utility states that an increase in the quantity of money by an additional unit will inevitably be ranked lower (that is, valued less) than any same-sized unit of money already in an individual’s possession. This is because the new money can only be employed as a means for removing a state of uneasiness that is deemed less urgent than the least-urgent uneasiness which one has up to now been removing with the money in one’s possession.

Money Demand

People hold money because money has purchasing power (which people desire, given the fact of uncertainty as an undeniable category of human action), and the purchasing power of money is determined by the supply of and demand for money.

If a rise in the money supply is accompanied by an equal rise in money demand, overall prices and the purchasing power of money remain unchanged. Once people start to exchange their increased money holdings against other goods, however, prices will start to rise, and the purchasing power of money will fall. That said, it is rise of the money supply relative to the demand for money that brings to the fore the obvious effect of an increasing money supply: rising prices.

Mises saw that money demand plays a crucial role for the possibility of an unfolding hyperinflation. If the central bank is expected to increase the money supply in the future, people can be expected to rein in their money demand in the present — that is, increasingly surrendering money against vendible items. This would, other things being equal, drive up money prices. Mises noted that “this goes on until the point is reached beyond which no further changes in the purchasing power of money are expected.”4 The process of rising prices would come to a halt once people have fully adjusted for the expected increase in the money supply.

What happens, however, if people expect that, in the future, the money-supply growth rate will increase to ever-higher rates? In this case, the demand for money would, sooner or later, collapse. Such an expectation would lead (relatively quickly) to a point at which no one would be willing to hold any money — as people would expect money to lose its purchasing power altogether. People would start fleeing out of money entirely. This is what Mises termed a crack-up boom:

If once public opinion is convinced that the increase in the quantity of money will continue and never come to an end, and that consequently the prices of all commodities and services will not cease to rise, everybody becomes eager to buy as much as possible and to restrict his cash holding to a minimum size. For under these circumstances the regular costs incurred by holding cash are increased by the losses caused by the progressive fall in purchasing power. The advantages of holding cash must be paid for by sacrifices which are deemed unreasonably burdensome. This phenomenon was, in the great European inflations of the ‘twenties, called flight into real goods (Flucht in die Sachwerte) or crack-up boom (Katastrophenhausse).5

The Unrelenting Power to Inflate

If people expect a forthcoming, drastic increase the money supply — but if they at the same time expect that such an increase will be limited (i.e., a one-off increase) — the central bank can actually orchestrate a debasing of money without causing its complete destruction. As long as government and its central bank succeed in making people believe that any future rise in the money supply will remain within an acceptable limit, from the viewpoint of the money holder, monetary policy is an effective and most perfidious instrument for expropriation and non-market-conforming income redistribution.

I am not saying that fiat money, once established on the ruins of gold, cannot then continue indefinitely on its own. Unfortunately … if fiat money could not continue indefinitely, I would not have to come here to plead for its abolition.6

Rothbard saw the danger that the government-controlled fiat money could be held up and running indefinitely, that it would not necessarily drive itself into a fatal and final collapse. As long as people do not expect that a money supply increase will spin out of control, the central bank is in a position to debase the currency without completely destroying it.

In other words: hyperinflation would be possible without destroying the money completely. The crack-up boom, as Mises pointed out, would unfold only when people come to the conclusion that the central bank will expand the money supply at ever-greater rates:

But then finally the masses wake up. They become suddenly aware of the fact that inflation is a deliberate policy and will go on endlessly. A breakdown occurs. The crack-up boom appears. Everybody is anxious to swap his money against “real” goods, no matter whether he needs them or not, no matter how much money he has to pay for them. Within a very short time, within a few weeks or even days, the things which were used as money are no longer used as media of exchange. They become scrap paper. Nobody wants to give away anything against them.7

Debt Levels

Today’s fiat-money regimes are characterized by ever-greater amounts of debt relative to real income — caused by policies that try to solve the economic problems caused by credit and money creation out of thin air by using even greater amounts of credit and money created out of thin air. And it is fair to say that the higher an economy’s overall debt level is, the more likely hyperinflation becomes.

To show this, let us assume that after a long period of money creation through bank circulation credit expansion a credit crisis emerges: Creditors are no longer willing to roll over maturing debt at prevailing interest rates. Borrowers cannot repay their obligations when payment is due, and neither can they afford paying higher borrowing costs. Investors start fleeing out of bonds, making interest rates increase sharply and thereby covering up unprofitable investment. More borrowers, including banks, fail to meet their obligations, and bankruptcies spread. Ensuing recession and rising unemployment aggravate the collapse of the credit structure.

Should investors in such a situation expect that the government and its central bank would opt for bailouts financed through additional money creation, the demand for money and fixed claims would most likely dry up. This would make it necessary for the central bank to extend ever-greater amounts of money to struggling borrowers in order to prevent the spread of bankruptcies. The larger the amount of outstanding debt is, the larger will be the potential increase in the money supply. The more the money supply grows, the more likely it is that there will be hyperinflation and a potential breakdown of money demand: the unfolding of a crack-up boom.

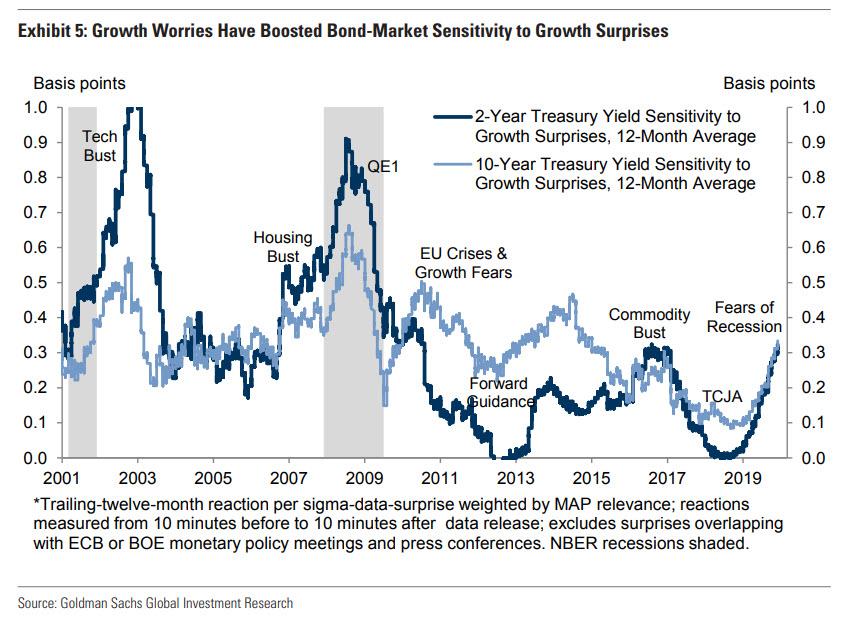

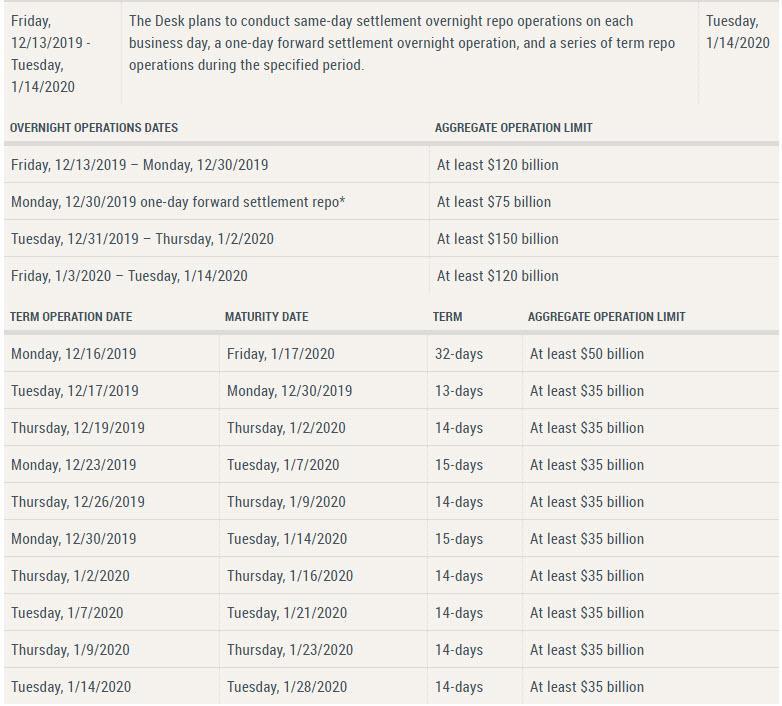

What Will The Market Care About In 2020? Here Is Goldman’s Answer

Now that two of the market’s greatest unknowns – Brexit/the UK election, and the “Phase One” part of the US-China trade war (with the Phase Two supposedly on the “to do” list after the Nov 2020 elections) – appear to have found an interim, if not fully satisfactory, resolution, a recurring question among the trader community is what will the market care about in the coming year.

Conveniently, an answer to that question is the topic of a Goldman report published over the weekend, and which points out that despite the immediate newsflow vacuum now that stocks will no longer rally on “optimism” of an imminent deal announcement, there is still quite a bit to occupy traders. Starting with the Treasury-market, Goldman notes that activity here will depend crucially on the Fed’s reaction function and the current pace of growth (among other things).

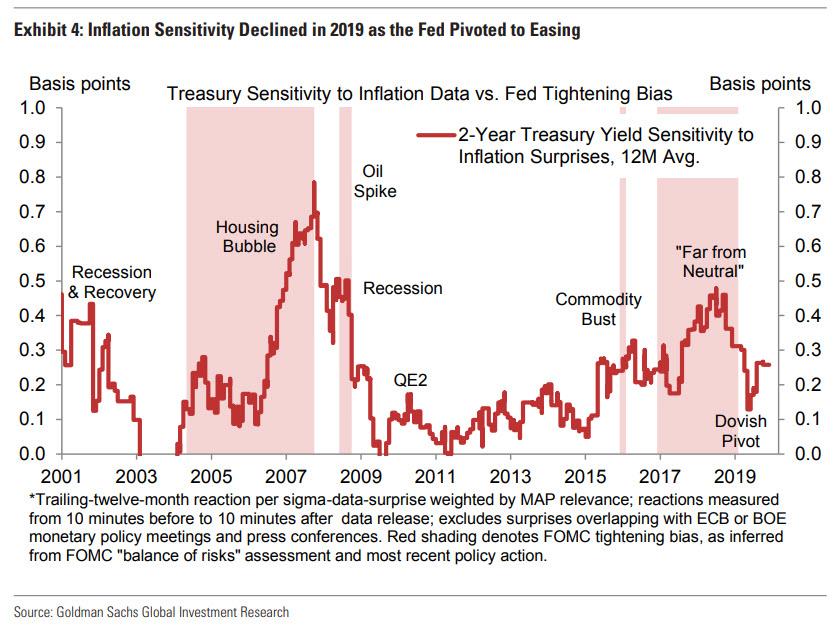

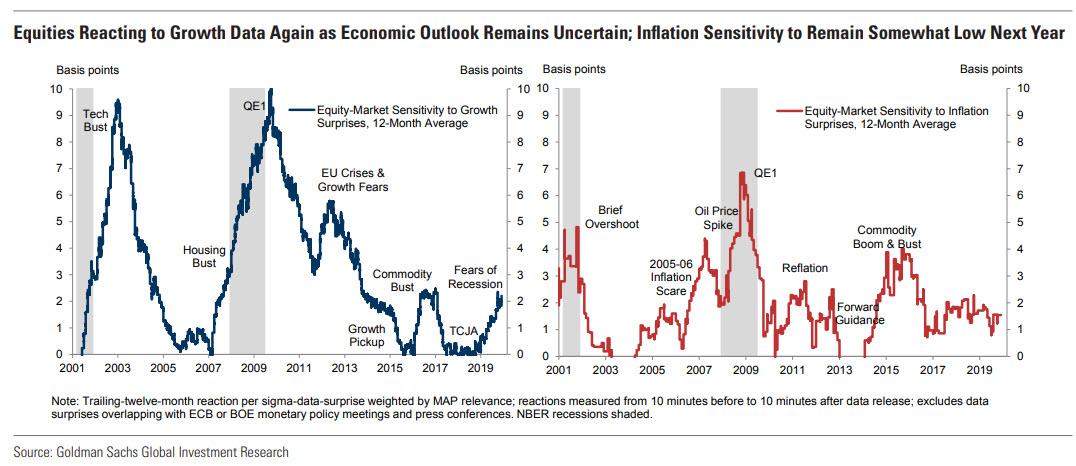

As shown in the chart below, sensitivity to inflation surprises picked up sharply in late 2017 and 2018 as the Fed hiked, as realized inflation moved towards the target, and as the risk of overheating entered the mainstream policy debate.

However, 2019 saw a reversal of all three trends, and inflation sensitivity declined arguably as a result.

Following the sharp tightening in financial conditions at the turn of the year, the combination of renewed growth fears, declining core inflation, and the dovish Fed pivot resulted in a roughly 50% decline in inflation sensitivity. Equity-market inflation sensitivity also declined, albeit more modestly.

In contrast, sensitivity to growth data picked up sharply in 2019, reflecting slowing growth and the return of recession fears. In fact, growth sensitivity in the bond market is already back to its level during the shale bust and capex-driven growth scare of 2016-17.

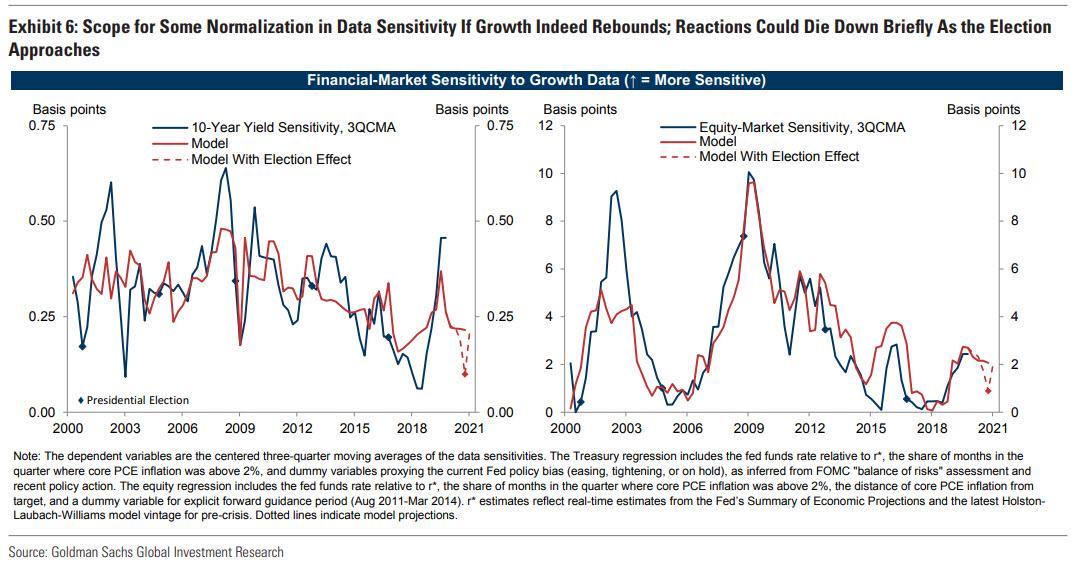

Looking ahead to 2020, Goldman expects another signal reversal, as its forecast of improving growth and diminished trade risks suggests scope for a modest pullback in sensitivity to growth data. Treasury-market sensitivity has already overshot relative to the bank’s predictions (see blue and red line in the left panel of Exhibit 6), and the end of the mid-cycle adjustment coupled with its expectation of firming US growth argues for more a normal degree of data sensitivity in early 2020.

Similarly, equity-market reactions to growth data could also wane a bit early next year if growth picks up.

It is also worth recalling that 2020 will be the year of the presidential election. As a result, Goldman analyzes the impact of elections on data sensitivity since 2000. Adding election dummy variables to the models shown in Exhibit 6, the bank finds a negative and significant “election effect” on growth sensitivity—with reactions to growth surprises attenuating in the quarter of presidential elections. Goldman analysts also find tentative evidence of attenuation in the quarter preceding the election (statistical power may be limited by the short sample).

The implications for 2020 are shown by the dotted lines above (i.e., a short-lived lull in data reactions in the coming fall 2020).

In contrast, the bank finds no such effects for inflation sensitivity. This may suggest that market participants view elections as more important for the growth outlook than for the near-term trajectory of core inflation (such that inflation news continues to be an important driver of price action, even if growth surprises are faded). In conclusion, Goldman expects inflation reactions to pick up gradually in 2020 as inflation rebounds towards the target and the Fed begins to contemplate its next move. All of that, of course, assumes that inflation will rebound next year as most on Wall Street now openly expect. However, if there is anything that 2019 once again vividly demonstrated, it is that when everyone expects something, the opposite happens.

It’s been a bad last 24 hours for the war propagandists.

WikiLeaks has published multiple documents providing further details on the coverup within the Organisation for the Prohibition of Chemical Weapons (OPCW) of its own investigators’ findings which contradicted the official story we were all given about an alleged chlorine gas attack in Douma, Syria last year. The alleged chemical weapons incident was blamed on the Syrian government by the US and its allies, who launched airstrikes against Syria several days later. Subsequent evidence indicating that there was insufficient reason to conclude the chlorine gas attack ever happened was repressed by the OPCW, reportedly at the urging of US government officials.

The new publications by WikiLeaks add new detail to this still-unfolding scandal, providing more evidence to further invalidate attempts by establishment Syria narrative managers to spin it all as an empty conspiracy theory. The OPCW has no business hiding any information from the public which casts doubt on the official narrative about an incident which was used to justify an act of war on a sovereign nation.

RELEASE: Third batch of documents showing doctoring of facts in released version of OPCW chemical weapons report on Syria. Including a memo stating 20 inspectors feel released version “did not reflect the views of the team members that deployed to [Syria]”https://t.co/ndK4sRikNk

1. The symptoms of the alleged victims of the supposed chemical incident were inconsistent with chlorine gas poisoning.

“Some of the signs and symptoms described by witnesses and noted in photos and video recordings taken by witnesses, of the alleged victims are not consistent with exposure to chlorine-containing choking or blood agents such as chlorine gas, phosgene or cyanogen chloride,” we learn in the unredacted first draft. “Specifically, the rapid onset of heavy buccal and nasal frothing in many victims, as well as the colour of the secretions, is not indicative of intoxication from such chemicals.”

“The large number of decedents in the one location (allegedly 40 to 45), most of whom were seen in videos and photos strewn on the floor of the apartments away from open windows, and within a few meters of an escape to un-poisoned or less toxic air, is at odds with intoxication by chlorine-based choking or blood agents, even at high concentrations,” the unredacted draft says.

This important information was omitted from the Interim Report and completely contradicted by the Final Report, which said that the investigation had found “reasonable grounds that the use of a toxic chemical as a weapon took place. This toxic chemical contained reactive chlorine. The toxic chemical was likely molecular chlorine.”

2. OPCW inspectors couldn’t find any explanation for why the gas cylinders supposedly dropped from Syrian aircraft were so undamaged by the fall.

“The FFM [Fact-Finding Mission] team is unable to provide satisfactory explanations for the relatively moderate damage to the cylinders allegedly dropped from an unknown height, compared to the destruction caused to the rebar-reinforced concrete roofs,” reads the leaked first draft. “In the case of Location 4, how the cylinder ended up on the bed, given the point at which it allegedly penetrated the room, remains unclear. The team considers that further studies by specialists in metallurgy and structural engineering or mechanics are required to provide an authoritative assessment of the team’s observations.”

We now know that a specialist was subsequently recruited to find an answer to this mystery. A leaked document dated February 2019 and published by the Working Group On Syria, Propaganda and Media in May 2019 was signed by a longtime OPCW inspector named Ian Henderson. Henderson, a South African ballistics expert, ran some experiments and determined that “The dimensions, characteristics and appearance of the cylinders, and the surrounding scene of the incidents, were inconsistent with what would have been expected in the case of either cylinder being delivered from an aircraft,” writing instead that the cylinders being “manually placed” (i.e. staged) in the locations where investigators found them is “the only plausible explanation for observations at the scene.”

More on Ian Henderson in a moment.

3. The team concluded that either the victims were poisoned with some unknown gas which wasn’t chlorine, or there was no chemical weapon at all.

“The inconsistency between the presence of a putative chlorine-containing toxic chocking or blood agent on the one hand and the testimonies of alleged witnesses and symptoms observed from video footage and photographs, on the other, cannot be rationalised,” the unredacted first draft reads. “The team considered two possible explanations for the incongruity:

a. The victims were exposed to another highly toxic chemical agent that gave rise to the symptoms observed and has so far gone undetected.

b. The fatalities resulted from a non-chemical-related incident.”

Again, none of this information made it into any of the OPCW’s public reports on the Douma incident. The difference between the information we were given (that a chlorine gas attack took place and the strong suggestion that it was dropped by Syrian aircraft) and the report the inspectors were initially trying to put together (literally the exact opposite) is staggering. For more insider information on the deliberation between OPCW inspectors who wanted their actual findings to be reported and the organisation officials who conspired to omit those findings, read this November report by journalist Jonathan Steele.

It’s worth noting that this memo is dated two weeks after the OPCW published its Final Report on the Douma incident in March 2019, because it further invalidates the bogus argument made by narrative management firms like Bellingcat claiming that the grievances of the dissenting OPCW inspectors had been satisfactorily addressed by the time the Final Report was published.

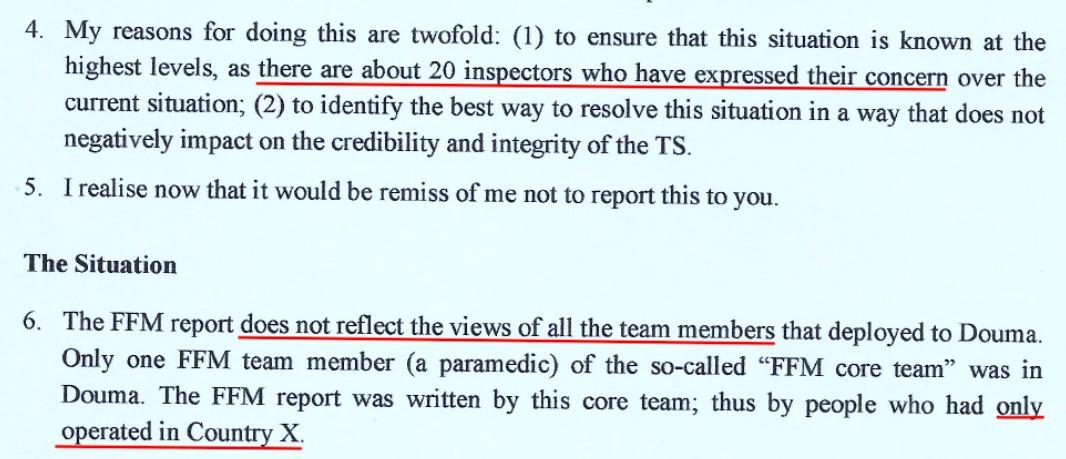

Clearly the concerns were not addressed, because the memo consists entirely of complaints, and according to its author “there are about 20 inspectors who have expressed their concern over the current situation.”

The memo’s author complains that the FFM report was made almost exclusively by team members who never even went to Douma, doing their research instead solely in “Country X”, which WikiLeaks speculates may be Turkey.

“The FFM report does not reflect the views of all the teams that deployed to Douma,” the memo says. “Only one team member (a paramedic) of the so-called ‘FFM core team’ was in Douma. The FFM report was written by this core team, thus by people who had only operated in Country X.”

“After the exclusion of all team members other than a small cadre of members who had deployed (and deployed again in October 2018) to Country X, the conclusion seems to have turned completely in the opposite direction. The FFM team members find this confusing, and are concerned to know how this occurred.”

The memo’s author is unnamed in the WikiLeaks document, but claims to have been “assigned the task of analysis and assessment of the ballistics of the two cylinders,” indicating that it was likely the aforementioned Ian Henderson. A concurrent publication by Peter Hitchens in the Daily Mail appears to confirm this. Hitchens reports that when Henderson lodged his Engineering Assessment in the OPCW’s secure registry after failing to get traction for his report, which the memo’s author also reports to have done, an unpopular unnamed OPCW official nicknamed “Voldemort” ordered that every trace of the report be removed.

“Mr Henderson tried to get his research included in the final report, but when it became clear it would be excluded, he lodged a copy in a secure registry, known as the Documents Registry Archive (DRA),” Hitchens reported. “This is normal practice for such confidential material, but when ‘Voldemort’ heard about it, he sent an email to subordinates saying: ‘Please get this document out of DRA … And please remove all traces, if any, of its delivery/storage/whatever in DRA’.”

So to recap, the OPCW enlisted a longtime ballistics expert with an extensive history of work with the organisation to run some experiments and produce an Engineering Assessment to explain how the alleged chlorine cylinders could have been found in the condition they were found in, and when he came to conclusions which were exculpatory for the Syrian government, his boss ordered every sign of it purged from the registry.

Again, not a whisper of any of this was breathed in the OPCW’s public reports on the Douma incident, despite somewhere around 20 inspectors having objections. The OPCW had no business hiding this from the public.

The usual regime change fanatics helped provoke more OPCW leaks by flagrantly lying about a whistleblower. Read the whole thread here. https://t.co/fyrfBnoxM2

This interesting email, sent to the OPCW’s Office of Strategy and Planning Director Veronika Stromsikova, defended Ian Henderson and objected to the mistreatment of a principled and respected team member.

“A member of the FFM team has been suspended from his post and escorted from the OPCW building in a less than dignified manner,” the email’s author complains. “After more than 12 years, I believe, serving the OPCW with dedication and professionalism, Ian Henderson’s personal and professional integrity have taken a knock in the most public of fora, the internet. A falsehood issued by the OPCW, that Ian did not take part in the Douma FFM team, has been pivotal in discrediting him and his work.”

“The denial is patently untrue,” the email’s author writes. “Ian Henderson WAS part of the FFM and there is an abundance of official documentation, as well as other supporting proof, that testifies to that.”

But I don’t suppose we can expect to see any apologies or corrections from the usual suspects in light of this new information.

“We are not insisting on being right in our assertions, but we are demanding to be heard,” the email’s author writes. “We have desperately tried to limit expression of concerns to within the Organisation and will continue to do so. However, we have been stonewalled throughout by obfuscation, exclusion, and even thuggish and bullying behavior.”

The author wraps things up by explaining why they’re pushing so hard to be heard with a quote from Edmund Burke: “All that is required for evil to triumph is for good men to do nothing.”

This July 2018 correspondence is significant mainly because it brings in hard evidence for the exchange described by the OPCW whistleblower “Alex” in the aforementioned Jonathan Steele report, which was described as follows:

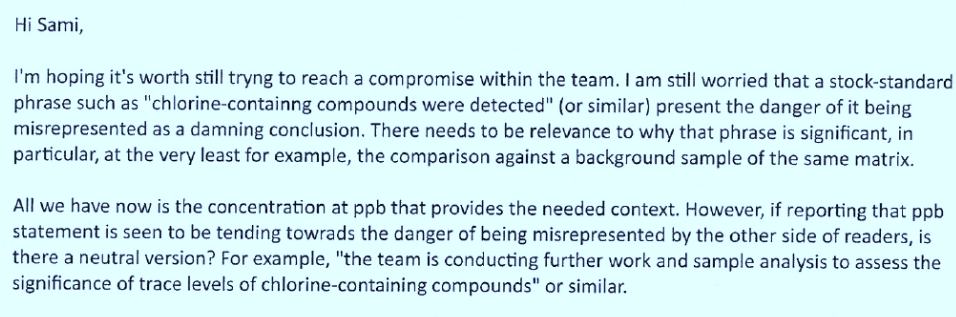

“This request was rejected but Sami Barrek, the team leader, was put in charge of replacing the doctored version with what turned out to be a toned-down but still misleading report. During the editing four of the Douma inspectors, including Ian Henderson, the engineering expert, had managed to get Barrek to agree that the low levels of COCs [Chlorinated Organic Chemicals] should be mentioned. On the day before the new publication date, July 6, they found that the levels were again being omitted.”

The back-and-forth exchanges feature one or more anonymous team members arguing with Barrek that more information needs to be included in the Interim Report so that people won’t jump to conclusions that the team had found evidence it hadn’t. And sure enough, Moon of Alabama documented multiple mass media headlines which falsely claimed the Interim Report had asserted chlorine gas was used (that invalid claim wasn’t made until the Final Report in March 2019).

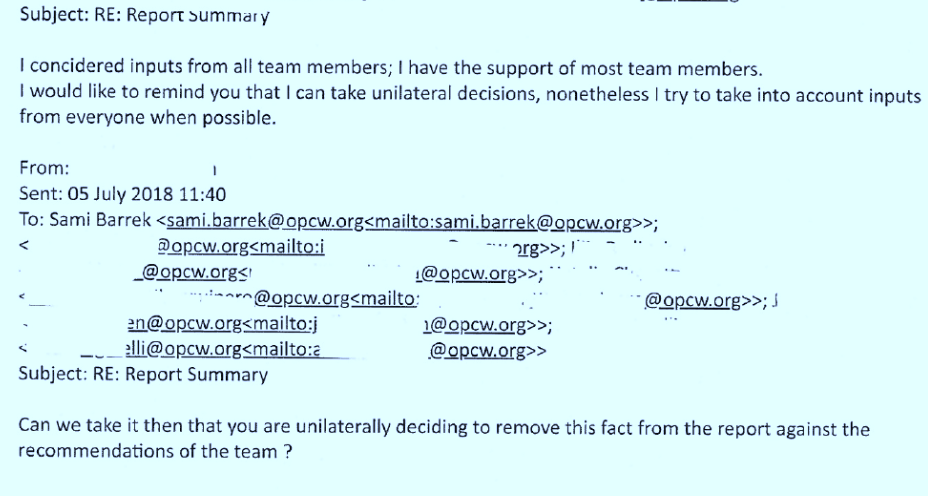

Here’s a sample exchange where one inspector tries to persuade Barrek to change the language in the report so readers will understand that the information they had about chlorinated organic chemical concentrations at the time hadn’t reached any “damning conclusion”, with Barrek throwing up inertia and saying he can unilaterally overrule them if he wants to:

Again, none of the findings which were inconsistent with the US narrative were included in either the final draft of the Interim Report or in the Final Report. Nothing about the low levels of chlorinated organic chemicals, nothing about the inconsistencies in symptoms with chlorine gas poisoning, nothing about the lack of damage to the cylinders, nothing about Ian Henderson’s findings. Nothing. The OPCW had no business withholding that information.

Eight weeks ago a whistleblower claimed to have documents showing “irregularities” in the OPCW’s investigation of a suspected chemical attack in Syria. Since then, only one document has surfaced. Where are the others? https://t.co/hacK3PeId1

These new leaks take care of the latest spin jobs by establishment narrative managers, who were just the other day beginning to argue that the fact that there hadn’t been any more OPCW leaks in a while indicated that the whole OPCW scandal was bogus. Sorry to disappoint you, fellas.

My full account of what took place at Newsweek.

Despite a number of offers, I decided to publish on my website because I take full responsibility for what’s reported

It’s a long piece so I recommend reading at a time when you can digest and on a computerhttps://t.co/obpcSgaa1A

The WikiLeaks documents and Hitchens’ Daily Mail article came out the same day as ex-Newsweek reporter Tareq Haddad shared emails sent to him by his editors forbidding him to publish information on the OPCW scandal, an important slice of information on the way mass media outlets stifle commentary on important stories that are inconvenient for US imperialism.

Newsweek’s foreign affairs editor Dimi Reider (who Haddad notes has Council on Foreign Relations ties) shot down Haddad’s pitch for a story about the OPCW scandal last month by falsely claiming that Bellingcat had “published a thorough refutation” of the story Haddad wanted to report on. In fact, as I documented at the time, Bellingcat had published an unbelievably pathetic spin job in which it tried to paint the whole OPCW scandal as a big misunderstanding.

Bellingcat argued that the concerns voiced in the leaked email published by WikiLeaks last month about the developing Interim Report in July 2018 had been fully addressed by the time the Final Report was published in March 2019, citing as evidence the fact that some slight adjustments had been made in the wording, like changing “likely” to “possible” and changing “reactive chlorine containing chemical” to “chemical containing reactive chlorine.” In focusing on this ridiculous, pedantic nonsense, Bellingcat tries to weave the narrative that because the whistleblower’s concerns were addressed with this pedantry, there was therefore no OPCW coverup. Never mind the fact that the multiple OPCW whistleblowers were still plainly so incensed by the organisation’s publishing that they felt the need to leak internal documents. Never mind that Bellingcat made no attempt whatsoever to address the aforementioned actual grievances by the OPCW whistleblowers like the low levels of chlorinated organic chemicals on the scene, the inconsistencies in symptoms and testimony with chlorine poisoning, or the Ian Henderson report.

But that’s what happens when mass media outlets like The New York Times and The Guardian publish swooning puff piece after swooning puff piece about Bellingcat; they grant a US government-funded narrative management firm so much unearned legitimacy that even a transparently bogus argument like the one they made about the OPCW scandal gets passed around newsrooms by credulous editors assuring each other that it’s a “thorough refutation” of facts and reality. Mass media outlets help puff up Bellingcat’s legitimacy, and in turn Bellingcat rewards them with an excuse to not have to ever challenge establishment narratives.

Reider also argued that Haddad’s report on the OPCW couldn’t be published because “not a single respected media outlet — many of whom boast far greater regional expertise, resources on the ground and in newsroom than Newsweek does — have taken the leak remotely seriously.”

That’s a great self-reinforcing system, isn’t it? MSM outlets validate US government-funded narrative managers like Bellingcat so they can tell them with authority why an unauthorised story shouldn’t be published, and each outlet sees the absence of other outlets reporting on it as evidence that it shouldn’t be reported on. And we wonder why no one’s reporting on the OPCW scandal.

Fake News By Omission — The Mass Media’s Cowardly Distortion Tool

“The exceptional silence on the OPCW scandal from imperial news media discredits them completely, but people won’t know about it unless they are told. Spread the word.” #OPCW#Syriahttps://t.co/MSrSh2vgP7

And Newsweek’s Digital Director Laura Davis gave Haddad the same answer, regurgitating the absolutely bogus Bellingcat line that the leaked email wasn’t newsworthy because “it predates the final report” and because no one else has written about it. It’s a system fully locked down against any oppositional reporting, and we can surmise that this is the norm for newsrooms throughout the English-speaking world.

Haddad also published a similar email he’d received from International Business Times then-editor-in-chief Julian Kossoff, who rejected a pitch he’d made for an opinion piece he’d written about the Khan Sheikhun incident in April 2017.

“Thanks for the suggested opinion piece,” Kossoff wrote. “However, I do not think we will be able to use it. Its narrative is highly controversial and likely to offend and only a writer or expert of repute (e.g Noam Chomsky) could get away with such an incendiary thesis.”

And what was this “incendiary thesis”? Well, Haddad published it with CounterPunch, so you can see for yourself. He simply argued what in my opinion should be a completely uncontroversial position: that there wasn’t yet enough evidence to be certain Assad was behind the attacks, and the US has a known history of entering into military entanglements based on lies, so the warmongers demanding Assad’s overthrow shouldn’t be listened to.

This insight into the dynamics behind the mass media’s lies by omission are very valuable, and they help us paint a better picture about the reason we’re not seeing more discussion of these OPCW leaks.

‘You Need Rehabilitation’: Nunes Letter Dismantles Schiff Over FISA Lies, Stroking Steele, And Participating In Coverup

“As part of your rehabilitation, it’s crucial that you admit you have a problem – you are hijacking the Intelligence Committee for political purposes while excusing and covering up intelligence agency abuses.” -Devin Nunes to Adam Schiff

Rep. Devin Nunes (R-CA) has written perhaps the most brutal ‘I told ya so’ letter in recent memory to Adam Schiff, his Democratic rival and chairman of the House Intelligence Committee.

After last week’s Inspector General report on FBI FISA abuse revealed Schiff was peddling lies to the American public in a February, 2018 ‘counter-memo’ to Nunes’s now-proven claims, Schiff passed the buck – telling Fox News host Chris Wallace on Sunday that he was ‘unaware’ of certain things unccovered by the IG – while failing to admit he’s been dead wrong on an ongoing basis about a number of things.

Nunes isn’t letting this go. In a Sunday letter, he reminded Schiff that “The IG’s findings of pervasive, major abuses by the FBI dramatically contradict the assertions of your memo released on February 24, 2018, in which you claimed, “FBI and DOJ officials did not ‘abuse’ the Foreign Intelligence Surveillance Act (FISA) process, omit material information, or subvert this vital tool to spy on the Trump Campaign.“

Schiff is in clear “need of rehabilitiation,” continues Nunes, adding “I hope this letter will serve as the first step in that vital process.“

“Outlining every false claim from your memo would require an extremely long letter,” Nunes continues, who then lists several key claims made by Schiff which ‘the IG report has exposed as false.’

FBI and DOJ officials did not omit material information from the FISA warrant.

The DOJ “made only narrow use of information from [Christopher] Steele’s sources about Page’s specific activities in 2016.”

In subsequent FISA renewals, DOJ provided additional information that corroborated Steele’s reporting.

The Page FISA warrant allowed the FBI to collect “valuable intelligence.”

“Far from “omitting’ material facts about Steele, as the Majority claims. DOJ repeatedly informed the Court about Steele’s background, credibility, and potential bias.”

The FI31 conducted a “rigorous process” to vet Steele’s allegations, and the Page FISA application explained the FBI’s reasonable basis for finding Steele credible.

Steele’s prior reporting was used in criminal proceedings.

Nunes goes on to dismantle Schiff’s bullshit point by point using findings from the IG report, which include:

Information provided by Christopher Steele played a “central and essential role” in the decision to seek a FISA warrant on Carter Page.

There were seventeen “significant errors or omissions” in the FISA application and renewals, and the IG did not get satisfactory explanations for them.

The Crossfire Hurricane team failed to inform the DOJ of “significant information”, and “much of that information was inconsistent with, or undercut” assertions in the FISA applications.

The FBI relied solely on Steele information for its assertions about Page’s alleged coordination with Russians to hack the 2016 elections.

(See entire list below)

Nunes then calls out Schiff for defending former UK spy Christopher Steele, whose discredited dossier funed by the Clinton campaign was peddled to the media six weeks before the 2016 US election.

“As you know, your misguided validation of the FISA warrant was part of a years-long pattern in which you touted Christopher Steele’s credentials and reliability,” writes Nunes.

“For example, during this committee’s March 20, 2017 open hearing, you claimed Steele “is reportedly held in high regard by U.S. Intelligence.” and proceeded to read into the congressional record numerous conspiracy theories proffered by Steele, all of which are false.”

Next, Nunes accused Schiff of participating in a coverup:

As is clear from the 16 report, Carter Page was the victim of a smear campaign that was funded by the Democratic National Committee and the Hillary Clinton campaign and was implemented by Christopher Steele and Fusion GPS. The FBI used these false allegations to obtain a warrant to spy on Page, a gross violation of an American citizen’s civil liberties. Your direct participation in the smear campaign against Page is extremely concerning. considering you are chairman of the committee responsible for uncovering precisely these sorts of abuses by the Intelligence Community. Instead of joining committee Republicans in exposing these abuses, however, you excused them. And by supporting the agencies’ stonewalling of our attempts to gather information on this affair, you helped cover up this misconduct.

Because of Schiff’s misdeeds, and his blind faith in the US intelligence communities which the House Intelligence Committee is supposed to monitor, Nunes says “This makes it clear your rehabilitation will be a long, arduous process.”

“this committee is responsible for overseeing the Intelligence Community and exposing abuses. Yet when the IG identified gross abuses in our jurisdiction, you expressed full faith in the agencies we’re supposed to be vigilantly monitoring. and you rejected any oversight whatsoever of their supposed clean-up efforts,” writes Nunes.

Read the entire letter below:

***

Dear Chairman Schiff:

As you are aware, on December 9, 2019, U.S. Department of Justice Inspector General (IG) Michael Horowitz published the results of his investigation of the FISA warrant and renewals obtained by the Federal Bureau of Investigations (FBI) and the Department of Justice (DOJ) to spy on Trump campaign associate Carter Page. The IG’s findings of pervasive, major abuses by the FBI dramatically contradict the assertions of your memo released on February 24, 2018, in which you claimed, “FBI and DOJ officials did not ‘abuse’ the Foreign Intelligence Surveillance Act (FISA) process, omit material information, or subvert this vital tool to spy on the Trump Campaign.”

After publishing false conclusions of such enormity on a topic directly within this committee’s oversight responsibilities, it is clear you are in need of rehabilitation, and I hope this letter will serve as the first step in that vital process.

Outlining every false claim from your memo would require an extremely long letter, so I will limit my summary to a few highlights. In your memo you made the following assertions:

FBI and DOJ officials did not omit material information from the FISA warrant.

The DOJ “made only narrow use of information from [Christopher] Steele’s sources about Page’s specific activities in 2016.”

In subsequent FISA renewals, DOJ provided additional information that corroborated Steele’s reporting.

The Page FISA warrant allowed the FBI to collect “valuable intelligence.”

“Far from “omitting’ material facts about Steele, as the Majority claims. DOJ repeatedly informed the Court about Steele’s background, credibility, and potential bias.”

The FI31 conducted a “rigorous process” to vet Steele’s allegations, and the Page FISA application explained the FBI’s reasonable basis for finding Steele credible.

Steele’s prior reporting was used in criminal proceedings.

The IG report has exposed all these declarations as false. Despite your denial of any problems with the FISA warrant, the 16 found:

Information provided by Christopher Steele played a “central and essential role” in the decision to seek a FISA warrant on Carter Page.

There were seventeen “significant errors or omissions” in the FISA application and renewals, and the IG did not get satisfactory explanations for them.

The Crossfire Hurricane team failed to inform the DOJ of “significant information”, and “much of that information was inconsistent with, or undercut” assertions in the FISA applications.

The FBI relied solely on Steele information for its assertions about Page’s alleged coordination with Russians to hack the 2016 elections.

The applications omitted information provided to the FBI about Page’s operational contact with another U.S. government agency and the agency’s positive assessment of him. In fact, an FBI official altered an email stating that Page was a source for another government agency in order to have it read the opposite—that he was “not a source.”

FBI Director James Conley and Deputy Director Andy McCabe sought to include Steele’s reporting in the Intelligence Community Assessment even though the CIA dismissed the Steele information as `Internet rumor.”

In FBI interviews, Steele’s own sources contradicted information from Steele that was used in the FISA applications.

The significance of Steele’s prior reporting was ‘-overstated.”

None of the Steele reporting on Caner Page used in the FISA applications could be corroborated, and some of it contradicted other information in the FBI’s possession.

The FBI omitted information about Steele’s bias provided by DOJ official Bruce Ohr.

The applications omitted exculpatory statements by Page and others.

The FBI failed to reveal in the applications that the Democratic National Committee and the Hillary’ Clinton campaign were receiving and/or funding Steele’s work through Fusion UPS.

Overall, the Inspector General found, “That so many basic and fundamental errors were made by three separate, hand-picked teams on one of the most sensitive FBI investigations that was briefed to the highest levels within the FBI, and that FBI officials expected would eventually be subjected to close scrutiny, raised significant questions regarding the FBI chain of command’s management and supervision of the FISA process… In our view, this was a failure of not only the operational team, but also of the managers and supervisors, including senior officials, in the chain of command.” Indeed, the problems are so severe that the Inspector General has initiated an audit to further investigate FBI’s compliance with Woods Procedures in FISA applications.

As you know, your misguided validation of the FISA warrant was part of a years-long pattern in which you touted Christopher Steele’s credentials and reliability. For example, during this committee’s March 20, 2017 open hearing, you claimed Steele “is reportedly held in high regard by U.S. Intelligence.” and proceeded to read into the congressional record numerous conspiracy theories proffered by Steele, all of which are false. These included:

Carter Page had a secret meeting with Rosneft CEO Igor Sechin.

Sechin offered Page a brokerage fee involving the sale of 19 percent of Rosneft.

Russians offered the Trump campaign dirt on Hillary Clinton in exchange for the Trump administration adopting policies favorable to Russia

Paul Manafort chose Page to act as a go-between for the Trump campaign and Russia.

As is clear from the 16 report, Carter Page was the victim of a smear campaign that was funded by the Democratic National Committee and the Hillary Clinton campaign and was implemented by Christopher Steele and Fusion GPS. The FBI used these false allegations to obtain a warrant to spy on Page, a gross violation of an American citizen’s civil liberties. Your direct participation in the smear campaign against Page is extremely concerning. considering you are chairman of the committee responsible for uncovering precisely these sorts of abuses by the Intelligence Community. Instead of joining committee Republicans in exposing these abuses, however, you excused them. And by supporting the agencies’ stonewalling of our attempts to gather information on this affair, you helped cover up this misconduct.

I am particularly concerned by the press release you issued after the release of the IG report. I applaud you for acknowledging that the report identified “issues and errors” and “potential misconduct” connected to the FISA warrant. This acknowledgement, though dramatically downplaying the scale of the abuse the IG uncovered, could be a valuable first step – a baby step, but a step nonetheless – in your rehabilitation. Nevertheless, in your statement you expressed full faith in FBI Director Christopher Wray’s promise to address the problem: demanded that the implementation of reforms be confined to “career officials, away from the political arena;” and denounced Attorney General Bill Barr and U.S. Attorney John Durham for expressing concerns about these matters.

This makes it clear your rehabilitation will be a long, arduous process. As previously noted, this committee is responsible for overseeing the Intelligence Community and exposing abuses. Yet when the IG identified gross abuses in our jurisdiction, you expressed full faith in the agencies we’re supposed to be vigilantly monitoring. and you rejected any oversight whatsoever of their supposed clean-up efforts. If agencies with a documented, severe abuse problem should be trusted to police themselves, then it’s fair to ask why this committee even exists and what we’re supposed to be doing, if anything, aside from being exploited by you as a launching pad to impeach the president for issues that have no intelligence component at all.

As part of your rehabilitation, it’s crucial that you admit you have a problem – you are hijacking the Intelligence Committee for political purposes while excusing and covering up intelligence agency abuses. The next step will be to convene a hearing with IG Horowitz, as the Senate Judiciary Committee has done and the Senate Homeland Security Committee will do next week.

I understand taking action on this issue will be difficult for you, as it will be an implicit acknowledgment that you were wrong to deny these abuses and that you were complicit in the violation of an American’s civil liberties. I also understand such an acknowledgement is made even more difficult by the fact that you’ve already been discredited by your years-long false claim that the Trump campaign colluded with Russia to hack the 2016 presidential election.

Nevertheless, I refuse to believe you are beyond redemption. I invite you to work closely with me on your rehabilitation program, and look forward to your scheduling a committee hearing with IG Horowitz at the nearest opportunity.

Second Damning FBI Lie About Carter Page Revealed In IG Report: Sperry

Thanks to the DOJ Inspector General report on FBI surveillance abuses, we now know that the agency didn’t just lie about former Trump campaign aide Carter Page – they fabricated evidence to obtain a surveillance warrant, excluding the fact that he had worked with the CIA.

But wait, there’s more!

Thanks to a deep dive into the IG report, the Mueller report, and interviews with Trump campaign officials, RealClearInvestigations‘Paul Sperry has found another fraud on the American public perpetrated by James Comey’s FBI: The agency, as well as Special Counsel Robert Mueller, knew full well that Page wasn’t “an agent of Russia,” and that he had no role in gutting a pro-Russia / anti-Ukraine GOP platform plank at the 2016 convention.

The FBI and Special Counsel Robert Mueller repeatedly kept alive a damning narrative that investigators knew to be false: namely, that a junior Trump campaign aide as a favor to the Kremlin had “gutted” an anti-Russia and pro-Ukraine plank in the Republican Party platform at the GOP’s 2016 convention.

Federal authorities used this claim to help secure spy warrants on the aide in question, Carter Page, suggesting to the court that he was “an agent of Russia” – even though investigators knew that Page was working for U.S., not Russian, intelligence, and that they had learned from witnesses, emails and other evidence that Page had no role in drafting the Ukraine platform plank.

The revelation is buried in the Justice Department watchdog’s just-released report on FISA surveillance abuses. RealClearInvestigations fleshed out this unreported story with footnotes from the Mueller report and exclusive interviews with Trump campaign officials who worked on the convention platform.

Of all the Trump-Russia rumors, insinuations and falsehoods – from secret payments for shadowy hackers, to videotaped prostitutes with active bladders, to a clandestine rendezvous with Kremlin figures in Prague – the supposedly pro-Russia Ukraine platform alteration stands out. It seemed to offer early, public, concrete evidence of an actual bending of prospective U.S. policy to suit Moscow. The false narrative is also significant because it was initially pushed not by Democrats, but by associates of Republican Sen. John McCain and other so-called Never Trumpers. As a bipartisan red flag, it helped build momentum around a narrative of Trump treachery with, then as now, Ukraine playing a central role. It also shows how the Russia and Ukraine controversies were linked from the beginning by Trump’s foes.

This episode loomed so large that the first person Mueller’s team interviewed after taking over the Russia investigation in May 2017 was Rachel Hoff, who was serving as McCain’s policy adviser on the Senate Armed Services Committee. Like her boss, Hoff was no fan of President Trump. Agents sought to confirm with her reports that the Trump campaign had “gutted” the GOP’s platform plank on Ukraine to favor Russia during the party’s convention in Cleveland in early July 2016.

As a disgruntled convention delegate, Hoff got the story started by putting Washington Post columnist Josh Rogin in touch with another Never Trump delegate, Diana Denman, who had lost her bid to amend the GOP plank to call for providing “lethal” weapons to Ukraine to help fend off Russian incursions, according to people with direct knowledge of the matter. Instead, the platform called for “appropriate assistance to the armed forces of Ukraine.”

Denman was overruled because heavily arming Ukraine was out of step with the GOP consensus at the time – to say nothing of the Obama administration’s policy, which refused to arm the Ukrainians. And it was at odds with Trump’s stated position, which sought to avoid military escalation in the region, while encouraging the European Union to take a larger peacekeeping role.

On July 18, 2016, the Post ran Rogin’s sensational story under the misleading headline,“Trump Campaign Guts GOP’s Anti-Russia Stance on Ukraine.” Pushing the narrative that Trump was doing the Kremlin’s bidding, it quoted Hoff warning that Trump “would be dangerous for America and the world.” The story left out the key part of the final Trump-approved plank pledging aid “to the armed forces of Ukraine.” Reached by phone, Rogin declined comment.

This story was quickly amplified in the Steele dossier, the series of now-debunked opposition research memos alleging Trump-Russia collusion. Compiled by ex-British intelligence officer Christopher Steele for the Clinton campaign, those memos became a foundation for the FBI and Mueller probes even though – as this week’s IG report established – bureau agents knew that the material in them included demonstrably false assertions and exaggerated gossip dismissed as nonsense by Steele’s own purported source.

Steele also embellished the GOP convention story by claiming that Carter Page had played a key role in drafting the Ukraine plank as part of a commitment he had allegedly made to his Kremlin handlers “to sideline Russian intervention in Ukraine as a campaign issue.”

None of this was true. And the FBI — and Mueller — knew it, the Justice inspector general reveals in his report.

Still, the FBI presented the Steele dossier’s smear, cataloged as “Steele Report 95,” as key evidence in all four of its warrant applications to obtain wiretaps to eavesdrop on Page, according to the IG report.

To keep renewing the spy warrants, the FBI had to produce fresh evidence for FISA judges to support suspicions Page was “an agent of Russia.” Just a few weeks before the FISA warrant was set to expire in June 2017, Mueller had his investigators interview Hoff, as his first witness, followed by Denman, hoping they could provide fresh details to keep building an espionage case against Page and the Trump campaign.

But Mueller struck out.

According to agents’ notes documenting their June 2017 interview, as revealed in the IG report, Denham told the FBI that Page was not involved in the drafting of the Ukraine plank. But Mueller’s team did not update its fourth and final FISA warrant application on Page with this exculpatory information. Instead, it recited the same baseless claim that he had shaped the Ukraine policy with guidance from Russia. And the court renewed the warrant that June to electronically monitor Page, allowing the government to continue vacuuming up all of his emails, phone calls, text messages and other communications for another 90 days.

“Although the FBI did not develop any information that Carter Page was involved in the Republican Platform Committee’s change, the FBI did not alter its assessment of Page’s involvement in the FISA applications,” Justice Department Inspector General Michael Horowitz noted in his 476-page report released Monday.

Added Horowitz: “We found that, other than this information from Report 95 [of the Steele dossier], the FBI’s investigation did not reveal any information to demonstrate that Page had any involvement with the Republican Platform Committee.” Yet, “all four FISA applications relied upon information in the Steele reporting” alleging Page’s role in drafting the Republican plank on Ukraine and Russia.

A former U.S. Navy lieutenant, Page was never charged with espionage or any crime. He told RealClearInvestigations that he has received “numerous death threats that directly resulted from the false allegations” that he was a traitor.

The FBI and Mueller failed to correct the record about Page in their FISA warrant applications even after they identified the Trump campaign officials who actually had a hand in influencing the GOP plank, J.D. Gordon and Matt Miller. A July 14, 2016, email from Gordon confirmed what Page had personally told the FBI in an interview — that he had not taken part in the decision. The FBI knew about the email since at least March 2017, when agents sat down with Page. (Gordon and Page were chatting by email about the convention, and it’s clear from Page’s responses he had no idea what Gordon had done in the Ukraine-Russia platform drafting sessions. IG Horowitz published the relevant excerpt in his report and noted the FBI had the email in its possession.)

Still, Horowitz found, “The FBI never altered the assessment.”

Horowitz further concluded that the FBI should not have included the dossier’s rumor even in its original October 2016 application for a FISA warrant targeting Page, let alone its three renewals, because a confidential source the FBI assigned to spy on Page at the time found no basis for it. In the IG report, Horowitz noted that during that same month of October 2016, the FBI informant met with Page and tape-recorded him denying he was involved in the drafting of the Ukraine plank. Page told the informant, Stefan Halper, that he “stayed clear of that.”

Horowitz’s investigators established that the informant’s recorded statements were sent to the FBI agent assigned at the time to Page’s case, and were copied to a supporting team of other agents, supervisors and analysts. Yet the FBI also withheld that critical exculpatory evidence from the FISA court in the initial application for a warrant on Page (and then continued to deny the court the information in subsequent requests to monitor Page).

The lead case agent, unnamed in the report, told investigators the FBI was operating on a “belief” that Page was involved in the Ukraine and Russia platform, and that he and the FISA team were “hoping to find evidence of that” from the wiretaps. Despite all the snooping on Page, the FBI never collected the hoped-for proof.

The lead supervisor, also unidentified, told investigators “he did not recall why Page’s denial was not included.”

Horowitz reports that the exculpatory documents were also sent to a Justice Department attorney before the warrant was renewed for the first time in January 2017, “[y]et, the information remained unchanged in the renewal applications.”

Added Horowitz: “The attorney told us that he did not recall the circumstances surrounding this, but he acknowledged that he should have updated the descriptions in the renewal applications to include Page’s denials.”

The FBI also failed to inform surveillance court judges that Page was an “operational contact” for the CIA for several years, according to the Horowitz report. In 2013, Page also volunteered as a cooperating witness in an FBI espionage case, and helped put away a real Russian agent in 2016. This was additional exculpatory evidence the FBI kept from the FISA court, as RealClearInvestigations first reported last year.

Peter Strzok, then the FBI’s top counterintelligence official, rode herd on the Page wiretap requests and reported back to FBI attorney Lisa Page (no relation to Carter), who in turn, updated then-Deputy FBI Director Andrew McCabe.

Text messages previously uncovered by Horowitz and shared with Mueller revealed that Strzok and Page, who were having an affair, rooted for Hillary Clinton during the 2016 campaign and held Trump in complete contempt. In one exchange, they discussed the need to “stop” Trump from winning the election. And the two of them had also huddled with McCabe in his office to devise an “insurance policy” in the “unlikely event” Trump ended up winning.

The inspector general’s report points out that it was McCabe who urged investigators to look at the Clinton-funded dossier. The previous year, his Democratic politician wife, Jill, received hundreds of thousands of dollars in donations arranged by Clinton ally and Virginia’s governor at the time, Terry McAuliffe.

Strzok remained central to the investigation well into 2017 – until Mueller was forced to kick him off his team when the anti-Trump bias was revealed. The bureau fired him in 2018, the same year Lisa Page resigned from the FBI. In spite of their anti-Trump political bias, Horowitz said he found “no evidence” their bias influenced their investigative decisions.

Lawyers for Strzok and McCabe did not respond to requests for comment. The FBI and a spokesman for Mueller declined comment.

Putting Carter Page under surveillance starting in October 2016 effectively let the FBI spy on the Trump campaign since its beginnings, because it allowed the bureau to scoop up all of Page’s prior communications. Former Trump officials who have reviewed Horowitz’s new findings confirmed their view that the bureau was trying to make it look like Page and the Trump campaign were doing something sinister to help Russia.

“Page actually had no role in the platform, whatsoever,” Gordon, the Trump campaign’s director of national security, told RCI. “Failing to include the exculpatory information in the FISA application is horrifying.”

While it’s true that Trump sought better relations with Russia, Gordon said, there was nothing nefarious about the drafting of the Ukraine platform. He said the FBI simply assumed it was watered down as a favor to Russia based on a false narrative driven by liberal media outlets like the Post and Never Trumpers such as Rachel Hoff. He said the FBI, under the direction of McCabe, Mueller and former FBI Director James Comey, also wanted to believe the worst about Trump, whom they simply did not like.

Gordon noted that, except for the two Never Trump delegates, nobody in the platform drafting sessions raised a fuss about the Ukraine plank — not even the press.

“The media was present in the room, yet not one person wrote about the Ukraine issue,” he said — until, that is, the Never Trumpers went to the Washington Post that July and helped launch the Trump-Russia “collusion” myth.

Moreover, the narrative was untrue even on its own terms – without the spurious inclusion of Carter Page. Internal platform committee documents show the Ukraine plank could not have been weakened as claimed, because the “lethal” weapons language was never part of the GOP platform in the first place. The final language actually strengthened the platform by pledging direct assistance not just to the country of Ukraine, but to its military in its struggle against Russian-backed forces.

Far from “gutting” assistance, the Trump administration approved the transfer of tank-busting Javelin missiles to Kiev — something the Obama administration refused to do. More than 200 of those weapons have been sold to Ukraine since Trump took office. And the sale and delivery of Javelins never stopped even during this year’s temporary suspension of military aid to Ukraine that is now the subject of the Democrats’ impeachment proceedings.

The final draft of the Ukraine plank also branded Russia a menace, and pledged to stand against “any territorial change imposed by force in Ukraine.” Yet Mueller and his prosecuting staff of mostly Democratic donors still suspected collusion, and they dispatched FBI agents to grill Gordon about the drafting of the platform three times between 2017 and 2019. They also got a grand jury to subpoena his phone records.

In the end, the Mueller report found no Russian influence in the platform.

But the false narrative – that the Ukraine plank stood as early proof of the “extensive conspiracy” between the Trump campaign and Moscow that Steele alleged in his now-debunked dossier – has persisted.

Earlier this year, House Judiciary Committee Chairman Jerry Nadler demanded Gordon provide additional documents, and he has complied. Nadler is now marking up articles of impeachment against Trump over a request he lodged with Ukraine’s new president this summer to help investigate the former Clinton-friendly regime’s attempts to “sabotage” Trump’s election bid in 2016. Trump also asked Kiev to look into possible corruption involving former Vice President Joe Biden’s son Hunter and a Ukrainian energy oligarch.

Meanwhile, Nadler’s impeachment partner, House Intelligence Committee Chairman Adam Schiff, continues to insist that the Trump team “softened” the GOP platform to accommodate “Putin’s invasion of Ukraine.”

A retired Navy commander and former Pentagon spokesman, Gordon said he has run up a five-figure legal bill defending against what he calls a “hoax” perpetrated by Never Trumpers, the media, Comey, Mueller, and now congressional Democrats.

“In the vicious frenzy to destroy President Trump and his associates at all costs, they attempted to turn a routine foreign policy debate in conjunction with the four-year renewal of the GOP platform into a crime scene,” Gordon said in an interview with RCI.

“Incredibly,” he added, “the GOP platform change hoax [later] became the very first order of business in Mueller’s nearly two-year investigation.”

How Trump Opened A Pandora’s Box By Announcing The “Phase One” Trade Deal

Trump’s “Phase One” deal left pretty much everyone disappointed: from experts who were expecting a realistic compromise between the two superpowers instead of the ludicrous and completely undoable Beijing promise to quadruple US agricultural purchases to $50 billion (a detailed explanation why this is impossible can be read in the following thread by the former USDA Chief Economist and USTR ag negotiator, Joe Glauber)…

1. So here is why I am skeptical about the size of the Phase 1 deal. US ag exports to China in FY 2017 were about $21.8 billion. Soybean exports accounted for $14.6 billion. pic.twitter.com/5LXRiZtjcU

Not unironically, the only party that appears to be happy with the outcome of the “Phase One” deal in addition to Trump of course, is China: as the Chinese foreign minister Wang Yi said on Saturday, the China-U.S. trade deal “ serves as bullish news for both countries and the rest of the world.”

Here alarms should be going off, because if indeed both Trump and China are happy with the deal outcome, by definition that means that the US is reverting back to the old “non zero-sum” world where US politicians catered to China in the context of a globalized world. In other words, Trump’s effort to keep China’s superpower ascent in check appears to have taken a back seat to the president’s desire to keep markets supporter and avoid the shock of a fresh re-escalation of the trade war.

But is that feasible?

Before, we answer that question, here is a recap of what the Trump admin announced on Friday as part of the “Phase One” trade deal:

List 4B (December 15) tariffs suspended: This was in line with our expectations and media reports in recent days.

List 4a (September 1) tariff ratereduced to 7.5% from 15%: This falls short of expectations influenced in recent days by the media reports, where WSJ suggested broader and deeper tariff reductions were possible.

List 1-3 tariffs remain unchanged: This too fell short of what the broader tariff rollbacks hinted by the media in recent days.

The first complication is that while Trump explicitly agreed to roll back some tariffs, substantial ambiguity on agriculture: While both sides agreed on increased agricultural and other US commodity purchases by China, it’s unclear what level such purchases will reach and how this will be enforceable. Given the US’s focus on this issue, experts remain concerned (and confident) that disappointment on this point as negotiations continue would be a potential catalyst for re-escalation of tariffs.

Yet even assuming no major re-escalation in the context of Phase One, which is in the history books, what happens next?

Well, as Morgan Stanley’s policy strategist Michael Zezas writes, with the easy stuff, i.e., the generally hollow and/or impossible promises that make up the bulk of Phase 1, agreed upon, it is only the difficult stuff that has to be resolved, or as MS puts it, “key execution risks remain as the US/China relationship moves forward.“

Specifically, the end of Phase 1 and commencement of Phase 2 negotiations will materially strain goodwill: recall, “Phase 2” negotiations are, per the US, to commence immediately. And given that ‘Phase 1’ focused on the “easy” topics that were ‘low-hanging fruit’, Zezas warns that “Phase 2 negotiations could be more challenging, problematic, and potentially subject to stalls, as both sides debate the far more difficult issues of industrial policy.”

In other words, Trump may have taken what wasn’t broken, namely the tried and true strategy of ramping the market higher on daily speculation and “trade deal optimism”, i.e., leaks, rumors and innuendo that an easy to achieve Phase 1 deal was imminent, and “fixed it”, in the process replacing the easy Phase 1 outcome with the vastly more complex Phase 2 process, where an agreement between the two superpowers and a successful outcome is next to impossible.

Hence, Morgan Stanley argues the dynamic has shifted from ‘uncertain pause’ to ‘uncertain progress’, with the following key takeaways for investors:

No game-changer for the tariff burden: About $380bn of imports remain under tariff. While phase 1 reportedly includes an agreement in principle to reduce all remaining tariffs over time as progress is made on phase 2, it is unlikely that such progress can be made quickly, if at all, given the relatively intractable nature of industrial policy issues.

No game-changer for corporate confidence: While this deal is certainly more durable than another simple swap of agricultural purchases for a pause in tariffs, the experience of this trade conflict has created a high hurdle for what corporate executives would judge to be confidence-inspiring. And as Morgan Stanley has noted in the past, companies in the US and China have already put plans in motion to protect themselves from changes in the US/China dynamic. It also means that they are unlikely to revert back to baseline as a result of Friday’s (non) deal.

In other words, as Morgan Stanley concludes, “given the execution risks going forward that we cited earlier and the lack of clarity on important details, we don’t yet have the conviction that this deal can be a catalyst to a meaningful uptick in business confidence.”

As for markets, the outcome could be even more dire for one simple reason: over the past year, the interminably recurring catalyst that pushed stocks ever higher, was “optimism” that a deal was imminent. Well the Phase One is “now in the books”, and not even the most gullible traders – or algos – will believe that a Phase 2 deal can be done before the elections, or frankly, ever. As such, the most important crutch behind the market climbing the trade war Wall of Worry for the past year is now gone.

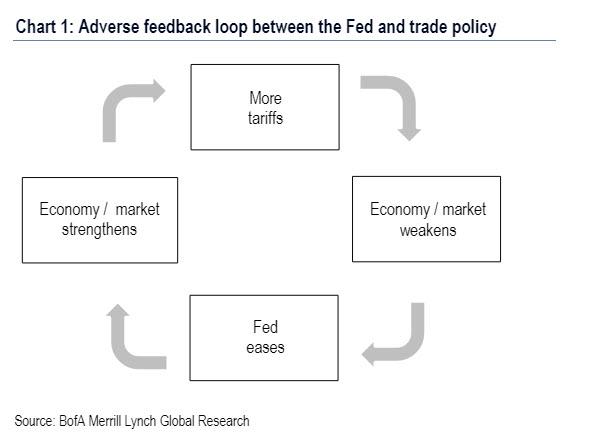

Worse, by removing the risk of trade war, the Fed’s monetary policy will no longer be constrained on the downside by the risk of a potential trade war re-escalation. This is critical because as we explained in August, it was the Fed itself that was underwriting Trump’s trade war.

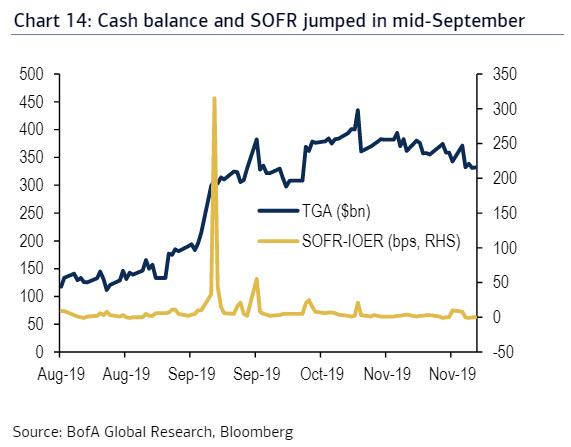

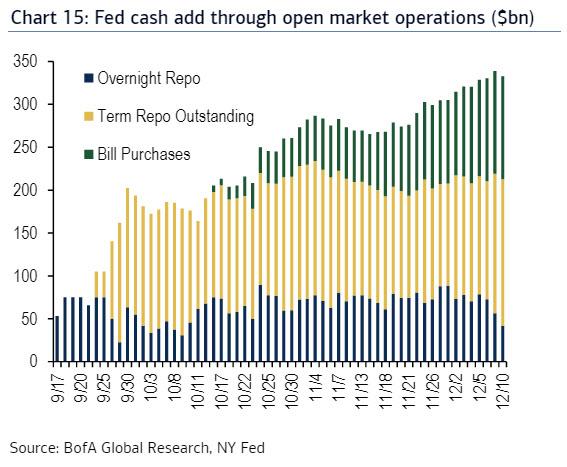

That said, there is a silver lining: the Fed’s “NOT QE” bailout of the repo market remains, and as long as Powell continues to inject hundreds of billions (just to stabilize a handful of banks and push markets higher), the risk of market bloodbath remains remote. However, if and when this process too begins to taper some time in Q2 2020, that may be the time to watch out below. Worst of all for Trump – this will take place just a few months before the November election. What he plans to do to full the void left by both “Trade Deal” optimism and “NOT QE4” remains unclear.

So that we can understand the financial and banking challenges ahead of us, this article provides an historical and technical background. But we must first get an important definition right, and that is the cause of the periodic cycle of boom and bust. The cycle of economic activity is not a trade or business cycle, but a credit cycle. It is caused by fractional reserve banking and by banks loaning money into existence. The effect on business is then observed but is not the underlying cause.

Modern banking has its roots in England’s Bank Charter Act of 1844, which led to the practice of loaning money into existence, commonly described as fractional reserve banking. Fractional reserve banking is defined as making loans and taking in customer deposits in quantities that are multiples of the bank’s own capital. Case law in the wake of the 1844 act, having more regard for the status quo as established precedent than for the fundamentals of property law, ruled that irregular deposits (deposits for safekeeping) were no different from a loan. Judge Lord Cottenham’s ruling in Foley v. Hill (1848) 2 HLC 28 is a judicial decision relating to the fundamental nature of a bank which held in effect that

The money placed in the custody of the banker is to all intents and purposes, the money of the banker, to do with it as he pleases. He is guilty of no breach of trust in employing it. He is not answerable to the principal if he puts it into jeopardy, if he engages in haphazardous speculation.

This was undoubtedly the most important ruling of the last two centuries on money. Today, we know of nothing else other than legally confirmed fractional reserve banking. However, sound or honest banking, with banks acting as custodians, had existed in the centuries before the 1844 act and any corruption of the custody status was regarded as fraudulent.

This decision has shaped global banking to this day. It created a fundamental flaw in the gold-backed sound-money system, whereby the Bank of England, as a prototype central bank, could only issue extra sterling backed entirely by gold while a commercial bank could loan money into existence, the drawdown of which created deposit balances. The creation of these deposits on a systemwide basis meant that any excesses and deficiencies between banks were easily reconciled through interbank lending.

Bankers’ Groupthink and the Credit Cycle

While an individual bank could expand its balance sheet, the implications of all banks doing the same may have escaped the early banking pioneers operating under the 1844 act. Thus, when their balance sheets expanded to a multiple of the bank’s own capital, there was little cause for concern. After all, so long as a bank paid attention to its reputation it would always have access to the informal interbank market. And so long as it could call in its loans at short notice, the duration mismatch between funding by cash deposits and its loan book would be minimized.

Since the Bank Charter Act, experience has shown that the expansion of bank credit leads to a cycle of credit expansion, overexpansion, and then sudden contraction. The scale of bank lending was determined by its management, with lenders tending to be as much influenced by their own crowd psychology as by a holistic view of risk. Of course, the expansion of bank credit inflates economic activity, spreading a warm feeling of improving economic prospects and feeding back into increasing the bankers’ confidence even further. It then appears safe and reasonable to take on yet more lending business without increasing the bank’s capital.

With profits rapidly increasing due to lending being a multiple of the bank’s own capital, confident bankers begin to think strategically. They reduce their lending margins to attract business they believe to be important to their bank’s long-term future, knowing they can expand credit further against a background of improving economic conditions to compensate for lower margins. They begin to protect margins by borrowing short from depositors and offering businesses term loans, reaping the benefits of a rising slope in the yield curve.

The availability of cheap finance encourages businesses to enhance their profits in turn by increasing the ratio of debt to equity and by funding expansion through debt. By this point, a bank is likely to be raking in net interest on loan business amounting to eight or ten times its own capital. This means that an interest margin of a net two percent is a 20 percent return to the bank’s shareholders.

There is nothing like profitable success to boost confidence, and the line between it and overconfidence is naturally fuzzed by hubris. The crowd psychology fueled by a successful banking business leads to an availability of credit too great for decent borrowers to avail themselves of, so inevitably credit expansion becomes a financing opportunity for poorly thought out loan propositions.