Blocking SWIFT Access Would Be “Declaration Of War”: Russia Warns Against US ‘Nuclear Option’

Last year during the height of controversy over the Kerch Strait incident, while two dozen Ukrainian sailors were still being held by Russia, Washington’s special envoy to Ukraine at the time, Kurt Volker, floated the possibility of Washington blocking Russian banks from SWIFT. He told Voice of Americaat the time that it was considered “a nuclear option” and it would have huge costs which would even inadvertently impact US allies.

“People refer to it as a nuclear option. It would have costs for everybody involved,” he said. “Big costs for Russia, but big costs for allies as well. Ultimately, we have to keep it on the table as a possibility because we just can’t continue to see Russia launch further steps of aggression in its neighborhood like this.”

No doubt it’s still in Washington’s playbook as a ‘nuclear option’ long after the Kerch Strait incident was diffused with an historic prisoner swap, and the Kremlin has taken note.

Russia’s Central Bank, via Wiki Commons.

On Thursday Prime Minister Dmitry Medvedev took Washington to task over the prior warning, telling reporters that Moscow is well aware of discussions to take sanctions further, even cutting off the country’s access to some 11,000 banks and financial institutions in over 200 countries by blocking SWIFT. This is exactly what the Trump White House did vis-à-vis Iran months after it pulled out of the 2015 JCPOA.

Medvedev said such far-reaching action would be tantamount to a declaration of war. According to statements reported in Russian media:

Speaking to reporters on Thursday, Medvedev recalled the West once seriously considered the option, and Moscow is aware of it.

“This would in fact be a declaration of war, but nevertheless it was discussed,” the Russian prime minister said, adding that this is one of the reasons why the government is looking into ways to protect the Russian part of the internet.

Though unlikely barring further major escalation between the US and Russia, the possibility is so much on the Kremlin’s radar because it was also threatened in 2015 at the height of tensions over the war in eastern Ukraine.

At that time, citing threatened financial sanctions “from the West” — specifically impacting access to the prime global interbank system, Medvedev let it be known that Russia’s response would be “without limits”.

“We’ll watch developments and if such decisions are made, I want to note that our economic reaction and generally any other reaction will be without limits,” he said in those prior comments. Indeed the unforeseen consequences of such a major global power (and energy provider to much of Europe and now even China) being suddenly isolated to that extent along with its fierce reaction, would likely create a global financial Armageddon and uncontrollable ripple effect.

Meanwhile Russia has over the past months flirted with the possibility of joining INSTEX — the special purpose vehicle set up by Europe to facilitate trade with Iran — and has thrown its political weight behind the project as it gains momentum with more EU countries joining in the past days.

A report issued on Dec. 4 by the Financial Stability Oversight Council (FSOC) highlighted potential problems resulting from stablecoins gaining wider recognition.

The FSOC was set up in 2008 to combat risks to the financial sector after the financial crisis. The panel is headed by United States Secretary of the Treasury Steven Mnuchin. Its voting members include Jay Clayton, the chairman of the Securities and Exchange Commission (SEC), as well as Heath Tarbert, who recently took over as chairman of the Commodity Futures Trading Commission (CFTC).

FSOC: stablecoins “could affect wider economy”

In its annual report for 2019, the regulators stated:

“If a stablecoin became widely adopted as a means of payment or store of value, disruptions to the stablecoin system could affect the wider economy. Financial regulators should review existing and planned digital asset arrangements and their risks, as appropriate.”

The FSOC additionally mentioned Bitcoin (BTC) and other cryptocurrencies as part of its coverage. It appeared unable to draw concrete conclusions about the phenomenon, acknowledging that trading data was “sparse and may be unreliable.”

The panel also expressed doubts over so-called distributed ledger technology (DLT) — a byword for digital currency projects notionally related to blockchain.

“The ultimate success of the technology, including applications in the financial sector, is not yet certain,” the report stated. The FSOC continued:

“Some early efforts have not resulted in the anticipated efficiency gains and other promised benefits, and as a result, have been scaled back, refocused, or abandoned.”

Cryptocurrency suspicions continue

As Cointelegraph reported, Mnuchin has been vocal as a critic of Bitcoin, alluding that the seminal cryptocurrency is likely a passing fad. In a July interview he said:

“I won’t be talking about Bitcoin in 10 years, I can assure you that […] I would bet even in 5 or 6 years I’m no longer talking about Bitcoin as Treasury Secretary. I’ll have other priorities […] I can assure you I will personally not be loaded up on Bitcoin.”

U.S. lawmakers continue to focus on the perceived risks stemming from the cryptocurrency sector, including associated schemes such as Facebook’s unlaunched Libra digital currency.

Pelosi Snaps At Being Accused Of Hating “Cruel, Coward, Rogue” President Trump

Update (1150ET): It did not take long for President Trump to respond to Pelosi’s outburst…

Nancy Pelosi just had a nervous fit. She hates that we will soon have 182 great new judges and sooo much more. Stock Market and employment records. She says she “prays for the President.” I don’t believe her, not even close. Help the homeless in your district Nancy. USMCA?

As we detailed earlier, having accused President Trump of “abuse of power” and calling for the House to draft articles of impeachment for “using the office of the President for personal gain,” pointing out that The Founders “could not have foreseen such a rogue president;” and then calling the president a “coward” for not helping kids on gun violence, blasting him as “cruel” for not helping DREAMers, and slamming him for being “in denial” over climate change; a reporter at Speaker Pelosi’s weekly press conference dared to ask if she “hated” President Trump.

Pelosi snapped…

“I don’t hate anybody. I was raised in a Catholic house, we don’t hate anybody – not anybody in the world. So don’t you accuse me of any [hate],” Pelosi said during her weekly press briefing in the Capitol.

“As a Catholic I resent you using the word ‘hate,'” she continued.

“Don’t mess with me when it comes to words like that.”

Watch the full clip here as The Speaker lost it…

Q: “Do you hate the president?”@SpeakerPelosi: “I don’t hate anybody…As a Catholic, I resent your using the word hate in a sentence that addresses me. I don’t hate anyone…So, don’t mess with me when it comes to words like that.”

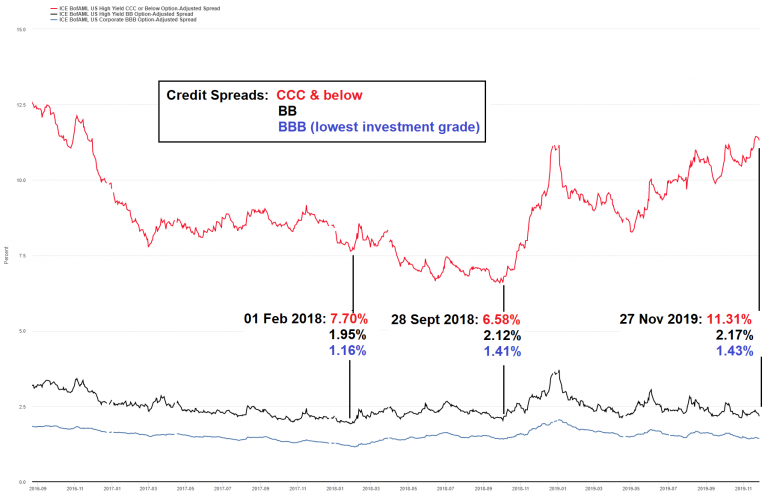

By all accounts, credit markets remain on fire. 2019 is already a record year for corporate bond issuance, beating the previous record set in 2017 by a sizable margin. Demand for the debt of governments and government-related issuers remains extremely strong as well, despite non-existent and often even negative issuance yields. Even now, with economic activity clearly slowing and numerous threats to the post-GFC recovery looming on the horizon, the occasional rise in credit spreads is routinely reversed. And yet, under the placid surface problems are beginning to percolate. Consider exhibit A:

The chart shows option-adjusted credit spreads on three rating categories – while spreads on ‘BB’ rated (best junk bond grade) and ‘BBB’ rated (weakest investment grade) bonds remain close to their lows, spreads on ‘CCC’ rated bonds continue to break higher – considerably so. An increase by 473 basis points from their late 2018 low indicates there is quite a bit of concern.

It is actually rare for credit spreads on these rating classes to drift apart to such a significant extent at a time when spreads on better-rated bonds are still close to their lows. Normally the exact opposite happens – when spreads are tightening, they also tend to tighten between the different rating classes – only when spreads are widening across the board will spreads on lower rated bonds display a tendency to widen to more rapidly than those on better-rated ones.

This bifurcation is actually a subtle warning indicating that the credit cycle may finally be coming to its end. It is “subtle” in the sense that it is generally not yet perceived as a sign that trouble is brewing – rather, it is dismissed as a sign that bond buyers have become slightly more selective (a good thing). In view of a record year for corporate bond issuance it is probably not surprising that concern remains muted.

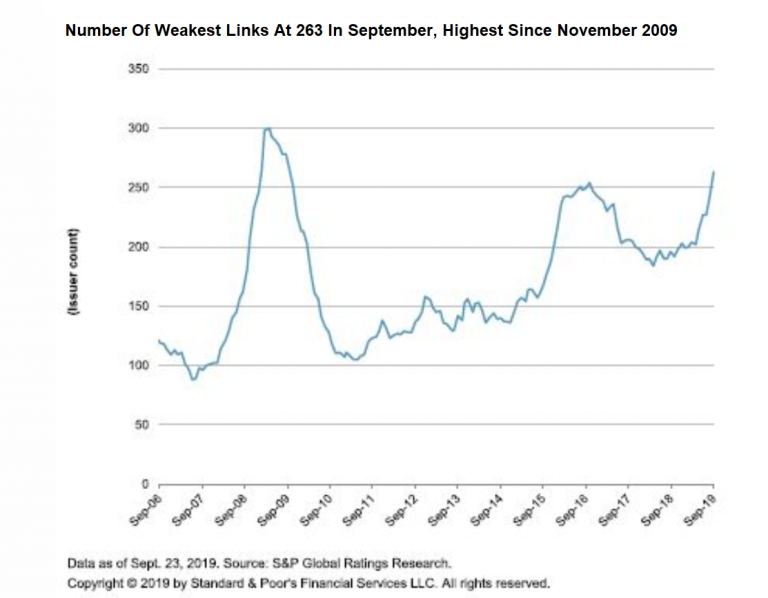

To be sure, high yield defaults remain very low – and while they are forecast to increase, a major surge in defaults is currently not expected. However, these superficially placid conditions are masking growing turmoil – as so often, the devil is in the details. Consider the following data point released by S&P in mid October:

According to S&P the number of “weakest links” is at a level last seen in November of 2009, when the speculative-grade default rate stood at 10.5%. This is an astonishing datum, to say the least.

Weakest links are defined as issuers rated ‘B–’ or lower by S&P Global Ratings with negative outlooks or ratings on credit watch with negative implications. As S&P helpfully explains:

“The default rate of weakest links is nearly eight times greater than that of the broader speculative-grade segment, and the rise in the weakest links tally may signify higher default rates ahead.”

Readers may be surprised to learn that contrary to 2015-2016, oil and gas companies are not leading the pack – consumer products companies are (52 issuers or ~20%). Energy companies are in second place, representing around 10% of the total, followed closely by media companies and restaurant chains.

All of these sectors are held to be under pressure due to industry-specific problems, but that doesn’t change the fact that a great many companies have obviously over-leveraged their balance sheets. The growth in “weakest links” in the strongest developed economy is testament to the proliferation of zombies central bank policies have created in recent years.

S&P nevertheless expects the US junk bond default rate to reach a mere 3.4% over the coming year, which is actually still a fairly benign number. Presumably this is not factoring in the possibility of a recession. It seems to us there is a substantial risk that this forecast will be subject to upward revisions as time goes on.

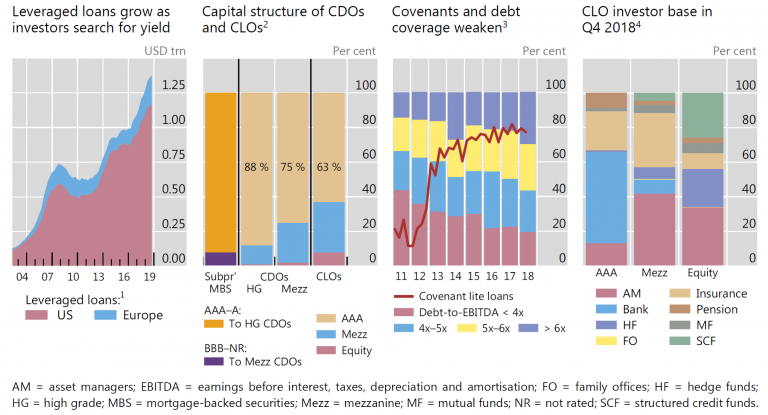

Leveraged Loans, Private Equity and Banks

In recent years enormous amounts have poured into private equity and venture capital funds. Not surprisingly, the rising popularity of unlisted alternative investments (read: illiquid investments) has made it more difficult for them to deliver the large returns that initially attracted investors. Leveraged loans play an important role in private equity buyouts – but recently the situation in leveraged loan land has deteriorated noticeably. Here is a brief summary from Almost Daily Grant’s, a publication of Grant’s Interest Rate Observer:

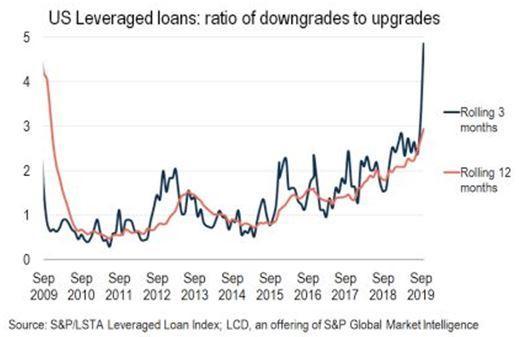

“Signs of trouble abound. According to S&P’s LCD unit, 282 issuers within the S&P/LSTA Index suffered a rating downgrade in the year-to-date through Oct. 11, up from 244 for all of last year and just 33 in 2017. That has pushed the proportion of leveraged loans rated triple-C (“In the event of adverse business, financial, or economic conditions, the obligor is not likely to have the capacity to meet its financial commitments on the obligation.”) to 7.5% of loans outstanding at the end of September, according to S&P. That’s the highest level since 2013 and up from 6.3% in June. Needless to say, the increasing prominence of private equity in tandem with a cyclical credit deterioration presents a delicate backdrop.”

The ratio of loan downgrades to upgrades has soared

The growth in private equity (PE) AUM has increased buyouts of listed companies and pushed up the prices at which they are done (the result of too much money chasing deals), but now the strategy is running into a problem: monetizing these investments has become increasingly difficult. Fewer and fewer deals are making it to the IPO stage, which is – apart from saddling the targets with debt so they can make large dividend payments – the main goal of PE investments.

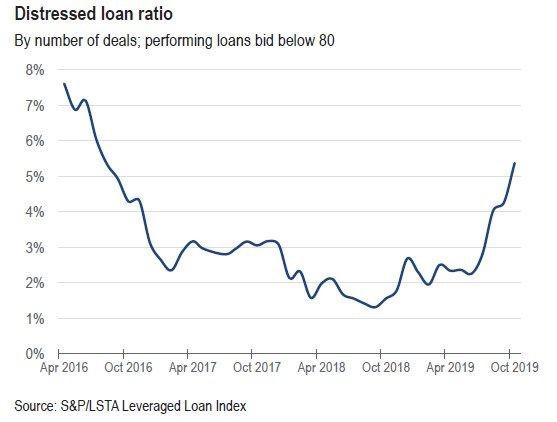

The percentage of distressed leveraged loans is on a strong upswing as well – note that the high levels in 2016 coincided with a raft of bankruptcies in the energy sector in the wake of the 2014-2016 oil price collapse.

As noted above, leveraged loans have become a favored form of debt in PE buyouts, and lately a number of deals either did not get done at all, or only after major concessions were made. This makes it more difficult to bear the debt and lowers the prospective returns of PE investments. Grant’s again:

“Higher price tags figure prominently in the downshift in return expectations. S&P’s LCD unit reports that the average U.S. leveraged buyout carried a purchase price equivalent to 12.9 times Ebitda in the third quarter to bring the year-to-date average to 11.5 times. That’s up from 10.6 times Ebitda last year and 9.7 times in 2007. But, the actual valuation expansion might be far higher, as a Sept. 19 report from S&P Global found that so-called add-backs (i.e. applying hypothetical future cost-savings today) represented 49% of reported Ebitda at deal inception.

Those increasingly fancy valuations (along with abundant use of thefinancials-flattering add-backs) coincide with rising debt burdens. A Nov. 21 research note from Morgan Stanley found that 57% of companies which have undergone an LBO carry net leverage above six times Ebitda. That’s up from 51% in 2007. With rising encumbrance comes an increased risk of impairment, as a survey of p.e. lenders from research firm Credit Benchmark suggests a 6% default probability for leveraged loans issued by private equity-owned firms, up from 5.44% a year ago and well above the 2.36% default likelihood of leveraged loans from their publicly-traded counterparts.

Meanwhile, the blistering rally in asset prices this year has provided little support for the ranks of leveraged loan issuers, with cash flow coverage falling to 3.1 times interest expense in the third quarter according to LCD, down from 3.6 times at year-end 2018 and the weakest coverage since at least the third quarter of 2016.”

There may be a period of regret on the way for investors in private equity. However, the risks posed by leveraged loans are more broadly distributed. In fact, they are systemic.

Leveraged loan data from the BIS, published mid-year – leveraged loans are packaged in CLOs, which attract a broad range of investors due to the yield pick-up they offer. The more capital has rushed into this segment over the years, the more debt covenants and debt coverage have deteriorated.

Leveraged loans are not only important for the PE business, they are also sold to various institutional investors packaged as CLOs (collateralized debt obligations). The banks that create these CLOs in turn are themselves major holders of leveraged loans and CLO tranches. Typically banks will hold the senior tranches, which are the least risky – but we would point out that many “AAA” rated senior tranches of CDOs and CMOs ultimately failed to protect investors when the housing bubble faltered in 2007-2008.

After all, the high ratings of the senior tranches of CLOs and similar structured products are not based on the ratings of the underlying loans, but on overcollateralization and the seniority feature. In 2007-2008 neither of them was sufficient. As a financial stability report published by the BoE informs us:

“Banks originate leveraged loans, a large share of which they distribute to non-bank investors including to collateralised loan obligations (CLOs) for securitisation. In total, banks retain exposures to over half of the leveraged loan market through loans that they have originated but not yet distributed (‘pipeline exposures’), loans they choose to retainon their balance sheets and CLO holdings.

The share of new leveraged loan issuance with no maintenance covenants has more than tripled since 2007, and remains close to record highs globally at almost 60% in 2019.Other traditional investor protections in loan terms have also been relaxed (such as restrictions on borrowers’ ability to transfer collateral beyond the reach of the lender), potentially increasing losses to lenders in the event of default. Borrowers are also increasingly indebted globally, with the average reported debt to EBITDA ratio of the borrowers issuing new leveraged loans around levels observed in 2007. There has been growing use of adjustments (‘add-backs’) to how earnings are calculated at the point a loan is made, which could further understate leverage. Add-backs and subsequent borrowing are typically not captured in public measures of leverage and if included leverage is likely to be above 2007 levels. For example, PRA supervisory data indicate that the share of new lending with leverage above seven times would increase from 18% to 28% if these were included.

Banks’ loan book exposures are mainly through revolving credit facilities (effectively overdrafts) and, to a lesser extent, holdings of term loans. Together they account for around 47% of the total leveraged loan market. Banks’ exposures through holdings of typically senior tranches of CLOs account for around 9% of the total leveraged loan market.

Many banks also have indirect exposures via facilities to credit and private equity funds which invest in leveraged businesses. Some banks also offer warehousing facilities, which are loans to CLO managers to finance the setting up of their CLOs.

Total direct and indirect exposures for some international banks active in this market are significant. For a sample of global systemically important banks (G-SIBs) active in this market, their exposure is on average around 75% of common equity Tier 1 (CET1) capital. Banks could face the risk of credit and mark-to-market losses on these exposures.”

(emphasis added)

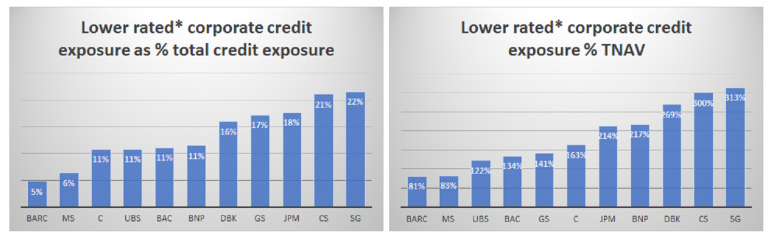

Exposure of 75% of CET-1 capital is not exactly chickenfeed. Any significant deterioration in leveraged loans will force banks to get rid of some of their exposure in order to remain in compliance with the strict post-GFC Basel III capital adequacy requirements. This would put greater pressure on prices, forcing even more deleveraging.

Leveraged loan exposure of several systemically important banks – as a percentage of their total credit exposure as well as of their tangible net asset value

Below are a few more charts illustrating the growing risks in leveraged loans. The first one depicts the recent deterioration in leveraged loan prices in a more granular manner. It also includes the effect of the slump in the oil patch from 2014 to 2016 in full:

Percentage of leveraged loans priced below 90 and below 80. The recent rise is reminiscent of the beginning of the 2014-2016 mini-crisis

The next chart is from the BoE and shows that the proportion of corporate borrowers with a net debt/EBITDA ratio in excess of 4 has increased to levels last seen in 2007. Keep in mind that this does not reflect the above mentioned “add-back” effects, which lead to lower ratios being reported on the basis of estimated or planned future improvements (i.e., imaginary figures). The BoE report this chart was taken from was published in mid-year so it is reasonable to assume that the situation has worsened further since then.

Net debt/EBITDA essentially indicates how many years it would take to pay back a company’s debt based on its current debt levels and income. Note that the chart includes only listed non-financial companies and does not include real estate, energy and mining companies. If the latter were included, the figures would look worse.

The next chart shows the distribution of leveraged loans by rating classes and how many loans have found their way into CLOs. The largest share is taken up by loans rated ‘B’.

Leveraged loans by rating classes and how many are packaged in CLOs

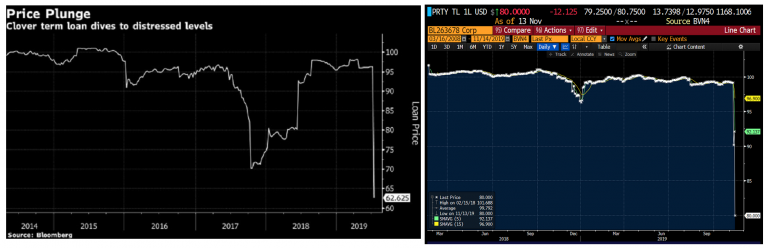

And lastly, we have noticed that despite the fact that leveraged loan investors are generally considered to be quite sophisticated, such loans are in practice often re-priced quite suddenly – which is to say, investors were surprised by adverse developments befalling the borrowers. Two such re-pricing events are shown below, one of a Clover term loan and a more recent one of a Party City term loan due in 2022 that was only issued last year (Party City conducted aggressive share repurchases and was reportedly also quite adept at the EBITDA add-back game).

Leveraged loans falling prey to sudden re-pricing

Conclusion

To sum up, there are growing signs of distress in certain forms of high-yield debt. As long as default rates remain low, this is not perceived as a big problem, not least in view of the fact that the market recovered quite smartly from the 2014-2016 downturn. However, as we previously reported, a veritable wall of maturities is looming in high-yield debt in the years 2020-2024.

This means that many of the so-called “zombie” companies that can only survive by constantly refinancing their debt will depend on investors continuing to “chase yield” with abandon. The strong demand for new debt issuance seen this year will have to continue or become even stronger. Central banks across the world are once again pursuing looser monetary policy, which supports this process. Despite this, global liquidity conditions actually remain relatively tight so far, which implies that economic activity is likely to slow further. The probability that the party may be ending is clearly rising.

* * *

Addendum: CDOs in 2007 vs. CLOs in 2018

A table from the BIS that compares several features of CDOs in 2007 to CLOs in 2018:

This is probably not going to make anyone feel better about the risks posed by CLOs.

World’s Largest Commodity Trader Plummets To Three Year Low On Bribery Probe

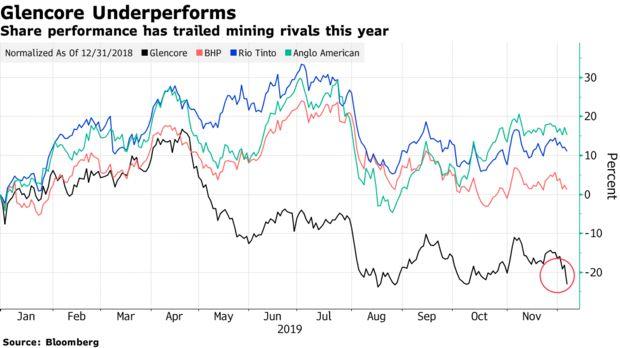

Glencore Plc, the world’s largest commodity trader, tumbled almost 9% to a three year low and was briefly halted following news that it was being investigated for bribery by U.K. authorities, deepening the company’s long-running legal troubles.

The announcement by the UK’s Serious Fraud Office adds to separate corruption probes that Glencore is facing in the U.S. and Brazil, which have sent the company’s stock sliding in recent years. Without providing much detail, the SFO said it’s looking into suspicions of bribery by the company, its employees, agents and associated persons.

Glencore said it will cooperate with the probe, but didn’t provide any further details.

“This is an obvious negative for the Glencore investment case,” RBC analyst Tyler Broda wrote in a research note. “We believe this clearly will hamper sentiment in what remains a complex investment case for investors.” He also said that the language of the U.K.’s investigation, albeit with limited detail, suggests it could be wider in scope. That potentially raises the penalty, if Glencore is found guilty or reaches a settlement.

As Bloomberg adds, The new probe also ramps up pressure on Glencore’s billionaire Chief Executive Officer Ivan Glasenberg. He told investors earlier this week to prepare for more leadership changes and hinted that his own departure may come sooner than previously anticipated.

The investigation will be also be a major test for the U.K. prosecutor, which has stumbled with some cases. Three Tesco Plc officials caught up in an accounting scandal were cleared after a pair of trials and the agency has dropped some high-profile probes into individuals at companies including Rolls-Royce Plc and GlaxoSmithKline Plc.

For trading powerhouse Glencore, which in recent years has emerged as the commodity equivalent of Deutsche Bank which appears to have involvement in virtually every single financial crime committed over the past two decades, the investigations have raised fundamental questions about how the business of commodities trading is conducted around the world, according to Bloomberg, as its traders have traditionally been willing to do business in many of the world’s most impoverished and corrupt countries. And they have long relied on agents – even more corrupt intermediaries who work on commission – to help them secure deals.

Last year, Bloomberg reported that the agency was preparing to open an investigation into Glencore and its work with Israeli billionaire Dan Gertler and former Democratic Republic of Congo President Joseph Kabila. Gertler and Kabila have been implicated in previous British and American bribery investigations. The U.S. imposed sanctions on Gertler in 2017, saying he’d used his friendship with Kabila to corruptly build his fortune.

Gertler and Glencore first invested together in a Congolese mine in 2007 and developed a close partnership over the years in the Mutanda and Katanga Mining copper and cobalt operations. While Glencore has cut its business relations with Gertler, it still must pay him royalties for the mines.

Glencore is also being investigated by the U.S. DOJ and Brazilian authorities in the Car Wash scandal. The company has also been subpoenaed by the Justice Department for documents relating to possible corruption and money laundering in Nigeria, the Democratic Republic of Congo and Venezuela. The U.S. Commodity Futures Trading Commission is also investigating the company for possible corrupt practices.

In response to the DoJ investigation, which the company said it’s cooperating with, Glencore set up a board committee to respond to a U.S. probe, that included chairman and former BP Plc Chief Executive Officer Tony Hayward.

“It’s more of the same, but now it’s getting attacked from a different angle,” said Hunter Hillcoat, a London-based analyst at Investec Securities Ltd. “Glencore was already trading at a discount because of the DoJ, but when this news comes out it gets whacked again.”

Glencore has lost over 20% of its value in 2019, dramatically underperforming the trading giants in its peer group, BHP, Rio Tinto and Angelo American.

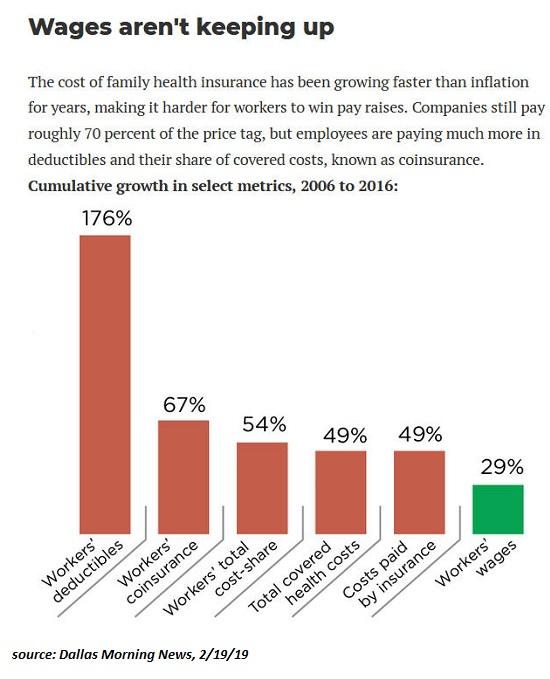

And how do we pay for these spiraling out of control costs? By borrowing more, of course.

If we had to choose one “big picture” reason why the vast majority of households are losing ground, it would be: the costs of essentials are spiraling out of control. I’ve often covered the dynamics of stagnating income for the bottom 90%, and real-world inflation, i.e. a decline in purchasing power.

But neither of these dynamics fully describes the relentless upward spiral of the cost basis of our economy, that is, the cost of big-ticket essentials: housing, education and healthcare.

The costs of education are spiraling out of control, stripping households of income as an entire generation is transformed into debt-serfs by student loan debt. The soaring costs of healthcare are a core driver of higher costs in the education complex (and government in general), and to cover these higher costs, counties raise property taxes, which add additional cost burdens to households and enterprises as rents rise.

Rising rents push the cost structure of almost every enterprise and agency higher.

Then there’s the asset inflation created by central bank ZIRP (zero interest rate policy) which has inflated a second echo-bubble in housing that has pushed home ownership out of reach of many, adding demand for rental housing that has pushed rents into the stratosphere in Left and Right Coast cities.

The increasing dominance of monopolies and cartels has eliminated competition in sector after sector. Monopolies and cartels skim immense profits even as the value, quality and quantity of their products and services decline: The U.S. Only Pretends to Have Free MarketsFrom plane tickets to cellphone bills, monopoly power costs American consumers billions of dollars a year.

Thanks to their political influence, monopolies and cartels have legalized looting, raising prices and evading anti-trust regulations because they can pay whatever it takes in our pay-to-play political system.

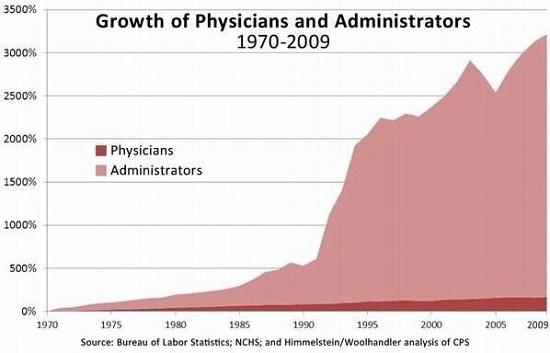

Let’s look at a few charts that illustrate the relentless rise in costs:

Do you reckon these two charts are connected–soaring costs and ballooning administrative payrolls?

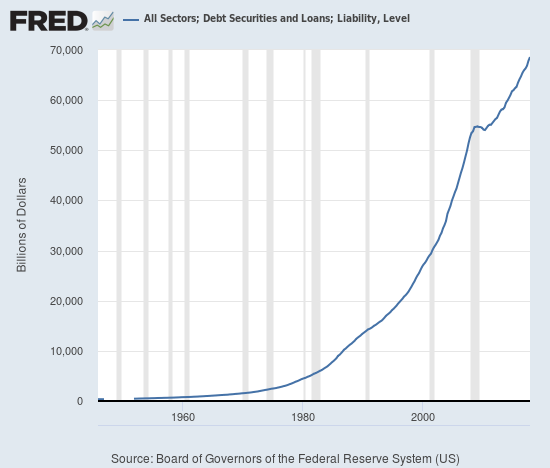

Student loan debt is soaring above $1.5 trillion, guaranteeing profits to lenders and debt-serfdom to the students exiting with degrees that are in over-supply, i.e. possessing little scarcity value in an over-credentialed economy:

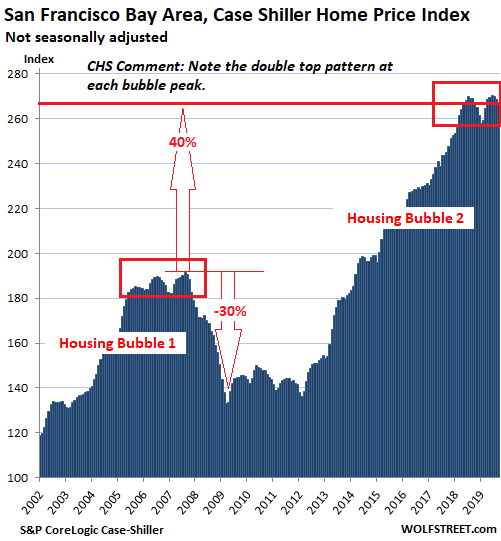

The echo housing bubbles in many locales exceed the nosebleed valuations of the previous bubble:

And how do we pay for these spiraling out of control costs? By borrowing more, of course:

Even at low rates of interest, the cost of servicing skyrocketing debt increases, leaving less net income to support additional borrowing.

What will it take to radically reduce the cost basis of our economy? A fundamental re-ordering that breaks up all the cartels and monopolies that push prices higher even as they deliver lower quality goods and services would be a good start.

France Paralyzed By Largest General Strike In Decades

In what appears to be the biggest disruption to French society since the gilets jaunes demonstrators nearly torched Paris last year, public workers across the country stayed home on Thursday, immobilizing public transit across the country as the first general strike in more than 20 years began.

The walkout was called by unions angry at President Emmanuel Macron’s pension reforms (not unlike how a planned – then scrapped – gas tax hike sparked the giles jaunes).

On the fist day of the strike, parts of Paris resembled a ghost town during what are typically busy morning-commute hours. Roads were empty, and train stations were deserted, according to the Times of London.

The biggest industrial action of Macron’s tenure is, so far, staggering in scale: 50% of French teachers are off work, nine out of ten trains were cancelled and eleven of the fourteen underground lines in Paris are closed. A total of 245 separate demonstrations have been announced across France as students, firefighters, healthcare workers and others joining in. Strikes at Air France forced a wave of flight cancellations, leaving thousands of travelers scrambling for a workaround. Air France cancelled 30% of its domestic flights and 10% of international short- and medium-haul flights on Thursday, RT reports.

Millions of workers are staying home.

In Paris, some resorted to bikes, skateboards or walking in the bitter cold as 90% of the trains in the country were closed.

Workers in Paris take to bikes, scooters and even skateboards to get to the office this mornin. And many more walking on a bitterly cold day. Big police presence at Gare Du Nord for protest later on Thursday. #grevedu5decembrepic.twitter.com/KsikwvchAv

Some joked that the strike had made Paris into a much more ‘eco-friendly’ city. Which is a great way of looking at the situation for thousands of progressives who have also joined in the climate action strikes.

Today #Paris is very quiet and ecological city (less cars and more bikes) due to the huge strike

The strike is expected to continue until Monday as the unions and Macron duke it out over the controversial pension reforms. Paris police are deploying 6,000 riot police to do battle with demonstrators who have decided to take their yellow vests out of the closet and back into action.

Huge police presence at Gare de l’Est in Paris where unions are congregating ahead of the march to Place de la Nation this afternoon. They fear a violent minority of extremists will try to hijack the demo. #grevedu5decembrepic.twitter.com/iIF4nchQ7O

Many of France’s most iconic tourist spots in Paris were forced to shut their doors because of the strikes. The Eiffel Tower and the Orsay museum remained closed on Thursday due to staff shortages, while the Louvre, the Pompidou Center and other museums were mostly closed as well (though some said certain exhibits would still be open).

Many noted that outside the typically packed Gare du Nord train station, there was an eerie silence, with taxi cabs lined up with their green lights on, struggling to find customers in the deserted streets.

The abundance of first-time cyclists created some confusion during the morning commute.

Haven’t seen so many cyclists in Paris since…. well the last Metro strike back in September. Two Parisian cyclists just crash into one another in front of me. “Sorry Im not used to this,” says the elderly man. “Me neither,” said the young woman. “We are all in the same mess” pic.twitter.com/dSR2cJmNHC

Of more immediate concern for Macron, dozens of gilet jaunes protesters are blocking fuel depots in the south and near the city of Orleans, leaving more than 200 petrol stations without fuel on Thursday, while another 400 are rapidly nearing the last of their inventory. These blockades could bring the country to its knees (since society still needs oil and refined petroleum products to function, despite what the Green New Deal supporters want), and might be the deciding factor that forces Macron to scrap his planned austerity ‘reforms’.

In addition to public transit, protesters blocked major thoroughfares in some parts of the country.

À Boulogne, un des rond-points de Capécure partiellement bloqué par un feu. Les manifestants ont commencé dès 3h du matin. Ça circule normalement pour les camions et voitures. #grevedu5decembrepic.twitter.com/UHploMJzn3

Protesters have now been demonstrating against the austerity measures imposed by Macron’s “Liberal” government for more than a year. Even as the EU threatens to reprimand Macron for overspending, his own people are threatening to oust him at the halfway point of his first term, making him the latest in a string of prime ministers who, after being elected with a popular mandate, swiftly lost favor with the people of France.

RT has a live stream in central Paris where police have gathered to prepare for a clash with protesters.

The “Silicon Six” – Facebook, Apple, Amazon, Netflix, Google and Microsoft. Collectively, they had 2018 revenues in excess of $800 billion and currently have a combined market capitalization of more than $4.5 trillion.

The “Silicon Six” have avoided over $100 billion in taxes between 2010 and 2019, according a report from Fair Tax Mark, a British organization that certifies businesses for good tax conduct. They analyzed 10-K filings to compare tax provisions, which is the amount corporations set aside to pay taxes, to cash taxes, which is the amount actually handed over to the government.

The aggregate tax contingencies of the six companies has increased from $8.9 billion at the end of 2010 to $47 billion in 2019. An additional $5.7 billion in interest and penalties has been accrued over the same period.

“The international tide is turning on the acceptability of corporate tax avoidance. The idea of countering the profit-shifting of Big Tech multinationals via the introduction of digital sales taxes has taken root in many countries. Investors need to look afresh at the future impact that this will have on company valuations and income flows,” said Paul Monaghan, Chief Executive of the Fair Tax Mark.

The report singled out Amazon as having the poorest tax conduct. Amazon paid just $3.4 billion in income taxes since 2010, or 12.7% of profits, while the federal tax rate in the U.S. was 35% for seven of the eight years analyzed. “The company is growing its market domination across the globe on the back of revenues that are largely untaxed and can unfairly undercut local businesses that take a more responsible approach,” said the report.

Facebook, which the report ranks as having the second-poorest tax conduct, paid taxes on just 10.2% of profits since 2010, the lowest cash tax paid of the six companies. Facebook also had the lowest foreign current tax charge at just 5% of profits since 2010.

The “Silicon Six” appear to be taking advantage of tax loopholes overseas more than at home. The report finds the majority of the shortfall came from outside the U.S., as the foreign current tax charge was just 8.4% of identified foreign profits since 2010. Fair Tax Mark points out profits continue to be funneled to tax havens such as Bermuda, Ireland, Luxembourg and the Netherlands.

While none of this is entirely surprising, and certainly not limited to the “Silicon Six,” it is just another example of the lengths corporations will go to generate value for shareholders.

US Factory Orders Contract YoY For 3rd Straight Month

Having fallen for the last two months, analysts expected a modest rebound in factory orders in October (despite renewed ISM weakness) and as expected they did rise 0.3% MoM (but from a downward-revised 0.8% MoM drop in September).

On a YoY basis, factory orders dropped 1.2% (better than the 3.7% drop in September but still in the red)…

Source: Bloomberg

This is the 3rd straight month of annual declines (and 5th of the last 6 months).

Factory orders ex-trans rose 0.2% in Oct. after falling 0.3% the prior month.

New orders ex-defense for Oct. unchanged after falling 1.0% in Sept.

The proxy for capital spending – Capital goods non-defense ex aircraft new orders – for Oct. rose 1.1% after falling 0.5% in Sept (but lower than the initial +1.2%)

{kind=link}

{kind=link}