Oil prices are higher since last week’s inventory data, thanks in large part to the chaos occurring in the Strait of Hormuz sparking some war premium back into a slightly squeeze-prone-positioning.

“Oil squeezed higher last week on tensions in the Middle East, but with so much uncertainty regarding the trade war and global economy, the demand argument is too shaky for a sustainable rally just yet,” Tyler Richey, co-editor at Sevens Report Research in Palm Beach Gardens, Florida, wrote in a note to clients.

But for tonight (and tomorrow’s EIA data), all eyes will be back on inventories…

API

Crude -7.55mm (-2.9mm exp) – biggest draw since March

Cushing -1.26mm

Gasoline -3.17mm

Distillates +160k

After last week’s crude draw, expectations are for more of the same this week and API reported a large 7.55mm crude draw – the biggest since March along with a sizable draw in Gasoline…

“It feels like demand is very, very weak,” said Michal Meidan, head China analyst at Energy Aspects. “On the supply side, the consensus really was OPEC rolling over the supply cuts,” so it’s quite surprising that prices haven’t risen further, especially with all the geopolitical stress, she said.

WTI hovered just below $58 ahead of the inventory print , but as API data hit, it spiked to the highs of the day…

via ZeroHedge News http://bit.ly/2KEDmNw Tyler Durden

After slashing guidance on more than one occasion heading into earnings, moments ago the world’s logistics belwether and the company that is arguably most impacted by ongoing trade war, FedEx, reported Q4 results that were generally stronger than consensus estimates:

Q4 adjusted EPS $5.01, stronger than the $4.81 EPS (this was $5.34 back in mid-March when Fedex slashed guidance).

Q4 revenue of $17.8BN in line with expectations

Q4 operating margin 9.6%

That said, investors’ bullish mood was hardly buoyed as company only beat thanks to a number of “one-time expenses.”

When looking ahead the picture turned ugly, starting with the company’s CapEx guidance, as FedEx now sees 2020 capital expenditure at $5.9 billion, well below the estimated $6.16 billion, as yet another company confirms that trade war is stifling spending plans (although this may result in more buybacks).

However, it was the management’s comments that were notably gloomy, as CFO Alan Graf warned that “our fiscal 2020 performance is being negatively affected by continued weakness in global trade and industrial production, especially at FedEx Express.”

The company echoed this warning saying 2020 performance will be hurt by ongoing global trade weakness, which considering FedEx just sued the US government for its aggressive trade policies, is to be expected: after all, every management team is delighted to have a scapegoat to blame for underperforming, even if it is the White House.

As a result, FedEx now sees mid-single-digit percentage point decline in diluted EPS prior to the year-end MTM retirement plan accounting adjustment and excluding estimated TNT Express integration expenses compared with fiscal 2019’s adjusted earnings of $15.52 per diluted share.

Separately, FedEx also said that TNT Express integration program expenses through fiscal 2021 are now estimated to be approximately $1.7 billion, of which $350 million is expected to be incurred in fiscal 2020.

Finally, and somewhat inexplicably, Fedex said it was unable to provide a fiscal 2020 EPS effective tax rate outlook on a GAAP basis, suggesting that not even management teams have any visibility what happens next as US business climate flips by 180 degrees on any given Trump tweet.

As a result of all this, FedEx stock is once again getting hammered and after a brief spike higher as algos saw the EPS beat, it has given up all gains and was last trading at new session lows.

via ZeroHedge News http://bit.ly/2ZV59wT Tyler Durden

Once upon a time, some of the most beautiful cities in the entire world were on the west coast, but now those same cities are degenerating into drug-infested cesspools of filth and garbage right in front of our eyes.

San Francisco is known as the epicenter for our tech industry, and Los Angeles produces more entertainment than anyone else in the world, and yet both cities are making headlines all over the world for other reasons these days. Right now, nearly a quarter of the nation’s homeless population lives in the state of California, and more are arriving with each passing day. When you walk the streets of San Francisco or Los Angeles, you can’t help but notice the open air drug markets, the giant mountains of trash, and the discarded needles and piles of human feces that are seemingly everywhere.

If this is what things look like when the U.S. economy is still relatively stable, how bad are things going to get when the economy tanks?

When Leilani Farha paid a visit to San Francisco in January, she knew the grim reputation of the city’s homeless encampments. In her four years as the United Nations Special Rapporteur for Adequate Housing, Farha has visited the slums of Mumbai, Delhi, Mexico City, Jarkarta, and Manila. The crisis in San Francisco, she said, is comparable to these conditions.

I have never been to Mumbai, Delhi, Mexico City, Jarkarta or Manila, and so I will just have to take her word for what the conditions are like there.

But how can this be happening in one of the wealthiest cities in the entire country?

Sadly, to a large degree San Francisco has done this to itself. Every single day drugs are openly bought and sold at “an outdoor market of sorts” right in the heart of the city, and authorities know exactly where it is happening…

To drill down on the epicenter of the crisis, a recent New York Times inquiry set out to find the dirtiest block in San Francisco. After asking statisticians to compile a list of streets with the most neighborhood complaints regarding sidewalk cleanliness, the Times landed on a winner: Hyde Street’s 300 block, which received more than 2,200 complaints over the last decade.

A visit to the block yields a harrowing sight of drug addicts and mentally ill residents, many of whom are part of the city’s overwhelmingly large homeless population. During the day, drug users host an outdoor market of sorts, selling heroin, crack cocaine, and amphetamines along the sidewalks.

They could shut down the drug dealing if they really wanted to do so.

And anywhere the illegal drug trade is thriving, you are also going to have a lot of property crime. At this point, no city in America has a higher rate of property crime than San Francisco does…

San Francisco is the nation’s leader in property crime. Burglary, larceny, shoplifting, and vandalism are included under this ugly umbrella. The rate of car break-ins is particularly striking: in 2017 over 30,000 reports were filed, and the current average is 51 per day. Other low-level offenses, including drug dealing, street harassment, encampments, indecent exposure, public intoxication, simple assault, and disorderly conduct are also rampant.

Meanwhile, things are not much better in Los Angeles. In fact, many would argue that L.A. is in even worse condition.

The homeless population in the city has risen 16 percent since last year, and it is taking over neighborhood after neighborhood. Los Angeles was once one of the most beautiful cities in the entire world, but now it is rapidly being transformed into a hellhole…

If someone predicted half a century ago that a Los Angeles police station or indeed L.A. City Hall would be in danger of periodic, flea-borne infectious typhus outbreaks, he would have been considered unhinged. After all, the city that gave us the modern freeway system is not supposed to resemble Justinian’s sixth-century Constantinople. Yet typhus, along with outbreaks of infectious hepatitis A, are in the news on California streets. The sidewalks of the state’s major cities are homes to piles of used needles, feces, and refuse. Hygienists warn that permissive municipal governments are setting the stage — through spiking populations of history’s banes of fleas, lice, and rats — for possible dark-age outbreaks of plague or worse.

Skid Row is the epicenter of the homeless problem in L.A., and I highly recommend that you do not go down there to check it out for yourself.

It is hard to believe that people are actually living this way in America in 2019. This is what one reporter witnessed during his visit to the neighborhood…

If you want to know how bad the homelessness crisis has gotten in California, just turn to 4 squares miles east of Main Street in downtown Los Angeles. The area, known as Skid Row, has long been inhabited by the city’s poorest residents. These days it resembles something akin to a nightmare.

Residents sleep in tents surrounded by discarded needles and feces, their belongings tucked into trash bags and shopping carts. Some shade themselves with tarps or use nearby light poles to connect to power. Others have contracted typhus from rats scurrying across the sidewalk. One resident was even found bathing in the water from a broken fire hydrant.

This is where the rest of the country is headed if we are not very careful. Bad policies have bad consequences, and our leaders have been taking us in the wrong direction for a very long time.

And instead of getting to the root of our problems, most of our politicians seem to think that engaging in bizarre social experiments will somehow solve our problems.

For example, Los Angeles Mayor Eric Garcetti is convinced that we can solve the homeless problem by building tiny housing units in the backyards of private homeowners…

As part of this mission, the city is pursuing a pilot program, made possible by a $1 million Bloomberg Philanthropies grant, that would help homeowners install backyard units on their properties. In exchange for a $10,000 to $30,000 stipend, homeowners would be able to charge a small rent to homeless tenants, who would pay their share through vouchers or their own income. The city also plans to institute a matchmaking process that pairs owners and tenants.

“Our homeless crisis demands that we get creative,” the mayor said. If the backyard pilot works, he added, the idea could be adopted anywhere.

So if you live in Los Angeles, soon you will be able to bring the needles and piles of human feces from Skid Row into your own backyard.

Meanwhile, homeless people keep dropping dead night after night in Los Angeles. Just check out these staggering numbers…

A record number of homeless people — 918 last year alone — are dying across Los Angeles County, on bus benches, hillsides, railroad tracks and sidewalks.

Deaths have jumped 76% in the past five years, outpacing the growth of the homeless population, according to a Kaiser Health News analysis of the coroner’s data.

Year after year, this homelessness crisis is only getting worse.

The fabric of our society is literally coming apart right in front of our eyes, and we can all see what is happening, and yet our leaders seem absolutely powerless to fix it.

If we continue on this trajectory, what is our nation going to look like in a few years?

Just something to think about…

via ZeroHedge News http://bit.ly/2KCC3yu Tyler Durden

A stunned equity market could not believe that Batman Powell and Doveboy Bullard dared to talk down the odds of a 50bps rate-cut in July…

Ugly day in China overnight after Monday’s snoozefest…

Mixed bag in Europe with a weak open but France and Spain rallying into the close (still red on week)…

Ugly US housing and confidence data did not help but the cash open saw immediate selling of the modest overnight gains. The ugly data sent the US Macro Surprise Index near its lowest since June 2017…

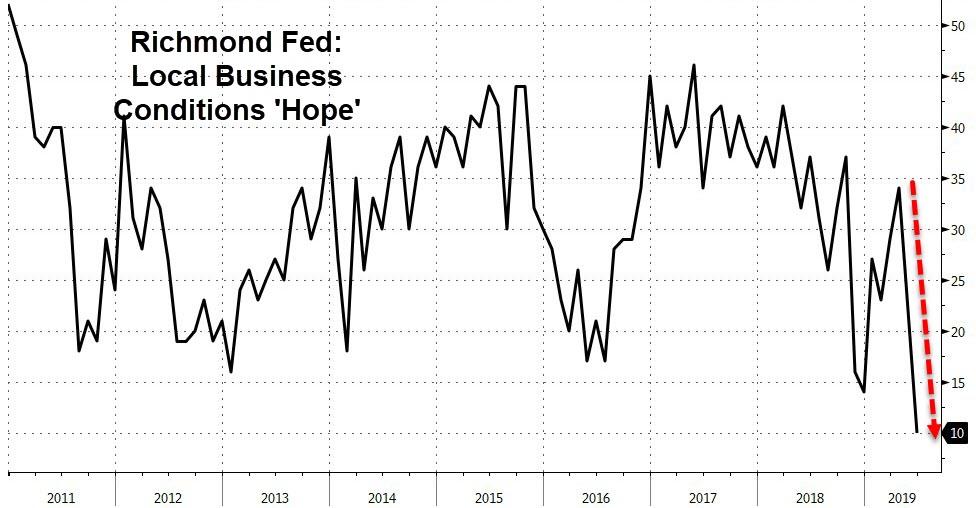

And while Richmond Fed’s headline beat, expectations for local business has crashed to a record low… (which seems very odd considering the Richmond Fed head said today that “US Consumer dynamics remain great.”)

Then these hit and spoiled the party…

1230ET Bullard – no need for 50bps

1300ET Powell – monitoring, won’t bow to political pressure

1330ET Trump-Xi meeting at G-20 not expected to produce a deal

All of which sent stocks lower for the second day… Trannies are the week’s worst performer followed by Nasdaq and Small Caps. For now The Dow is doing best but still lower since quad-witch…

Not a pretty day at all…

As the Nasdaq pushed back towards its 50DMA

Winners of June have been losers this week…

Abbvie and Allergan’s mega-deal did not end well for the former… ABBV lost a stunning $18bn in market cap on this deal…

VIX and Stocks remain decoupled…

As July odds for a 50bps rate-cut swung violently from 40% (pre-Bullard) to 16% (post-Powell) and back up to 26% after the ‘no trade-deal’ news…

Credit markets have seen notable decompression in the last few days…

Treasury yields continued to fade today except flat 2Y (despite a spike on Bullard headlines)…

10Y yields tumbled below 1.98%…

NOTE – this is the lowest closing yield for 10Y since Nov 8th 2016

The dollar spiked today on Bullard/Powell but faded on trade and in context to the post-FOMC move, it was nothing…

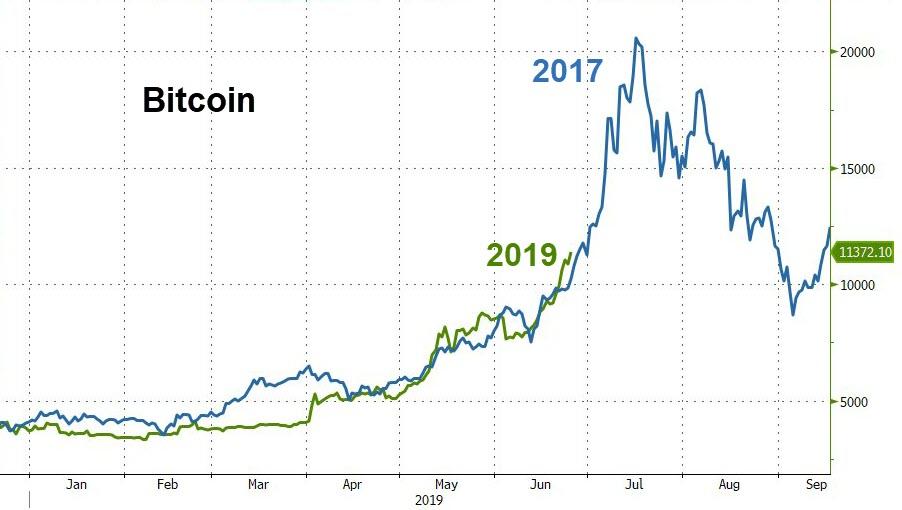

Bitcoin extended its gains, testing near $11,500 intraday (the highest since March 2018)…

As the big crypto tracks its 2017 analog…

But the rest of the crypto space did not play along…

Silver was down on the day as Copper, Crude, and Gold managed gains…

Gold was a little noisy intraday on the FedSpeak (pushing the dollar around) but held gains breaking to new 6-year highs overnight…

Gold/Silver soared to a new cycle high…

Gold’s “VIX” soared to 3 year highs, decoupling from other asset-classes…

Finally, don’t forget, there’s only one thing that matters…

And if The Fed doesn’t pay up and give-in to the market’s 50bps demands, the jaws of death will snap shut…

via ZeroHedge News http://bit.ly/2KExOCs Tyler Durden

Over the weekend, when previewing the most likely outcome of the Trump-Xi talks, Goldman’s political analyst Alec Phillips said that “a commitment to re-engage seems the most likely outcome. US officials, including President Trump and US Trade Representative Lighthizer, have emphasized their interest in restarting talks.”

As Phillips further noted, “in the two analogous face-to-face meetings that President Trump previously held with foreign leaders—with European Commission President Juncker in July 2018 and President Xi in December 2018—he agreed to postpone tariff increases in return for an unspecified commitment to negotiate an agreement. This seems to be the most likely outcome once again.”

It appears that Goldman was right, because as Bloomberg reported moments ago, citing people familiar with the plan, “the U.S. is willing to suspend the next round of tariffs on an additional $300 billion of Chinese imports while Beijing and Washington prepare to resume trade negotiations.”

The decision, which is still under consideration, may be announced later this week after a meeting between Presidents Donald Trump and Xi Jinping at a Group of 20 summit in Osaka, Japan.

This tentative agreement was reached during a discussion of the broad outline of the Trump-Xi agenda in a phone call Monday between Robert Lighthizer, the U.S. trade representative, and his counterpart in Beijing, Vice Premier Liu He.

As Bloomberg adds, “the American readout of the conversation characterized the call as productive.”

On the other hand, the probability of an actual breakthrough besides delaying new tariffs is virtually nil as “the U.S. won’t accept further conditions on tariffs as part of reopening negotiations and no detailed trade deal is expected from the leaders’ summit.”

As a reminder, it was a critical Chinese pre-condition to resume negotiations that the US completely eliminate already implement tariffs; it now appears that that won’t happen.

So what will happen once talks resume? According to the Bloomberg sources, “although each side still wants significant concessions from the other, both agreed to dial down the tit-for-tat responses and aim for an extended truce that could soothe financial markets.” Even so, it was not clear if they would set a definite timetable for their tariff truce.

The immediate paradox is that the market has interpreted this as negative news with the S&P sliding to LOD, because avoiding a worst case scenario and preventing more tariffs is precisely the one thing that could stop Powell from cutting rates by 25bps or 50bps in July, in the process tightening financial conditions sharply, and causing the market – which had already priced in 100% odds of a July rate cut – to plunge.

The irony: the best outcome for Trump, who is now obsessed with all time highs in the S&P, at this junction is to force China’s hand and to escalate the trade feud, which would then “force” him to go all in on China tariffs, in the process also forcing the Fed to start the easing cycle, and push stocks higher.

As to what Trump ends up doing, we’ll just have to wait and see until Saturday when the G-20 summit concludes.

via ZeroHedge News http://bit.ly/2X2zbwz Tyler Durden

There are two important points to remember when it comes to the financial crisis of 2008.

The root cause of the financial crisis was a “purely human factor. This human factor is the completely false sense of omnipotence, self-importance and entitlement among the country’s elite, as well as the nurturing of these beliefs at Ivy League colleges and other elite universities.”

Unless this purely human factor is addressed, “the US will be doomed to suffer other calamities every bit the equal of the financial crisis.”

Recently, Lawrence Summers proved – beyond a shadow of a doubt – the veracity of these two conclusions.

The Financial Times published an article profiling President Trump’s latest candidate for a position on the Federal Reserve, Judy Shelton. Among the most conspicuous differences between Shelton and her potential future Fed colleagues is she is completely dubious of the Fed’s ability to accurately set interest rates. In fact, she likens the entire notion of the Fed being as actively involved in the economy as it currently is, as being little different than Soviet-style central planning! A position I both wholeheartedly agree with and endorse!

However, in response to the Financial Times article, Summers tweeted, “Judy Shelton does what I would have not thought possible. She falls well below Cain or Moore as a potential Federal Reserve governor. Hers would be a dangerous appointment.”

In this tweet, Summers captures the enormous psychological defects that nearly all of the Confederacy of Dunces have.

Summers speaks as if he had nothing to do with what has been happening in the country for the past thirty years, or as if the Fed has some sort of unblemished record of success, and was thus beyond reproach. As the bursting of two enormous bubbles, and the apparent bursting of a third – even larger bubble now – clearly show, all sorts of economic assumptions and central banking practices need to be revisited. See the chart, which has been published on the site several times before, for visual evidence of the obvious economic defects the country has suffered through for decades.

Summers is both completely blind to the obvious need to redress some clearly faulty economic assumptions and his massive role in the promulgation of these incorrect assumptions. Moreover, if Summers had any academic or intellectual integrity – which he most certainly does not – he would realize that Judy Shelton is hardly alone in her criticism of today’s Federal Reserve, and its fatal, post-1971, infatuation with central planning via its Open Market Committee.

Here is just a brief sampling of some of the well-respect economists and financiers who were deeply skeptical of a central bank assuming even a small fraction of the power the Fed currently has;

Walter Bagehot, “In a crisis, a central bank can lend freely, but only against good collateral and only at high rates of interest.”

Dr. Benjamin Anderson, “The first four sources of capital – direct capitalization, (consumer saving), business thrift and, finally, taxation for capital purposes, are all wholesome, sound and safe. They have never been overdone; no country has ever gone wrong in creating capital these ways. The great troubles of the 1920s grew out of a fifth source of capital, namely new bank credit for capital purposes.” (i.e. a central bank creating bank reserves out of thin air)

Wilhelm Ropke, “If in the production of goods the most important pedal is the accelerator, in the production of money it is the brake. To ensure that this break works automatically and independently of the whims of government and the pressure of parties and groups seeking ‘easy money,’ has been one of the main functions of the gold standard. That the liberal should prefer the automatic brake of gold to the whims of government in its role of trustee of a managed currency is understandable.”

Fischer Black (of Black-Scholes option pricing fame), “I believe that in a country like the US, with a smoothly working fianncial system, the government does not, cannot, and should not control the money stock in any significant way. The government does, can only, and should simply respond passively to shifts in the private sector’s demand for money. Monetary policy is passive, can only be passive and should be passive. The pronouncements of the Federal Reserve Board on monetary policy are a charade.”

All the people quoted here are completely sympathetic to Judy Shelton’s skepticism of not just the ability of the Fed to set interest rates, but the enormous dangers inherent with the Fed attempting to do so. Moreover, the dust still hasn’t finished settling from the collapse of the housing bubble! Yet Summers can still haughtily claim it is Judy Shelton that is dangerous and the Fed isn’t some sort of menace?

The facts surrounding all this are completely clear, and a psychologically healthy person would have no problem seeing them. In particular, the time has long since passed when all of the operating assumptions around the Federal Reserve’s Open Market Committee need to be revisited. That Lawrence Summers – with his degrees from Harvard and MIT, and his Wall Street millions – can’t draw the correct conclusions from such obvious facts proves he is the danger, not Judy Shelton.

He also proves the two foundational conclusions mentioned at the beginning are completely correct.

In an otherwise slow news-cycle, the mainstream media has somehow failed to report on an undercover exposé by Project Veritasin which a senior Google employee admits that the company is manipulating its algorithms ahead of the 2020 election in order to prevent the “next Trump situation.”

“We all got screwed over in 2016, again it wasn’t just us, it was, the people got screwed over, the news media got screwed over, like, everybody got screwed over so we’re rapidly been like, what happened there and how do we prevent it from happening again,” said longtime Google employee and head of “Responsible Innovation,” Jen Gennai, in the undercover Veritas sting.

“We’re also training our algorithms, like, if 2016 happened again, would we have, would the outcome be different?” she added.

Google Exec Jen Gennai: “We all got screwed over in 2016. It wasn’t just us, it was like people got screwed over. The news media got screwed over, like everybody got screwed over…” FULL VIDEO: https://t.co/ODXUgUp137pic.twitter.com/wukd2WCXWU

As noted by Infowars‘ Jamie White, “CNN, WaPo, CNBC, HuffPost, The New York Times, Vox, Vice, Newsweek, Politico, and even The Daily Beast haven’t written a single piece on the devastating evidence.”

Meanwhile, YouTube parentGoogle has scrubbed the video from its video sharing platform (also ignored by the MSM).

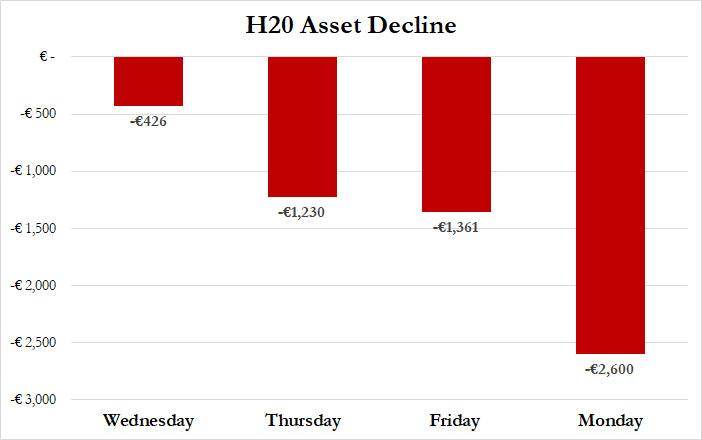

Yesterday when describing the latest developments surrounding the Natixis-owned, ill-named H20 Asset Management, which has found itself in a toxic spiral of holding illiquid assets yet facing growing redemptions following Morningstar’s questioning of the “liquidity and appropriateness” of some of H2O’s corporate-bond holdings as well as potential conflicts of interest, and suspended its recommendation on Wednesday, we reported that the fund unveiled an “ingenious”

way to halt redemptions without actually imposing gates: it marked down the balance of its holdings “to remove incentives for investors to pull even more.”

We also asked, rhetorically, whether this plan work?

That’s the question as fund managers hope to reverse outflows from a group of H2O funds that saw their assets drop by 1.1 billion euros on Thursday as analysts questioned their holdings.

Less than 24 hours later we have the question: it did not, because on Monday H20 saw its assets decline even more as a group of its largest funds seeing their biggest ever single-day drop. In the fourth consecutive day of accelerating redemptions, the money manager paradoxically named for liquidity – of which it has none as it scrambles to offload its most illiquid holdings – saw six of H20’s biggest funds fall by 2.6 billion euros, or about $3 billion, on Monday.

Yet while to most funds the redemption of nearly €6 billion in funds would prove terminal, perhaps H2O will manage to turn the tide – the fund said it received “material” inflows after a slowdown in net outflows since Monday:

H2O AM hereby confirms that the net outflows have slowed significantly since Monday June 24th. In addition, H2O funds received some material inflows on Tuesday June 25th.

On the other hand, it won’t be the first time that a fund facing liquidation says pretty much anything to restore confidence.

As Bloomberg notes, the fall in assets comes one day after as H2O said it had sold 300 million euros of the Windhorst-linked holdings on Monday. The sale and a marking down of the non-rated corporate bond holdings across H2O’s range reduced the value of the non-rated corporate bonds to 500 million euros, a spokeswoman said on Monday.

Morningstar raised concerns about the “liquidity and appropriateness” of some corporate-bond holdings as well as potential conflicts of interest last week. The funds, which allow clients to make daily withdrawals, hold rarely traded bonds issued by companies linked to controversial German financier Lars Windhorst investment vehicle Tennor.

So where do we stand: the good news for the fund that may soon join the unhappy procession of investors such as Third Avenue, UK property funds following Brexit, GAM and Woodford which all threw in the towel after their bond holdings were exposed as especially illiquid, is that it had a lot of assets to start the year: H2O’s assets were €32.5 billion at the start of the year. The bad news is that if management is non-GAAPing the truth and redemptions continue, the fund probably has a bout a week of life left if redemptions continue to grow at this rate. And until there is some confirmation that the fund has managed to turn the tide of outflows, there is no reason to expect that H20 will have finally found the oh so critical market substance that it was named for.

via ZeroHedge News http://bit.ly/2RBYmVz Tyler Durden

“Apologize for what? Cory should apologize. He knows better. There’s not a racist bone in my body.”

Thus did a stung Joe Biden answer rival Cory Booker’s demand he apologize for telling contributors, in a southern drawl, “I was in a caucus with James O. Eastland, He never called me ‘boy.’ He always called me ‘son.”

Joe was recalling fondly a time in the 1970s when he came into the Senate at 30, having lost his wife and child in an accident, and “Jim” Eastland, the arch-segregationist from Mississippi, took him under his wing and became a patron, mentor and friend.

“You don’t joke about calling black men ‘boy’,” Booker had said. “Biden’s relationships with proud segregationists are not the model for how we make America a safer and more inclusive place for black people.”

Kamala Harris piled on: If Biden’s segregationist friends “had their way … I wouldn’t be in the United States Senate.”

New York Mayor Bill de Blasio tweeted a photo of his black wife and two children, saying, “Eastland thought my multiracial family should be illegal & that whites were entitled to ‘the pursuit of dead n——-s.’”

Said The Washington Post, “(Biden’s) history of collegiality with racists is being seen by many in his party as a reason to question his judgment — and not, as Biden says, a sign of his civility.”

This portends a coming clash over race inside the Democratic Party in 2019 and perhaps 2020. For Joe is bleeding and his rivals can see in his segregationist friends of yesterday a way to peel off the black support crucial to his nomination.

Biden is about to have his nose rubbed in friendships formed almost half a century ago.

Like reparations for slavery, on which hearings have opened in the House, this issue seems certain to arise in the debates next week, where taking down Biden will be an objective of every other candidate.

And Jim Eastland is not the only segregationist friend Joe had.

Joe called Strom Thurmond of South Carolina, who conducted the longest filibuster in history against the 1957 Civil Rights Act, “one of my closest friends,” and delivered a eulogy at Strom’s funeral.

When Joe backed an anti-busing amendment in the 1970s, Sen. Jesse Helms, on the Senate floor, welcomed him to the “ranks of the enlightened.” On leaving the Senate for the vice presidency in 2009, Biden spoke of his “close personal relationships” with “Eastland, Stennis, Thurmond … all these men became my friends.”

Those three Senators all signed the Southern Manifesto pledging “massive resistance” to desegregation of the public schools mandated by the Brown decision of 1954. All three opposed the Civil Rights Act of 1964 and the Voting Rights Act of 1965, enacted after bloody Sunday at Selma Bridge.

Asked her views on Biden’s remarks, Elizabeth Warren joined the attack: “It’s never OK to celebrate segregationists. Never.”

But if that is the new Warren Rule in Democratic politics, it may be hard to maintain.

For the Democratic Party, the oldest party on earth, was from its founding to the final third of the 20th century, the bastion of slavery, secession and segregation.

Jim Crow voted a straight Democratic ticket.

Thomas Jefferson and Andrew Jackson, founding fathers of the party, were slave owners, as were James Madison and James Monroe, who succeeded Jefferson in the White House. And so were John Tyler and James K. Polk, who succeeded them.

Washington, a slave owner, was the Father of our Country and gave us our independence and a new nation from the Atlantic to the Mississippi. Jefferson executed the Louisiana Purchase. Jackson seized Florida. Tyler annexed Texas. Polk got us the Southwest, California and clear title to Washington and Oregon. All were slave owners — and also the Democrats who gave America almost all of her land and frontiers.

The first Democratic president of the 20th century, Woodrow Wilson, restored segregation to the U.S. government. The second, FDR, chose a segregationist vice president, “Cactus Jack” Garner, put a Klansman, Hugo Black, on the Supreme Court, and, with Wilson, carried all 11 segregated states of the Old Confederacy, all six times they ran.

To hold a segregated South against Eisenhower in 1952, liberal Adlai Stevenson continued the Southern strategy by putting on his ticket John Sparkman of Alabama. Returning to the Senate after Adlai’s defeat, Sparkman signed the Dixie Manifesto and opposed the civil rights acts of both 1964 and 1965.

On his second run for the presidency over a decade ago, Joe Biden joked of his home state: “Delaware … was a slave state that fought beside the North. That’s only because we couldn’t figure out how to get to the South. There were a couple of states in the way.”

The Warren Rule notwithstanding, Southern segregationists remain honored today. The Old Senate Office Building was renamed in 1972 for Sen. Richard Russell of Georgia and John C. Stennis of Mississippi.

via ZeroHedge News http://bit.ly/2LncvF0 Tyler Durden

Following President Trump’s upset election in 2016 followed by more than two years of constant ‘Russiagate’ coverage, there now appears to be a “Trump slump” across all forms of media as we wait for what promises to be popcorn-worthy debates between Trump and his Democratic challenger in 2020.

Top news executives have told Axios‘s Sara Fischer and Neal Rothschild that “Trump fatigue is very real,” and that “Interest in political coverage overall is down,” causing newsrooms to redirect their efforts on other beats such as technology and the global economy.”

Democrats don’t appear to be the lifeline media companies are hoping can fill the gap for diminished Trump interest. Executives say they expect this week’s debate ratings to be nothing like the ratings for the 2016 Trump debates.

Part of the problem is that 2020 Democrats don’t have a knock-out media star to drive interest in the election. To date, the Democrats’ biggest media attraction has been Rep. Alexandria Ocasio-Cortez, who isn’t running for president.

Other candidates split the spotlight in the crowded Democratic primary field. –Axios

What do the numbers indicate?

According to traffic analytics company Parse.ly, digital demand for all things Trump dropped 29% between the first six months of Trump’s presidency and the most recent six months. Axois, meanwhile, provides more evidence of the “Trump slump.”

In March, New York Times COO Meredith Kopit Levien told Axios during a panel at SXSW that the paper’s subscription “Trump Bump” ended in mid-2018.

In December, media research firm MoffettNathanson found that live news network ratings were down “in the -10% to -20% range” for the better part of 2018. Overall, the firm found that ratings around TV news coverage overall began to decline after the 2016 election.

Cable TV networks, which still reach a majority of Americans with political news coverage, began pulling back on Trump campaign rallies late last year because they weren’t driving ratings, according to Politico. –Axios

Is this why the MSM has been featuring war hawk ‘analysts’ such as Raytheon board member and former Navy Admiral James Winnefeld?

As The American Conservative‘s Barbara Bolandpointed out last week, the mainstream press jumped all over President Trump for not bombing Iran in response to the Islamic Republic shooting down a US drone that may or may not have been in Iranian airspace.

The piece approvingly cites Mark Dubowitz, chief executive of the hawkish Foundation of Defense for Democracies, who told The New York Times that Iran had likely mined oil tankers in the region in order “to demonstrate that Trump is a Twitter Tiger.”

Meanwhile, invoking Ronald Reagan, David Adesnik at the National Review ladles all the praise on Trump’s hawkish secretary of state. “Mike Pompeo brought a Reagan-esque flourish to the Trump administration’s foreign policy, demanding nothing short of Iranian surrender. While insisting that President Trump is prepared to negotiate a new deal with Tehran, Pompeo listed no fewer than twelve preconditions for an end to American pressure.”

ABC used the headline (5/24/19) “1,500 More Troops and Defensive Capabilities Headed to Middle East to Deter Iran.” How the US sending soldiers to the doorstep of a country that has not attacked it is “defensive,” or the evidence of the need to “deter” Iran, goes unexplained, an egregious omission when one considers that there is every reason to doubt US claims that Iran is about to attack the US.

A CNBC headline (5/24/19) told readers that the “Pentagon Will Send 1,500 Troops, Along With Drones and Fighter Jets, to the Middle East to Counter Iran Threat.” CNBC presents US officials’ justifications for their military maneuvers as though they were facts:

Currently, the USS Arlington, USS Abraham Lincoln carrier strike group, a Patriot missile defense battery and a US Air Force bomber task force have been sent to the region in order to deter Iranian and proxy threats.

…

Both the ABC and CNBC articles note that Vice Adm. Michael Gilday, the director of the Joint Chiefs of Staff, blamed Iran for attacks on Saudi Arabia’s oil infrastructure and for a rocket that landed near the US embassy in Baghdad. Neither piece notes that US officials have said they have no evidence that Iran was behind either drone attacks on the pumping stations or the sabotage of four oil tankers, two of which were Saudi, in the Persian Gulf. Nor did either report inform their readers that the US produced no evidence that Iran was responsible for the rocket in Iraq. (Yemeni Houthis, falsely depicted as pawns of Tehran, said they carried out attacks of Saudi oil pumping stations in retaliation for the Saudi/US/UAE/UK/Canadian invasion and immiseration of Yemen.) –Fair.org

Also notable is a survey of opinion journalism released last month by FAIR which found that when it came to violent regime change in Venezuela, there were “no voices in elite corporate media that opposed regime change in that country.” (h/t Mintpress)

The media watchdog’s study, Zero Percent of Elite Commentators Oppose Regime Change in Venezuela, reviewed three months of commentary in the New York Times and the Washington Post, as well as on three major Sunday morning talk shows — ABC’s This Week, CBS’ Face the Nation, and NBC’s Meet the Press — and the PBS NewsHour.

“Over a three-month period (1/15/19 – 4/15/19), zero opinion pieces in the New York Times and the Washington Post took an anti–regime change or pro-Maduro/Chavista position,” the survey’s author, Teddy Ostrow, wrote. “Not a single commentator on the big three Sunday morning talk shows or PBS NewsHour came out against President Nicolás Maduro stepping down from the Venezuelan government.” –MPN

In short, the MSM really needs some fireworks to improve their slumping bottom line – and are happy to report one side of the story in order to help light the fuse.

via ZeroHedge News http://bit.ly/2KD09cl Tyler Durden

{kind=link}